Reverse Morris Trusts in Pharma: When Tax Engineering Meets Royalty Reality

The Reverse Morris Trust has become Big Pharma's favourite instrument for shedding non-core assets without triggering billions in corporate tax. But for royalty investors, royalty holders, and licensors who have carefully structured their claims against a specific counterparty, an RMT is not just a tax-efficient divestiture — it is a corporate earthquake that can fundamentally alter the identity of the entity obligated to pay them, the creditworthiness behind their cash flows, and the strategic incentives governing their product's commercialization.

When Pfizer used an RMT to combine its Upjohn off-patent medicines business with Mylan to form Viatris in November 2020, royalty holders on products like Lipitor, Lyrica, and Viagra suddenly found themselves looking across the table at a completely different company. Their counterparty was no longer Pfizer — one of the most creditworthy pharmaceutical companies on earth — but a newly minted, heavily leveraged generics company with $24.5 billion in debt and a fundamentally different commercial strategy. That shift happened without a single dollar changing hands in a conventional acquisition. And by February 2025, S&P had downgraded Viatris from BBB- to BB+ — pushing it below investment grade entirely.

This is the paradox of the Reverse Morris Trust for royalty stakeholders. The structure is explicitly designed to avoid the tax consequences of a sale, yet its economic effect on downstream royalty and licensing arrangements can be every bit as disruptive as an outright acquisition. For anyone holding royalties, licensing agreements, or structured financing arrangements secured by pharmaceutical cash flows, understanding how RMTs work — and how they interact with the contractual protections discussed in our previous analysis of change-of-control triggers — is no longer optional.

What Is a Reverse Morris Trust?

A Reverse Morris Trust is a transaction structure unique to U.S. tax law that allows a corporation to divest a subsidiary or business line without incurring corporate-level tax on the transfer. It combines two otherwise separate corporate events — a tax-free spin-off under IRC Section 355 and a tax-free merger under IRC Section 368 — into a single choreographed sequence.

The parent company first separates the unwanted business into a new subsidiary, distributes that subsidiary's shares to its own shareholders, and then immediately merges the subsidiary with a pre-arranged buyer. The critical legal requirement is that the parent company's shareholders must retain more than 50% ownership of the combined entity after the merger, which means the buyer must be roughly the same size or smaller than the divested business.

The structure takes its name — somewhat misleadingly — from a 1966 case involving a North Carolina bank and its insurance department. In the original Morris Trust, the parent company itself merged with the buyer after spinning off an unwanted division; in the "reverse" variant, it is the spun-off subsidiary that merges with the buyer.

The reverse form has become dominant in modern practice because it is mechanically simpler and avoids certain state transfer taxes. In the pharmaceutical industry, where multi-billion dollar portfolio divestitures have become routine, the RMT has emerged as the preferred structure for separating mature product lines, generics businesses, and consumer healthcare operations from innovation-focused parent companies.

The Mechanics: How an RMT Actually Works

The Reverse Morris Trust traces its origins to a 1966 Fourth Circuit ruling in Commissioner v. Mary Archer W. Morris Trust, 367 F.2d 794. In that case, American Commercial Bank needed to divest its insurance department before merging with a nationally chartered bank that could not legally operate such a business.

The court blessed the spin-off of the insurance business immediately prior to the merger as tax-free under Section 355, finding that the active business requirement was satisfied even though the distributing corporation merged into another entity immediately afterward.

The IRS acquiesced in Rev. Rul. 68-603, and for three decades companies used this structure to divest assets tax-free. Congress partially curtailed the strategy in 1997 by enacting Section 355(e) — the "anti-Morris Trust" provision — but the Reverse Morris Trust variant survives because it satisfies the critical ownership continuity requirement.

The modern RMT combines two distinct corporate transactions into a single, choreographed sequence designed to achieve what neither transaction alone could deliver on a tax-free basis.

Step 1: Separation. The parent company (ParentCo) transfers the assets it wants to divest into a new subsidiary (SpinCo). This separation involves carving out operations, contracts, employees, intellectual property, and liabilities into a standalone entity capable of operating independently.

Step 2: Distribution. ParentCo distributes SpinCo shares to its own shareholders, typically through a pro rata spin-off or, less commonly, a split-off (an exchange offer in which shareholders tender ParentCo shares for SpinCo shares). Under IRC Section 355, this distribution is tax-free to both ParentCo and its shareholders, provided it satisfies several stringent requirements including the active trade-or-business test (both entities must have been engaged in active business for at least five years), the business purpose requirement, and the device prohibition.

Step 3: Combination. Immediately following the distribution, SpinCo merges with a pre-identified merger partner (the Buyer). The merger is structured as a tax-free reorganization under IRC Section 368. Because the merger follows the spin-off, it is the Buyer that combines with SpinCo — the "reverse" in Reverse Morris Trust — rather than the more intuitive structure where the Buyer acquires SpinCo directly from ParentCo.

The critical constraint: after the combination, former ParentCo shareholders must retain more than 50% of the vote and value of the combined entity. This ownership requirement, embedded in Section 355(e), is what distinguishes a legitimate RMT from a disguised taxable sale. It means the Buyer must be approximately the same size as or smaller than SpinCo. If former ParentCo shareholders end up with less than 50%, the spin-off loses its tax-free status retroactively, and ParentCo faces corporate-level tax on the distribution — potentially billions of dollars.

The Pfizer-Mylan transaction illustrated these mechanics precisely. Pfizer transferred the Upjohn business into a new subsidiary (Upjohn Inc., organized in Delaware on February 14, 2019), distributed the shares to Pfizer shareholders, and then merged Upjohn Inc. with Mylan. Post-combination, Pfizer shareholders owned 57% and Mylan shareholders owned 43% — comfortably above the 50% threshold. The carve-out spanned more than 100 jurisdictions in which the Upjohn business had been an integrated part of Pfizer's operations.

Why Big Pharma Loves the RMT

The appeal is straightforward: an RMT allows a large pharmaceutical company to divest a multi-billion dollar business line without paying corporate-level tax on the transaction. In a conventional asset sale or stock sale, the selling company would typically recognize taxable gain equal to the difference between the sale price and its tax basis in the divested assets. For a business that has appreciated substantially — as most pharmaceutical portfolios have — that tax bill can run into the billions.

Consider the arithmetic. If Pfizer had simply sold the Upjohn business (with approximately $10.2 billion in 2019 revenue, according to its SEC filings) at a market-implied enterprise value in the $25–30 billion range, the corporate-level tax at the then-prevailing 21% rate could have exceeded $4–5 billion, depending on Pfizer's tax basis. By structuring the transaction as an RMT, that tax liability was eliminated entirely.

The RMT also solves a strategic problem that simple spin-offs cannot. A standalone spin-off creates an independent company that must compete for management talent, investor attention, and capital markets access on its own. By combining the spun-off business immediately with an established merger partner — Mylan, in this case — the resulting entity has greater scale, operational infrastructure, and public market presence than SpinCo would have achieved alone. As Macabacus notes, this is precisely why the Reverse Morris Trust is generally preferred over the Regular Morris Trust: it is mechanically simpler, often avoids state transfer taxes, and delivers a combined entity with immediate operational viability.

For the pharmaceutical industry specifically, RMTs have proven particularly well-suited for three recurring scenarios. The first involves the divestiture of mature, off-patent product portfolios that no longer fit an innovation-focused strategy but that generate substantial cash flows (Pfizer-Upjohn/Mylan is the canonical example). The second involves the separation of consumer healthcare businesses from prescription pharmaceutical operations, a trend that has accelerated dramatically since 2020. The third involves the separation of generics or biosimilar businesses from branded operations, allowing each to pursue distinct commercial and R&D strategies.

The Royalty Investor's Nightmare: Counterparty Transformation

For a royalty investor, an RMT creates a fundamentally different risk than a conventional acquisition. In a standard M&A transaction, the acquirer absorbs the target's obligations — including royalty and licensing commitments — and the acquirer's balance sheet stands behind those obligations going forward. Change-of-control triggers, as we explored in our previous article, can force buyouts, consent requirements, or renegotiation to protect the investor's position.

An RMT inverts this dynamic in a way that can be deeply problematic.

The entity obligated to pay the royalty is SpinCo — the carved-out subsidiary. When SpinCo merges with the Buyer, the royalty obligation transfers to the combined entity by operation of law through the statutory merger mechanism. No assignment occurs; no consent is required under generic anti-assignment language; and unless the royalty agreement specifically contemplates this exact transaction structure, no change-of-control trigger fires.

The result is a form of counterparty arbitrage. Before the RMT, the royalty was backed by the full faith and credit of ParentCo — a AAA-rated pharmaceutical giant with $50 billion in annual revenue. After the RMT, the royalty is backed by the combined SpinCo-Buyer entity — which may be significantly more leveraged, less diversified, and less creditworthy. ParentCo has shed the obligation entirely, without ever technically "assigning" or "selling" the contract.

In the Pfizer-Viatris example, this shift was dramatic. Pfizer's long-term debt was rated A+ by S&P and A1 by Moody's. Viatris launched with approximately $24.5 billion in debt and a BBB- rating from S&P (Baa3 from Moody's) — already at the lowest rung of investment grade. The trajectory worsened from there: S&P placed Viatris on negative outlook in April 2024, and in February 2025 downgraded the company to BB+ — pushing it below investment grade entirely. A royalty investor who had priced their return assumptions based on Pfizer's credit profile in 2019 saw their counterparty fall five notches in under five years — from A+ to junk.

Moreover, the commercial incentives governing the product can shift materially. Pfizer, as an innovation-focused company, had certain strategic reasons to maintain products like Lipitor and Lyrica — they contributed to physician relationships, its presence in primary care, and its overall commercial infrastructure. Viatris, as a generics-focused company, approached these same products purely as cash-flow-generating assets to be optimized for profitability and eventually harvested. By late 2023, Viatris had already announced agreements to divest approximately $3.6 billion in businesses, including its OTC, women's healthcare, and Indian API operations — further fragmenting the portfolio that royalty holders depended upon.

The Delaware Problem, Revisited

The legal architecture that makes RMTs so dangerous for royalty holders traces back to the same Delaware doctrine discussed in our previous article on change-of-control triggers.

Under Delaware's Meso Scale Diagnostics v. Roche Diagnostics framework, a merger transfers contractual obligations by operation of law — not by assignment. The surviving entity in a merger is automatically vested with the disappearing entity's contracts without any act of assignment. This means that standard anti-assignment provisions, which prohibit "assignment, delegation, or transfer" of the contract without consent, are powerless to prevent the transfer.

The RMT compounds this vulnerability because it involves two sequential transactions, each of which raises distinct legal questions. The spin-off distributes SpinCo shares to ParentCo's shareholders — but does this constitute a "change of control" of SpinCo? Technically, SpinCo has gone from being 100% owned by ParentCo to being owned by ParentCo's dispersed public shareholders. The identity of the ultimate economic owner has changed, but the mechanism is a distribution rather than an acquisition.

The subsequent merger of SpinCo with the Buyer clearly constitutes a change-of-control event under most conventional definitions — the Buyer's shareholders acquire a stake in the combined entity, and the Buyer's management typically runs the combined company (as happened with Viatris, where Mylan's Robert Coury became Executive Chairman and Mylan named eight of thirteen board members). But if the royalty agreement defines change of control solely by reference to ParentCo's ownership of the royalty-paying subsidiary, the spin-off itself may have already satisfied the trigger — leaving the merger as a separate event that may or may not be captured.

The problem is one of drafting precision. Most change-of-control provisions were written to capture two scenarios: someone buys more than 50% of the company's stock, or the company sells substantially all of its assets. An RMT fits neither pattern cleanly. ParentCo doesn't sell the subsidiary — it distributes it. No single acquirer buys more than 50% of SpinCo — instead, SpinCo merges with a smaller entity while retaining majority shareholder continuity. As the Harvard Law School Forum on Corporate Governance has observed, the key to the tax-free nature of an RMT is precisely that historic stockholders of the distributing parent retain control — the very feature that makes change-of-control triggers fail to activate.

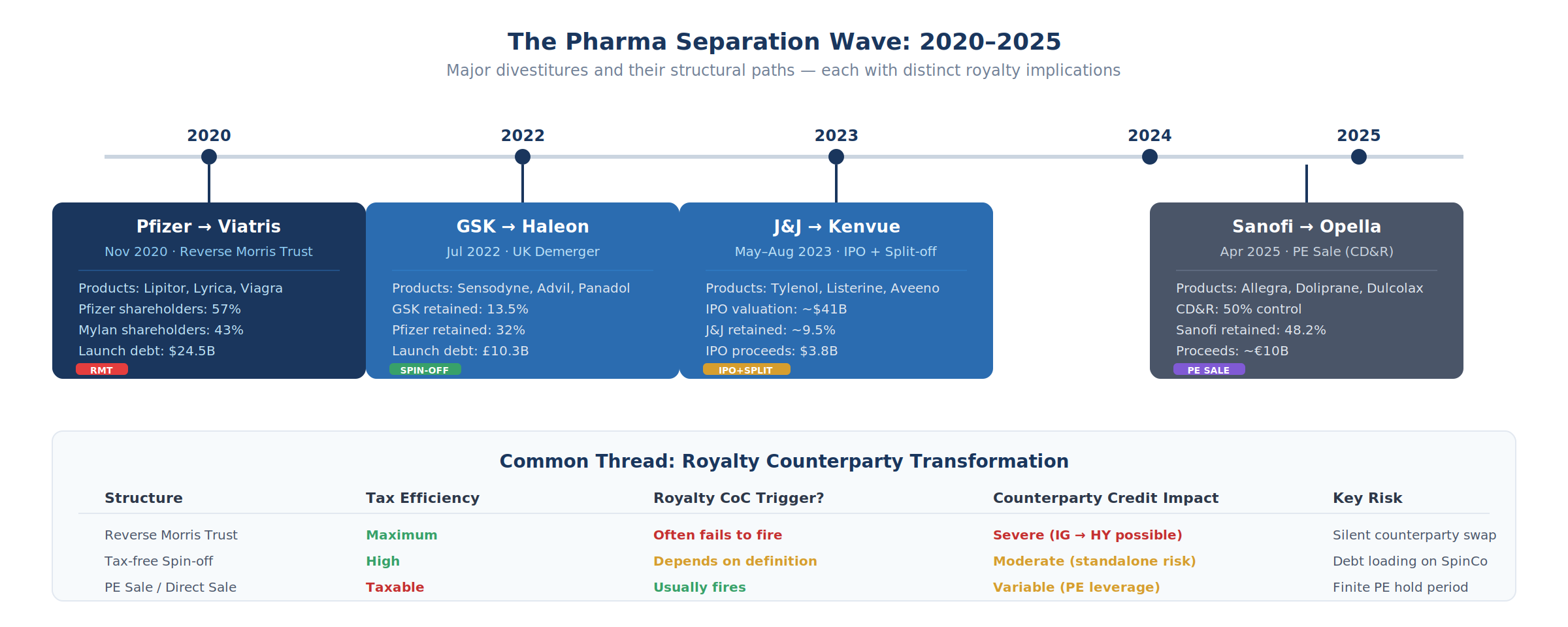

The Pharma Separation Wave: RMTs and Their Cousins

The period from 2019 to 2025 has produced an unprecedented wave of pharmaceutical separations, with companies divesting consumer healthcare, generics, and mature product portfolios. While not all used the Reverse Morris Trust structure specifically, the wave illustrates the broader trend and its implications for royalty stakeholders.

Pfizer-Upjohn/Mylan → Viatris (2020): The Defining RMT

The Pfizer transaction remains the defining pharma RMT. Pfizer contributed its Upjohn off-patent business — including Lipitor ($2.0 billion in 2019 sales), Lyrica ($3.3 billion pre-LOE), Viagra, Norvasc, and dozens of other products — into Upjohn Inc. The carve-out was extraordinarily complex: Clifford Chance, advising Pfizer, described deploying a custom legal tech solution to manage complexity across more than 100 jurisdictions. Upjohn was then spun off to Pfizer shareholders and immediately merged with Mylan in what the companies described as an "all-stock, Reverse Morris Trust transaction." Cravath, Swaine & Moore represented Mylan; Skadden advised on the tax structuring.

The royalty implications were substantial. Any entity holding royalty or milestone rights tied to these products — whether university licensors, co-development partners, or royalty investors — saw their counterparty shift from Pfizer (market cap approximately $200 billion) to Viatris (market cap approximately $16 billion at launch). The credit differential alone represented a meaningful increase in counterparty risk. And the transaction was structured to be tax-free to Pfizer and its shareholders while taxable to Mylan shareholders — illustrating how the tax benefits flow asymmetrically in an RMT.

Johnson & Johnson → Kenvue (2023): The IPO-Plus-Exchange Path

Johnson & Johnson's separation of its consumer health business into Kenvue took a different structural path — an IPO followed by a split-off exchange offer — but raised analogous concerns for royalty holders. J&J first conducted a $3.8 billion IPO for approximately 10% of Kenvue's shares in May 2023 (the largest U.S. IPO since Rivian in 2021), then completed the separation through a voluntary exchange offer in August 2023 in which it distributed at least 80.1% of Kenvue shares — the minimum required for tax-free treatment under Section 355.

The exchange offer was 4.2× oversubscribed, reflecting strong shareholder demand at the 7% discount offered. J&J retained approximately 9.5% of Kenvue following completion. But Kenvue's subsequent performance illustrated the risks of newly separated entities: shares traded below IPO price within months amid securities class action litigation alleging misleading disclosures regarding phenylephrine efficacy, and by March 2025 activist investor Starboard had acquired a stake and taken a board seat.

GSK → Haleon (2022): The UK Demerger

GSK's spin-off of Haleon in July 2022 was structured as a UK demerger — the domestic equivalent of a Section 355 distribution — and represented the biggest European listing in more than a decade, with a market valuation of approximately £30.5 billion. The consumer healthcare business, originally a joint venture between GSK (68%) and Pfizer (32%) formed in 2019, was distributed to GSK shareholders, with Pfizer retaining its 32% stake in Haleon directly. GSK held approximately 13.5% post-demerger, with the remaining shares held by GSK shareholders.

Haleon launched with approximately £10.3 billion in debt — transferred from GSK as part of the separation mechanics. Analysts at Barclays described the debt load as "significant" at approximately 4× estimated earnings. For any royalty or licensing arrangements tied to consumer healthcare products within the portfolio, the shift from GSK's diversified pharmaceutical balance sheet to Haleon's standalone consumer health operation represented a material change in counterparty profile.

Sanofi → Opella (2025): The Private Equity Variant

Sanofi's separation of its consumer healthcare business, Opella, took yet another path — a sale of a 50% controlling stake to private equity firm Clayton, Dubilier & Rice (CD&R) that closed in April 2025. The valuation was based on an enterprise value of approximately €16 billion (roughly 14× estimated 2024 EBITDA). Sanofi retained a 48.2% stake, with Bpifrance acquiring 1.8%, and received approximately €10 billion in net cash proceeds.

While not an RMT (Sanofi sold its stake for cash, triggering a taxable event), the transaction illustrates how the structural path affects royalty holders differently. Because Sanofi chose a direct sale to PE rather than a tax-free spin-off or RMT, change-of-control triggers in licensing agreements tied to Opella products were more likely to fire — giving royalty holders the opportunity to exercise put options, require consent, or renegotiate terms. The trade-off for Sanofi was paying tax on the gain but receiving immediate cash. For royalty holders, the PE ownership model brings a different set of concerns: finite investment horizons, leverage-driven return expectations, and the possibility of secondary buyouts or eventual IPO that could trigger additional change-of-control events.

Structural Vulnerability: Why Standard Protections Fall Short

The standard toolkit of royalty investor protections — anti-assignment clauses, change-of-control triggers, put/call options — was designed for a world of bilateral transactions where Company A acquires Company B. The RMT challenges each of these mechanisms in specific ways.

Anti-Assignment Clauses

As discussed above, anti-assignment provisions are largely useless against RMTs. The merger step transfers obligations by operation of law, not by assignment. Even broadly drafted provisions that include "transfer by merger, consolidation, or operation of law" may not capture the full RMT sequence, because the entity performing the merger (SpinCo) is a newly created subsidiary — not the original contracting party.

Consider the sequence: ParentCo enters into a royalty agreement. ParentCo then transfers the underlying product and the royalty obligation to SpinCo as part of the internal separation. SpinCo is then distributed to shareholders and merges with the Buyer. The royalty holder's original counterparty is ParentCo, but at no point does ParentCo "assign" the agreement — it transfers it to a wholly-owned subsidiary (which may be permitted under affiliate transfer carve-outs), and the subsidiary then merges with a third party.

Each individual step may be permissible under the contract, even though the aggregate effect — replacing ParentCo with a fundamentally different combined entity — is exactly what the anti-assignment clause was designed to prevent.

Change-of-Control Definitions

Standard change-of-control definitions capture acquisitions of more than 50% of voting stock. But in an RMT, no single party acquires more than 50% of SpinCo. The Buyer's shareholders receive less than 50% of the combined entity (that is the entire point of the 50% test under Section 355(e)). Former ParentCo shareholders retain majority ownership, even though they are now dispersed public shareholders rather than a single controlling entity.

The question becomes: does the loss of ParentCo's 100% ownership of the subsidiary constitute a "change of control"? If the definition requires acquisition of a specified percentage by a "person" or "group," the answer may be no — because no single person or group has acquired the shares. They were distributed pro rata to existing shareholders.

Dual-tier definitions that capture both entity-level changes and asset-level dispositions — of the kind negotiated by Healthcare Royalty Partners in the La Jolla agreement discussed in our previous article — offer better protection. If the royalty agreement triggers upon the product being held by an entity other than the original contracting party or its wholly-owned subsidiaries, the RMT should activate the trigger when SpinCo merges with the Buyer (since the combined entity is no longer wholly owned by ParentCo).

Put/Call Options

Even where change-of-control triggers successfully fire, the put/call economics may be distorted. The formula price in most royalty financings — typically 1.3× to 1.8× the funded amount minus royalties paid, as seen in the KalVista-DRI Healthcare structure — was calibrated for a single M&A event. In an RMT, the question of who pays the buyout price becomes complicated.

ParentCo has divested the business. SpinCo is merging with the Buyer. If the put is exercised, does ParentCo pay from its corporate treasury (it still exists and is solvent), or does the combined SpinCo-Buyer entity pay from the newly combined balance sheet (which may be significantly more leveraged)? The answer depends on which entity is the counterparty to the royalty agreement and whether the obligation was successfully transferred to SpinCo as part of the internal separation.

Section 355(e) and Its Ripple Effects on Royalty Holders

The most important tax constraint for RMT planning is Section 355(e), enacted in 1997 specifically to prevent abuse of the Morris Trust structure. This provision imposes corporate-level tax on the spin-off distribution if, within the two years preceding or following the distribution, there is a "plan or series of related transactions" resulting in a 50% or greater change in ownership of either the distributed subsidiary or the distributing parent.

Because the parent company faces catastrophic tax consequences if the 50% test is breached, it will typically negotiate tax matters agreements with both SpinCo and the Buyer that severely restrict post-closing ownership changes. These restrictions can include lockups on share sales, limitations on secondary offerings, and prohibitions on M&A activity for 24 months post-spin. SpinCo typically agrees to indemnify the distributing parent if SpinCo takes any action that triggers taxable gain under Section 355(e).

For royalty investors, Section 355(e) creates an important secondary effect. These post-closing restrictions effectively freeze the combined entity's strategic options for two years — meaning that even if a royalty holder's change-of-control trigger fires and the holder wants to negotiate a buyout, the combined entity may be contractually prohibited from executing certain transactions during the restricted period. The two-year window can delay resolution, creating uncertainty that depresses the royalty's market value.

The IRS issued revised ruling guidance in May 2024 tightening requirements around debt exchanges in spin-off transactions and imposing new requirements on post-distribution payments between SpinCo and ParentCo. These changes affect the economics of RMTs going forward and may influence how aggressively companies use leverage as part of the separation mechanics — a factor that directly impacts the creditworthiness of the entity inheriting royalty obligations.

Drafting for the RMT Era

The proliferation of pharmaceutical RMTs demands specific contractual provisions that go beyond traditional change-of-control protections.

Explicitly enumerate divisive reorganizations. The change-of-control definition should capture spin-offs, split-offs, Reverse Morris Trust transactions, and any other corporate reorganization that results in the product or the royalty obligation being held by an entity other than the original contracting party or its direct, wholly-owned subsidiaries. The trigger should fire upon either the distribution of SpinCo shares or the subsequent merger — whichever occurs first.

Address the internal transfer. The initial step of an RMT — transferring the product and obligations from ParentCo to SpinCo — is typically permitted under affiliate transfer carve-outs. But these carve-outs should be conditioned on SpinCo remaining a wholly-owned subsidiary. If SpinCo shares are subsequently distributed or SpinCo merges with a third party, the affiliate transfer should retroactively require consent or trigger consequences.

Include credit protection mechanisms. Because the primary risk in an RMT is counterparty credit deterioration, royalty agreements should include provisions that trigger upon specified credit events: rating downgrades below investment grade, leverage ratio breaches, or net worth covenants. These triggers operate independently of corporate restructuring and capture the economic effect even if the structural mechanics evade conventional change-of-control definitions. Had royalty holders on Upjohn products negotiated an investment-grade maintenance covenant, the Viatris downgrade to BB+ would have triggered protective rights automatically.

Specify ParentCo guarantee survival. The royalty agreement can require that any internal transfer of the obligation to a subsidiary be accompanied by a guarantee from ParentCo that survives the spin-off. This ensures the royalty investor retains recourse to ParentCo's credit even after the subsidiary is distributed and merged. The practical challenge is that ParentCo will resist guarantees that persist indefinitely, so negotiation typically centres on guarantee duration (often two to five years post-spin) and conditions for release.

Require advance notice and consent. Unlike a hostile acquisition, an RMT is a planned, consensual transaction that unfolds over 12 to 18 months. The Pfizer-Mylan deal was announced in July 2019 and closed in November 2020 — a 16-month timeline. Contractual provisions requiring advance notice (90 to 180 days) and affirmative consent for any divisive reorganization give the royalty investor time to evaluate the proposed structure, negotiate protections, or exercise put options before the transaction closes.

The Valuation Impact: What Changes for Royalty Holders

The economic impact of an RMT on a pharmaceutical royalty can be decomposed into four components.

Credit risk repricing. The shift from ParentCo's investment-grade credit to SpinCo-Buyer's potentially lower-rated credit increases the discount rate applicable to future royalty cash flows. For a royalty with 10 years of remaining duration, a 200-basis-point increase in the appropriate discount rate can reduce present value by 15–20%. In the Pfizer-Viatris case, the five-notch decline from A+ to BB+ represents a far more severe repricing.

Commercial strategy risk. The new entity may pursue a different commercialization strategy — reduced promotional spend, accelerated generic entry, portfolio rationalization — that reduces expected future sales and, consequently, royalty payments. This risk is particularly acute when the RMT partner is a generics company (as with Mylan) or a private equity-backed vehicle whose return expectations are driven by cost reduction rather than revenue growth.

Secondary trading liquidity. For royalty investors who hold their positions in tradeable form (increasingly common as the royalty investment market matures), the change in counterparty can affect the liquidity and pricing of the royalty in secondary markets. A royalty backed by Pfizer trades differently from one backed by Viatris, even if the underlying product and contractual terms are identical.

Optionality compression. The put/call mechanics that protect royalty investors in conventional M&A scenarios may not activate in an RMT, eliminating the optionality premium that compensates for event risk. Even where triggers fire, the two-year Section 355(e) restriction period can delay resolution, creating uncertainty that depresses the royalty's market value.

Lessons for Market Participants

For Royalty Investors

The RMT wave demands a fundamental reassessment of how royalty investors evaluate counterparty risk. The traditional framework — assessing the probability and terms of change-of-control triggers in a standard M&A context — is necessary but insufficient. Investors must now also evaluate the probability that their counterparty will execute a divisive reorganization, and whether their contractual protections are adequate to address that scenario.

Due diligence should include a review of ParentCo's publicly stated strategic priorities (is the product in a "core" or "non-core" portfolio?), management commentary about potential separations or portfolio simplification, and analyst speculation about restructuring alternatives. If the product sits in a segment that ParentCo has signalled it might divest — as Pfizer did with its established medicines business years before the Viatris transaction — the royalty investor should ensure their agreement contains RMT-specific protections.

For Pharmaceutical Companies

Companies contemplating RMTs must diligence the royalty and licensing agreements attached to the products being transferred. Change-of-control triggers, consent requirements, and put/call options in these agreements can create significant unexpected costs that alter the transaction's economics.

In the La Jolla/Innoviva example discussed in our previous article, the potential acceleration of Healthcare Royalty Partners' $225 million cap — which exceeded the $146 million acquisition price itself — demonstrated how a single royalty agreement can constrain or even torpedo a transaction. The same risk applies, with even greater complexity, in an RMT involving dozens or hundreds of product-level agreements.

For Licensors and Universities

Academic institutions and research organizations that license intellectual property to pharmaceutical companies face a particular vulnerability. Their royalty agreements, often drafted decades ago when the licensee was a small biotech, may contain provisions entirely inadequate for the modern era of pharmaceutical restructuring.

A university that licensed a foundational patent to a biotech in 2005, which was subsequently acquired by a major pharma company in 2012, may find that its royalty agreement — now generating millions in annual income — is governed by provisions drafted for a pre-RMT world. The combination of affiliate transfer carve-outs, operation-of-law merger doctrine, and the absence of explicit RMT triggers can leave these institutions exposed to counterparty transformations they never contemplated.

Technology transfer offices should audit their existing royalty agreements for structural vulnerabilities and negotiate amendments where possible. For new agreements, the provisions outlined in the drafting section above should be considered standard.

Looking Ahead: The RMT in an Era of Permanent Restructuring

The pharmaceutical industry's restructuring cycle shows no signs of decelerating. The wave of consumer healthcare divestitures — Pfizer/Upjohn, GSK/Haleon, J&J/Kenvue, Sanofi/Opella — has largely been completed, but the next phase is already underway. Companies are increasingly evaluating separations of other non-core segments: mature vaccines, established generics portfolios, contract manufacturing operations, and even specific therapeutic areas that no longer align with corporate strategy.

Each of these separations creates the same set of risks for royalty holders. The Reverse Morris Trust will remain the preferred structure whenever the tax savings justify the complexity — and in pharmaceutical transactions involving multi-billion dollar portfolios, the tax savings almost always justify the complexity.

The royalty financing market, now exceeding $15 billion in annual transaction volume, has grown up in an environment where the typical counterparty risk was a binary question: will the product succeed, and can the company pay? The RMT adds a third dimension: will the company remain the company?

For participants across the pharmaceutical royalty ecosystem — investors, licensors, universities, and the companies themselves — the answer to that question increasingly requires not just clinical and commercial analysis, but a sophisticated understanding of corporate restructuring mechanics and the contractual architecture needed to navigate them. The dormant clauses that protect against conventional acquisitions may sleep right through an RMT, waking only when it is too late to matter.

All information in this article was accurate as of the research date and is derived from publicly available sources including company press releases, SEC filings, regulatory announcements, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice.

Member discussion