Force Majeure and MAC Clauses in Pharmaceutical Royalty Agreements: The Pandemic's Unfinished Legal Lesson

When COVID-19 spread across the global economy in early 2020, lawyers across every sector reached for the same clause in their contracts: force majeure. In pharmaceutical licensing, supply, and manufacturing agreements, the consequences were immediate and visible. In pharmaceutical royalty agreements, something subtler and more instructive happened.

Almost nothing changed — not because the clauses were adequate, but because they were structurally irrelevant to the commercial risk that was actually materialising.

Five years on, the pharmaceutical royalty market has processed the implications of that discovery. This article examines whether force majeure and MAC provisions are present in royalty agreements, what function they actually serve, what could plausibly happen if the next pandemic or systemic shock materialises, and why the realistic answer is considerably less dramatic than the theoretical one.

The Two Mechanisms and Why They Are Different

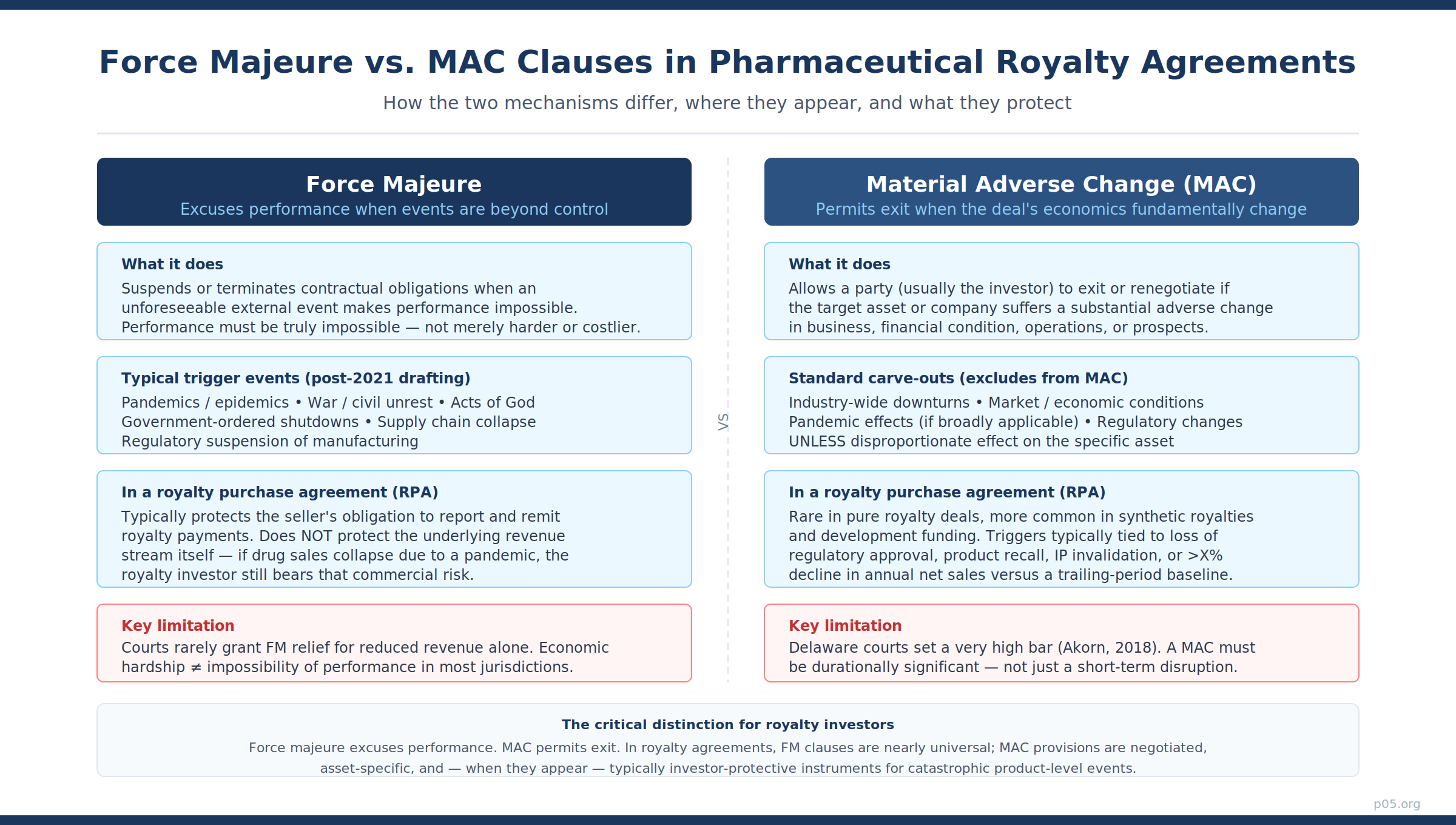

Force majeure and material adverse change (MAC) clauses are related but distinct instruments. Understanding the distinction is essential before asking whether either applies in royalty agreements.

A force majeure clause excuses a party from performing its contractual obligations when an external event, beyond the party's reasonable control, makes performance impossible. The emphasis is on impossibility — not on performance becoming more expensive, less economically attractive, or commercially inconvenient. Most common law courts, particularly in the United States and England, interpret force majeure provisions narrowly.

As Norton Rose Fulbright summarised, economic downturns, changes in market price, or increases in cost of performance will not typically constitute force majeure events even if the changes are very substantial.

A MAC clause operates differently. Where force majeure responds to external events that prevent performance, a MAC provision allows a party — typically the investor or acquirer — to exit or renegotiate a transaction when the value of the underlying asset or business has suffered a substantial adverse change. The triggering event is not impossibility but a material deterioration in financial condition, operations, or prospects.

As the Harvard Law School Forum on Corporate Governance noted in its detailed analysis, MAC clauses allow parties to avoid obligations because of a material adverse change in the other party's financial condition, even where performance remains technically possible.

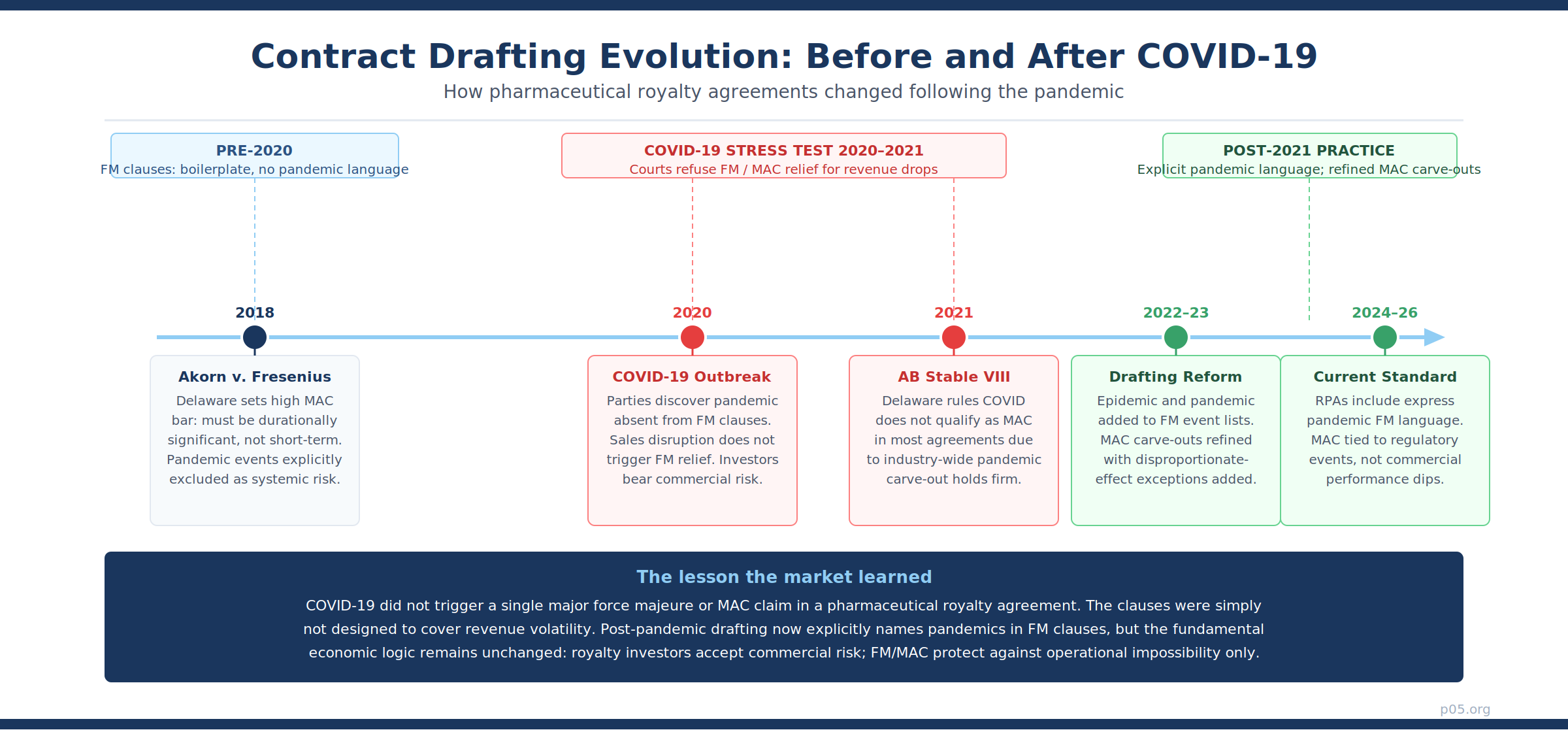

The Delaware Court of Chancery's 2018 decision in Akorn, Inc. v. Fresenius Kabi AG remains the leading case on MAC standards in a pharmaceutical context. The court found that for a MAC to be validly invoked, the adverse change must be durationally significant — persistent over time and showing no sign of abating — not merely a short-term disruption.

Crucially, the court observed that pandemic events, earthquakes, and other systematic risks are ordinarily allocated to the acquirer through MAC carve-outs precisely because they are beyond the control of all parties.

Are These Clauses Present in Royalty Purchase Agreements?

The short answer is: force majeure almost universally, MAC provisions rarely and specifically.

Pharmaceutical royalty purchase agreements (RPAs) are long-term, complex instruments that routinely run to forty or fifty pages of operative provisions before the schedules. They are typically governed by New York or Delaware law and negotiated between sophisticated institutional parties with significant legal resources on both sides.

Force majeure clauses are standard boilerplate in virtually every RPA. Their function, however, is narrowly defined: they protect a party's obligation to report and remit royalty payments when an external event makes that procedural obligation temporarily impossible. A government-ordered lockdown that closes a company's finance office, a cyberattack that disables its payment systems, or a natural disaster that physically prevents operations from functioning — these are the intended use cases.

The underlying royalty stream, the product's net sales, and the commercial success of the drug itself are not protected by the force majeure provision.

MAC provisions appear in RPAs with more specificity and less frequency. Where they exist, they are typically investor-protective provisions tied to discrete, catastrophic events rather than general commercial deterioration.

The standard triggers in well-drafted royalty agreements include regulatory withdrawal or suspension of the product's marketing authorisation, product recall, invalidation of core underlying intellectual property, or a contractually-defined decline in annual net sales measured against a trailing-period baseline — often 30–50% below a reference period for two or more consecutive years.

What you will not find in a well-drafted RPA is a MAC provision that allows the royalty investor to exit because drug sales fell during a pandemic. That risk is precisely what the investor purchases. It is the definition of the asset class.

What COVID-19 Actually Revealed

The pandemic stress-tested royalty agreement drafting in ways that will inform the asset class for a generation. The results were instructive.

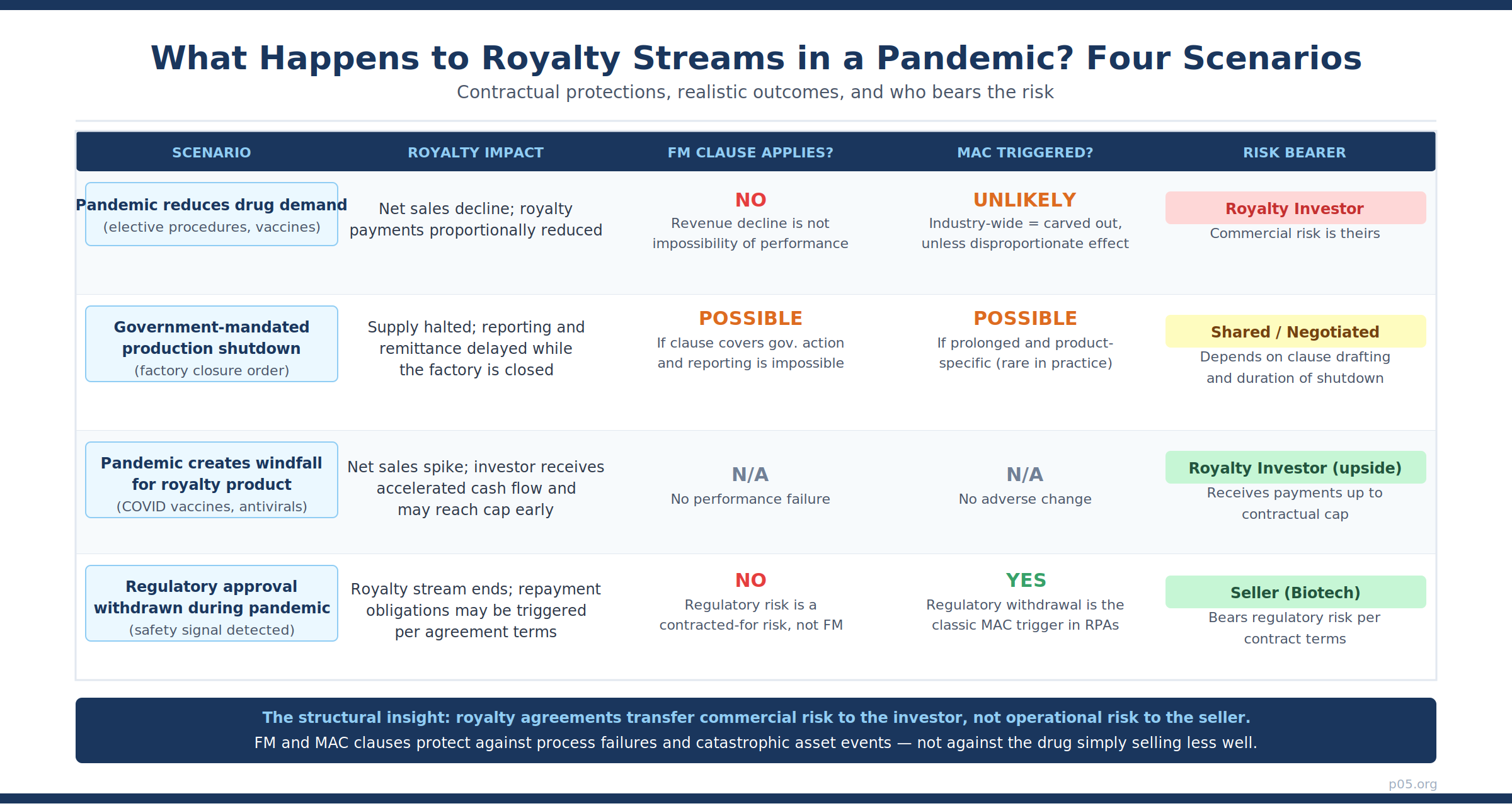

Force majeure was technically invoked in related contracts but not in royalty instruments. Pharmaceutical supply agreements, clinical trial service agreements, and manufacturing contracts all saw force majeure invocations as factories closed and clinical operations halted. These clauses are written to address performance obligations — deliver the product, conduct the study, manufacture the batch. Royalty agreements do not have those performance obligations.

The seller's obligation is to pay the investor a percentage of net sales. If there are no net sales, there is nothing to remit, and no force majeure clause is needed to excuse non-payment.

Pandemic carve-outs in MAC definitions were tested but held firm. As the Hogan Lovells analysis of COVID-19 contractual implications documented, MAC clauses in M&A and financing agreements almost universally excluded pandemic effects as a qualifying MAC event, because such effects are industry-wide systematic risks.

Delaware's AB Stable VIII LLC v. Maps Hotels and Resorts One LLC (2020) confirmed this in the M&A context: pandemic-related declines did not qualify as a MAC because the agreement explicitly carved out broadly applicable calamities. Courts have shown very little appetite for voiding long-term agreements based on pandemic disruption.

The gap everyone missed was in the FM clause list. As the Stanford Law Review noted after the first wave of COVID-19 litigation, the term "pandemic" was almost entirely absent from force majeure clauses drafted prior to the outbreak. When pharmaceutical sector lawyers reviewed their existing royalty agreements in 2020, they discovered that most FM provisions listed earthquakes, hurricanes, wars, and acts of government — but not pandemics or epidemics specifically.

This created uncertainty about whether government-ordered shutdowns that prevented reporting or remittance obligations could be excused under the general sweeper language, even if not by the specific enumerated events.

In practice, no major pharmaceutical royalty fund invoked force majeure against a seller, and no seller invoked force majeure to avoid remittance obligations during the pandemic. The legal machinery was simply not implicated at the level of royalty payment obligations.

How Drafting Has Changed Since 2021

The post-pandemic market has made two material changes to standard RPA boilerplate.

First, explicit pandemic language is now standard in force majeure clauses. New royalty agreements executed since 2021 routinely enumerate "epidemic, pandemic, or public health emergency declared by a national or supranational governmental authority" as a qualifying force majeure event.

The American Bar Association's guidance and multiple major law firm advisories, including from WilmerHale and Baker McKenzie, recommended this drafting update. The change has practical significance primarily for procedural obligations — reporting timelines, audit cooperation, annual reconciliation certifications — rather than for the payment obligation itself.

Second, MAC carve-outs are now drafted with greater precision. The International Bar Association's 2025 analysis of MAC clause evolution documented the increasing precision of pandemic and public health carve-outs, which now routinely include explicit references to government responses, quarantine orders, and travel restrictions as excluded systematic risks — alongside the traditional carve-outs for general economic conditions, changes in capital markets, and industry-wide developments.

The disproportionate-effect exception deserves particular attention in royalty contexts. Standard MAC carve-outs exclude industry-wide effects unless they disproportionately affect the specific asset relative to comparable products in the same therapeutic area.

For a royalty on a product with a narrow patient population — say, an orphan disease indication — a pandemic that eliminates patient access to specialty clinics might qualify as a MAC-triggering event even where the broad pandemic carve-out would otherwise exclude the claim. This is a genuinely open area where the drafting has not been tested in litigation.

The Structural Reason Royalty Investors Are Not Exposed

There is a deeper reason why force majeure and MAC provisions are relatively peripheral to pharmaceutical royalty investing, and it goes to the fundamental structure of the asset class.

A pharmaceutical royalty is, at its core, a purchase of commercial exposure to a specific drug's net sales. The royalty investor deploys capital today in exchange for a percentage of future revenues, subject to a cap or term. The investor's return depends entirely on how well the drug sells. It does not depend on whether the seller performs a set of obligations — it depends on whether patients buy the medicine.

This structure means that the investor and the seller share the same commercial risk, but from different positions. Neither can invoke force majeure to alter the economics of a bad drug or a declining market.

The Covington & Burling overview of royalty financing structures confirms that royalty monetisations sit at the lowest-risk end of the life sciences financing spectrum precisely because the investor's return is tied to product performance rather than the counterparty's balance sheet. In a pandemic, if the drug sells less, the investor receives less. That is not a force majeure event — it is the deal.

What force majeure and MAC clauses protect against in a royalty agreement context is a different category of risk: the failure of the institutional framework that enables the commercial transaction to continue.

The FM clause covers the scenario where a government-ordered shutdown prevents the licensee from manufacturing and reporting, making remittance physically impossible for a defined period. The MAC provision covers the catastrophic scenario where the regulatory basis for the product is withdrawn, the intellectual property is invalidated, or the product is recalled and cannot legally be sold. Both scenarios are genuine risks that require contractual allocation. Neither describes pandemic-driven revenue volatility.

Realistic Scenarios for Future Invocation

With that structural context established, the question of what could realistically happen in the next pandemic or systemic disruption becomes more tractable.

Scenario 1: Pandemic-driven supply disruption. A future pandemic causes a government to mandate factory closures affecting the manufacturing of a royalty-bearing product. The product cannot be shipped for six months. In this scenario, a well-drafted post-2021 FM clause would likely excuse the seller's reporting and remittance obligations for the duration of the closure — but only those obligations. There would be no royalty payments to remit because there are no sales; the FM clause is technically vacuous in its application but provides procedural comfort.

Scenario 2: Regulatory emergency action. A health authority issues an emergency suspension of a product's marketing authorisation in response to a pandemic-era safety signal — perhaps an adverse interaction with a widely distributed emergency treatment.

Depending on the RPA's MAC drafting, this regulatory suspension could constitute a triggering event if: (a) the agreement defines loss of regulatory authorisation as a MAC event; (b) the suspension is not expressly carved out as a regulatory change caused by an industry-wide event; and (c) the suspension persists beyond any cure or re-evaluation period in the agreement. This is the most realistic scenario in which an investor might actually exercise a MAC-based right, because the underlying asset — the right to receive royalties on a legally saleable drug — has been impaired.

Scenario 3: Pandemic creates windfall, then regulatory backlash. A product enjoys pandemic-driven revenue spikes — the Shingrix and COVID vaccine experience — then faces regulatory or pricing pressure as public health emergency conditions recede. The investor receives accelerated cap attainment during the boom and either receives nothing further or, if uncapped, continues to receive payments at normal rates. No FM or MAC provision is implicated by the revenue trajectory, up or down.

Scenario 4: Compulsory licensing. A government invokes its TRIPS Article 31 rights to issue a compulsory licence for a royalty-bearing product, permitting generic manufacturing at reduced or zero royalty rates. This is the most legally contested future scenario, particularly given the ongoing evolution of pandemic preparedness frameworks including the 2025 WHO Pandemic Agreement.

Compulsory licensing typically constitutes a government action that triggers FM relief for the affected royalty obligation — but only for the duration and scope of the compulsory licence. More importantly, it raises the question of whether the MAC trigger for governmental action extinguishing rights applies, given that compulsory licensing is an exercise of sovereign authority rather than a private contractual failure. The answer is jurisdiction-specific and has not been definitively litigated in the context of pharmaceutical royalty monetisation.

The MAC Nobody Is Talking About: IRA Drug Pricing

If force majeure is a theoretical concern and pandemic MAC is a structural impossibility for revenue-driven reasons, there is a different type of MAC risk that deserves more attention from the royalty market in 2026: the impact of the Inflation Reduction Act's Medicare drug price negotiation programme.

For products in the Royalty Pharma portfolio and peer funds' holdings, the first cohort of negotiated prices took effect on 1 January 2026. The programme sets Maximum Fair Prices well below existing Medicare reimbursement rates — the first ten products saw price reductions averaging in the range of 38–79%.

The IRA negotiation mechanism was not expressly contemplated by most royalty agreements executed before 2022, and the resulting price compression is not a pandemic or force majeure event. It is a regulatory change to pricing — exactly the type of systematic risk that MAC carve-outs typically exclude.

This is precisely where the disproportionate-effect exception becomes commercially significant. If a product's IRA negotiated price reduces net sales in the Medicare channel by 60%, and that product happens to be predominantly used by Medicare-eligible patients — as is the case for Janssen's Stelara or Merck's Januvia — the price reduction is industry-wide in form but disproportionate in effect on that specific royalty asset. Whether that disproportionate effect is sufficient to trigger a MAC is an open drafting question that royalty market participants should address proactively in new transactions.

What This Means for Deal Structuring in 2026

The Gibson Dunn Royalty Report documented $29.4 billion in life sciences royalty financings from 2020 to 2024. The overwhelming majority of those transactions were structured as pure royalty monetisations with no equity component and with MAC provisions, where present at all, tied to regulatory and IP events rather than commercial performance.

That structuring reflects a coherent risk allocation: the investor accepts commercial risk in exchange for the royalty return; contractual protections address the categorical risks that would eliminate the legal right to receive a royalty at all.

For parties negotiating new royalty agreements in 2026, the practical checklist should address several areas that have become more contested since the pandemic:

The FM clause should enumerate "epidemic, pandemic, or public health emergency declared by the WHO or a national government authority" as a qualifying event, covering both procedural obligations and, where relevant, manufacturing obligations under development-stage royalty financing structures.

The mitigation obligation — requiring the non-performing party to take all reasonable steps to resume performance — should include specific reference to accessing alternative manufacturing facilities and government-licensed supply channels.

The MAC definition should address the disproportionate-effect exception explicitly in the context of both pandemics and government pricing interventions. For products with concentrated payer exposure — particularly US Medicare or Medicaid — this means defining the reference market and the relevant comparator set with precision rather than relying on boilerplate carve-out language.

For synthetic royalty structures or development-stage transactions where the royalty investor is also providing capital for clinical development, the FM and MAC provisions should address the scenario of clinical trial interruption by government public health order. Trial delays caused by pandemic-related site closures are now a documented risk, and the agreement should allocate that risk explicitly rather than leaving it to the general FM analysis.

Finally, both parties should review the interaction between FM provisions and the typical cure period structure. If a FM event persists beyond 90 or 180 days, many agreements permit termination or conversion to an alternative compensation structure. For a royalty on a product with a long anticipated commercialisation period, that termination right needs careful drafting to distinguish a temporary operational disruption from a permanent impairment of the underlying asset.

Conclusion

Force majeure and MAC provisions are present in pharmaceutical royalty agreements, and they matter — but not in the way most commentators assume when they raise the pandemic question. They do not protect royalty investors against pandemic-driven revenue declines. They protect the institutional infrastructure of the transaction: the obligation to report, remit, and maintain the legal basis for the royalty itself.

COVID-19 demonstrated that the commercial risk of a pharmaceutical royalty — the risk that a product sells more or less than projected — sits entirely with the investor. No FM or MAC clause was designed to, or did, transfer that risk back to the seller.

What the pandemic accelerated was a drafting evolution: explicit pandemic language now appears in FM clauses, MAC carve-outs are drafted with greater precision around systematic risks and the disproportionate-effect exception, and parties are more attentive to the interaction between force majeure provisions and their underlying risk allocation.

The more significant near-term risk in 2026 is not another pandemic. It is the continued implementation of drug price negotiation under the IRA and its interaction with royalty agreement MAC provisions. That question sits in the space between the systematic risk carve-out and the disproportionate-effect exception — and it is not yet resolved.

All information in this report was accurate as of the research date and is derived from publicly available sources including judicial decisions, law firm publications, regulatory filings, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. Sebastian Gensior is not a lawyer or financial adviser.

Member discussion