How a 12th-Century Financial Instrument Built a $50 Billion Asset Class

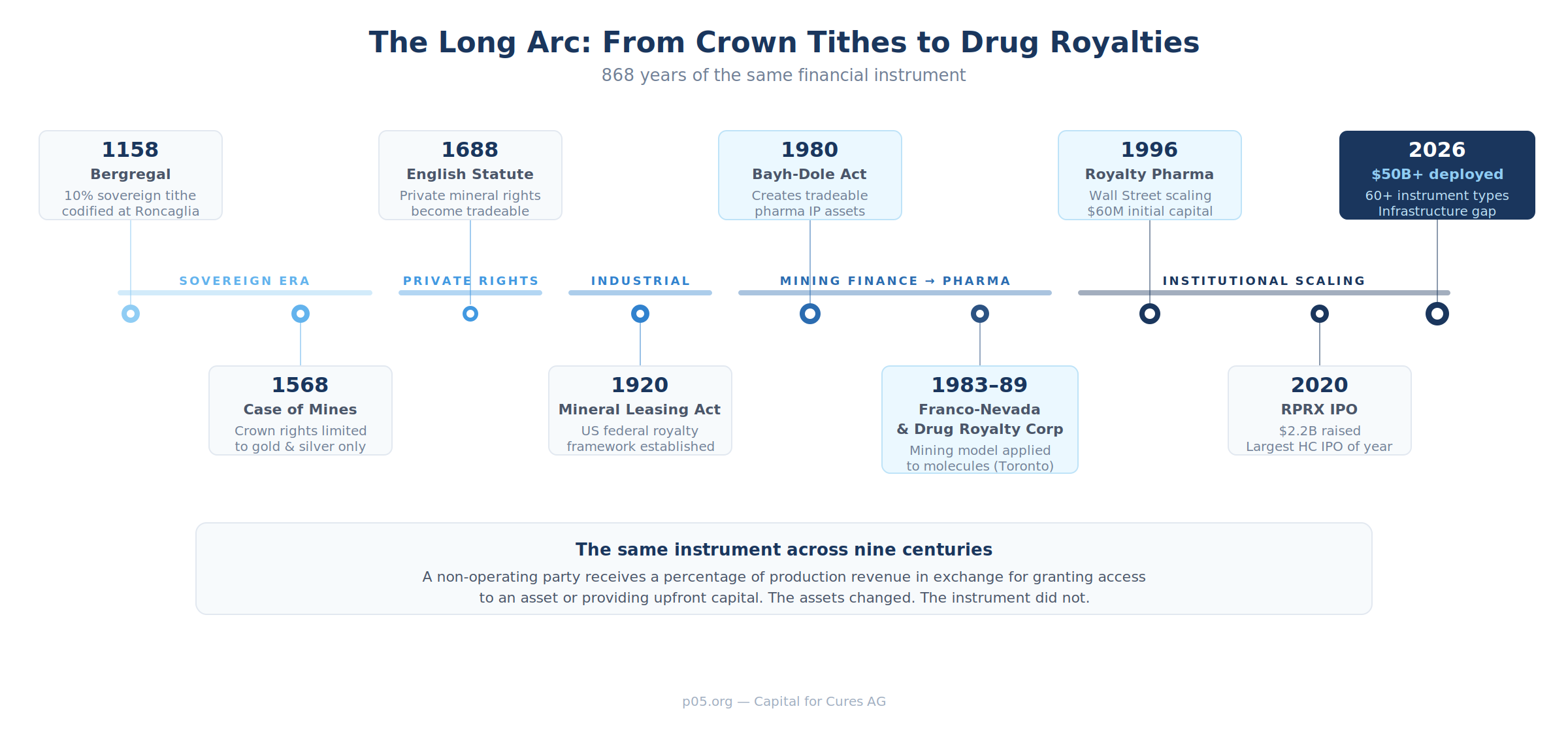

In November 1158, on the plains outside Piacenza, Emperor Frederick Barbarossa convened the Diet of Roncaglia to reassert imperial authority over the wealthy cities of northern Italy.

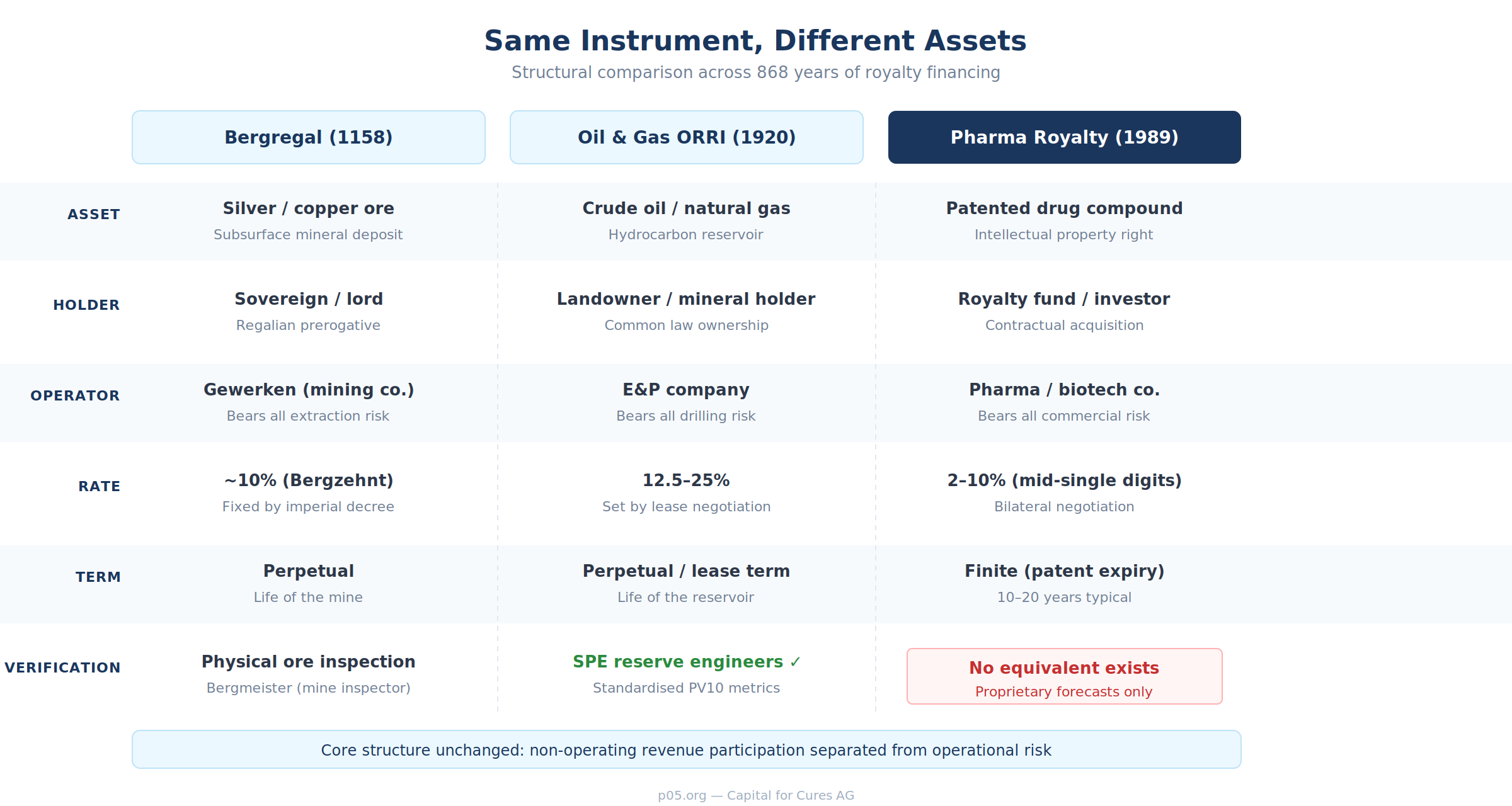

Among the prerogatives he claimed was one that would have seemed entirely unremarkable to his contemporaries but reads, to a modern royalty investor, like a term sheet: the Bergregal, the sovereign's right to a fixed percentage of all mineral production within his territories. The standard rate was ten per cent. No operational involvement. No capital expenditure. Just a share of whatever came out of the ground.

Eight hundred and sixty-eight years later, in a glass tower on the west side of Manhattan, Royalty Pharma collects a percentage of every dollar that Vertex earns from selling cystic fibrosis treatments to American patients. The company has no laboratories, employs no scientists, and runs no clinical trials. It simply owns a contractual right to a slice of revenue from an approved medicine.

The rate is negotiated rather than decreed by an emperor. The asset is a molecule rather than a mine. But strip away the context, and the underlying instrument is almost structurally identical to what Barbarossa codified on the plains of Piacenza.

This is not a loose analogy. The word "royalty" itself betrays the lineage. It derives from the payments owed to the crown — payments that originated in the mines of medieval Europe and travelled, via English common law, American land grants, Texas oil fields, and Toronto's Bay Street, to the laboratories of Cambridge, Massachusetts. Understanding that journey is not merely an exercise in financial archaeology.

It explains why the pharmaceutical royalty market looks the way it does today, why it is concentrated where it is, and what it still lacks.

The Sovereign's Cut

The Bergregal was not an invention of Barbarossa's. It was a codification of something older. From the twelfth century onwards, mineral resources across the Holy Roman Empire were counted among the ruler's regalian rights — sovereign privileges that were supposed to generate revenues. The entitlement took the form of a tithe, the Bergzehnt or Fron: a fixed percentage, usually ten per cent, of the commodity extracted from each pit. The ruler also enjoyed a right of first refusal on production, which in practice amounted to a purchasing monopoly.

This was not a tax in the modern sense. It was a revenue participation interest. The sovereign did not fund the mine. He did not manage it. He simply owned the subsurface rights and granted permission to dig in exchange for a perpetual share of output. The arrangement financed the courts of Saxony and Hanover for centuries.

When production declined, treasuries emptied. The incentive structure was stark: territorial princes invested in the promotion of mining not out of civic duty but because a decline in the mining industry meant an empty treasury.

The men who actually worked the mines were organised into bodies called gewerken, whose members initially laboured underground themselves but later became primarily financial participants. By the fifteenth century, shares in these mining organisations were freely traded — arguably the earliest example of securitised production interests in Western finance. A merchant in Augsburg could own a fractional interest in a silver mine near Freiberg without ever setting foot in Saxony.

He bore no operational risk beyond his capital commitment and received a proportional share of output after the sovereign had taken his cut. The resemblance to a modern royalty fund's limited partnership structure is not superficial. It is structural.

What made the Bergregal distinctive, and what makes it relevant to the story of pharmaceutical royalties, was the clean separation it imposed between ownership of the resource, operation of the extraction, and entitlement to revenue. The sovereign owned the resource. The gewerken operated the mine. The revenue was split by contractual formula. Each party's return was a function of production, not of profit — a distinction that matters enormously in royalty finance, where the royalty holder is insulated from the operator's cost overruns, mismanagement, and balance-sheet distress.

This structure worked because it solved a problem that has recurred in every century since: the owner of a productive asset needs capital or legitimacy; the provider of capital or legitimacy wants a predictable return without operational entanglement. In 1158, the productive asset was silver ore and the provider was the emperor. In 2026, the productive asset is a patent on a GLP-1 receptor agonist and the provider is a New York investment fund. The problem is the same. The instrument is the same. Only the assets have changed.

The English Fork

The Bergregal model travelled well across continental Europe but collided with a different legal tradition when it reached England. On the continent, mineral deposits belonged to the crown — full stop. But in 1568, the Case of Mines restricted the English crown's mining rights to gold and silver, of which England had virtually no meaningful deposits. Everything else — iron, zinc, copper, lead, tin, and crucially coal — belonged to the landowner.

This judicial decision, later reinforced by statute in 1688, created something that did not exist on the continent: a private, alienable property right in subsurface minerals. An English landlord who owned coal under his estate could mine it himself, or — and this is the critical innovation — he could lease the mineral rights to an operator and collect royalties. Not royalties owed to a king, but royalties owed to a private party under a commercial contract.

The distinction seems technical. It was revolutionary. Continental mineral law kept royalties within the domain of sovereign prerogative and public administration. English common law turned them into private property that could be bought, sold, leased, mortgaged, and inherited. When English settlers crossed the Atlantic, they carried this legal framework with them. American mineral law inherited the English common-law presumption that the landowner owns what lies beneath the surface. The entire architecture of the modern oil and gas royalty market — overriding royalty interests, net profits interests, mineral trusts, volumetric production payments — descends from this single fork in medieval property law.

The continental tradition produced state-controlled mining bureaucracies. The English tradition produced tradeable royalty interests. Only one of these traditions could generate an investable asset class.

Texas and Toronto

The American mining and oil industries scaled the English model to industrial proportions. The Mineral Leasing Act of 1920 permitted the federal government to issue leases for mineral development on public lands in exchange for annual rentals and production royalties. The Relinquishment Act of 1919 in Texas made the surface owner an agent of the state while retaining a one-sixteenth royalty interest for the state treasury.

By the mid-twentieth century, the royalty interest was a mature, well-understood financial instrument in American natural resources. It had standardised terms. It had independent verification. It had liquid secondary markets.

But it remained, for decades, something that the owner of the land held passively — a legacy interest rather than an investment thesis. The conceptual leap from "I own mineral rights under my ranch" to "I will build a company whose entire strategy is acquiring royalty interests from other people" took until the early 1980s and happened, somewhat improbably, in Canada.

Royal Gold was founded in 1981 in Denver. Franco-Nevada followed in 1983, created by Seymour Schulich and Pierre Lassonde in Toronto with a thesis that would have been familiar to any fifteenth-century Saxon merchant: buy a percentage of future production from mine operators, build a diversified portfolio, and let someone else worry about the operational headaches. Franco-Nevada proved that a company could generate outsized returns while employing almost no one, owning almost nothing physical, and bearing almost no operational risk.

The model's elegance was in its asymmetry: when gold prices rose, Franco-Nevada's revenue rose proportionally, but its costs did not, because it had no costs. When a mine flooded or a strike shut down production, the mine operator absorbed the loss; Franco-Nevada simply stopped receiving revenue from that stream and collected from the rest of its portfolio. It was diversification without diversification's usual cost — and optionality without optionality's usual premium.

By the time Newmont acquired it in 2002, Franco-Nevada had delivered annualised returns that rivalled the best mining operators — with a fraction of the volatility. The company re-emerged as an independent entity in 2007 and today commands a market capitalisation exceeding $20 billion. Its model has been replicated dozens of times. But the more interesting replication happened not in mining, but in medicine.

Wheaton Precious Metals, founded in 2004, added another layer of innovation with streaming agreements: an upfront payment for the right to purchase future production at a fixed price below market value. Not technically a royalty, but functionally similar — a non-operating revenue participation that traded operational risk for cash-flow predictability.

The critical point is that these companies emerged from Toronto and its surrounding ecosystem. The Toronto Stock Exchange and its venture boards had spent a century financing mining companies and were comfortable with the concept of separating operational risk from production economics.

Bay Street had the lawyers, the accountants, the geologists, and the deal professionals who could structure, underwrite, and trade mineral interests. When someone in that ecosystem looked at pharmaceutical patents and saw a structurally similar asset — a finite-life right to a revenue stream generated by someone else's operations — the intellectual leap was short.

The American Catalyst

Before anyone in Toronto or New York could buy pharmaceutical royalties, someone had to create them. That someone, in a sense, was the United States Congress.

The Bayh-Dole Act of 1980 is one of the most consequential pieces of economic legislation of the late twentieth century, and one of the least discussed outside specialist circles. Before its passage, the federal government retained ownership of patents arising from federally funded research. The result was predictable: fewer than five per cent of 28,000 government-held patents were ever commercially licensed. Inventions funded by taxpayers sat in filing cabinets.

Bayh-Dole changed the default. Universities could now retain patents on inventions made with federal funding, provided they shared royalties with the inventors and made reasonable efforts to commercialise. The response was dramatic. University patents rose from roughly 390 per year to over 3,000 by 2009. Technology transfer offices multiplied from around 30 to more than 300. Over 11,000 university spin-off companies were formed. The estimated GDP contribution of Bayh-Dole-enabled innovation runs to $1.3–1.7 trillion.

For the purposes of this story, the Act's most important effect was creating a new class of concentrated, transferable financial assets. When Stanford and the University of California, San Francisco held the Cohen-Boyer recombinant DNA patents — licensed to 468 companies before expiring in 1997, generating more than $250 million — they held something that looked remarkably like a mineral royalty: a right to a percentage of commercial production, derived from an underlying intellectual property claim, with a defined expiration date and predictable cash flows.

Columbia University's Axel co-transformation patents produced $790 million over seventeen years. Northwestern University's pregabalin (Lyrica) royalty generated over $700 million through 2018. Emory University earned more than $540 million from its emtricitabine (Emtriva) royalty.

The University of Minnesota's abacavir (Ziagen) royalty added another $450 million through 2016. NYU's Remicade royalty exceeded $650 million. City of Hope's interests in Herceptin and Rituxan surpassed $500 million. These were not isolated windfalls. They were a pattern: federally funded research at American universities had produced a new class of financial asset whose value rivalled that of producing oil fields.

These were enormous sums flowing to institutions that, for the most part, had no particular expertise in managing them. A university treasurer sitting on a $40 million annual royalty stream from a blockbuster drug faced an unfamiliar problem: how to value the stream, how to manage the risk of patent expiration and generic entry, and whether to hold or sell.

The institutions were motivated sellers. They needed liquidity, faced internal pressure to monetise, and lacked the specialist knowledge to negotiate effectively with buyers.

In short, Bayh-Dole created a pool of motivated sellers holding concentrated, predictable, finite-life revenue streams — exactly the conditions under which a specialist buyer can earn outsized returns.

The Precursors

Before the first dedicated royalty fund appeared, the 1980s produced a precursor model that taught a generation of financiers how royalty-based returns on drug development actually worked. R&D limited partnerships allowed investors to deduct research expenditures while receiving royalty-like returns on successful products. Genentech used the structure for its 1980 IPO, which raised $35 million with no approved products.

Amgen raised nearly $40 million in 1983. Biogen and Centocor both employed variations throughout the decade.

The partnerships worked because they combined a tax deduction on the research investment with a future revenue share — effectively, a royalty on whatever the research produced. The Tax Reform Act of 1986 curtailed the tax benefits that made the structure attractive, but by then the fundamental insight was established: an investor could fund pharmaceutical development and receive a predictable percentage of future sales, without taking equity risk in the operating company.

According to Andrew Lo at MIT, members of what would become Royalty Pharma's management team had experience establishing R&D partnerships during the 1980s before transitioning to the direct acquisition model. The intellectual lineage is direct.

The 1986 tax reform killed the R&D limited partnership. But the people who understood the structure simply pivoted to buying royalties that already existed rather than creating new ones through funded research.

Toronto's Invention

Drug Royalty Corporation emerged in Toronto between 1989 and 1993. Its founders, including James Webster and R. Ian Lennox (the latter from Monsanto Canada), operated in the same Bay Street ecosystem that had produced Franco-Nevada six years earlier. The company listed on the Toronto Stock Exchange in 1993, becoming the first publicly traded pharmaceutical royalty entity.

The parallels with the mining royalty model were explicit. DRI — as it became known after rebranding to DRI Capital in 2007 — built a portfolio of royalty interests in approved drugs the way Franco-Nevada built a portfolio of royalty interests in producing mines. Early acquisitions included stakes in the royalty streams of Taxol (oncology, $1.6 billion in peak annual sales), Neupogen (supportive care, $1.3 billion), ReoPro (cardiovascular, $400 million), and Remicade (autoimmune, $8 billion).

By 2007, DRI managed over $1 billion. Over its life, the firm has deployed more than $3 billion across seventy-five-plus royalties.

DRI's history also illustrates the governance risks inherent in any pioneering financial vehicle. In 2002, the Khosrowshahi family's Persis Holdings acquired DRI Capital for $133 million, funded partly from the proceeds of selling Future Shop to Best Buy.

The company went through a trust structure IPO in 2021 with an external management agreement that charged 6.5 per cent of cash royalty receipts plus twenty per cent performance fees — a fee structure that would have made a hedge fund manager blush.

In July 2024, CEO Behzad Khosrowshahi was forced to resign after an investigation uncovered $6.5 million in irregularly charged consulting and other expenses. The CFO was suspended. Shares fell 32 per cent. The trust subsequently internalised its management for a $48 million termination payment — paid to the family of the man whose expense fraud had triggered the crisis. The board argued, probably correctly, that the internalization would save $200 million over ten years. The optics were, to put it charitably, imperfect.

The DRI story matters beyond its entertainment value because it demonstrates something important about asset-class formation. First movers bear experimental risk. They test structures, make governance mistakes, and create precedents — both positive and cautionary — that subsequent entrants learn from. DRI proved the model. Its turbulence proved that the model needed better governance. Both lessons were necessary.

New York's Scaling

Pablo Legorreta founded Royalty Pharma in New York in 1996 after a decade at Lazard, where he had developed a view that academic institutions sitting on drug royalties were systematically undervaluing them. Co-founded with Rory Riggs, the company raised $60 million in initial capital from investors including the Giuliani brothers, Italian industrialists whom Legorreta reportedly met at Milan's airport.

Where DRI had imported mining-royalty logic from Toronto's Bay Street, Royalty Pharma brought Wall Street's institutional scaling machinery. Legorreta's insight was twofold. First, university technology transfer offices were motivated sellers — they needed liquidity, faced board pressure to monetise uncertain future cash flows, and typically lacked the biostatistical expertise to value late-stage drug royalties accurately. Second, the assets themselves were misunderstood by generalist investors.

A royalty on an approved drug — particularly one past its launch phase, with eighteen to twenty-four months of commercial data — is among the most predictable cash-flow instruments in private markets: tied to prescription volumes, shielded from the operating company's cost structure, and bounded by a known patent expiry. The risk is real but quantifiable. The returns, for a specialist buyer, were exceptional.

Royalty Pharma grew steadily through the 2000s, acquiring cornerstone positions in university royalties on drugs including Lyrica, Emtriva, and the HIV franchise. It IPO'd on the NASDAQ in June 2020, raising $2.2 billion in the largest healthcare IPO of that year. By 2025, the company had deployed more than $30 billion cumulatively and reported royalty receipts approaching $3 billion annually. It is the undisputed market leader — the Franco-Nevada of pharmaceuticals.

The publicly traded pharmaceutical royalty landscape has broadened beyond Royalty Pharma and DRI. XOMA Corporation, once a traditional biotech, has reinvented itself as a royalty aggregator with over 120 assets in its portfolio, acquiring economic interests in the milestones and royalties of drugs it had no hand in developing.

Ligand Pharmaceuticals has pursued a similar strategy, building a portfolio of royalty and milestone interests through its Captisol and OmniAb platform technologies. These companies, together with DRI Healthcare on the Toronto Stock Exchange, give public-market investors multiple points of access to pharmaceutical royalty economics — a far cry from the single, thinly traded DRI trust of the early 2000s.

The concentration is striking. Royalty Pharma, Healthcare Royalty Partners, and Blackstone Life Sciences together account for roughly seventy-one per cent of royalty origination deal value. The entire dedicated pharmaceutical royalty market, measured by deployed capital, exceeds $50 billion. Annual deployment from 2020 to 2024 reached $29.4 billion — more than double the preceding five years.

The Instrument Zoo

One of the most illuminating exercises in understanding pharmaceutical royalties is to compare the instrument set that exists in pharma with what exists in other revenue-based financing markets. The comparison reveals how much pharma has borrowed from mining — and how much it has not.

Oil and gas developed the overriding royalty interest (ORRI), a non-operating interest carved from the lessee's working interest that conveys a percentage of production revenue with no exposure to operating costs. It also developed the volumetric production payment (VPP), an advance sale of a fixed quantity of future production — essentially a commodity-linked loan. Net profits interests, production payments, and mineral trusts round out a toolkit that is, by pharmaceutical standards, extraordinarily diverse.

Music developed its own variant. When Blackstone closed a $1.47 billion asset-backed securitisation backed by royalties from 45,000 Hipgnosis songs in late 2024, twenty-five institutional investors participated in a single issuance. The music industry has rated ABS tranches, public secondary markets in catalogue royalties, fractional retail platforms, and a transparent marketplace where individual song catalogues trade like real estate.

Mining has streaming agreements. Technology has revenue-based financing, where SaaS companies sell a percentage of future recurring revenue in exchange for upfront growth capital. Real estate has ground rents. Each of these markets developed instruments specific to its asset characteristics — instruments that reflect the risk profile, duration, liquidity, and verification infrastructure of the underlying assets.

Pharmaceutical royalties, by contrast, operate with a remarkably narrow toolkit. The standard transaction is a bilateral acquisition: one buyer, one seller, a negotiated price for a percentage of future drug sales through patent expiry. There is no ABS market for drug royalties. There is no rated securitisation. There is no public secondary market where existing royalty positions trade transparently. There are no retail products.

Syndication — routine in leveraged finance, private credit, and even music royalty deals — remains rare. When Royalty Pharma wrote a $905 million cheque for the vorasidenib royalty from Agios, it did so alone.

This narrowness is deceptive, however, because it obscures the structural diversity that does exist within the pharmaceutical royalty market. The instruments may all be called "royalties," but a gross sales override on a blockbuster oncology drug and a revenue interest purchase agreement on a pre-revenue rare disease company are as different from each other as a government bond is from a convertible note.

The Periodic Table of Royalties — a classification framework developed by Capital for Cures that maps over sixty pharmaceutical royalty instrument types across eight structural groups — reveals just how varied the taxonomy has become.

There are direct royalties (gross and net sales), derived claims (profit shares and licensing income), contingent instruments (milestones and tiered structures), and engineered instruments (synthetics and securitisations). There are hybrid structures that combine royalty economics with debt covenants, equity kickers, or geographic carve-outs.

Revolution Medicines' $2 billion package from Royalty Pharma — $1.25 billion synthetic royalty plus $750 million term loan, with coordinated change-of-control provisions and tiered rates from 4.55 per cent tapering to zero above $8 billion in cumulative sales — is not the same instrument as Northwestern University's simple percentage-of-net-sales royalty on Lyrica.

But they share a common ancestor, and they sit on the same periodic table.

The point is not the complexity itself. It is that pharma has developed structural diversity without developing the shared language, the standardised classifications, or the independent verification infrastructure that would make that diversity legible to the broader capital markets. Oil and gas can describe a volumetric production payment in terms that any energy lender understands.

Music can rate a catalogue ABS tranche in terms that any fixed-income investor recognises. Pharma cannot yet do the equivalent for a milestone-linked synthetic royalty with a cap and a change-of-control ratchet. Every deal looks bespoke. Comparability is elusive. Mispricing is invisible.

The reason for this narrowness is not that pharmaceutical royalties are inherently unsuitable for more sophisticated structuring. It is that pharma lacks the verification infrastructure that enables those structures in other markets. Oil and gas has SPE-certified reserve engineers who produce independent, standardised reserve estimates (the PV10 metric) that rating agencies, lenders, and secondary buyers all rely on.

Music has ASCAP and BMI tracking mechanical and performance royalties in real time. Mining has independent geological reports and commodity exchanges that provide transparent pricing.

Pharma has none of this. Drug sales forecasts are proprietary. Two analysts can disagree by a factor of three on the same asset. There is no independent reserve-engineer equivalent for drug royalties — no standardised methodology for valuing a royalty stream on a Phase III oncology asset that a rating agency would accept. There is no observable return index that institutional investors can benchmark against. The result is a market that functions bilaterally, between specialist buyers and motivated sellers, with minimal price transparency and no secondary liquidity.

This is not an inherent limitation. It is an infrastructure gap. And infrastructure gaps get filled.

Europe's Absence

If the history of pharmaceutical royalty financing is a story about the migration of a medieval instrument through English common law, American patent reform, and Canadian mining finance, then Europe's absence from the modern market is not mysterious. It is overdetermined.

Start with the intellectual property regime. Across continental Europe, a tradition known as "professor's privilege" gave individual academics, rather than their universities, ownership of inventions arising from their research. France reformed this in 1999, Germany in 2002, Denmark in 2000, Austria in 2002, Norway in 2003. Sweden still maintains it. Each of these reforms came roughly two decades after Bayh-Dole.

The consequence was that European universities had fewer concentrated royalty streams to sell. A fragmented landscape of individual inventor-held patents did not produce the kind of large, institutional royalty positions that specialist buyers could acquire efficiently.

Then consider the capital markets infrastructure. Europe had no equivalent of Toronto's mining finance ecosystem — no deep bench of professionals who understood non-operating revenue participation interests and could adapt the model to a new asset class. The legal, accounting, and fund-structuring expertise that enabled DRI and Royalty Pharma to build their businesses was specific to North American capital markets.

The result was that when European royalties did emerge, North American capital bought them. LifeArc, the British medical research charity, held one of Europe's most valuable pharmaceutical assets: a royalty on Keytruda, the anti-PD-1 immunotherapy that became the world's best-selling cancer drug. LifeArc sold a portion to DRI Capital for $150 million in 2016 and the remainder to Canada's CPPIB for $1.297 billion in 2019. Europe's biggest pharmaceutical royalty was monetised entirely by Canadian capital.

The pattern is starting to shift. Partners Group, headquartered in Baar, Switzerland, launched what appears to be the industry's first European-managed multi-sector royalty platform in 2024. KKR's acquisition of a majority stake in Healthcare Royalty Partners in 2025, adding $3 billion in assets under management, brought further institutional scale.

European limited partners are increasingly allocating to royalty strategies — Healthcare Royalty's recent funds reportedly drew more than sixty per cent of their capital from non-US investors.

The EU's BioTechEU initiative, announced with a €10 billion mobilisation target for 2026–2027, has yet to include any royalty fund component — a notable omission given that royalty financing is precisely the kind of non-dilutive, IP-preserving capital instrument that European biotech companies lack. The European Investment Fund has committed €2 billion cumulatively to life sciences but has never backed a dedicated royalty vehicle.

The UK's Mansion House Accord set a target of ten per cent pension allocation to private markets, versus an actual figure closer to 0.36 per cent. The gap between policy ambition and capital deployment remains vast.

But the funds themselves remain US-managed. No European Royalty Pharma has emerged. No European DRI. The asset class was invented in Europe a millennium ago. It was reinvented for pharmaceuticals in North America thirty years ago. The round trip has not yet been completed.

What the Origin Story Explains

The history of royalty financing is not a curiosity. It is a diagnostic tool. The patterns that recur across mining, oil and gas, music, and pharmaceuticals reveal a set of preconditions that must be satisfied before royalty financing can take hold in any sector.

First, there must be an asset that generates a predictable revenue stream from someone else's operations. A mine produces ore. A well produces oil. A patent produces licensing income. A song generates mechanical and performance royalties. In each case, the revenue arises from an activity that the royalty holder does not perform and cannot control.

Second, there must be a pool of motivated sellers. University technology transfer offices that needed liquidity. Landowners sitting on mineral rights they lacked the capital to develop. Songwriters who wanted to monetise a lifetime of catalogue earnings in a single transaction.

The seller must have a reason to prefer a lump sum today over an uncertain stream of future payments — typically because they face a valuation asymmetry (the buyer knows more about the asset's future value than the seller does), a liquidity need (the seller wants cash now), or an institutional constraint (the seller's board or governance structure prefers monetisation).

Third, there must be a concentrated group of specialist buyers who develop expertise, deal flow, and valuation capabilities that generalist investors cannot replicate. Franco-Nevada in mining. Royalty Pharma in drugs. Hipgnosis and Round Hill in music.

The specialist buyer's advantage is not capital — capital is abundant. It is knowledge: the ability to value a finite-life, uncertain cash-flow stream more accurately than the seller or than competing bidders.

Fourth, and this is where pharma remains underdeveloped, there must be verification infrastructure. Oil and gas built an elaborate ecosystem of independent reserve engineers, standardised reserve classifications (proved, probable, possible), publicly reported PV10 metrics, and commodity exchanges that provide transparent reference pricing.

This infrastructure is what enables rated securitisations, liquid secondary markets, retail investment products, and institutional-scale deployment. It is what turns a bilateral market into a capital market.

Music built a version of this with mechanical royalty tracking, performance rights organisations, and catalogue valuation methodologies that, while imperfect, are transparent enough to support rated ABS issuances.

Pharma has not. Drug sales forecasts are proprietary. Royalty deal pricing is opaque. There is no standardised methodology for independently valuing a pharmaceutical royalty stream that a rating agency or secondary buyer would accept without conducting its own full due diligence.

The result is that pharmaceutical royalties trade bilaterally, at valuations that are essentially private negotiations between sophisticated parties, with no benchmark index, no observable market-clearing price, and no independent verification layer.

This is not a criticism of the market's participants. It is a description of its maturity stage. Oil and gas took a century to build its verification infrastructure.

Mining took decades. Music is still building. Pharma is perhaps twenty years into the process and has reached the point where the market is large enough — $50 billion in deployed capital, $29 billion deployed in five years — that the absence of infrastructure is itself becoming a constraint on growth.

The Shape of the Risk

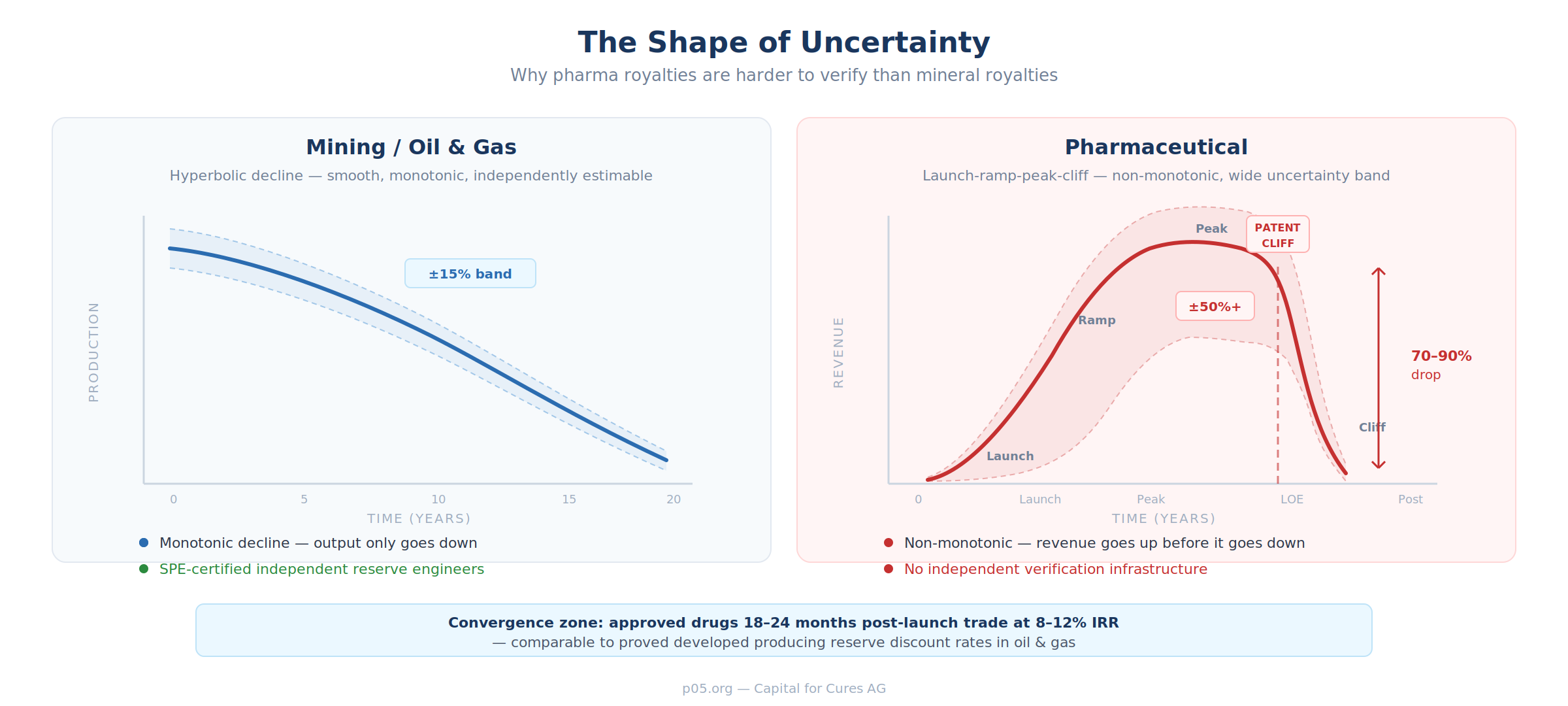

One objection to the mining-to-pharma analogy deserves serious treatment, because it explains why pharmaceutical royalty markets have developed more slowly than their natural-resources counterparts.

A producing gold mine follows what petroleum engineers call a decline curve: output starts at a peak and diminishes steadily, year after year, as the deposit is depleted. The curve's shape varies — exponential, hyperbolic, harmonic — but the direction is always down. Crucially, the uncertainty band is narrow. An independent reserve engineer can estimate remaining production within perhaps fifteen per cent of the eventual outcome.

This predictability is what enables rated securitisations, standardised valuations, and liquid secondary markets.

A pharmaceutical royalty follows a fundamentally different curve. A drug launches, ramps through market penetration over two to four years, reaches a commercial peak, plateaus for some period, and then falls off a cliff when the patent expires or a generic enters the market. The cliff can mean a seventy to ninety per cent revenue decline within twelve to twenty-four months.

Unlike a mine, the curve is non-monotonic — revenue goes up before it goes down. And unlike a mine, the uncertainty band is wide: two competent analysts can disagree by a factor of three on the same asset's future revenue, depending on their assumptions about market uptake, competitive dynamics, label expansion, pricing, and the timing and impact of generic entry.

This is not an abstract distinction. It is the reason that pharmaceutical royalties are harder to rate, harder to securitise, and harder to trade on secondary markets than mineral royalties.

The oil and gas verification ecosystem — reserve engineers, PV10 metrics, commodity exchanges — works because the underlying production curves are smooth, monotonic, and independently estimable. The pharmaceutical equivalent would require a standardised methodology for modelling launch curves, peak sales, and patent-cliff dynamics that independent parties could agree on. No such methodology exists.

There is, however, a convergence zone. Commercial-stage royalties — those on drugs that have been on the market for eighteen to twenty-four months, with observable prescription data, established competitive positioning, and a known patent expiry — are substantially de-risked. They trade at seven to twelve times annual royalty receipts, implying IRRs of eight to twelve per cent.

These discount rates are not far from the rates applied to proved developed producing reserves in oil and gas. It is in this convergence zone — where pharma royalty risk begins to resemble commodity-production risk — that the infrastructure gap is most acutely felt and most economically valuable to close.

Building the Missing Layer

What would pharmaceutical royalty verification infrastructure look like? The oil and gas analogy suggests several components.

Standardised royalty receipt reporting — the pharmaceutical equivalent of production reporting in oil and gas — would give investors and analysts a consistent, comparable view of how much cash individual royalty streams are generating, quarter by quarter. Today, this information is available for publicly traded vehicles like Royalty Pharma and DRI Healthcare, but not for the dozens of private funds and bilateral arrangements that account for a significant share of the market.

Consensus sales forecast providers would serve the function that reserve engineers serve in oil and gas: independent, standardised estimates of future production (in this case, future drug sales) that can be used by multiple parties for valuation, underwriting, and risk assessment. Providers like IQVIA, EvaluatePharma, and Visible Alpha exist, but their forecasts are not standardised in the way that SPE reserve classifications are, and they are not accepted by rating agencies as a basis for securitisation.

Observable return indices would allow institutional investors to benchmark pharmaceutical royalty returns against other asset classes — a prerequisite for meaningful allocation decisions by pension funds, endowments, and sovereign wealth funds. Today, there is no pharmaceutical royalty return index comparable to what exists for private equity, private credit, or real estate.

Transparent deal pricing benchmarks would do for pharmaceutical royalties what the Texas Comptroller's valuation surveys do for mineral interests: provide a public reference point for what assets trade at, segmented by risk category, development stage, and therapeutic area.

Each of these components is technically feasible. None requires regulatory change. All require coordination, standardisation, and — critically — a willingness by market participants to sacrifice some informational advantage in exchange for a larger, more liquid, more institutional market. The specialist buyers who dominate the current market have rational reasons to prefer opacity: their returns depend on valuation asymmetries that transparency would erode.

But history suggests that the benefits of scale — lower cost of capital, broader investor participation, secondary liquidity — eventually outweigh the benefits of information advantage. It happened in mining. It happened in oil and gas. It is happening in music. The question for pharmaceutical royalties is not whether it will happen, but when, and who will build it.

The Long Arc

The royalty is among the oldest revenue-participation instruments in continuous use — predating joint-stock companies by centuries, even if debt on Mesopotamian clay tablets got there first.

The royalty is arguably the oldest financial instrument in continuous use. The Bergregal codified at Roncaglia in 1158 was already a formalisation of practices that predated it by centuries. The English Case of Mines in 1568 privatised it.

The American Mineral Leasing Act of 1920 industrialised it. Franco-Nevada in 1983 turned it into an investment strategy. Bayh-Dole in 1980 created the pharmaceutical version of the underlying asset. Drug Royalty Corporation in 1989 applied the mining model to molecules.

Royalty Pharma in 1996 scaled it. The 2020s are institutionalising it.

Through every iteration, the core structure has not changed: a non-operating party receives a percentage of production revenue in exchange for granting access to an asset or providing upfront capital. What has changed is the sophistication of the assets, the complexity of the cash-flow modelling, and the scale of capital deployed.

What has also changed, over centuries, is the infrastructure that surrounds the instrument — the verification systems, the standardised classifications, the secondary markets, the legal frameworks, and the institutional norms that determine whether a royalty interest is a bilateral private contract or a liquid, rateable, tradeable security.

The pharmaceutical royalty market has the assets. It has the capital. It has the specialist buyers and the motivated sellers. It has thirty years of demonstrated returns. What it does not yet have is the infrastructure layer that would allow it to operate at the scale its fundamentals warrant. Mining built that infrastructure over a century.

Oil and gas did it in decades. Music is doing it now. Pharma needs to do it in years, not decades — because the capital waiting to enter this market does not have the patience of a medieval emperor.

The Bergregal was a ten per cent tithe on silver ore, collected by a sovereign who granted mining rights in exchange. A pharmaceutical royalty is a mid-single-digit percentage of net sales, collected by an investor who provided upfront capital in exchange.The assets could not be more different.

The instrument — older than equity, older than insurance, older than the bill of exchange — could not be more similar.

The irony is rich: the concept was born in Europe, perfected in North America, and is now being deployed primarily against European-originated assets by American capital. Over twenty per cent of global pharmaceutical royalty deals involve European sellers. The intellectual property flows out; the financial returns flow back to New York and Toronto.

A European fund manager who understood this history — who saw the Bergregal not as a historical curiosity but as a structural template — might recognise the opportunity to close the circle. The instrument came from here. Perhaps it is time it came home.

Understanding that lineage is the first step toward understanding where this market goes next.

Disclaimer: The author is not a lawyer, financial adviser, or investment professional. This content is for informational purposes only and does not constitute investment, legal, or financial advice. Readers should consult qualified professionals before making any investment decisions or entering into transactions described herein.