Buying More of the Same Royalty: Top-Ups, Tier Extensions and the Anatomy of an Amendment

Royalty financing rarely ends at signing.

The cleanest recent illustration of why is the AnaptysBio/Sagard relationship on Jemperli. Three documents, three years apart, restructure who owns what slice of GSK's payment obligation, and the legal architecture is doing real economic work.

This piece walks through the documents, the SPE chain, and the protective covenants that recur. Most of the discussion is grounded in the actual filed text of Amendment No. 1, which has been on EDGAR since August 2024 as exhibit 10.29 to AnaptysBio's 10-Q for the period ended 30 June 2024.

The headline numbers

2021: Sagard pays $250M for the 8% royalty on Jemperli sales below $1B.

2024: Sagard pays another $50M for the 12 / 20 / 25% upper tiers, plus combination products. Cap reset to $600M / $675M.

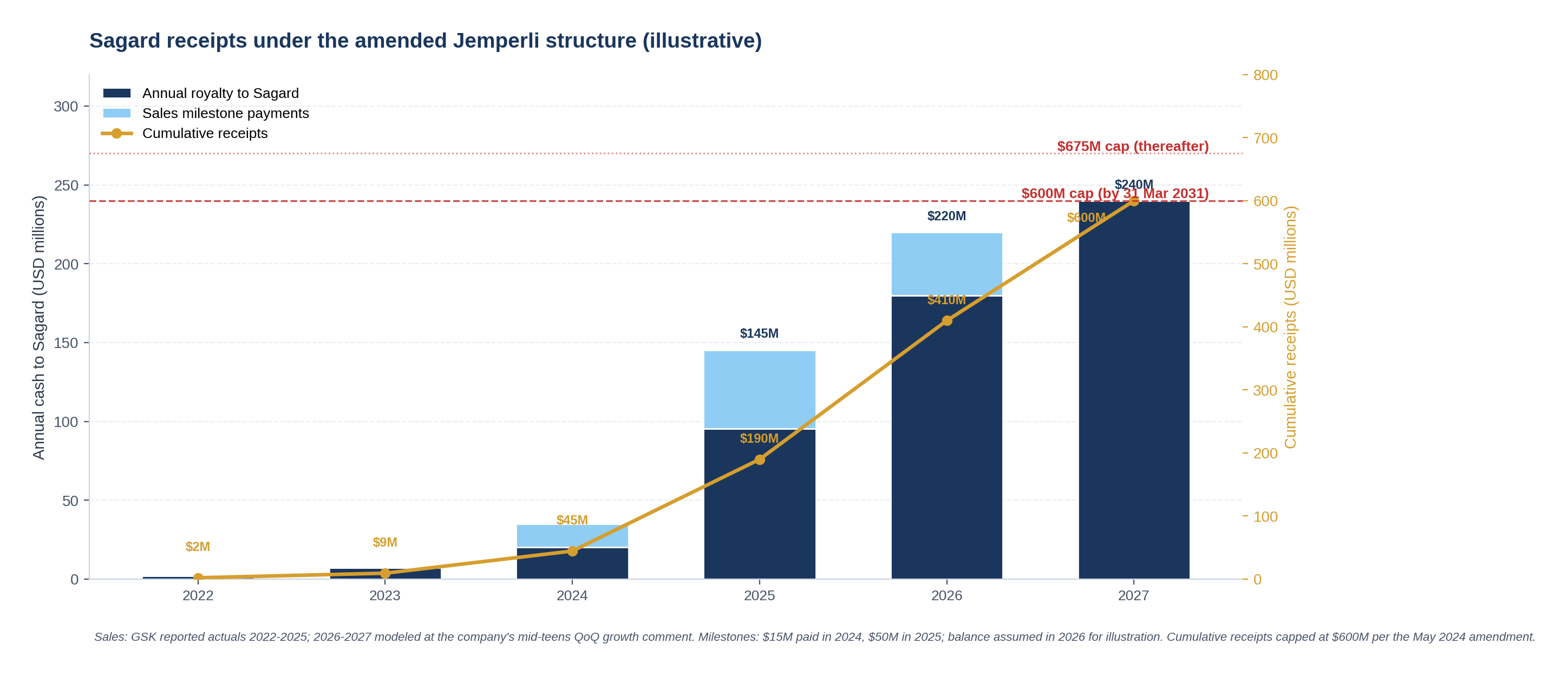

2025: Jemperli does £861M (~$1.128B) in sales. GSK reaffirms peak guidance above £2B monotherapy.

Mid-2027: AnaptysBio's own Q3 2025 release projects full paydown of the $600M non-recourse debt between Q2 2027 and Q2 2028.

The amendment is now expected to deliver Sagard the full $600M cap roughly five and a half years after the original deal closed and three years after the top-up. Whether that pricing was right for both sides is a question the rest of this piece works through.

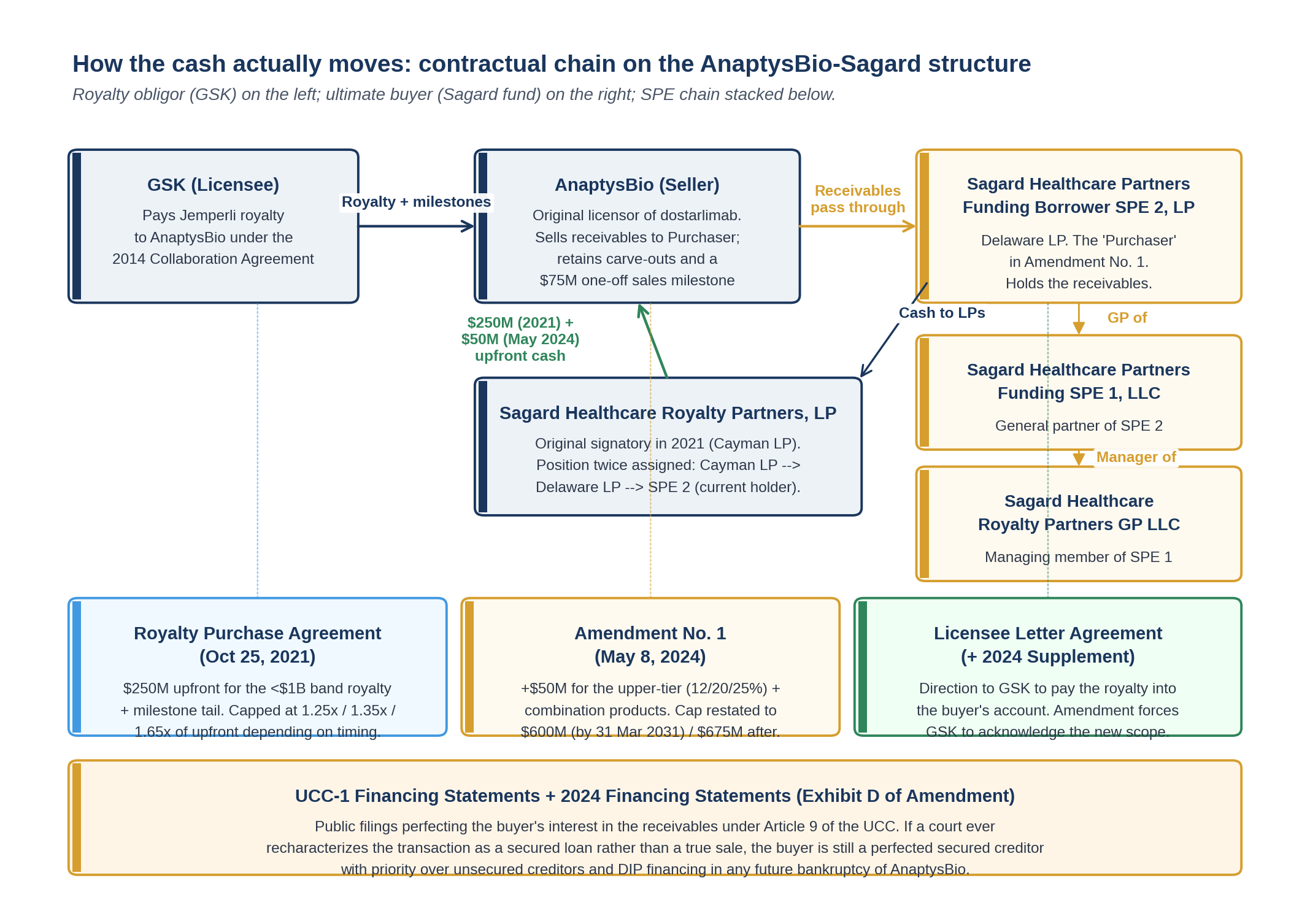

The structure: three parties, three documents, four entities

Before the mechanics, the entities. The transaction does not run between AnaptysBio and "Sagard." It runs between AnaptysBio and a Delaware limited partnership at the bottom of a three-tier SPE chain.

The Amendment names the counterparty in full:

"SAGARD HEALTHCARE PARTNERS FUNDING BORROWER SPE 2, LP, a Delaware limited partnership (as assignee of Sagard Healthcare Partners (Delaware) II LP, a Delaware limited partnership, which was, in turn, assignee of Sagard Healthcare Royalty Partners, LP, a Cayman Islands exempted limited partnership)"

That preamble is doing four jobs at once.

One, it tells you the position has been moved twice since 2021. The original signatory was the Cayman fund. Sagard then pushed the position into a Delaware LP, then into SPE 2. Each move would have required AnaptysBio's prior consent under the original assignment provisions of the 2021 agreement. By the time the May 2024 amendment was being drafted, AnaptysBio's counsel was negotiating not against the fund but against the SPE.

Two, it confirms Delaware as the jurisdiction of the operative entity. Delaware LPs sit on a body of statutory and case law that supports the bankruptcy-remote and true-sale features that make a royalty monetization legally robust. Cayman remains the home of the underlying fund for tax and investor reasons; Delaware is the jurisdiction that actually has to hold up if AnaptysBio ever defaults or files.

Three, the SPE chain is bankruptcy-remote in both directions. If a different Sagard fund or vehicle defaults on its own creditors, those creditors cannot reach into SPE 2 to satisfy the claim. Equally, if AnaptysBio defaults, SPE 2 has a perfected interest in receivables that are not part of AnaptysBio's bankruptcy estate.

Four, by being the legal counterparty, SPE 2 is the entity whose representations and warranties are made in Section 2(b) of the Amendment, and whose limited indemnification obligations are restated in Section 5(q). The substantive promises run to and from a special-purpose vehicle, not the broader Sagard franchise.

The original 2021 deal: what was actually sold

The 8-K filed on the day of signing summarizes the October 25, 2021 transaction in three paragraphs. Stripped of marketing language, the structure was:

| Item | Detail |

|---|---|

| Upfront | $250M to AnaptysBio |

| Royalty sold | 8% on annual global net Jemperli sales below $1B |

| Milestones | Up to $105M ($15M regulatory + $90M commercial below the $1B threshold) |

| Retained by AnaptysBio | 12 to 25% royalties above $1B; cobolimab/anti-LAG-3 payments; ZEJULA royalty |

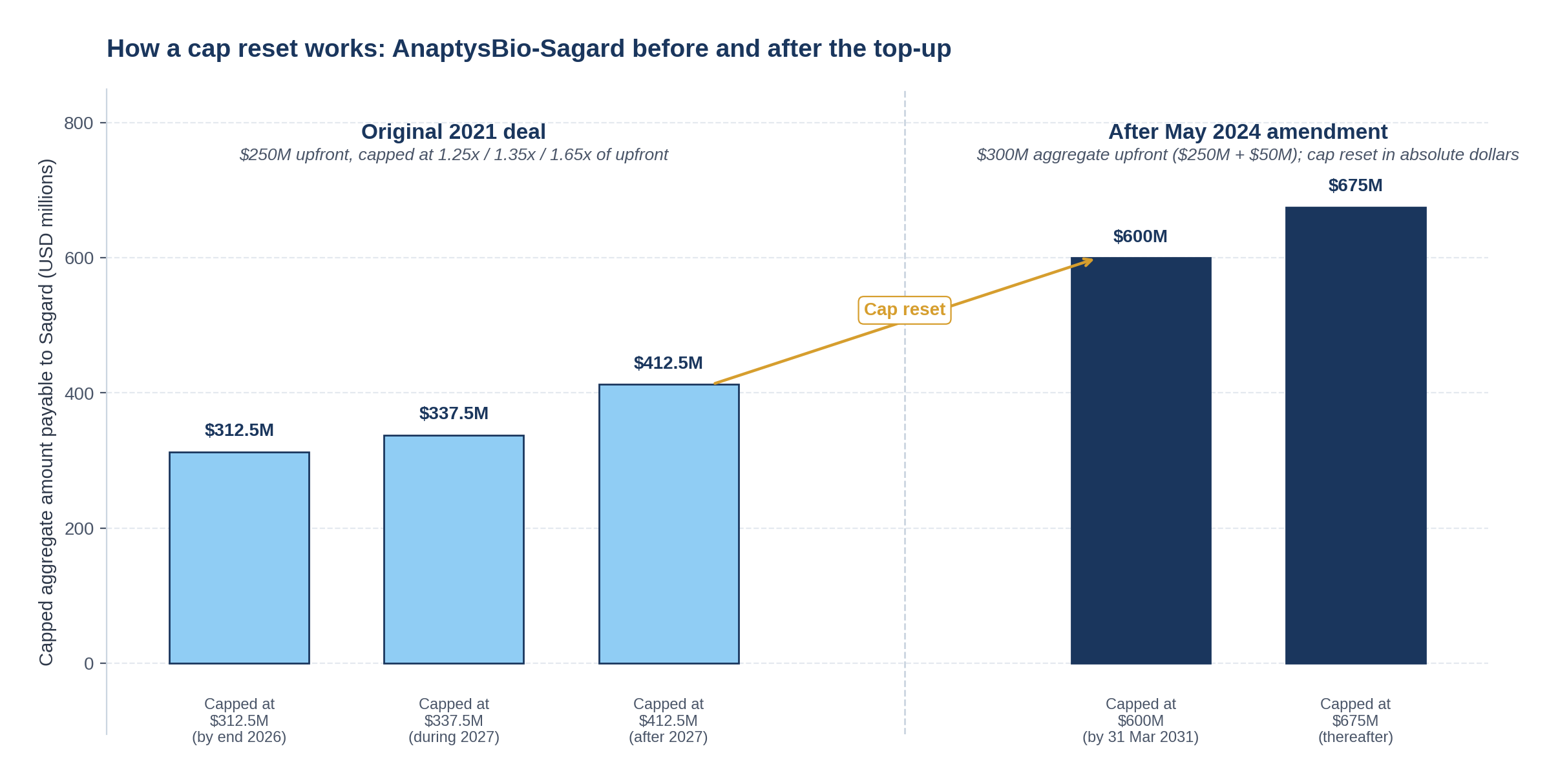

| Cap | $312.5M (1.25x) by end-2026, or $337.5M (1.35x) during 2027, or $412.5M (1.65x) thereafter |

| Term | Until cap is hit |

Two design choices stand out.

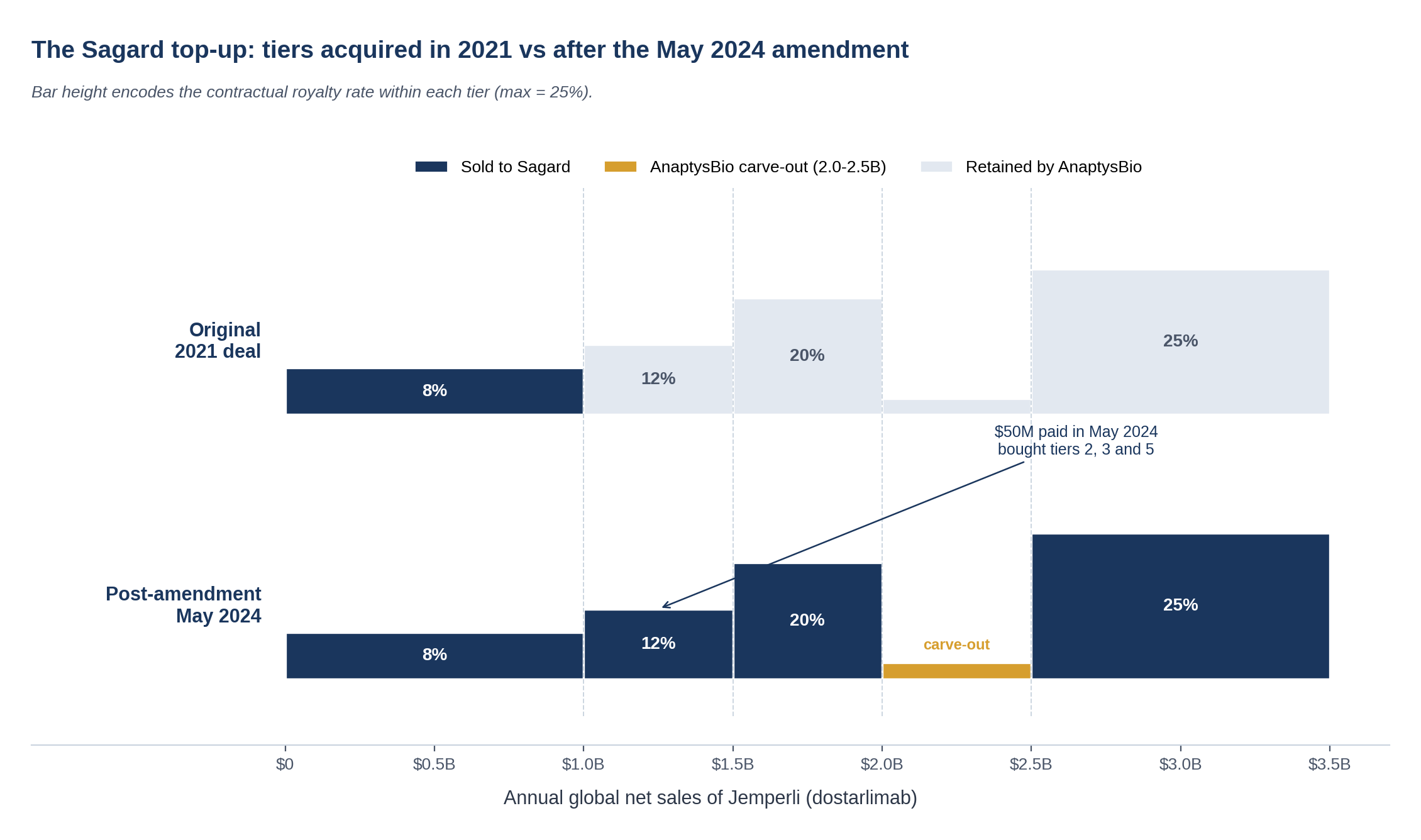

The upper tier was a hard carve-out, not just unmonetized. Anything above $1B in any year stayed with AnaptysBio. In late 2021 GSK's peak guidance was a $1.4 to $2.8B range and the upper-tier band looked too valuable to monetize at the prevailing discount rate. The Original Purchase Agreement defined a term, "Specified Royalty Payments," that explicitly carved out everything above the $1B threshold from what Sagard was buying.

The cap was a multiple of the upfront, not an absolute number. The 1.25x / 1.35x / 1.65x ladder rewards Sagard if the asset takes time to clear (the post-2027 cap is materially higher) and bounds AnaptysBio's exposure if the asset takes off (the 1.25x cap binds early and cuts off the buyer's upside). It is a structure that prices time as much as outcome.

By Q1 2024, both choices were under stress.

Why the amendment happened when it did

Three things converged in the first half of 2024.

Jemperli was tracking past the original peak band. Q1 2024 sales of £74M and the strong RUBY-1 frontline endometrial-cancer data had repositioned the asset toward the top of the original peak guidance. GSK's revised guidance moved above $2B. The 12 to 25% upper tier carved out to AnaptysBio in 2021 was suddenly a substantial expected cash flow.

AnaptysBio needed non-dilutive capital. The wholly-owned pipeline (rosnilimab, ANB033, ANB101, imsidolimab) had several Phase 2 readouts approaching, and the company had been clear in its capital allocation messaging that it preferred royalty monetization over equity issuance.

Sagard had a deployed counterparty already underwritten on the asset. A new royalty buyer would have needed to repeat the entire diligence process on Jemperli, the GSK Collaboration Agreement, and the AnaptysBio licensing chain back to TESARO. Sagard had done this in 2021. The marginal transaction cost of an amendment was low.

The result: a $50M top-up structured as Amendment No. 1 to the 2021 Royalty Purchase Agreement, executed on May 8, 2024.

What Amendment No. 1 actually does

The "WHEREAS" recitals lay out the four-fold purpose of the amendment in plain terms:

"Seller and Purchaser now desire to amend the Original Purchase Agreement to, among other things, (i) eliminate the annual cap on the Royalty Payments contemplated by the definition of Specified Royalty Payments in the Original Purchase Agreement, (ii) expand the definition of Dostarlimab in the Original Purchase Agreement to include any Product containing dostarlimab, whether or not such Product constitutes a Combination Product, (iii) expand the definition of Receivables in the Original Purchase Agreement to reflect the changes described in clauses (i) and (ii) above [...], (iv) increase the Threshold Amount, and (v) reflect that Purchaser is purchasing such Additional Purchased Receivables"

Each clause maps to a specific operative section. The four moves are worth breaking out.

Move 1: Eliminate the upper-tier carve-out

The 2021 deal contained a term, "Specified Royalty Payments," that confined Sagard's economics to the band below $1B. Section 5(i) of the Amendment is short:

"The definition of 'Specified Royalty Payments' in Section 1.1 (Definitions) of the Original Purchase Agreement is hereby deleted in its entirety."

Combined with Section 5(b), which deletes the "Annual Period" definition (the mechanism that reset the $1B threshold each year), this single pair of deletions opens the entire sales waterfall to Sagard. Section 5(f) then re-defines "Receivables" to flow across the full Royalty Payment, not just the carved slice:

"'Receivables' means, collectively, (a) with respect to Dostarlimab and each country, each Royalty Payment to the extent attributable to Net Sales of Dostarlimab invoiced in such country during the Purchased Royalty Period applicable to Dostarlimab and such country, (b) each Specified Milestone Payment and (c) any interest on any amounts referred to in the immediately foregoing clauses (a) and (b) payable by the Licensee pursuant to Section 7.1 of the License Agreement."

The interaction with the 2014 GSK collaboration matters. Sagard does not get a different rate in the upper tier. Sagard gets whatever GSK pays AnaptysBio under the underlying license, which happens to be 12% on the $1 to $1.5B band, 20% on $1.5 to $2B, and 25% above $2.5B. The 2014 license is an arms-length contract between AnaptysBio and TESARO/GSK that was negotiated in a different decade for a different molecule profile. Amendment No. 1 simply changes which party receives the cash flow under that license; the rate is whatever the underlying contract says.

Note one thing the Amendment does not do: it does not extinguish the $2B to $2.5B carve-out that AnaptysBio retains, nor the $75M one-off sales milestone payable on the first achievement of $1B in annual global net sales. Those carve-outs survive Amendment No. 1 and are part of the price negotiation. We come back to this below.

Move 2: Broaden the product definition

Section 5(c):

"'Dostarlimab' means dostarlimab (also known as JEMPERLI or dostarlimab-gxly) and (i) includes all instances in which dostarlimab is sold as part of any Combination Product that contains dostarlimab and (ii) includes all instances in which dostarlimab is sold as part of any combination product that contains both dostarlimab and one or more other Development Antibodies."

This is the kind of clause that reads as a footnote and matters in practice. Jemperli is in active development with niraparib (a PARP inhibitor) and cobolimab (anti-TIM-3) across multiple indications. Without the amended definition, the parties would eventually have had to litigate or re-negotiate the allocation of net sales between dostarlimab and the partner molecule in any combination product, on a contract drafted in 2021 that did not anticipate the question.

Two sub-points worth flagging on this clause.

The first sub-clause covers "Combination Products" with a capital C, the defined term in the 2014 license, which typically refers to commercial combinations sold under a single SKU. The second sub-clause is broader: it covers dostarlimab co-administered with another AnaptysBio "Development Antibody" (cobolimab and anti-LAG-3 are explicitly carved out in the 2021 8-K language as separate economics). The Amendment closes the gap by saying "if it contains dostarlimab, the dostarlimab share of net sales is part of the receivable, full stop." That cleans up two ambiguities at once.

Move 3: Restate the cap

This is the headline number. Section 5(j):

"'Threshold Amount' means: (a) from (and including) the date hereof through (and including) March 31, 2031, $600,000,000, and (b) from (and including) April 1, 2031 and thereafter, $675,000,000."

Three things change.

| Dimension | Original 2021 cap | Amended 2024 cap |

|---|---|---|

| Form | Multiple of upfront (1.25x / 1.35x / 1.65x of $250M) | Absolute dollars ($600M / $675M) |

| Date structure | Three steps tied to calendar years (end-2026 / 2027 / after 2027) | Single date cutoff (31 March 2031) |

| Implied multiple on combined upfront ($300M) | Not directly comparable | 2.0x and 2.25x |

The shift from multiple-of-upfront to absolute dollars is meaningful. Multiple-of-upfront caps embed a refinancing-style economics (the buyer gets paid back N times what they put in). Absolute-dollar caps embed a hard ceiling on dollar-IRR; if the asset overperforms, the buyer benefits from earlier payback (better IRR) but does not capture additional dollars. The choice tells you both sides expect the asset to clear the cap on its own steam, and the negotiation is over the timing rather than the absolute amount.

The hard 31 March 2031 cutoff is a step function, not a ladder. There is no intermediate cap between $600M and $675M; the higher cap applies in full only if Sagard fails to clear $600M by the cutoff date. For a buyer that expects to be paid in full by mid-2027 (per AnaptysBio's own Q3 2025 release), the $675M cap is essentially out-of-the-money and the $600M cap is what matters.

Move 4: Carry the deal forward without reopening it

Sections 5 through 7 of the Amendment exist to make sure that nothing in the Amendment accidentally re-opens issues that were settled in 2021. The drafting move is to define a tightly bounded set of new obligations ("Additional Receivables," "Additional Purchased Receivables," "Amendment Purchase Price," "Additional Bill of Sale"), restate only the parts of the original contract that touch them, and explicitly preserve everything else.

Section 6 captures the catch-all:

"Except as amended and modified by this Amendment, the Original Purchase Agreement is unchanged and remains in full force and effect."

This is the lawyer's belt-and-braces for everything not enumerated in Section 5. Original-deal indemnification mechanics, audit rights, information rights, change-of-control provisions, anti-stacking language, cross-default to the underlying license: all of it survives untouched unless the Amendment names it specifically. That is what an amendment-as-top-up is buying for the parties: the ability to add scope and adjust the cap without reopening the main contract for renegotiation.

The ten levers that get pulled in any amendment

Looking past the Jemperli specifics, an amendment to a royalty purchase agreement is a negotiation over a fairly standard list of protective levers. The Amendment to the AnaptysBio-Sagard deal touched almost all of them, in some cases by reaffirmation rather than rewrite.

Three of these deserve a closer look.

True sale and the bankruptcy question

The single biggest legal risk in a royalty monetization is that a court later characterizes the transaction as a secured loan rather than a true sale of receivables. The implication is severe. In a true sale, the receivables leave the seller's estate at closing and the buyer is paid even if the seller goes bankrupt. In a recharacterized loan, the receivables stay in the seller's estate, the buyer becomes a secured creditor, and payment is subject to bankruptcy-court priorities, automatic stay, and potential cramdown.

The Amendment uses standard true-sale language. Section 1(a):

"Seller shall sell, transfer, assign and convey to Purchaser, and Purchaser shall purchase, acquire and accept from Seller, free and clear of all liens and encumbrances (other than those created by Purchaser, if any), all of Seller's right, title and interest in and to the Additional Purchased Receivables."

This wording does not by itself guarantee true-sale treatment. Courts apply a multi-factor test that includes the parties' intent, who bears the risk of non-payment, whether the buyer has recourse to the seller, whether the transaction is treated as a sale on the books and tax returns, and whether market-standard true-sale opinions were delivered at closing. The Amendment language preserves the form. The accounting treatment described in AnaptysBio's 10-Q ("the proceeds received from Sagard of $250.0 million and $50.0 million were recorded as a nonrecourse liability") preserves the substance.

There is a tension in the accounting language worth noting. AnaptysBio records the proceeds as a "nonrecourse liability" and amortizes the future payments as non-cash interest expense over the life of the arrangement. This is the GAAP treatment for a sale of future revenue under ASC 470-10-25 (the "Liability Recognized for Sale of Future Revenue" model), which treats the cash received as debt for accounting purposes even though the legal characterization is sale. That dichotomy — debt for accounting, sale for legal/bankruptcy — is the standard outcome for U.S. royalty monetizations on biotech balance sheets.

Belt and braces: UCC-1 financing statements

Even if the parties agree the transaction is a sale, prudent practice is to file UCC-1 financing statements as if it were a secured loan. The reasoning is simple: if a court later disagrees on characterization, the buyer wants to be a perfected secured creditor with priority over unsecured creditors and any DIP financing in a future bankruptcy.

The Amendment authorizes new filings to ride alongside the 2021 ones. Section 1(c):

"It is understood and agreed that Seller has authorized Purchaser to file such financing statements (or amendments to existing financing statements) as Purchaser shall deem necessary or appropriate relating to the transactions contemplated by this Amendment (the forms of such additional financing statements and/or amendments to existing financing statements are attached hereto as Exhibit D and are referred to herein as the '2024 Financing Statements')."

The Exhibit D forms are the actual UCC-1 templates, redacted in the public filing. The substantive effect is that the same Article 9 perfection regime that protects the buyer's 2021 position now also covers the additional receivables acquired in 2024.

The licensee letter: making sure GSK pays the right account

A receivable is only as collectible as the obligor's willingness to pay the right party. In a royalty monetization, the licensee (here GSK) is the obligor; if the licensee continues to pay the seller because no one told it otherwise, the buyer may have a contractual claim against the seller for the diverted cash but nothing direct against the obligor.

The 2021 transaction included a "Licensee Letter Agreement" between AnaptysBio, Sagard, and GSK directing GSK to pay the relevant royalty stream into Sagard's designated account. The Amendment requires a supplement to that letter to capture the new scope:

"On or prior to the Amendment Effective Date, Seller shall have delivered to Purchaser a duly executed agreement among Licensee, Seller and Purchaser in the form of Exhibit B attached hereto (the 'Licensee Letter Supplement')."

This is the part of the deal that requires GSK's cooperation. Section 6.23 of the Original Purchase Agreement (referenced in the WHEREAS clauses of the Amendment) required Sagard's prior written consent for AnaptysBio to deliver the supplement to GSK. The Amendment confirms that consent was given. GSK signed. The receivables flow goes directly to SPE 2.

If GSK had refused to sign, the Amendment would still have been enforceable between AnaptysBio and Sagard, but the operational mechanics would have been awkward: GSK would continue to pay AnaptysBio, AnaptysBio would have a contractual obligation to pass the cash through to SPE 2, and any delay or dispute would create a hole between the legal title to the receivable and the actual cash.

Why is this fair to both sides

The implied economics on the combined capital are worth working through.

From the seller's side, AnaptysBio took $300M of upfront cash ($250M in 2021, $50M in 2024) against an obligation that AnaptysBio expects to satisfy in full between Q2 2027 and Q2 2028. The retained carve-outs (the $2 to $2.5B sales gap, the $75M one-off milestone, the upper tier above the cap, and everything from cobolimab/anti-LAG-3 collaboration economics) survive the Amendment. The 2026 planned spin-off of biopharma operations into "First Tracks Biotherapeutics" leaves the royalty management entity holding a clean cash flow stream once Sagard is paid out. The $50M was the price to lock in early termination of the obligation and to monetize the upper tier without dilutive equity.

From the buyer's side, Sagard puts in $300M total against a $600M cap likely satisfied within roughly five and a half years of original deal close. The implied IRR on the combined capital, adjusting for the $50M paid in 2024 rather than 2021, sits in the low-to-mid teens depending on which milestone payments come in when. The exit is hard-dated: Sagard is paid in full and the relationship terminates. There is no tail risk on the upper tier because Sagard does not own anything above the cap.

The carve-outs are the pricing tool. The $2 to $2.5B sales gap looks technical but matters at the margin: it leaves AnaptysBio with a slice of upside that motivates the company to keep advocating for Jemperli's continued development. The $75M one-off milestone (achieved when annual sales first crossed $1B in Q4 2025) is similar; it is paid by GSK to AnaptysBio, not to Sagard, and it sits outside the cap. These features tell you the negotiation was not adversarial. Both sides were sizing the deal to leave each with a coherent post-transaction position.

The same architecture, different dial: Cytokinetics, May 2024

Two weeks after the Sagard amendment, Cytokinetics restructured its royalty relationship with Royalty Pharma on aficamten. The press release describes the change in one sentence:

"Royalty Pharma's royalty on aficamten was restructured so that Royalty Pharma will now receive 4.5% up to $5.0 billion of annual net sales of aficamten and 1% above $5.0 billion of annual net sales compared to the prior 4.5% up to $1.0 billion of annual net sales and 3.5% above $1.0 billion of annual net sales."

The mechanism is different from the Sagard amendment in two respects. First, Cytokinetics did not have an upper tier "carved out and waiting" the way AnaptysBio did with Jemperli; the 2022 deal had given Royalty Pharma economics across the entire sales curve, just at unrealistic rates above $1B. The amendment was a re-pricing of the curve rather than an extension. Second, the $575M of total commitment from Royalty Pharma included a $250M tranche at signing, an additional $175M term loan drawable on FDA approval, $50M from a stock option/private placement, and $150M of further synthetic royalty funding contingent on a CK-586 Phase 3 trial. The package was a multi-instrument financing, not a single sale of receivables.

But the legal architecture rhymes. The 8-K filed on May 22, 2024 references an "Aficamten RPA Amendment" to the original 2022 Revenue Participation Right Purchase Agreement, alongside a "2024 Development Funding Loan Agreement" and a "Stock Purchase Agreement." Each instrument has its own counterparty in the Royalty Pharma SPE structure. The amendment to the original royalty document does the rate restructuring; the new instruments handle the additional capital and the equity component.

What this tells you about the market: the amendment-as-top-up is not specific to a particular shape of underlying deal. Sagard's amendment moved economics into a previously carved-out band; Royalty Pharma's amendment re-priced the existing band. Both used the same legal vehicle (an amendment to the original royalty purchase agreement) and both bundled the new economics with a new bill of sale.

Threshold reset: Cystic Fibrosis Foundation, December 2020

The third archetype is older and structurally distinct. The December 2020 transaction between the Cystic Fibrosis Foundation and Royalty Pharma was a pure threshold reset.

Royalty Pharma had earlier acquired 100% of CFF's royalty on Vertex's CF franchise up to $5.8B of annual sales, plus 50% of royalties above $5.8B, for $3.3B. (An intermediate amendment had moved the threshold from $5.0B to $5.8B.) The December 2020 transaction acquired the residual 50% above the $5.8B threshold for $575M plus a $75M milestone.

The CFF transaction is structurally distinct from the Sagard amendment in that the rate was unchanged. CFF's underlying contract with Vertex was a flat percentage on net sales; the only dial that moved across the various amendments was the share of the high-end slice.

This is the "threshold reset" archetype and it is rarer than the tier extension, because it requires a flat-rate underlying royalty. Tiered royalty contracts are now the norm in pharma licensing, which means that future top-ups will skew toward the AnaptysBio shape rather than the CFF shape. But the legal mechanism is the same in both: an amendment to the original purchase agreement, an additional purchase price, and a new bill of sale.

Why amendments are happening more often

Three trends are driving the rise of the amendment-as-top-up structure in pharma royalty finance.

Underwriting models age faster than the assets. A royalty deal closed in 2021 was priced against analyst consensus, GSK guidance and a market structure that did not yet incorporate IRA price negotiations, MFN agreements, or the full implications of the obesity-driven repricing of incretin-related assets. Five years later, the same asset is in front of a different underwriting environment. Where the asset has outperformed (Jemperli), the buyer has an opportunity to acquire incremental upside at a discount to current fair value because the seller's alternative cost of capital is high.

Sellers face capital needs at predictable points in the asset life cycle. Phase 3 readouts, NDA filings, and launch year are all moments at which biotechs need significant non-dilutive capital. A seller with an existing royalty relationship has a counterparty already underwritten on the asset; a fresh royalty buyer would need to repeat the entire diligence process. The transaction cost of an amendment is lower, and the pricing reflects that.

Buyers face deployment pressure. Royalty Pharma, Sagard, HCRx and Ligand (post the pending XOMA acquisition) are all running large dedicated funds with deployment targets. Amendments to existing deals are typically faster to close than new transactions and tap a counterparty that already understands the structure.

The 2024-2025 cohort of top-ups has been particularly active because all three trends are aligned. Sagard's amendment was struck in the same week as Cytokinetics' restructuring. Within twelve months of that, Heidelberg Pharma's HCRx/Soleus tripartite amendment on TLX250-Px in early 2026 added a third investor to an existing royalty financing line, again as an amendment to the original document rather than a parallel agreement.

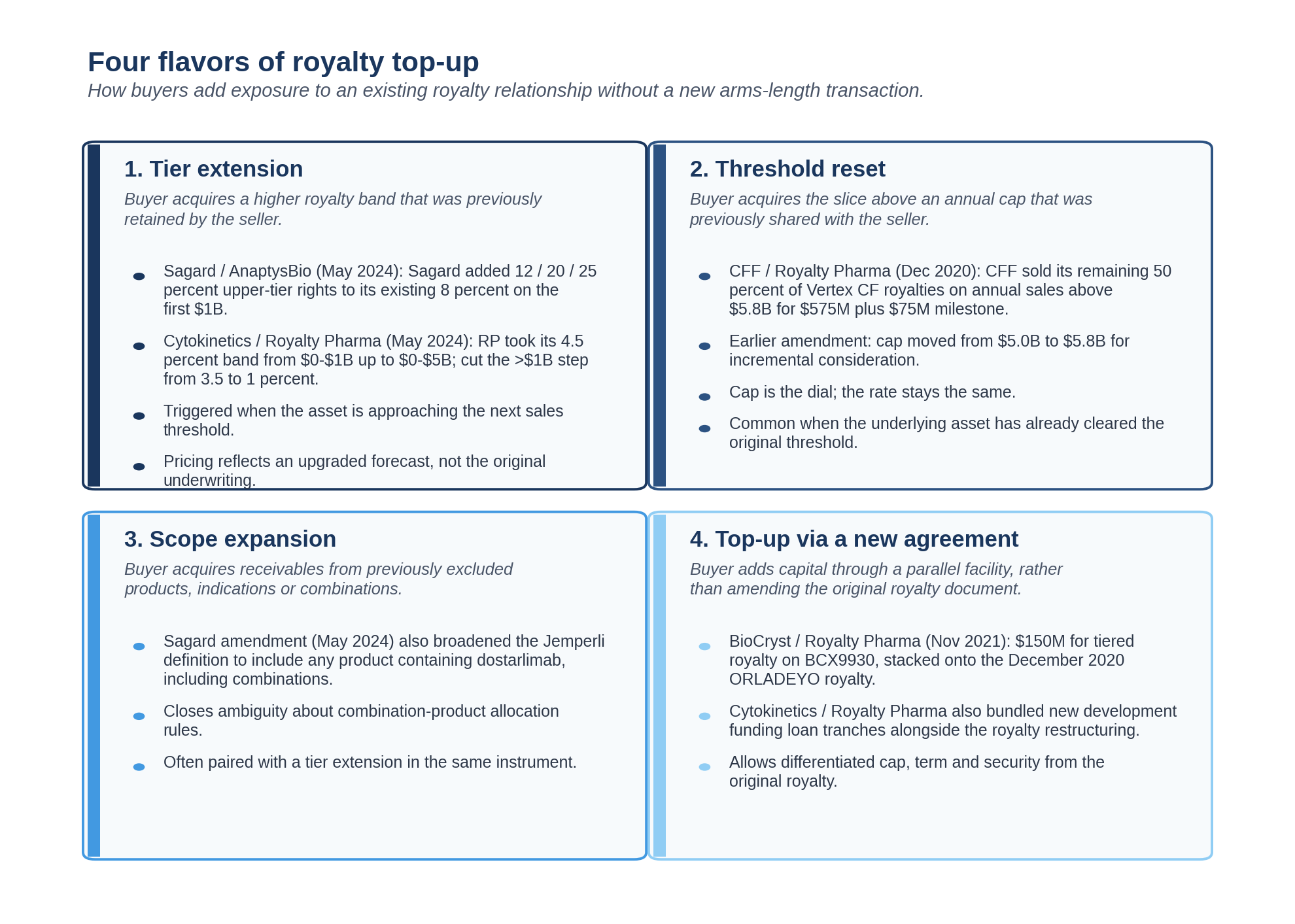

The four flavors of top-up

The Sagard, Cytokinetics, and CFF transactions sit on a small map. Most amendment activity in the market falls into one of four categories.

The legal vehicle is the same across all four: an amendment to the original royalty purchase agreement, with additional purchase price for additional purchased receivables, a new bill of sale, and a refresh of UCC filings. The economic shape is what differs.

Tier extension moves new sales bands into the buyer's economics. This is the AnaptysBio-Sagard shape. The original deal had unmonetized upper tiers; the amendment monetizes them.

Threshold reset moves the share above an existing cap from shared to fully-owned. This is the CFF shape. The original deal had a flat rate with a shared upper slice; the amendment buys out the seller's residual share.

Scope expansion moves new product variants (combinations, indications, geographies) into the receivable. This is what the Sagard amendment did in addition to the tier extension. Many older royalty agreements do not address combination products explicitly, and the first amendment is often the moment to fix that.

Top-up via a new agreement adds capital through a parallel facility rather than amending the original document. This is the Cytokinetics shape, where the royalty restructuring sat alongside new development funding loan tranches and an equity component. The original royalty document was amended for the rate restructuring; the new capital came through fresh instruments.

What to pull on when evaluating the next one

A reader trying to model an amendment-as-top-up should focus on a small number of threads.

The implied multiple on combined capital. AnaptysBio's $300M combined upfront against a $600M cap implies 2.0x at full cap satisfaction. The time-to-cap (currently expected by mid-2027 per management) implies a low-to-mid teens IRR after netting the $50M top-up and the milestone payments. Whether this represents a good return for Sagard depends on the comparison to alternative deployments, but the shape is consistent with current pricing in the late-stage royalty market.

The carve-out structure. The $2 to $2.5B gap and the $75M one-off threshold milestone in the Sagard amendment tell you that AnaptysBio's negotiating position was strong enough to retain meaningful upside. In a softer underlying-asset position, you would expect carve-outs to disappear and the buyer to take the full upper tier without a gap. Carve-outs are a pricing tool: shifting a slice of upside back to the seller is economically equivalent to lowering the absolute-dollar cap, but legally cleaner because it avoids re-negotiating the cap mechanic.

The cap mechanic. Multiple-of-upfront caps are easier to model but introduce an agency problem: the seller has reduced incentive to drive sales after the cap is in sight. Absolute-dollar caps with hard date cutoffs (as in the Sagard amendment) discipline the buyer's IRR by forcing earlier delivery and tend to produce cleaner valuation outcomes. The market has been moving toward the absolute-dollar/hard-date construction.

The product definition. Combination products and combination indications were under-attended in royalty contracts written before 2022 and are now a standard area of negotiation. Any amendment that does not address combination product treatment is leaving meaningful economic value undefined.

Anti-stacking and most-favored-nation language. As royalty buyers consolidate, the same buyer increasingly holds positions in multiple parts of the same therapeutic area. Amendments are the natural moment to refresh anti-stacking and MFN clauses to reflect the new contractual neighborhood.

The bottom line

The point of buying more of an existing royalty is precisely that the buyer already knows the asset and the seller already knows the buyer's cost of capital. The amendment converts that mutual knowledge into incremental capital at a tighter spread than a new deal would clear.

The legal architecture that makes this work — sale-of-receivables form, additional purchase price, expanded definitions, restated thresholds, refreshed UCC filings, supplemental licensee letter, three-tier SPE chain — is now mature enough to be considered a market standard. The next several years of pharma royalty financing will run through these amendments at least as much as through new deal originations.

For the AnaptysBio-Sagard relationship specifically, the May 2024 amendment is on track to deliver the $600M cap before the 31 March 2031 cutoff. That is the answer to whether the top-up was correctly priced. From AnaptysBio's perspective, the $50M was the price paid to lock in early termination of an obligation that was already running. From Sagard's perspective, the $50M acquired upper-tier rights that were already starting to switch on, on an asset that was already outperforming the original underwriting. The number of dollars on each side of the table is roughly the same; the difference is in the timing of when those dollars get realized, and that difference is what the amendment was pricing.

This article reflects publicly available information. It does not constitute investment, legal, or tax advice. The contractual mechanics described are derived from the redacted text of Amendment No. 1 to the Royalty Purchase Agreement filed as exhibit 10.29 to AnaptysBio's 10-Q for the period ended 30 June 2024, the original 8-K filed on 25 October 2021, AnaptysBio's most recent 10-Q for the period ended 30 September 2025, and the press releases of the relevant counterparties. Royalty holders and counsel evaluating specific positions should rely on the underlying contracts and counsel.