Convertible Royalty Notes in Pharmaceutical Financing

The Instrument in Context

Non-recourse royalty-backed notes, discussed in the companion article on this site, represent one evolutionary step in the maturation of pharmaceutical royalty financing. The convertible royalty note represents the next.

Where a standard royalty-backed note gives the investor a defined, capped return secured against a product revenue stream, a convertible royalty note adds a third layer: the option — belonging either to the investor, the issuer, or both — to convert some or all of the instrument into equity.

The addition of this conversion feature transforms a bounded-return debt obligation into a multi-modal instrument capable of delivering fixed income, royalty income, or equity participation depending on which path a drug's commercial trajectory triggers.

That three-way optionality is not accidental. It reflects a deliberate market evolution in which royalty investors and biotech CFOs have become increasingly sophisticated in their structuring, and in which the persistent gap between public equity valuations and intrinsic asset values has created demand for instruments that can bridge debt and equity without immediately sacrificing either.

Gibson Dunn's 2026 Life Sciences Industry Outlook documented that hybrid financing structures blending traditional royalty economics with elements of term debt or structured credit are becoming increasingly prevalent, with transactions now regularly incorporating return caps, milestone-linked triggers, debt-like covenants, and even make-whole provisions at maturity — the precise toolkit from which convertible royalty notes are assembled.

Definition: What Is a Convertible Royalty Note?

A convertible royalty note is a debt instrument — formally a note or loan — issued by a pharmaceutical or biotechnology company, the repayment of which is partially or wholly secured by a pledged royalty stream, and which includes a contractual right permitting conversion of the outstanding principal (and sometimes accrued interest) into an alternative form of consideration.

That alternative consideration takes several forms depending on the specific deal:

Equity conversion. The investor exercises an option to convert the outstanding note balance into shares of the issuer at a pre-agreed price or at a discount to the issuer's next qualified financing round. This is the most common form and most closely resembles a convertible promissory note in venture financing — but with the royalty stream serving as collateral in lieu of general corporate recourse.

Royalty acquisition option. The investor holds the right to purchase additional royalty percentage points upon certain trigger events (regulatory approval, commercial milestone, financing round), effectively deepening their position in the revenue stream rather than converting to equity.

Issuer call with premium. The issuer holds the right to repurchase the note at a specified premium prior to maturity, providing a clean exit mechanism that can eliminate the royalty obligation in exchange for a lump-sum payment.

These three modes are not mutually exclusive. Some deals combine all three, creating a menu of optionality that can be exercised depending on circumstances. At its core, the convertible royalty note is distinguished from its close cousin the non-recourse royalty-backed note by one feature: it does not simply repay and extinguish. It can transform.

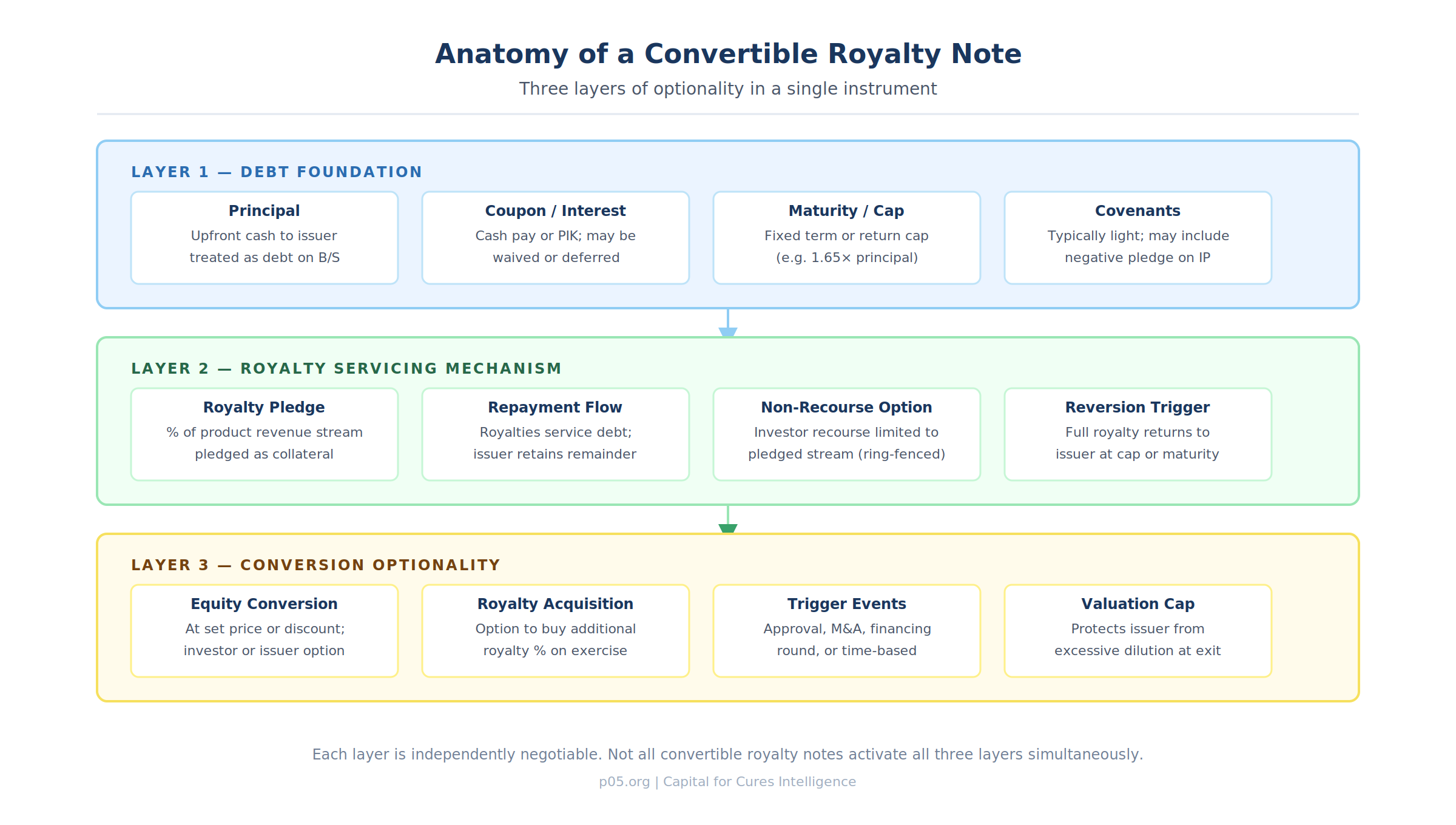

The Three-Layer Structure

A convertible royalty note is most clearly understood through its three distinct structural layers, each independently negotiable.

[See graphic: Anatomy of a Convertible Royalty Note]

Layer 1: The debt foundation. The note carries a principal amount, a coupon (which may be zero, cash-pay, or payment-in-kind), and a maturity date or return cap. It sits on the issuer's balance sheet as a liability. The issuer records the upfront cash received as a borrowing; subsequent royalty payments directed to the noteholder are treated as debt service, not as a sale of an asset. This has meaningful implications for financial reporting — the issuer avoids recognising a gain on sale and preserves the royalty asset on its books.

Layer 2: The royalty servicing mechanism. Rather than relying on general corporate cash flows to service the debt, the issuer pledges a defined percentage of a royalty stream as security. Royalty payments from the commercial partner (the licensee) flow first to the investor, up to an agreed proportion, with the remainder continuing to the issuer. In a non-recourse structure, if the royalty stream is insufficient to fully repay the note, the investor has no claim against the issuer's other assets.

In a limited-recourse structure, the investor retains certain fallback claims — commonly triggered by bankruptcy, change of control, or material breach — but not by simple commercial underperformance.

Layer 3: Conversion optionality. This is the defining layer. The conversion right specifies: who holds it (investor, issuer, or both); what triggers it (time, regulatory approval, acquisition offer, qualified financing round, or investor election); at what price or ratio conversion occurs (fixed price, discount to future round, market price at time of conversion); and what happens to the royalty pledge upon conversion (it typically terminates, with the full stream reverting to the issuer or, in some structures, being retained pro-rata by the investor).

The interplay of these three layers creates a return profile that no single traditional instrument can replicate: a floor provided by the debt structure, a middle path provided by royalty repayment, and a ceiling — potentially significant — provided by equity participation in a successful drug franchise.

How It Functions: The Economics

To illustrate, consider a stylised transaction:

A mid-cap biotech company has licensed a drug to a major pharmaceutical partner. The partner pays tiered royalties of 8–12% on net sales. The biotech holds the royalty stream but needs $150 million to fund a Phase 3 trial in a second indication. It issues a convertible royalty note to a royalty-focused investor on the following terms:

| Term | Value |

|---|---|

| Principal | $150 million |

| Coupon | 0% (repaid via royalties) |

| Royalty pledge | 25% of the royalty stream |

| Return cap | 1.75× principal ($262.5M) by year 8 |

| Reversion | 100% royalties revert upon reaching cap |

| Conversion option | Investor may convert at $22.00/share (20% premium to issue price) within 36 months |

| Trigger | Investor election or acquisition event |

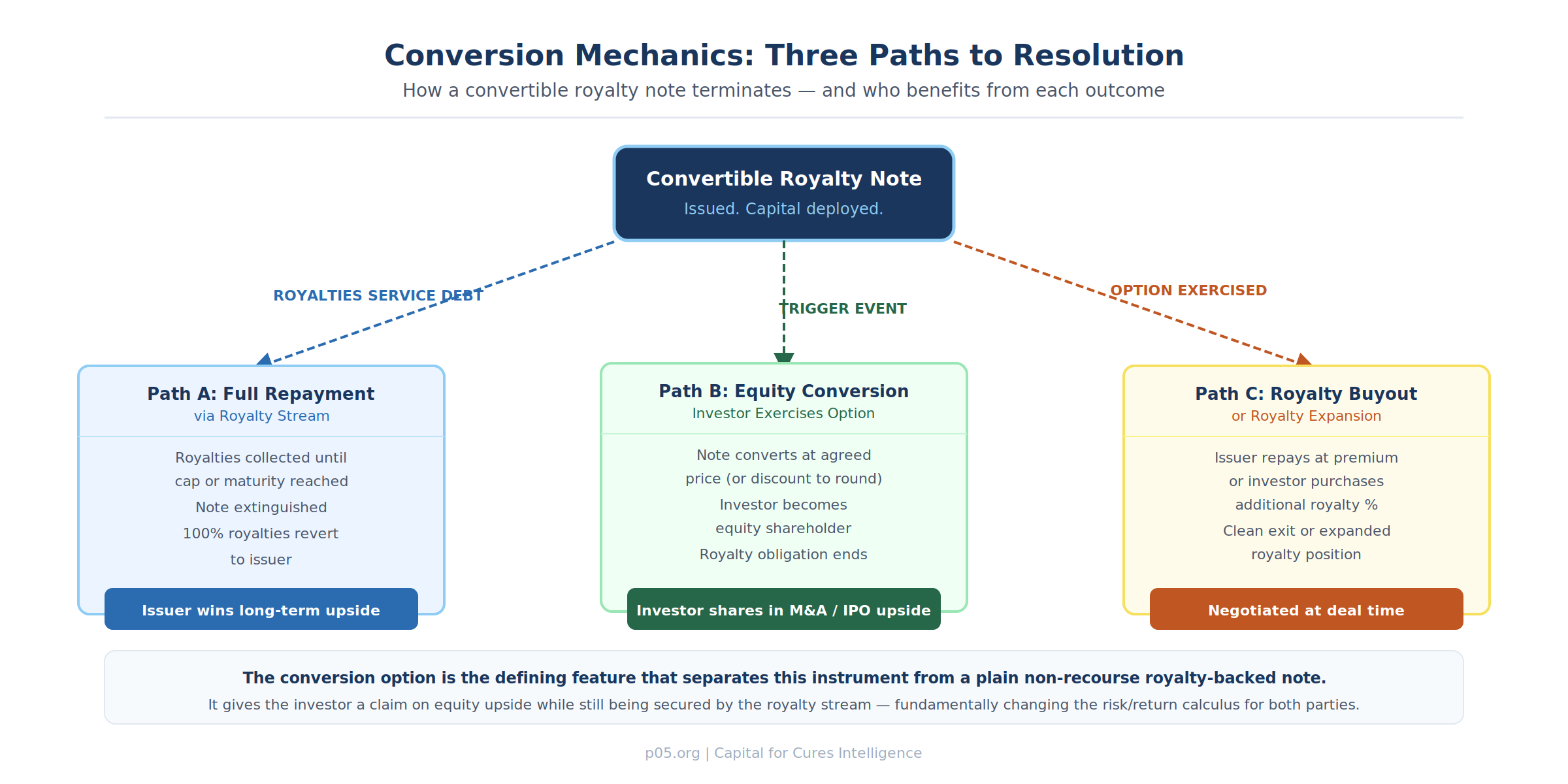

Under this structure, three scenarios play out differently:

In Scenario A — the drug commercialises successfully — the 25% royalty slice generates sufficient cash to hit the 1.75× cap well before year 8. The note is discharged. The issuer recovers 100% of the royalty stream. The investor earns an IRR determined by how quickly the cap is reached — faster commercial uptake means higher IRR. The conversion option is not exercised because the royalty path is more lucrative.

In Scenario B — the drug is acquired by a larger pharmaceutical company at a significant premium — the investor exercises the conversion option, converting the outstanding note balance into shares at $22.00, then participating in the acquisition at the deal price. This is materially more valuable than waiting for royalty repayment. The investor profits from equity upside they could not access through the royalty stream alone.

In Scenario C — commercial performance disappoints — the royalty stream slows. The investor collects its 25% share for as long as exclusivity holds. It does not exercise the conversion option. The note approaches maturity unpaid. In a true non-recourse structure, the investor absorbs the shortfall. In a limited-recourse structure, the issuer may owe a make-whole payment.

This three-scenario topology is the reason convertible royalty notes have found institutional buyers among both royalty funds and crossover investors. The instrument is not purely a drug-commercial bet (as a non-recourse royalty note is). It is also a corporate valuation bet.

The Conversion Mechanics in Detail

The mechanics of conversion are where most of the negotiation occurs. Several structural choices materially affect the economics of the instrument.

Conversion price determination. In late-stage biotech deals, the conversion price is typically set at a premium to the issuer's current share price — commonly 10–30% above the trading price at signing. This gives the investor protection against paying more than market on conversion while giving the issuer room to argue the instrument is not immediately dilutive.

For private companies, the conversion price is more commonly expressed as a discount to the next qualified financing round — typically 15–25% below the round's per-share price — replicating the structure of a conventional convertible note but with the royalty stream as additional security.

Optional versus mandatory conversion. Most pharmaceutical convertible royalty notes treat conversion as optional for the investor — a right, not an obligation. This preserves the investor's ability to remain a creditor (with secured collateral) rather than an equity holder if the conversion economics are unfavourable. Some structures include mandatory conversion upon a change of control above a price threshold, ensuring the investor participates in a buyout rather than remaining as a floating creditor.

Treatment of accrued interest upon conversion. If the note carries a cash coupon that accrues prior to conversion, the agreement must specify whether accrued-but-unpaid interest is: converted into additional shares at the conversion price; paid in cash at the time of conversion; or forgiven in exchange for the equity position. The most investor-friendly structure includes accrued interest in the conversion calculation. The most issuer-friendly forgives it in exchange for a clean equity conversion.

Royalty pledge on conversion. Upon conversion, the pledge of the royalty stream typically terminates. The investor, now a shareholder, no longer has a ring-fenced collateral claim on the royalty revenue — they are an unsecured equity holder. This is a significant shift in the investor's risk position. In exchange, the investor gains full participation in the company's equity upside, including any value beyond the royalty stream embedded in the development pipeline, balance sheet, or strategic positioning.

Valuation cap. For transactions involving private companies or smaller biotechs, a valuation cap — borrowed from the venture convertible note playbook — may be included. This ensures the investor converts at the lower of the cap price or the discount to the qualified financing round, protecting against a scenario in which the company's valuation skyrockets before the investor has converted.

The Capital Stack Position

A convertible royalty note occupies an unusual position in the capital stack — and that position shifts upon conversion.

Before conversion, the note behaves like secured debt. The pledged royalty stream is ring-fenced collateral; the investor has priority over that specific cash flow. If the issuer goes bankrupt, the investor's claim is against the royalty collateral, not the general estate. This gives the pre-conversion instrument better downside protection than unsecured debt and substantially better protection than equity.

After conversion, the investor is a common shareholder. Downside protection evaporates; they are subordinated to all creditors. In exchange, they have unlimited upside participation. For a royalty investor whose mandate is typically defined-return credit investing, the decision to convert is a deliberate step outside their normal risk profile — and one that must be contractually authorised by their fund documentation.

This creates an important selection effect: investors who include conversion rights in royalty note transactions are implicitly signalling they have equity-like conviction in the underlying company, not merely product-level conviction. The royalty stream provides the floor; the equity conversion provides the bet. The combination is available in no other single instrument.

For existing equity holders, the convertible royalty note creates dilution risk — but deferred, contingent dilution, not immediate. Unlike a direct equity offering, the note does not dilute until conversion. If the conversion price is set at a meaningful premium, dilution is triggered only in scenarios where the company's equity has already appreciated — aligning the issuer's dilution cost with performance outcomes.

Distinction from Related Instruments

The market's vocabulary around hybrid royalty instruments is imprecise, and four instruments are frequently confused.

Convertible royalty note versus non-recourse royalty-backed note. As analysed in detail in the companion article, the non-recourse royalty-backed note — exemplified by the Royalty Pharma–Zymeworks transaction announced in March 2026 — has no equity conversion feature. It is purely a debt instrument repaid via royalties, with a capped return and full reversion. The convertible royalty note adds the third layer: the option to transform into equity.

Convertible royalty note versus synthetic royalty. A synthetic royalty, as described by Covington & Burling, typically involves a funder receiving a percentage of product revenue, sometimes with IP or product-level security, and often with put rights triggered by defined events (bankruptcy, change of control, breach). Synthetic royalties rarely include equity conversion features; they are revenue-interest instruments dressed in royalty clothing. Convertible royalty notes are explicitly designed with equity optionality as a core term.

Convertible royalty note versus traditional convertible note. A standard convertible note as used in venture financing is a short-term debt instrument converting to equity at the next qualified financing round. It carries no royalty pledge and no ring-fenced collateral. The convertible royalty note grafts the royalty security structure onto this convertible architecture — creating an instrument with a secured floor and an equity ceiling that a traditional convertible note cannot provide.

Convertible royalty note versus development funding agreement (DFA). Royalty Pharma's 2022 and 2024 agreements with Cytokinetics illustrate the DFA model: staged tranches of capital available upon clinical and regulatory milestones, repaid through either fixed quarterly instalments or (if successful) royalty payments. DFAs are more complex and multi-layered than convertible royalty notes; they are pipeline financing structures rather than single-asset secured instruments. The convertible royalty note is narrower in scope — one asset, one note, one conversion right.

Representative Deal Structures

Because convertible royalty notes are negotiated privately and not always publicly reported with full structural detail, the market is harder to survey than the broader royalty financing landscape. The table below captures illustrative structural patterns drawn from publicly disclosed transactions and market precedents.

| Structure | Principal | Royalty Pledge | Conversion Feature | Notable Terms |

|---|---|---|---|---|

| Royalty note + equity conversion option | $50–200M | 15–40% of stream | Investor option at premium to issue price | Triggered by FDA approval or M&A; valuation cap included |

| Development funding + royalty purchase + equity | $100–575M | Royalty purchased outright, not pledged | PIPE purchase concurrent with note | Cytokinetics–Royalty Pharma 2024; debt repaid or converted to royalty |

| Convertible royalty note (early-stage) | $10–50M | % of future licensing revenue | Investor option, discount to next round | Pre-commercial; relies on licensing pipeline not sales royalties |

| Capped note + royalty acquisition option | $150–300M | 20–30% of stream | Investor may purchase additional 10% royalty upon approval | Return cap for debt portion; royalty option creates expansion path |

The Cytokinetics–Royalty Pharma collaboration, while technically structured as a combination of a development funding agreement, royalty purchase amendment, and equity purchase rather than a single convertible royalty note, illustrates the multi-layer logic: Royalty Pharma committed up to $575 million, received enhanced royalty terms on aficamten (restructured to 4.5% on sales up to $5 billion), funding conditioned on regulatory milestones, and a $50 million concurrent equity purchase — demonstrating how royalty investors increasingly seek multi-modal exposure to their portfolio companies.

Why Convertible Royalty Notes Are Gaining Traction

Several structural forces have aligned to make convertible royalty notes more common in the pharmaceutical financing landscape as of early 2026.

The IPO market correction. As Gibson Dunn documented, biotech capital markets in the first half of 2025 were effectively frozen, with Liberation Day tariff uncertainty collapsing deal activity. Companies that would previously have financed clinical programmes through equity offerings turned to structured alternatives. Convertible royalty notes provide capital without immediate dilution and without the covenant intensity of venture debt — a compelling combination when equity markets are hostile.

Issuer conviction about asset undervaluation. When a company's stock trades at a discount to the net present value of its royalty portfolio, issuing a convertible note at a premium to the current share price is arguably accretive. The issuer accepts some dilution risk upon conversion but only at a price that implies the market has already recognised more value. This logic closely mirrors the rationale Zymeworks articulated for its non-recourse royalty-backed note in March 2026 — the convertible adds an equity optionality layer on top of the same core conviction.

Investor appetite for equity participation. Traditional royalty funds — including Royalty Pharma, HealthCare Royalty Partners, and newer entrants — have historically been defined-return investors. Their mandates typically require bounded IRR targets rather than uncapped equity participation. But crossover investors and hybrid funds, increasingly active in the royalty market, have mandates that accommodate equity conversion. As WilmerHale documented, the investor base for royalty financings has deepened considerably since 2020, with new participants bringing different return expectations and structural preferences.

M&A optionality. The convertible royalty note gives investors a path to participate in a buyout premium. For a drug company widely considered an M&A target — where the equity could gap significantly above current levels on an acquisition announcement — holding an equity conversion right is qualitatively different from holding a capped royalty claim. Investors who believe a company will be acquired within the note's conversion window have a strong incentive to negotiate the conversion feature, even at some cost to the royalty economics.

Growing market scale. The aggregate royalty financing transaction value reached approximately $6.5 billion in 2025, according to Gibson Dunn's tracking, up from $5.7 billion in 2024. As the market grows and structures proliferate, the convertible royalty note is becoming a recognised category rather than a bespoke one-off — lowering the legal and structuring costs that previously made it inaccessible to smaller transactions.

Accounting and Tax Treatment

The accounting treatment of a convertible royalty note is more complex than either a straight debt instrument or a royalty sale, because the instrument contains embedded derivatives — the conversion option — that must be bifurcated and valued separately under both US GAAP and IFRS.

Under US GAAP (ASC 470-20). The FASB's ASU 2024-04, issued in November 2024, updated guidance on induced conversions of convertible debt instruments, requiring a preexisting contract approach to determine whether induced conversion or extinguishment accounting applies. For a convertible royalty note with a standard investor-election conversion right, the note is generally recorded in full as a liability. If the conversion feature is not clearly and closely related to the debt host, it must be bifurcated and recorded as a derivative at fair value, with changes in fair value flowing through the income statement — a source of earnings volatility that CFOs should model before signing.

Under IFRS 9. The convertible royalty note presents a hybrid financial instrument. The debt host is measured at amortised cost; the conversion option, being an equity conversion into a variable number of shares (if not fixed price), may be classified as a financial liability measured at fair value through profit or loss. The royalty pledge component adds further complexity, as it may need to be assessed as a separate financial instrument or an embedded derivative.

Tax characterisation. As RSM has documented, the substance-over-form analysis governs. A convertible royalty note that walks and talks like debt — fixed repayment schedule, security interest, no permanent transfer of ownership, conversion at the investor's election rather than the issuer's command — is generally treated as debt for US federal tax purposes. The issuer continues to recognise royalty income and deducts the interest component of payments to the noteholder. Upon conversion to equity, the investor recognises capital gain or loss on the difference between the converted amount and their tax basis in the note.

Structural Risks and Investor Considerations

The convertible royalty note's multi-modal optionality creates risks that do not arise in simpler instruments.

Royalty stream risk. If the underlying drug underperforms commercially, the royalty stream may be insufficient to service the note. The investor's conversion option provides no floor against this scenario — a out-of-the-money equity conversion right is not a substitute for principal recovery. The collateral analysis must therefore be robust enough to support the principal even in a downside commercial scenario.

Conversion price risk for the issuer. If the conversion price is set too low, conversion at full scale creates material dilution. If the conversion window is too long, the issuer remains under threat of significant equity issuance throughout the window. CFOs should model diluted share counts under conversion scenarios before agreeing to conversion terms, particularly if the company is also carrying other convertible instruments or warrant obligations.

Fund mandate misalignment. Pure royalty funds whose mandates restrict equity ownership may find that a conversion right they negotiate but cannot ultimately exercise provides negative optionality — they are giving the issuer a lower royalty rate or more favourable note terms in exchange for a conversion feature they cannot use. Legal review of fund documentation before including conversion rights is essential.

Bankruptcy treatment. The ring-fenced royalty pledge provides the investor with collateral security in a bankruptcy scenario. Upon conversion to equity, that security is lost. The timing of conversion relative to the issuer's financial health is therefore critical. An investor who converts in good faith and subsequently faces the issuer's insolvency is no longer a secured creditor — they are an unsecured equity holder.

M&A encumbrance. The conversion right can complicate acquisition transactions. A buyer conducting diligence on a target with outstanding convertible royalty notes must model the cost of conversion (dilution) versus the cost of triggering any change-of-control repayment provisions. This can impede M&A transactions or reduce headline acquisition prices — exactly the dynamic that Cytokinetics investors cited as a concern following the 2024 Royalty Pharma collaboration announcement.

When Does the Convertible Royalty Note Make Sense?

For issuers, the convertible royalty note is most appropriate when several conditions are met simultaneously: the issuer holds a valuable royalty stream but does not wish to permanently monetise it; the issuer's equity is believed to be undervalued and is expected to appreciate meaningfully; the issuer has a near-to-medium term catalyst (regulatory approval, M&A process, clinical data) that could trigger favourable conversion economics; and the issuer can tolerate the accounting complexity and contingent dilution that the instrument entails.

For investors, the instrument is attractive when their mandate accommodates equity participation; when they have strong conviction in both the drug's commercial trajectory (supporting the royalty floor) and the company's equity story (supporting the conversion ceiling); and when the deal terms provide sufficient royalty security to make the instrument defensible even if the conversion option expires unexercised.

The convertible royalty note is not appropriate as emergency financing — the structural complexity and negotiation time required make it unsuitable for companies in acute capital distress. Nor is it appropriate when the conversion feature cannot be priced rationally — pre-commercial assets without a clear equity valuation anchor make the conversion economics speculative to the point of un-underwritability.

The Market Direction

Gibson Dunn's 2026 outlook noted that 87% of surveyed biopharma executives expect to incorporate royalty financing into their capital-raising strategies over the next three years, and that the expanded capabilities of leading royalty participants signal an active environment in 2026. Within this growth, structural innovation is the primary competitive dimension. Return caps, milestone triggers, step-down royalty rates, and put/call rights have become standard. The convertible royalty note is the logical next step: adding equity participation to the already-complex royalty toolkit.

The Royalty Pharma–Zymeworks non-recourse note from March 2026 established clean precedent for the non-convertible variant. The convertible variant is not yet standardised — terms vary substantially across deals, and there is no equivalent public benchmark transaction to anchor market expectations. But the building blocks are fully in place, and the demand from both sides of the transaction is evident.

As the royalty financing market continues its trajectory from $6.5 billion in 2025 toward a larger and more diverse capital formation venue, the convertible royalty note will increasingly fill the space between plain debt and full royalty monetisation — a space that biotech CFOs urgently need to occupy, and that a new generation of hybrid investors is explicitly positioning to serve.

All information in this article was accurate as of the publication date and is derived from publicly available sources including SEC filings, company press releases, regulatory announcements, legal firm publications, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.

Member discussion