Japan's Pharmaceutical Royalty Market: Will We See More Assets Out of Japan?

The conversation about Asia-Pacific pharmaceutical royalties tends to start and end with China. The out-licensing volume data from 2025 makes that reflex understandable, and Royalty Pharma's appointment of Kenneth Sun as Head of Asia is the clearest institutional signal yet that Western royalty capital is moving east.

But there is a second Asian market worth examining in the same breath, one that is structurally different in ways that matter a great deal to royalty investors: Japan.

Japan's pharmaceutical royalty opportunity does not require the same set of structural negotiations that China does. There is no VIE architecture, no ambiguity around enforceability, no capital repatriation approval process, no question about whether a contractual claim is legally coherent.

The legal framework is robust, the IP courts are functional and increasingly pro-patentee, and deal economics flow in currencies that royalty investors have modelled for decades. The question, as of March 2026, is not whether the architecture works. It does. The question is whether the structural conditions that historically suppressed Japan-sourced royalty volume are changing, and whether the current moment represents a genuine inflection.

There is a reasonable case that it is.

The Pricing Trap: What Suppressed Japan Royalty Volume

To understand the Japan royalty opportunity, you have to understand the pricing system, because that system is both the core problem and the axis around which the current reform debate turns.

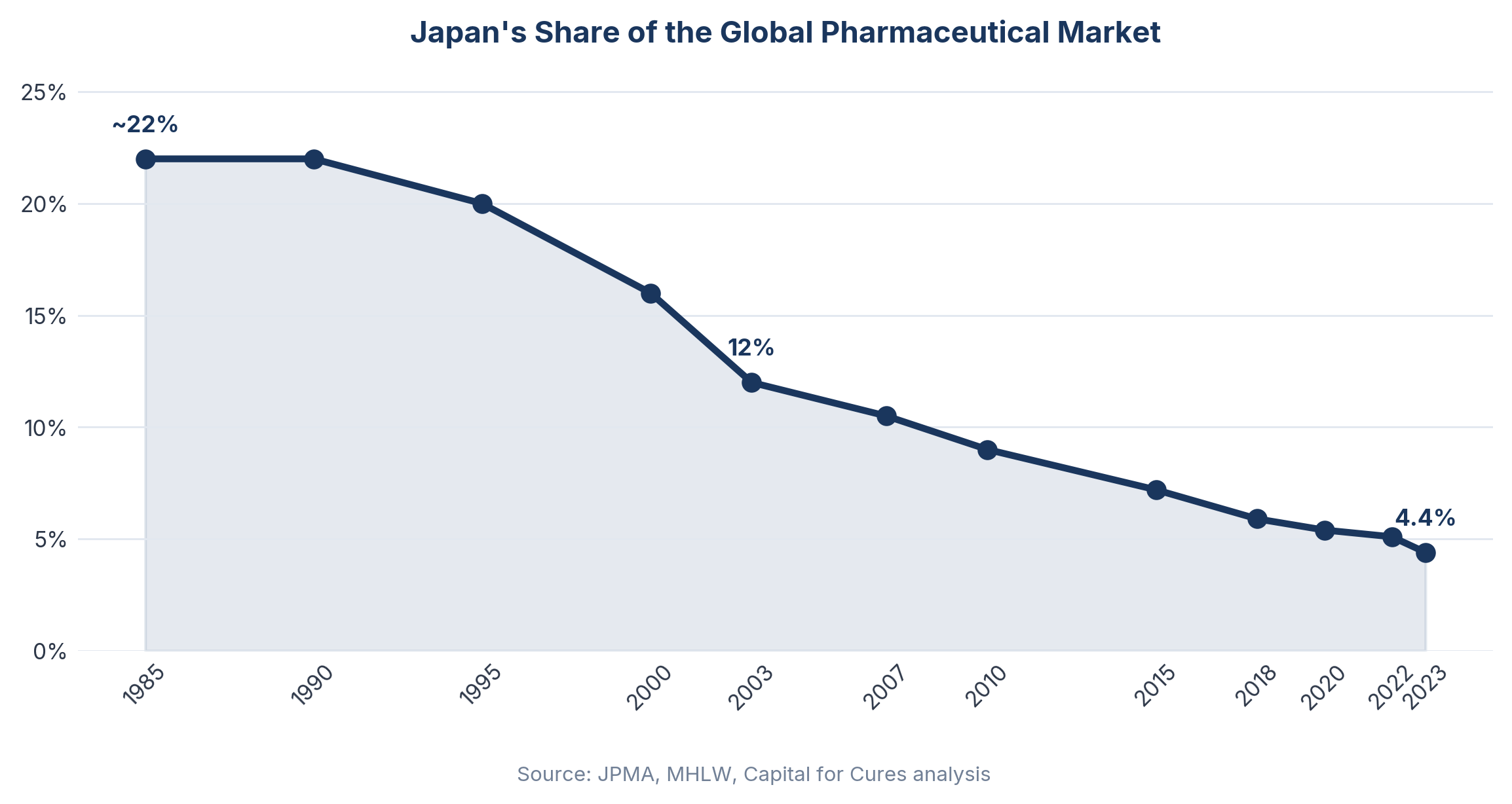

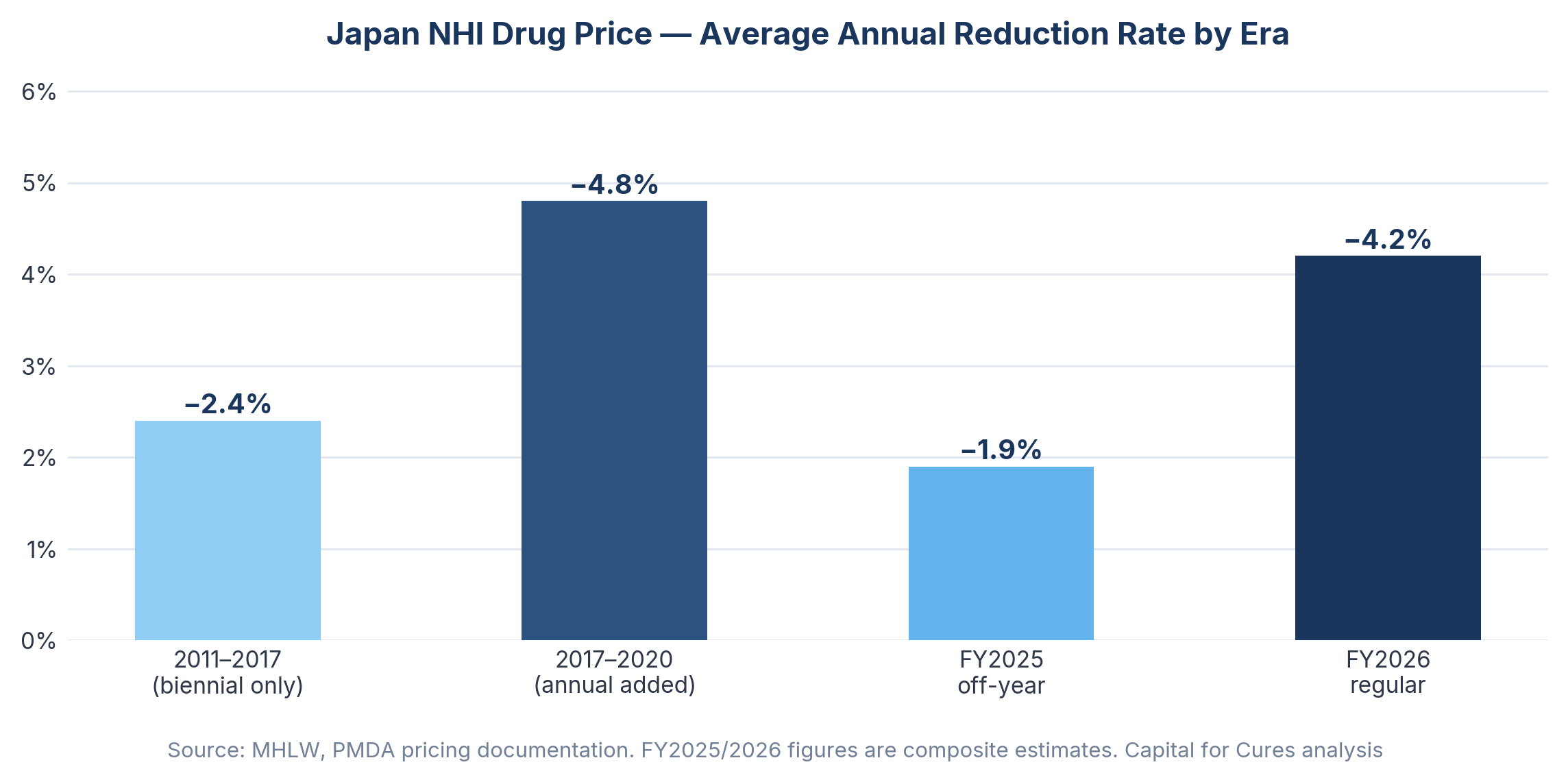

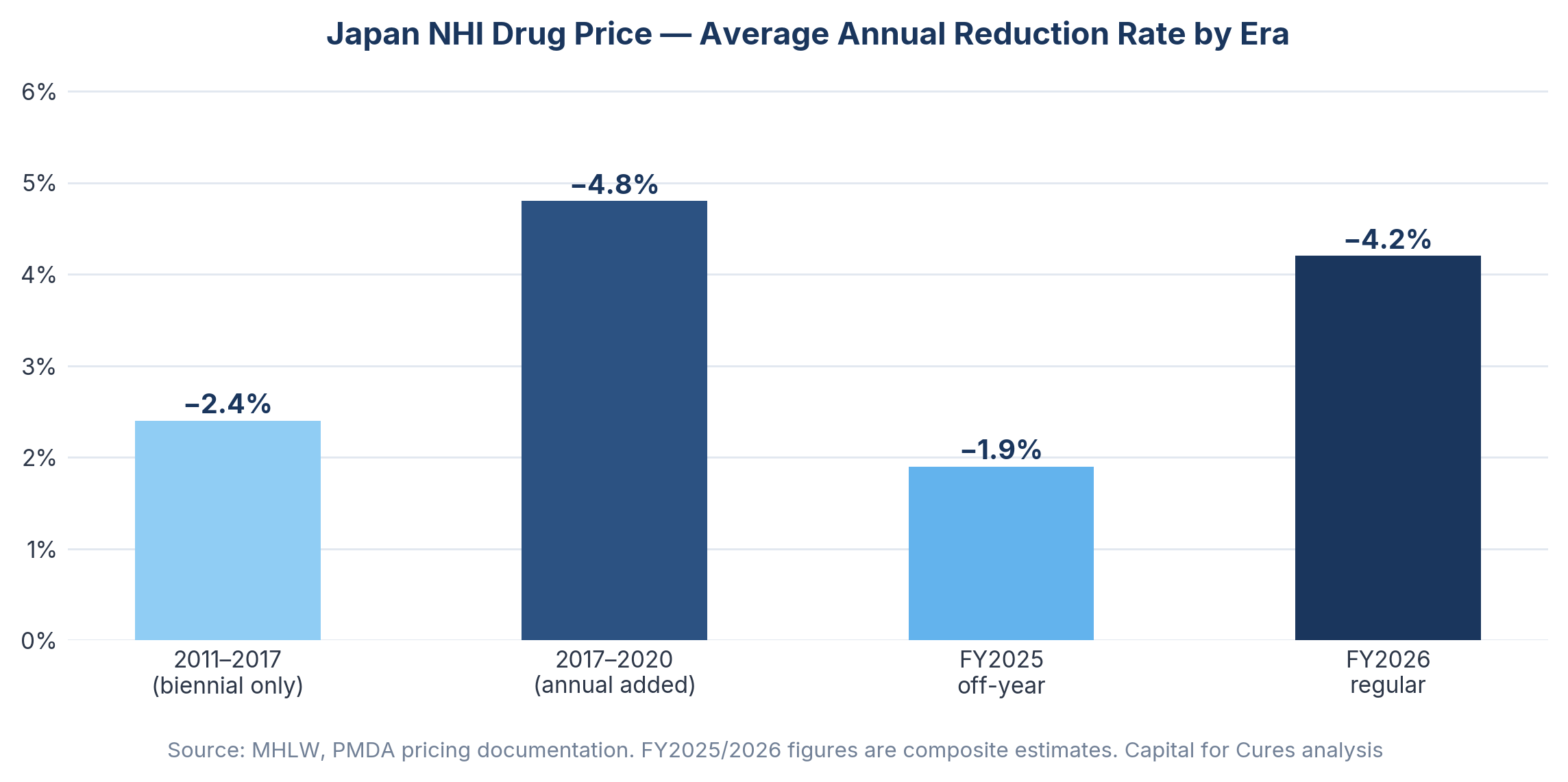

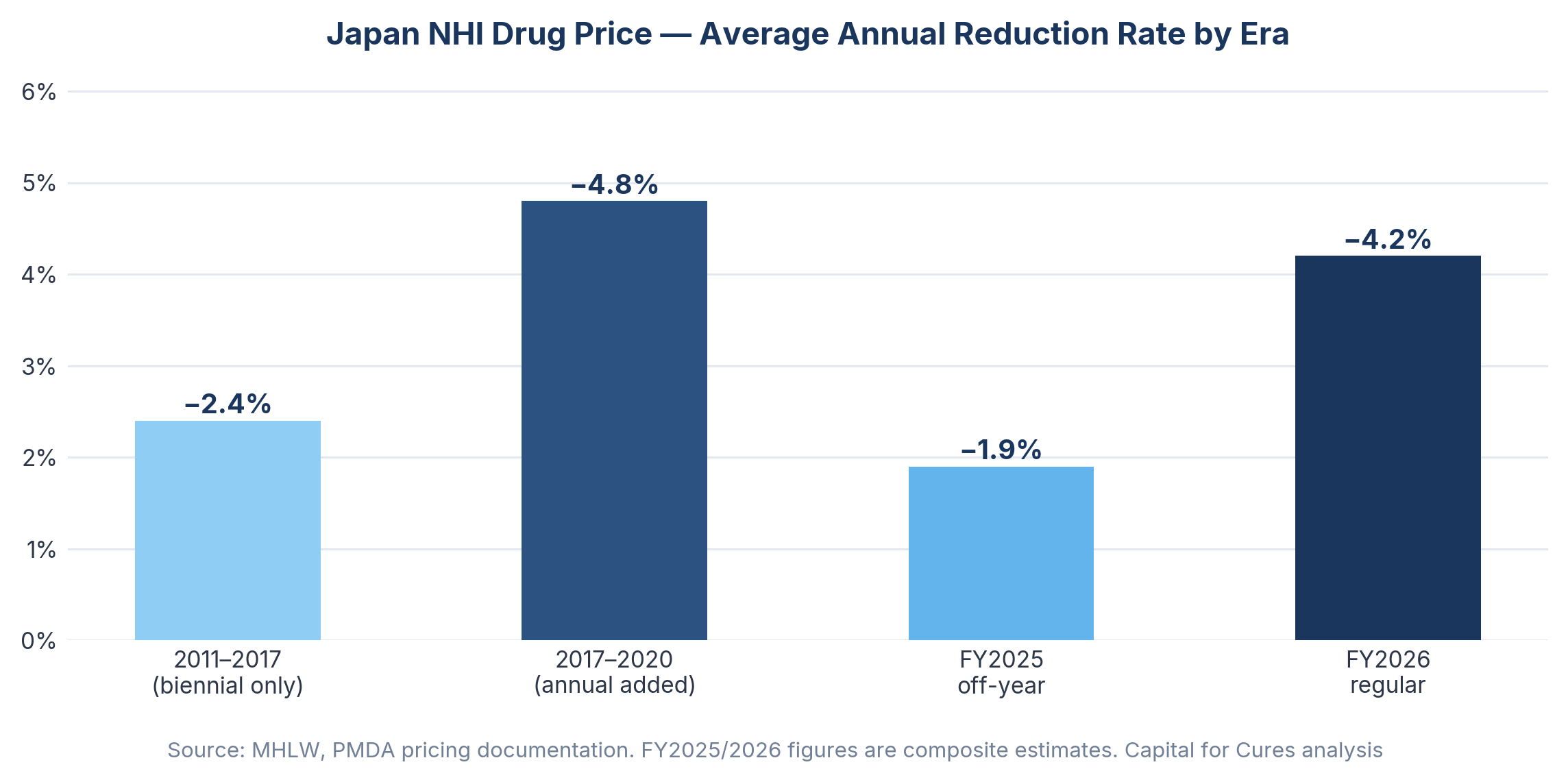

Japan's National Health Insurance mechanism sets a uniform reimbursement price for every listed drug nationwide, revised downward on a regular schedule based on surveys of actual transaction prices between manufacturers and hospitals. Since 2018, annual off-year revisions have compounded the biennial revision cycle, meaning that virtually every drug on the market faces price reductions with metronomic regularity. Japan's share of the global pharmaceutical market showed continuous decline over the past 20 years, from 12.0% in 2003 to 5.1% in 2022, and the annual NHI drug price reduction rate roughly doubled from approximately 2.4% in the 2011–2017 period to around 4.8% between 2017 and 2020.

The consequences for royalty valuation are direct. A royalty stream tied to Japanese drug revenues is not a flat or modestly growing cash flow — it is a structurally declining one, subject to a policy cycle that operates independently of clinical performance. For a royalty investor building a discounted cash flow model, that baseline decline has to be incorporated into every Japan-facing projection, making Japanese domestic revenue streams materially less attractive than equivalently-sized US or European streams.

The FY2026 biennial revision compounds this through a mechanism worth understanding in detail: the Price Maintenance Premium (PMP) return. The PMP, which originated in 2010 as a policy response to drug lag, now behaves like a deferred tax on success. When generics launch at roughly a third of the originator price, the reference point used in the revision survey collapses, and the stored PMP is removed as well. Forxiga illustrates this clearly: generic entry in December 2025 triggered a simultaneous collapse in the survey reference price and removal of accumulated PMP, creating a dual pricing shock ahead of April 2026.

Japan's Ministry of Health, Labor and Welfare confirmed in December 2025 that NHI drug prices will be cut by 0.86% on a healthcare spending basis in FY2026, translating into a reduction of approximately 105.2 billion yen in central government expenditure. The JPMA, in its statement to Chuikyo on the FY2026 reform, noted that less than 10% of the social security budget is spent on medicines but 70% of budget reductions come from drug price cuts — a structural asymmetry that illustrates how exposed the pharmaceutical sector has become as a fiscal adjustment mechanism.

This pricing environment has driven what industry stakeholders call "drug loss" and "drug lag": the phenomenon where globally approved drugs are either never developed in Japan or arrive years behind their US and EU launch dates.

Japan's share of the global pharmaceutical market had dropped to 4.4% in 2023, putting it nearly on par with the German market — a significant decline from the early 1980s when it exceeded 25% of the global market. As of March 2024, 82 drugs approved overseas had not yet begun development in Japan, with 53 products in drug-lag status.

The practical effect for royalty investors has been twofold: Japanese domestic revenue streams have been heavily discounted due to the repricing trajectory, and internationally-oriented royalty opportunities — where Japanese companies out-license to Western counterparts and royalties flow on US or European sales — have been the dominant mode of Japan-facing investment, precisely because those revenues escape the NHI repricing cycle entirely.

The ADC Precedent: How Daiichi Sankyo Changed the Framing

Any analysis of Japan's current royalty position has to start with Daiichi Sankyo, because the ADC story it has built over the past seven years is the most important structural precedent in the market.

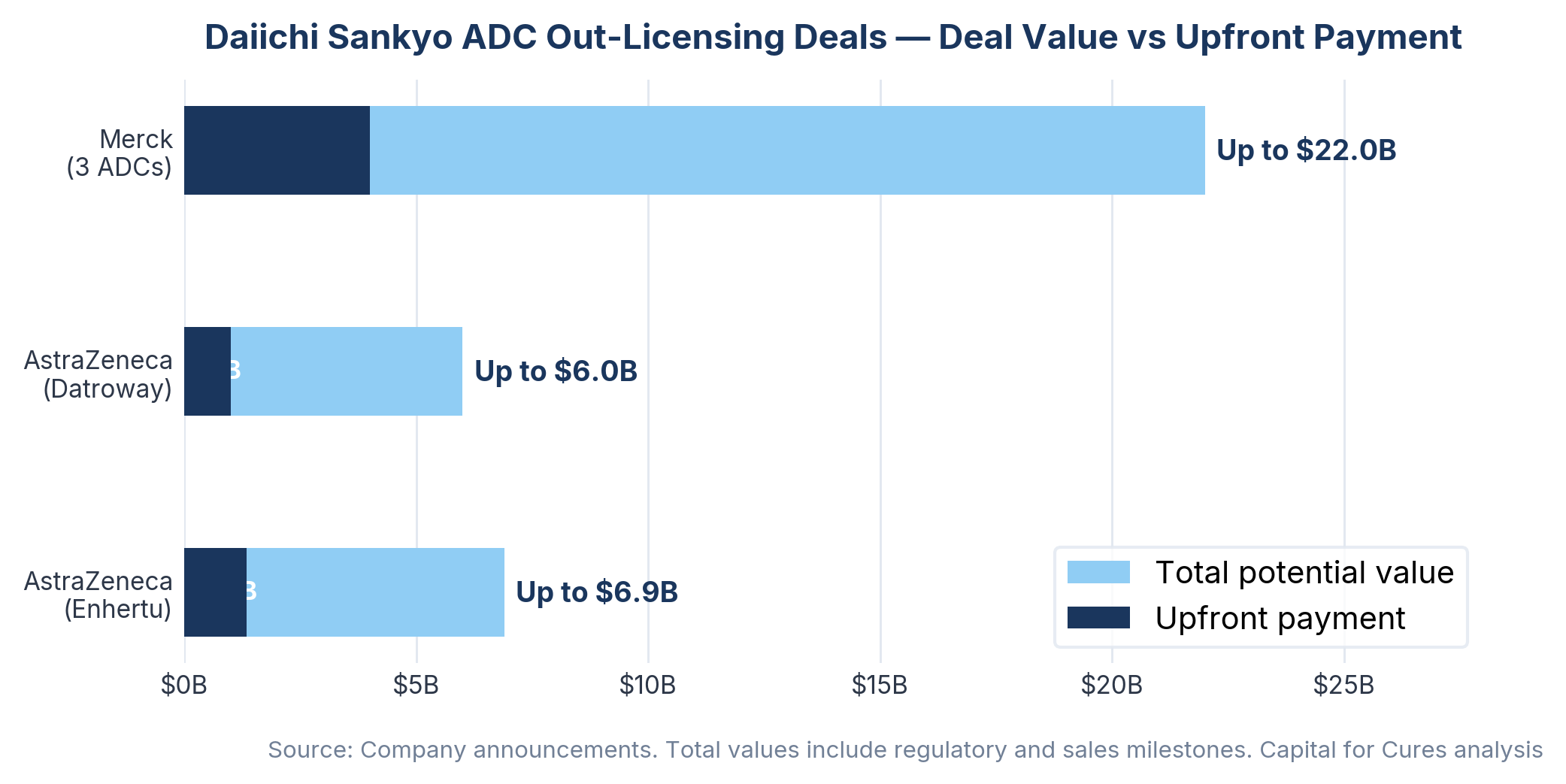

Daiichi Sankyo's Enhertu collaboration with AstraZeneca, signed in 2019, was valued at up to $6.9 billion. The TROP2-directed ADC Datroway followed in 2020 with a further partnership.

Then in September 2023, Daiichi Sankyo announced a $22 billion collaboration with Merck, covering three further ADC candidates. AstraZeneca paid $1.35 billion upfront to license Enhertu in 2019, then paid another $1 billion upfront the following year for the drug now sold as Datroway. Combined, the AstraZeneca and Merck deals promise up to $27 billion in conditional fees tied to regulatory and sales milestones.

The royalty implications are substantial. Enhertu brought in sales of approximately $3.58 billion in the first nine months of 2024, and analysts have suggested it could generate more than $5 billion annually at peak.

Daiichi Sankyo pays its alliance partners 50% of gross profit for product sales in countries outside Japan where Daiichi books revenue, while Japan domestic revenues remain exclusively with the originator.

What this precedent establishes is important: Japanese companies with proprietary ADC platforms have demonstrated that Japan-originated assets can generate royalty-eligible cash flows at a scale that competes with the most valuable programs in global oncology. The structural question is whether Western royalty investors can access those flows directly, and at what point in the asset's lifecycle the transaction makes economic sense.

For Daiichi Sankyo specifically, the answer has largely been handled through the AstraZeneca and Merck partnership structures rather than through third-party royalty financing. But the Daiichi example defines what a Japan-originated royalty asset looks like at its upper end, and that definition is important context for the emerging mid-tier opportunity.

The Structure That Royalty Investors Should Understand: Japan Retained, Ex-Japan Licensed

The most important structural insight for royalty investors approaching the Japan market is one that has been hiding in plain sight for decades. Japanese pharmaceutical companies have a long, well-documented tradition of retaining their domestic rights while out-licensing ex-Japan commercialisation to a Western partner — and those ex-Japan royalty streams are precisely the type of cash flow that royalty investors price, model, and deploy capital against most efficiently.

This is not a new or emerging pattern. It is the established architecture of Japan-originated pharmaceutical out-licensing, and it has produced some of the most consequential royalty streams in the industry.

Ono Pharmaceutical and Opdivo. The most instructive example is Ono Pharmaceutical and nivolumab, the anti-PD-1 antibody now sold globally as Opdivo. In 2011, Ono granted Bristol-Myers Squibb exclusive rights to develop and commercialise Opdivo globally, except in Japan, South Korea, and Taiwan, where Ono retained all rights.

The structure was precise: Ono kept the markets it could serve directly, and BMS paid to access the rest of the world. When the drug became one of the most commercially significant oncology products of the decade — generating multi-billion dollar annual revenues across US and European markets — the royalty economics flowing back to Ono from that ex-Japan license were substantial. For a royalty investor, the Ono-BMS structure is a textbook illustration of how Japan-originated IP, retained in Japan, generates investable cash flows from non-Japanese revenues that are not subject to the NHI pricing cycle.

Shionogi and the ViiV Healthcare HIV portfolio. A structurally different but equally instructive case is Shionogi's relationship with ViiV Healthcare. Shionogi discovered and developed dolutegravir and cabotegravir, two integrase strand transfer inhibitors that became the backbone of modern HIV therapy.

In 2012, Shionogi contributed its HIV portfolio to ViiV Healthcare in exchange for royalty commitments and a 10% equity stake in the company. The royalties on the global ViiV portfolio have since compounded into a major revenue line for Shionogi: total royalty income and dividend income from ViiV for the fiscal year ended March 31, 2025 amounted to 285 billion yen, a record high, an increase of 21.6%.

In January 2026, Shionogi deepened its position further by acquiring Pfizer's 11.7% stake in ViiV for $2.125 billion, increasing its economic interest to 21.7%. This is Japanese pharmaceutical IP generating ex-Japan royalty and dividend income at a scale that rivals the revenue base of mid-sized pharmaceutical companies — and doing so through a structure governed by UK law, with counterparties including GSK.

Otsuka Pharmaceutical and Abilify. The Otsuka-BMS collaboration on aripiprazole, the antipsychotic sold as Abilify, follows the same territorial logic. Otsuka retained exclusive commercialisation rights in Japan, China, South Korea, and a set of other Asian markets, while granting BMS an exclusive license to commercialise the drug in the rest of the world.

The US and European revenues generated under the BMS license made Abilify one of the world's best-selling pharmaceuticals during its exclusivity period, with the royalty and profit-sharing payments to Otsuka from those ex-Japan revenues representing a significant portion of its income.

Eisai and Leqembi (lecanemab). More recently, Eisai presents a variation on this theme. Eisai obtained global rights to lecanemab from BioArctic in 2007 and subsequently structured its collaboration with Biogen such that Eisai serves as lead developer and regulatory applicant globally — including in Japan, where Leqembi received approval in September 2023.

This is an inversion of the classical structure: Eisai holds the global rights and manages the ex-Japan commercialisation itself. But the royalty layer is still present: BioArctic receives a high single-digit royalty on global Leqembi sales, flowing on revenues from the US, Japan, China, and every other approved market. As Leqembi sales grow — Eisai recorded JPY 18 billion in Q3 FY2025 alone, generating a 68% year-on-year increase in royalties paid to BioArctic — the royalty-eligible base expands across markets that are not individually subject to the NHI pricing cycle.

What this means for royalty investors. The pattern across these cases establishes a clear structural template. Japanese pharmaceutical companies routinely out-license ex-Japan rights and receive royalties from their Western partners' sales. The royalty streams those out-licenses generate are: denominated in USD, EUR, or GBP; governed by Western legal frameworks; not subject to Japan's NHI pricing regime; and backed by IP that is enforced in established court systems.

These are the characteristics that royalty investors evaluate when building a portfolio.

The gap that exists is not in the structure itself, which is proven and well-understood. The gap is in third-party royalty monetisation: the step where a Japanese pharmaceutical company holding an ex-Japan royalty receivable from a Western partner sells or pledges that future cash flow to a royalty investor in exchange for upfront non-dilutive capital.

From 2020 through 2024, royalty financings in biopharma totalled approximately $29.4 billion globally, more than double the amount of the preceding five-year period, with law firms active in the market noting increasing interest in Asian transactions specifically. Japanese pharma holders of ex-Japan royalty receivables are the natural next segment for that capital to reach — if the investors building the origination pipelines are willing to invest in the relationship infrastructure required.

What Is Actually Happening Right Now

Three sets of developments in the months immediately preceding March 2026 are shaping the Japan royalty landscape in ways that did not exist twelve months ago.

The Takeda-XOMA royalty restructuring. On December 30, 2025, XOMA Royalty and Takeda amended their long-standing collaboration through a strategic royalty-sharing transaction. Takeda's royalty and milestone payment obligations to XOMA Royalty related to mezagitamab were reduced, while XOMA Royalty received the right to payments based on low to mid-single-digit royalties and milestones across a basket of nine development-stage assets held within Takeda's externalized assets portfolio.

This is a significant data point: a major Japanese pharmaceutical company using royalty portfolio restructuring as an active capital-efficiency tool, trading reduced obligations on one asset for diversified exposure across nine programs. It confirms that Takeda — the most globally-oriented of Japan's large pharma companies — is a willing counterparty in sophisticated royalty transactions structured under Western law.

The Sumitomo Pharma "Boost 2028" announcement. On March 2, 2026, Sumitomo Pharma announced its "Boost 2028 — Accelerating Strong Sumitomo Pharma" growth strategy for FY2026 through FY2028. The company is targeting more than 350 billion yen in combined FY2028 sales from Orgovyx and Gemtesa, while also planning to raise 140 billion yen through a public offering. This follows a period of significant restructuring: Sumitomo divested its Asian business to a Marubeni subsidiary in 2025 to shore up the balance sheet.

A company rebuilding around two commercial-stage assets with disclosed revenue targets is precisely the profile that has attracted royalty monetization transactions in the US and European biotech context — known cash flows, defined asset risk, and management motivated to minimize equity dilution. The public offering path was chosen; the royalty monetization path was not. That comparison is itself informative.

The Kyowa Kirin-rocatinlimab discontinuation. On March 3, 2026, Kyowa Kirin announced the discontinuation of all ongoing clinical trials for rocatinlimab, an investigational anti-OX40 monoclonal antibody, following a safety review that identified emerging concerns of malignancies with possible viral or immune-related links.

The drug had met primary endpoints in Phase 3 atopic dermatitis trials and had been expected to move toward regulatory submission in the first half of 2026. One new confirmed case and an additional suspected case of Kaposi sarcoma were reported. This is not a royalty opportunity — it is the opposite. But it is relevant context: it illustrates the binary risk embedded in Japan-originated pipeline assets, and underscores why royalty investors targeting Japan need to focus on assets that have already cleared major clinical hurdles rather than pre-approval programs carrying unresolved safety risk.

The Legal and Structural Environment

One of the more underappreciated features of the Japan pharmaceutical royalty market, relative to its Chinese counterpart, is the quality of the legal infrastructure available to foreign investors.

In recent years, Japan has reached a significant turning point in its approach to patent litigation. The Japan Patent Office delivers high-quality examinations in a timely manner, with an average time from examination request to first office action of 9.4 months and average time to registration of just 13.8 months. Once granted, a patent is likely to withstand opposition or invalidation.

In May 2025, the IP High Court issued a judgment ordering two generic pharmaceutical companies to pay Toray Industries approximately JPY 21,762 million in a patent infringement case — notable both for its scale and for the court's clarification of the scope of patent protection during extended terms.

For royalty investors, this matters directly. A royalty stream tied to Japanese pharmaceutical revenues is backed by IP that is well-protected domestically and increasingly well-protected against international infringement.

There are no VIE structures to navigate, no questions about whether a contractual royalty interest is enforceable, and no capital repatriation approval required. Standard Western deal documentation — governed by New York or English law, with arbitration through ICC or JCAA — is established practice in transactions involving Japanese counterparties, and Japanese pharmaceutical companies have decades of experience executing cross-border licensing agreements under these frameworks.

The Emerging Startup Layer

The more forward-looking royalty opportunity in Japan is not in large-cap pharma, where Takeda and Daiichi Sankyo have sufficient capital access and self-manage their portfolio economics. The emerging opportunity is in Japan's biotech startup ecosystem, where government policy has shifted materially over the past three years.

The Japanese government has allocated JPY 350 billion (approximately USD 2.3 billion) to support startups, with AMED establishing a program to support biopharmaceutical startups developing patentable pharmaceuticals. AMED registers venture capital firms to provide hands-on support and funding: approved startups supported by a registered VC may receive grants up to double the VC's investment amount. AMED may provide grants up to JPY 6.7 billion per pipeline, with a total per-startup ceiling of JPY 10 billion. As of August 2025, 30 venture capital firms were registered with the program.

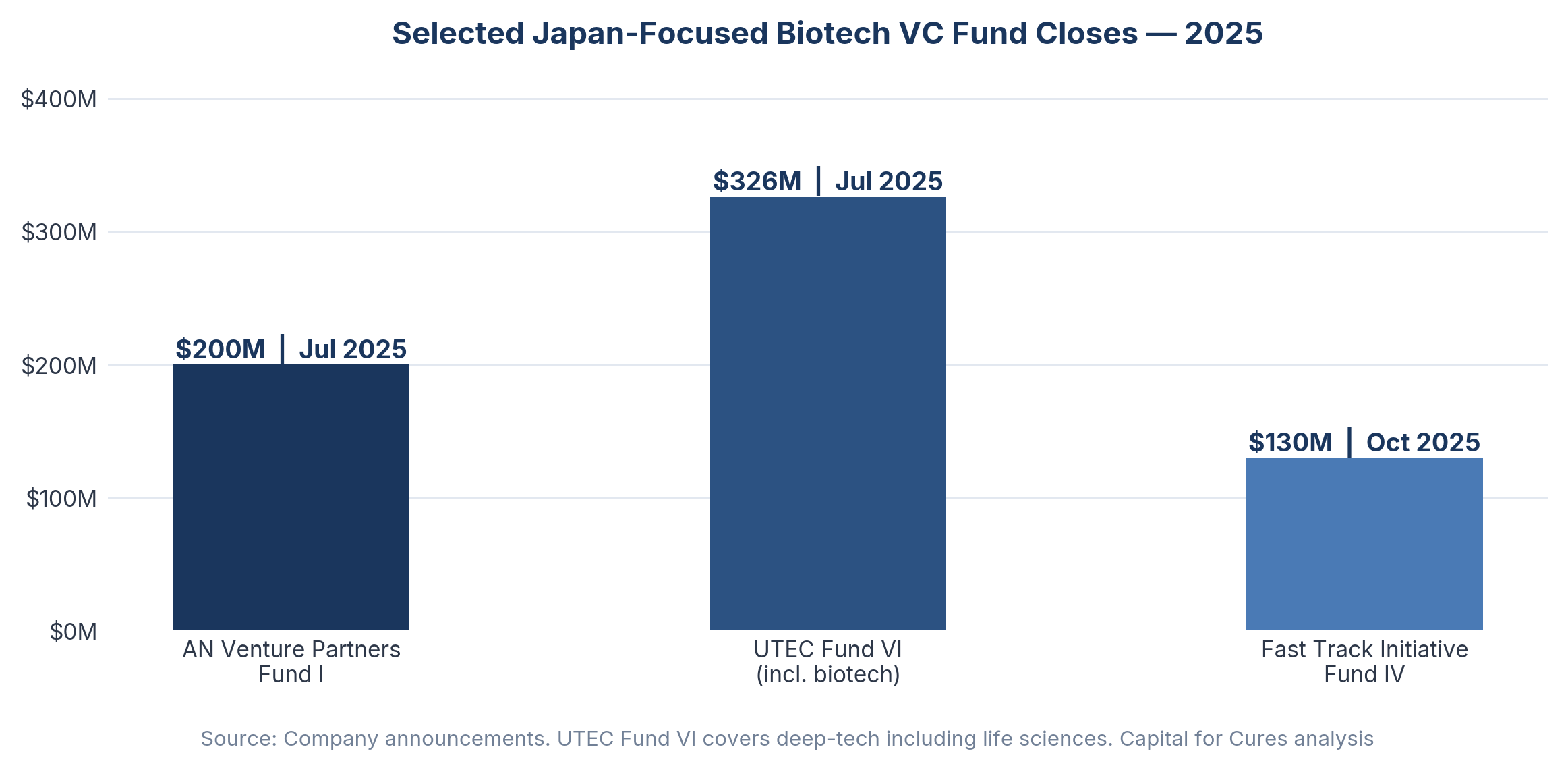

In July 2025, AN Venture Partners closed its first fund at $200 million, one of the largest Japan-focused biotech funds to date. In the same month, University of Tokyo Edge Capital Partners closed its sixth fund at approximately JPY 47 billion ($326 million), bringing its assets under management above $1 billion. Fast Track Initiative closed its approximately $130 million Fund IV in October 2025.

The key dynamic for royalty investors is this: the AMED program creates a pipeline of Japanese biotech companies with non-dilutive grant support through early clinical stages, registered VC investors already comfortable with Western-style deal structures, and assets that — if they reach Phase II or III — will need capital structures that equity alone cannot efficiently provide.

Japan's domestic IPO valuation ceiling, commonly around JPY 10–11 billion on the TSE Growth Market, can starve later clinical stages of capital. Royalty financing, which provides upfront non-dilutive capital against a proportion of future sales, is a natural complement to an ecosystem where equity valuations do not adequately price Phase III assets.

The Pricing Reform Wildcard

The biggest unknown in the Japan royalty market is whether the ongoing reform agenda delivers enough pricing stability to make domestic revenue streams materially more attractive to royalty investors.

Japan increased the number of annual opportunities to assign drug pricing from four to seven in 2025, designed to minimize the gap between approval and reimbursement. In February 2025, the MHLW also initiated a trial policy allowing companies to report certain post-approval manufacturing changes via annual summaries rather than immediate notifications.

The Sakigake pathway, offering a pricing premium of 10–20% for pioneering drugs with Japan-first development, has been accompanied by a newer "rapid introduction" premium of 5–10% for products launched simultaneously with or shortly after US or EU approval. Unlike Sakigake, there is no requirement for the drug to be filed first in Japan — only that Japanese clinical trials occur no later than in other markets.

The JPMA pressed Chuikyo for further reform: expanding the scope of allowable comparators for initial NHI price-setting, reviewing pricing methods for regenerative medicines that lack established comparators, and creating more stable price maintenance for on-patent innovative drugs.

The political appetite for reform is genuine — the government revised the Pharmaceutical and Medical Device Act in 2025 to expand the scope of the conditional approval scheme and introduced an incentive extending the maximum reexamination period for orphan drugs.

But the fiscal constraint is equally real. For royalty investors, the practical implication is that Japan domestic revenue streams remain subject to structural pricing risk that does not have a Western equivalent. The reforms are directionally positive for innovative drugs, but the repricing cycle has not been eliminated — it has been adjusted at the margins.

Modelling Japan domestic royalties requires building in a declining price curve for most assets, with specific carve-outs for drugs that maintain strong clinical differentiation and PMP eligibility across revision cycles. That modelling complexity is solvable, but it represents analytical investment that most Western royalty shops have not yet made.

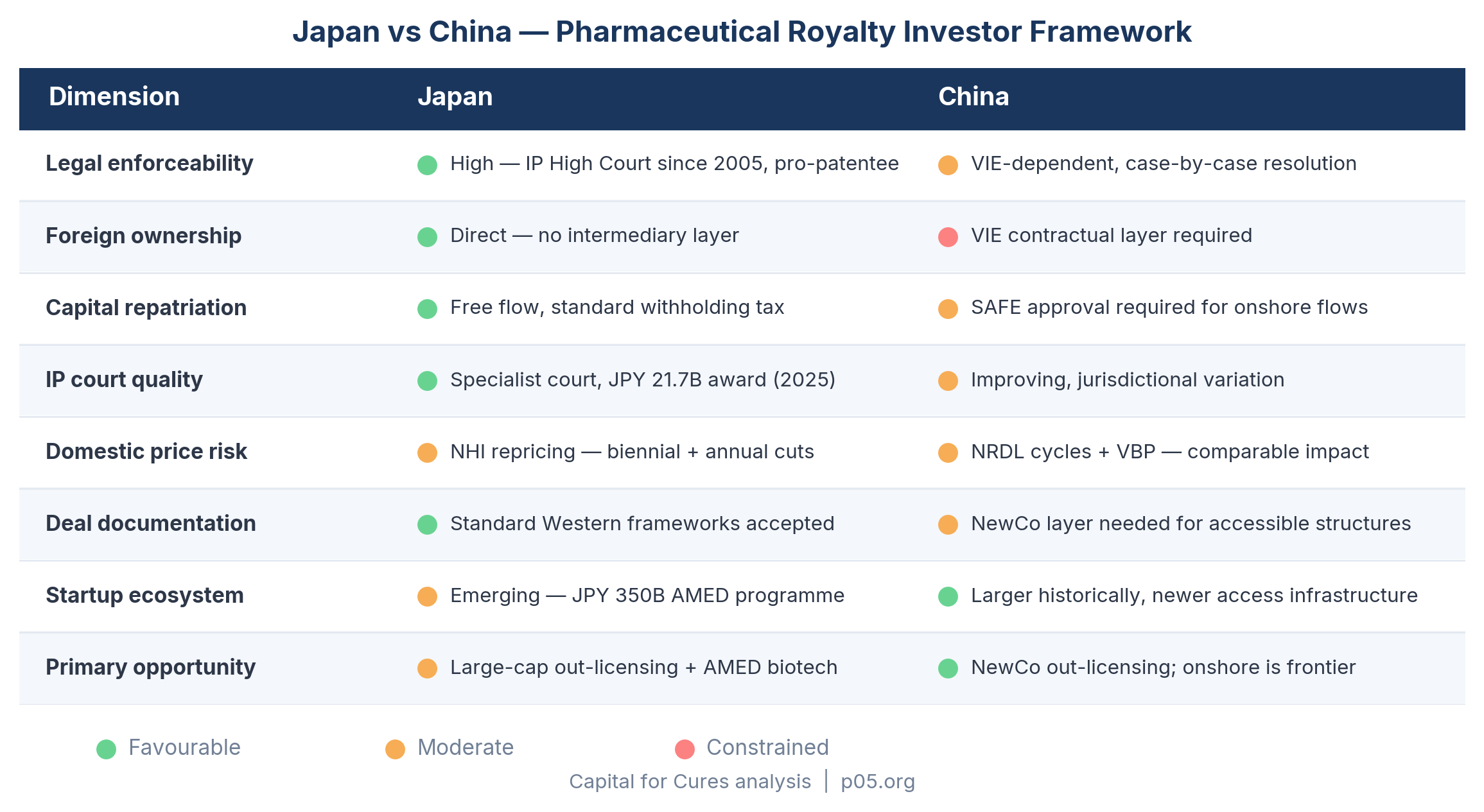

Comparative Framework: Japan vs China for Royalty Investors

| Dimension | Japan | China |

|---|---|---|

| Legal enforceability | High — established courts, specialist IP High Court since 2005 | Sector-dependent — VIE contractual architecture, case-by-case resolution |

| Foreign ownership structure | Direct — no intermediary layer required | VIE layer; no direct equity ownership of operating entity |

| Capital repatriation | Free flow, standard withholding tax | SAFE approval required for onshore royalty flows |

| IP court quality | Specialized, pro-patentee trend — JPY 21.7bn pharma damages award, May 2025 | Improving, but less consistent; jurisdictional variation |

| Domestic revenue price risk | Structural NHI repricing cycle — biennial/annual cuts | NRDL cycles, VBP exposure — different mechanism, comparable revenue impact |

| Deal documentation | Standard Western frameworks accepted | NewCo layer needed for accessible structures; onshore requires bespoke architecture |

| Startup ecosystem | Emerging — JPY 350bn AMED program, new dedicated VC funds | Larger historically, though access infrastructure is newer |

| Primary royalty opportunity | Large-cap out-licensing streams, emerging AMED-funded biotech | NewCo out-licensing; direct China onshore royalties are the frontier |

Where the Market Is Heading

The near-term Japan royalty opportunity is concentrated in three places.

The first is the stock of existing ex-Japan royalty receivables sitting on the balance sheets of Japanese pharmaceutical companies. The Ono-BMS, Shionogi-ViiV, and Otsuka-BMS precedents demonstrate that Japanese pharma has been generating these receivables for decades. What has been largely absent is the appetite — on both sides — to monetise them through third-party royalty financing.

A Japanese company holding a multiyear ex-Japan royalty stream on a commercial product can exchange a portion of future receipts for an upfront capital injection, with no equity dilution and no covenant package that interferes with its domestic operations. The analytical work required — modelling US or European revenue trajectories on disclosed products — is work that Western royalty investors already perform as their core competency.

The second is the externalized and commercial-stage assets of Japan's mid-tier pharmaceutical companies. Companies like Sumitomo Pharma, which is rebuilding around specific commercial assets and demonstrated willingness to use non-dilutive capital structures in its Asian business restructuring, are natural royalty monetization candidates.

The Takeda-XOMA transaction demonstrates that even large Japanese pharma companies use royalty restructuring as a portfolio management tool. For the mid-tier, where balance sheet pressure is greater and equity dilution more costly, the case for royalty monetization is stronger.

The third is the emerging Phase II/Phase III biotech cohort coming through the AMED program. These companies have government-matched capital through early clinical stages, VC investors comfortable with Western deal structures, and assets that will need late-stage development funding outside the AMED eligibility window. The domestic IPO market is not priced to support programs requiring $200 million or more for Phase III. Royalty monetization is.

The structural gap, as of March 2026, is not legal or financial infrastructure. It is origination: most Western royalty firms do not have the Japan-specific networks, language capacity, or pricing model depth to source and evaluate these transactions efficiently.

The firms that build those capabilities first — through dedicated Japan business development, relationships with AMED-registered venture capital firms, and Japan-specific revenue modelling that incorporates the NHI pricing trajectory — will have a structural origination advantage for a decade.

Royalty Pharma's Asia appointment is aimed primarily at China. Japan will be part of that mandate. But the Japan opportunity is likely to be led initially by mid-market royalty investors who can move faster on smaller transactions and who are prepared to invest in the relationship infrastructure that the largest firms have not yet built. The legal foundation is there.

The pipeline is assembling. What is missing is the capital and the deal teams willing to spend the time to learn the market.

All information in this article was accurate as of the research date (March 2026) and is derived from publicly available sources including company press releases, regulatory publications, legal analyses, and financial reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. I am not a lawyer or financial adviser.

Member discussion