Private Credit Under Stress: Implications for Pharmaceutical Royalty Funds

Redemption freezes at Blue Owl, record outflows at Blackstone's BCRED, and a wave of withdrawals across the industry's largest funds have placed the $1.8 trillion private credit market under its most sustained pressure in years.

For those in the adjacent world of pharmaceutical royalty financing, the turmoil has raised the question of how much of what is going wrong is specific to private credit's structure, and how much reflects forces that cut across alternative investment vehicles more broadly.

What Happened

The deterioration has been rapid.

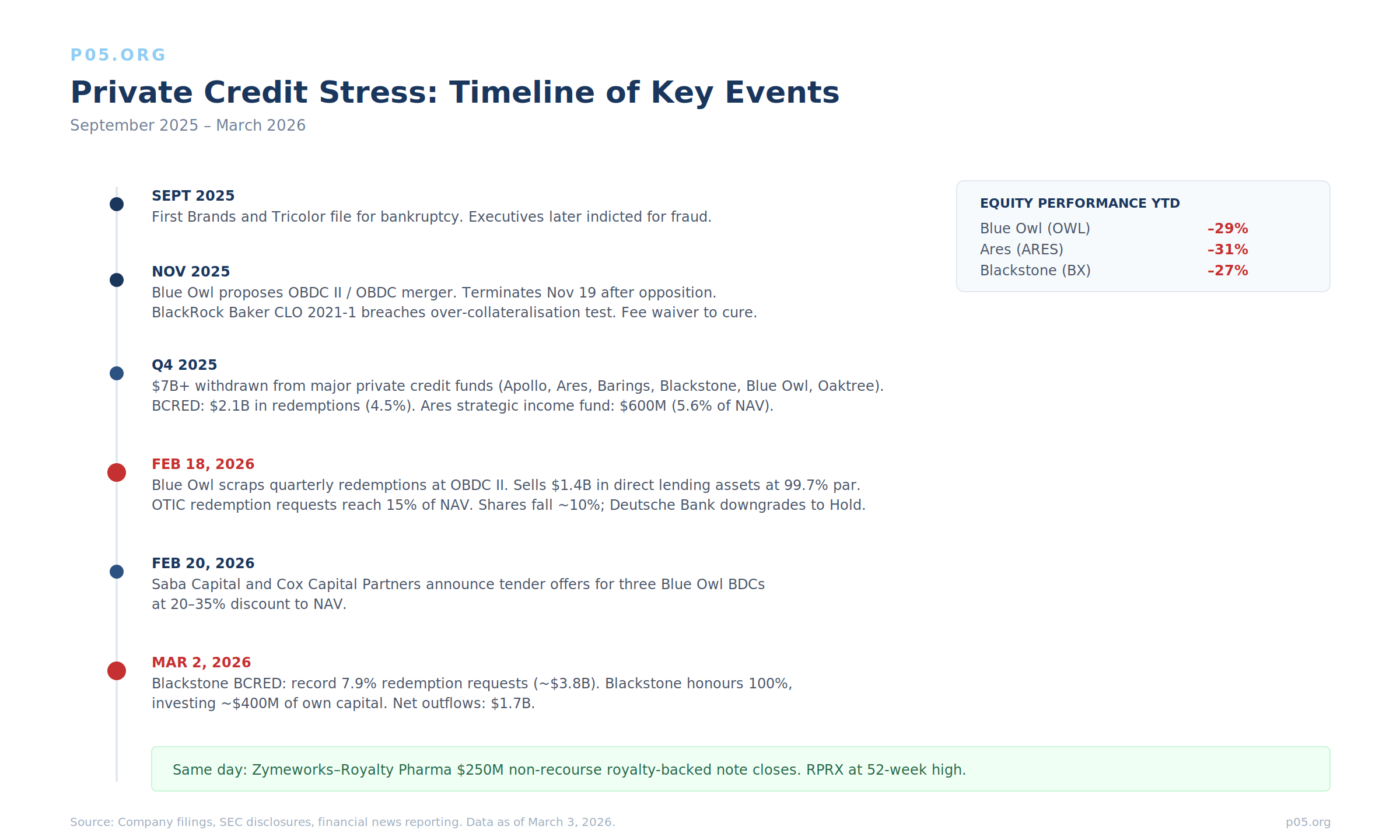

In November 2025, Blue Owl Capital proposed merging its non-traded BDC, OBDC II, into the larger publicly traded OBDC. The implied economics would have forced OBDC II investors to accept shares trading at roughly a 20% discount to NAV. The proposal drew opposition; Blue Owl terminated the merger on November 19, citing "current market conditions." A shareholder class action was subsequently filed, alleging insufficient disclosure of redemption pressure during the preceding months.

Blue Owl's troubles did not emerge in isolation. Private Equity Wire reported that investors withdrew more than $7 billion from Wall Street's largest private credit funds in Q4 2025. Elevated redemption requests hit vehicles managed by Apollo, Ares, Barings, Blackstone, BlackRock's HPS Investment Partners, Blue Owl, Cliffwater, and Oaktree. Blackstone's BCRED recorded $2.1 billion in Q4 redemptions (4.5% of the fund). Ares' $23 billion strategic income fund saw roughly $600 million in withdrawals (5.6% of NAV).

The bankruptcies of auto-parts suppliers First Brands and Tricolor had already shaken confidence in private credit underwriting, and subsequent criminal fraud charges against executives at both companies raised questions among investors and regulators — though both Cambridge Associates and Goldman Sachs have argued the failures were fraud-driven and idiosyncratic rather than indicative of systemic underwriting weakness. First Brands' founders were charged in New York; Tricolor's CEO and COO were indicted in Manhattan for allegedly inflating collateral values over a period of years.

A further data point emerged in November 2025. BlackRock's Baker CLO 2021-1, a $495 million private credit collateralised loan obligation originated through HPS Investment Partners (which BlackRock acquired for $12 billion in 2024), breached its over-collateralisation test after the value of its underlying loans fell too far relative to its highest-rated bonds. BlackRock waived management fees to cure the breach, a rarity in the CLO market. S&P Global Ratings downgraded the deal's junior tranches, citing deteriorated credit quality.

The portfolio held loans to companies including Renovo Home Partners, which filed for bankruptcy shortly after its debt had been carried at par. The riskiest bonds in the deal had been continuously failing their OC tests since April 2024. A single CLO breach is not systemic. But it provided an unusually transparent window into the valuation dynamics of an asset class that, by design, discloses comparatively little.

On February 18, 2026, Blue Owl scrapped quarterly redemptions at OBDC II entirely, replacing them with a "return of capital" model.

The fund executed a $1.4 billion sale of direct lending assets across three vehicles: $600 million from OBDC II (roughly 34% of its portfolio), $400 million from OTIC, and $400 million from the publicly traded OBDC, sold to four North American public pension and insurance investors at 99.7% of par value. OBDC II will use proceeds to repay approximately $275 million under a Goldman Sachs credit facility and distribute up to $2.35 per share (roughly 30% of NAV) to all shareholders by March 31, 2026. Redemption requests at OTIC, Blue Owl's tech-focused BDC, had reached 15% of NAV.

Blue Owl shares fell roughly 10% on the announcement and are down 29% year to date. Deutsche Bank downgraded the stock from Buy to Hold with a $10 price target. One of the firm's structured notes, issued by a Citigroup subsidiary, was quoted below 50% of face value. Two days later, Saba Capital Management and Cox Capital Partners announced cash tender offers for shares in three Blue Owl non-traded BDCs — OBDC II, OTIC, and Blue Owl Credit Income Corp — at an expected 20-35% discount to NAV.

The emergence of secondary-market buyers willing to offer liquidity at a significant discount to stated NAV highlighted, for the market, the gap between reported values and the price at which capital could actually be released.

On March 2, Blackstone disclosed that BCRED's first-quarter 2026 redemption requests had surged to a record 7.9% of shares, approximately $3.8 billion, well above the standard 5% quarterly cap. Blackstone is honouring 100% of requests by expanding a tender offer to 7% and investing roughly $400 million of its own capital alongside employees to cover the remaining 0.9%.

Net outflows were $1.7 billion after accounting for roughly $2 billion in new commitments. Blackstone shares are down nearly 27% year to date; Ares is down 31%; Apollo over 26%.

Mohamed El-Erian asked publicly whether Blue Owl's restructuring was a "canary in a coal mine moment." JPMorgan's Troy Rohrbaugh was blunter: "I'm shocked that people are shocked." Ares CEO Michael Arougheti called the fears "odd" and "frustrating," noting that 97% of wealth clients had not asked to redeem. The SEC has designated private credit and retail-facing illiquid products as a top examination priority for fiscal year 2026.

The Core Structural Issue

Credit quality matters, and concerns about AI disruption of software borrowers and rising defaults are not unfounded. Bank of America has projected private credit default rates of 4.5% in 2026, down from 5% in 2025, while noting that the asset class remains among the more fragile segments of the leveraged finance universe. Once selective defaults and liability management exercises are included, the effective distress rate approaches 5%, and payment-in-kind interest now accounts for roughly 8% of public BDC investment income, a proportion that has risen steadily.

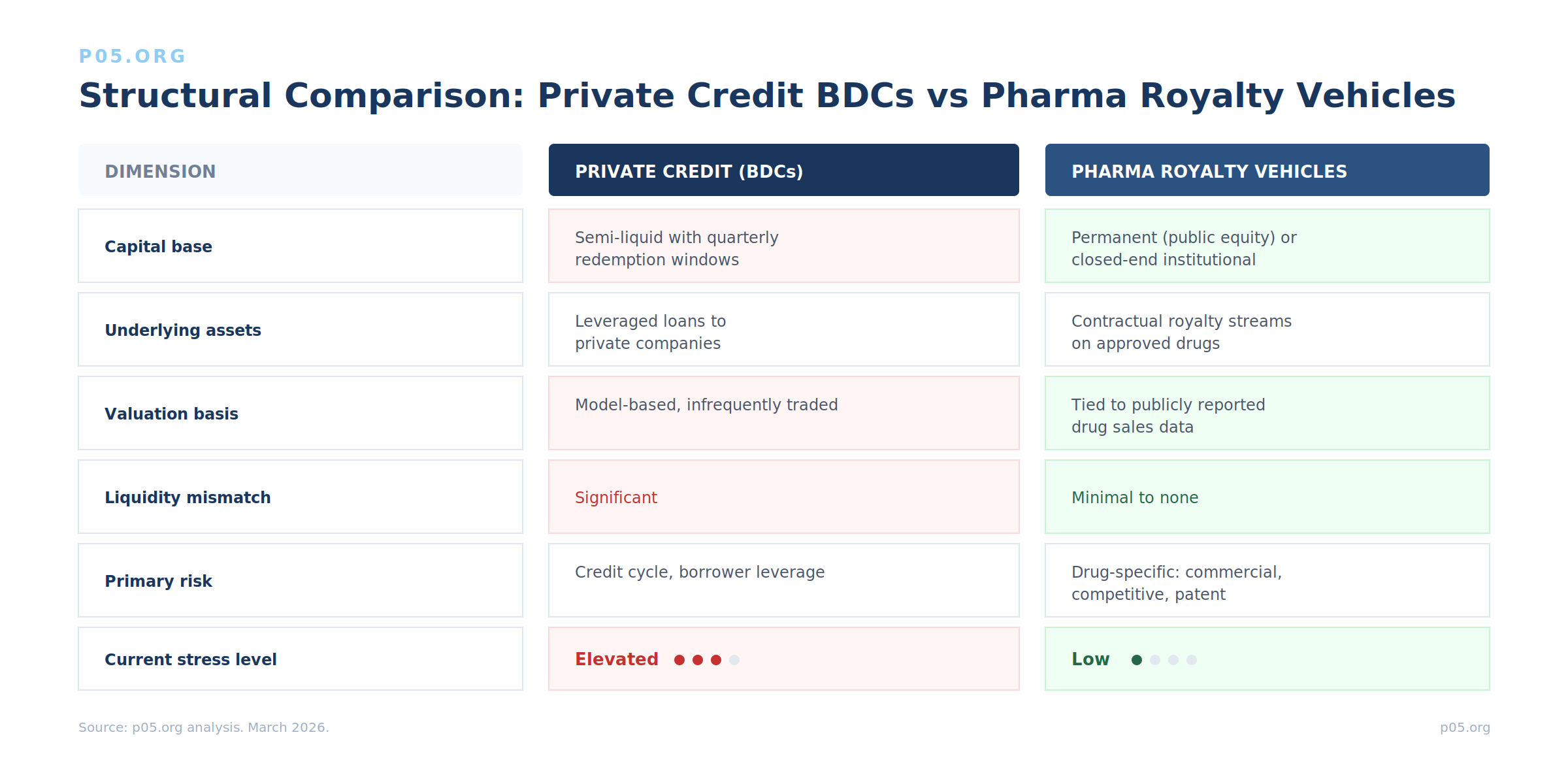

But the proximate cause of the current stress is architectural: the collision between illiquid assets and semi-liquid fund wrappers. Private credit funds hold directly originated loans to middle-market companies that rarely trade. The vehicles that house them, however, offered retail investors quarterly redemption windows, typically capped at 5% of NAV. Moody's has projected private credit AUM to reach $4 trillion by 2030 but cautioned that deepening ties between private credit funds and traditional financial institutions could heighten contagion risk.

The promise of periodic liquidity in a fundamentally illiquid asset class held up only as long as redemption requests stayed within the structural caps. Once they did not, the limitations of the structure became apparent.

Relevance to Pharmaceutical Royalty Financing

The question now being asked across the royalty financing market is whether the stress in private credit could eventually reach adjacent asset classes. The answer depends on a more granular question: how much of the current dysfunction is specific to the BDC model, and how much reflects vulnerabilities shared by other alternative investment vehicles? The dominant royalty vehicles are organised differently. But the two markets are not as separate as they once were.

Fund Structures

Royalty Pharma (Nasdaq: RPRX) operates as a publicly traded company with a permanent capital base funded by equity and investment-grade unsecured debt. There is no redemption mechanism; investors access liquidity through the public equity market. Royalty Pharma reported Q4 2025 portfolio receipts of $874 million (up 18% year-over-year), deployed $2.6 billion into nine new royalties in 2025, and guided for $3.275-3.425 billion in 2026 portfolio receipts. The stock recently hit a 52-week high.

HealthCare Royalty Partners (HCRx), majority-owned by KKR since the $3 billion acquisition in 2025, operates through closed-end fund partnerships with committed institutional capital and defined investment periods. There is no quarterly redemption feature. XOMA Royalty Corporation (Nasdaq: XOMA) similarly trades on the public market.

The structural distinction is significant: none of these vehicles offers the periodic redemption windows that lie at the centre of the current private credit dislocation. An investor in Royalty Pharma who wishes to exit does so through the public equity market. The redemption mechanics that have created friction in the BDC market simply do not apply.

Underlying Assets and Valuation

The valuation debate in private credit centres on the opacity of model-based marks for directly originated loans that rarely trade. The DOJ has warned about "creative" marks in private portfolios. When Blue Owl sold $1.4 billion in loans at 99.7% of par to demonstrate mark accuracy, the necessity of such a demonstration said as much about prevailing sentiment as it did about the quality of the underlying marks.

Pharmaceutical royalty streams are tied to reported net sales of drugs marketed by public companies with SEC reporting obligations. The present value of future streams requires modelling, but the underlying revenue data is publicly observable. The risks are drug-specific, commercial performance, competition, patent life, licensee execution, rather than systemic credit cycle risks.

For a detailed treatment of how non-recourse royalty-backed notes isolate drug-level risk from corporate credit, see our recent analysis of the Zymeworks-Royalty Pharma transaction.

Points of Intersection

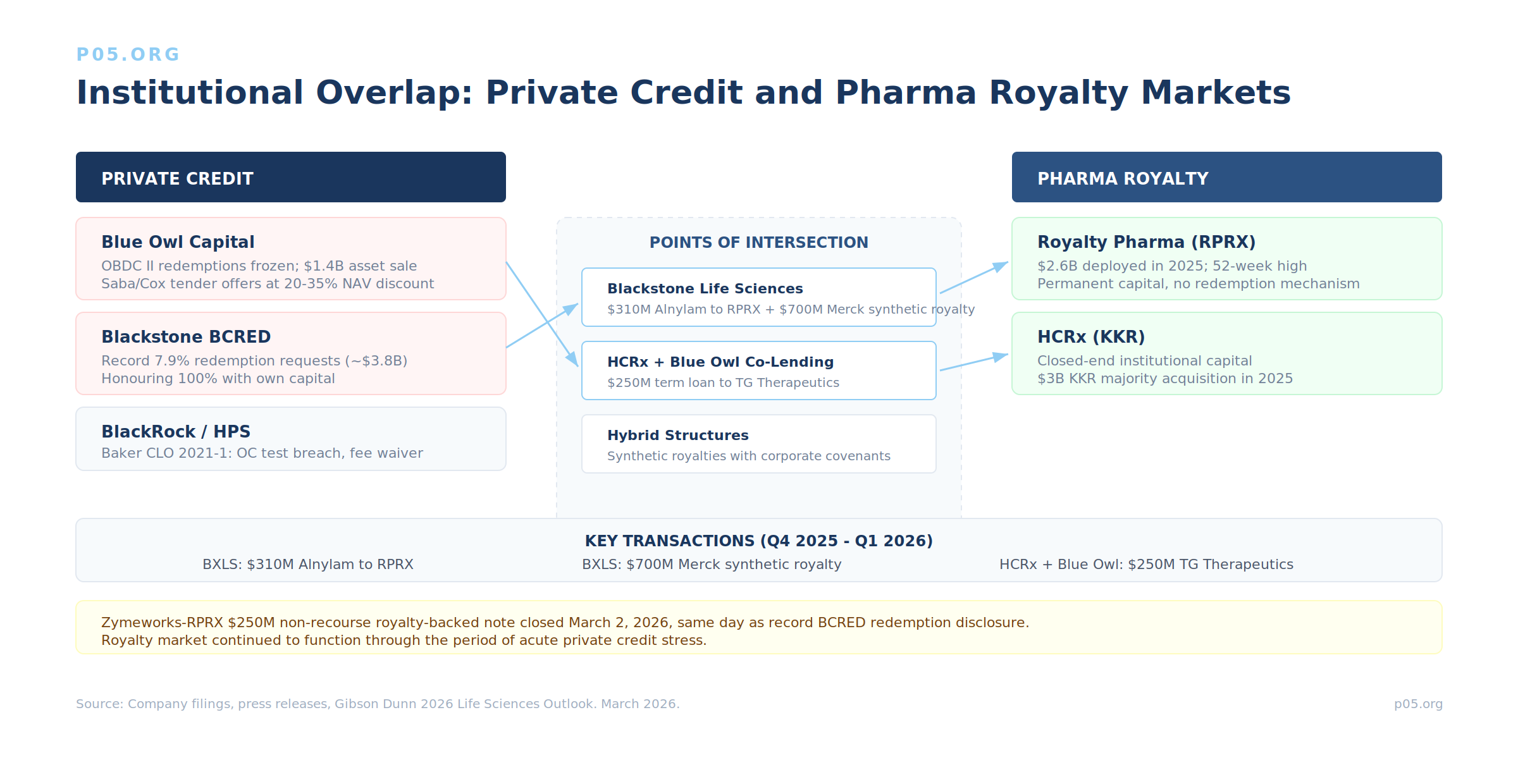

The structural differences are clear. What has drawn attention from allocators and advisers, however, is the growing institutional overlap.

Blackstone's presence in pharmaceutical royalty financing has deepened significantly. In Q4 2025 alone, Blackstone completed a $310 million sale of its royalty interest in Alnylam's Amvuttra to Royalty Pharma and entered into a $700 million synthetic royalty transaction with Merck tied to sacituzumab tirumotecan. KKR's majority acquisition of HCRx further reflects the institutional convergence.

The institutional connections extend further: HCRx and Blue Owl jointly provided a $250 million term loan facility to TG Therapeutics, illustrating shared deal flow across the two markets.

Blackstone Life Sciences operates as a separate vehicle from BCRED, with its own capital structure and investor base. The $310 million Alnylam disposition in Q4 2025 was consistent with routine portfolio management, and Blackstone simultaneously deployed $700 million into the Merck synthetic royalty, suggesting continued active participation on both sides of the ledger.

That said, market participants will naturally monitor whether sustained pressure on any part of a multi-strategy platform influences deployment pace or capital allocation priorities elsewhere, even where the underlying businesses are operationally distinct. Similarly, if regulatory action on semi-liquid retail products produces structural changes, any royalty-focused vehicles that adopt similar fund wrappers could be affected, though no major royalty vehicle currently operates on a semi-liquid BDC model.

The hybrid financing structures that blend royalty economics with elements of term debt sit along a spectrum. Those closer to the credit-like end, particularly synthetic royalties with limited recourse and corporate-level covenants, share more characteristics with private credit than a pure royalty purchase.

The concern in the market is that if the current environment produces broader scepticism about structured alternative lending, these instruments could face increased scrutiny even where the underlying drug economics are sound.

Implications for Capital Formation

There is also a more immediate dimension for the royalty market. If private credit dislocation constrains the supply of alternative capital to life sciences companies, royalty financing could absorb some of the displaced demand.

Aggregate royalty financing transaction value reached approximately $6.5 billion in 2025, up from $5.7 billion the prior year. The Zymeworks-Royalty Pharma $250 million non-recourse royalty-backed note, announced on March 2, the same day as Blackstone's record BCRED disclosure, illustrates the continued functioning of the royalty market during a period of acute stress elsewhere. WilmerHale has noted that royalty financing economics are less closely tethered to macroeconomic forces than traditional equity or debt.

Tighter underwriting standards, slower fund deployment, and regulatory headwinds in private credit could push biotech borrowers towards royalty monetisation as an alternative. The capacity appears to be there: HCRx's expanding debt-focused vehicles, Royalty Pharma's increasingly diverse deal structures, and the steady entry of new participants all suggest the supply side can accommodate greater volume.

Structural Comparison

What to Watch

Multi-strategy platform dynamics. Blackstone Life Sciences and BCRED are separate vehicles with distinct mandates. The question for royalty investors is not whether one subsidises or drains the other, but whether sustained pressure on the broader platform affects the pace of new royalty deployment or the appetite for large-scale transactions.

Regulatory extension. The SEC's examination priority on semi-liquid retail products is focused on private credit, but regulatory frameworks tend to expand. Any royalty-focused vehicle that adopts a periodic-liquidity structure could fall within scope.

Hybrid structure scrutiny. The growing prevalence of financing structures that combine royalty economics with debt-like features means the boundary between the two markets is less clean than it was five years ago. The expectation across the market is that the valuation and transparency questions currently being directed at private credit will, in time, extend to the more credit-like end of the royalty spectrum.

All information in this article was accurate as of the publication date and is derived from publicly available sources including company press releases, SEC filings, regulatory announcements, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.

Member discussion