Manufacturing Royalties vs. Sales Royalties: The CDMOs Entering the Royalty Space

When Fujifilm Diosynth Biotechnologies signed a 10-year, $3 billion manufacturing agreement with Regeneron in April 2025, the deal was widely reported as a milestone in U.S. biologics reshoring.

What received considerably less attention was its structural significance for the pharmaceutical royalty market: for the first time at that scale, a contract manufacturer had committed its entire new North Carolina facility to a single drug owner under a multi-decade economic partnership whose returns depend not on a fixed fee per batch but on the commercial trajectory of Regeneron's marketed biologics portfolio.

Fujifilm is not receiving a licence royalty. It is receiving something different — and that difference matters enormously to anyone structuring, financing, or investing in pharmaceutical cash flow streams.

The distinction between manufacturing royalties and sales royalties sits at a fault line that the pharmaceutical royalty financing community has so far treated as peripheral. It will not remain peripheral.

As CDMOs evolve from transactional batch processors into long-term economic partners of the drug companies whose products they produce, a new asset class is emerging — one that requires a distinct legal architecture, a different valuation methodology, and a fundamentally different risk framework from the royalties that Royalty Pharma, HCRx, DRI Healthcare, and XOMA have built billion-dollar franchises around.

This article examines the structural, legal, and financial anatomy of manufacturing royalties, maps the conditions that are pushing CDMOs into royalty space, and analyses what happens when the two royalty paradigms intersect in the same deal — as they increasingly will.

The Two Royalties Defined

Before examining where CDMOs fit, the foundational distinction must be stated precisely, because it is routinely conflated in commercial negotiations and occasionally obscured in legal drafting.

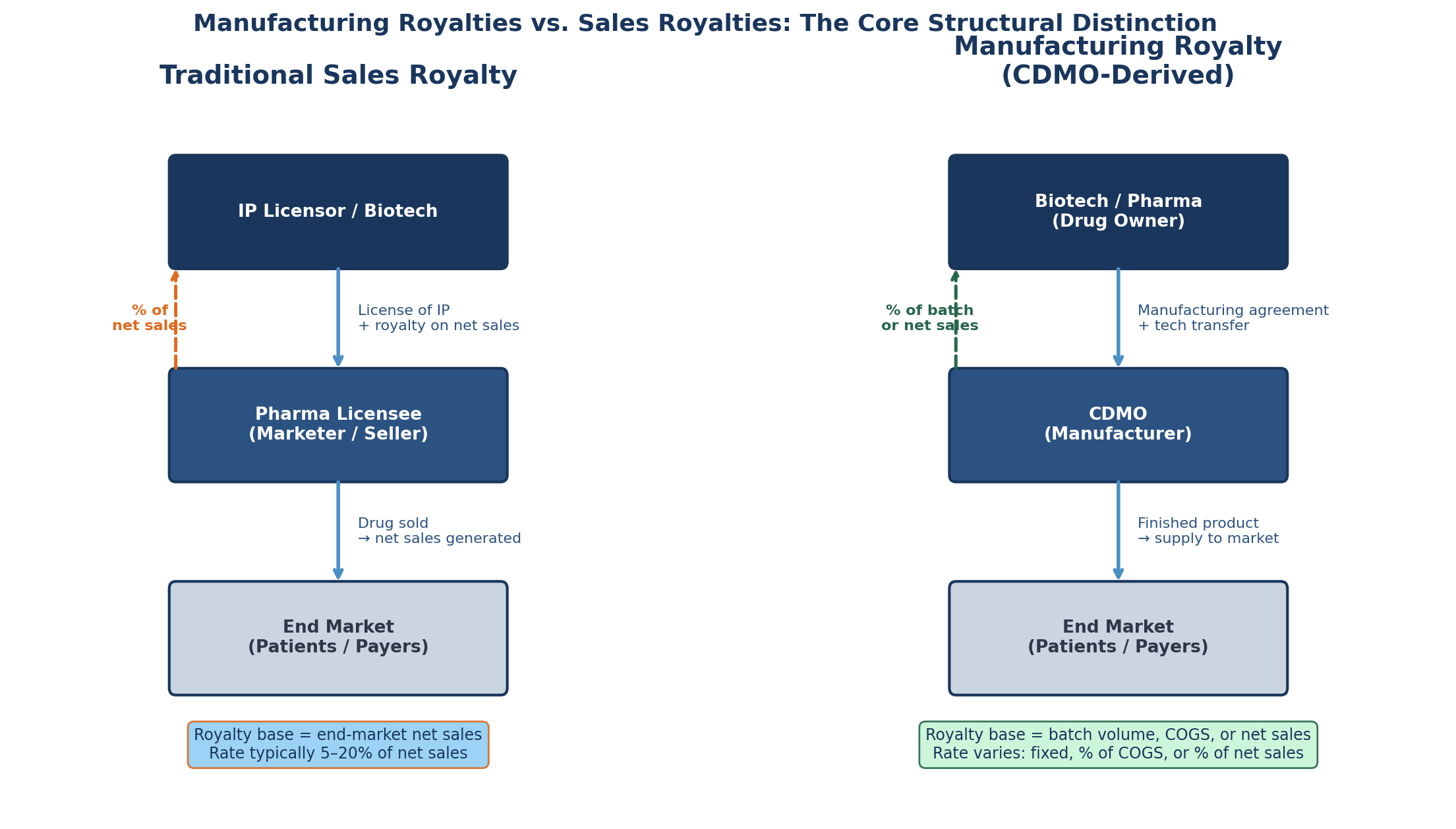

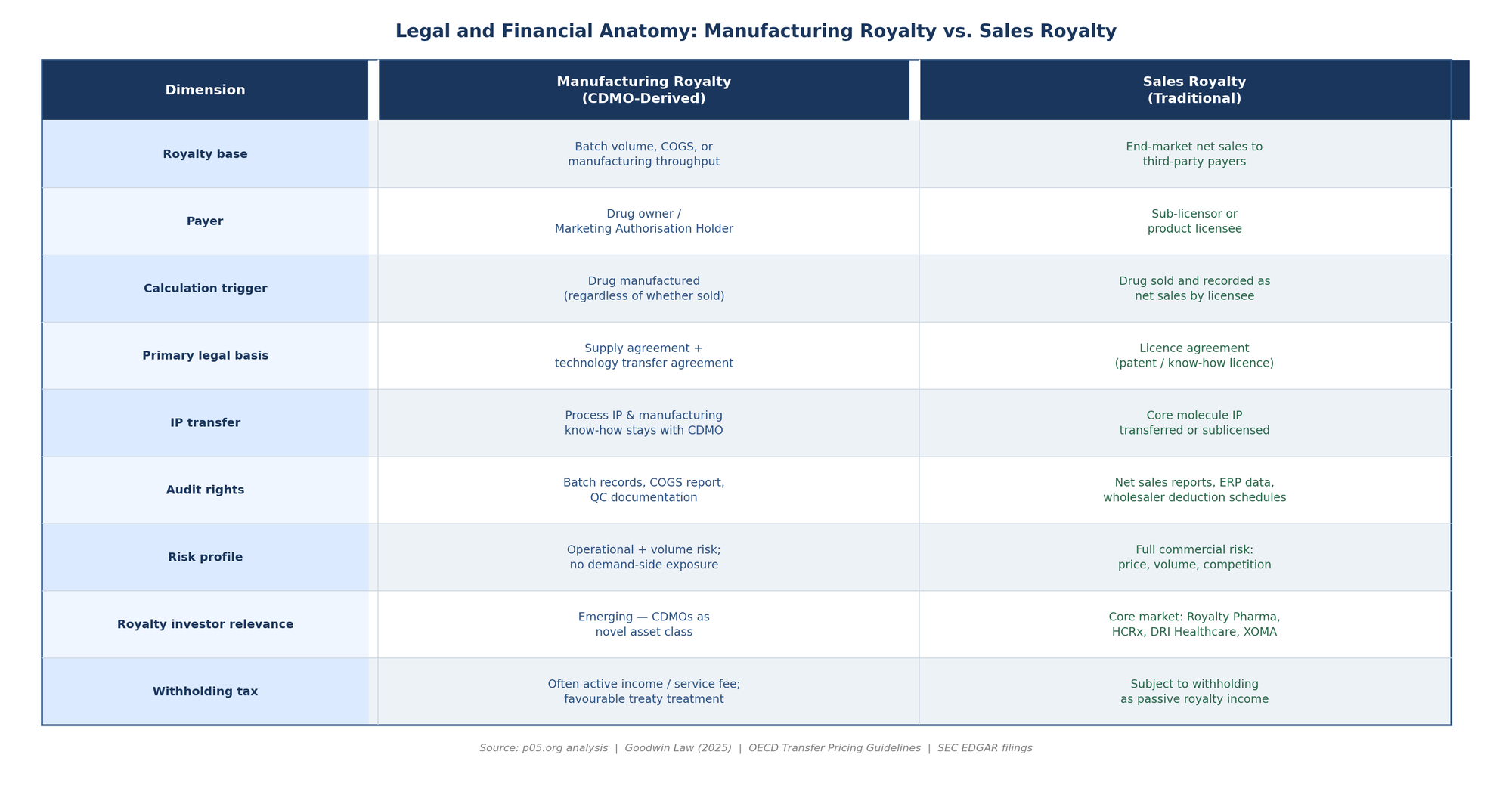

A sales royalty is a percentage of end-market net sales — the revenue that the marketing authorisation holder or its sub-licensee records when selling the finished drug to wholesalers, hospitals, pharmacy benefit managers, or patients. The royalty obligation is triggered by the act of selling the product. The payer is typically the licensee: the large pharma company that in-licensed the molecule from a biotech, or the biotech that received milestone and royalty terms in exchange for its compound.

The royalty base is calculated after contractually specified deductions — chargebacks, rebates, government price concessions, returns — applied to the invoice price to arrive at net sales. This is the territory of Royalty Pharma's synthetic royalties, HCRx's streaming agreements, and DRI Healthcare's university licensing monetisations. It is a well-mapped, deeply litigated, and increasingly efficiently priced market.

A manufacturing royalty is structurally different in almost every dimension. The payer is the drug owner — the party that holds the manufacturing rights and engages the CDMO. The royalty base is not net sales but some measure of the manufacturing relationship: the number of batches produced, the cost of goods of the manufactured product, or the gross or net revenue attributable to the units produced. Critically, the calculation trigger is the act of manufacturing rather than the act of selling.

A CDMO earning a manufacturing royalty receives payment when it produces the drug, not when a patient receives it or a payer reimburses it. The economic exposure is fundamentally different: the CDMO captures volume risk — whether its manufacturing slots are utilised at commercial scale — but in principle does not directly bear the downstream demand risk that a sales royalty investor takes on.

In practice, the boundary blurs. A CDMO that accepts a percentage of net sales in lieu of a manufacturing fee has effectively taken on a sales royalty position despite the manufacturing relationship that underlies it. This hybrid structure — manufacturing economics layered over a sales royalty base — is where the most interesting and most legally complex arrangements now sit.

Why CDMOs Are Moving Into Royalty Space

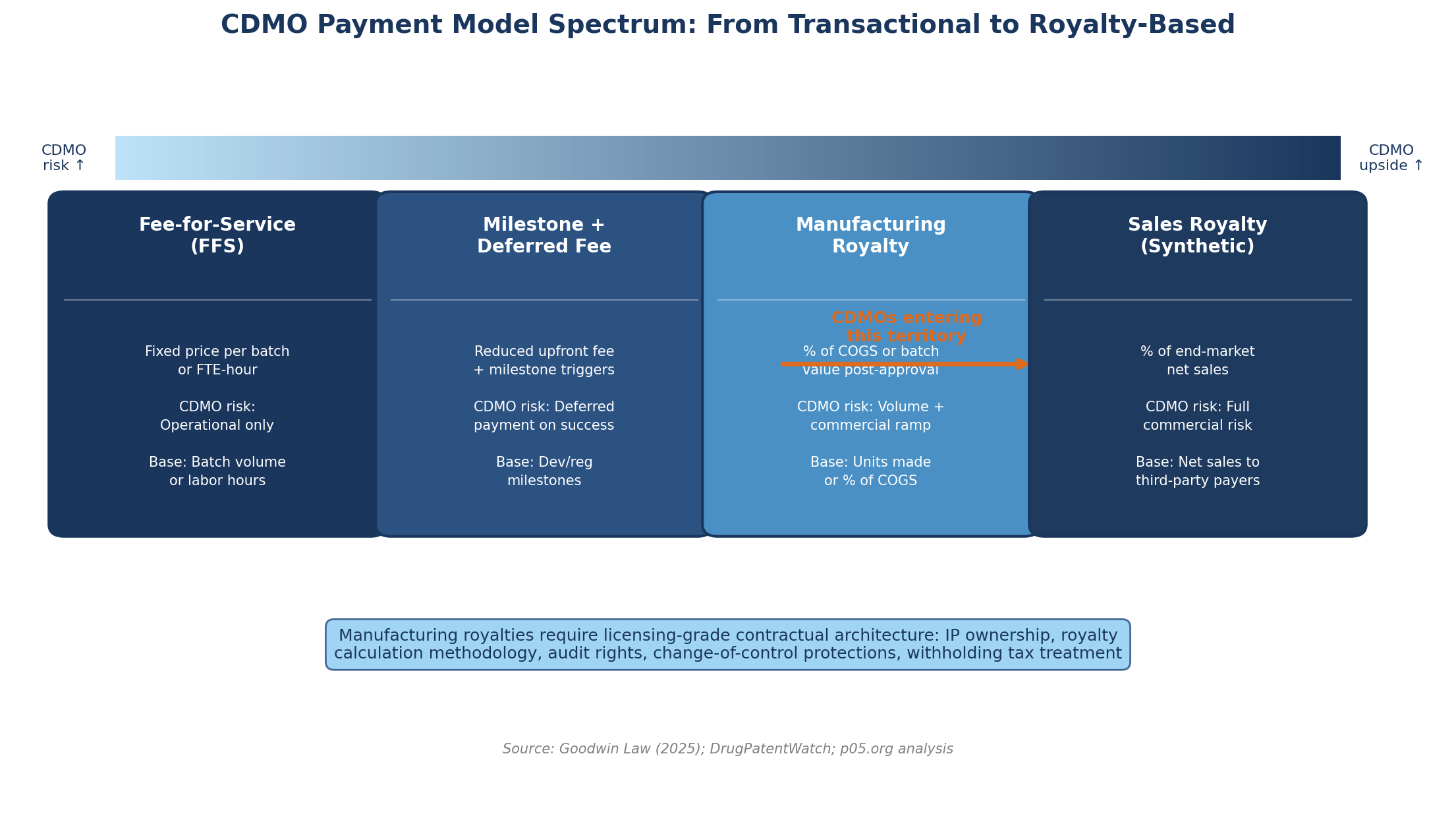

The forces pushing CDMOs from pure fee-for-service toward contingent and royalty-based compensation are structural, not cyclical. They reflect a convergence of capital pressure, competitive differentiation, and an evolving understanding of value creation that is reshaping the CDMO business model from the ground up.

The Biotech Funding Gap

The biotech funding environment of 2023 and 2024 — characterised by a sharp contraction in Series A and Series B rounds, near-zero IPO windows for preclinical assets, and a flight to quality among institutional investors — left a significant population of early-stage drug developers unable to meet their manufacturing obligations under conventional fee-for-service terms.

CDMOs with spare capacity and PE backing found themselves in a position to offer deferred fees, milestone-contingent payments, and ultimately royalty-based compensation in exchange for securing the manufacturing relationship and the long-term economics of commercial supply.

The Goodwin Law 2025 survey of CDMO-pharma partnerships, published in April, identified this precisely: private equity-backed CDMOs are "taking greater up-front risk for more favorable back-end economics" as smaller biotechs in capital-constrained conditions seek manufacturing partners willing to share the commercial gamble.

The legal team at Goodwin noted that these structures require "complex legal provisions more typically found in licence and collaboration agreements" — a clear signal that the contractual architecture of a manufacturing relationship is migrating toward royalty-agreement territory.

The Proprietary Platform Premium

A second driver is the increasing proprietary technology content that advanced CDMOs embed in their manufacturing services. A biologics CDMO that offers its own cell line development platform, its own process analytical technology suite, and its own manufacturing know-how is not simply providing commodity batch capacity — it is contributing intellectual property to the product's commercial success.

That contribution should, in theory, be compensated through a participation in the product's commercial economics rather than a fixed batch fee that underprices the IP contribution.

Samsung Biologics' ExellenS platform, WuXi Biologics' TrueSite TI and WuXiHigh 2.0 formulation technology, and Lonza's proprietary Ibex Dedicate cell line optimisation tools all represent CDMO-owned IP that is embedded in the manufacturing of specific approved products.

When a CDMO's proprietary process is so thoroughly intertwined with a product's manufacturing that the drug cannot be made anywhere else without significant redevelopment, the CDMO has de facto licensing power — and the economics of that power are most naturally expressed through a royalty rather than a batch fee.

Capital Intensity and Dedicated Build-Outs

The third driver is the extraordinary capital intensity of next-generation biologics manufacturing. Building a single commercial line for an antibody-drug conjugate now exceeds $200 million, with validation adding a further $20 million before first commercial batch. Lonza's CHF 500 million Ibex Dedicate ADC hub, Samsung Biologics' $2.1 billion Bio Campus IV, and Fujifilm's $7 billion global expansion programme represent capital commitments that no CDMO can responsibly make on the basis of a three-year fee-for-service contract.

Long-term manufacturing agreements with royalty or volume-linked economics provide the revenue certainty that justifies multi-billion-dollar facility investments.

As Goodwin observed, CDMOs are "increasingly passing capital expenditure costs to customer partners, creating a shared investment model" — but when the CDMO commits its own balance sheet to a dedicated build-out, it expects to participate in the product's success in proportion to its financial commitment.

The Legal Architecture: Why These Are Not the Same Contract

The practical importance of the sales royalty / manufacturing royalty distinction becomes most acute when lawyers sit down to draft the underlying agreement. The two royalty types emerge from different legal traditions and require substantially different contractual provisions.

The Governing Agreement

A traditional sales royalty arises from a licence agreement: the licensor transfers or sublicences patent rights, know-how, or both to the licensee, who pays royalties in exchange for the right to exploit the IP commercially. The OECD Transfer Pricing Guidelines and most national IP laws treat this as a passive income stream — the licensor has transferred economic risk to the licensee and is entitled to a participation in the commercial outcome.

A manufacturing royalty, by contrast, arises from a supply agreement or a technology transfer agreement layered onto the supply contract. The CDMO is not transferring IP to the drug owner — it is providing a service, retaining its own process IP, and receiving contingent compensation for that service. This is an active income stream tied to operational performance, not a passive royalty for rights transferred. The characterisation matters enormously for withholding tax, transfer pricing, and the bankruptcy treatment of the cash flow stream — issues explored below.

Royalty Base Definition

The single most consequential drafting decision in any manufacturing royalty agreement is the definition of the royalty base. Unlike a sales royalty agreement, where decades of practice have produced reasonably standardised "net sales" definitions (albeit still fiercely negotiated), manufacturing royalty agreements have no settled market standard. The base can be:

Cost of goods manufactured (COGM): the CDMO receives a percentage of the fully loaded cost of producing the drug, including raw materials, direct labour, overhead, and quality testing. This base aligns CDMO returns with manufacturing efficiency and rewards scale, but it can be gamed by the drug owner through allocation of overhead or by the CDMO through inflation of production costs.

Batch value or unit value: a fixed amount per unit produced or per batch completed. This is the simplest formulation but creates misaligned incentives if the commercial price of the drug changes dramatically after contract execution.

Net sales derived: the CDMO receives a percentage of the net sales that can be attributed to units it manufactured. This base provides the most direct participation in commercial success but imports all the complexity of net sales accounting — deductions, gross-to-net adjustments, geographic allocations, payor mix — into what began as a manufacturing relationship.

Each base carries different legal risks. A COGM-based royalty requires extensive cost accounting audit rights and transfer pricing analysis if the CDMO and drug owner are related parties or if the contract is later assigned. A net-sales-based manufacturing royalty may be characterised by tax authorities as a licence royalty subject to withholding rather than a service fee — with consequences for the drug owner's deductibility and the CDMO's net receipt.

Intellectual Property Provisions

A sales royalty agreement typically does not need to address the licensor's ongoing use of the underlying IP — the licensor has already transferred it. A manufacturing royalty agreement must address a series of IP ownership questions that do not arise at all in traditional royalty structures:

Who owns process improvements made by the CDMO during the commercial manufacturing term? If the CDMO develops a step-change improvement to the cell culture process that increases yield by 30%, does that improvement belong to the CDMO (as part of its proprietary manufacturing know-how) or to the drug owner (as an enhancement to the drug's manufacturing profile)? The answer affects both the CDMO's royalty base (higher yield means more units produced, potentially increasing the royalty if the base is volume-linked) and the drug owner's ability to switch CDMOs at the end of the term.

Who has the right to grant sub-licences of the manufacturing know-how? If the drug is approved in a territory where the CDMO does not operate, and a third-party manufacturer needs a technology transfer, who controls and prices that transfer? These questions are routine in licence agreements but genuinely novel in the context of a manufacturing royalty structure.

As Goodwin noted, "ownership of intellectual property (IP) will need to be clearly delineated as CDMOs participate in critical product development work and, in many cases, contribute their own proprietary technology to product development" — a drafting priority that existing CDMO master service agreement templates are not designed to address.

Audit Rights

Traditional royalty agreements grant the licensor the right to audit the licensee's books to verify net sales. In a manufacturing royalty arrangement, the audit rights run in both directions and cover a broader range of data: the drug owner wants to verify the CDMO's COGM calculations or the accuracy of batch records that determine volume-based royalties; the CDMO wants the right to audit net sales records if its compensation is linked to commercial outcomes it has no ability to control.

The audit right architecture in a manufacturing royalty agreement is consequently more complex than in a traditional licence: it must cover GMP batch records, quality control data, supply chain documentation, and — if the base is net-sales-linked — all the standard sales royalty audit provisions. Getting this right at the contract drafting stage is not a peripheral concern. It is the mechanism through which disputes about royalty underpayment are ultimately resolved.

The Intersection Problem: When Both Royalties Attach to the Same Product

The most legally and financially complex scenario arising from CDMO entry into royalty space is not simply a CDMO-pharma manufacturing royalty in isolation. It is the situation where a traditional sales royalty (held by a royalty investor such as Royalty Pharma or DRI Healthcare) and a CDMO manufacturing royalty both attach to the same product's commercial economics.

Consider the following structure, which is increasingly plausible as both phenomena mature simultaneously:

A mid-sized biotech discovers a GLP-1 analogue. It licences manufacturing rights to a biologics CDMO that contributes significant process development and accepts a deferred net-sales-linked manufacturing royalty of 1.5% in lieu of upfront batch fees. The biotech then licences the commercial rights to a large pharma company on standard terms — 15% sales royalty, escalating tiered.

The biotech, now holding both a traditional royalty stream (from the large pharma licensee) and an obligation to pay a manufacturing royalty (to the CDMO), monetises the inbound royalty stream by selling a percentage of it to a royalty fund. The royalty fund acquires a claim on the large pharma net sales royalty. The CDMO retains its separate manufacturing royalty claim.

Both claims — the royalty fund's and the CDMO's — are economically dependent on the same product's commercial success. But they are legally structured from entirely different positions in the pharma value chain, governed by different agreements, denominated against different bases, and held by parties with different enforcement rights.

Priority and Waterfall

In the event that the drug owner becomes financially distressed, the priority of the manufacturing royalty claim versus the sales royalty claim becomes critical.

A traditional sales royalty that has been properly structured as a true sale — with the royalty stream conveyed to the investor as a present ownership interest rather than a future payment obligation — sits outside the drug owner's bankruptcy estate under the jurisprudence reaffirmed by Covington's 2024 analysis of royalty monetisation structuring. The royalty fund's claim, if properly isolated, survives the drug owner's insolvency.

However, the In re Mallinckrodt Third Circuit ruling of 2024 confirmed that royalty obligations not tied to an IP licence are dischargeable unsecured claims in bankruptcy — a holding that cuts directly against CDMOs whose manufacturing royalty is structured as a contingent fee rather than a property interest in the IP stream.

If the drug owner rejects the manufacturing contract, the CDMO loses its royalty stream and is left with a general unsecured damages claim for the lost future royalties, discounted to present value, subordinated to secured creditors.

The structuring implication is that CDMOs accepting net-sales-linked manufacturing royalties should demand collateral assignment of the royalty stream, change-of-control protections analogous to those in senior royalty investor agreements, and step-in rights that allow them to assume control of the supply relationship (and potentially the royalty claim) in the event of the drug owner's default.

Withholding Tax Asymmetry

Cross-border royalty payments attract withholding tax under most bilateral tax treaties — typically at rates of 5–15% for passive royalties. Fee-for-service manufacturing payments are generally treated as active business income of the CDMO's jurisdiction, not subject to royalty withholding.

A manufacturing royalty that is drafted with a net-sales-based royalty base and governed by a document that uses the word "royalty" throughout risks reclassification by a source-country tax authority as a passive royalty payment subject to withholding — even if the underlying relationship is genuinely one of manufacturing services.

The economic consequences for a CDMO receiving a 1.5% royalty on $2 billion of annual net sales ($30 million) could include a $4.5 million annual withholding cost (at a 15% treaty rate) that was not priced into the original transaction.

Tax counsel drafting CDMO manufacturing royalty agreements should prioritise the active income characterisation at every level: the governing agreement should be a supply agreement, not a licence; the compensation should be defined as a "contingent manufacturing fee" rather than a royalty; and the CDMO should not transfer any IP rights — even process know-how — as part of the transaction, since IP transfer is a key indicator of passive royalty characterisation under BEPS Action 8-10 guidance.

Benchmarking: What Rate Is Arm's Length for a Manufacturing Royalty?

The royalty valuation discipline faces a significant gap when asked to benchmark manufacturing royalties. The comparables databases — RoyaltyRange, RoyaltyStat, Dealogic — are populated almost entirely with sales royalties: licensing deals between innovators and commercial licensees. There are almost no publicly disclosed transactions in which a CDMO has received a percentage of net sales or a percentage of COGS as compensation for a long-term manufacturing commitment.

This creates a genuine challenge for both commercial negotiation and transfer pricing compliance. If a CDMO and a biotech agree on a 2% net-sales-linked manufacturing royalty, what is the arm's-length benchmark? The parties must construct one from adjacent evidence:

Third-party royalty financing transactions provide indirect evidence. When Royalty Pharma acquires a 7.5% synthetic royalty on a marketed biologic for $2 billion, and DRI Healthcare pays $100 million for a royalty of 8–10% on a clinical-stage asset, these transactions represent genuine negotiations between unrelated parties over the value of pharmaceutical cash flows.

A manufacturing royalty at 2% of the same net sales is economically equivalent to approximately 27 cents on the dollar of the full royalty — a ratio that should reflect the CDMO's contribution to the product's value relative to the licensor's IP contribution. If the CDMO's process innovations genuinely account for 15–25% of the product's commercial value (a plausible range for highly complex biologics where manufacturing is the rate-limiting constraint), a 2% manufacturing royalty against a 7.5% sales royalty is arguably underpriced.

Comparable manufacturing agreements with volume escalators offer a different benchmark. Lonza's Ibex Dedicate dedicated facility arrangements and Samsung's long-term supply contracts contain price-per-batch structures with volume-linked escalation. If these can be reverse-engineered as effective royalties on the commercial value of units produced, they provide COGM-based comparables that neither party has incentive to disclose.

DEMPE analysis (Development, Enhancement, Maintenance, Protection, Exploitation) is now required under BEPS Actions 8-10 for intercompany manufacturing royalties — and its logic applies equally to arm's-length negotiations. A CDMO that contributes genuine Enhancement functions (process optimisation, scale-up of a novel modality) and Maintenance functions (ongoing GMP compliance, process analytical technology) is performing DEMPE activities that deserve a share of residual profit, not merely a routine service return.

| Royalty Type | Typical Rate Range | Base | Key Driver |

|---|---|---|---|

| Sales royalty — preclinical | 3–4% | Net sales | IP risk premium |

| Sales royalty — Phase II | 12–15% | Net sales | Clinical de-risking |

| Sales royalty — approved | 15–25% | Net sales | Market exclusivity |

| Manufacturing royalty — COGM | 5–12% | COGM | Operational complexity |

| Manufacturing royalty — net sales | 0.5–2.5% | Net sales | Volume + IP contribution |

| Milestone + deferred fee hybrid | Varies | Batch + milestone | Funding gap coverage |

Sources: DrugPatentWatch; Goodwin Law (2025); p05.org analysis. Manufacturing royalty ranges are estimated; limited publicly disclosed comparables exist.

The Major CDMOs: Where Each Sits on the Spectrum

The five largest biologics CDMOs — Lonza, Samsung Biologics, Fujifilm Diosynth, Thermo Fisher (Patheon), and Catalent (now Novo Holdings) — are at different points in the transition from pure fee-for-service toward contingent and royalty-based compensation, driven by their ownership structures, capital positions, and client base characteristics.

Lonza, the world's largest pure-play CDMO by mammalian bioreactor capacity at approximately 660,000 litres following the Roche Vacaville acquisition, has pursued a dedicated capacity model — Ibex Dedicate — in which clients co-invest in facility construction in exchange for manufacturing priority and pricing protections.

This is a capital-sharing structure rather than a royalty structure, but it creates the long-term economic entanglement that, if the drug succeeds at scale, converges toward manufacturing royalty economics. Lonza's CHF 500 million ADC hub exemplifies the model: if the ADC therapeutics sector performs as the consensus forecasts — commercial ADC revenues projected to exceed $30 billion by 2030 — Lonza's dedicated facilities will capture a disproportionate share of manufacturing economics.

Samsung Biologics, which signed $1.41 billion and $1.24 billion contracts in January and October 2024 respectively and now holds supply agreements with 17 of the top 20 global pharma companies, operates primarily on long-term fee-for-service terms with volume escalators. Its Bio Campus IV expansion, representing a $2.1 billion investment in 180,000 litres of additional mammalian capacity, is funded by committed order books rather than royalty streams.

Samsung is not yet in manufacturing royalty space, but its sheer scale and the concentration of its client portfolio creates the leverage to demand royalty-adjacent participation in the economics of its most critical programmes.

Fujifilm Diosynth, with the Regeneron $3 billion 10-year deal as its landmark anchor, is arguably the CDMO furthest into long-term manufacturing partnership territory. The Regeneron agreement is structured as a supply agreement rather than a royalty, but its 10-year horizon, dedicated facility commitment, and strategic importance to Regeneron's U.S. reshoring narrative create an economic alignment that resembles manufacturing royalty economics even if the legal form does not yet carry that label.

Thermo Fisher (Patheon), through its late 2024 "Accelerator Drug Development" integration of its CRO and CDMO businesses under a single outsourcing offering, is pursuing the most aggressive strategic pivot: capturing clients from preclinical development through commercial manufacturing under contracts that span the entire drug development lifecycle.

A CDMO that is present at the inception of a programme and provides both development and manufacturing services is in the strongest possible position to negotiate royalty-based participation — having shared the development risk, it has a legitimate claim to share the commercial upside.

Catalent, following its $16.5 billion acquisition by Novo Holdings in 2024, sits in a unique position: it is now a captive CDMO for Novo Holdings' pharmaceutical portfolio while simultaneously competing for third-party contracts. The extent to which Novo Holdings will allow Catalent to take royalty-linked economics from third-party clients — creating economic interests potentially adverse to Novo Holdings' own competitive position — is an open question that will define Catalent's strategy over the next cycle.

The Royalty Investor's Perspective: A New Asset Class or a New Risk?

For traditional pharma royalty investors, CDMOs entering royalty space presents both an opportunity and a structural threat.

The opportunity is product diversification. A royalty stream whose source is a CDMO's manufacturing relationship has a different risk profile from a traditional IP licence royalty. The CDMO's royalty does not depend on the licensor's continued patent ownership — the manufacturing relationship continues regardless of patent expiry if the drug owner retains sole reliance on the CDMO's proprietary process. A CDMO manufacturing royalty can, in principle, survive the loss of patent exclusivity because the value it captures is the manufacturing know-how, not the IP.

The structural threat is priority dilution. If a drug owner has committed a net-sales-linked manufacturing royalty to its CDMO, that obligation reduces the economic value available to a traditional royalty investor acquiring a claim on the same net sales. A 2% manufacturing royalty and a 15% sales royalty against the same product creates an aggregate burden of 17% of net sales — a level that may not be supportable for smaller molecules or products in highly competitive markets where net profit margins are compressed.

Traditional royalty investors acquiring interests in drugs manufactured by royalty-bearing CDMOs must now conduct manufacturing royalty due diligence alongside the clinical, patent, and commercial diligence that is already standard. The key questions mirror those in transfer pricing analysis: which entity in the value chain holds which economic claim, what is the priority of each claim in the event of financial distress, and does the aggregate burden of royalty obligations reduce the available cash flow to a level that impairs the investment thesis?

Legal Framework for the Emerging Class

Several contract provisions are essential in any well-structured manufacturing royalty agreement. Their absence in early-generation manufacturing royalty deals will generate the same category of disputes that plagued early synthetic royalty agreements before the market standardised around Royalty Pharma's documentation templates.

Anti-assignment and step-in rights: the CDMO's royalty interest should survive any assignment of the drug owner's marketing rights, merger, or acquisition of the drug owner by a larger entity. Without an explicit anti-assignment clause, a drug owner acquired by a large pharma with its own manufacturing infrastructure could terminate the CDMO supply relationship and extinguish the royalty stream by bringing manufacturing in-house. This mirrors the change-of-control protections already standard in senior royalty investor agreements.

Technology transfer restrictions: the CDMO should have contractual control over technology transfer to any successor manufacturer. If the drug owner seeks to dual-source manufacturing at a competitor CDMO, the original CDMO's process know-how should not be transferable without consent and without compensation — typically structured as a lump-sum technology transfer fee or an ongoing sub-royalty to the originating CDMO.

Net sales reporting and gross-to-net protections: if the manufacturing royalty base is net-sales-linked, the drug owner should be required to provide quarterly net sales reports with the same level of detail as a commercial licence agreement. The CDMO should retain audit rights over the drug owner's gross-to-net deduction schedules, which are the primary mechanism through which net sales royalty bases erode over a product's commercial lifecycle.

Withholding tax mechanics: cross-border manufacturing royalties must include a gross-up provision requiring the drug owner to pay additional amounts if a source-country tax authority imposes withholding on the manufacturing fee — whether classified as a royalty or not. Without a gross-up, the CDMO bears an unexpected tax cost that was not priced into the original economic arrangement.

Bankruptcy remoteness: the manufacturing royalty stream, if large enough to justify the structuring cost, should be isolated in a bankruptcy-remote special purpose vehicle or secured through a collateral assignment of the royalty obligation. Following In re Mallinckrodt, and as Covington's annual synthetic royalty study confirms, no unsecured royalty financing by a public biotech has come to market since December 2022 — a market-wide signal that the CDMO community would do well to internalise before the first major manufacturing royalty default arrives.

The Road Ahead

The convergence of three forces — CDMO capital intensity requiring long-term revenue certainty, biotech funding constraints creating willingness to offer royalty-linked compensation, and a mature royalty investor community capable of pricing and financing these cash flows — will produce a generation of manufacturing royalty transactions over the next five years.

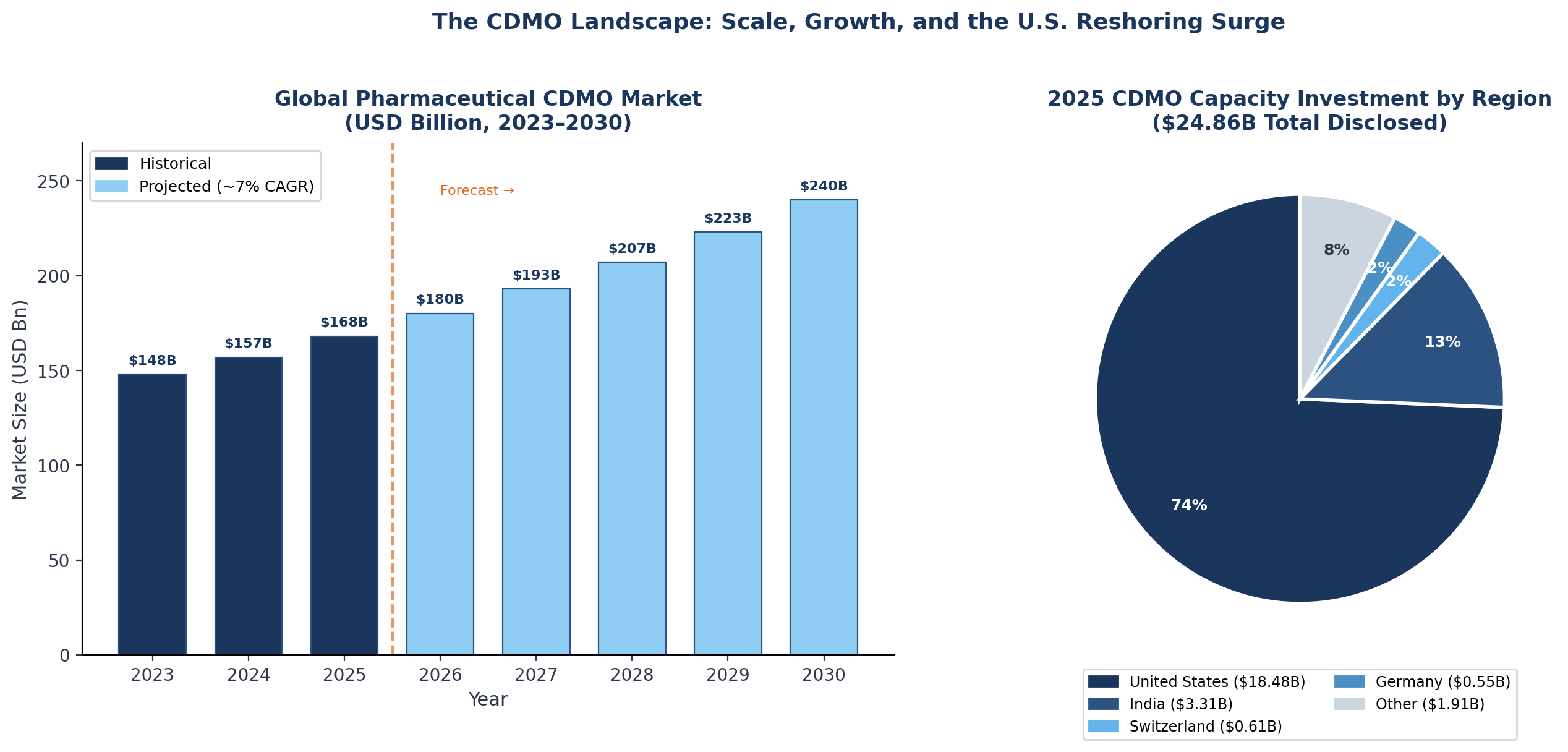

Total disclosed CDMO capacity investment reached $24.86 billion in 2025 alone, with 74% flowing to the United States — a scale of commitment that simply cannot be recouped on fee-for-service economics over any reasonable payback horizon.

The question is whether the legal and financial infrastructure will keep pace. Sales royalty agreements have been standardised through decades of negotiation, litigation, and investor community pressure into documentation that, while still negotiated intensively, has a settled architecture.

Manufacturing royalty agreements are still in the discovery phase: the royalty base definitions are unstandardised, the priority analysis in distressed scenarios is untested, and the transfer pricing treatment of COGM-based royalties is genuinely uncertain under BEPS-era guidance.

For the pharmaceutical royalty community — investors, bankers, lawyers, and the drug companies who are both payers and recipients of royalty streams — the emergence of manufacturing royalties from CDMOs is neither a threat to the existing market nor merely an incremental addition to it. It is a structural change to who sits in the royalty chain and on what basis they assert their economic claim.

The lawyers drafting these agreements and the investors acquiring interests in royalty-bearing products will spend the next decade working out the implications. The CDMOs, for their part, have already decided that the fee-for-service model does not adequately compensate them for what they actually contribute. They are right about that. The rest of the industry now needs to develop the frameworks to accommodate them.

All information in this article was accurate as of March 2026 and is derived from publicly available sources including company announcement and SEC filings. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, tax, or financial advice. The author is not a lawyer, tax adviser, or financial adviser.

Member discussion