Royalties on Antibody-Drug Conjugates: The Linker-Payload Patent Problem and Who Owns the Royalty When Three Parties Each Contributed a Component

The antibody-drug conjugate has a structural feature that makes it uniquely problematic from an intellectual property standpoint: it is, by design, a composite of three distinct technologies developed by three communities of scientists who largely did not know each other. The antibody came from one tradition, the cytotoxic payload from another, and the linker chemistry that connects them from a third. When those three traditions are each owned by separate institutions, and each institution negotiates its own royalty on net sales, the commercial economics of a blockbuster ADC can become a compounding exercise in royalty subtraction.

This is not a theoretical concern. Brentuximab vedotin (Adcetris), the CD30-directed ADC now generating over $1 billion in annual sales, was built from a chimeric antibody developed at one company, an MMAE payload technology controlled by Seattle Genetics (now Pfizer), and a protease-cleavable valine-citrulline linker whose foundational IP traces to Seattle Genetics' own laboratories.

Because Seattle Genetics owned both the linker and the payload, the royalty problem was contained. Kadcyla (trastuzumab emtansine) is the more instructive cautionary tale: Genentech owns trastuzumab, ImmunoGen (now AbbVie) owns the DM1 maytansinoid payload and the SMCC linker technology, and a third-party patent holder attempted to claim rights over the HER2-targeted ADC concept itself.

The resulting IP tangle produced litigation, inter partes review petitions, and an initial royalty structure that ImmunoGen's own disclosures suggested was negotiated at a level modest enough to underreflect the drug's eventual commercial power.

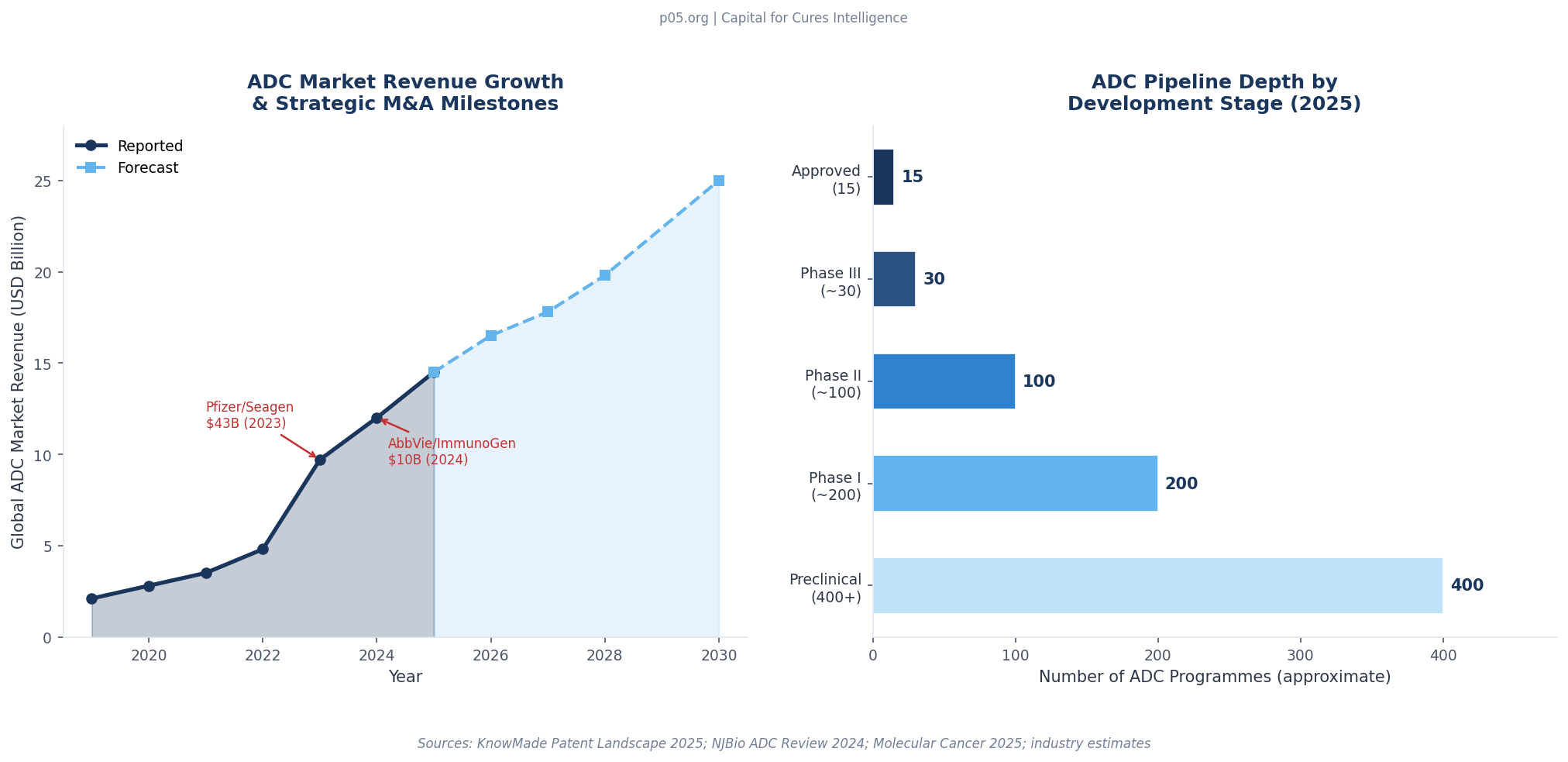

The scale of the stakes has multiplied many times since. With 15 FDA-approved ADCs, more than 200 in clinical trials, and over 400 in active development as of early 2026, and with the global ADC market having crossed $12 billion in 2024 revenues, the question of who owns which royalty on a multi-component biologic has migrated from the IP department to the front page of M&A due diligence.

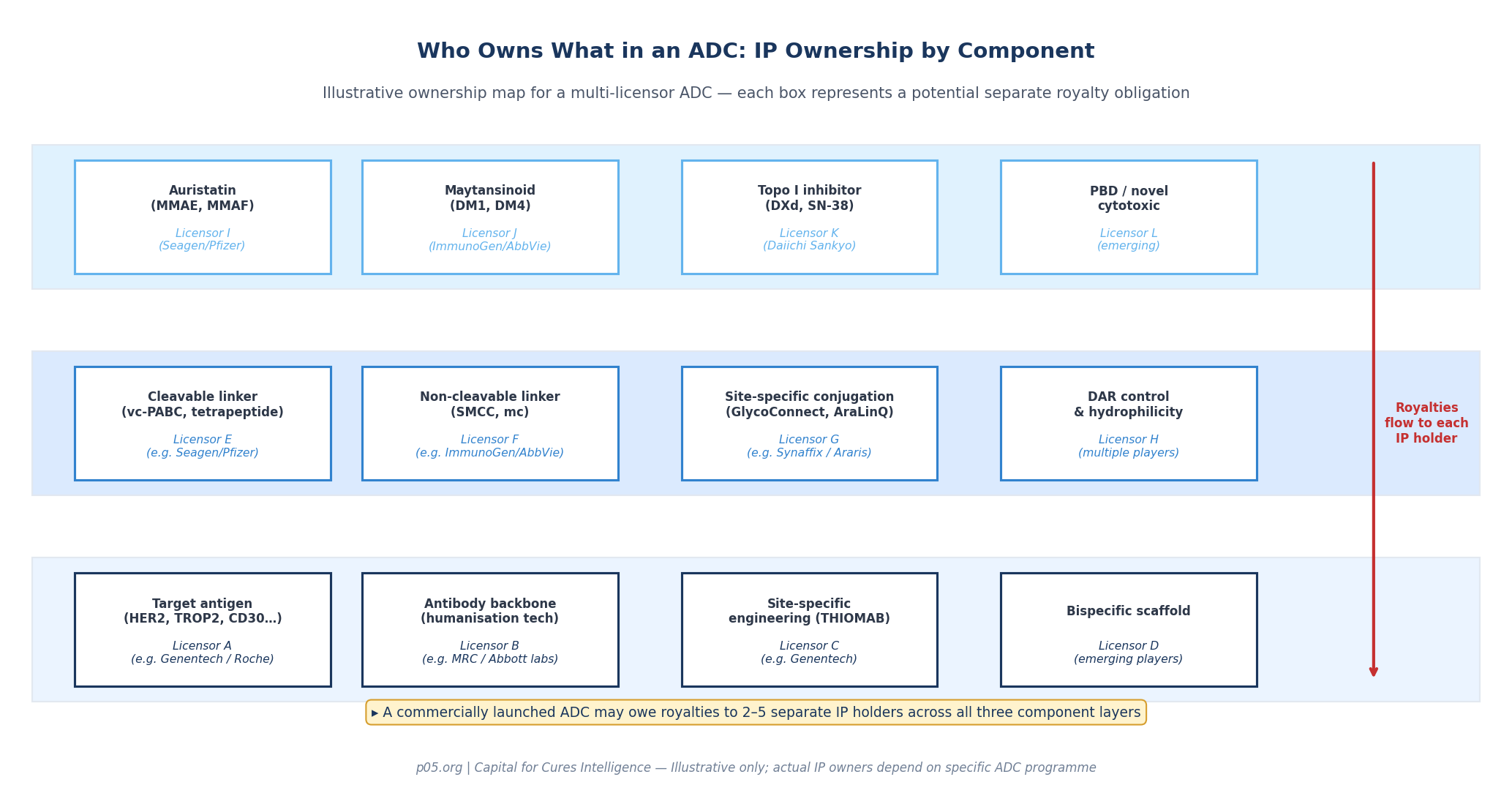

The Three-Layer Architecture and Why It Creates a Royalty Stack

An ADC is architecturally simple in concept and extraordinarily complex in execution. The three mandatory components are a monoclonal antibody, a cytotoxic payload, and a linker that connects them and governs payload release. Each component contributes a distinct function to the therapeutic index: the antibody provides tumour selectivity, the payload provides cell-killing potency, and the linker controls stability in circulation while enabling release inside the tumour cell.

The critical insight for royalty analysis is that each component is independently patentable and has, historically, been developed by independent entities with distinct licensing strategies. This creates what IP lawyers call a "royalty stack": the obligation by a single commercial product to pay royalties to multiple patent holders, each holding rights to a different functional element of the same drug.

The royalty stacking problem in ADCs operates across at least three distinct layers, each with its own internal complexity.

The antibody layer carries the highest variable cost but is also the most frequently internalised by developers. An antibody patent typically covers the complementarity-determining regions (CDRs), the target antigen binding domain, and sometimes the humanisation technology used to reduce immunogenicity. Where the antibody was developed in-house, no third-party royalty is owed.

But where a developer has licensed a target-validated antibody, or where foundational humanisation patents (many traceable to MRC Technology's original CDR-grafting patents) apply, a royalty obligation attaches to the antibody itself. AbbVie's acquisition of ImmunoGen for $10.1 billion in 2024 and Pfizer's $43 billion acquisition of Seagen in 2023 were both, in part, acquisitions of the right to eliminate downstream royalty obligations on commercially successful ADC franchises.

The payload layer has historically been dominated by two companies, each controlling a foundational class of cytotoxic agent. ImmunoGen pioneered the maytansinoid class — derivatives of the natural product maytansine, of which DM1 and DM4 are the most clinically developed — and built an outright technology licensing business around them. Seattle Genetics (Seagen/Pfizer) controls the auristatin class, particularly monomethyl auristatin E (MMAE) and monomethyl auristatin F (MMAF), synthetic analogues of the marine natural product dolostatin 10.

These two payload families accounted for the overwhelming majority of early clinical ADC programmes. A developer wishing to use either MMAE or DM1 as a payload had no practical alternative: it had to license from the IP holder, paying royalties on net sales that, depending on the vintage of the deal, ranged from the low single digits to the mid-single digits as a percentage of product revenue.

The linker layer is where the most dynamic and commercially contested patent activity is currently occurring. Linker chemistry is the component that, more than any other, determines the ADC's therapeutic window. A linker that releases payload too early causes systemic toxicity. A linker that is too stable fails to release payload inside the tumour. The valine-citrulline protease-cleavable linker used in Adcetris represented a genuine breakthrough in stability; Seagen's protease-cleavable linker patents became among the most contested in the field.

The SMCC (succinimidyl-4-(N-maleimidomethyl)cyclohexane-1-carboxylate) non-cleavable linker used in Kadcyla is an ImmunoGen proprietary technology. New generations of site-specific conjugation platforms — including Synaffix's GlycoConnect and HydraSpace technologies (now part of Lonza following acquisition) and Araris Biotech's AraLinQ peptide linker (acquired by Taiho Pharmaceutical) — have added another layer of claimants to royalty entitlements.

The table below maps the approved ADC field against these three layers, showing how the royalty stack complexity varies considerably by programme architecture.

| Approved ADC | Antibody | Linker | Payload | Primary IP Holder(s) | Royalty Stack Complexity |

|---|---|---|---|---|---|

| Adcetris (brentuximab vedotin) | cAC10 (anti-CD30) | vc-PABC cleavable | MMAE | Seagen/Pfizer (linker + payload) | Low — one primary licensor |

| Kadcyla (trastuzumab emtansine) | Trastuzumab (Genentech) | SMCC non-cleavable | DM1 | Genentech (Ab) + ImmunoGen/AbbVie (linker+payload) | Moderate — two primary licensors |

| Enhertu (trastuzumab deruxtecan) | Trastuzumab | Tetrapeptide cleavable | DXd (exatecan) | Daiichi Sankyo (all components) | Low — fully integrated |

| Trodelvy (sacituzumab govitecan) | Anti-TROP2 | CL2A cleavable | SN-38 | Immunomedics/Gilead (all) | Low — post-acquisition integrated |

| Elahere (mirvetuximab soravtansine) | Anti-FRα | Sulfo-SPDB | DM4 | ImmunoGen/AbbVie (all) | Low — post-acquisition integrated |

| Padcev (enfortumab vedotin) | Anti-Nectin-4 | vc-PABC | MMAE | Astellas (Ab) + Seagen/Pfizer (linker+payload) | Moderate — two licensor relationships |

| Tivdak (tisotumab vedotin) | Anti-TF | vc-PABC | MMAE | Genmab (Ab) + Seagen/Pfizer (linker+payload) | Moderate — two licensor relationships |

| Platform-licensed ADC (illustrative) | Licensed HER3 Ab | GlycoConnect platform | toxSYN payload | 3 separate IP holders | High — full royalty stack |

Two patterns stand out. First, many of the commercially successful ADCs that appear "low complexity" today achieved that status through post-approval M&A — Gilead's acquisition of Immunomedics, AbbVie's acquisition of ImmunoGen — not through clean IP architecture at inception. Second, the programmes with persistent moderate complexity (Padcev, Tivdak) are precisely those where the antibody originator and the linker-payload technology owner remain institutionally separate. Those are the royalty stacking cases that merit the most careful analysis.

The Enhertu Litigation: A Case Study in Overlapping Claims

No recent case better illustrates the royalty stacking problem than the patent dispute between Seagen and Daiichi Sankyo over Enhertu (trastuzumab deruxtecan), the HER2-directed ADC that has become one of the most consequential cancer medicines in a generation.

Enhertu's architecture is entirely Daiichi Sankyo's own: the DXd ADC platform uses a proprietary topoisomerase I inhibitor payload (an exatecan derivative) attached to a HER2-directed antibody via a tetrapeptide-based cleavable linker. Daiichi and AstraZeneca entered their collaboration to jointly develop and commercialise Enhertu in March 2019, with AstraZeneca paying $1.35 billion upfront — at the time one of the largest upfront payments in oncology licensing history.

Then Seagen filed a patent infringement suit. Seagen's US Patent 10,808,039 covers auristatin compounds coupled to an antibody via a linker. Seagen's theory was that Enhertu's DXd payload, though not itself an auristatin, fell within the broader claim scope of the '039 patent because of structural similarities in the linker-payload conjugation approach. A Texas district court initially agreed, awarding Seagen nearly $42 million in damages based on past royalties and imposing an ongoing 8% royalty on Enhertu sales.

The significance of that 8% number is difficult to overstate. Enhertu generated $3.58 billion in sales in the first nine months of 2024 alone. Analysts projected peak annual revenue potentially exceeding $5 billion. An 8% royalty on those figures would represent hundreds of millions of dollars flowing to Seagen/Pfizer for a drug that Daiichi Sankyo's scientists developed entirely using their own proprietary technology — if the patent had survived.

It did not. The US Patent and Trademark Office delivered a final decision invalidating the '039 patent, and the federal appeals court subsequently reversed the 2022 infringement verdict and vacated the damages award. The episode ended with Daiichi Sankyo vindicated — but it came within a judicial decision of one of the most consequential royalty obligations in ADC history.

The Enhertu case illustrates a structural vulnerability of the ADC patent system: because linker-payload chemistry involves conjugation approaches with shared conceptual origins (nucleophilic residues on antibodies, cleavable bonds, potent cytotoxics), patent claims can read across nominally different technologies in ways that are not immediately obvious at the time a programme is designed.

The Platform Licensing Model and Layered Royalty Obligations

The emergence of dedicated ADC platform companies has created a new category of royalty claimant: the platform licensor. Unlike ImmunoGen or Seagen, which developed specific payload-linker combinations and licensed them for use in partner-selected programmes, platform companies like Synaffix and LigaChem Biosciences license the entire conjugation infrastructure — antibody modification technology, linker, and in some cases a payload library — as a bundled package.

The platform model solves the royalty stacking problem for the developer in one dimension (a single licensing relationship rather than three) while potentially concentrating more royalty value in fewer hands. Synaffix's January 2023 licensing deal with Amgen covers access to GlycoConnect site-specific conjugation, HydraSpace hydrophilicity modification, and selected toxSYN linker-payloads for up to five programmes, with Synaffix eligible for up to $2 billion in milestone payments plus tiered royalties on commercial sales.

The tiered royalty rate was described as consistent with Synaffix's other recently signed licences — a reference point that reflects a normalised market for platform technology royalties in the low-to-mid single digit range per programme.

But the platform model does not eliminate the stacking risk. A developer licensing Synaffix's platform for the linker-payload still owes separate royalties if the antibody was itself in-licensed. A developer using Daiichi Sankyo's DXd platform through a collaboration agreement — as AstraZeneca and Merck have done — does not face a linker-payload royalty stack on DXd programmes because Daiichi Sankyo controls all three components.

But a mid-size developer assembling an ADC from third-party components faces a fundamentally different royalty arithmetic.

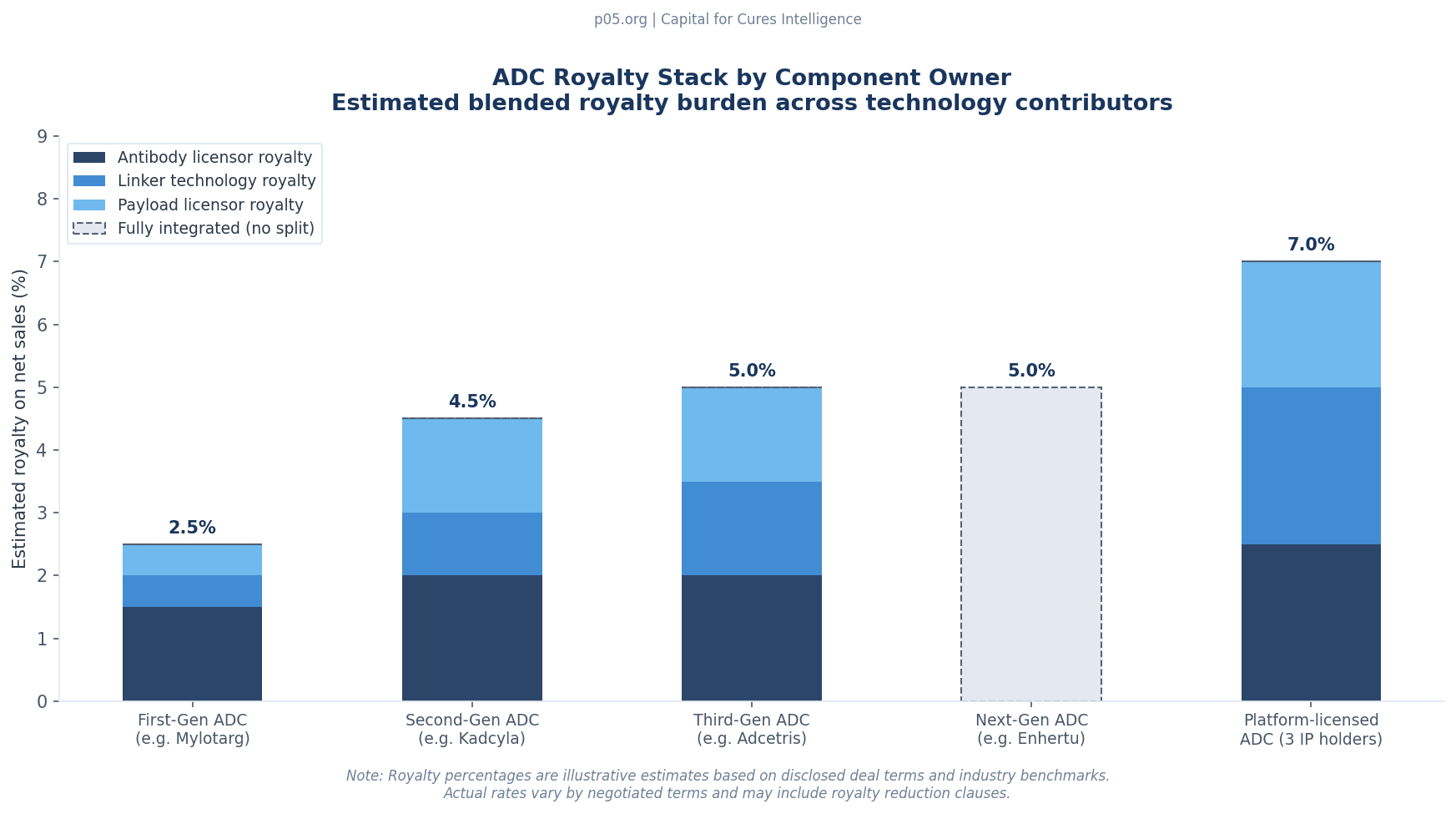

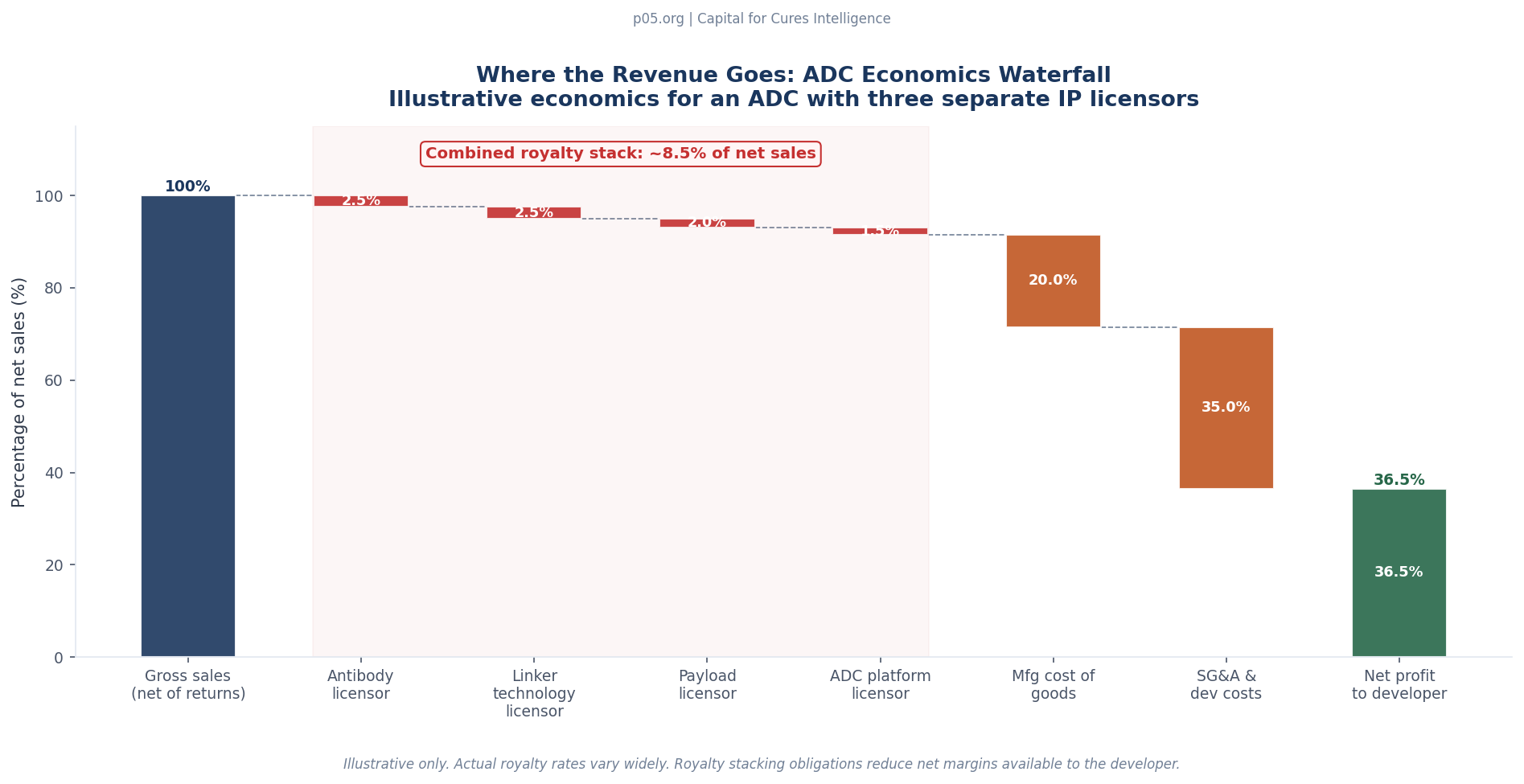

The Royalty Stack in Quantitative Terms

Consider a hypothetical ADC with $500 million in annual net sales, assembled from licensed components: a humanised antibody from a third-party licensor, an MMAE payload from Seagen/Pfizer, and a valine-citrulline linker from a specialist conjugation company. The layered royalty obligations might look like this:

| Component | IP Holder | Royalty on Net Sales (est.) | Annual obligation ($M) |

|---|---|---|---|

| Antibody (humanisation + CDRs) | Third-party licensor | 2.0–2.5% | $10–12.5M |

| MMAE payload | Seagen/Pfizer | 1.5–2.5% | $7.5–12.5M |

| Linker technology | Specialist licensor | 1.5–2.0% | $7.5–10M |

| Site-specific conjugation platform | Platform licensor | 1.0–1.5% | $5–7.5M |

| Total royalty stack | 6.0–8.5% | $30–42.5M |

That aggregate royalty of $30–42.5 million per year on a $500 million product is before manufacturing costs, sales and marketing expenses, and clinical development costs for label expansion. For comparison, the blended EBITDA margin for a commercially launched pharmaceutical is typically in the 30–40% range before royalties. A royalty stack of 6–8.5% compresses the effective margin meaningfully, particularly when combined with the cost structure of an ADC, which requires highly specialised manufacturing for both the biological antibody component and the highly potent active pharmaceutical ingredient (HPAPI) payload.

The Three-Party Attribution Problem

The deepest challenge for royalty investors is not the total magnitude of the royalty stack but the attribution question: when three parties each contributed a component, and the resulting combination produced unexpectedly superior clinical results, who owns the value creation?

The legal framework provides a starting point: each licensor owns what it licensed. A maytansinoid payload licensor owns royalties on the use of that payload. An antibody licensor owns royalties on the use of that antibody. They are independent contractual relationships that run in parallel to the same commercial outcome. The commercial success of the ADC as a whole does not change the legal entitlements of any individual licensor, except to the extent that tiered royalty provisions create rate escalation at higher sales thresholds.

But the economic reality is more nuanced. The DXd conjugation chemistry explains the multi-billion-dollar performance gap between Enhertu and Kadcyla, both of which use the same HER2-targeting trastuzumab antibody but different linkers and payloads. Kadcyla uses ImmunoGen's DM1 maytansinoid via a non-cleavable SMCC linker and achieved $2.192 billion in sales in 2024. Enhertu uses Daiichi Sankyo's DXd exatecan derivative via a tetrapeptide cleavable linker and achieved $3.754 billion in sales in 2024. Both drugs target HER2; the antibody is the same.

The linker-payload combination accounts for essentially the entire performance differential.

This creates a royalty valuation asymmetry. Genentech/Roche, as the licensor of trastuzumab, holds royalty rights in both Kadcyla and (via Daiichi Sankyo's development agreement) Enhertu.

The value of that antibody royalty has compounded dramatically as Enhertu's clinical superiority has expanded its label and addressable market. The royalty investor who financed Genentech's trastuzumab programme decades ago could not have anticipated that the relevant risk-adjusted value would sit not in the antibody itself but in the linker chemistry that would be attached to it twenty years later.

Implications for Royalty Financing Transactions

For royalty investors evaluating ADC-based royalty opportunities, the multi-party IP architecture creates specific due diligence requirements that differ materially from royalty transactions on conventional small molecules or naked antibodies.

Freedom-to-operate coverage: A royalty investment in an ADC product is indirectly exposed to all third-party IP claims against that product. If a platform licensor's patent is invalidated, the developer no longer owes a royalty to that licensor — which improves the product's economics — but the developer also loses the certainty that the FTO is clean. If a previously unidentified patent surfaces and is found to read on the ADC's linker chemistry, the developer faces new royalty obligations that reduce the cash flows available to the royalty investor. FTO analysis for ADCs must encompass all three components: antibody, payload, and linker.

Royalty reduction clauses: Many ADC licensing agreements contain provisions allowing the developer to reduce the royalty rate payable to one licensor if the developer is required to obtain additional licences from third parties to commercialise the product. These royalty stacking offset provisions — sometimes called "royalty reduction" or "third-party IP credit" clauses — are designed to prevent the aggregate royalty burden from becoming economically prohibitive.

From the royalty investor's perspective, these clauses represent a contingent dilution risk: if a new IP claim materialises post-approval, the royalties flowing to the investor may be reduced by the cost of acquiring the new licence.

Change-of-control dynamics: The M&A consolidation in the ADC sector has fundamentally restructured the IP ownership landscape. Pfizer's $43 billion acquisition of Seagen in 2023 brought the MMAE payload and the vc-PABC linker under the same ownership as several commercial ADC products that had previously been licensees. Post-acquisition, Pfizer effectively royalty-freed its own products while maintaining royalty claims against third-party licensees. AbbVie's $10.1 billion acquisition of ImmunoGen in 2024 had the same structural effect for the DM1/DM4 maytansinoid family and Elahere.

Any royalty investor holding interests in these platforms must analyse how the acquiring entity's own ADC pipeline interacts with the licensing economics they inherited.

The Daiichi Sankyo model as a benchmark: The vertically integrated model pioneered by Daiichi Sankyo — where the same organisation owns the DXd payload, the tetrapeptide linker, and the manufacturing infrastructure — eliminates the inter-company royalty stack entirely. The DXd platform now underlies at least six clinical-stage ADCs across collaborations with AstraZeneca (Enhertu, Datroway) and Merck ($22 billion deal for three additional DXd ADCs).

The royalty obligations in those collaboration agreements run to Daiichi Sankyo as a unified platform owner, not to three separate IP holders. From a royalty investor's perspective, this makes DXd-based ADCs structurally cleaner but also concentrates IP risk: if Daiichi Sankyo's core DXd patents were successfully challenged, the impact would cascade across an entire drug family.

The Emerging Royalty-Investor-Relevant Questions

Who captures value when a linker makes a payload work better?

The historical royalty structures for maytansinoids and auristatins were negotiated when those payloads were the primary source of ADC differentiation. The linker was, in first-generation ADCs, largely a passive connector. That assumption is now obsolete. The linker controls the drug-antibody ratio (DAR), the bystander killing effect, the systemic toxicity profile, and the pharmacokinetics of the entire construct. A superior linker can make a mediocre payload clinically viable; an inferior linker can render even a potent payload therapeutically useless.

Yet most legacy royalty structures continue to value the payload as the primary contributing technology, with the linker attracting a smaller royalty rate on the assumption that it is enabling but not definitive.

The DXd precedent — where the linker-payload combination is responsible for dramatically superior clinical outcomes relative to competing products using the same antibody — suggests that this value attribution is increasingly incorrect. Future licensing negotiations will need to grapple with how to allocate royalty entitlements when the linker is itself the primary source of differentiation.

How do next-generation conjugation platforms change the stack?

The emergence of site-specific conjugation technologies — which attach payloads to defined positions on the antibody rather than using the heterogeneous cysteine-reduction or lysine-conjugation approaches of earlier generations — adds a new layer of patentable innovation to the ADC architecture.

Araris Biotech's AraLinQ platform, which attaches payloads via a peptide bond to a privileged Q295 site in the IgG-Fc framework, produces highly homogeneous ADCs with improved stability and therapeutic index. Taiho Pharmaceutical's acquisition of Araris for $400 million upfront — plus additional milestones bringing potential total value to $1.14 billion — reflects the market's recognition that site-specific conjugation is itself a billion-dollar technology.

For royalty investors, the implication is that the conjugation chemistry layer is now economically material alongside the payload layer. An ADC programme that uses GlycoConnect conjugation, a vc-PABC linker, and MMAE payload may carry three separate royalty obligations for what is conceptually a single linker-payload function. The royalty stacking risk compounds as the technology stack grows more sophisticated.

What happens when the antibody becomes cheap?

A structural shift is occurring in the antibody component of the royalty stack. The foundational humanisation patents — the MRC Technology CDR-grafting patents and the Queen et al. humanised antibody patents — have substantially expired or are approaching expiration.

The cost and IP complexity of generating a high-quality humanised monoclonal antibody has decreased dramatically with advances in transgenic mouse platforms (Regeneron's VelocImmune, Humanigen's HuMab) and computational antibody design. This means the antibody layer of the royalty stack is gradually becoming less contested, while the linker-payload layer is becoming more so.

For royalty investors evaluating ADC royalties from the perspective of long-term cash flow durability, the expiration of antibody-layer royalties is a natural tailwind, but it should be modelled against the increasing risk of new royalty obligations being asserted against the linker and conjugation layers as those patents age into their commercial peak.

The M&A Lens: Why These Questions Matter for Deal Valuation

The pharmaceutical M&A wave that has swept through ADC assets since 2021 — Gilead's $21 billion acquisition of Immunomedics in 2020, Pfizer's $43 billion Seagen acquisition in 2023, AbbVie's $10.1 billion ImmunoGen acquisition in 2024, and Johnson & Johnson's $2 billion Ambrx acquisition in 2024 — reflects in part a strategic desire to consolidate the IP stack and eliminate downstream royalty obligations. When a single company owns the antibody, the linker, and the payload, the royalty stacking problem disappears: the company pays royalties to itself.

This consolidation dynamic has a direct implication for royalty financing. Where a royalty investor holds a product royalty on an ADC with fragmented IP — particularly where the royalty was acquired from an entity that does not control all three components — the investor's cash flows are exposed to the risk that an acquirer will restructure the IP relationships post-transaction to reduce or eliminate the royalty obligation.

The structuring of royalty agreements to include change-of-control protections, buyout provisions, and anti-assignment covenants becomes critical in an environment where the acquirer may have independent economic incentives to unwinding the original royalty relationship.

The obverse situation is equally significant. A royalty investor holding rights over a linker technology licensor — for example, a royalty interest in the cash flows generated by Synaffix's portfolio of licensing agreements — benefits from M&A activity in the ADC sector because each new programme signed under the Synaffix platform creates an additional royalty stream. But the investor must also model the risk that a major acquirer, having licensed the technology, will choose to acquire the licensor outright rather than continue paying royalties — which is precisely what the Taiho/Araris transaction represents.

What This Means for the Next Wave of ADC Royalty Deals

The ADC royalty market is at an early but rapidly maturing stage. Of the approximately 400 ADC programmes in development as of early 2026, the vast majority will never reach commercial approval. But the attrition pattern in ADC development is meaningfully different from other oncology modalities: ADCs fail more often at the development stage (linker instability, off-target toxicity, manufacturing challenges) than at the Phase III efficacy stage, meaning the clinical signal for an ADC that reaches Phase II is relatively strong.

This creates a specific opportunity for royalty investors who can accurately assess the IP ownership of a programme's component technologies and model the royalty obligations that will apply at commercialisation. The questions they need to answer are now substantially different from those required for a conventional royalty transaction:

Who owns the linker IP, and is it the same entity as the payload IP owner? If not, are there royalty reduction provisions in the payload licence if a separate linker royalty is owed?

Has a freedom-to-operate analysis been conducted across all three component layers, and what is the residual patent risk in each layer over the projected commercial horizon?

Does the developer own the conjugation method, or does site-specific conjugation involve a third-party platform licence with independent royalty obligations?

What is the vintage of the payload licence, and do the royalty rates reflect the value of older negotiated terms or current market benchmarks?

Are there royalty reduction provisions triggered by the developer's obligation to license third-party IP? If so, what is the developer's obligation to disclose new IP claims to the royalty investor, and what is the investor's recourse if such claims reduce the royalty base?

These questions are answerable but require a degree of IP-layer analysis that many royalty investors have not historically needed to perform on pharmaceutical royalty assets. The growth of the ADC sector makes this analysis a core competency rather than a specialist edge case.

Conclusion

The antibody-drug conjugate is a genuinely revolutionary therapeutic modality that has improved survival outcomes for patients with cancers that were previously untreatable. It is also, from an intellectual property standpoint, a multi-body problem: a commercial product composed of independently patentable components, each potentially owned by a different institution, each potentially asserting independent royalty rights against the same revenue stream.

The resolution of this problem varies by programme architecture. Vertically integrated platforms like Daiichi Sankyo's DXd system have essentially solved it by bringing all three components under unified ownership. Legacy programmes like Kadcyla navigated it through early bilateral licensing. Mid-tier developers assembling ADCs from third-party components face a layered royalty stack that can reduce net margins by six to nine percentage points before manufacturing costs are counted.

For royalty investors, the analytical implication is clear. Valuing an ADC royalty requires not just a clinical and commercial model, but a component-by-component IP ownership analysis that maps every royalty obligation in the technology stack and assesses the durability and defensibility of each claim. The developer who successfully commercialises a blockbuster ADC will have navigated this minefield. The royalty investor whose cash flows sit downstream of that navigation cannot assume the minefield has been cleared — only that it has been crossed.

The next time a term sheet for an ADC royalty crosses a deal desk, the first question should not be about peak sales projections. It should be: who owns the linker?

All information in this article was accurate as of March 2026 and is derived from publicly available sources including company press releases, SEC filings, patent databases, peer-reviewed literature, and publicly disclosed licensing terms. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. I am not a lawyer or financial adviser. Nothing in this article should be construed as advice to make any investment or legal decision.

Member discussion