Royalty Buybacks: When and Why Pharma Companies Repurchase Their Own Royalties

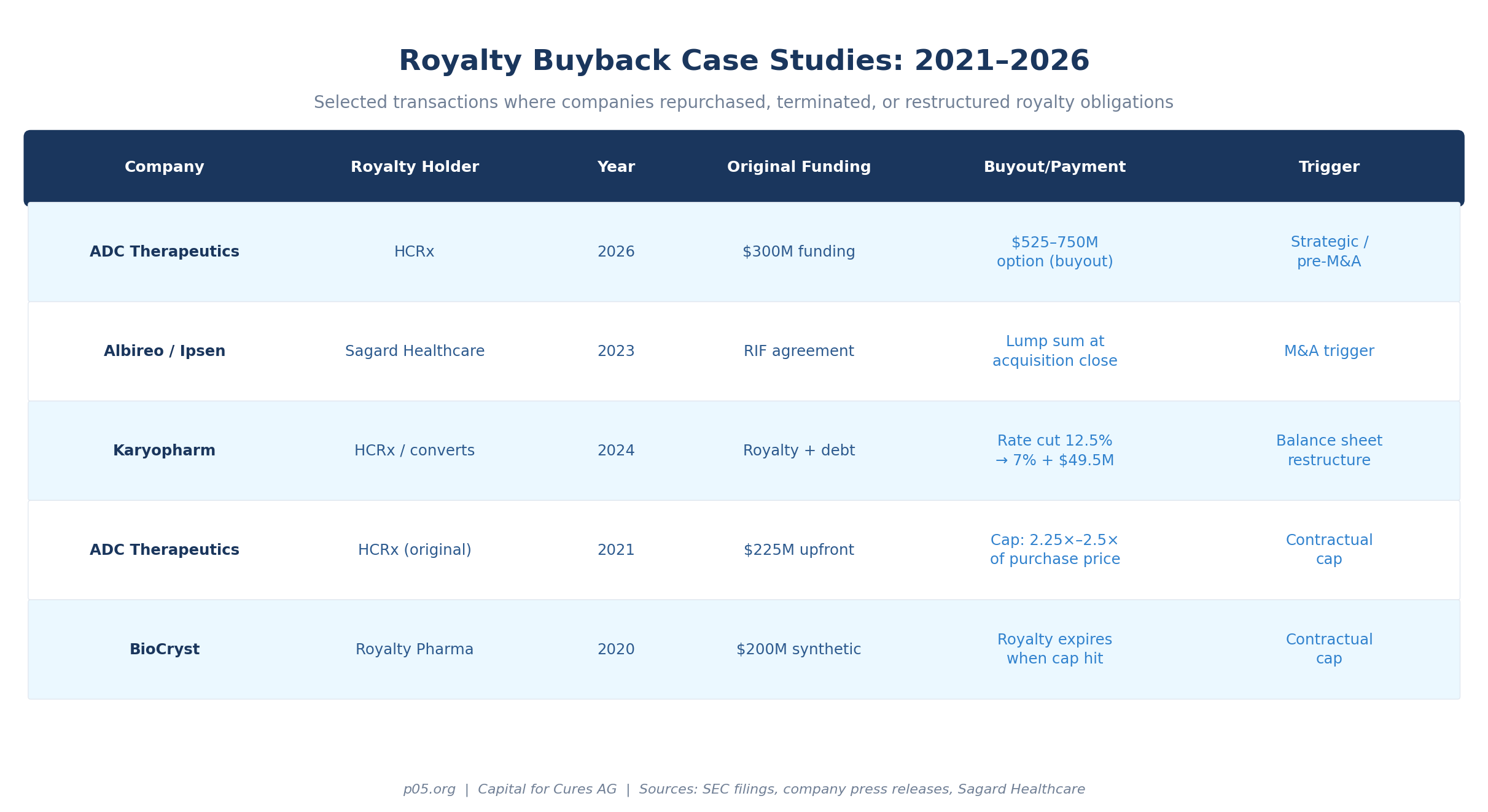

When ADC Therapeutics filed its February 2026 8-K amending its royalty agreement with HealthCare Royalty, the headline focused on the dramatic reduction of its change-of-control payment. Buried in the same filing was a contractual detail that answers a question the royalty financing industry rarely discusses directly: what happens when the company that sold a royalty wants it back?

The answer is a buyout option. Under the amended terms, ADC Therapeutics or any future acquirer may pay HealthCare Royalty $525 million on or before December 31, 2029, or $750 million thereafter, less royalties already paid and any change-of-control payment, to terminate all remaining royalty obligations on ZYNLONTA. The option exists. Whether it ever gets exercised is a separate question, and one that depends on a calculation most deal analysts never model.

This article examines the anatomy of pharmaceutical royalty buybacks: the contractual mechanisms that make them possible, the strategic logic that makes them rational, the market conditions that make them likely, and the examples from 2021 to 2026 that illustrate how they actually unfold. The answer to whether royalty buybacks "happen" is yes, but the frequency, form, and motivation vary significantly by context.

What Is a Royalty Buyback?

A royalty buyback occurs when the company whose product underlies a royalty obligation repurchases that obligation, terminating or reducing future payments to the royalty holder. It is the reverse of a royalty monetisation: instead of converting future revenue streams into present cash, the company converts present cash into the elimination of a future liability.

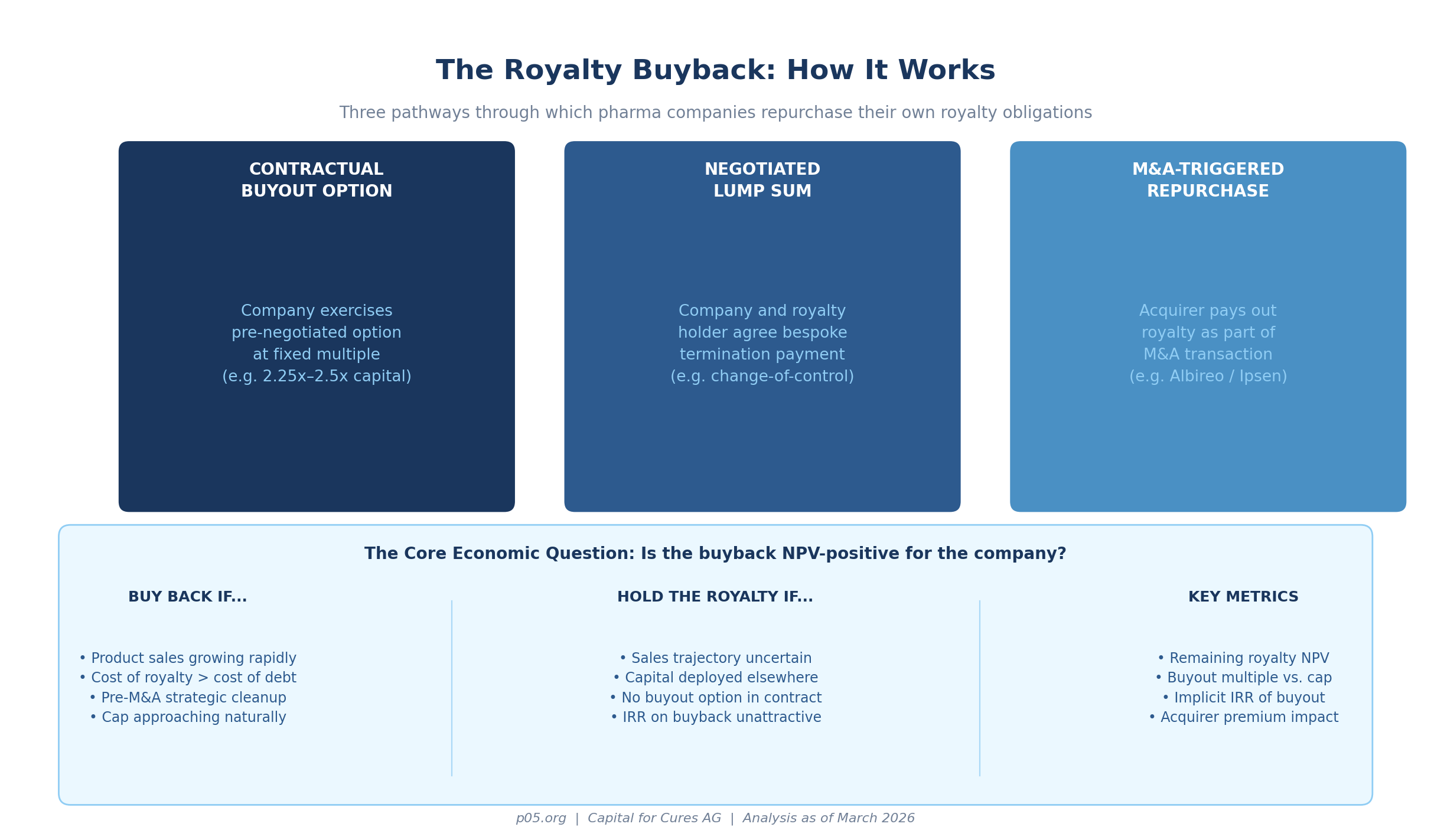

The mechanics depend entirely on the contract. Royalty agreements can be structured in three ways that permit buybacks:

Contractual caps. The simplest structure terminates automatically. The royalty agreement specifies that obligations end once the royalty holder has received a fixed multiple of the original investment, typically between 1.5x and 3.0x of capital deployed. When sales accumulate enough to hit the cap, the royalty terminates without any active repurchase. From the company's perspective, the cap represents the ceiling cost of the original financing; from the royalty holder's perspective, it limits upside but provides certainty.

Pre-negotiated buyout options. Many revenue interest financing agreements include explicit buyout provisions giving the company the right, but not the obligation, to terminate remaining royalty obligations by paying a lump sum. These options are typically structured as a fixed multiple of the original investment, net of royalties already paid.

The ADC Therapeutics option at $525 million to $750 million, against $300 million of original funding, represents a 1.75x to 2.5x gross multiple. The original 2021 ADC/HealthCare Royalty agreement specified that the royalty would terminate upon payment of 2.25x to 2.5x of the purchase price, a typical range for commercial-stage assets.

Negotiated terminations. Where no contractual option exists, companies may negotiate directly with royalty holders to terminate obligations at an agreed price. This is rarer and requires both parties to agree on the net present value of remaining royalties, a calculation that depends heavily on contested assumptions about future sales.

Does It Actually Happen?

The short answer is yes, but the frequency is lower than popular perception suggests, and the pathways are narrower than most companies expect.

Caps are the most common form. In the synthetic royalty market, capped structures where the royalty terminates automatically after the investor receives a fixed return are standard practice. Gibson Dunn's Royalty Report tracked $29.4 billion in life sciences royalty financings from 2020 to 2024, with synthetic royalties growing as a share of that total.

Most of these transactions include caps. The cap is not a buyback in the active sense, but it functions identically from the company's perspective: at some point, the obligation ends and the full revenue stream reverts to the company.

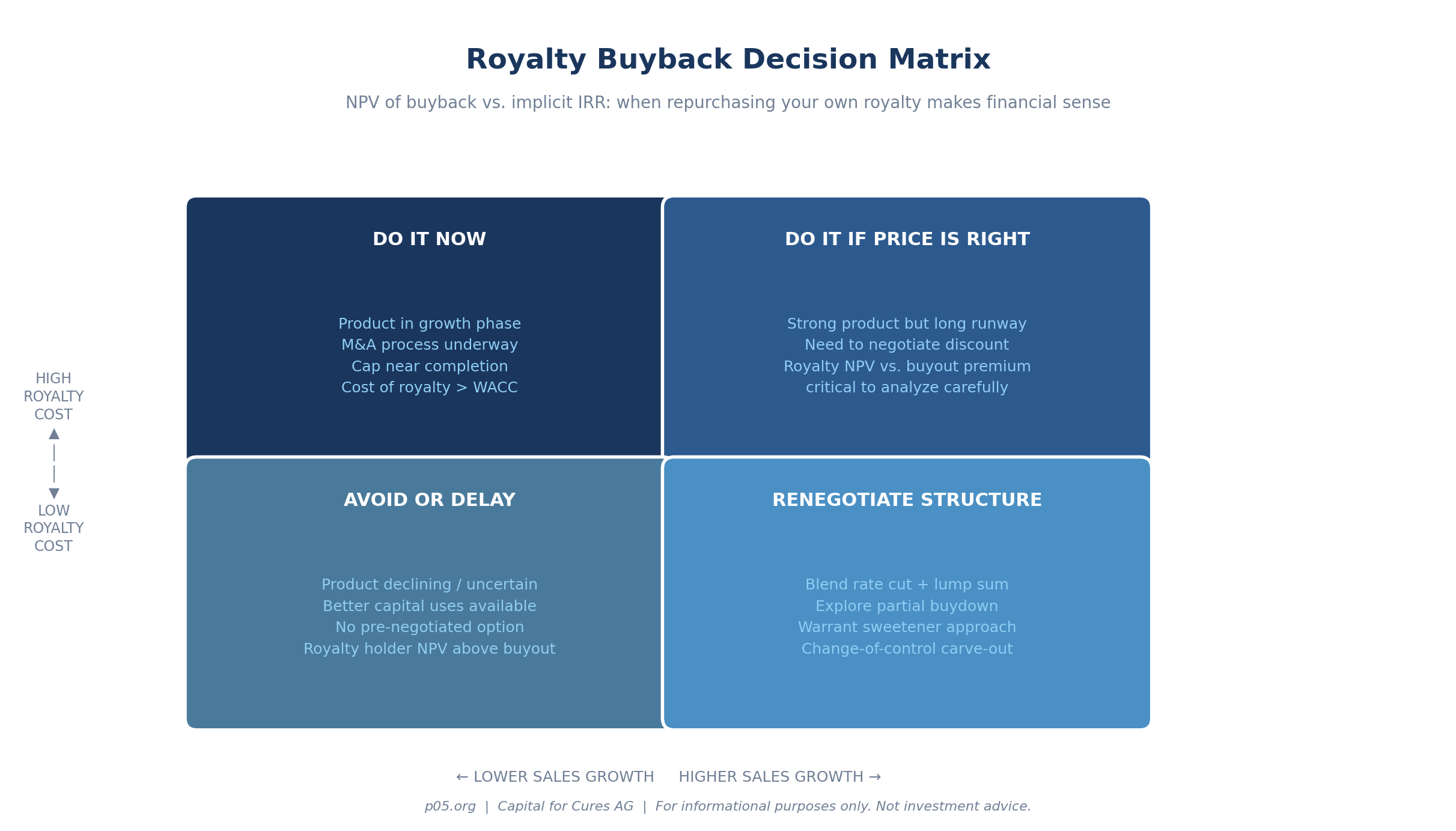

Active buyouts are rarer. Exercising a pre-negotiated buyout option requires the company to have sufficient cash or debt capacity to fund the lump sum, and to conclude that the NPV of eliminating future royalty payments exceeds the immediate cost.

This calculation rarely favours buyout early in a product's commercial life, when royalties are small and the product's trajectory remains uncertain. It becomes more attractive as products approach blockbuster status and the remaining royalty NPV grows.

M&A is the most powerful catalyst. The most reliable trigger for royalty buybacks is acquisition activity. When a large pharmaceutical company acquires a biotech, it routinely seeks to eliminate all encumbrances on the acquired product portfolio. A royalty obligation representing, for example, a 7% burden on net sales of a $500 million product is worth roughly $35 million annually in perpetuity at steady state. An acquirer with a 10% cost of capital would pay up to $350 million to eliminate it.

If the contractual buyout price is below this NPV, the buyback is economically rational. This is why buyout provisions in royalty agreements are sometimes called "M&A provisions": they are structured with eventual acquisition in mind.

The Strategic Logic: Why Companies Buy Back Royalties

Four motivations drive royalty repurchases in practice.

Cost of capital arbitrage. A royalty obligation carrying an implied yield of 10% to 15%, a typical range for commercial-stage synthetic royalties per Covington's life sciences financing overview, is expensive relative to investment-grade debt at 5% to 7%. For a company that has achieved commercial success and acquired a solid credit profile, retiring high-cost royalty obligations with cheaper debt creates immediate financial value.

The savings compound over the remaining life of the royalty. This logic parallels corporate bond refinancing: when the original financing terms become expensive relative to prevailing rates, repurchase is rational.

M&A preparation. As I examined in Royalties That Wake Up: How Change-of-Control Triggers Reshape Pharma Deal Economics, change-of-control provisions in royalty agreements can become acquisition deterrents. A $750 million change-of-control payment against a $500 million market capitalisation, as ADC Therapeutics faced before its February 2026 amendment, renders a company essentially unacquirable. Reducing that payment, or eliminating the royalty entirely through a pre-acquisition buyback, directly increases acquirability and likely increases the acquisition premium the company can command.

The buyback, in this framing, is a value-creation exercise for equity holders: eliminating a liability that was suppressing the company's strategic value.

Balance sheet simplification. Royalty obligations complicate financial analysis. Equity investors unfamiliar with the royalty market may discount companies with large outstanding royalty liabilities more than warranted, because the liability is non-linear: rising faster than sales when products outperform. Eliminating the royalty converts a complex off-balance-sheet liability into a simple, understood expense (interest on the debt used to fund the buyback).

This optionality is particularly valuable ahead of equity raises or analyst coverage initiation.

Incremental margin recapture. On a blockbuster product, a 7% royalty on net sales represents substantial foregone revenue. For a product generating $800 million in annual sales, elimination of a 7% royalty recaptures $56 million per year in perpetuity. At a 10x earnings multiple, that has a $560 million equity value impact.

Buying out the royalty for $400 million would represent an immediate $160 million of value creation for shareholders, even before accounting for the increased strategic flexibility.

Case Studies

ADC Therapeutics and HealthCare Royalty: The Buyout Option

The longest-running documented example in the current market involves ADC Therapeutics and HealthCare Royalty Partners. In August 2021, ADC Therapeutics entered into a royalty purchase agreement with HealthCare Royalty for up to $325 million, selling a 7% royalty on ZYNLONTA sales.

The agreement included a provision terminating the royalty upon cumulative payments of 2.25x to 2.5x the purchase price, which at $300 million of actual funding represents a cap of approximately $675 million to $750 million.

The February 2026 amendment, which also reduced the change-of-control payment from $750 million to $150 million to $200 million, clarified the buyout option terms: ADC or any acquirer may pay $525 million (on or before December 31, 2029) or $750 million (from January 1, 2030), minus royalties paid and any change-of-control payment. The existence of this option is not incidental; it is central to any valuation of the company's strategic worth.

At ZYNLONTA's current sales trajectory, the royalty cap will not be hit organically for many years. But a buyout could be rational well before that point if an acquirer's cost of capital is low enough to make paying $525 million now preferable to paying $525 million to $750 million progressively through the cap over a decade.

Albireo Pharma and Sagard Healthcare: The M&A-Triggered Buyout

Sagard Healthcare's analysis of revenue interest financing documents the Albireo Pharma transaction as a textbook example of an M&A-triggered buyback. Albireo had entered into a revenue interest financing agreement with Sagard that included a buyout option requiring a payment of a fixed multiple on invested capital, net of royalties received.

When Ipsen acquired Albireo for $952 million in March 2023, exercising its tender offer at $42 per share plus a contingent value right, the acquisition triggered the buyout provision. Ipsen paid the contractual buyout amount as part of the transaction, eliminating the royalty obligation on Bylvay (odevixibat). The fact that the buyout provision existed and was structurable made Albireo more acquirable: Ipsen knew the cost of full ownership before bidding, eliminating the uncertainty that a trailing royalty obligation would otherwise create.

This pattern repeats consistently in pharmaceutical M&A. Acquirers of royalty-burdened companies routinely execute buyouts at closing, treating them as a known transaction cost rather than an unresolvable encumbrance.

Karyopharm Therapeutics: The Partial Buydown

Karyopharm's May 2024 refinancing represents a variant: the partial royalty repurchase. Rather than eliminating the royalty entirely, Karyopharm negotiated a rate reduction from a tiered schedule reaching 12.5% to a flat 7.0% on XPOVIO sales. In exchange, HealthCare Royalty received a $49.5 million cash payment, a $15 million term loan note, and $5 million in convertible notes.

This is not a full buyback but functionally resembles one: the company is paying cash today to reduce future royalty expense permanently.

The net present value calculation is identical. If $49.5 million in cash today eliminates, say, $8 million per year in additional royalty expense (the difference between the old tiered rate and the new 7% flat rate at relevant sales levels), and the company's cost of capital is 10%, the NPV of the benefit is approximately $80 million against a cost of $49.5 million. The partial buydown is economically rational, and it preserves the royalty relationship for future financing needs.

BioCryst Pharmaceuticals: The Organic Cap

BioCryst's synthetic royalty agreement with Royalty Pharma on Orladeyo provides an example of the organic cap mechanism. Under the original agreement signed in 2020, Royalty Pharma acquired a royalty on Orladeyo sales for $200 million, with the royalty expiring automatically once cumulative royalty payments reach a fixed cap.

As Orladeyo sales have grown toward blockbuster trajectory, the company has been paying down the cap progressively without any active buyback decision. When the cap is reached, the full Orladeyo revenue stream reverts to BioCryst automatically.

The cap structure illustrates a key difference from a negotiated buyback: no cash outflow, no IRR calculation, no negotiation.

The buyback, in effect, happens passively as a consequence of commercial success. Companies with strong product trajectories and capped royalty structures are effectively guaranteed to recapture full economics at some point; the only variable is when.

The Prevalence Question: How Often Does This Happen?

Precise data on royalty buyback frequency is unavailable, because most terminations occur quietly, as contractual caps are reached without any announcement, or as provisions in larger M&A transactions without separate disclosure. But several structural observations allow an estimate.

The Gibson Dunn Royalty Report documented $29.4 billion in life sciences royalty financings from 2020 to 2024. Of that total, roughly 40% to 50% were synthetic royalties with capped structures. If average cap multiples of 2.0x to 2.5x and average royalty durations of 8 to 12 years are assumed, a meaningful fraction of the capped synthetic royalties from the 2015 to 2020 vintages are approaching or have reached cap.

This implies quiet terminations occurring throughout the market at a steady pace, unreported because they require no announcement.

Negotiated buyouts and M&A-triggered terminations are rarer but concentrated in high-value transactions. Any pharmaceutical acquisition above $500 million involving a royalty-burdened target will typically include a royalty buyout. Based on Royalty Pharma's disclosure that roughly 40% of major pharma M&A transactions from 2016 to 2023 involved a product on which Royalty Pharma holds royalties, the rate of M&A-triggered royalty resolution is meaningful.

Goodwin's October 2025 analysis of the royalty market noted that the aggregate transaction volume for 2025 was annualising at approximately $5.4 billion, compared with $5.1 billion for 2024, with average transaction sizes declining slightly even as volumes held firm.

This growth in new royalty creation, without a commensurate increase in reported buybacks, suggests the total stock of outstanding royalty obligations is expanding faster than it is being retired, consistent with the industry being in an early-to-mid growth phase where products are still building toward cap rather than hitting it.

Structural Features That Enable or Prevent Buybacks

Not all royalty agreements contain buyout provisions. Whether a company can execute a buyback depends on what was negotiated at inception, a point that is often underappreciated at the time of the original deal.

Caps vs. perpetual royalties. Traditional licensing royalties, where a university or research institution receives a royalty on all future sales in perpetuity, typically contain no buyout provision. These are genuine perpetual obligations. By contrast, synthetic royalties and revenue interest financing agreements almost always include caps or buyout options, because they are structured as financing transactions where the investor's return target requires a defined endpoint.

Change-of-control mechanics. The ADC/HealthCare Royalty amendment is instructive because it illustrates how change-of-control provisions interact with buyout options. Before the amendment, the $750 million change-of-control payment was functionally a non-optional buyout triggered by acquisition, at a price that may have deterred acquirers.

The amendment created a lower, more acquirer-friendly change-of-control payment while preserving an optional buyout. The distinction matters: mandatory change-of-control payments are acquisition deterrents; optional buyout provisions are acquisition facilitators.

Royalty cap design. The specific level at which a cap is set determines the effective cost of the financing. A 2.25x cap on a $300 million investment means the company will pay at most $675 million, regardless of how successful the product becomes. For a product achieving $1 billion in annual sales with a 7% royalty, the cap would be reached in approximately 3.2 years at that sales level, after which all royalty payments cease.

The cap is therefore both a ceiling on financing cost and an implicit buyout: the company purchases back full economics by reaching the cap.

The Buyer's Perspective: Why Royalty Holders Accept Buyouts

A royalty holder accepting a buyout is forgoing future cash flows in exchange for present certainty. The rationality of this depends on two factors: the holder's view of the product's future trajectory, and the price relative to its own NPV estimate.

Royalty investors accept buyouts when they can redeploy capital at higher returns than the remaining royalty would generate. As the Gibson Dunn report noted, target returns for commercial-stage royalties are typically in the high-single to low-double-digit range. If a royalty is now generating a 9% return on the original investment (because the product has succeeded and the remaining NPV at a higher discount rate is modest), the royalty holder might prefer to take the buyout at 1.5x cost and redeploy into a new investment targeting 12% to 15%.

This creates an interesting alignment: royalty buybacks are most likely to be negotiated when both parties perceive the product as successful enough to make the existing royalty expensive for the company but not so uniquely valuable that the royalty holder insists on a prohibitive price. The zone of agreement in buyout negotiations is often narrower than it appears.

Implications for M&A Due Diligence

Any acquirer of a pharmaceutical company must model royalty buyout costs as a first-order variable, not a footnote. For targets with synthetic royalty obligations, this requires:

Identifying all royalty agreements in the data room. Royalty obligations may appear in multiple places: as disclosed liabilities in financial statements, as obligations under licensing agreements, and as encumbrances on product economics. Each agreement must be reviewed for buyout provisions, change-of-control triggers, and cap mechanics.

Calculating the NPV of remaining obligations. The present value of future royalty payments, under the acquirer's sales assumptions and at the acquirer's cost of capital, is the theoretical maximum rational buyout price. If the contractual buyout price is below this NPV, immediate exercise is economically rational. If it is above, retaining the royalty obligation and paying it down naturally may be preferable.

Modelling the impact on the acquisition premium. A company with a $400 million royalty obligation generating $35 million per year should be valued differently from an otherwise identical company with no royalty obligation. The market often fails to make this calculation precisely, creating opportunities for acquirers who do.

Assessing the royalty holder's likely cooperation. In cases where no contractual buyout option exists, the acquirer's willingness to offer a premium over the royalty NPV, and the royalty holder's willingness to accept it, determines whether an elective buyout is achievable.

Accounting and Disclosure

Royalty buybacks have specific accounting consequences that are sometimes overlooked. Under both US GAAP (ASC 470 and ASC 835) and IFRS, royalty financing arrangements are typically accounted for as debt or as non-debt liabilities, depending on whether the arrangement meets the definition of a financial liability. When the royalty has a fixed cap, the liability represents the present value of future royalty payments up to the cap, accreted over the expected payment period.

When a company exercises a buyout option and pays a lump sum to terminate a royalty, the accounting treatment depends on whether the buyout price exceeds the carrying value of the liability. If it does, the excess is recognised as a loss on extinguishment. If it is below carrying value, the difference is a gain. For companies with long-standing royalty arrangements where the product has significantly outperformed original projections, the carrying value may be substantially below the buyout price, resulting in a loss that surprises analysts unfamiliar with royalty accounting.

What to Watch

Three structural trends suggest the frequency of royalty buybacks will increase through 2026 to 2030.

First, the large synthetic royalty deals executed between 2018 and 2022 are approaching the window where exercise of buyout options becomes economically rational. Products backed by these deals, including several with cap structures, are hitting commercial scale. The cohort of potential buyouts is growing.

Second, pharmaceutical M&A is recovering. After a period of subdued deal activity, the combination of strong large-pharma cash flow and a pipeline of mid-cap royalty-burdened targets creates conditions for M&A-triggered buyouts at scale. Any major acquisition of a company with outstanding synthetic royalties will require royalty resolution.

Third, the interest rate environment has moderated sufficiently that refinancing high-cost royalty obligations with investment-grade debt is once again economically attractive. The cost of a royalty at a 12% implied yield versus 6% investment-grade debt represents a 600 basis point spread that compounds significantly over the remaining life of a product's royalty period.

For companies now entering into royalty financing agreements, the lesson is contractual: negotiate the buyout option at inception, not when the royalty has become burdensome and the holder's leverage has increased. The ADC Therapeutics experience, where the buyout option was present from the start and the February 2026 amendment merely clarified its terms, illustrates the value of pre-negotiated exit mechanics.

Conclusion

Royalty buybacks are real, they are rational, and they are underappreciated as a strategic tool in pharmaceutical capital allocation. They happen in three distinct ways: automatically through cap attainment, actively through exercise of pre-negotiated buyout options, and transactionally through M&A-triggered termination payments. Of these, cap attainment is the most frequent, active buyout exercise is the rarest, and M&A-triggered termination is the most economically significant.

The conditions that make buybacks rational, commercial success of the underlying product, improving access to lower-cost capital, and pending acquisition activity, are precisely the conditions that make the royalty holder's assets most valuable. Negotiating from a position of strength requires having negotiated the option to buy back at inception, before the royalty holder knows the product will succeed.

The next generation of royalty financing agreements, shaped by the lessons of the 2018 to 2024 cohort, will almost certainly incorporate more sophisticated buyout mechanisms: tiered pricing, time-sensitive options, and hybrid structures that blend rate reductions with partial lump sums, much as Karyopharm demonstrated in 2024. The question is no longer whether pharma companies repurchase their royalties. It is whether they have the contractual tools to do so on terms that make financial sense.

All information in this report was accurate as of the research date and is derived from publicly available sources including company press releases, SEC filings, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.

Member discussion