Royalty Assignment vs. Novation: Legal Distinctions That Matter at Exit

When a pharmaceutical royalty deal ends up in the middle of a merger, an asset sale, or a portfolio restructuring, one question surfaces faster than almost any other: can this agreement be transferred, and if so, how? The answer turns on a distinction that is elementary in contract law but routinely underestimated in deal rooms — the difference between an assignment and a novation.

These are not interchangeable terms. They describe fundamentally different legal operations, carry different consent requirements, produce different liability outcomes, and interact with deal structure in ways that can determine whether a transaction closes cleanly or stalls at the counterparty consent stage.

In the pharmaceutical royalty context specifically, the choice between assignment and novation — or the failure to make that choice deliberately — can affect everything from acquirer due diligence to the tax treatment of the transferred interest.

This article examines the legal mechanics of each, traces how they appear in royalty purchase agreements and SEC filings, and explains why the distinction matters most precisely when it is hardest to revisit: at exit.

The Foundational Distinction

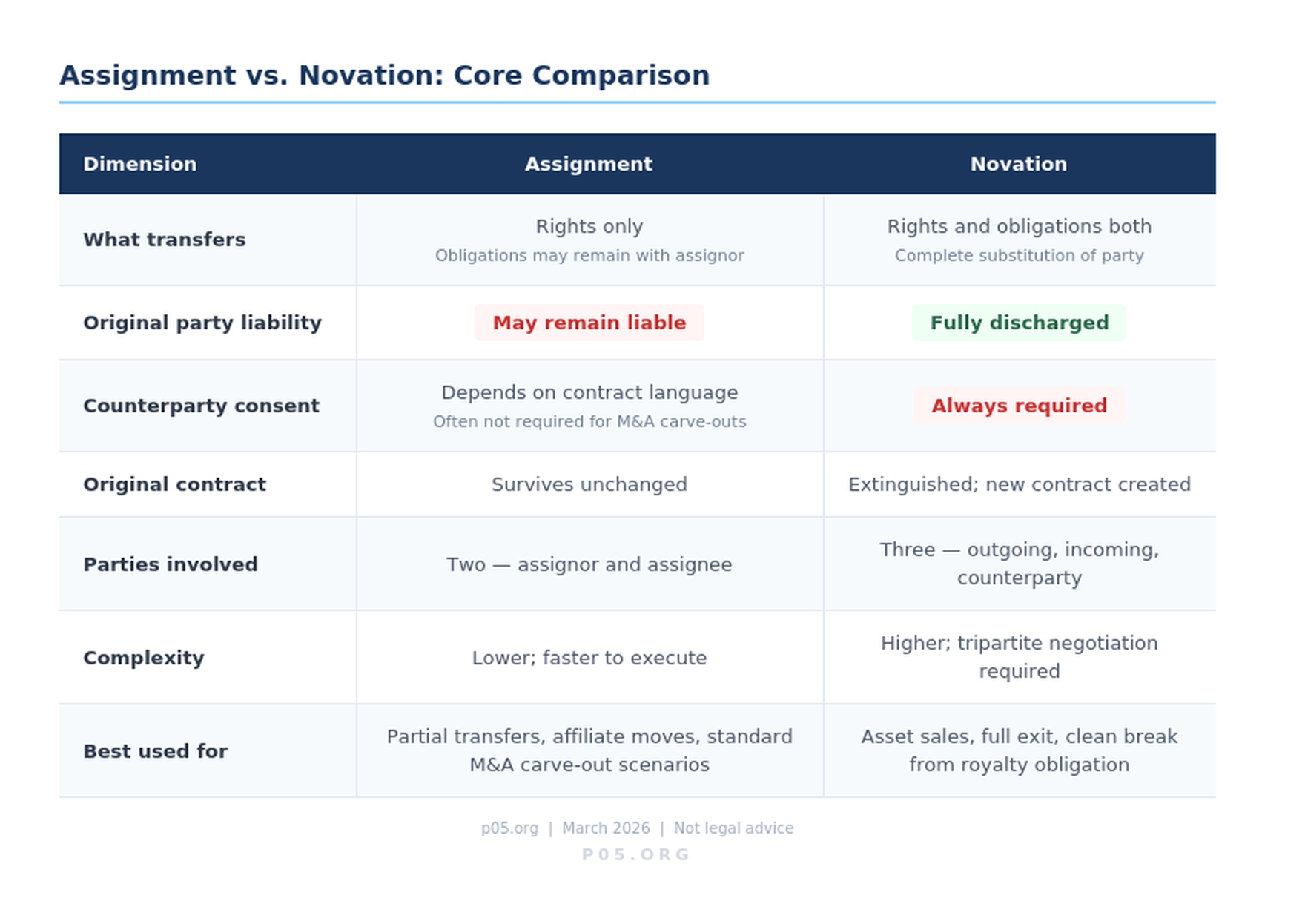

At its core, the difference is about what moves and who remains responsible.

An assignment transfers the rights under a contract from one party (the assignor) to another (the assignee). The original contract remains intact. Crucially, unless the non-assigning counterparty has expressly released the assignor from its obligations, the assignor typically remains on the hook for performance.

In a royalty context, a biotech that assigns its royalty payment obligations to a successor entity may discover, in litigation, that it retains contingent liability if the successor defaults.

A novation goes further. It extinguishes the original contract entirely and replaces it with a new agreement involving a new party. The departing party is fully released. All three parties — the outgoing party, the incoming party, and the counterparty — must consent. This tripartite consent requirement is what makes novation more procedurally demanding but legally cleaner: once executed, the original party has no residual exposure.

The table below captures the operational differences:

| Dimension | Assignment | Novation |

|---|---|---|

| What transfers | Rights (and sometimes obligations) | Rights and obligations both |

| Original party liability | May remain contingently liable | Fully discharged |

| Counterparty consent required | Depends on contract language | Always required |

| Original contract | Survives | Extinguished; replaced by new agreement |

| New contract created | No | Yes |

| Complexity | Lower | Higher |

| Primary use case | Transferring benefits; partial transfers | Clean exits; full substitution of party |

How Royalty Purchase Agreements Typically Handle Transfer

Pharmaceutical royalty purchase agreements — whether structured as synthetic royalties, royalty monetisations, or royalty-backed loans — almost universally contain assignment clauses that differ meaningfully from standard commercial contracts.

Because the royalty investor's return depends entirely on product-specific cash flows, and because the biotech's identity, regulatory relationships, and commercial infrastructure are integral to generating those flows, counterparties negotiate transfer restrictions carefully.

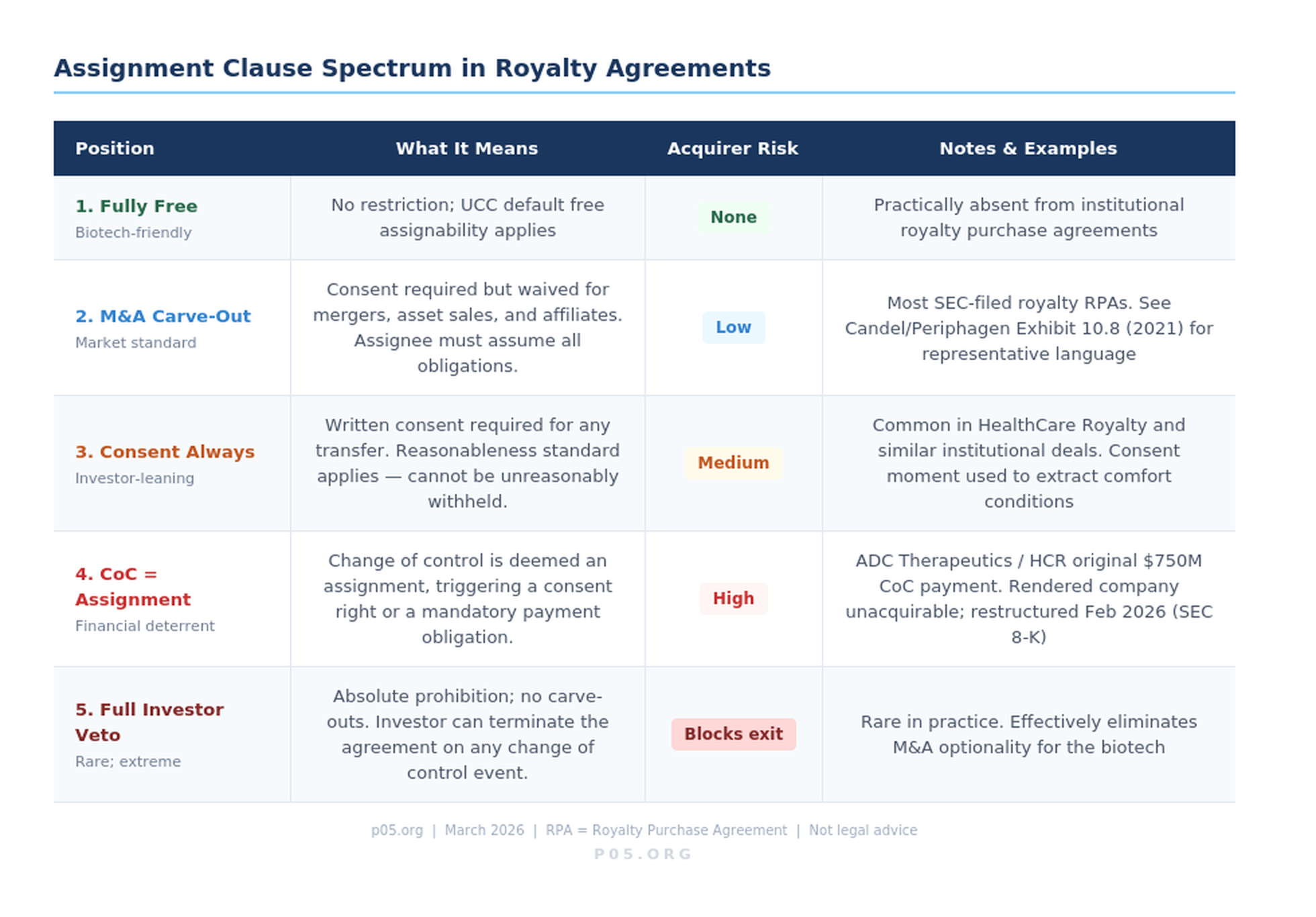

The standard construction in SEC-filed royalty agreements takes one of three forms.

Consent-required assignments. The most common formulation prohibits either party from assigning rights or obligations without the prior written consent of the other, which consent shall not be unreasonably withheld, conditioned, or delayed. The reasonableness qualifier matters: it prevents the counterparty from using consent as leverage to renegotiate economic terms, while preserving its right to object to a transfer that materially changes the counterparty's risk profile.

In practice, royalty investors who oppose a proposed acquirer — perhaps because the acquirer's commercial track record in the relevant therapeutic area is weak — will test whether their objection clears the "unreasonably withheld" threshold.

M&A carve-outs. Most agreements include an express carve-out permitting assignment without consent in connection with a merger, consolidation, or the sale of all or substantially all of the assignor's assets, provided that the assignee assumes all obligations.

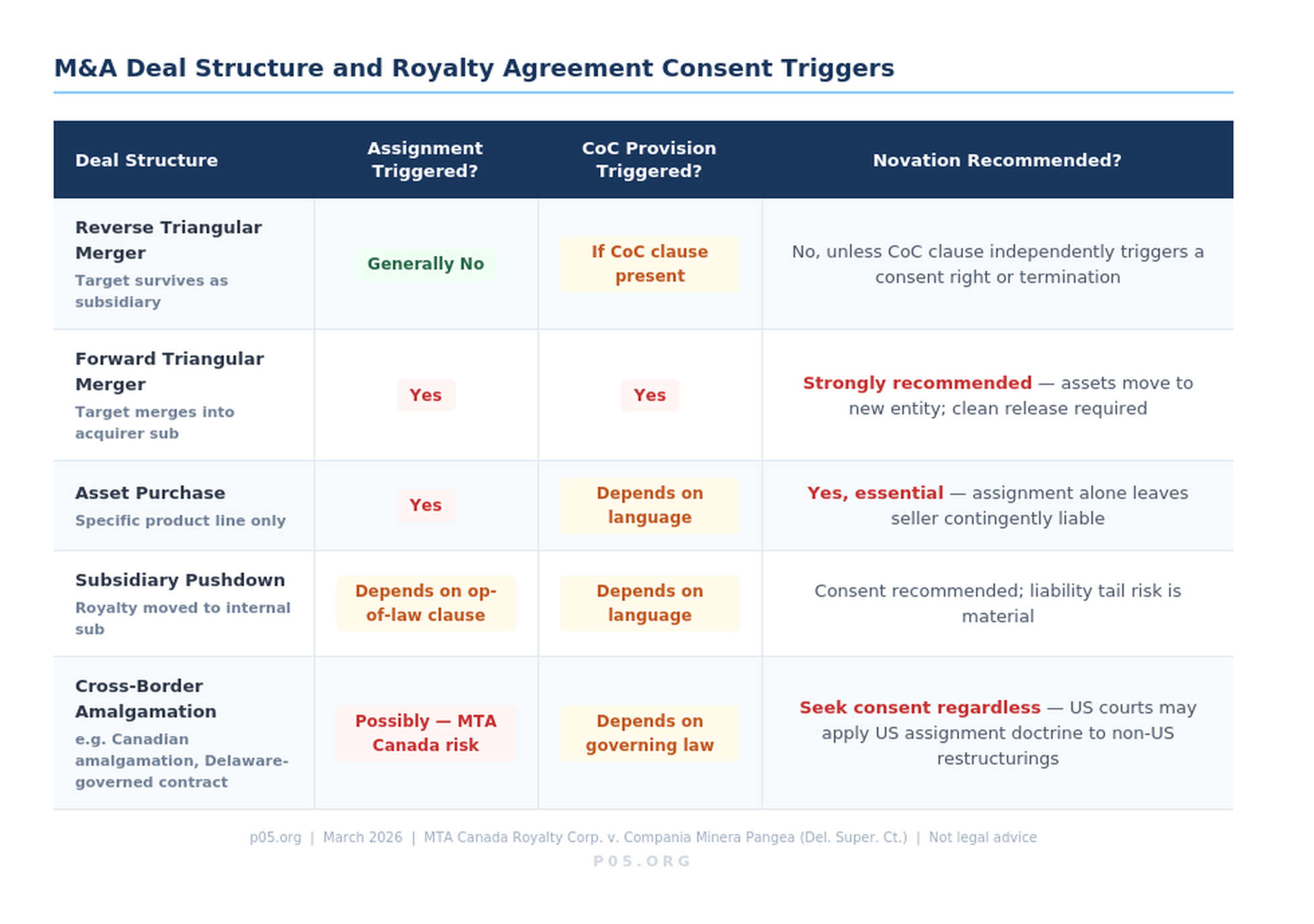

This carve-out is significant: it means a reverse triangular merger — the most common M&A structure — will generally not require the royalty investor's consent to transfer the royalty-burdened assets to the acquirer. The royalty obligation follows the assets automatically. What it does not mean is that the acquirer's post-closing capital structure choices — such as pushing the royalty obligation down to a subsidiary — can be made without a fresh consent analysis.

Change-of-control triggers. A subset of royalty agreements treat a change of control as a deemed assignment, triggering consent requirements even in equity transactions where no formal assignment occurs. ADC Therapeutics' royalty purchase agreement with HealthCare Royalty, disclosed in an 8-K filed with the SEC on February 23, 2026, is an example of a change-of-control provision so stringent — a $750 million payment obligation — that it rendered the company practically unacquirable until it was restructured.

The amended agreement reduced that trigger to $150–$200 million in exchange for warrants, but the original construction illustrates what happens when change-of-control consent mechanics are drafted as financial deterrents rather than counterparty-protection mechanisms.

The full spectrum of assignment clause construction — from freely assignable to absolute investor veto — is illustrated below.

The Assignment by Operation of Law Problem

Equity transactions create a specific doctrinal hazard that practitioners frequently underestimate: assignment by operation of law.

In a standard forward merger or asset purchase, the contract is formally assigned from the seller to the buyer. Anti-assignment clauses are triggered, consent is required, and the process is visible. In a reverse triangular merger — where an acquisition subsidiary merges into the target, leaving the target as the surviving entity — no formal assignment occurs. The contracts remain with the target company, which is now a subsidiary of the acquirer. Under general common law, this does not constitute an assignment.

The complication arises where royalty agreements contain language prohibiting not just direct assignment but assignment "by operation of law." Courts in Delaware have interpreted certain cross-border restructurings — including Canadian amalgamations — as assignments by operation of law, even where the contracting parties and their lawyers believed no assignment had occurred.

The MTA Canada Royalty Corp. decision held that a British Columbia amalgamation, governed by a contract subject to Delaware law, constituted an assignment by operation of law. The result: the anti-assignment provision was triggered without consent, potentially voiding the contract.

For pharmaceutical royalty agreements with multi-jurisdictional parties — which describes the overwhelming majority of the market, given the prevalence of Swiss, Irish, and Cayman structures for both biotechs and royalty funds — this is not a hypothetical risk.

Any restructuring that involves an amalgamation, statutory merger under non-US law, or cross-border entity conversion needs a careful analysis of whether the royalty agreement's anti-assignment language captures the transaction structure, regardless of whether the parties intended an assignment.

When Novation Is Required

Novation is not always available and is not always preferable. But in certain royalty exit scenarios, it is the only mechanism that achieves a clean legal result.

The clearest case is an asset sale. When a biotech sells the royalty-generating product line — the approved drug, its associated intellectual property, the marketing authorisation — to a third party as part of a standalone asset transaction, the royalty purchase agreement does not automatically follow the assets unless it is expressly assigned. And even if assigned, the original biotech may remain contingently liable to the royalty investor under the original agreement.

A novation novates the royalty agreement entirely: the original biotech is released, the acquirer of the product line steps in as the new obligor, and the royalty investor — who must consent — has presumably conducted diligence on the new counterparty before agreeing.

From the royalty investor's perspective, the consent right in novation is substantive, not procedural. The investor is being asked to accept a new obligor in place of the original. If the new party has weaker commercial capabilities, a different capital structure, or operates in a different regulatory environment, the royalty's risk profile changes materially.

Royalty investors will condition novation consent on representations about the acquirer's financial condition, its assumption of all downstream commercialisation obligations, and in some cases its posting of credit support. SEC filings for novation of royalty agreements typically attach the full novation agreement as an exhibit to the Form 8-K, making the consent terms publicly visible.

The less obvious novation case arises in portfolio restructurings within royalty fund families. When a royalty fund vehicle transfers a royalty interest from one fund to an affiliated entity — for example, from a legacy fund nearing end-of-life to a new fund with longer duration — the formal mechanism is often novation rather than assignment, because the royalty agreement's anti-assignment clause applies to both parties.

The original biotech counterparty must consent to the substitution of the new fund entity. In practice, biotech companies with ongoing relationships with royalty funds consent routinely, but the consent requirement creates a negotiating moment: biotechs have sometimes used novation consent as leverage to seek minor commercial concessions, such as modifications to payment timing or reporting obligations.

Deal Structure and Consent Triggers: A Practical Map

The interaction between assignment restrictions, change-of-control provisions, and M&A deal structures creates a matrix of consent obligations that acquirers must map before signing.

The practical implication for acquirers: royalty purchase agreements must be identified and analysed during diligence, not as an afterthought. Unlike standard commercial contracts where anti-assignment consent can sometimes be waived at closing, royalty investors are institutional parties with legal counsel, economic stakes often exceeding $100 million, and no particular incentive to cooperate under time pressure.

Consent timing — particularly in competitive auction processes — becomes a negotiating variable in its own right.

As the OlenderFeldman analysis of anti-assignment clauses notes, counterparties to consent-required assignments may leverage the consent moment as an opportunity to renegotiate more favourable terms or refuse consent altogether.

For pharmaceutical royalty investors — who have every incentive to engage constructively with acquirers willing to honour the royalty stream — the more typical dynamic is not outright refusal but the extraction of comfort conditions: representations about the acquirer's financial strength, operational undertakings, and in strategic situations, equity kickers as demonstrated by the ADC Therapeutics amendment.

SEC Filing Patterns: What the Disclosures Reveal

Royalty assignment and novation events generate a predictable pattern of SEC disclosure that allows practitioners to track market practice in real time.

A Form 8-K under Item 1.01 (Entry into a Material Definitive Agreement) is required within four business days when a public company enters into a material agreement, including a royalty purchase agreement, or a material amendment to an existing one. When the agreement involves assignment or novation of an existing royalty obligation, the 8-K must describe the material terms of the transfer, including the identity of the new counterparty and the conditions under which the original party is released.

A Form 8-K under Item 2.01 (Completion of Acquisition or Disposition of Assets) is filed when a royalty interest is itself classified as a significant asset and changes hands. This is more common for royalty fund transactions — such as Royalty Pharma's 2025 acquisition of Royalty Pharma Manager, LLC — than for individual royalty transfers by biotechs, where the royalty obligation is typically a liability rather than an asset.

Annual report disclosures (Form 10-K and 20-F) provide the clearest sustained window into assignment restrictions. Companies disclose their royalty obligations in the notes to financial statements under "Royalty Financing Obligations" or equivalent headers, and the narrative description typically summarises the key restriction language. Royalty Pharma's annual filings describe its portfolio-level transfer mechanics in detail.

The Candel Therapeutics license and royalty agreement, filed as Exhibit 10.8 to a registration statement, illustrates a representative assignment clause: Candel may not assign without Periphagen's prior written consent, but may assign without consent to any affiliate or in connection with the transfer or sale of all or substantially all of its business, provided that any permitted assignee assumes all obligations.

This is the market-standard carve-out, and it leaves the novation question open: where the assignment carve-out applies (affiliate transfer, M&A), the original assignor may remain contingently liable. Where a clean break is needed, novation is the appropriate tool.

The Liability Tail: Why Assignment Alone Is Often Insufficient

The contingent liability problem with assignment-without-novation has practical consequences that are easy to underestimate at the time of a transaction but can resurface years later.

Consider a biotech that assigns its royalty payment obligations to an acquirer as part of an asset sale, relying on the M&A carve-out in the royalty agreement to avoid the consent requirement. The assignment is technically permitted. The acquirer assumes the obligations contractually. But the royalty investor never consented to the release of the original biotech.

Three years later, the acquirer misses a royalty payment — perhaps because the product's sales declined after a competitive entrant, or because the acquirer's financial condition deteriorated. The royalty investor turns to the original biotech for payment. Whether the original biotech has a claim against the acquirer (it does, under its indemnification agreement in the asset purchase) does not resolve the immediate problem: it faces a liability it believed it had escaped.

This scenario is the structural reason why sophisticated sell-side counsel in pharmaceutical royalty-heavy transactions consistently push for novation agreements as part of the closing documentation, even where the royalty agreement's assignment carve-out technically permits the transfer without consent. The cost of obtaining novation consent — which requires engaging the royalty investor and negotiating the terms of the new arrangement — is modest compared to the contingent liability it eliminates.

Royalty investors, for their part, are generally willing to novate in M&A transactions where the acquirer is a creditworthy entity with strong commercial capabilities. The investor's primary concern is that the royalty stream continues uninterrupted. If the acquirer provides better coverage of that concern than the original biotech — which is often true in acquisitions by large pharmaceutical companies — the investor has every incentive to consent to a clean novation.

Cross-Border Complexity

Pharmaceutical royalty transactions are inherently multinational. The royalty-generating product may be approved in the US, EU, and Japan. The biotech obligor may be incorporated in Switzerland (as ADC Therapeutics is). The royalty investor may be a Cayman-domiciled fund. The governing law of the royalty agreement may be New York or Delaware. And the restructuring that triggers the assignment question may be structured under the law of any of these jurisdictions.

The governing law clause of the royalty agreement determines which jurisdiction's rules on assignment and novation apply. Under New York law — which governs most major pharmaceutical royalty agreements — the general rule is that contractual rights are freely assignable unless the contract provides otherwise, but delegations of duties require the obligee's consent if performance by the delegate would materially differ from performance by the original obligor. Under English law, a similar framework applies but with different nuances around equitable assignment (which can occur without counterparty consent for pure payment rights, but requires notice) versus legal assignment (which requires written instrument and notice).

For cross-border transactions, the question of which jurisdiction's assignment-by-operation-of-law doctrine applies can be determinative. As the MTA Canada Royalty litigation demonstrated, a Delaware court will apply Delaware's interpretation of "assignment by operation of law" to a contract governed by Delaware law, even if the restructuring itself was effected under Canadian law. Companies with royalty agreements governed by New York or Delaware law must therefore conduct the assignment analysis under US law regardless of where the corporate reorganisation is occurring.

Drafting Implications: Getting the Language Right Before You Need It

The assignment and novation provisions in a royalty agreement drafted at the time of the initial financing will govern exit mechanics years later. The following drafting considerations reflect current market practice as of early 2026.

For biotechs entering royalty agreements, the priority is to ensure that the M&A carve-out is broad enough to facilitate a future sale without triggering a consent requirement. The ideal clause permits assignment without consent in connection with any merger, consolidation, change of control, or sale of all or substantially all of the assets or business, provided the acquirer assumes all obligations, and explicitly states that a reverse triangular merger does not constitute an assignment. Biotechs should resist language that deems a change of control to be an assignment requiring consent, since this gives the royalty investor veto power over M&A transactions.

For royalty investors, the priority is the opposite: consent rights over assignments to parties with materially different credit profiles or commercial capabilities, combined with a clear change-of-control provision that gives the investor notice and, in cases of significant credit deterioration, the right to accelerate. The investor should also ensure that any permitted assignment without consent does not release the original obligor — the liability tail is a credit protection tool.

For both parties, the governing law and dispute resolution provisions should be consistent with the counterparties' home jurisdictions and the jurisdictions where the royalty is generated. Using New York law for a royalty on a product that is primarily sold in the EU and marketed by a Swiss company, with a Cayman fund as investor, creates predictable friction when assignment questions arise at exit.

The following clause language, based on market-standard formulations reviewed across SEC-filed royalty agreements, illustrates the biotech-preferred construction:

"Neither party may assign or transfer this Agreement or any of its rights or obligations hereunder without the prior written consent of the other party, which consent shall not be unreasonably withheld, conditioned or delayed; provided that, without such consent, either party may assign this Agreement and its rights and obligations hereunder in connection with (a) any merger, consolidation, reorganisation or similar transaction, (b) the sale, transfer or other disposition of all or substantially all of its business or assets, or (c) an assignment to an Affiliate, in each case provided that the assignee assumes all obligations of the assigning party hereunder in writing. For clarity, a reverse triangular merger in which the assigning party survives as a wholly-owned subsidiary shall not constitute an assignment for purposes of this Section."

The investor-preferred addition appends: "…and provided further that no such permitted assignment shall relieve the assigning party of its obligations hereunder absent the express written consent of the non-assigning party."

Those two additions — the reverse triangular merger clarification and the liability tail preservation — represent the core negotiating battleground.

Conclusion

The assignment/novation distinction is a threshold legal question in every pharmaceutical royalty exit, yet it routinely receives less attention than the financial mechanics of change-of-control payments, buyout options, and royalty caps. That imbalance is worth correcting.

Assignment transfers rights. Novation transfers everything and releases the original party. The choice between them determines who bears contingent liability for royalty obligations after an M&A transaction, whether counterparty consent is required and when, and how the transaction interacts with governing law rules on assignment by operation of law. Across the roughly $29.4 billion in life sciences royalty financings completed between 2020 and 2024, these obligations have been accumulating in balance sheets that are increasingly subject to M&A activity as the market matures.

The SEC filing record offers a real-time map of how these transfers are documented and disclosed. Practitioners who understand the distinction between assignment and novation — and who build the right mechanics into royalty agreements at the outset — will find exits materially simpler and cleaner than those who discover the difference at the closing table.

All information in this article was accurate at the date of publication and is derived from publicly available sources including SEC filings, regulatory announcements, court decisions, and published legal analysis. Information may have changed since publication. This content is for informational purposes only. The author is not a lawyer or financial adviser, and nothing in this article constitutes investment, legal, or financial advice. Readers should consult qualified legal counsel before making decisions based on the concepts discussed.

Member discussion