Patent Challenges and Royalty Survival: Invalidation Risk, Contractual Defences, and the Royalty Investor's Dilemma

When a generic manufacturer files a Paragraph IV certification against an Orange Book-listed patent, or when a hedge fund petitions the PTAB for inter partes review of a composition-of-matter claim, the immediate question for every royalty holder in the capital stack is existential: does the royalty survive?

The answer is not "yes" or "no." It is "it depends on what the royalty is actually on" — and that distinction, between a royalty anchored to a patent right and a royalty anchored to a contractual obligation with non-patent consideration, is the central structural question in pharmaceutical royalty financing today. It determines whether a patent challenge is a valuation haircut or a terminal event, and it shapes how royalty purchasers, securitisation vehicles, and synthetic royalty counterparties price the single largest non-clinical risk in their portfolios.

What follows is the expert-level anatomy of how patent challenges interact with royalty payment obligations: the legal mechanisms through which patents are attacked, the contractual architectures that determine whether royalties survive invalidation, the jurisdictional divergences that make the same royalty stream robust in one market and fragile in another, and the practical implications for royalty investors conducting diligence on assets where the patent cliff is not a date on a calendar but a litigation probability.

The challenge landscape: four vectors of patent attack

Patent challenges in pharmaceuticals do not arrive through a single channel. They come through at least four distinct procedural mechanisms, each with different timing, burden of proof, and consequence profiles. Understanding the vector matters because each creates a different risk topology for the royalty holder.

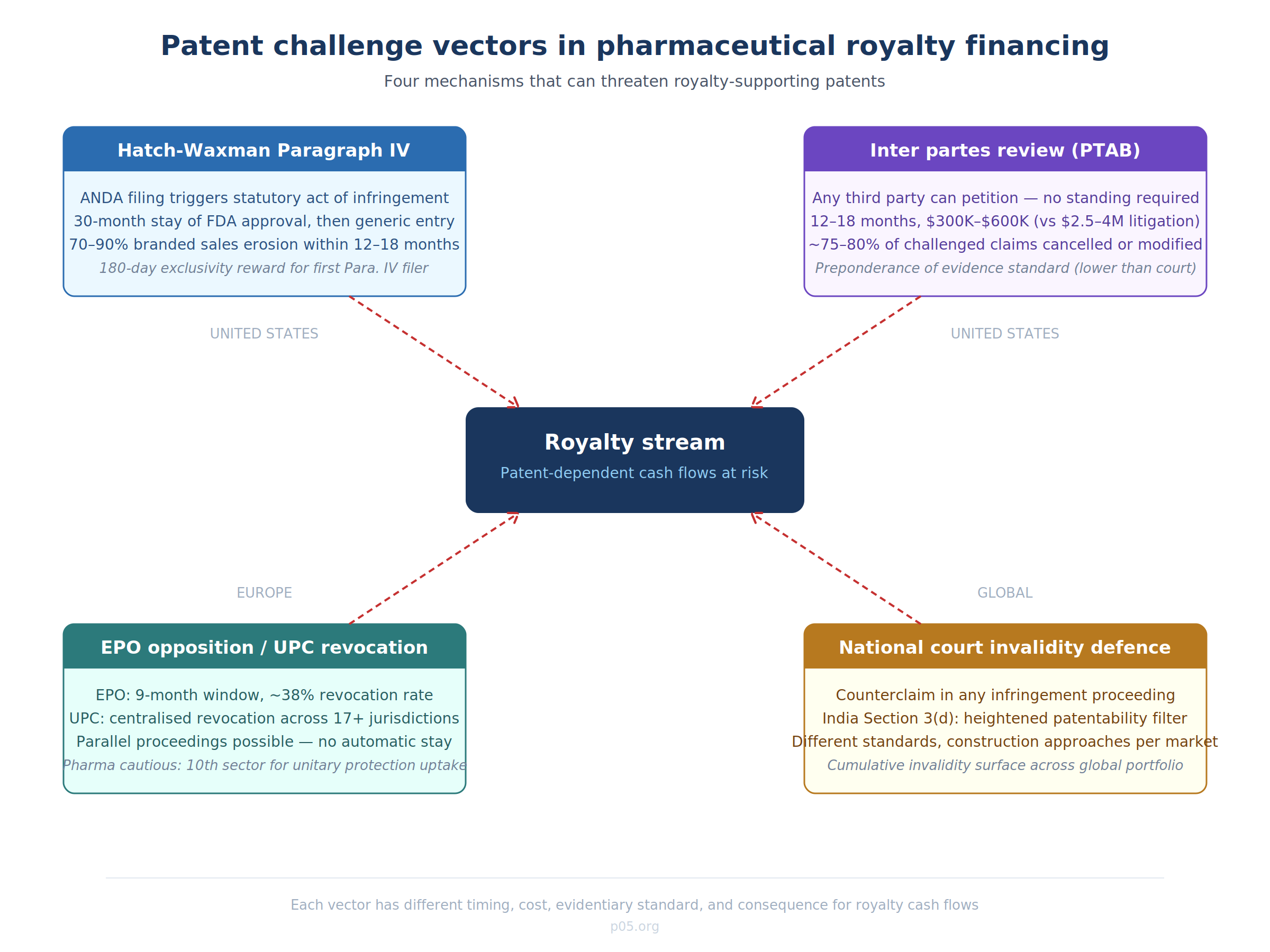

Hatch-Waxman Paragraph IV certification (United States)

The Hatch-Waxman Act created a system in which a generic manufacturer can seek FDA approval for a generic drug before the expiration of patents listed in the Orange Book by filing an Abbreviated New Drug Application containing a Paragraph IV certification — a formal assertion that the listed patent is invalid, unenforceable, or will not be infringed by the generic product. The filing itself is treated as a statutory act of patent infringement, allowing the brand-name company to sue before any generic product reaches the market.

If the patent holder sues within 45 days of receiving notice, FDA approval of the generic is automatically stayed for 30 months (or until a court rules on validity/infringement, whichever comes first). The first generic filer that successfully challenges a patent earns a 180-day period of marketing exclusivity — a prize that can be worth hundreds of millions of dollars — which is precisely why Paragraph IV challenges are so aggressively pursued.

For royalty holders, the Paragraph IV mechanism creates a specific timeline of risk. The 30-month stay provides a buffer, but a court finding of invalidity or non-infringement terminates the stay immediately and opens the door to generic competition. Once generics enter, the branded drug's net sales typically decline by 70–90% within 12–18 months. If the royalty is calculated as a percentage of net sales of the branded product, that revenue erosion is catastrophic and essentially irreversible.

The frequency is not trivial. Paragraph IV challenges are a routine feature of the US pharmaceutical market: for any branded drug with significant commercial value, multiple ANDA filers will typically submit Paragraph IV certifications, often within the first year of a patent's listing in the Orange Book.

Inter partes review at the PTAB (United States)

The America Invents Act of 2011 introduced inter partes review, a proceeding before the Patent Trial and Appeal Board that allows any third party (not just generic manufacturers) to challenge the validity of issued patent claims on grounds of anticipation or obviousness, using patents and printed publications as prior art. The standard is preponderance of the evidence — substantially lower than the "clear and convincing evidence" standard applied in federal district court litigation — and the PTAB applies the broadest reasonable interpretation of claims.

The statistics are sobering for patent holders. IPR proceedings are typically resolved within 12–18 months at a cost of $300,000–$600,000, compared to multi-year district court litigation costing $2.5–$4 million or more. Historically, approximately 75–80% of patents challenged via IPR have had claims cancelled or modified. Although pharmaceutical patents have been somewhat more resilient than technology patents in IPR proceedings, the mechanism remains a potent weapon.

The Kyle Bass episode illustrated the strategic breadth of IPR as a tool. Bass's Coalition for Affordable Drugs challenged patents held by 28 pharmaceutical companies through IPR petitions, claiming a goal of invalidating weak patents. The pharmaceutical industry alleged the challenges were designed to enable short-selling of stock. Regardless of motive, the episode demonstrated that IPR standing requirements are minimal — any person who is not the patent owner can file, and there is no requirement of commercial interest in the relevant drug market.

For royalty investors, IPR risk is structurally different from Hatch-Waxman risk. A Paragraph IV challenge is linked to a specific generic entry pathway and comes with regulatory timing mechanics. An IPR petition can be filed by anyone, at (almost) any time after nine months from patent grant, and can invalidate claims that are essential to the royalty-supporting patent portfolio without any connection to generic entry. The proposed 2026 USPTO rule changes — which would create a "one-and-done" system where patents surviving any initial IPR challenge become nearly immune from subsequent proceedings — would materially change this risk profile if adopted, particularly benefiting branded pharmaceutical companies.

EPO opposition and the new UPC revocation pathway (Europe)

In Europe, any member of the public (except the patent holder) can file an opposition with the European Patent Office within nine months of publication of the patent grant. The grounds include lack of novelty, lack of inventive step, insufficient disclosure, and added subject matter. In 2023, the EPO received approximately 3,500 opposition filings; roughly 38% of opposed patents were revoked entirely, 32% were maintained in amended form, and 30% were upheld unchanged. These are not negligible odds for the patent holder.

The Unified Patent Court, operational since June 2023, has introduced a new dimension. The UPC has jurisdiction over European patents (both unitary patents and traditional bundle patents that have not been opted out) across participating member states, and it can hear standalone revocation actions as well as infringement counterclaims. The critical innovation is centralised revocation: a single successful revocation action at the UPC invalidates the patent across all participating jurisdictions simultaneously. Previously, challengers had to attack national designations of European patents country by country.

Pharmaceutical companies have been notably cautious about the UPC. The sector ranks only tenth overall for requests for unitary patent protection, reflecting wariness about exposing high-value assets to centralised invalidation risk. Yet the UPC has already attracted major pharma litigation — Amgen and Sanofi filed actions against each other on the court's first day of operation, with estimated litigation values of €100 million per proceeding.

For royalty investors with European exposure, the UPC creates a new risk calculus. Under the old system, a patent could be invalidated in Germany while remaining valid in France and the UK. Royalty streams could be partially impaired but not zeroed out. Under the UPC system, a single revocation action can eliminate patent protection across 17+ jurisdictions in a single proceeding. The EPO opposition and UPC revocation can now run in parallel — and the UPC has made clear it will not automatically stay its proceedings pending EPO outcomes, meaning patent holders can face simultaneous challenges in both fora with potentially divergent results.

National patent litigation and invalidity defences (global)

Beyond these structured mechanisms, patent validity can be challenged as a defence in any infringement litigation in any jurisdiction. In the UK, India, Japan, Korea, China, and other major pharmaceutical markets, defendants routinely raise invalidity as a counterclaim. India's Section 3(d) — requiring new forms of known substances to demonstrate significantly enhanced efficacy — has been a particularly effective filter, most famously in the Novartis v. Union of India decision on Gleevec.

For a royalty stream with global scope, the cumulative invalidity surface is substantial. A patent family covering a blockbuster drug may face Paragraph IV challenges in the US, EPO opposition in Europe, UPC revocation actions, and national invalidity proceedings in India, Japan, and Korea — all simultaneously, with different evidentiary standards, different claim construction approaches, and different policy orientations toward patent protection.

The survival question: what happens to royalties when patents fall?

The interaction between patent invalidation and royalty obligations is not a single legal question. It is at least four distinct questions, each governed by different doctrinal frameworks.

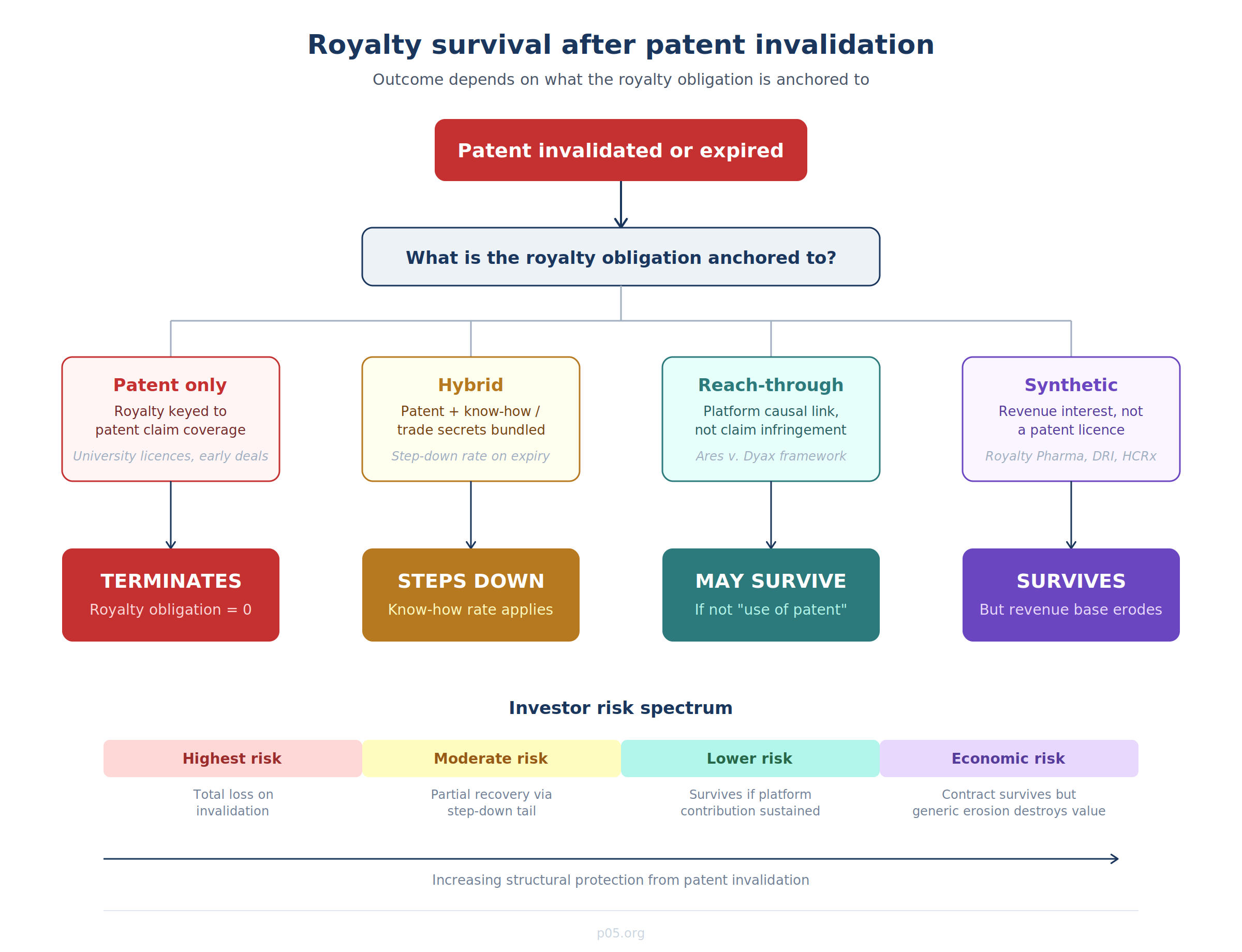

Question 1: Is the royalty "on" the patent?

This is the threshold inquiry, and it is more nuanced than it appears. A royalty obligation can be structured in several fundamentally different ways.

Patent-only royalties are calculated as a percentage of sales of products covered by the licensed patent claims. If the patent is invalidated, the product is no longer "covered," and the royalty trigger is extinguished. Many early-stage university licence agreements are structured this way — royalties are payable "for so long as the Licensed Patents remain valid and in force," and a final, unappealable judgment of invalidity terminates the obligation. Some agreements are even more explicit: the licensed patents are "deemed to have expired upon... the judgment of invalidity or unpatentability by a court or administrative agency of competent jurisdiction from which no appeal is taken or can be taken."

Hybrid royalties cover both patent rights and non-patent assets — typically know-how, trade secrets, proprietary data, or biological materials. Under this structure, even if the patent component is invalidated, the non-patent consideration survives, and so does the contractual obligation to pay. The typical contractual architecture is a "step-down": the full royalty rate applies while patents are valid, and a reduced rate applies after patent expiry or invalidation, reflecting the continuing value of the know-how licence. In life sciences deals, where licences routinely bundle patents and know-how, the step-down is customary — precisely because the Brulotte/Kimble doctrine in the US makes post-expiry patent royalties unenforceable per se, while royalties for know-how or trade secrets (which have no statutory expiration) can continue indefinitely.

Reach-through and platform royalties, as explored in depth in the companion article on reach-through royalties, are keyed to a causal relationship between an upstream tool/platform and a downstream product, rather than to infringement of specific patent claims. The Third Circuit's September 2024 decision in Ares Trading v. Dyax Corp. is directly relevant here: the court held that post-expiration royalties on Bavencio were permissible because the downstream product would not have infringed the licensed phage display patents even if they had still been in effect. The royalty was not "for post-expiration use of a patent" within the meaning of Brulotte; it was compensation for the platform contribution that led to the drug's discovery. If a patent challenge invalidates the upstream platform patents, this structure provides a doctrinal pathway for royalty survival — provided the contract is drafted to anchor the obligation in the platform contribution rather than in claim coverage.

Synthetic royalties and revenue-participation agreements are financial instruments, not patent licences. They are typically structured as a percentage of product revenue (not patent-derived licensing income) and are contractually independent of patent status. A synthetic royalty purchased by a fund like Royalty Pharma, DRI Healthcare, or HealthCare Royalty is usually documented as an asset purchase agreement or a revenue interest agreement, not a patent licence. Patent invalidation does not directly terminate the contractual obligation — but it does destroy the economic value of the stream, because generic entry will collapse the revenue base on which the royalty is calculated.

Question 2: Can the licensee challenge the patent and still benefit from the licence?

This was the question in Lear v. Adkins (1969), in which the US Supreme Court overturned the doctrine of licensee estoppel. The Court held that public interest in clearing invalid patents overrides the contractual principle that a licensee should not repudiate the bargain while continuing to enjoy its benefits. Post-Lear, a licensee may challenge the validity of the licensed patent without automatically losing the licence.

MedImmune v. Genentech (2007) extended this principle further, holding that a licensee need not stop paying royalties or breach the licence agreement before bringing a declaratory judgment action challenging the patent. MedImmune could continue paying under protest while seeking a judicial determination that Genentech's Cabilly II patent was invalid — avoiding the Hobson's choice of either paying royalties on a potentially invalid patent or ceasing payments and risking an infringement suit.

The practical implication is that licensees in the pharmaceutical space have robust legal tools to challenge the patents underlying their royalty obligations, and the royalty holder cannot contractually prevent this challenge through "no-challenge" clauses. In the US, such clauses are generally unenforceable as against public policy — though the precise boundaries remain contested, particularly in settlement contexts.

Question 3: Does the licensee owe royalties during the challenge period?

This is a distinct question from whether the licensee may challenge. In Lear, the Court suggested that a licensee who ceases payment and challenges the patent should not owe royalties for the challenge period if the patent is ultimately found invalid. But the Federal Circuit in Go Medical v. Inmed Corp. clarified that the Lear doctrine requires notice: the licensee cannot retroactively invoke Lear — it must actually stop paying and notify the licensor that it considers the patent invalid. Royalties accrue until that notice is given.

For royalty investors, this creates a gap risk. During the challenge period (which can last 12–18 months for IPR, or 2–5 years for Hatch-Waxman district court litigation), royalty payments may continue — but they may be recoverable by the licensee if the patent is ultimately invalidated. Whether the licensee has been paying under protest, escrowing payments, or continuing to pay under the existing agreement determines the cash-flow risk profile during the litigation window.

Question 4: What is the effect of invalidation on royalties already paid?

This is the most commercially consequential question and the least doctrinally settled. The general US rule is that royalties paid prior to a licensee's challenge cannot be recovered — even if the patent is subsequently invalidated. This is not universal: some commentators argue that if the patent was always invalid, the licensee was effectively paying for nothing and should be entitled to restitution. But courts have generally not adopted this position, treating the licence as providing "insurance" value (freedom from infringement suit) that justifies the payments regardless of ultimate validity.

The asymmetry is important for royalty investors. Past cash flows are generally safe; future cash flows are at risk. This creates a duration-dependent risk profile: a royalty stream with 15 years of remaining patent life has more invalidation exposure than one with 3 years remaining, even if the underlying patent quality is identical.

Contractual defences: how royalty agreements are engineered to survive patent attack

Sophisticated royalty agreements — and the diligence frameworks used by royalty purchasers — address patent challenge risk through several interlocking contractual mechanisms.

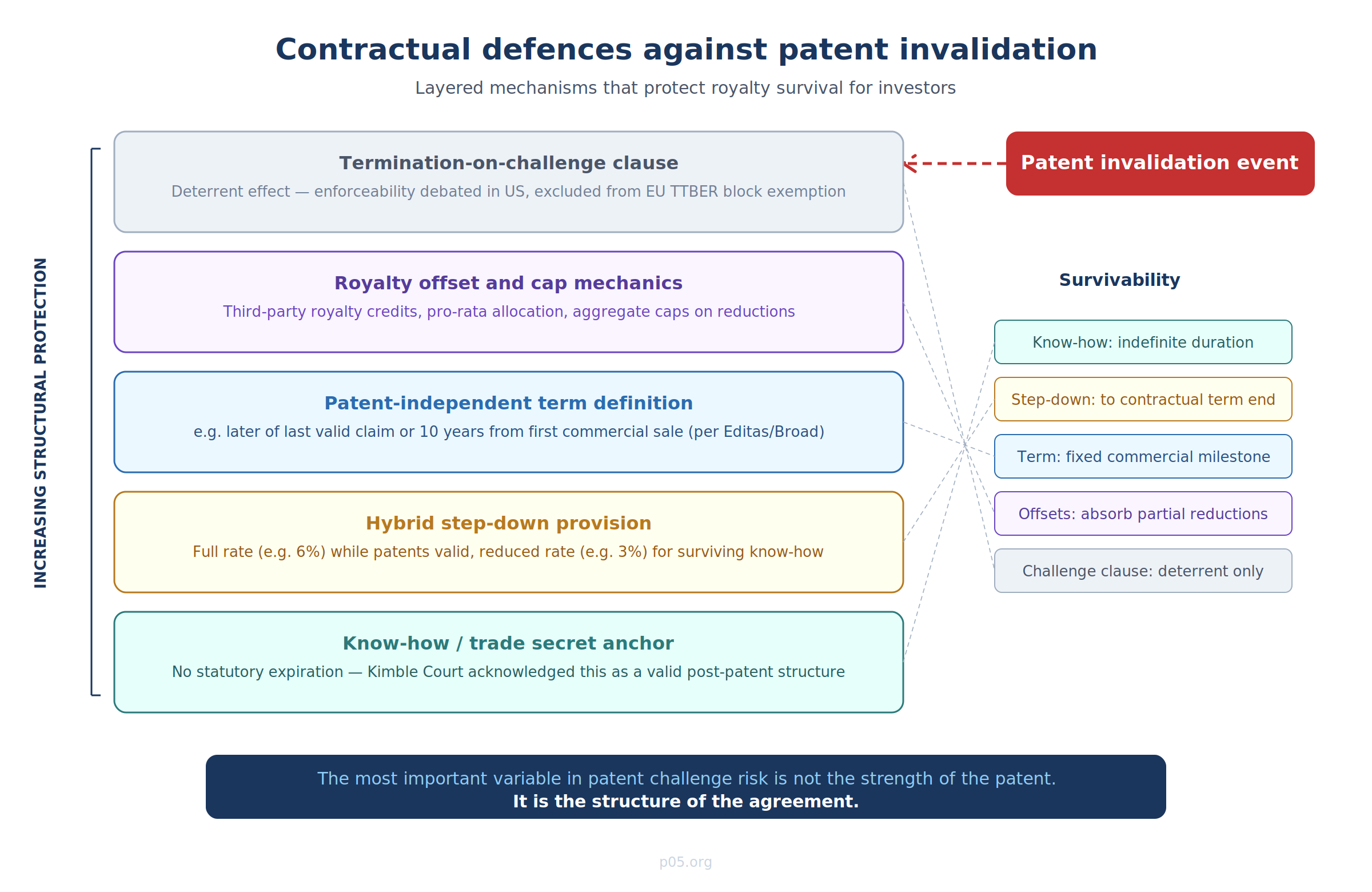

The know-how anchor

The most fundamental structural defence is ensuring that the royalty obligation is not solely dependent on patent validity. By bundling patent rights with know-how, trade secrets, proprietary data, regulatory dossiers, or biological materials, the licensor creates a basis for continuing payments even after patent expiry or invalidation. The Kimble Court itself acknowledged this workaround: parties "can often find ways to achieve similar outcomes," including "tying royalties to non-patent rights."

The step-down mechanism operationalises this: a 6% royalty while patents are valid, stepping down to 3% (or 2%, or 1%) after patent expiry or invalidation, with the reduced rate reflecting know-how value. The step-down rate must be commercially credible — a token 0.1% step-down invites the argument that the royalty is in substance still a patent royalty, disguised as know-how consideration.

Royalty term definitions

The Broad/Harvard–Editas CRISPR licence provides an instructive example of modern term architecture. The "Royalty Term" is defined (country-by-country and product-by-product) as ending on the later of expiry of the last valid claim covering the product or the tenth anniversary of first commercial sale. Once the last valid claim expires, the product is reclassified as an "Enabled Product" and attracts the enabled-category royalty rate for the remainder of the term.

This is not indefinite, but it is explicitly designed to survive patent events — including invalidation. If the last valid claim is invalidated rather than naturally expiring, the reclassification mechanism still operates, and the royalty continues at the enabled-product rate until the tenth anniversary of first commercial sale. The contractual tail is anchored to a commercial milestone, not a patent milestone.

Patent challenge and termination-on-challenge provisions

Some licence agreements contain "termination-on-challenge" clauses — provisions allowing the licensor to terminate the licence if the licensee challenges the patent. In the US, the enforceability of these clauses is debated. Post-Lear and MedImmune, there is a strong argument that such clauses are unenforceable as against public policy, though the Federal Circuit has not issued a definitive ruling. In practice, they create a deterrent even if unenforceability is likely: a licensee may prefer to continue paying royalties rather than risk losing its licence entirely by triggering a termination-on-challenge clause.

The EU treats this differently. Under the Commission's Technology Transfer Guidelines, termination-on-challenge clauses are not treated as hardcore restrictions but are excluded from the block exemption — meaning they require individual assessment under Article 101 TFEU. The revised TTBER and Guidelines expected to come into force on 1 May 2026 are expected to maintain this treatment, though the evolving drafts should be monitored closely.

Royalty offset and stacking mechanics

As discussed in the reach-through article, sophisticated agreements include offset provisions allowing the licensee to credit third-party royalties against the licensed royalty obligation, subject to caps. These mechanics are relevant to patent challenges because a successful challenge to one patent in a stacked portfolio may reduce the total royalty burden without eliminating it entirely. The cap structure determines whether the offset operates symmetrically (reducing the licensor's income proportionally) or asymmetrically (the licensor absorbs a disproportionate share of the reduction).

Jurisdictional divergence: the same patent, different royalty outcomes

The enforceability of royalty obligations after patent invalidation varies dramatically across jurisdictions, creating a patchwork of risk for globally diversified royalty portfolios.

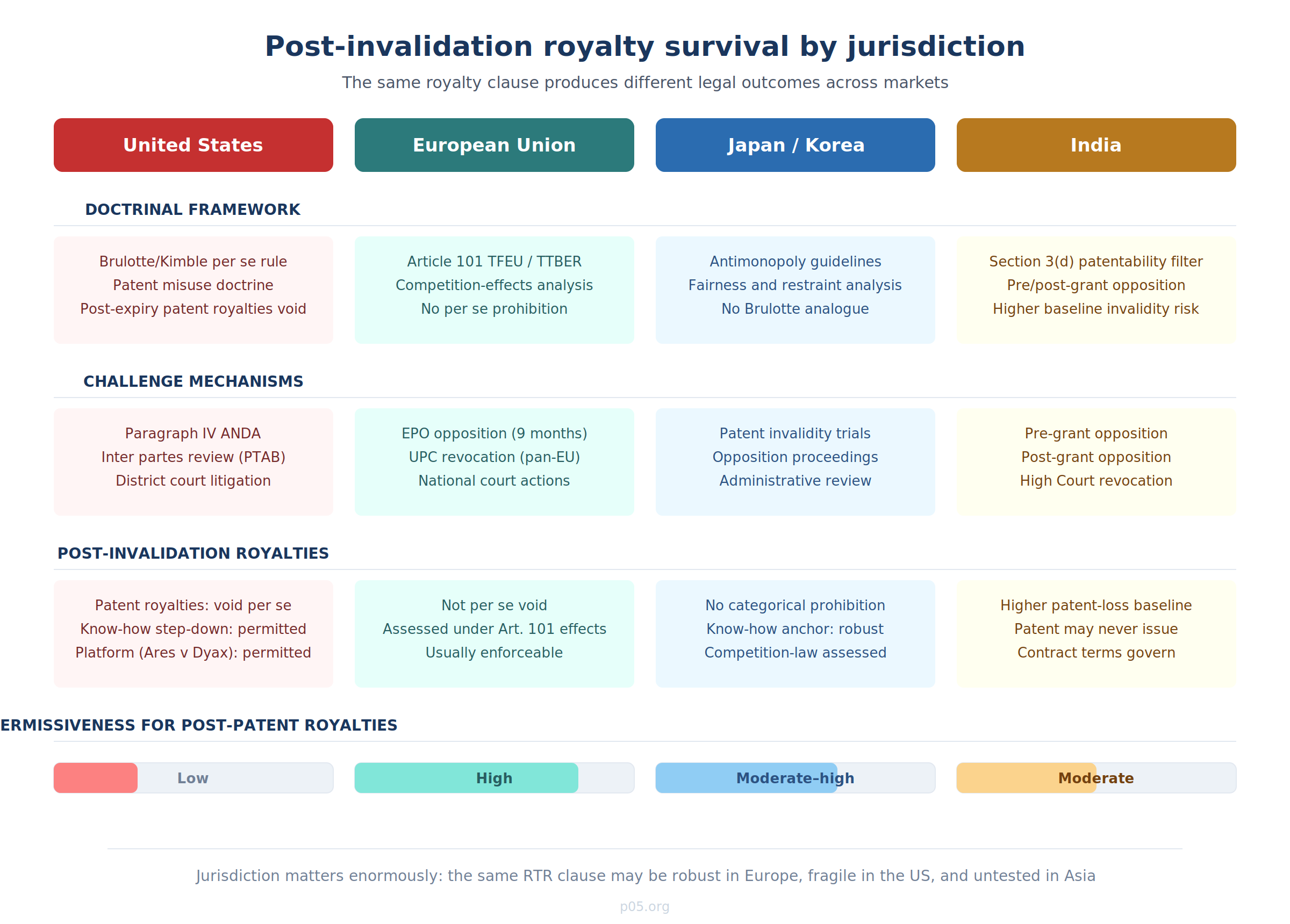

United States: Brulotte/Kimble as the hard constraint

The US per se rule against post-expiration patent royalties (Brulotte v. Thys Co., reaffirmed in Kimble v. Marvel Entertainment) applies with equal force to post-invalidation royalties. If a royalty is "for post-expiration use of a patent," it is unenforceable — and invalidation is functionally equivalent to expiry for this purpose. The workarounds identified by the Kimble Court (know-how licences, deferred payments, business arrangements other than royalties) are the same workarounds available for invalidation scenarios.

The Ares Trading v. Dyax decision from the Third Circuit is the most important recent development. By holding that royalties on a product that would not have infringed the licensed patents (even if they were still valid) are not subject to Brulotte, the court validated the platform-contribution model as a distinct basis for royalty obligations that survives patent events. This is directly relevant to patent challenges: if the downstream product does not practise the licensed claims, invalidation of those claims does not affect the royalty obligation.

European Union: competition law, not patent policy

In the EU, the question is framed through competition law rather than patent policy. The Commission's Technology Transfer Guidelines provide that parties can normally agree to extend royalty obligations beyond the period of validity of licensed IP rights without falling foul of Article 101(1), because post-expiry competition from third parties will "normally be sufficient" to prevent appreciable anti-competitive effects.

This framework is structurally more permissive than the US approach. Post-invalidation royalties are not per se illegal; they are assessed under a competition-effects analysis. For royalty investors, this means that European-anchored royalty streams are more likely to survive patent challenges — provided the royalty does not function as a foreclosure mechanism or tie the licensee to the licensor in a way that forecloses competition.

Japan and Korea: antimonopoly and fairness frameworks

Japan and Korea address post-patent royalties through competition and fairness frameworks rather than a Brulotte-style per se rule. The JFTC's IP Guidelines emphasise that know-how, unlike patents, has no guaranteed protection period, creating a natural anchor for post-patent obligations. Korea's OECD-aligned framework assesses licensing restraints through a competition-effects lens, without categorical prohibitions on post-expiry royalties.

India and emerging markets

India's patent system, with its Section 3(d) filter and robust opposition mechanisms, creates a higher baseline risk of patent invalidation for pharmaceutical products. For royalty investors with Indian market exposure, the question is not only "will the patent survive?" but "was a valid patent ever grantable for this formulation in India?" The answer frequently is no — and the royalty agreement must be structured to accommodate a jurisdiction where the patent-based royalty trigger may never activate.

The royalty investor's diligence framework: pricing patent challenge risk

For royalty purchasers, patent challenge risk is not binary (patent valid/invalid); it is a probability distribution that must be priced into the acquisition.

Patent quality assessment

The first layer of diligence is a technical assessment of the patent portfolio's vulnerability to challenge. This includes prior art landscape analysis (what published references could an IPR petitioner or ANDA filer deploy?), claim scope analysis (are the claims narrow and well-supported, or broad and potentially vulnerable to written description or enablement challenges?), prosecution history analysis (did the applicant make representations during prosecution that could create estoppel or narrow claim scope?), and Orange Book listing analysis (are the listed patents appropriately matched to the approved drug, or do they include method-of-use patents with narrow therapeutic coverage?).

Challenge probability modelling

Sophisticated royalty investors model challenge probability as a function of drug economics. A drug with $2 billion in annual sales will attract more aggressive and better-funded challenges than one with $200 million. The expected timing of the first Paragraph IV filing, the likelihood of IPR petitions, and the probability of EPO opposition can be estimated from comparable drug litigation histories.

The Covington guide on synthetic royalty dealmaking states the point directly: sellers should "clean house" and ensure their patents are not subject to pending challenges before attempting to monetise a royalty stream. A purchaser's IP diligence will focus on whether the patents can survive challenge, particularly the potential for generic entry during the purchaser's return horizon.

Risk-adjusted valuation

The patent challenge risk is ultimately expressed in the discount rate or in scenario-weighted cash-flow models. A royalty stream backed by a single composition-of-matter patent with strong prior art defence will command a lower discount rate than one backed by multiple method-of-use patents with known prior art vulnerabilities.

The valuation arithmetic can be written as:

E[NPV] = Σ [ p(patent survives at t) × α × Sales(t) + p(patent falls at t) × α' × Sales'(t) ] / (1 + r)^t

where α' is the step-down royalty rate (if any) and Sales'(t) is the post-generic-entry sales forecast. If the agreement provides no step-down and the royalty is purely patent-anchored, α' = 0 and Sales'(t) reflects the generic erosion curve.

This is why contractual structure matters so much to royalty investors. The difference between α' = 0 (royalty terminates on invalidation) and α' = 0.5α (royalty steps down to 50%) can represent hundreds of millions of dollars in expected value.

Case study: the anatomy of a patent-dependent royalty collapse

Consider a hypothetical (but representative) scenario. A royalty fund acquires a 3% royalty on US net sales of a branded oncology product with $1.5 billion in annual revenue, paying $400 million for a stream expected to generate $45 million per year over the remaining 12-year patent term. The acquisition is based on a single composition-of-matter patent with an Orange Book listing.

Eighteen months after acquisition, a generic manufacturer files an ANDA with a Paragraph IV certification, arguing the patent is obvious over a combination of two prior art references. The patent holder sues, triggering a 30-month stay. During the stay, the royalty continues — $45 million per year, or roughly $112 million over the 30-month period.

At the 24-month mark, the district court finds the patent invalid. The 30-month stay terminates immediately. Within six months, three generic manufacturers enter the market. Branded sales decline from $1.5 billion to $300 million within 18 months. The royalty stream drops from $45 million annually to $9 million — and continues to decline as generics take additional share.

The royalty fund has received approximately $157 million in total royalty payments ($45M × 2 years + $67M in the declining period) against a $400 million acquisition price. The remaining 8 years of expected cash flows are largely destroyed.

Now consider the alternative: the same drug, but with a hybrid licence that includes a know-how step-down from 3% to 1.5% after patent expiry or invalidation. The step-down rate applies to total product revenue (branded plus authorised generic, if any). Even with generic erosion, the step-down royalty generates $4.5 million per year on the reduced revenue base, and the know-how term extends for 10 years from first commercial sale (which has already occurred). The present value of the step-down tail is approximately $30–40 million — not enough to recover the investment loss, but materially better than zero.

The structural lesson is that the contractual architecture determines whether patent invalidation is a total loss or a recoverable impairment. Royalty investors who pay premium multiples for "clean" patent-only streams without step-down protection are making an implicit bet that the patents will survive — a bet that, given IPR success rates and the frequency of Paragraph IV challenges, should be priced accordingly.

Is patent challenge a "big problem" for royalty financing?

The honest answer is: it is the biggest non-clinical risk, but it is a manageable one.

Patent challenge is not a "big problem" in the sense that it makes royalty financing unworkable. The market is enormous and growing — royalty deal values have been growing at a compound annual growth rate of roughly 45% over recent years, with Royalty Pharma alone executing close to $2 billion in deals in a single month in 2024. If patent risk were unmanageable, this market would not exist.

But patent challenge is a "big problem" in the sense that it is the risk most likely to produce catastrophic loss for a royalty investor who has not structured the acquisition correctly. Unlike clinical risk (which is largely resolved before a royalty stream is created) or commercial risk (which erodes value gradually), patent invalidation can destroy 80–90% of a royalty stream's value in a single event, within a compressed timeline.

The risk is also asymmetric. Patent challenges have become cheaper, faster, and more accessible since the America Invents Act. IPR proceedings cost a fraction of district court litigation and resolve in 12–18 months. The UPC creates a new centralised revocation pathway in Europe. Hedge funds, generic manufacturers, and competitors have strong economic incentives to challenge valuable patents, and the institutional infrastructure (specialised law firms, PTAB practitioners, patent analytics platforms) makes challenges operationally straightforward.

The mitigants are contractual, not legal. The law does not protect the royalty holder from patent invalidation — it simply provides the framework within which contractual protection must be engineered. Know-how anchors, step-down mechanisms, reach-through structures, multi-patent portfolios, and non-patent consideration provisions are the tools. The royalty investor's job is to diligence these protections before acquisition, not to discover their absence afterward.

Implications for deal structuring and the royalty market

Three structural implications follow for the royalty financing market.

First, the premium on contractual sophistication is increasing. As patent challenge mechanisms become more potent and more accessible, the relative value of well-drafted royalty agreements — with know-how anchors, step-down provisions, and patent-independent term definitions — increases. Royalty purchasers should expect to pay higher multiples for streams with robust contractual protection and should discount heavily for patent-only structures without invalidation protection.

Second, patent thicket analysis is becoming a core competency for royalty investors. The "last man standing" patent strategy — in which drug companies build layered portfolios of secondary patents (formulation, method-of-use, dosing regimen, polymorphic form) to extend protection beyond the primary composition-of-matter patent — means that royalty diligence cannot focus on a single patent. It must assess the entire portfolio, identify the "last valid claim" under various challenge scenarios, and model the royalty term accordingly. Yale Law and Policy Review research found that 91% of drugs receiving patent term extensions continue their monopolies past those extensions through secondary patents, suggesting that the effective patent life (and royalty life) is frequently longer than the primary patent term.

Third, jurisdictional arbitrage in royalty structuring will intensify. The divergence between the US per se rule (Brulotte/Kimble) and the EU competition-effects approach creates structural incentives to anchor royalty obligations in European law where possible, particularly for reach-through and platform royalties where post-patent tails are economically significant. The UPC's centralised revocation risk partially offsets this advantage, but for royalties structured around non-patent consideration, the EU framework remains more permissive than the US.

Conclusion

Patent challenges do not make pharmaceutical royalty financing unworkable. But they make it structurally unforgiving of sloppy contract design and inadequate diligence. The investor who acquires a patent-only royalty stream without step-down protection is not accepting a "small risk" of patent invalidity — they are accepting a binary bet at odds determined by patent quality, challenge economics, and the increasingly efficient machinery of inter partes review and Hatch-Waxman litigation.

The contractual tail, as always, is only as valuable as the thread that sustains it. In the patent challenge context, that thread is not the patent itself — it is the contractual architecture that determines whether the royalty obligation is anchored to a wasting asset (the patent) or to continuing non-patent consideration (know-how, data, platform contribution) that survives the patent's demise.

For the royalty market, the lesson is straightforward but frequently underpriced: the most important variable in patent challenge risk is not the strength of the patent. It is the structure of the agreement.

All information in this report was accurate as of the research date and is derived from publicly available sources including court opinions, regulatory guidance, academic literature, SEC filings, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.