China's Royalty Market and VIE Structures: Navigating Enforceability in a $130B Opportunity

On March 2, 2026, Royalty Pharma announced the appointment of Kenneth Sun as Senior Vice President and Head of Asia, effective May 2026. Sun, formerly Head of Asia Pacific Healthcare Investment Banking at Morgan Stanley, will be based in Hong Kong and lead the company's royalty business across the region.

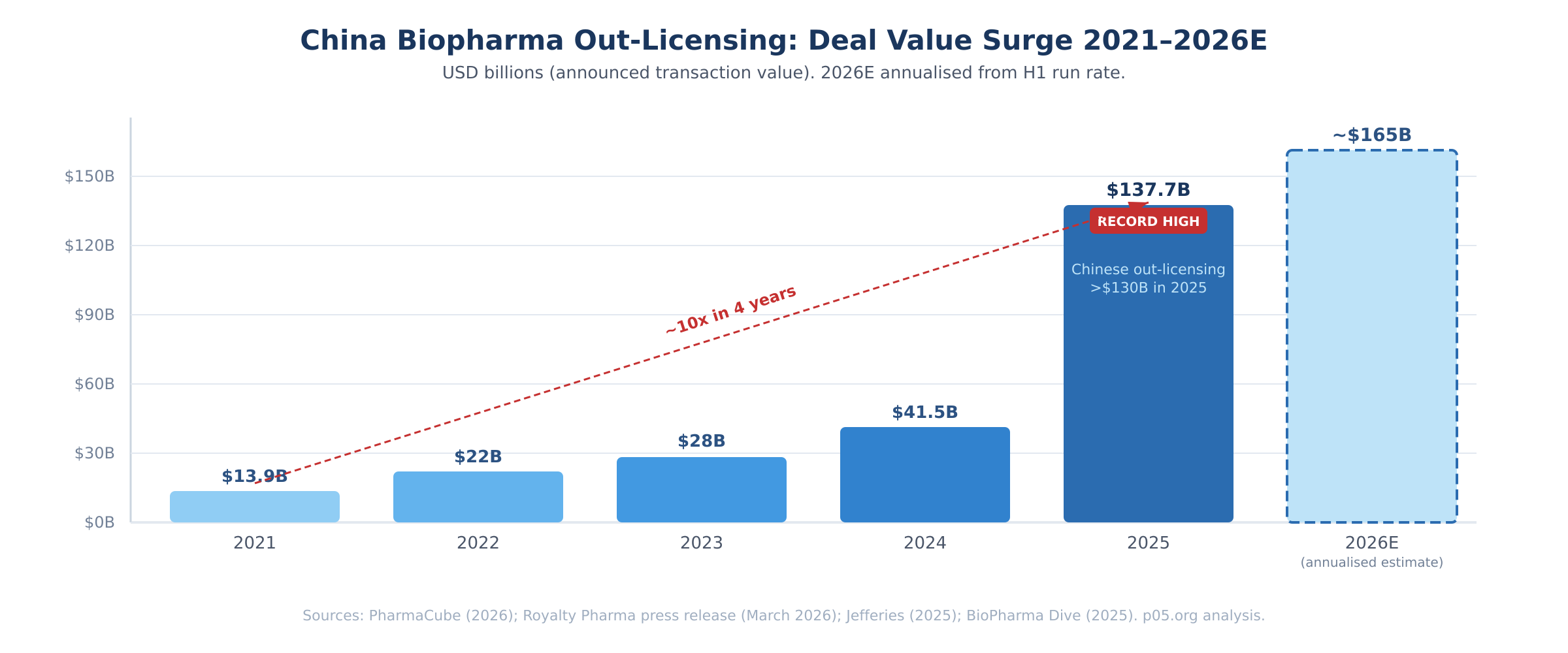

The announcement noted that Chinese medicine out-licensing alone comprised over $130 billion in announced transaction value in 2025, up from approximately $14 billion in 2021.

That move reflects a considered reading of where the royalty market is heading. As Greater China biotechs generate increasingly sophisticated pipelines and as out-licensing deal structures mature, the conditions for a dedicated royalty financing ecosystem in Asia are clearly developing.

This article looks at the structural and legal questions that practitioners in this market are actively working through — specifically around Variable Interest Entity (VIE) structures and the enforceability considerations they raise for royalty investors.

The Scale of the Market

China biopharma out-licensing reached a record $137.7 billion in 2025, a nearly tenfold increase from 2021's $13.9 billion, according to PharmaCube. One-third of global industry licensing spending in 2025 involved drugs sourced from China, per Jefferies.

Average deal size in early 2026 stands at approximately $1.3 billion, a 76% increase over the 2025 average. Chinese companies now account for approximately 20% of all drugs in development globally.

The pipeline composition has shifted materially. Chinese ADCs, bispecific antibodies, and GLP-1 receptor agonists are now among the most actively pursued assets in global pharma business development, and the NewCo deal structure — which places licensed ex-China rights into an offshore vehicle backed by Western investors — has become a well-understood and frequently used mechanism.

The royalties generated by these transactions, typically in the 3–10% of net sales range on licensed territories, are creating the cash flow streams that royalty investors need to build a dedicated Asia portfolio.

Royalty Pharma's thesis might be that this mirrors the founding conditions of the Western royalty market, where Royalty Pharma and its peers built the asset class by working directly with universities, research institutions, and early-stage biotechs before institutional frameworks were fully in place.

How VIE Structures Work

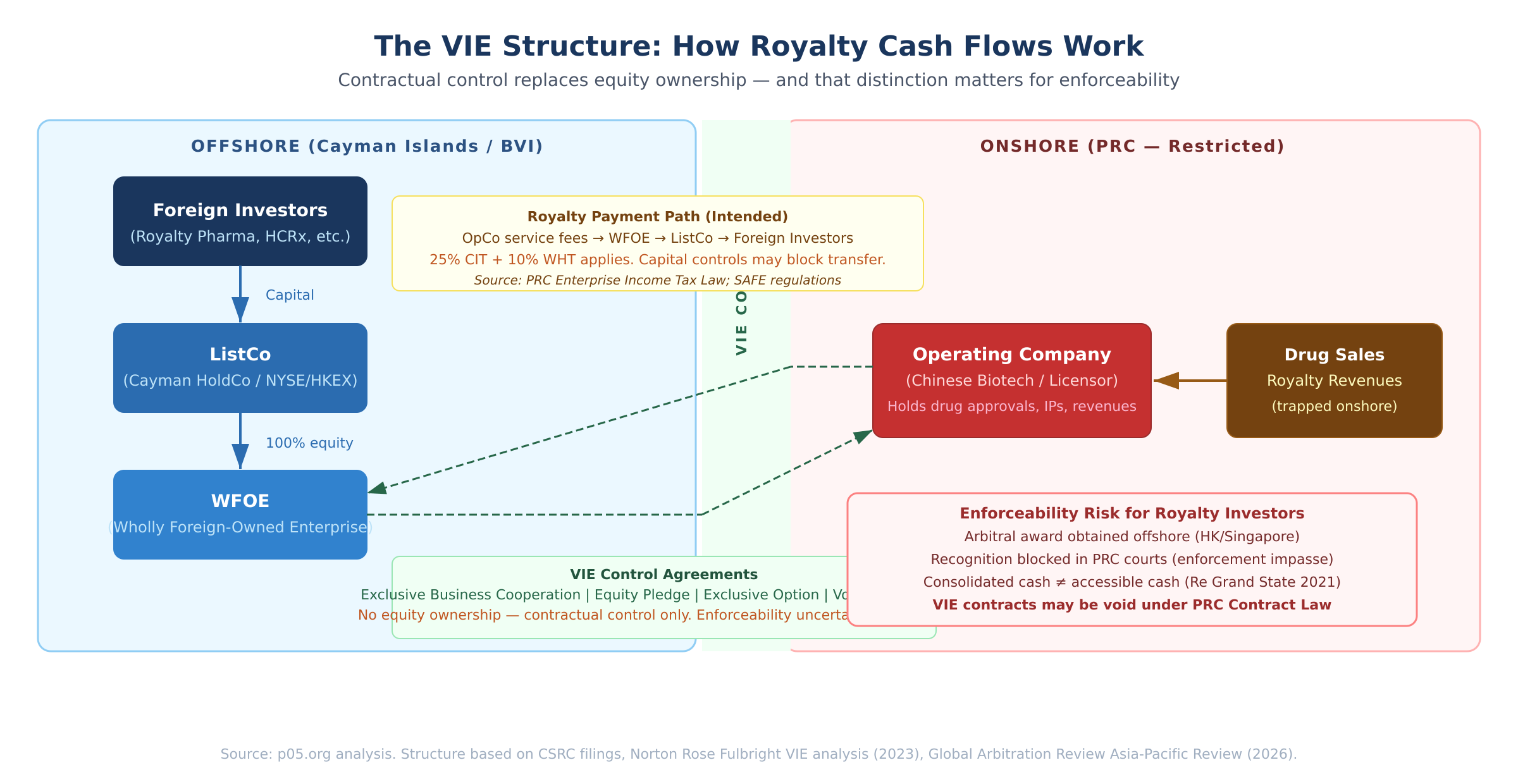

Understanding VIE mechanics is a prerequisite for thinking about royalty deal structuring in this market, since many Greater China biotechs are organised this way, particularly those with US or Hong Kong listings.

China restricts foreign ownership in certain sectors. To access international capital markets despite these restrictions, Chinese companies developed the Variable Interest Entity model, first used by SINA Corporation for its US listing and subsequently adopted by Alibaba, Tencent, Baidu, JD.com, and hundreds of others. By 2021, VIE-structured companies represented 68.8% of all US-listed Chinese firms.

The architecture is as follows. Foreign investors hold securities in an offshore holding company (ListCo) — typically Cayman Islands or BVI incorporated — which in turn owns a Wholly Foreign-Owned Enterprise (WFOE) in mainland China. The WFOE does not directly conduct the restricted business.

Instead, it exercises effective control over the Chinese operating company, owned by founders or PRC nationals, through a suite of contractual arrangements: an Exclusive Business Cooperation Agreement, Equity Pledge Agreement, Exclusive Option Agreement, and Voting Rights Proxy Agreement.

The economic and governance rights flow contractually rather than through direct equity ownership. This distinction — contractual control rather than equity ownership — is what creates the legal questions that royalty investors need to work through carefully.

China's CSRC issued its New Overseas Listing Rules in February 2023, requiring overseas-listed VIE companies to file with the regulator and disclose their VIE arrangements in detail, including control risks and tax considerations. PRC counsel must verify and opine on the structure's legitimacy as part of any listing application.

The market's general reading of this is constructive — it signals that the CSRC is willing to regulate VIE-structured companies within a defined framework, which is a different posture from seeking to prohibit them.

That said, the CSRC's supervisory stance is not a formal legal endorsement of the underlying contractual arrangements, and the fundamental question of VIE validity under PRC law has not been definitively ruled on by Chinese courts. As Norton Rose Fulbright has noted, regulatory and enforcement actions in this space tend to proceed on a case-by-case basis rather than from a settled general ruling.

Enforceability Considerations for Royalty Investors

For a royalty investor whose instrument is a contractual claim on a specific drug's revenue stream, the VIE layer introduces several considerations that differ from the Western deal environment. These are not necessarily deal-stoppers — the market is clearly proceeding — but they shape how deal structures need to be built.

Contractual Control vs Perfected Security

In Western royalty transactions, investors typically hold a perfected security interest over a defined revenue stream, documented under established UCC frameworks or their European equivalents, with enforcement through courts that have decades of royalty-specific jurisprudence. In a VIE context, the investor's claim rests on contractual arrangements where the underlying legal enforceability has not been uniformly settled.

The precedents that do exist are mixed. A 2012 Shanghai arbitral tribunal ruled a VIE structure in online gaming illegal on grounds that the sector was restricted from foreign control through contracts.

In 2015, China's Supreme People's Court upheld an investment agreement involving a VIE in the private school sector, without ruling on the structure's legality as such. Pharmaceutical assets sit in a different regulatory category from internet and gaming businesses, which matters for sector-specific risk, but the underlying structural question applies across VIE arrangements generally.

Offshore Award Recognition

Where disputes arise, the standard approach is offshore arbitration — Hong Kong or Singapore being the typical venues. Both are well-regarded arbitral jurisdictions. The more complex question is what happens if a valid award needs to be enforced against assets located in mainland China.

The Global Arbitration Review's 2026 Asia-Pacific Arbitration Review identifies the "enforcement impasse" as a structural challenge: valid offshore awards face meaningful hurdles to recognition in PRC courts. Since the operating company and its revenues are onshore, an award that cannot be recognised in China has limited practical utility.

This is a well-understood dynamic in the market and informs how deal documentation, security arrangements, and offshore asset structuring are approached.

The Cayman court precedent in Re Grand State Investments Limited is relevant here: consolidated financial statements that include onshore PRC subsidiary cash do not mean the Cayman parent has a legal right to access or deploy those funds. Any transfer requires compliance with PRC law, and the Cayman parent has no direct control over that process. Accounting consolidation and legal access to cash are different things.

Repatriation Mechanics and Tax Structure

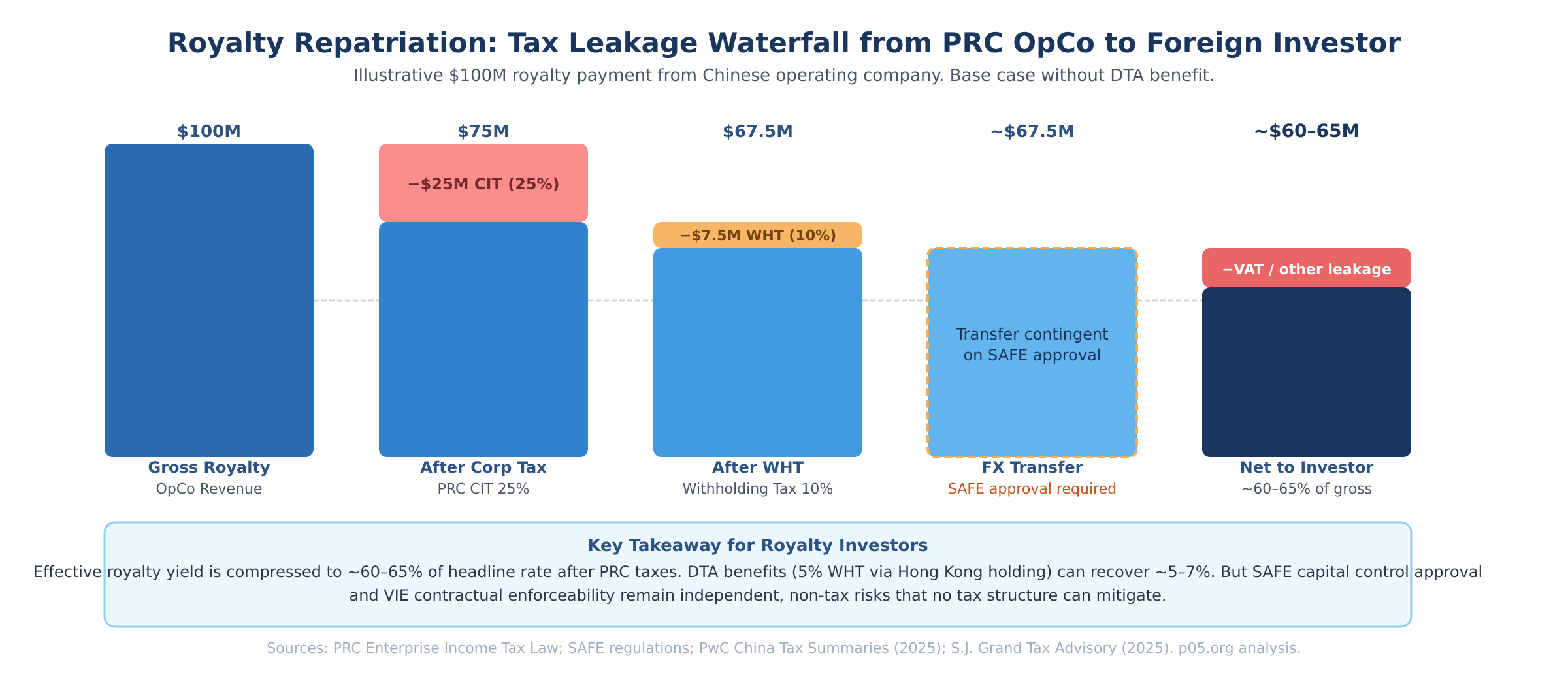

Royalty cash flows from a Chinese operating company to a foreign investor must pass through several layers, each carrying cost and process friction.

Dividends from a WFOE to its Cayman parent are subject to 25% corporate income tax at the operating entity level, plus a standard 10% withholding tax on the dividend payment itself. An intermediate holding company in Hong Kong can reduce the withholding rate to 5% where double taxation agreement conditions are met and the beneficial owner test is satisfied — a structuring step that is widely used but requires substance and careful documentation.

Service fee and royalty repatriation channels face VAT plus withholding corporate income tax. State Administration of Foreign Exchange (SAFE) approval is required for cross-border capital movements, and its processing depends on the nature and documentation of the payment.

China's June 2025 reinvestment tax credit policy offers a 10% credit for foreign investors who reinvest distributed profits into domestic operations for five years or more, which may be relevant for structures where the royalty investor also holds equity in the Chinese company — a hybrid structure increasingly discussed in the NewCo context.

The net effect is that effective royalty yields in China are meaningfully below the headline rate agreed in any licensing contract. Modelling those yields requires assumptions about tax structure, repatriation route, and SAFE processing that add noise to discounted cash flow valuations.

This is solvable — practitioners routinely do it in other emerging market royalty contexts — but it requires market-specific modelling that is distinct from Western deal analysis.

China-Specific Commercial Risk Factors

Beyond the structural and legal considerations, Chinese drug revenue trajectories have characteristics that differ materially from Western reference cases and that affect royalty valuation directly.

The National Reimbursement Drug List (NRDL) annual negotiation cycle typically compresses prices significantly in exchange for inclusion — and inclusion drives the volume growth that underpins revenue projections. Volume-Based Procurement (VBP) operates on a different mechanism, substituting branded drugs with generics at scale in hospital procurement, and can erode market share for patented products in affected segments.

China's January 2025 Anti-Monopoly Guidelines for the pharmaceutical sector, issued by SAMR, bring pharmaceutical licensing arrangements within the scope of antitrust scrutiny for the first time, including scrutiny of IP licensing and royalty platform arrangements. These are known variables that experienced market participants incorporate into deal pricing, but they require a different analytical framework from European or US royalty modelling.

The NewCo Layer and What It Solves

Much of the 2025 Chinese out-licensing volume flowed through NewCo structures rather than direct VIE engagement, and this distinction is important for understanding where different types of royalty investments sit.

Under the NewCo model, a Chinese biotech assigns ex-China development and commercialisation rights to a newly formed offshore company, typically US or Cayman incorporated, in which Western investors hold equity and the Chinese licensor retains a meaningful stake.

The royalty stream flows from the Western commercial entity back to the NewCo — a contractual arrangement governed by familiar law, enforceable through established arbitral venues, and not subject to SAFE approval. Hengrui's Kailera Therapeutics, Braveheart Bio, and AbbVie's RemeGen deal at up to $5.6 billion are prominent examples.

For royalty investors, the NewCo layer is largely accessible using existing deal architecture. The Chinese VIE sits behind the licensor, but the royalty investor's counterparty is the offshore NewCo entity — Western law applies, enforcement works through recognised channels, and the cash flow does not require SAFE approval.

The harder, and more original, market opportunity is what Royalty Pharma is describing: partnering directly with Greater China biotechs against their domestic Chinese revenue streams, before or instead of a NewCo structure.

It is also the context in which the VIE, enforcement, and repatriation considerations discussed above are most directly relevant, and where deal structures will need to be designed specifically for the environment rather than adapted from Western templates.

Deal Architecture Considerations

Practitioners in this market are working through a set of structural design questions that will define the emerging deal standard.

Dispute resolution clauses in China-facing royalty transactions will typically specify Hong Kong or Singapore arbitration — both well-regarded, both with established pharma-sector experience. The more active design question is how to create meaningful security arrangements against offshore assets, not solely contractual commitments relying on onshore enforcement.

Structures that include pledges over HKEX-listed shares, offshore intellectual property assignments, or escrow arrangements funded by initial royalty payments are among the approaches being evaluated.

Tax structuring through a Hong Kong intermediate holding company is near-standard for transactions involving Chinese revenue streams, given the DTA benefits available. But meeting the beneficial owner requirements under the DTA requires genuine substance in the Hong Kong entity, which adds operational complexity.

Founder and management risk — the dynamic illustrated by cases like GigaMedia's loss of T2CN — has no direct Western equivalent and requires specific contractual and governance provisions. Enhanced step-in rights, offshore security packages, and careful attention to the control document (chop) arrangements that operationally underpin VIE structures are among the tools available.

Valuation methodology needs to incorporate NRDL pricing dynamics, VBP exposure, and Chinese market epidemiology as first-order inputs rather than adjustments. The analytical frameworks exist; they require investment to build into deal screening processes.

Comparative Structure: China vs Western Royalty Transactions

| Dimension | Western Market | China (VIE) |

|---|---|---|

| Contractual enforceability | High — established case law | Sector-dependent — case-by-case regulatory approach |

| Security interest | Perfected UCC / patent pledge | Contractual control; equity pledge over opco shares |

| Arbitral award recognition | Most major jurisdictions | Offshore awards — enforcement impasse in PRC courts |

| Cash repatriation | Free (subject to WHT) | SAFE approval; capital controls |

| Effective tax rate on royalty | 0–15% WHT | ~35% before DTA; ~25–28% with HK holding |

| Reimbursement risk | Moderate | Material (NRDL cycles, VBP) |

| Founder / management risk | Standard governance | Elevated — VIE operational control through chops |

| DTA available | Yes | Yes, via HK intermediate (5% WHT) |

Where the Market Is Heading

Royalty Pharma's Hong Kong appointment will likely prompt parallel moves from HealthCare Royalty, DRI Healthcare, and others who have been watching the deal volume data with similar interest. The competitive dynamic resembles what happened in the mid-2000s as the Western royalty market institutionalised — early movers who built relationships and developed deal architecture before the market standardised established lasting advantages in deal flow and pricing.

Three things will define how quickly the Asia royalty market develops into a recognised asset class. First, standardisation of deal documentation — the first set of completed, disclosed China-onshore royalty transactions will provide the precedents around which market terms converge. Second, valuation model development — firms that invest in building China-specific revenue projection frameworks will price deals more accurately and win more transactions on the margin.

Third, regulatory evolution — China's policy environment for foreign investment in healthcare is moving in a constructive direction, with the CSRC's New Listing Rules and the NMPA's 2025 reform agenda both pointing toward greater integration with global norms, which over time reduces the structural uncertainty that currently requires bespoke deal architecture.

The underlying opportunity — royalty streams generated by an innovation ecosystem that now accounts for one-third of global licensing spending — is evidently attracting the capital and talent needed to build that infrastructure.

All information in this article was accurate as of the research date (March 2026) and is derived from publicly available sources including company press releases, regulatory publications, legal analyses, and financial reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. I am not a lawyer or financial adviser.

Member discussion