Fund of the Week: Blue Owl Capital's Life Sciences Platform

Overview: The Platform and Its Vehicles

Blue Owl Capital Inc. (NYSE: OWL) is one of America's largest alternative asset managers, with $157.8 billion in credit platform assets under management as of December 31, 2025. The firm was created through the 2020 combination of private lender Owl Rock and Dyal Capital, a specialist in acquiring stakes in other private capital firms.

Blue Owl's credit business operates through a constellation of business development companies (BDCs), special purpose vehicles (SPVs), and fund structures targeting different investor types and asset classes. Healthcare is the platform's second-largest sector, and a dedicated life sciences team within the Credit platform has deployed over $2.5 billion across nine disclosed transactions since late 2023.

This analysis examines the fund architecture, credit ratings, financing mechanics, and performance of Blue Owl's vehicles, before reconstructing the life sciences royalty portfolio from SEC filings and assessing what the ongoing private credit crisis means for the platform.

The BDC Complex: Structure, Ratings, and Performance

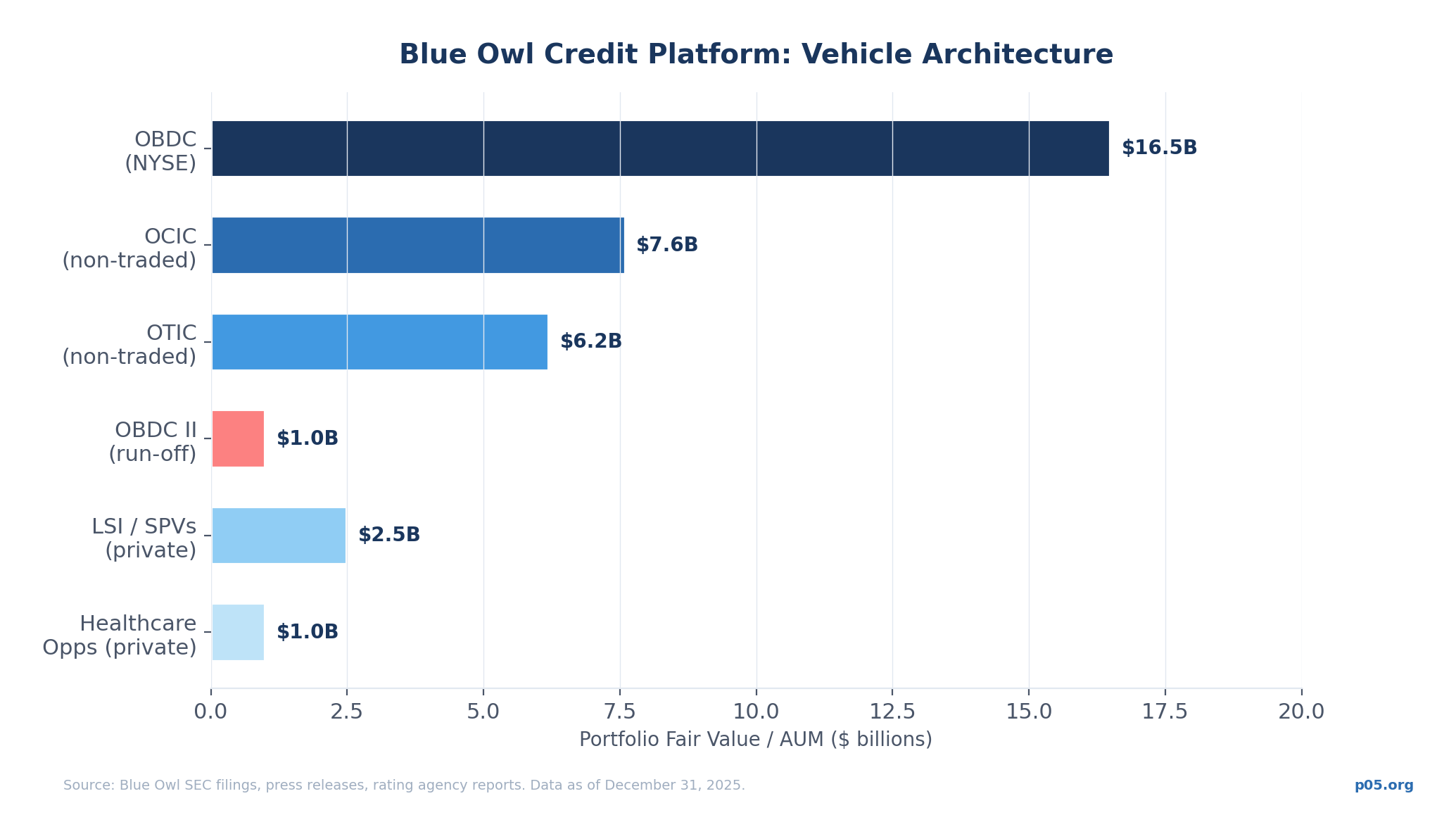

Blue Owl runs its credit business through six BDCs and one interval fund, each designed for a different investor channel and strategy. The key vehicles are:

| Vehicle | Ticker / Status | Type | Portfolio (FV, 31 Dec 2025) | Strategy |

|---|---|---|---|---|

| Blue Owl Capital Corp. | NYSE: OBDC | Publicly traded BDC | $16.5B (234 companies) | Diversified direct lending |

| Blue Owl Capital Corp. II | OBDC II (non-traded) | Non-traded BDC (run-off) | ~$1.0B post-sale (183 companies pre-sale) | Legacy feeder / run-off |

| Blue Owl Credit Income Corp. | OCIC (non-traded) | Perpetual non-traded BDC | ~$7.6B capacity | Diversified direct lending |

| Blue Owl Technology Finance | NYSE: OTF | Publicly traded BDC | Not separately disclosed | Technology lending |

| Blue Owl Technology Income | OTIC (non-traded) | Perpetual non-traded BDC | $6.2B (190 companies) | Technology lending |

| LSI Financing LLC / SPVs | Private | Dedicated life sciences SPVs | ~$2.5B+ committed | Life sciences credit & royalty |

| Blue Owl Healthcare Opps | Private | Private fund | ~$1B AUM | Mid-to-late stage biopharma equity |

Moody's upgraded the senior unsecured ratings of both OBDC and OCIC to Baa2 (stable outlook) on January 22, 2026, placing them among a small group of similarly rated BDCs. Moody's cited net loss rates well below middle-market lending norms: OBDC recorded average annual realised net losses of just 27 basis points since inception in 2016, while OCIC and the broader platform posted a 7 basis point average.

S&P Global Ratings issued a separate report on OBDC II affirming stable credit fundamentals and stating it fully expects OBDC II to repay its upcoming $350 million unsecured debt maturity in November 2026. KBRA analysed the OBDC II loan sale tranche and confirmed the 92% senior secured first-lien composition.

| BDC | Avg. Annual Net Loss Rate (inception–2025) |

|---|---|

| OBDC | -0.29% |

| OBDC II | -0.27% |

| OCIC | -0.14% |

| OTF | +0.23% |

| OTIC | +0.03% |

| FLF | -0.45% |

| OLF | -0.08% |

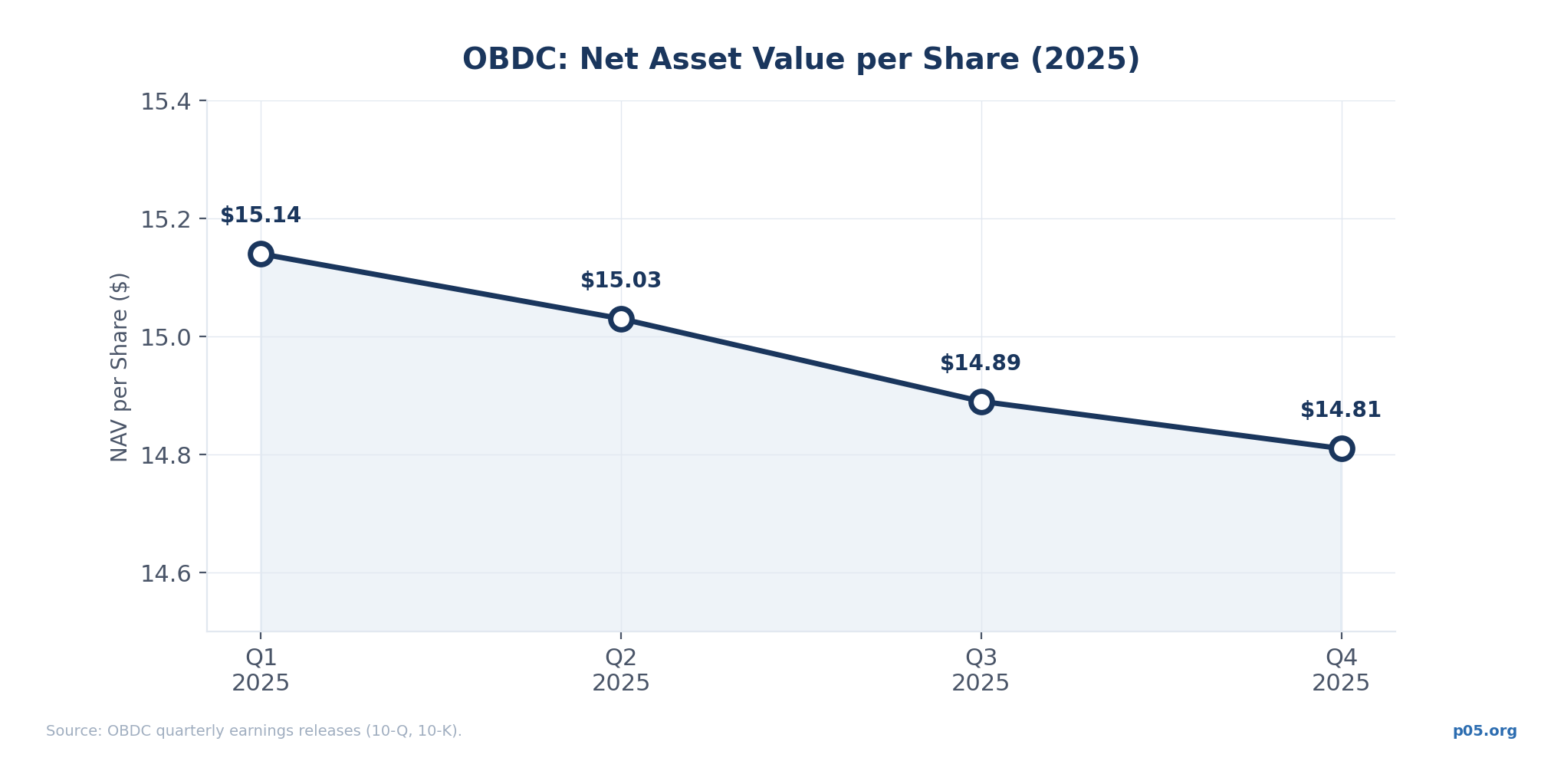

OBDC Performance (Q4 2025)

OBDC, the publicly traded flagship, reported the following for Q4 2025:

| Metric | Q4 2025 | Q3 2025 |

|---|---|---|

| Adjusted NII per share | $0.36 | $0.36 |

| NAV per share | $14.81 | $14.89 |

| Annualised dividend yield | 10.0% | 9.9% |

| Non-accrual (at cost) | 2.3% | 2.7% |

| Non-accrual (at fair value) | 1.1% | 1.3% |

| Net leverage | 1.19× | 1.22× |

| Portfolio companies | 234 | 238 |

| Portfolio fair value | $16.5B | $17.1B |

| Borrower revenue growth | +8% | — |

| Borrower EBITDA growth | +11% | — |

ROE for the quarter was 9.7%. The board declared a Q1 2026 dividend of $0.37 per share. OBDC repurchased approximately $148 million of common stock at 86% of book value during Q4, the largest quarterly buyback in the company's history, and authorised a new $300 million repurchase programme.

Blue Owl's BDCs fund their lending through a layered capital structure of secured bank facilities, CLOs (collateralised loan obligations), unsecured senior notes, and equity.

Secured facilities. OBDC maintained $3.0 billion in cash and undrawn committed capacity through secured bank lines as of the Moody's upgrade. OCIC maintained $7.6 billion. Secured debt represented roughly 26% of OBDC's assets and 23% of OCIC's.

CLOs and securitisations. Blue Owl issues CLOs backed by portfolios of its direct lending assets, providing term-matched, non-recourse funding at lower cost than revolving facilities. The platform's CLO management capability spans broadly syndicated leveraged loans as well as proprietary middle-market CLOs.

Unsecured senior notes. OBDC faces a $1.0 billion senior note maturity in July 2026, which Moody's noted the company has adequate liquidity to meet. OBDC II has a $350 million unsecured maturity due November 2026. The BDC sector more broadly faces a "maturity wall" of over $12 billion in unsecured debt coming due across the industry in 2026, forcing many managers to prioritise refinancing over new origination.

Equity and leverage. OBDC operated at 1.19× net debt-to-equity as of Q4 2025, within its stated target range of 0.9×–1.25×. OCIC maintained 0.80×. Maximum regulatory leverage for standard BDCs is 2.0×; OBDC II operates under a 1.0× cap.

The Private Credit Crisis: What Happened

The events of February 2026 have become a stress test for the $2 trillion private credit industry, with Blue Owl at the centre of the narrative.

The OBDC II Unwind

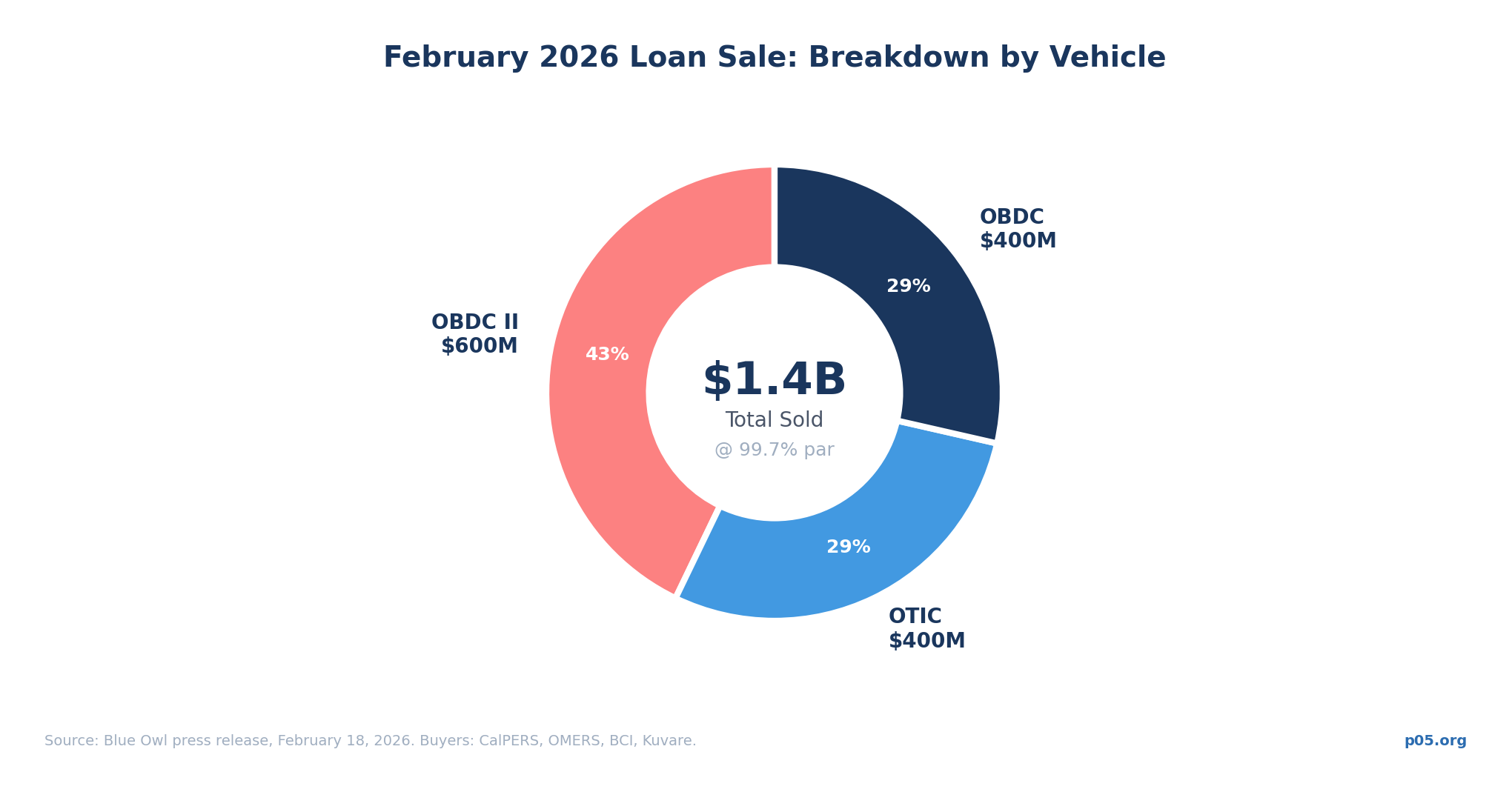

On February 19, 2026, Blue Owl permanently halted quarterly redemptions at OBDC II, its $1.6 billion non-traded BDC, replacing them with return-of-capital distributions. The fund had operated for eight years under a "semi-liquid" model offering quarterly tender offers of up to 5% of outstanding shares. When redemption requests exceeded the quarterly cap across multiple vehicles, management concluded the structure was unsustainable.

To fund an accelerated return of capital, Blue Owl executed a $1.4 billion secondary loan sale across three vehicles:

| Vehicle | Loans Sold | Purpose |

|---|---|---|

| OBDC II | ~$600M (~34% of portfolio) | Fund $2.35/share return-of-capital distribution (~30% of NAV) |

| OTIC | ~$400M | Pay down debt, increase flexibility |

| OBDC | ~$400M (74 companies, 24 industries) | Pay down debt, increase diversification |

The assets were sold to four North American pension and insurance investors — CalPERS, OMERS, BCI, and insurer Kuvare — at 99.7% of par value. Management stated this was consistent with the firm's internal marks. The sold portfolio comprised 128 companies across 27 industries, with an average investment size of $5 million per position, 97% senior secured, and the largest industry concentration (13%) in internet software and services.

OBDC II's credit agreement was amended on February 17, 2026: revolving commitment slashed from $225 million to $75 million, availability period shortened to October 2027, and the unused commitment fee increased to 0.50–0.65% from 0.375%. The fund's dividend reinvestment plan was terminated; all future distributions will be in cash.

The Failed Merger

The OBDC II crisis has an 18-month backstory. In November 2025, Blue Owl announced a definitive merger agreement to fold OBDC II into the publicly traded OBDC, with OBDC as the surviving entity. The deal was terminated after investor backlash: OBDC II investors argued they would be forced to accept roughly 20% losses because OBDC traded at a discount to NAV. The failed merger left OBDC II without a path to public market liquidity.

Market Response

OWL shares fell from a January 2025 high of $25.02 to approximately $11.22 by late February 2026 — a decline of roughly 55%. Saba Capital and Cox Capital Partners launched tender offers for shares of OBDC II, OTIC, and OCIC at 20–35% discounts to NAV. Saba Capital's founder publicly warned of the "wheels coming off" private credit at the iConnections conference.

Deutsche Bank downgraded the stock. UBS cut its price target three times in two months, from $18 to $16.50 to $12. Other analysts — Barclays, Goldman Sachs, Wolfe Research, Oppenheimer — trimmed targets but maintained Neutral or positive ratings, noting that OBDC II represents a small portion of Blue Owl's roughly $307 billion total AUM.

The Broader Private Credit Context

Blue Owl's difficulties are not occurring in isolation. The private credit market, which has ballooned past $2 trillion in global assets, is facing several concurrent stresses:

The SaaS devaluation narrative. Fears that AI-driven products will undermine software-as-a-service business models — a core segment for many BDC portfolios — have depressed sentiment. OBDC's technology exposure is approximately 16%, while OTIC invests at least 80% in software and technology.

Rising PIK (payment-in-kind) income. Across the BDC sector, PIK interest — where borrowers pay interest with more debt rather than cash — has risen to represent approximately 8% of total investment income for some public BDCs. Blue Owl reported that 90% of its PIK positions were underwritten that way at inception and the firm has never taken a principal loss on those positions.

The retailisation problem. Morningstar noted that ending quarterly redemptions at OBDC II "highlights the potential mismatch that exists between illiquid assets and semiliquid funds." Moody's February 2026 Outlook warned that as retail investor participation in private credit grows, "funds will need to hold a larger proportion of more liquid and lower-yielding investments," potentially dragging returns.

Maturity wall. Over $12 billion in unsecured BDC debt matures across the industry in 2026, forcing refinancing into an uncertain market.

Where the Life Sciences Assets Live — And Why They're Different

A point that has received limited attention in the market commentary is the structural separation. The BDC crisis is a crisis of fund wrappers, not underlying asset quality across the entire platform. The life sciences portfolio sits in a completely different structural container.

The SPV Architecture

Blue Owl's life sciences royalty and credit investments are originated and held through dedicated SPVs — special purpose vehicles that are legally separate from the BDC fund structures:

| SPV / Vehicle | Assets Held | Legal Domicile |

|---|---|---|

| LSI Financing 1 DAC | BridgeBio global acoramidis royalty | Ireland |

| Acoramidis Royalty SPV, LP | BEYONTTRA European royalty | Delaware |

| LSI Financing Fund, LP | BEYONTTRA European royalty | Delaware |

| XRL 1 LLC | XOMA/VABYSMO royalty-backed loan | Delaware |

| LSI Financing LLC | ITM Isotope term loan | Delaware |

| Blue Owl Healthcare Opportunities | Cowen Healthcare equity funds (~$1B AUM) | — |

The structural separation is relevant to understanding the BDC crisis. There is no mechanism for retail investors to "redeem" out of a bilateral royalty purchase agreement with BridgeBio or a non-recourse loan to a XOMA SPV. These are long-duration, contractual cash flow arrangements tied to pharmaceutical sales revenue.

The BDC direct lending positions — such as the TG Therapeutics and Madrigal Pharmaceuticals term loans — may be held partially within OBDC alongside hundreds of other credits. These are senior secured first-lien positions, consistent with the composition of assets that were sold at 99.7% of par in the February transaction.

Were Any Life Sciences Assets Sold?

The royalty assets — held in dedicated SPVs outside the BDC structures — were not included in the $1.4 billion sale, based on the disclosed composition of the sold portfolio and the structural separation of the SPV vehicles. Bilateral contractual arrangements held in separate legal entities cannot be liquidated through a BDC portfolio strip sale process.

On the Q4 2025 earnings call, Blue Owl's CEO confirmed that OBDC holds 45 healthcare investments totalling $2.5 billion — a statement made after the $1.4 billion sale was announced. Some small healthcare direct lending positions were likely trimmed as part of the 74-company strip (average position size: $5 million), but these would represent small fractions of a $2.5 billion healthcare book.

The Life Sciences Royalty Portfolio: Deal by Deal

Blue Owl's life sciences platform has assembled a portfolio across nine disclosed transactions, using three distinct structural approaches: outright royalty purchases, royalty-backed lending, and senior secured direct lending to commercial-stage biopharma.

| Deal | Drug / Asset | Structure | Committed Capital | Cap / Terms | Co-Investors | Drug Revenue (latest) |

|---|---|---|---|---|---|---|

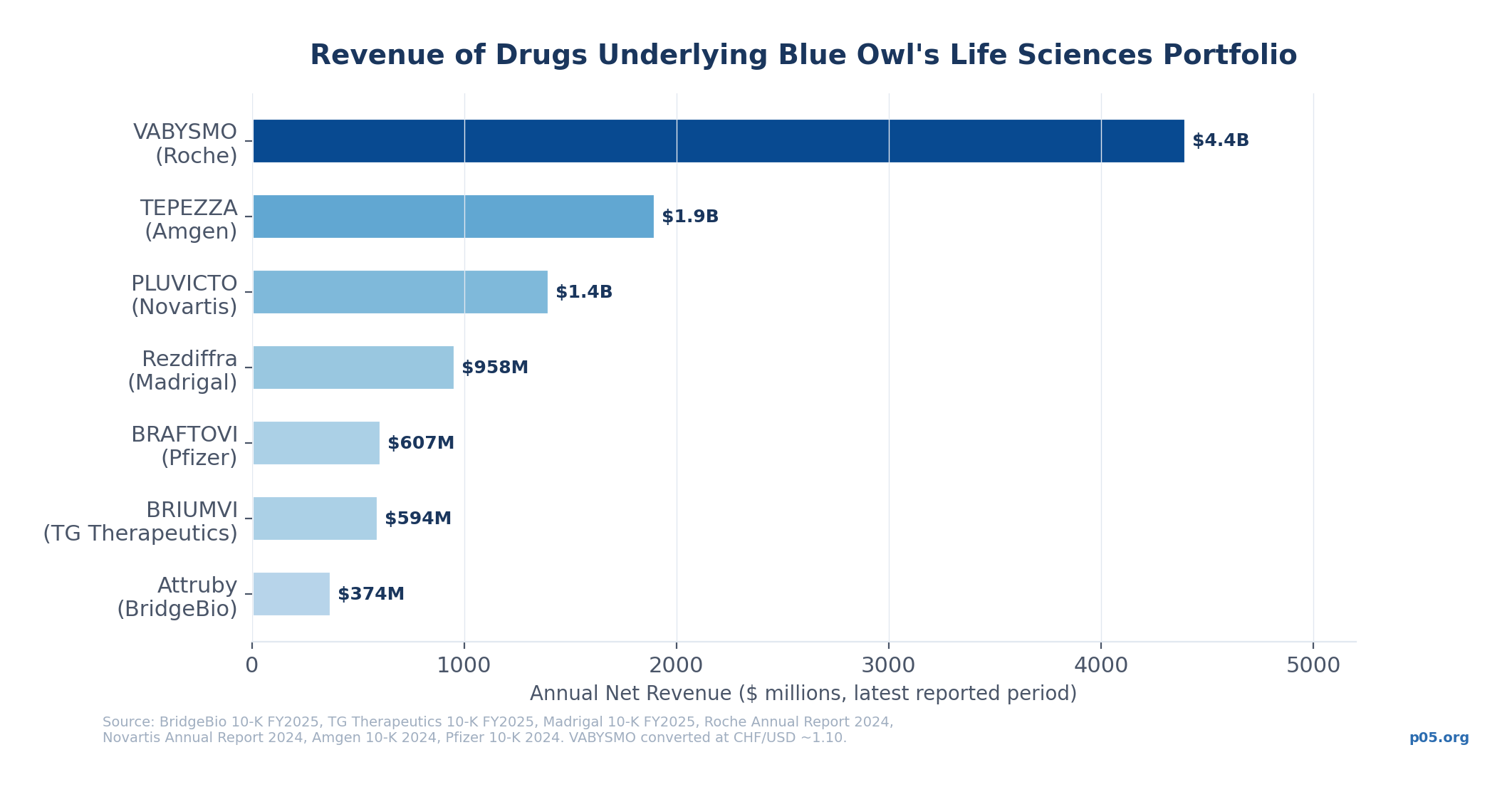

| BridgeBio I | Attruby (ATTR-CM) | 5% royalty, capped 1.9× | $500M ($300M Blue Owl) | Cap: $950M | CPP Investments (40%) | $362M U.S. FY25 + $11.4M EU/Japan |

| BridgeBio II | Corporate credit | SOFR + 650 bps, 5yr | $450M | Repaid Feb 2025 | — | N/A (repaid) |

| BridgeBio III | BEYONTTRA (EU royalty) | 60% of EU royalties, capped 1.45× | $300M | Cap: $435M | HealthCare Royalty | $5.3M Q4 2025 (early ramp) |

| XOMA | VABYSMO (retinal) | Royalty-backed loan, 9.875% fixed | $140M (15yr) | Non-recourse to XOMA | — | CHF 4B+ (Roche global, 2024) |

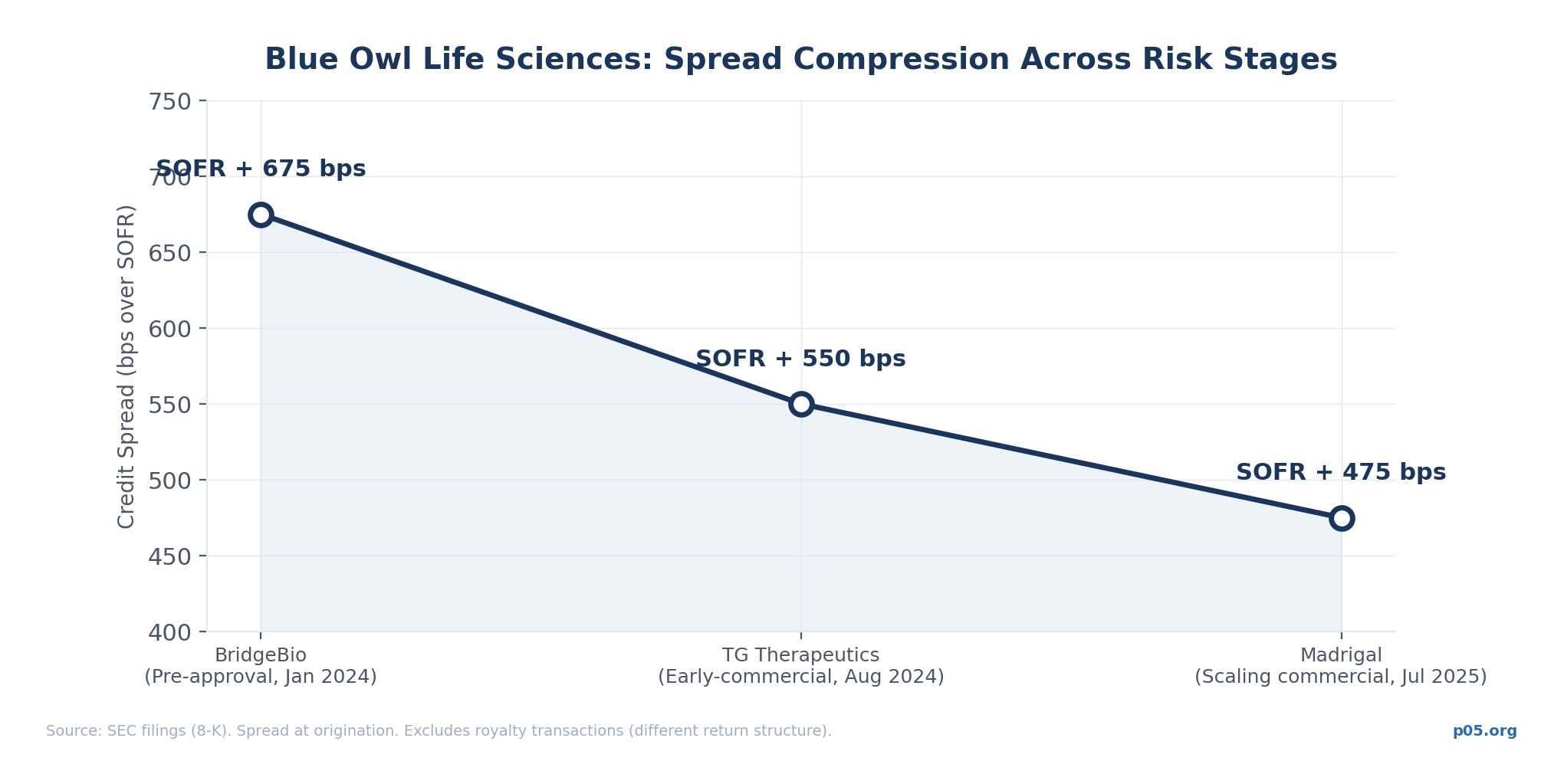

| TG Therapeutics | BRIUMVI (MS) | SOFR + 550 bps | $250M ($125M each) | 5yr, interest-only to Jun 2028 | HealthCare Royalty (50%) | $594M U.S. FY25 |

| Madrigal | Rezdiffra (MASH) | SOFR + 475 bps | $500M (sole lender) | 5yr + $250M accordion | — | $958M FY25 |

| Purdue/PRF | PLUVICTO (prostate cancer) | Royalty purchase | $100M+ | Undisclosed cap | — | $1.4B (Novartis, 2024) |

| Horizon/Amgen | TEPEZZA (TED) | Economic interest | Undisclosed | 3% on sales >$300M | — | $1.9B (Amgen, 2024) |

| NMS/Pfizer | BRAFTOVI (CRC) | Capped royalty | $50M+ | Undisclosed cap | — | $607M (2024) |

| ITM Isotope | ITM-11 (NET) | Term loan | $262.5M ($140M funded) | Pre-NDA filing | — | Pre-revenue |

The Refinancing Pattern

A distinctive feature of Blue Owl's direct lending approach is the systematic refinancing of Hercules Capital venture debt. Both TG Therapeutics and Madrigal used Blue Owl proceeds to retire Hercules facilities, positioning Blue Owl as the natural "graduation" lender as biotechs transition from venture-stage to commercial-stage financing.

The spread compression across the portfolio reflects this risk graduation: SOFR + 675 bps (pre-approval BridgeBio) → SOFR + 550 bps (early-commercial TG) → SOFR + 475 bps (rapidly scaling Madrigal). Blue Owl prices risk on a drug's revenue trajectory, not biotech sector sentiment.

How the Royalties Are Structured

Blue Owl's royalty approach differs markedly from Royalty Pharma (NYSE: RPRX), the sector's largest player:

| Feature | Blue Owl | Royalty Pharma |

|---|---|---|

| Return cap | Explicit (1.45×–1.9×) | Typically uncapped / perpetual |

| Credit component | Often paired with senior secured loan | Pure royalty buyer |

| Fund structure | Private SPVs within credit platform | Publicly traded permanent capital |

| Target IRR | Low-to-mid teens | High single digits to low teens |

| Upside participation | Capped at multiple | Full blockbuster upside |

| Investor type | Institutional / BDC co-investment | Public equity investors |

The capped structure trades away right-tail blockbuster outcomes for a higher probability of achieving target returns — better suited to credit-oriented fund mandates. The hybrid credit-plus-royalty template (as with BridgeBio's $950 million total financing) provides a one-stop origination wedge that pure-play royalty buyers cannot match without syndication.

Blue Team / Red Team: The Fund-Level Assessment

🔵 Blue Team: Structural Insulation and Performing Assets

SPV structural separation. Based on publicly filed documents, there is no mechanism for BDC investors to trigger redemptions against a bilateral royalty purchase agreement. The life sciences assets are held in dedicated vehicles outside the BDC fund structures.

The underlying drugs are generating revenue. Attruby recorded $362 million in U.S. net revenue in FY2025 (per BridgeBio's 10-K). BRIUMVI grew 92% to $594 million (per TG Therapeutics' filings). Rezdiffra reached $958 million (per Madrigal's filings). VABYSMO exceeded CHF 4 billion (per Roche's annual report). PLUVICTO grew 42% to $1.4 billion (per Novartis). These figures are sourced from each company's public disclosures.

Credit quality indicators. The $1.4 billion loan sale at 99.7% of par — to CalPERS, OMERS, BCI, and Kuvare — provided third-party price discovery on Blue Owl's portfolio marks. OBDC's non-accrual rate stood at 1.1% at fair value, below public market default rates. Moody's upgraded OBDC and OCIC to Baa2 in January 2026.

Historical loss rates. The platform's average annual net loss rate of 7–27 basis points across funds since 2016 is below the Cliffwater Direct Lending Index average, and substantially below high-yield bond or leveraged loan loss rates over the same period.

NIH cuts and origination. As academic institutions face budget cuts from NIH funding reductions, some are reported to be considering monetising pharmaceutical royalties on licensed IP. Blue Owl's management has publicly referenced this as a potential source of new origination.

The BDC crisis is structural, not credit-driven. Cliffwater's February 20, 2026 research note argued that OBDC II's problems stem from an obsolete fund structure (the "BDC 2.0" feeder model), not asset quality deterioration. OBDC II delivered an annualised return of 9.11% from inception through September 2025.

🔴 Red Team: Narrative Contagion and Capital Constraints

Capital allocation is constrained. With OWL shares down 55%, the firm executing over $200 million in corporate buybacks, and managing BDC stabilisation, the capacity to deploy fresh capital into new life sciences transactions could be curtailed. New fund formation requires investor confidence that is currently impaired.

Counterparty perception. Biotech companies choosing royalty financing partners consider long-term platform stability. If the Blue Owl brand becomes associated with corporate distress, potential counterparties may weigh alternatives such as Royalty Pharma ($20.7B market cap), KKR-backed HCRx, or DRI Healthcare. The royalty market is relationship-driven.

The life sciences platform is opaque. Blue Owl does not separately disclose life sciences AUM, fee revenue, or portfolio marks. Healthcare is described only as the "second-largest sector" within Credit. The Q4 2025 earnings call did not specifically address life sciences, with management noting only that "30% of the credit business away from direct lending" encompasses alternative credit, life sciences, and other strategies. For context, the platform has deployed $2.5 billion in under three years without granular public disclosure of this segment.

Talent risk is concentrated. The life sciences platform is run by a relatively small, specialised team within a larger credit organisation. In a corporate environment where the parent stock has declined 55%, talent retention warrants monitoring. Key departures could affect the platform's origination and structuring capabilities.

Fundraising headwinds. Raymond James notes that OBDC II is a small part of the roughly $307 billion total AUM, but reputational spillover may affect fundraising across channels. If the life sciences platform cannot raise new capital because of corporate overhang, the parent loses a fee stream regardless of existing portfolio performance.

Retail channel dependency. Moody's warns that the deeper the ties between private credit funds, retail wealth channels, and insurers, the greater the systemic risk from valuation opacity. Blue Owl's wealth channel is its primary fundraising engine. Rebuilding retail investor confidence, if damaged, typically takes time.

Rate and spread compression pressures NII. Weighted average loan spreads compressed by approximately 30 basis points during 2025. Lower base rates and tighter spreads could pressure the dividend across all BDCs, including any life sciences co-investment capacity funded through the platforms.

Capital Reallocation Scenario

If conventional direct lending fundraising is impaired, the firm may redirect organisational focus toward life sciences. The segment carries wider spreads (475–675 bps on credit, plus royalty economics, versus 400–600 bps on standard direct lending) and requires specialised domain expertise that limits competition. Whether corporate-level pressures offset any such reallocation is an open question.

What the Filings Signal

Positive Indicators

Moody's upgrade to Baa2 (January 2026). Non-accrual rate at 1.1% at fair value (Q4 2025). Loan sale executed at 99.7% of par to four institutional investors. Life sciences deal activity continued through H2 2025 with three new transactions (BEYONTTRA, ITM, Madrigal). BridgeBio credit facility fully repaid without loss. BRIUMVI and Rezdiffra revenue trajectories above initial guidance. Portfolio company revenue and EBITDA growing 8% and 11% respectively (per management). $4 billion in total liquidity.

Risk Indicators

OBDC II credit facility reduced from $225M to $75M (February 2026 amendment). Non-accruals estimated at approximately 15% of OBDC II's remaining portfolio post-sale. Internet software and services at 13% of sold loans. Failed OBDC/OBDC II merger (terminated November 2025). Saba/Cox activist tender offers at 20–35% NAV discounts. NAV per share declining from $15.26 (Q4 2024) to $14.81 (Q4 2025). Management noting that lower rates and spread compression may pressure future earnings.

What's Missing

No separate life sciences AUM disclosure. No life sciences fee revenue breakdown. No portfolio-level marks for royalty assets. No discussion of individual royalty performance on earnings calls. Public equity investors assessing OWL currently have limited visibility into the life sciences segment.

What to Watch

Q1 2026 OBDC II distribution execution. The promised $2.35/share distribution (~30% of NAV) is due by March 31, 2026.

New life sciences deal announcements. Continued deployment would indicate the team retains internal support and capital allocation priority.

Key personnel movements. Senior departures from the life sciences team would be a material development for platform continuity.

BridgeBio Attruby trajectory. Q1 2026 U.S. sales and BEYONTTRA European launch data will inform the portfolio's near-term value.

OWL stock price and fundraising capacity. The parent's ability to raise new capital for non-BDC strategies determines the life sciences platform's growth trajectory.

Saba/Cox tender offers. The terms and uptake of activist tender offers for OBDC II, OTIC, and OCIC will indicate the extent of retail investor demand for liquidity.

The life sciences royalty portfolio is held in dedicated SPVs, outside the BDC fund structures that are experiencing redemption pressure. The underlying pharmaceutical assets are generating revenue. The BDC direct lending portfolios sold at par. Credit ratings remain investment-grade. These are the observable data points.

The open questions are at the corporate level: whether Blue Owl can raise new life sciences capital while managing BDC stabilisation, whether counterparties continue to transact with the platform, and whether the organisational infrastructure supporting the life sciences team remains intact through the current period. The answers will emerge in the next two to three quarters.

This article is for informational purposes only and does not constitute investment, financial, or legal advice. The author is not a lawyer, financial adviser, or investment professional. Nothing in this article should be construed as a recommendation to buy, sell, or hold any securities.

All data is sourced from publicly available SEC filings, company press releases, earnings transcripts, rating agency reports, and news sources. The author has made reasonable efforts to ensure accuracy but cannot guarantee the completeness or correctness of all information presented. Readers should conduct their own due diligence and consult qualified professionals before making any investment decisions. The information reflects publicly available, and may be subject to change.

Member discussion