Reach-Through Royalties and the Contractual Tail: Perpetuity, Stacking, and the AI Attribution Problem

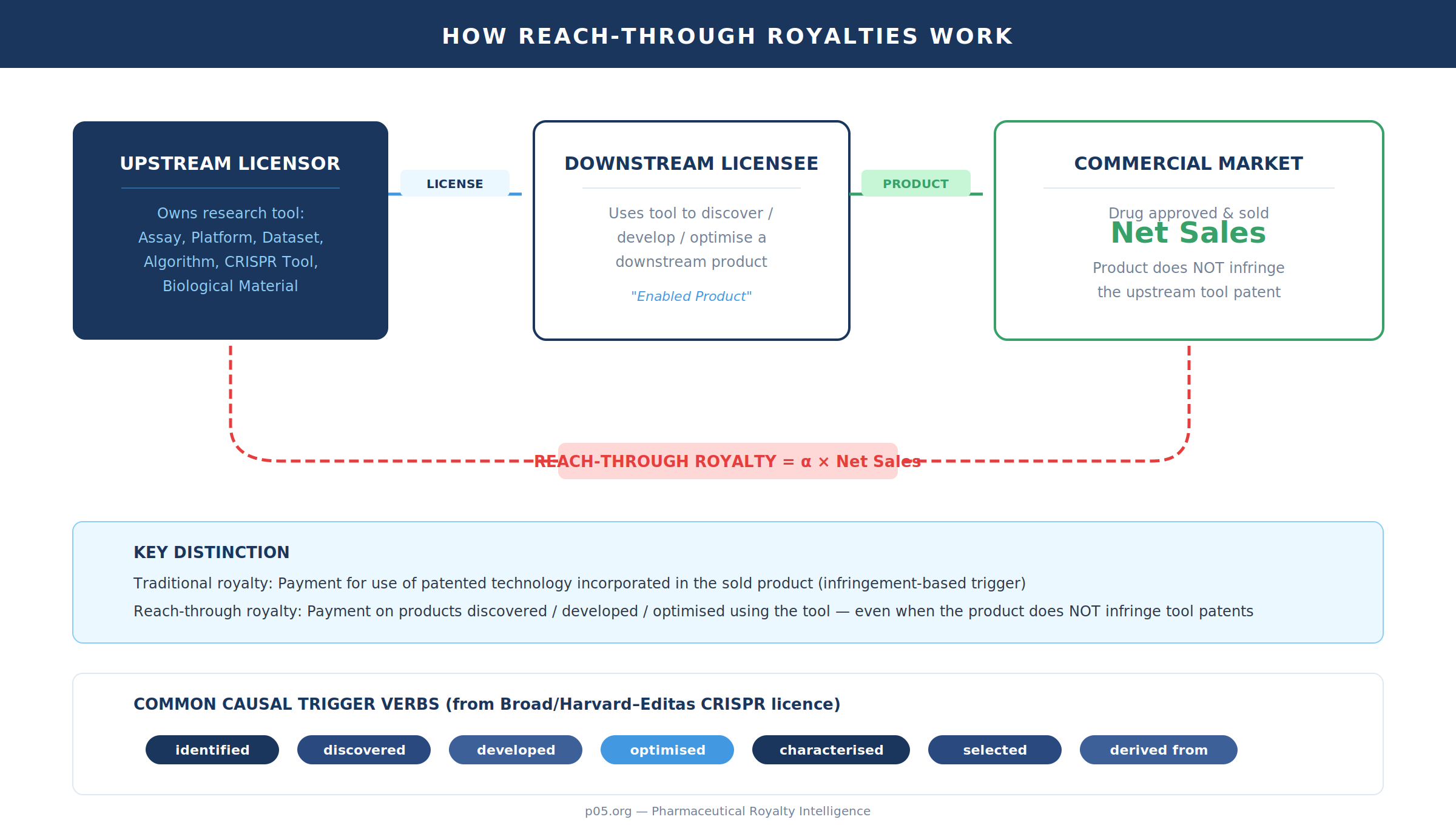

When Editas Medicine sold its future Cas9 licence fees to a DRI Healthcare subsidiary for $57 million upfront, the transaction crystallised something that pharmaceutical royalty practitioners have long understood but rarely said out loud: reach-through royalties are not "royalties on the tool." They are engineered downstream participation — a payment obligation keyed to future commercial products that are causally linked to a licensed assay, platform, biological material, dataset, or algorithm, often even where no composition-of-matter or product claim is infringed by the downstream product.

The legal and economic point is that the royalty trigger is drafted as use ("identified," "discovered," "developed," "optimised," "materially informed by") rather than incorporation of the licensed technology in the marketed article. Royalties are charged on products discovered or developed through use of the research tool, even though the end product does not infringe any patents claiming the enabling tool. This is explicit in mainstream practitioner descriptions of reach-through licensing.

Two contemporaneous public-data anchors illustrate how RTRs are now implemented with unusually precise definitional machinery.

First, in Bayer v Housey (D. Del.), Bayer pleaded that the licensor's licensing terms required royalties tied to downstream R&D budgets and sales of commercialised products where the patented technology was "utilised in the research and development leading to the drug," and that the royalty term purportedly extended through the life of the licensee's downstream patents.

Second, in the Broad/Harvard–Editas CRISPR licence (SEC-exhibited), the agreement defines an "Enabled Product" to include products "identified, discovered, developed, optimised, characterised, selected, derived from or determined to have utility" (in whole or part) by use or modification of patent rights, licensed products, or institution transfer materials — classic reach-through causality language — while simultaneously carving out certain small/large molecules that were merely "identified or discovered" using the materials but do not otherwise meet the "Enabled Product" criteria.

What follows is the expert-level problem set: why RTRs appear "perpetual" in economics, where they collide with patent-policy limits (especially in the United States), why Europe is structurally more permissive, why NIH-policy friction persists, and why AI-driven discovery is breaking the attribution assumptions that made reach-through look administrable.

Reach-through as downstream participation: causal triggers and definitional engineering

The canonical RTR structure can be written (abstracting away base definition, offsets, tiers, and caps) as a royalty on downstream net sales:

Royalty(RTR) = α × Net Sales(Downstream Product)

In real contracts, the battle is not the multiplication. It is the ontology: what counts as a downstream product, and what level of causal nexus is sufficient to say it was "discovered using" the tool.

The Broad/Harvard–Editas agreement is unusually explicit in showing what modern drafting treats as "causal use." "Enabled Product" is defined to include any product (other than a "Licensed Product") that is or incorporates, or is "made, identified, discovered, developed, optimised, characterised, selected, derived from or determined to have utility" (in whole or part) by using or modifying enumerated upstream inputs (patent rights and covered inventions, licensed products, institution transfer materials, and progeny/derivatives of the foregoing).

That is not accidental verbosity: it is the contract attempting to turn epistemic causality (a research history) into a justiciable boundary condition.

Two aspects of this definition matter for expert practice.

First, the definitional list is deliberately broader than patent infringement vocabulary. The verbs ("identified," "characterised," "selected," "determined to have utility") are discovery-workflow verbs, not infringement tests. This is the core move that makes RTRs "not on the tool, but on the future."

Second, the same agreement shows the counter-move: negative definition to bound overreach. It expressly excludes "any large or small molecule" that was "identified or discovered" using the materials/technology but "does not otherwise meet the definition of Enabled Product" — that is, mere identification is not enough unless the molecule is otherwise incorporated in, made by, or depends on the licensed toolkit in a manner drafted to count.

In other words, sophisticated licensors increasingly price the reach-through option while simultaneously limiting the category to reduce enforceability risk and to keep the royalty stack within investable tolerances.

The royalty base itself is often drafted to include both the upstream and downstream categories in a single "Net Sales" definition. In the same SEC-exhibited agreement, "Net Sales" is defined on sales/transfers of "Licensed Products, Licensed Services, Enabled Products or Enabled Services," less negotiated deductions and with elaborate fair-market-value logic for non-cash consideration, non-arm's-length transactions, and discounted pricing.

The point is structural: once "Enabled Products" are inside the "Net Sales" base term, the reach-through royalty becomes operationally indistinguishable from a conventional running royalty — except that product inclusion is driven by the causal definition, not by IP claim coverage.

The hard question is whether this causal linkage is a stable predicate over the life of a drug (or platform). In a narrow assay-to-molecule story it can be: one screen, one hit series, one IND. In modern discovery — multi-omic target inference, iterative modelling, and combinatorial toolchains — the "use" boundary becomes a litigation surface rather than an accounting surface. The agreement can draft "identified" and "determined to have utility"; it cannot draft away the evidentiary entropy.

Perpetuity by design: patent expiry constraints and contract workarounds

RTR "perpetuity" is rarely actuarial perpetuity. It is a contractual tail that is long relative to the upstream asset's patent term, and often long relative to the upstream asset's commercial life as a standalone product. The legal feasibility of that tail is jurisdiction-sensitive.

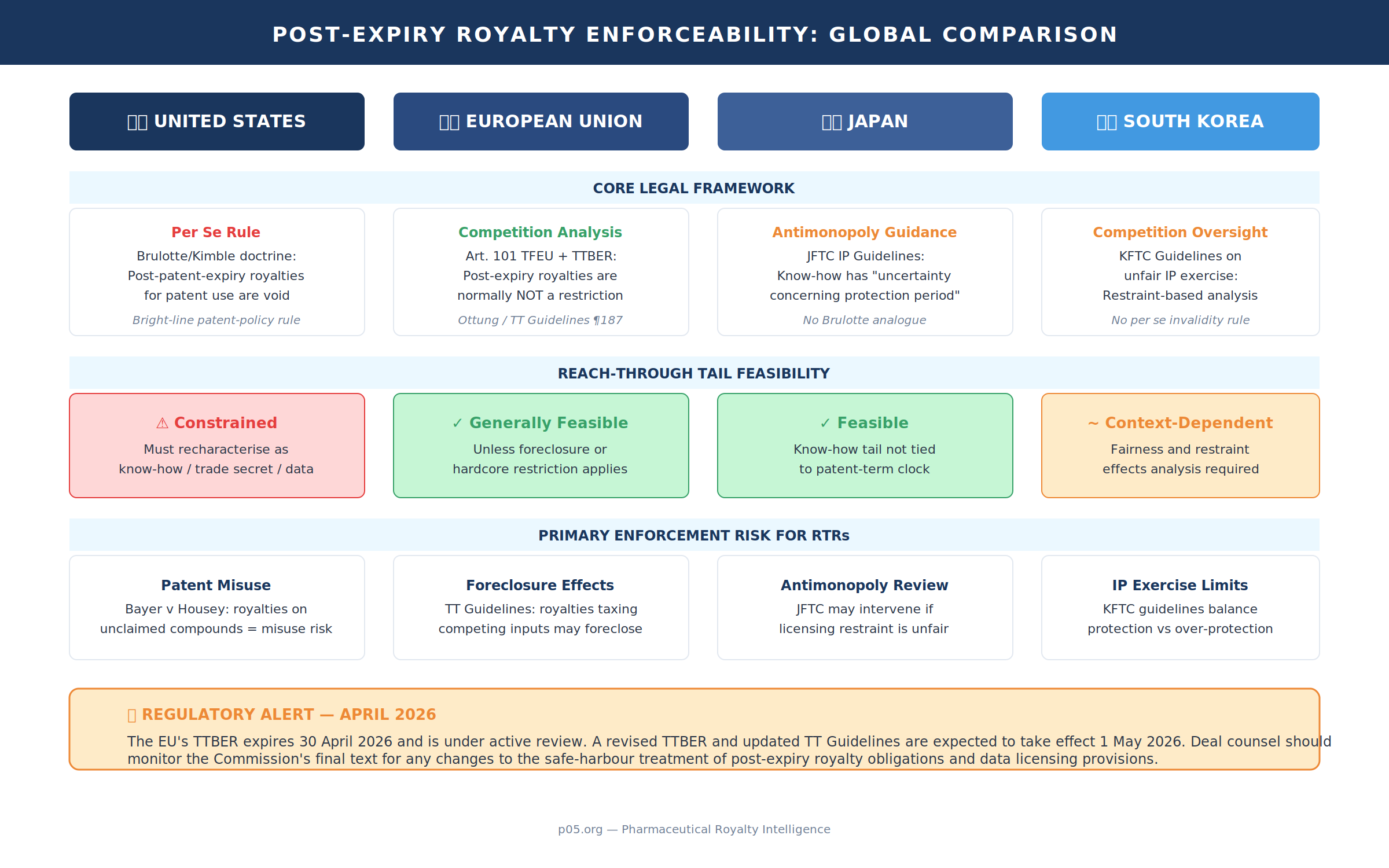

United States: Brulotte/Kimble as the guardrail — and the map around it

In US law, the bright-line policy constraint is the Supreme Court's post-expiration royalty doctrine. In Brulotte v Thys Co. the Court held that royalty provisions requiring payment "for the period beyond the expiration" of the licensed patents are unenforceable as an impermissible extension of the patent monopoly. In Kimble v Marvel Entertainment the Court reaffirmed Brulotte, again treating post-expiration royalties for use of a patent as unlawful per se under the doctrine.

But Kimble is equally important for its drafting implications: the Court explicitly notes that parties "can often find ways to achieve similar outcomes," including deferring payments for pre-expiration use, tying royalties to non-patent rights, or using non-royalty business arrangements. This is the conceptual doorway through which many reach-through structures pass: if the royalty is characterised as consideration for continuing access to know-how, trade secrets, biological materials, or data rights, rather than for the use of the patented invention, Brulotte risk can be managed (not eliminated).

The trade secret point matters because trade secret protection is not time-limited in the way patents are; WIPO states directly that trade secret protection has no temporal limit (patents last in general for up to 20 years). If a licence is credibly supported by continuing secrecy-based value (or continuing contractual access controls), the economic logic of the tail is straightforward:

NPV(RTR) = Σ [α × Net Sales(t)] / (1 + r)^t

The legal logic is the tricky part: the longer the tail, the more a counterparty will argue that the royalty is in substance payment for public-domain patent subject matter rather than for surviving non-patent rights.

Bayer v Housey demonstrates how quickly reach-through can be reframed as misuse when the royalty looks like patent-term extension by contract. Bayer alleged Housey demanded royalties on commercialised compounds not claimed in the licensed assay patents, and royalties continuing after expiry of the assay-method patents. The district court refused to dismiss Bayer's patent-misuse claim at the pleading stage, signalling that reach-through economics are scrutinised through patent-policy lenses when the structure appears to extend the patentee's statutory rights beyond claim scope and term.

Notably, the Third Circuit's September 2024 decision in Ares Trading v Dyax Corp. provided fresh clarity on this boundary. The court held that post-expiration royalties were permissible where the downstream product (Bavencio) would not have infringed the licensed patents even if they had still been in effect — essentially validating the reach-through model where the royalty is truly on the discovery contribution rather than on the use of patented subject matter. This decision is the most significant recent US judicial development for RTR practitioners.

European Union: competition-law framing is materially more permissive

EU doctrine is structurally different. Rather than a US-style Brulotte per se rule, the primary constraints are competition-law constraints (Article 101 TFEU) applied to technology transfer agreements, with "safe harbour" mechanics under the TTBER and the Commission's Technology Transfer Guidelines.

The Commission's 2014 Technology Transfer Guidelines state plainly that, although the block exemption applies only while technology rights are valid and in force, parties can normally agree to extend royalty obligations beyond the period of validity of the licensed intellectual property rights without falling foul of Article 101(1) of the Treaty. The stated rationale is that, once rights expire, third parties can legally exploit and compete, which will "normally be sufficient" to prevent appreciable anti-competitive effects.

CJEU case law has long supported that posture. In Ottung, the Court's summary indicates that an obligation to pay royalties for an indeterminate period, and thus after the expiry of the patent, does not in itself constitute a restriction of competition within Article 85(1) (now Article 101(1)) in the relevant context. The key EU intuition is that royalty duration is principally a contract/competition issue, not an intrinsic patent-policy violation.

Two practice implications follow.

First, under EU competition guidance, post-expiry royalties are generally a drafting and market-power problem, not a categorical invalidity problem. That makes "perpetual" reach-through tails more feasible in Europe than in the US — provided the clause does not become a foreclosure mechanism (for instance by effectively taxing third-party inputs or tying unrelated products).

Second, the TTBER regime itself is time-sensitive in 2026. The current TTBER expires on 30 April 2026 and has been under active review by the Commission. On 11 September 2025, the Commission published a draft for consultation of a revised TTBER and updated Technology Transfer Guidelines, with revised rules intended to come into force on 1 May 2026. While the evaluation confirmed that the TTBER and Guidelines have helped companies self-assess the antitrust compliance of their technology licences, it concluded they do not provide sufficient legal certainty. The revisions also respond to the growing significance of data licensing — directly relevant to AI-mediated reach-through — though many provisions important to pharma licensing (such as non-compete restrictions on licensees, exclusive grant-backs, and termination-on-challenge provisions) remain essentially unchanged. Deal counsel should monitor the Commission's final text closely for any changes to the safe-harbour treatment of post-expiry royalty obligations.

Japan and Korea: know-how and competition oversight rather than a Brulotte analogue

Japan's competition/IP interface is also framed through antimonopoly guidance rather than a US-style post-expiry doctrine. The JFTC's IP Guidelines highlight a core feature of know-how: unlike patents, it is not granted a statutory exclusive right, and it is characterised by (among other attributes) "uncertainty concerning the protection period." That observation aligns with the reach-through drafting strategy: if the economic bargain is credibly attributable to continuing know-how or access constraints, the tail is not automatically anchored to a 20-year patent clock.

Korea similarly addresses licensing restraints primarily through competition-law oversight and guidelines on unfair exercise of IP rights (rather than a categorical per se invalidity rule). Korea's OECD submission on licensing of IP rights and competition law situates IP licensing within the broader competition-law policy framework balancing protection and over-protection. For RTRs, the practical inference is that enforceability analysis will hinge on restraint effects and fairness constraints in the licensing relationship, not merely on patent-term arithmetic.

Policy and competition-law friction: NIH anti-encumbrance stance and misuse boundaries

RTRs are not merely private ordering. In life sciences, they sit inside a dense policy ecosystem that sometimes treats reach-through as an anti-transfer tax on scientific infrastructure.

NIH posture: minimise encumbrances, avoid reach-through in NIH-funded tool sharing

NIH's Research Tools Policy is unusually direct: NIH "expects" that agreements to acquire NIH-funded materials from not-for-profit entities for use in NIH-funded research "will not include" royalty reach-through or product reach-through rights back to the provider, describing such reach-through provisions as "inappropriate" in this context. The NIH Grants Policy Statement likewise points recipients to Research Tools Policy principles for dissemination and sharing of research tools.

This is not a universal prohibition on RTRs. It is a funding-policy and norm-setting stance: reach-through is treated as an encumbrance that can inhibit dissemination and downstream investment. For practitioners, it creates a bifurcated market: what universities may try to do as licensors in private deals can be constrained (or at least reputationally priced) when NIH-funded resources are involved.

Patent misuse boundary conditions: royalty base, coercion, and term extension

US "misuse" doctrine is the other friction vector. Zenith Radio v Hazeltine is the classic diagnostic: conditioning a patent licence on royalties for unpatented products can constitute misuse, though total-sales royalties may be permissible if adopted for mutual convenience rather than coercion. Reach-through royalties are not identical to "total-sales royalties," but they rhyme: both extend payment beyond the set of products covered by the licensed claims, and both raise the question whether the licensor used patent leverage to tax non-infringing value.

Bayer v Housey is the more targeted reach-through warning shot: Bayer alleged royalties on compounds not claimed by the assay patents and royalties continuing after patent expiry, and the court held the pleaded facts could support a misuse theory, refusing to dismiss the misuse claim. In effect, the court treated reach-through as a candidate mechanism for extending the patentee's statutory rights beyond reasonable claim scope and term.

Europe frames similar risks via competition analysis of royalty design. The Commission's Technology Transfer Guidelines caution that royalty structures may become hardcore restrictions where the licence is a sham or where royalties extend to products produced solely with the licensee's own technology rights. The same section warns that royalties based on products made with third-party technology can have foreclosure effects by increasing the cost of using competing inputs. This is not reach-through-specific, but it maps directly onto modern multi-tool discovery, where "use" can be argued across interdependent inputs.

Why contracts carry the reach-through load: EPO treatment of reach-through claims in patents

A final policy-lens point is that "reach-through" is not only contractual. In patent prosecution, "reach-through claims" are often viewed as attempts to claim future inventions (for example, claiming all agonists/antagonists identifiable by a screening method). The EPO Guidelines for Examination explain that such claims define compounds functionally and can impose an "undue burden" because one would have to test every known and conceivable future compound; the applicant is "attempting to patent what has not yet been invented," and claims should be limited to the actual contribution to the art.

This doctrinal hostility to patent-based reach-through claims pushes value capture into contract space. If patent law will not let the tool owner claim the downstream compound broadly, contract law becomes the substitute instrument — subject to misuse and competition constraints rather than sufficiency-of-disclosure constraints.

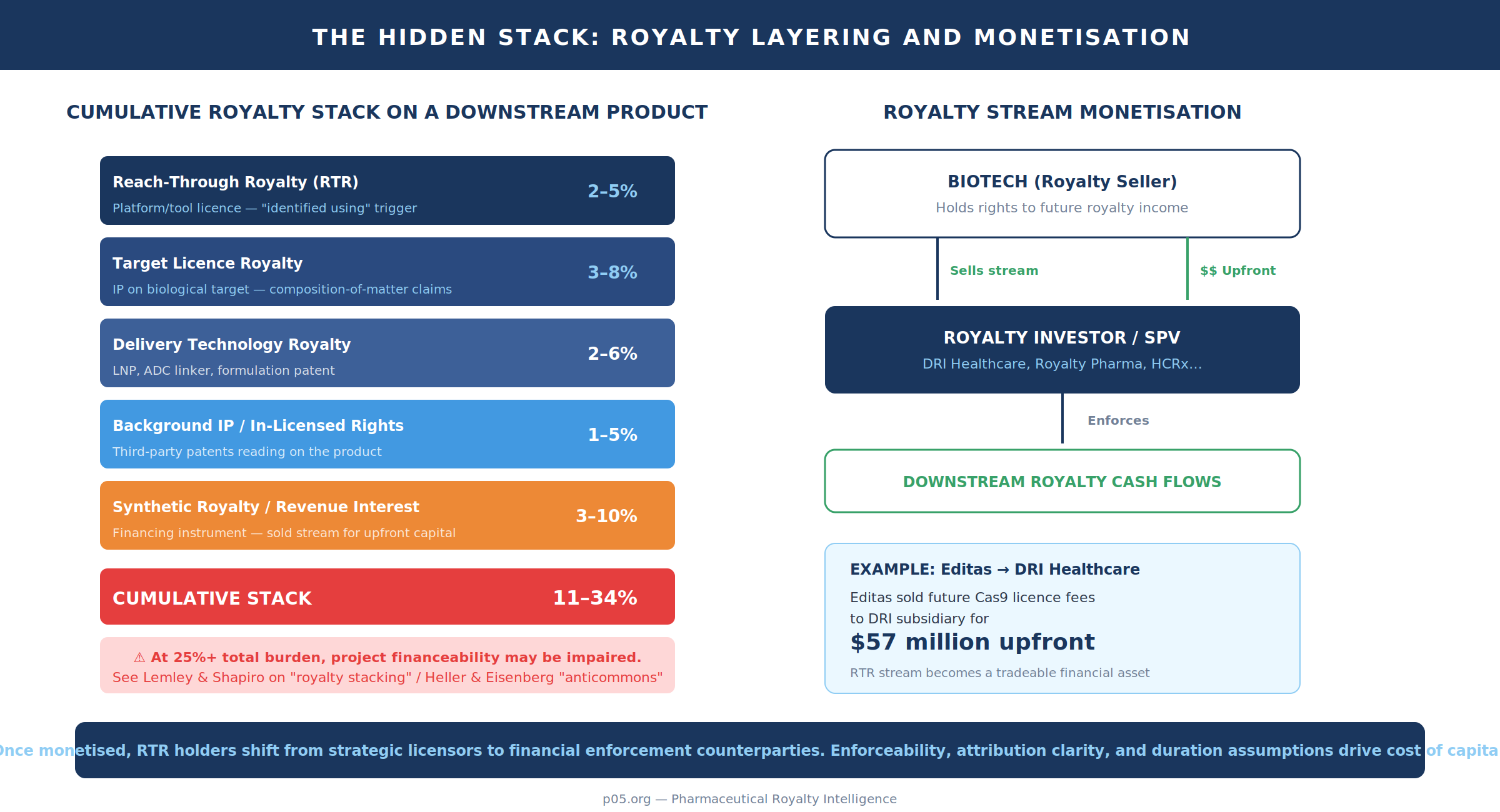

The hidden stack: layering reach-through with other royalties and financing instruments

Reach-through royalties are rarely solitary. They accumulate with target licences, delivery technology royalties, in-licensed background IP, and now synthetic royalty financings and revenue interests. The core arithmetic is simple:

Total Royalty Rate = Σ α(i)

The consequences are not. They include double marginalisation, impaired gross margins, reduced pricing flexibility (particularly in markets with payer pressure), and reduced M&A optionality once the royalty stack becomes visible in diligence.

The "royalty stacking" concept is well-developed in the academic and policy literature. Lemley and Shapiro describe royalty stacking as the situation when multiple patents read on a single product, and argue holdup problems are magnified in its presence. While their central case studies are in complex products and standards, the analytical structure translates to biotech pipelines built on layered platforms: multiple licensors, each pricing a small slice of downstream value, can produce a cumulative rate inconsistent with the licensee's required return on capital.

Life sciences have long had a related concern framed as an "anticommons": too many upstream rights can cause underuse of resources and impede downstream development. Heller and Eisenberg's canonical work states that proliferation of IP rights can create an anticommons in which resources are underused because too many owners can block each other. Reach-through royalties can behave like "soft blocks" (a tax rather than a veto), but the economic effect can be similar if cumulative tolls destroy project financeability.

Modern contracts actively manage this stack, and the Editas/Broad agreement provides a public example of how. It contains explicit royalty-offset logic: if the company is legally required to pay third-party running royalties necessary to commercialise a licensed or enabled product, it may credit up to a capped percentage of those royalties against royalties payable under the agreement, with aggregate caps. That is a contractual recognition that stacking is not hypothetical — it is statistically expected over a platform's downstream life.

Financial engineering sits on top of the IP stack. Royalty financings and revenue monetisations are increasingly used to raise capital by selling rights to actual or potential royalty/income streams for upfront lump sums. PwC has noted the growing frequency of life sciences companies monetising revenues from existing products, with ring-fenced cash flows including royalties. The total value of royalty deals has been growing at a compound annual growth rate of roughly 45%, compared with approximately 25% for equity deals over a recent four-year period, according to a ZS analysis. Royalty Pharma alone struck deals potentially worth close to $2 billion in May 2024, including the $525 million acquisition of royalties and milestones for ImmuNext's anti-CD40 therapy frexalimab.

For reach-through, the implication is that the "hidden stack" is no longer only an operating-company issue; it is an asset-pricing issue. Once a downstream product exists and payment logic is clear, an RTR stream can be carved out, collateralised, or sold. The cost of capital then depends on enforceability, attribution clarity, and duration tail assumptions.

AI platforms: attribution collapse, foundation-model throughput, and drafting responses

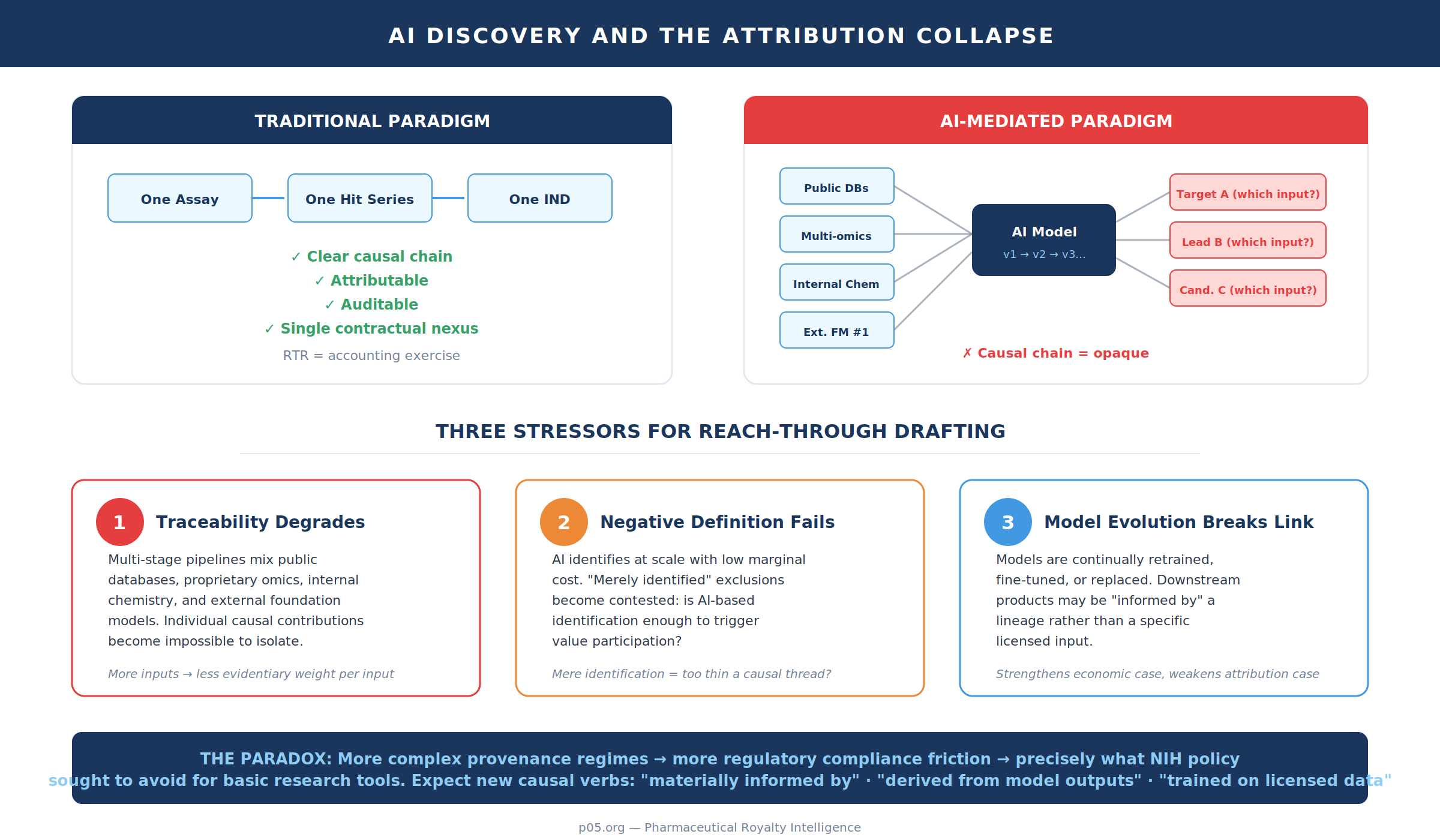

AI-driven discovery pushes reach-through from a "single assay, single hit" paradigm into a "model-mediated inference" paradigm. The contractual question becomes: when a target, binder, lead series, or candidate is proposed by a model trained on proprietary data, is the model a mere tool, or is it foundational enabling infrastructure whose contribution is economically closer to co-development?

The pace and scale of model proliferation matter. A 2025 drug discovery review on foundation models reports that, starting in 2022, the number of foundation models has surged, with more than 200 such models published to date, spanning applications including target discovery and molecular optimisation. In parallel, 2025 marked AI's graduation from point solutions to platform-scale engines for discovery, with developments including AlphaFold3's expanded structural predictions covering DNA/RNA, ligands, and antibody-antigen complexes, the Recursion–Exscientia merger integrating phenomic screening with automated precision chemistry, and open-source alternatives like OpenFold3 and Boltz-2 delivering commercially usable co-folding capabilities.

Nearly 100 partnerships between AI vendors and Big Pharma have formed since 2015, with acceleration visible in 2024–2025 — Sanofi signed a potential $1.2 billion collaboration with Insilico Medicine, and Novartis partnered with Isomorphic Labs to leverage AlphaFold technology. The FDA released draft guidance in January 2025 on using artificial intelligence to support regulatory decision-making for drug and biological products, providing the first formal framework for AI-discovered compounds — but the IP attribution questions remain largely unaddressed by regulators.

In this environment, traditional reach-through drafting faces three stressors.

First, traceability degrades. In a multi-stage pipeline — public databases, proprietary multi-omics, internal chemistry, external foundation models — individual causal contributions become hard to isolate. The contract's list of verbs (identified, optimised, characterised, selected) is attempting to solve precisely this: it wants "use" to include informational dependence, not merely physical incorporation. But as the number of inputs rises, the evidentiary weight of any single input falls.

Second, the "negative definition" problem gets harder. The Editas agreement's exclusion of certain molecules that are merely "identified or discovered" using the tool shows an attempt to constrain reach-through to products that more robustly embody or depend on the licensed technology. In AI contexts, where "identification" may occur at large scale and with low marginal cost, licensors and licensees will increasingly fight over whether "identification" alone should trigger value participation. The exclusion language is a clue: even tool owners sometimes concede that mere identification is too thin a causal thread to bear a downstream annuity.

Third, longevity and "model evolution" complicate the consideration story. When the licensor's continuing value proposition is proprietary data or model weights (often protected as trade secrets, and not time-limited), the economic case for post-patent tails strengthens. But model evolution also weakens the attribution case: if the deployed model is continually retrained, fine-tuned, or replaced, the downstream product may be "informed by" a lineage rather than a specific licensed input. That is fertile ground for disputes over whether the contractual nexus remains satisfied several years and several training cycles later.

One should therefore expect contractual countermeasures to move in two directions: more expansive causal verbs ("materially informed by," "derived from model outputs," "trained on licensed data") and more operational audit/traceability mechanisms (logging requirements, model-card style provenance, and definitional safe harbours). The paradox is that the more complex the provenance regime, the more it begins to resemble a regulatory compliance system — precisely the kind of friction NIH policy sought to avoid for basic research tools.

Enforceability, M&A friction, and monetisation: from diligence surprises to tradable cashflows

The enforcement risk in reach-through is not only whether the clause is valid; it is whether it is provable. That is why reach-through is simultaneously attractive to licensors (it prices upside across unknown futures) and unattractive to downstream acquirers (it imports unpriced tail liabilities into enterprise value).

US doctrine provides multiple ways for a reach-through arrangement to become an enforcement target. Brulotte/Kimble remains a hard constraint when the royalty is plausibly payment for the use of patented subject matter post-expiry. Bayer v Housey illustrates a different attack surface: royalties on unclaimed downstream compounds and royalties continuing after expiry were pleaded as misuse, and the court allowed the misuse claim to proceed — an early judicial willingness to "look through" the contract structure to assess whether it extends patent leverage beyond permissible scope.

In the EU, by contrast, the Commission's TT Guidelines and CJEU summaries indicate that post-expiry royalty obligations are usually not a competition restriction per se, and parties can normally agree to extend royalty obligations beyond IP validity without infringing Article 101(1). That tends to shift M&A attention from "is it void?" to "how expensive is it, how defensible is it, and can we renegotiate it?"

The Editas/Broad licence again signals where sophisticated markets are going. The agreement anticipates royalty stacking and provides offset mechanics for third-party royalties necessary for commercialisation, with caps and pro-rata allocation across related agreements. This is not merely accounting: it is an enforceability stabiliser, because it reduces the probability that the royalty stack renders the product commercially irrational (and thus reduces the incentive for the licensee to litigate or to seek declaratory relief).

Monetisation transforms the stakes again. Once a royalty stream is sold or securitised, the holder is no longer a strategic licensor with a broader relationship; it is a financial counterparty optimised to enforce payment. The market is expanding rapidly: the total value of royalty deals has been growing at roughly twice the rate of equity deals, and specialist buyers like Royalty Pharma struck deals potentially worth close to $2 billion in May 2024 alone, including the $525 million acquisition of royalties and milestones for ImmuNext's anti-CD40 therapy frexalimab.

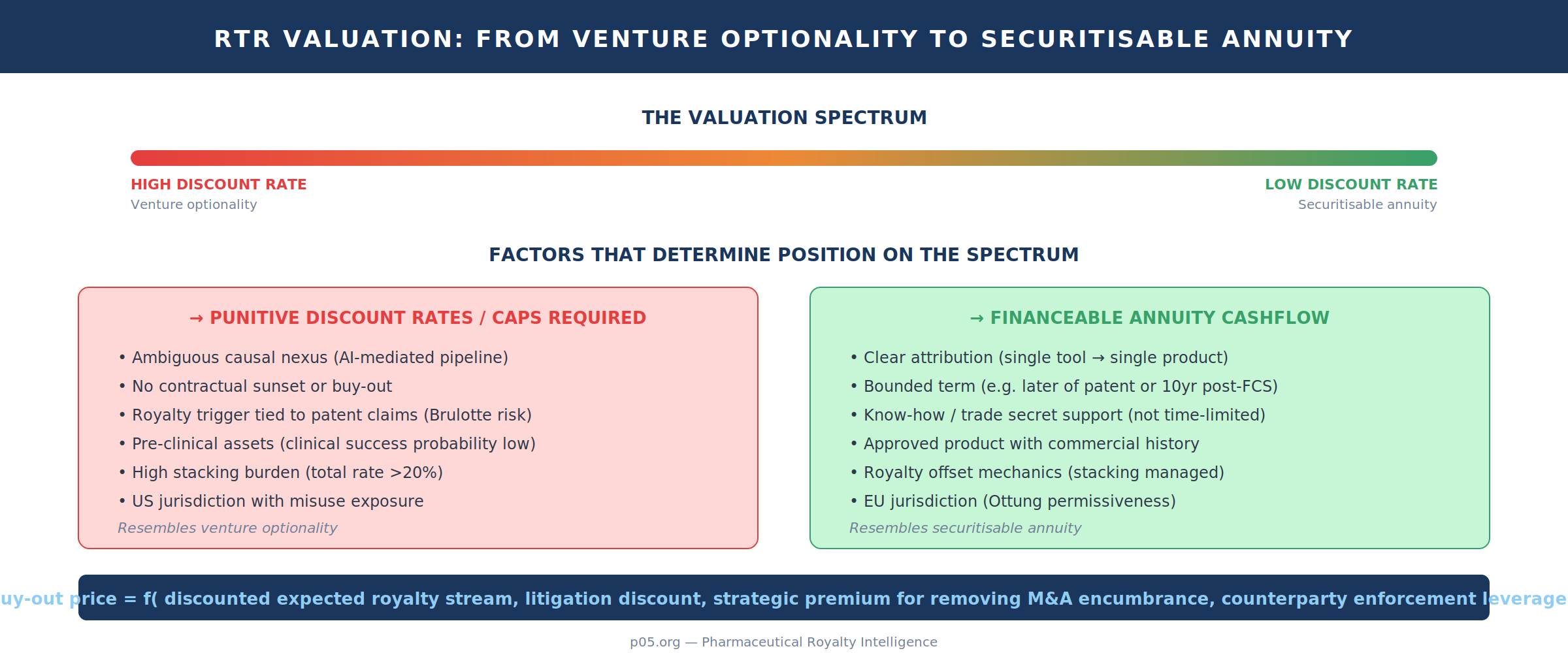

This is where "perpetuity" becomes less rhetorical. The longer and cleaner the tail, the more it resembles a financeable annuity — subject to the standard biopharma caveats of patent cliffs, competitive entry, and lifecycle-management dynamics. Conversely, the more ambiguous the causality (especially in AI-mediated pipelines), the more the stream resembles venture optionality rather than a securitisable cashflow, and the more capital markets will demand either punitive discount rates or contractual de-risking (caps, buy-outs, sunsets, and provenance obligations).

Valuation as pipeline optionality: tails, discount rates, and buy-outs

RTR valuation is a non-linear object because the underlying assets often do not exist at contract signature. At time zero, the licensor owns an entitlement whose payoff distribution is a function of (i) platform adoption, (ii) project selection, (iii) clinical success probabilities across multiple assets, (iv) commercial outcomes, and (v) contract interpretation over causality and scope.

A generic risk-adjusted expected value is:

E[NPV(RTR)] = Σ p(j) × Σ [α × Sales(j,t)] / (1 + r)^t

where N may itself be endogenous to the tool's adoption (and, in AI, to the throughput of computational lead generation).

The "perpetuity" intuition arises when (a) the royalty trigger is not tied to a patent claim set, (b) know-how or data access rights persist, and (c) there is no contractual sunset or buy-out. Because trade secret protection is not time-limited in principle, and can therefore provide a doctrinal anchor for long-lived contractual consideration, the economic tail can be long even when patents expire. The contractual analogue is an annuity-like stream whose valuation is highly sensitive to the discount rate and terminal erosion assumptions.

The Editas/Broad licence shows a particularly instructive hybrid tail design. "Royalty Term" is defined (country-by-country and product-by-product) as ending on the later of (a) expiry of the last valid claim covering the product/service or (b) the tenth anniversary of first commercial sale of the relevant licensed or enabled product/service. Moreover, once the last valid claim covering a licensed product/service expires, the agreement deems the product/service an "Enabled Product/Enabled Service" and applies enabled-category royalty rates for the remainder of the royalty term.

This is not true perpetuity, but it is explicitly designed to survive patent expiry — while still being bounded by an agreed post-launch time window.

Buy-outs — when they exist — are therefore not merely about "paying off a percentage of sales." They are negotiated prices on a complex stochastic stream under legal uncertainty. The negotiating range is often set by (i) a discounted expected royalty stream, (ii) a litigation discount for causality disputes, (iii) a strategic premium for removing an encumbrance in M&A or financing, and (iv) the counterparty's ability to threaten enforcement (including audit rights, reporting burdens, and termination leverage).

Europe's competition-law framework makes the duration question more of a "does it foreclose competition?" analysis than a "does it offend patent policy?" analysis. The Commission's TT Guidelines explicitly contemplate that royalty obligations can extend beyond IP validity without normally breaching Article 101(1). That predictably affects pricing: if enforceability risk is lower, the discount applied to the tail is lower — unless causality is itself unprovable.

The unresolved policy tension

The unresolved policy tension is therefore not whether reach-through is "good" or "bad." It is whether, in any given ecosystem, the reach-through annuity is economically proportional to the upstream contribution, and whether the legal system will treat the clause as legitimate private ordering or as an attempt to recreate, by contract, a property right that patent law refused to grant or refused to extend.

The EPO's stance on reach-through patent claims — limiting claims to the actual contribution and rejecting functionally defined future inventions — foreshadows the regulatory instinct in one domain; contracts are now testing how far the same instinct will migrate into licensing doctrine.

For dealmakers and royalty investors, the practical takeaway is threefold.

First, jurisdiction matters enormously: the same RTR clause may be robust in Europe, fragile in the US, and untested in Asia.

Second, AI-mediated pipelines are eroding the evidentiary foundations that made traditional RTR drafting workable — expect the next generation of disputes to centre on "materially informed by" language and model-provenance obligations.

Third, as RTR streams become tradable financial assets through monetisation, the enforcement posture shifts from relationship-based licensing to financial-counterparty optimisation — and the discount rate applied by capital markets will increasingly reflect not just clinical risk, but attribution risk and jurisdictional enforceability.

The contractual tail, in other words, is only as valuable as the causal thread that sustains it.

All information in this report was accurate as of the research date and is derived from publicly available sources including SEC filings, court opinions, regulatory guidance, academic literature, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.

Member discussion