Royalty meets venture

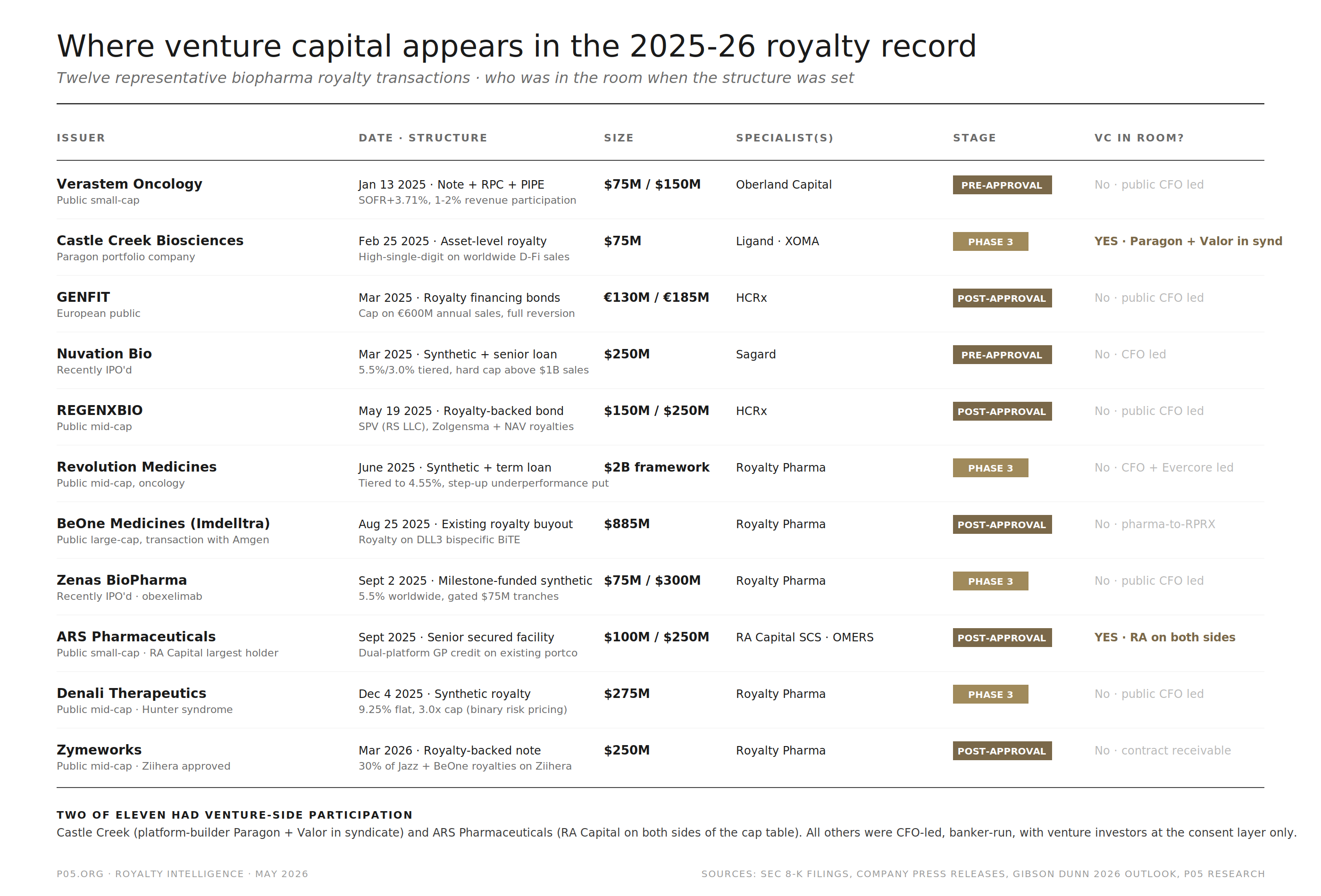

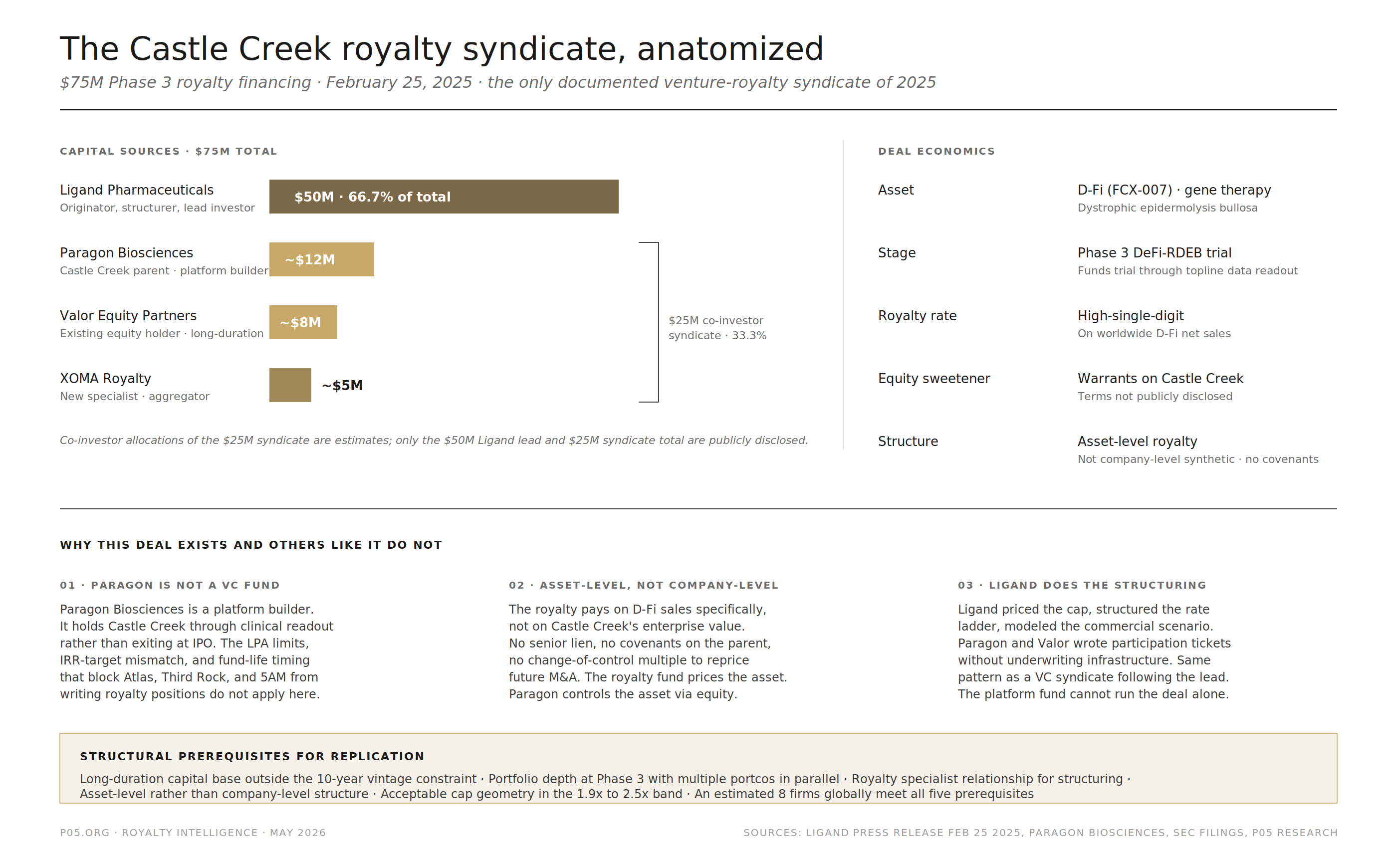

Of the twenty-seven biopharma royalty transactions executed in 2025, one had venture investors writing into the syndicate. Castle Creek Biosciences, February 25, 2025. Ligand wrote $50 million, three co-investors wrote $25 million, the royalty paid high-single-digit on worldwide D-Fi sales. Two of those three co-investors were existing equity holders in Castle Creek.

A market that ran $7.1 billion through 27 deals produced exactly one instance of what the legal trade press calls the future of biotech finance. The question worth asking is not why so few. The IRR mismatch between royalty and venture capital explains that. The question is what Castle Creek had that the other twenty-six did not, why exactly two firms wrote into the royalty alongside Ligand, and whether the structural conditions that produced this one deal can be made to produce more.

The pattern is visible. Eleven representative 2025 and early-2026 transactions. Eight are pre-approval or post-approval on public companies, with the CFO and a banker leading the process and venture investors present only at the consent layer. Two are dual-platform: ARS with RA Capital on both sides, Adaptive with OrbiMed across instruments (not shown). One is the Castle Creek pattern. Eleven deals, one instance of the structure most discussions are gesturing at when they talk about venture-royalty integration.

What Castle Creek actually was

The press releases described Castle Creek as a venture-royalty syndicate. The framing is wrong in a specific way that explains both why this deal exists and why it has not been replicated.

Paragon Biosciences is not a venture capital fund. It is a platform builder. Paragon creates, builds, and funds bioscience companies. It holds seven portcos across cell and gene therapy and adaptive biology. Castle Creek is a Paragon-built portco. Paragon led the $112.8 million Series in May 2022, has participated in every prior round, and remains the controlling shareholder.

Valor Equity Partners operates similarly. Antonio Gracias's vehicle holds long-duration positions across Tesla, SpaceX, and a small biotech book including Castle Creek. Valor is not constrained by standard 10-year fund-life timing.

Two existing Castle Creek investors wrote $25 million combined into the royalty syndicate. Both operate outside the 10-year vintage fund structure that defines traditional biotech VC. That single structural fact is what made the deal possible.

Paragon is not trying to clear 25 percent IRR on the royalty position. Paragon is using the syndicate to extend Castle Creek's runway through topline data without diluting the equity stake the platform already controls. The royalty pays high-single-digit on worldwide D-Fi sales if the trial succeeds. If it fails, Paragon loses its share of the $25 million and the equity position is unchanged. Asymmetric upside on a portfolio company Paragon already underwrites. No LPA amendment, no separate IC, no fund-life mismatch.

The asset-level structure is the other half. The royalty pays on D-Fi sales specifically, not on Castle Creek's enterprise value. No senior lien on the parent, no covenants on the company, no change-of-control multiple to reprice future M&A. The royalty fund prices the asset's commercial probability. The platform builder controls the asset through the equity position. The two sides do not collide because they are pricing different things.

Ligand did the structuring. Without Ligand the deal does not exist. The platform builder does not have the technical capacity to price the royalty cap, structure the rate ladder, or model the worldwide commercial scenario tree. The specialist runs the underwriting, the platform writes a participation check. This is the same pattern as a syndicate lead and a follow-on investor in a venture round, transposed onto royalty.

Why the Series B Atlas fund cannot do what Paragon did

Three structural constraints prevent the traditional vintage biotech VC fund from replicating Castle Creek on its own portfolio companies.

The LPA constraint. Most biotech VC LPAs restrict the fund to equity investments in portfolio companies, with allowances for venture debt and bridge financing. Royalty positions, even on a portfolio company's own asset, sit outside the standard investment policy. The fund would need an LPA amendment, a side-letter, or a separate co-investment vehicle. All three are expensive and slow.

The IRR target mismatch. A $25 million royalty position with a 1.9x cap pays back at most $47.5 million over 10 to 15 years. That is 4 to 7 percent IRR on the royalty line item. Below the fund hurdle, which is typically 20 percent net to LPs. The royalty position drags the fund's blended return. A platform builder that holds long-duration capital does not face the same drag because the platform's return is measured on the equity position, with the royalty as a secondary instrument.

The fund-life timing constraint. A 2020-vintage fund is in year five or six by 2025. Reserves at year five are typically committed to equity follow-ons in the same portfolio. A royalty position is not a follow-on. It does not increase ownership. It is a separate instrument with separate economics and a separate downstream profile. The reserve allocation does not naturally accommodate it.

The result. Traditional biotech VC funds will continue to consent to royalty deals on their portfolio companies under the NVCA-form preferred consent triggers, will continue to occasionally participate in concurrent PIPEs alongside public-company royalty deals after the portco is public, and will continue to have effectively zero participation in the Castle Creek-style asset-level royalty syndicate at private-company Phase 3.

This is why the 2025 deal record produced one Castle Creek and not five.

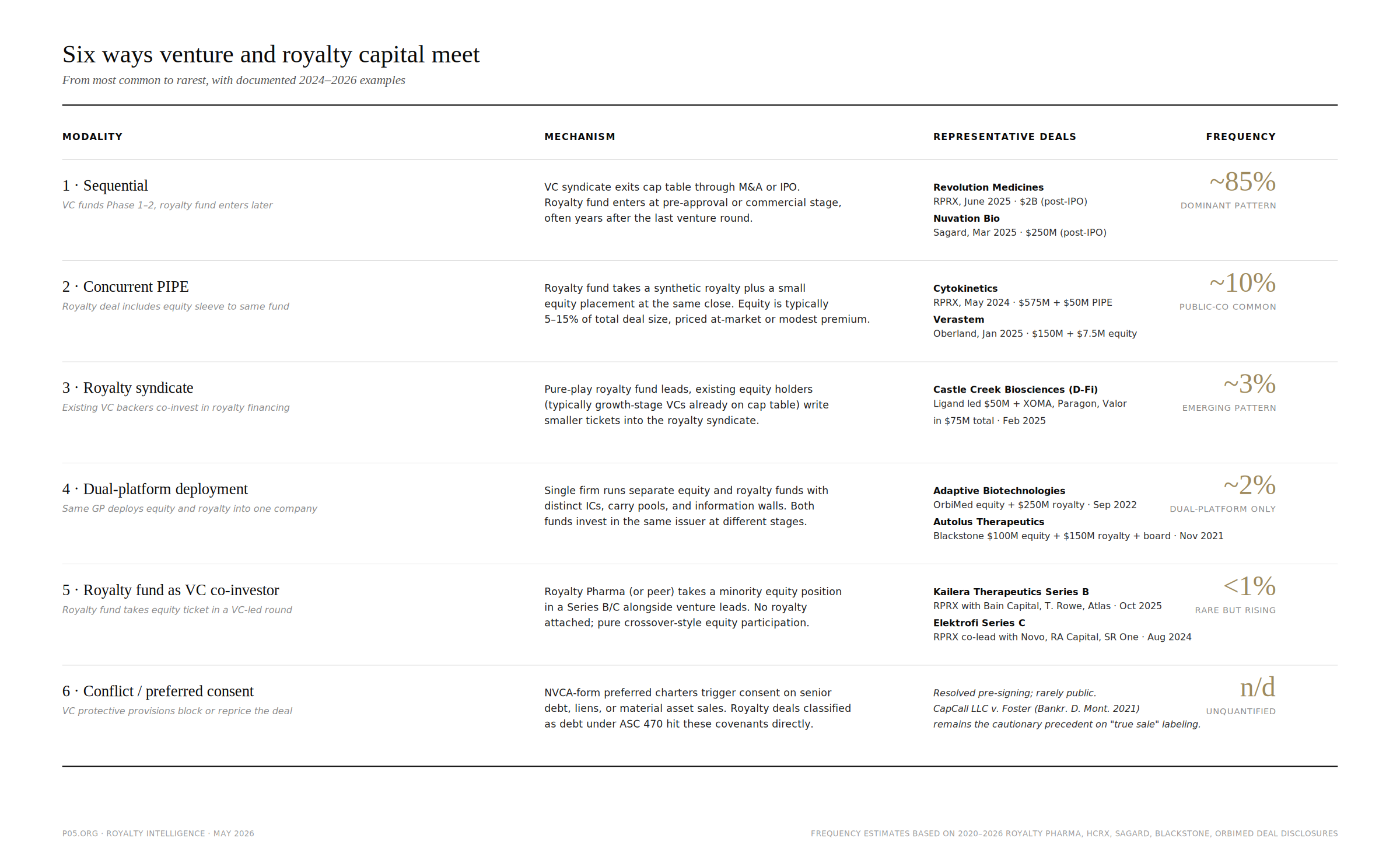

The six modalities place Castle Creek at modality three, "Royalty syndicate," with a frequency estimate around three percent and the label "emerging pattern." The dominant pattern is modality one, sequential operation: VC exits cap table through M&A or IPO, royalty fund enters later. The five remaining modalities including Castle Creek sit at five percent of deal count or below combined.

Who actually has the structural capacity

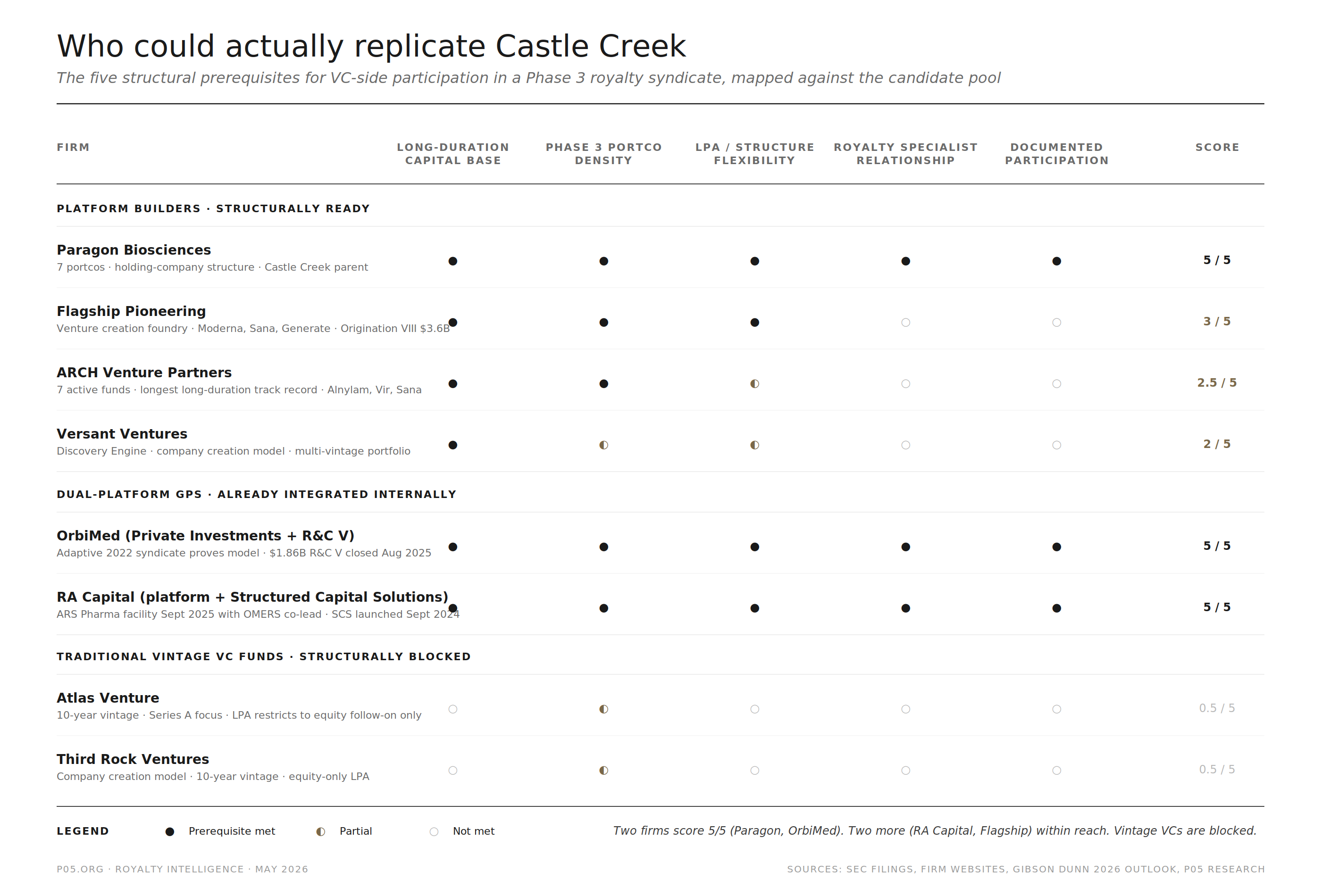

The five prerequisites for replicating Castle Creek are specific enough to enumerate. Long-duration capital base. Portfolio depth at Phase 3 with multiple portcos in parallel. LPA or structure flexibility for non-equity instruments. Royalty specialist relationship for structuring. Documented willingness to participate.

The candidate universe is small.

Two firms score five-for-five. Paragon (Castle Creek proves it). OrbiMed, where Private Investments preceded the $250 million Royalty and Credit royalty into Adaptive Biotechnologies in 2022 and the Royalty and Credit V fund closed at $1.86 billion in August 2025. Two more are within reach. RA Capital, where Structured Capital Solutions launched September 2024 and the $250 million ARS Pharmaceuticals facility in September 2025 with OMERS as co-lead is the proof of concept. Flagship Pioneering, where Origination Fund VIII closed at $3.6 billion and the portfolio includes Moderna, Sana, Generate, Tessera, and roughly forty other portcos at various stages.

ARCH and Versant sit in the middle. Both have long-duration capital and company-creation models. Neither has a documented royalty syndication on its own portfolio. The bio strategy inside Andreessen Horowitz operates under the firm's RIA structure with the structural flexibility, but its portfolio is younger and Phase 3 density is not yet there.

The 10-year vintage funds at the bottom of the table cannot do this. Atlas, Third Rock, 5AM, Frazier, MPM. The structural constraints described above are not negotiable inside a standard fund vehicle.

Roughly eight firms globally have the capacity. None has yet run the Castle Creek pattern as a programmatic strategy. The reasons are not about willingness.

Why the platform builders have not done this yet, repeatedly

Three plausible answers for why a Flagship, ARCH, or a16z bio has not yet routed multiple Phase 3 portcos into royalty syndicates as a default capital tool.

The IRR drag is real even for platform funds. A $25 million royalty position paying back at 4 to 7 percent IRR is still a drag on the platform's blended return, even if the platform's mandate accommodates it. The platform has to decide whether the cap-table-preservation benefit on the equity position justifies the IRR cost on the royalty position. The answer is sometimes yes and often no.

The optics are complicated. A platform fund that finances its own portco through a royalty syndicate is, in the worst-case framing, transferring asset-level upside from the equity stack (where the platform owns it through the equity position) to a royalty stack (where the platform owns a smaller slice). The platform fund has to explain to its LPs why it wrote both sides of the same asset. Information walls and separate IC discipline reduce the optical problem but do not eliminate it.

The royalty specialists prefer to deal direct. Ligand structured Castle Creek. Paragon and Valor followed. The specialist does not need the platform fund's participation to clear the syndicate. The specialist could syndicate to other royalty funds, structured credit funds, or family offices and reach the same total. The specialist routes through the platform fund only when the platform fund is already on the cap table and the structuring conversation is easier with them inside than outside. Without that prior relationship, the deal happens without them.

The structural argument for repeating Castle Creek therefore depends on something that does not yet exist: a default relationship layer between platform-builder funds and royalty specialists, where the specialist commits to structuring the platform's eligible Phase 3 portcos and the platform commits to follow-on participation on pre-negotiated terms. GP-to-GP relationship rather than deal-by-deal. The closest analog is what SVB built with venture capital funds for venture debt.

The covenant geometry has been moving against issuers

While the platform-builder thesis explains where the partnership could plausibly happen, the broader 2020-to-2026 market has been making the partnership harder, not easier, on the company side.

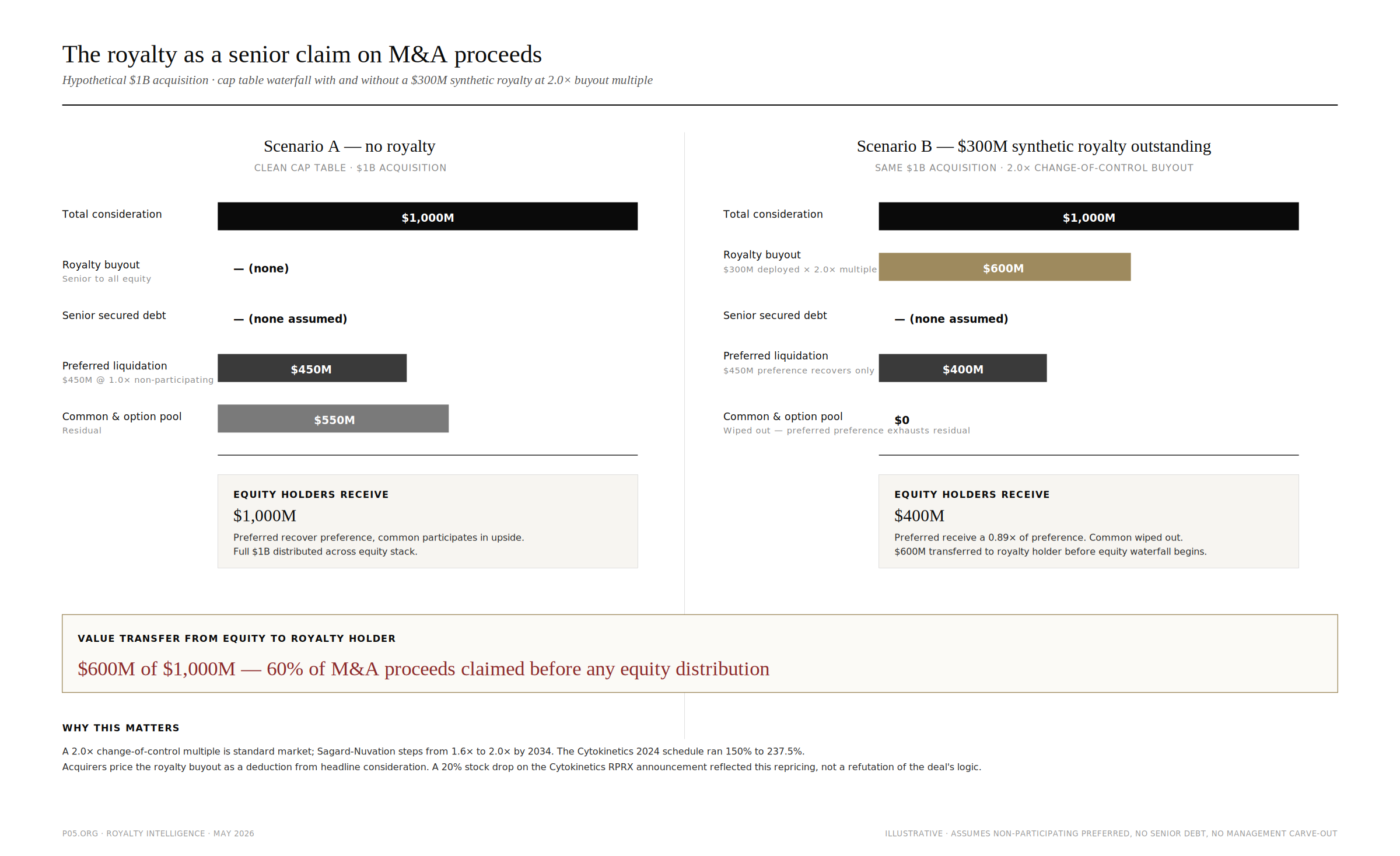

Caps stratified into a 1.43 to 3.0x band by risk class. Median 1.9x. Change-of-control multiples standardized at 1.5 to 2.5x with time-step ladders. Sagard-Nuvation taletrectinib steps 140/160/175/200 percent. Cytokinetics 2024 runs 150 to 237.5 percent. Step-up rate clauses now trigger if prior-year sales miss target. The Royalty Pharma-Revolution Medicines structure has a step-up clause from 2030 to 2041 that raises the royalty rate if sales miss threshold, which is an underperformance put on issuer commercial execution dressed as a royalty.

The 91 percent share of synthetic value in 2024-2025 reflects buyer-favorable structuring, not issuer-favorable terms. The Cytokinetics episode remains the empirical anchor. May 22 2024 expansion sent the stock from $59.23 to $48.62 intraday. Mizuho's Salim Syed surveyed 29 buy-side investors. Pre-deal 17 of 29 placed M&A probability at 50 percent or higher. Post-deal 21 of 29 placed it at one in five or lower.

The mechanism is contractual. A $300 million royalty at 2.0x change-of-control buyout multiple flows $600 million to the royalty holder before any equity waterfall begins. Clarke Futch of HCRx pushed back in December 2025: across 110 HCRx deals, acquisitions have not been an issue. Revolution Medicines traded flat on the June 2025 announcement, suggesting the market differentiates extending runway for a known commercializer from signaling no buyer is coming. The mechanism is still present in every modern synthetic. A venture investor underwriting M&A within three years has to price this in. A platform builder underwriting a long-duration equity hold does not, because the M&A scenario is further out and the asset-level structure does not stack against M&A proceeds in the same way.

That is the second reason Castle Creek-style deals work for platform builders and not for vintage funds. The M&A repricing risk is borne differently. The vintage fund needs M&A within three to five years to clear the fund. The platform builder can wait a decade.

The market has been growing without the venture leg

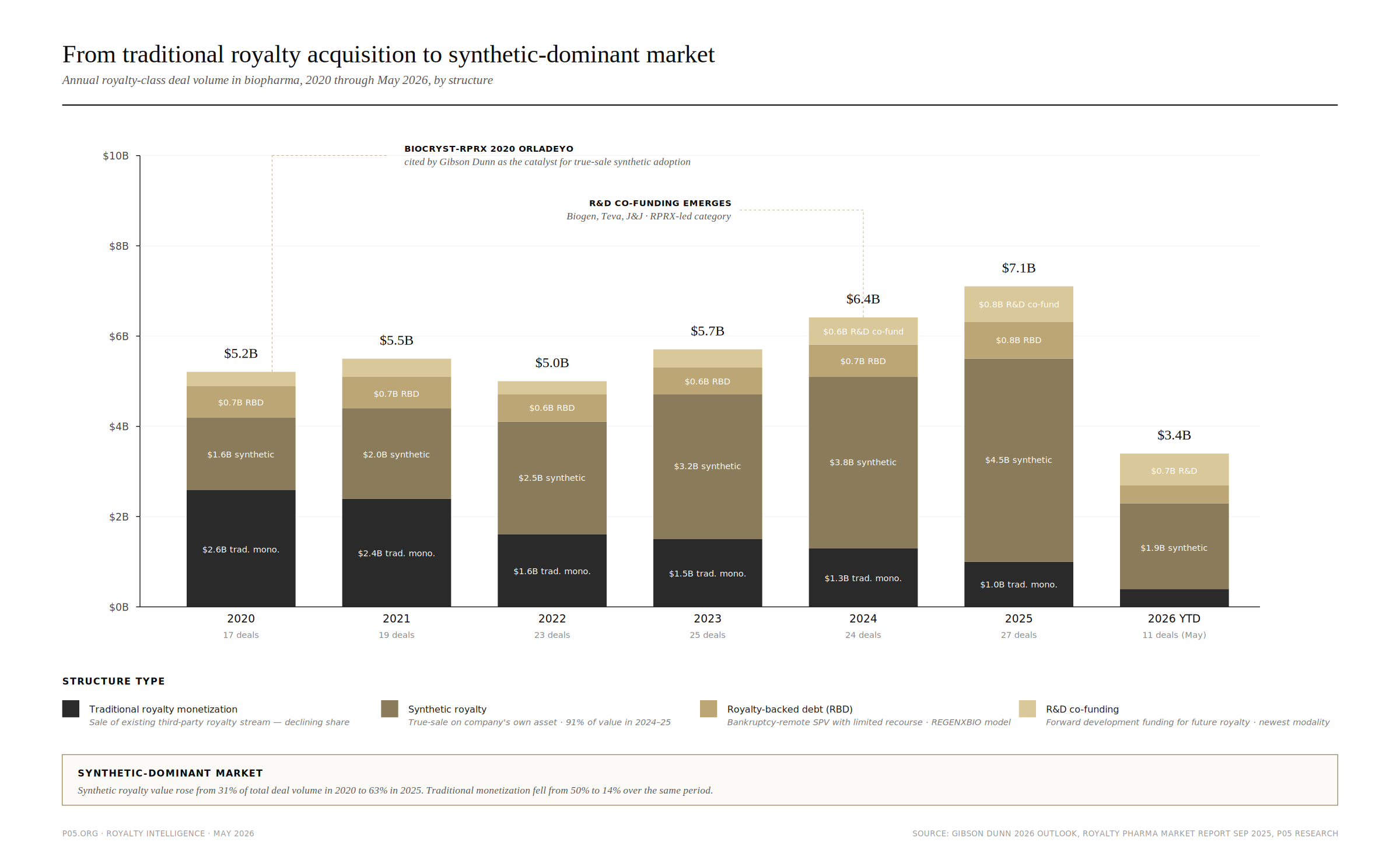

The 2020-to-2026 expansion of the royalty asset class happened through public-company synthetics and pre-approval R&D co-funding, not through venture-stage participation.

Annual deal value rose from $5.2 billion in 2020 to $7.1 billion in 2025. Deal count stable at 25 to 27 per year. Traditional royalty monetization shrank from 50 percent of value in 2020 to 14 percent in 2025. Synthetic royalty grew from 31 percent to 63 percent. R&D co-funding emerged as the newest modality. None of this growth was venture-routed. It was CFO-led, banker-run, structurer-driven, with venture investors at the consent layer.

The implication for the platform-builder thesis: the market has been demonstrating the demand for royalty capital at scale without involving venture firms at the origination layer. Whether the platform builders can carve out a separate channel where they participate on their own portcos' Phase 3 syndicates is a different question from whether the market itself needs them to. The market does not. The platform builders might.

The LP layer is doing what the GP layer is not

The integration the convergence narrative gestures at does exist, but at a different layer than the GP-to-GP one most discussions focus on.

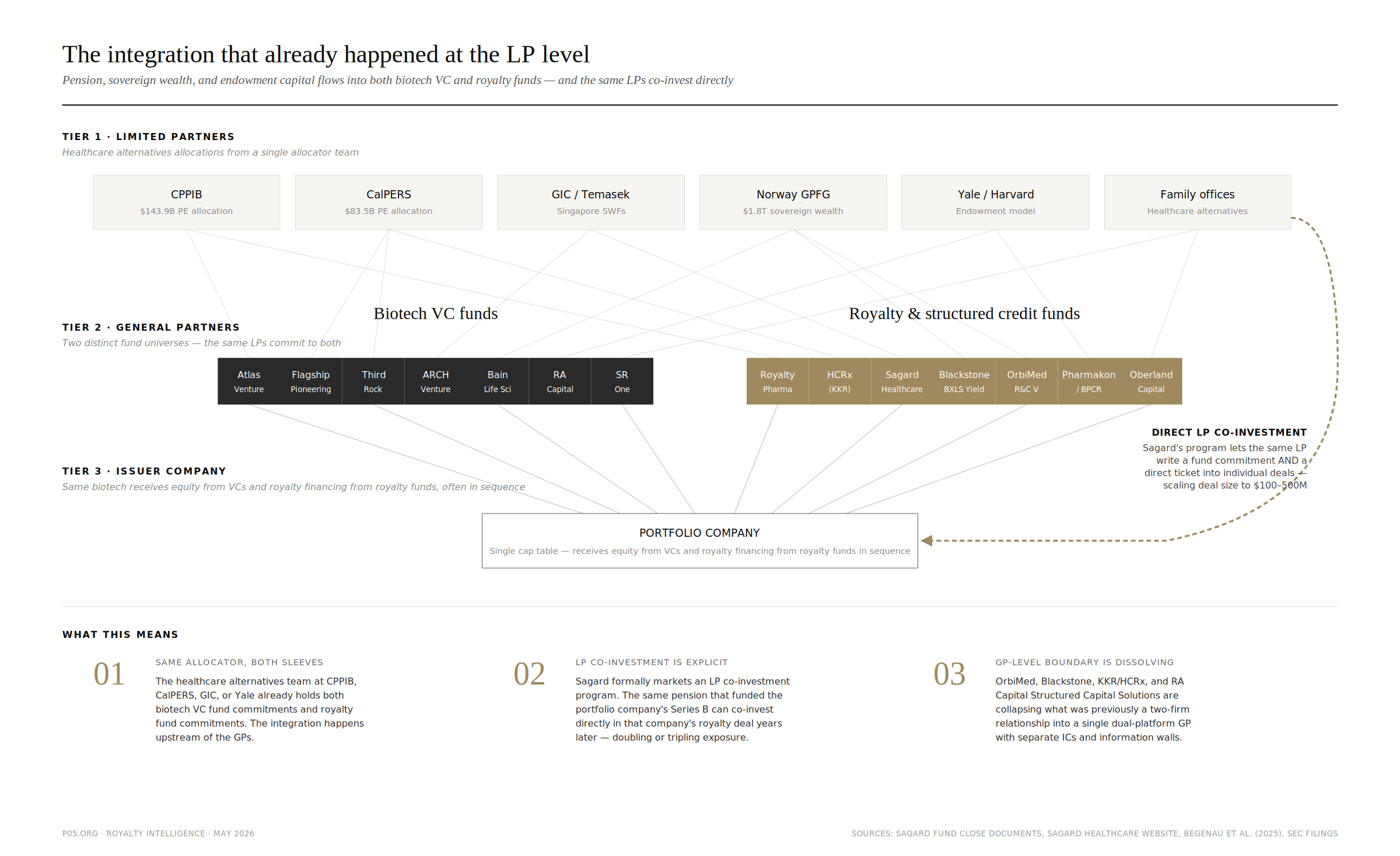

CPPIB, CalPERS, GIC, Norway GPFG, Yale, Harvard, and the family-office tier hold biotech VC and royalty funds out of the same healthcare alternatives allocation. Sagard markets a formal LP co-investment program into individual royalty transactions. The same pension fund that funded a portfolio company's Series B can write directly into its synthetic four years later.

The September 2025 ARS Pharmaceuticals deal is the most legible 2025 signal of where this goes. RA Capital led with $100 million initial of a $250 million facility. The co-lead was OMERS Life Sciences, the direct-investing arm of the Ontario Municipal Employees Retirement System. OMERS is not a royalty fund. OMERS is a pension that allocates to biotech VC out of one healthcare alternatives bucket and to royalty and structured credit funds out of the same bucket. By writing direct into ARS alongside RA Capital, OMERS bypassed the dual-platform GP construct and put its own capital across the venture-royalty seam without needing a GP integrator.

If LP-direct cross-sleeve coordination becomes a pattern, the dual-platform GP construct loses part of its rationale. The pension and sovereign allocator becomes the integrator instead of the GP. The competitive moat OrbiMed, KKR/HCRx, Blackstone, Carlyle/Abingworth, and RA Capital have been building at the GP level is being arbitraged by their own LPs at the same time it is being constructed.

For the platform-builder thesis, the LP-direct signal matters in a specific way. If pension allocators are willing to write direct alongside the GP they already fund, they could also write direct alongside a platform builder on a portfolio company's Phase 3 syndicate. Paragon's $25 million share at Castle Creek could plausibly have been a $25 million Paragon ticket plus a $50 million CPPIB or OMERS direct ticket, structured by Ligand, syndicated alongside. That deal does not exist in 2025 either. The structural prerequisites are present.

Where this points

Castle Creek is the proof of concept. It is also the limit case. One deal in 2025. Specific to a platform-builder structure with a Phase 3 asset and a specialist willing to syndicate to non-traditional co-investors. The platform builders and dual-platform firms that meet the prerequisites number roughly eight globally. None has run the pattern repeatedly.

The structural opportunity that emerges from the case study is the relationship layer between platform-builder funds and royalty specialists, mediated by an LP base that is already integrated and starting to write direct. Three components:

A royalty specialist with mid-market origination capacity that builds a programmatic platform-fund partnership. Ligand-XOMA after Q3 2026 closing is the leading candidate. The combined platform will hold more than 200 assets across stages with Ligand's $25 to $60 million origination capacity on Phase 3 assets and XOMA's aggregator infrastructure on smaller partnered interests.

A platform-builder fund with multiple Phase 3 portcos that commits to follow-on participation as a default. Paragon has done this once. Flagship Pioneering and ARCH have the structural capacity and the portfolio depth. Neither has signaled a programmatic move yet.

An LP direct-investment posture across the seam. OMERS at ARS is the visible signal. CPPIB, GIC, Norway GPFG, and Yale have the architecture in place. None has built the deal-level coordination yet that would make the LP-direct route programmatic.

If these three components converge over the next 18 months, the Castle Creek pattern becomes a market segment. If they do not, the asset class continues to grow through public-company synthetics, the dual-platform GPs continue to capture firm-level economics, and the venture-royalty interaction at the company level continues to produce one deal per year.

So what is the relationship

Venture and royalty capital are not partners and probably will not become partners in the way the convergence narrative suggests. The IRR seam is hard. The underwriting cultures are different. The covenant geometry has been moving against issuers since 2020.

The exception is the platform-builder fund operating with long-duration capital outside the 10-year vintage constraint. For these firms, writing into an asset-level royalty syndicate on a portfolio company's Phase 3 asset is structurally feasible. Paragon and Valor did it once at Castle Creek. Roughly six other firms globally could do the same on their own portcos. None has, except as a one-off.

The integration the convergence narrative gestures at is real at the LP layer, where it has been operational for over a decade, and starting to surface at the GP-LP coordination layer through programs like Sagard's LP co-investment and direct-investment tickets like OMERS at ARS. It is performative at the GP-to-GP dual-platform layer, where the conflict is internalized rather than resolved. It is essentially absent at the company level for venture-stage biotechs, with one Castle Creek per year as the exception.

The market opportunity sits in the relationship infrastructure that would let the platform builders do Castle Creek repeatedly. That infrastructure does not exist yet. The first specialist that builds it will define the segment. The first platform builder that commits to it will set the template. The first LP that writes direct alongside both will demonstrate the LP-arbitrage of the dual-platform GP construct.

Everything else in the convergence narrative is sequencing dressed as partnership.

All information in this report was accurate as of the research date and is derived from publicly available sources including court opinions, regulatory guidance, academic literature, SEC filings, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.