Secondary Royalty Market Liquidity: Bid-Ask Spreads and Price Discovery

When Royalty Pharma announced in December 2025 that it had acquired a "pre-existing royalty interest" in Nuvalent's neladalkib and zidesamtinib from "an undisclosed third party" for up to $315 million, most readers focused on the therapeutic thesis. The more interesting detail was the four words hidden in the transaction structure: pre-existing and undisclosed third party.

That phrasing is as close as the pharmaceutical royalty market gets to describing a secondary transaction. Someone owned a royalty they no longer wanted. Royalty Pharma was willing to buy it.

A price was agreed in private, the seller remains unnamed, and the deal closed without a quoted spread, a visible clearing price, or any mechanism for the broader market to observe what the royalty was worth before it sold. In a mature secondary market, that transaction would generate a data point. In this one, it generates a press release.

This article is about what that gap means: why a true secondary market for pharmaceutical royalties does not yet exist, how the limited secondary activity that does occur actually works, what the structural prerequisites for a proper market would look like, and why those prerequisites remain frustratingly far from being met.

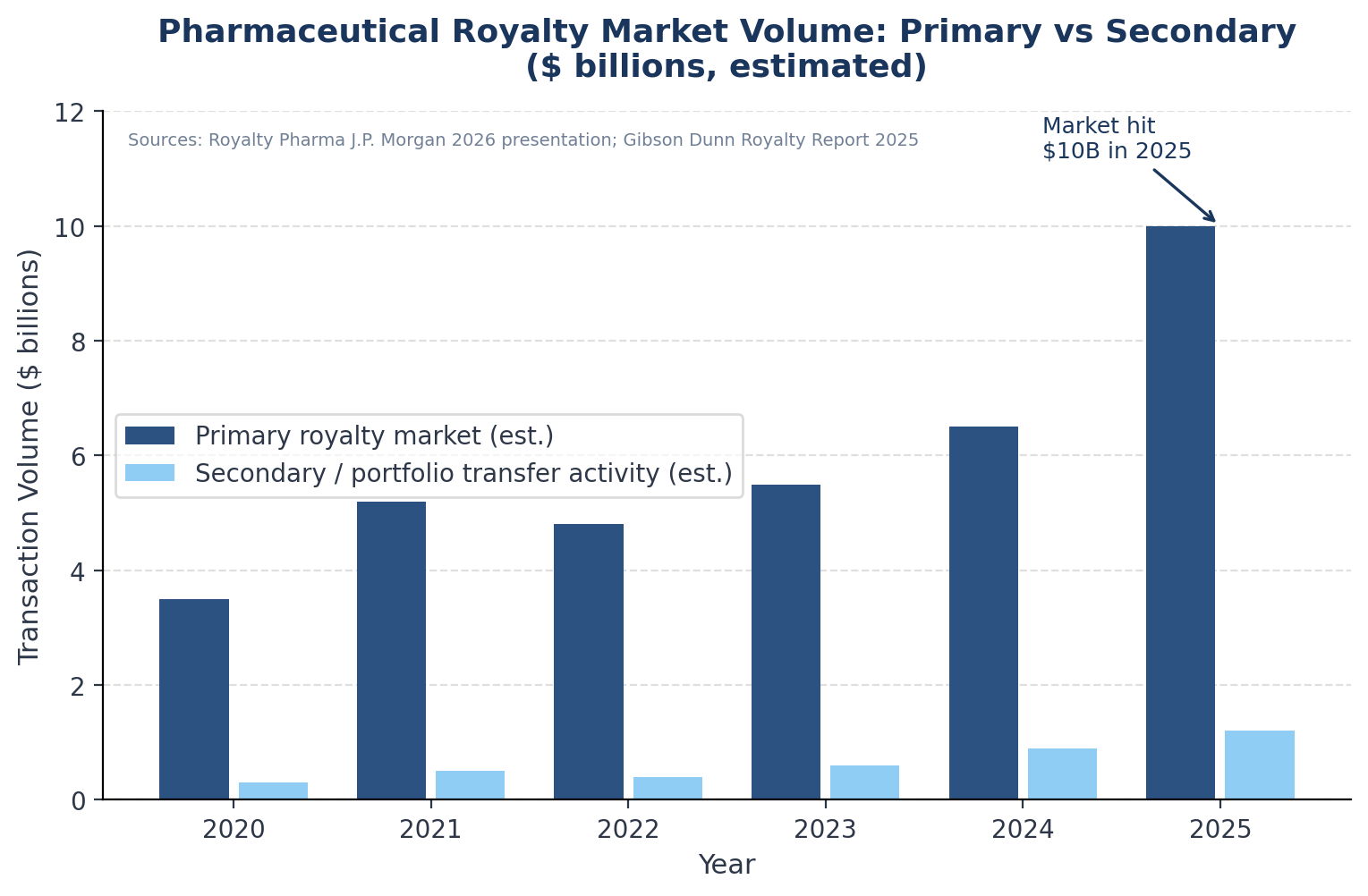

The $10 Billion Market Without a Secondary

The pharmaceutical royalty market has grown from an estimated $200 million annually at the turn of the century to a market that, by Royalty Pharma's own account, crossed $10 billion in total transaction value for the first time in 2025. Royalty Pharma itself deployed $2.6 billion on royalty transactions in 2025, with announced transaction value of $4.7 billion, representing approximately 40% market share.

The Gibson Dunn Royalty Report documented $29.4 billion in life sciences royalty financings from the leading participants between 2020 and 2024.

These are large numbers. But nearly every dollar in them represents a primary transaction: a biotech company creating a new royalty stream and selling it to an investor in exchange for capital.

What remains almost entirely absent is the infrastructure for the royalty interest itself to be resold — for the investor who bought it to exit to a different buyer, for valuation to be continuously observable, for there to be any price between which a seller can offer and a buyer can bid.

The contrast with adjacent markets is stark. The private equity secondaries market exceeded $160 billion in transaction volume in 2024, with average LP-led secondary pricing reaching 89% of NAV, reflecting years of infrastructure investment in pricing databases, placement platforms, and standardised documentation.

The leveraged loan market, while also OTC and relationship-driven, has the Loan Syndications and Trading Association's standard documentation, a robust secondary market, and continuous dealer quotes. The pharmaceutical royalty market has none of these things.

Does a Secondary Market Exist At All?

It would be inaccurate to say no secondary market exists. What exists is a thin, opaque, bilateral market in which transfers of existing royalty interests occasionally occur, conducted entirely through private negotiation with no centralised infrastructure. The activity falls into three recognisable patterns.

Pattern 1: Portfolio Monetisation by Fund Managers

The clearest examples are transactions in which a royalty fund or private equity firm that originally created a royalty position later decides to monetise it. Royalty Pharma's acquisition of Alnylam's AMVUTTRA royalty from Blackstone for $310 million in November 2025 follows this template: Blackstone Life Sciences had originally created the royalty position and later sold it to Royalty Pharma, presumably near or at end-of-fund-life or as part of a portfolio rebalancing.

Earlier in 2025, the acquisition of the Nuvalent TKI royalty from an unnamed seller at $315 million is a similar transaction.

These deals do constitute a secondary market in the economic sense: an existing royalty was transferred from one investor to another at a negotiated price. What they do not constitute is a market in the trading sense. The counterparties are known to each other. Terms are negotiated bilaterally over weeks or months. No competing bids are solicited in a structured process.

The price is never publicly disclosed in a form that would allow inference of discount to book value or implied yield. The seller in the Nuvalent transaction is, three months later, still simply "an undisclosed third party."

Pattern 2: Original Royalty Holders Monetising to Funds

The most active form of secondary activity is original royalty holders — typically universities, research hospitals, or the inventors behind licensed drugs — selling their royalty interests to specialist funds. This is the commercial model of Royalty Pharma, which describes itself as funding innovation "both directly and indirectly — directly when it partners with companies to co-fund late-stage clinical trials, and indirectly when it acquires existing royalties from the original innovators."

Royalty Pharma's December 2025 acquisition of the remaining portion of PTC Therapeutics' royalty on Roche's Evrysdi for $240 million upfront plus up to $60 million in milestones exemplifies this. PTC Therapeutics originally held a tiered 8-16% royalty on worldwide Evrysdi net sales as the originating licensor.

It monetised that royalty to Royalty Pharma in stages over several years. This is a secondary transfer in legal form, but in practice it is closer to a primary transaction in that the original royalty holder is exercising a financial right created at the time of the original licensing deal, not engaging in portfolio trading.

Pattern 3: Corporate Balance Sheet Monetisations

The third pattern involves companies monetising royalty assets embedded in their balance sheets. Royalty Pharma's January 2025 sale of MorphoSys Development Funding Bonds for $511 million, monetised at a 5.35% discount rate, represents this category: Royalty Pharma sold a fixed-income-like instrument to "a syndicate of investors" through BofA Securities acting as placement agent. Pablo Legorreta, Royalty Pharma's CEO, noted that the company "does not generally sell royalty investments" but that Novartis' acquisition of MorphoSys created a "unique opportunity."

The qualifier "does not generally sell" is informative. Even the market's largest and most sophisticated participant treats secondary sales as exceptional events requiring specific justification, not as routine portfolio management activity.

The Bid-Ask Problem: Why Spreads Cannot Be Observed

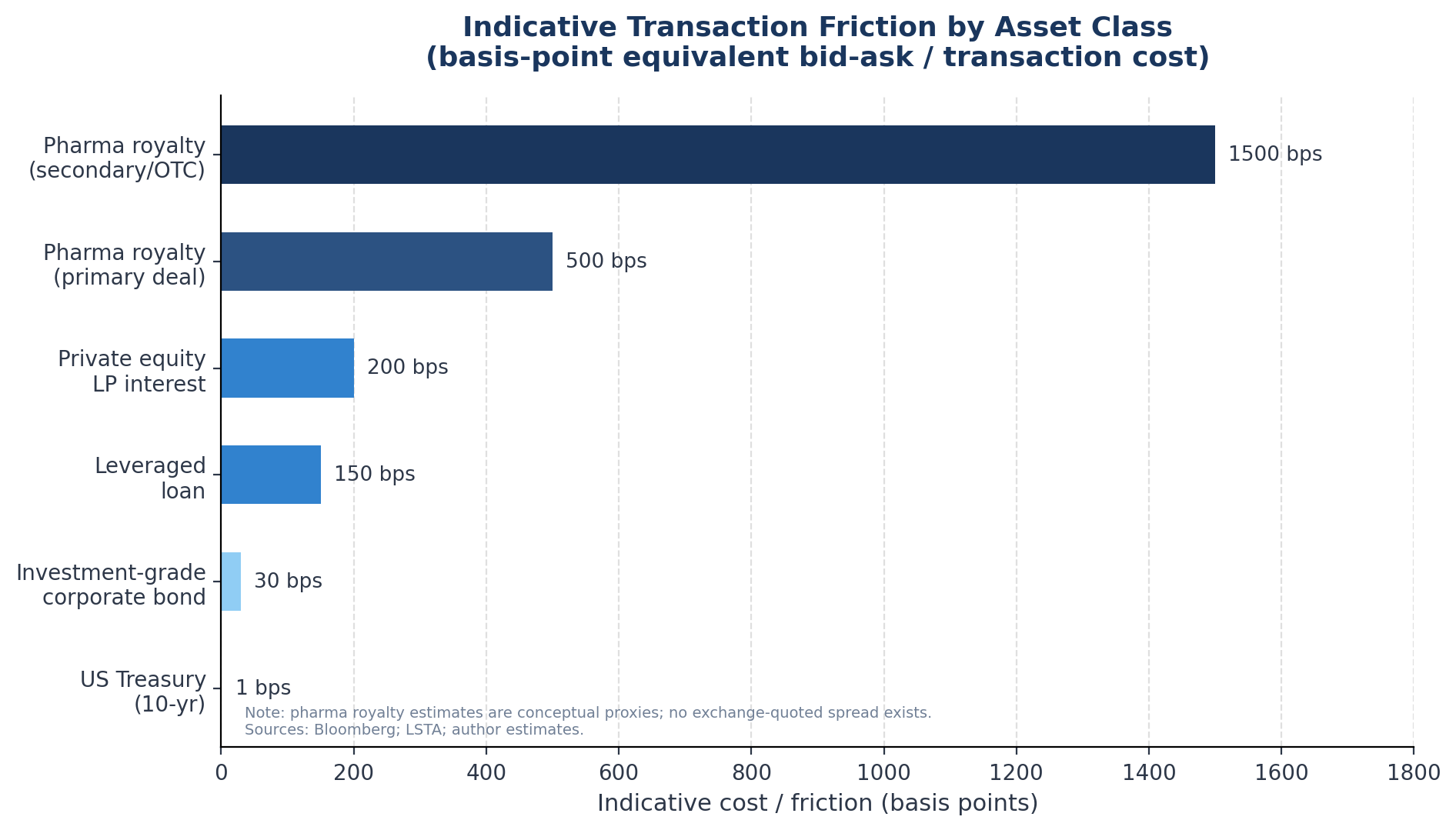

In any functioning market, a bid-ask spread is the difference between the highest price a buyer is willing to pay and the lowest price a seller is willing to accept. The spread reflects several forces simultaneously: transaction costs, information asymmetry, inventory risk for market makers, and the difficulty of valuing the underlying asset. In liquid markets like US Treasuries, the bid-ask spread on a ten-year note is measured in fractions of a basis point.

In leveraged loans — OTC, but with established secondary market infrastructure — spreads typically run 50-200 basis points depending on credit quality. In private equity LP interests, where the Jefferies secondary market data shows transaction-weighted discounts of around 11% from NAV in 2024 (a measure that functions as a rough proxy for the cost of immediate exit), the implied spread is hundreds of basis points.

For pharmaceutical royalties, there is no observable bid-ask spread because there is no market structure in which bids and asks are simultaneously expressed. What exists instead is a sequential bilateral process: a potential seller approaches a known buyer — almost always one of the handful of dedicated royalty funds — the buyer conducts diligence, makes an offer, and the seller either accepts or walks away.

The "spread" in this context is the difference between the seller's reservation price (usually their internal NPV calculation) and the buyer's offer (usually a significantly discounted alternative calculation). That gap is never published, and the transactions that do close are announced with minimal price transparency.

The absence of a quoted spread is not merely a cosmetic inconvenience. It has real economic consequences: it prevents arbitrage, it allows individual royalty buyers to extract information rents from sellers who cannot benchmark their offers, it makes portfolio mark-to-market for royalty investors fundamentally subjective, and it prevents the market from sending price signals about shifting assumptions on drug trajectories, patent duration, or therapeutic risk.

For comparison, the conceptual bid-ask friction in a pharmaceutical royalty secondary transaction — accounting for the cost of bilateral negotiation, the absence of competing bids, information asymmetry, and the illiquidity premium demanded by buyers — likely runs to several hundred basis points equivalent, or 1,000-1,500 basis points for smaller or more complex assets.

No comparable friction exists in investment-grade credit markets, and even the private equity secondaries market — far more developed than pharmaceutical royalties — has narrowed its bid-ask spread considerably over the past decade.

Why No Proper Market Exists

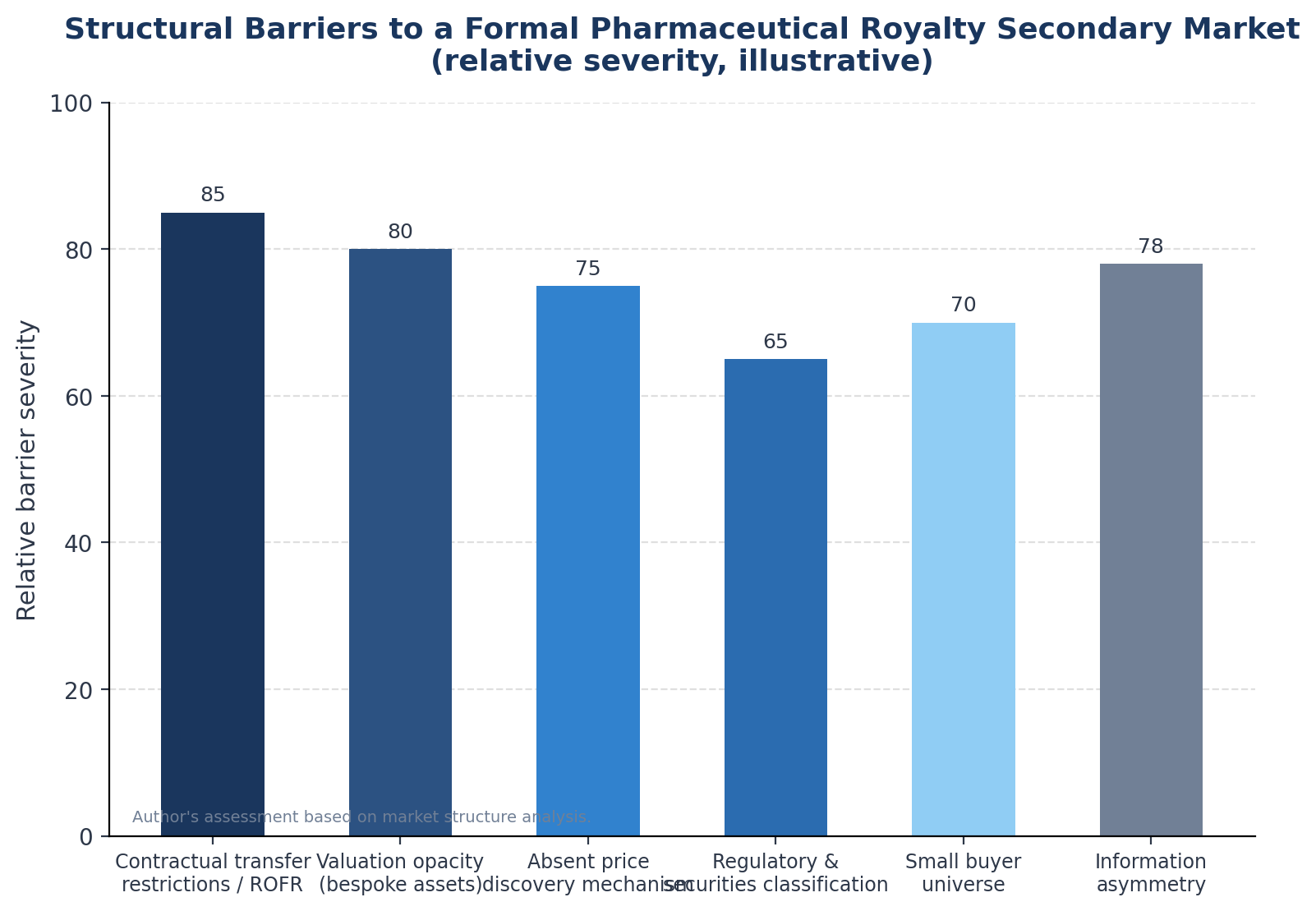

The absence of a functioning secondary market for pharmaceutical royalties is not an oversight. It reflects a combination of structural, legal, and informational barriers that reinforce each other.

Contractual Transfer Restrictions and Rights of First Refusal

The starting point for most pharmaceutical royalty agreements is a licensing agreement between a drug developer and a commercialising company, typically a large pharmaceutical firm.

These agreements routinely contain provisions restricting assignment of the royalty interest without the consent of the underlying drug company. The drug company — the entity actually paying the royalties — often has a right of first refusal on any proposed transfer, the ability to approve prospective assignees, and sometimes explicit consent rights over the categories of investors who can hold the royalty.

These provisions exist for defensible commercial reasons: a drug company has ongoing relationships with its royalty counterparties, and does not want its royalty obligations to be transferred to an activist hedge fund or a competitor. But the practical effect is to make every secondary transaction a bilateral negotiation with the drug company as a necessary participant, even when the drug company is not the buyer or seller.

The ROFR alone can add months to a secondary sale process and creates a situation in which the most natural buyer — the drug company itself, wishing to buy back its royalty obligation — is systematically advantaged over outside buyers, suppressing secondary market pricing.

In the leveraged loan market, analogous transfer restrictions — covered in detail by the LSTA's standard loan trading documentation — have been substantially standardised and their scope negotiated to allow secondary market function. The pharmaceutical royalty market has no equivalent standardisation effort underway.

Valuation Opacity and the Information Problem

Every pharmaceutical royalty is, at its core, a long-duration claim on a fraction of drug sales. Valuing that claim requires assumptions about peak sales, ramp trajectory, duration of patent exclusivity, competitive landscape, IRA pricing pressure, reimbursement dynamics, payer mix, and terminal decline. Each of those assumptions can move the NPV of a royalty by multiples.

As PwC has noted, getting to sales accounting for royalty monetisation transactions is "difficult and rarely achieved," in part because the royalty holder and the drug's commercial team have fundamentally different information sets. The commercial team at the drug company knows its current market share, its payor negotiations, its competitive intelligence on pipeline threats.

The royalty investor knows only what the drug company discloses in public filings. A secondary buyer — one degree further removed — has even less.

This information asymmetry is not merely a problem for pricing individual transactions. It makes it almost impossible to design an exchange or platform that could provide meaningful price discovery, because any price arrived at without access to drug company commercial data is systematically underinformed relative to the drug company's own view.

The Small Buyer Universe

The pharmaceutical royalty market's primary participants are a small number of dedicated funds — Royalty Pharma, HealthCare Royalty Partners, Blackstone Life Sciences, CPPIB's royalty unit, DRI Capital, Oberland Capital, and a handful of others — plus universities and research hospitals on the sell side.

The total universe of buyers capable of writing nine-figure cheques for pharmaceutical royalties, conducting the necessary diligence, and managing the ongoing monitoring obligation can be counted on two hands.

Gibson Dunn's survey methodology focuses on eight buyers because those eight represent the overwhelming majority of market activity. A secondary market requires multiple simultaneous buyers and sellers. When there are eight buyers globally, none of them competing simultaneously for the same asset in a visible auction, the conditions for price discovery simply do not exist.

Regulatory and Securities Classification Uncertainty

A pharmaceutical royalty interest is a bespoke contractual right to receive a percentage of drug sales. Its legal characterisation — as a security, a commodity, a financial instrument, or an ordinary contract — varies by jurisdiction, by deal structure, and by how the instrument was created.

In the United States, royalty interests created through licensing agreements are generally not classified as securities under the Securities Act, which means they can be transferred without registration. But synthetic royalties, milestone-contingent royalties, and royalty interests held by or transferred through investment funds may attract different treatment.

This classification ambiguity means that any platform attempting to create a secondary market for pharmaceutical royalties would face substantial regulatory uncertainty. Would listing royalty interests for trade constitute operating a securities exchange? Would aggregating royalty interests into a fund and offering participations constitute creating a security requiring registration?

These questions have not been authoritatively resolved, and the cost of resolving them through regulatory engagement is prohibitive for any entrant that does not already have significant legal resources committed to the space.

How Secondary Transactions Actually Work Today

Given all of the above, the secondary transactions that do occur follow a recognisable process that has more in common with private M&A than with securities trading.

Identification: The seller — typically a fund approaching end-of-life, a research institution with a one-off royalty, or a company wishing to monetise a royalty on its balance sheet — reaches out to a small number of known buyers. There is no formal listing process, no RFP to the market, and no broker-dealer with a position in the royalty to facilitate price discovery.

Diligence: The buyer — almost always a specialist royalty fund with in-house clinical, commercial, and financial expertise — conducts proprietary diligence.

This typically involves constructing an independent NPV model from public information (SEC filings, drug company earnings calls, analyst consensus, epidemiological data), stress-testing assumptions, and arriving at a bid price that reflects the buyer's required return on invested capital, typically in the high-single to low-double digit range for approved products as disclosed by Royalty Pharma, or teens for development-stage assets.

Counterparty Consent: Before or concurrently with price negotiation, the parties identify any consent rights held by the underlying drug company and either begin the consent process or structure the transaction to avoid triggering it (for example, through assignments to affiliates or transfers that are exempted from consent requirements under the original agreement's terms).

Negotiation and Close: Price is negotiated bilaterally. There is no competitive tension from alternative bids, no auction mechanism, and no broker making a market. The seller's leverage is primarily the threat of approaching a different buyer — a threat that is weak given the small universe of qualified buyers, most of whom know each other's return thresholds.

Disclosure: If either party is a public company, the transaction may be disclosed in a press release, often with minimal financial detail. The Royalty Pharma / Nuvalent transaction disclosed a price range of "up to $315 million" and the description "from an undisclosed third party." That is substantially the complete market information available to any outside observer.

The process described above is not a market in any meaningful sense. It is a series of private transactions conducted through a small network of parties who know each other, have broadly aligned views on valuation methodology, and have no incentive to create the transparency infrastructure that would make their informational advantages less valuable.

The Case for a Formal Secondary Market

Despite the structural barriers, there are genuine economic arguments for developing secondary market infrastructure, and the barriers are becoming progressively less theoretical as the primary market grows.

For Royalty Investors

A functioning secondary market would give royalty funds the ability to manage duration, rebalance portfolio concentration, and exit positions before end-of-fund-life without the ad hoc processes that currently make secondary exits expensive and slow. Fund managers approaching the end of their investment period currently face a binary choice: extend the fund's life, or attempt to sell royalty assets in a thin bilateral market at prices that may significantly understate NAV.

Continuous secondary market pricing would also allow mark-to-market valuations that reflect observable market prices rather than manager-constructed models — a significant benefit for institutional LPs attempting to manage their own portfolio exposures.

For Royalty Sellers (Biotechs and Universities)

For the biotech companies and research institutions that originate royalties, a functioning secondary market would increase the transparency of what their royalty interests are worth, making it easier to negotiate primary deal terms, easier to monetise partial interests without going through a full bilateral sale process, and easier to use royalty interests as collateral for other financing.

For Drug Companies

Perversely, even the drug companies paying royalties might benefit from a secondary market, because a more liquid royalty would more accurately price the option value of royalty buybacks. Companies currently face significant uncertainty when estimating the buyback premium they would need to pay to eliminate a royalty obligation. Observable secondary market prices would give them a benchmark.

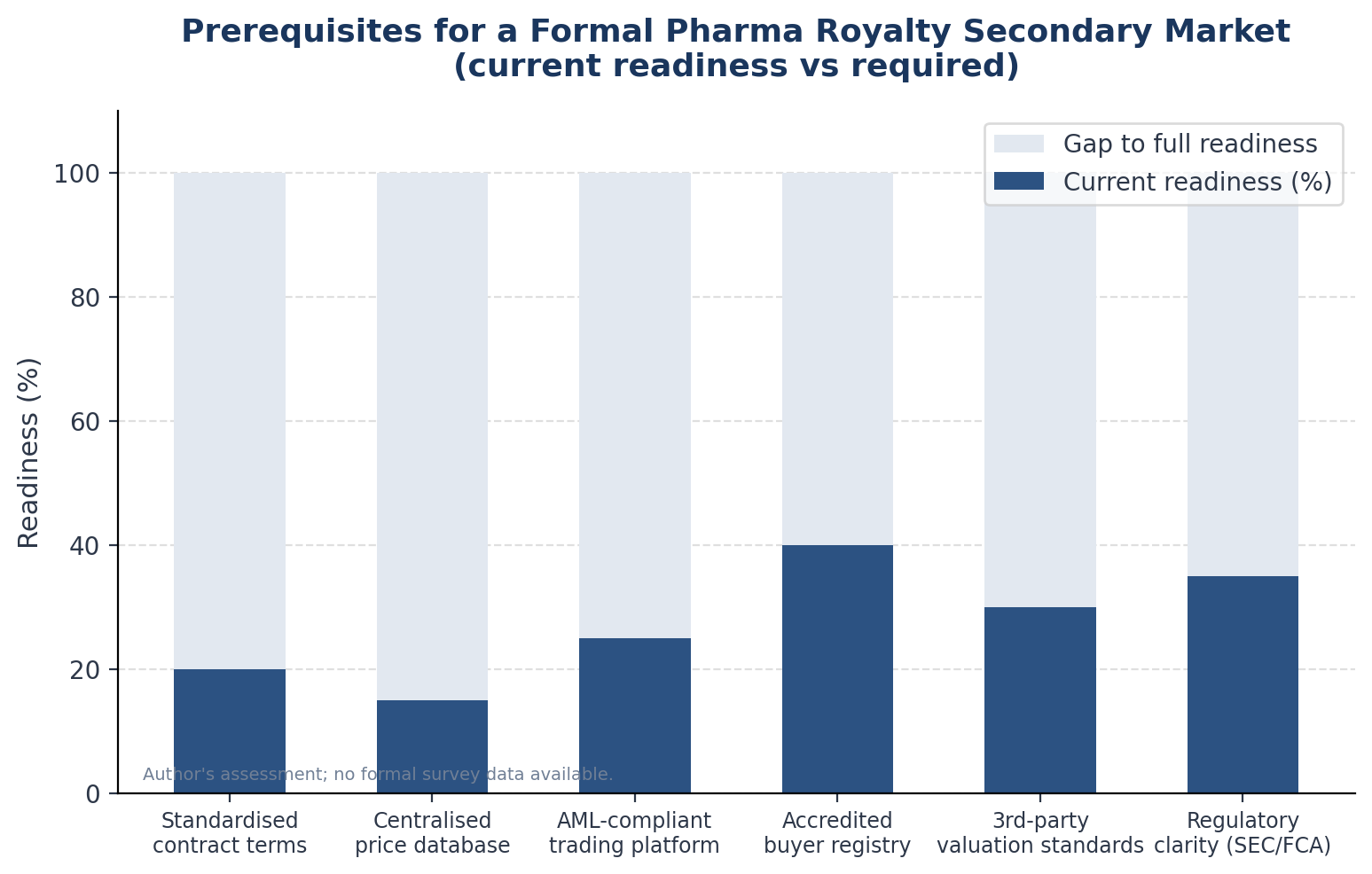

What Would Be Needed

Building a genuine secondary market for pharmaceutical royalties would require simultaneous progress on at least five fronts.

Standardised contract terms. The Loan Syndications and Trading Association transformed the leveraged loan market by developing standard documentation for secondary transfers that covered assignments, participations, consent mechanics, and settlement. A pharmaceutical royalty equivalent would need standard clauses for assignment, ROFR waivers or carve-outs, consent rights, successor-holder representations, and information-sharing obligations.

ISDA-style master agreements for royalty instruments would represent a significant step. No industry body is currently working on this.

A centralised pricing database. Price discovery requires historical transaction data. The leveraged loan market has LSTA/Reuters pricing. Private equity secondaries have Jefferies' quarterly review.

Pharmaceutical royalties have a handful of press releases with incomplete pricing data and no systematic aggregation of what those transactions imply about discount rates, risk premiums, or asset-class pricing over time.

This is the gap Capital for Cures is building to close. The platform is constructing a systematic, machine-extracted database of pharmaceutical royalty transactions drawn from SEC filings, press releases, and licensing agreements across the full spectrum of deal types: traditional royalty monetisations, synthetic royalties, milestone-linked structures, and the secondary transfers discussed in this article.

The extraction pipeline uses large language models running on dedicated inference infrastructure to process tens of thousands of SEC filings — 10-Ks, 10-Qs, 8-Ks — identifying deal terms that are frequently disclosed in embedded exhibits but never aggregated by any existing commercial data provider.

The critical edge is private company data. As senior executives from the major royalty funds confirmed at Capital for Cures' most recent network events, public asset data is already reasonably accessible through EDGAR and press releases.

The gap that no existing platform — not IQVIA, not Dealforma, not Evaluate — fills is the systematic extraction and structuring of royalty deal terms across private companies and smaller transactions that never generate analyst coverage or media attention. That private data layer is where valuation opacity is most severe, and where a centralised database would create the most immediate value for market participants attempting to benchmark a secondary transaction.

A comprehensive database of this kind — covering royalty rate, deal value, asset stage, therapeutic area, deal structure, and implied yield across thousands of transactions — would represent the first genuine input for pharmaceutical royalty price discovery. It would not immediately create a quoted spread.

But it would give buyers and sellers a shared reference point, reduce the information asymmetry that currently allows buyers to extract rents from less well-informed sellers, and eventually support the emergence of third-party valuation standards that a formal secondary market would require.

An accredited buyer registry. Most royalty agreements restrict transfers to "qualified institutional buyers" or similar designations, but the specific characteristics required of a transferee vary by agreement. An industry-standard definition of eligible royalty transferees — covering AML/KYC obligations, minimum asset size, sector expertise requirements — would reduce the legal friction in each secondary transaction from weeks of bespoke due diligence to a standard checklist.

Third-party valuation standards. Without observable market prices, royalty portfolios are valued using internal models. A standard framework for royalty valuation — akin to the IPEV guidelines for private equity — would reduce the variance between buyer and seller valuations and make it easier for neutral third parties to provide independent assessments.

The components of such a framework already exist (rNPV is the standard methodology; discount rate conventions can be derived from primary market data), but they have not been assembled into a recognised standard.

Regulatory clarity. The SEC and FCA have not definitively addressed whether platforms facilitating secondary trading in pharmaceutical royalty interests would be operating securities exchanges or trading facilities.

Obtaining no-action letters or regulatory guidance specific to royalty instruments — similar to guidance obtained by ABS platforms or alternative trading systems for private credit — would reduce the regulatory risk for any infrastructure provider. The current environment of regulatory uncertainty effectively constitutes a barrier to entry for any institutional platform developer.

Analogue Markets and Their Lessons

The markets that have successfully built secondary infrastructure for illiquid assets offer useful comparisons.

Private equity secondaries ($160B+ annually by 2024) developed over three decades. The key innovations were, in order: the emergence of dedicated secondary funds in the 1990s willing to buy LP interests at a discount; the development of Jefferies, Lazard, and other placement agents with systematic deal origination; the creation of standard LP transfer documentation; and finally the broadening of the buyer base to include retail and semi-liquid vehicles.

The pharmaceutical royalty market is at an earlier stage than private equity secondaries were in the early 1990s.

Leveraged loans became tradeable through the LSTA's standardisation effort beginning in the 1990s, which reduced settlement times from months to weeks and made bilateral dealer markets viable.

The key was that the borrower — the entity whose cash flows underlie the loans — had a commercial incentive to allow secondary trading (cheaper primary capital costs) that outweighed the costs of negotiating standardised consent procedures. In pharmaceutical royalties, the drug company has little commercial incentive to facilitate secondary trading of royalties they would prefer to buy back or extinguish.

Catastrophe bonds offer a different model: an entirely standardised instrument, defined by ISDA-like terms, with objective trigger criteria and independent third-party risk assessment (by firms like AIR Worldwide), that trades in a liquid OTC market within months of issuance. The standardisation that made catastrophe bonds liquid was designed in from the beginning by issuers and investors with aligned interests in creating market efficiency. Pharmaceutical royalties were not designed for secondary trading.

The Path Forward: Incremental vs Transformative

Two distinct models for developing secondary market infrastructure in pharmaceutical royalties are conceivable.

The incremental model — more likely and already visible in nascent form — involves the current primary market buyers gradually building secondary trading capabilities alongside their primary deal origination. Royalty Pharma's willingness to acquire pre-existing royalties from undisclosed third parties at market prices is already a form of de facto market making: the firm functions as a buyer of last resort for sellers who can find no other counterparty.

As the primary market grows and fund-of-funds structures emerge, the volume of secondary transactions will increase organically, eventually generating enough data to support a pricing database.

The transformative model would involve deliberate infrastructure construction: a trade association (perhaps AUTM or a life sciences finance lobby group) sponsoring standard documentation; a specialist data platform investing in a centralised royalty transaction database; a regulatory engagement process to clarify securities status; and a platform connecting buyers and sellers with pre-screened accreditation.

This model would accelerate development by decades but would require coordinated action from parties — drug companies, royalty funds, regulators — who have different and sometimes conflicting interests. Capital for Cures is operating in this space: building the data infrastructure layer — systematic deal extraction, valuation benchmarking, and transaction intelligence — that functions as the prerequisite for any future trading or matching platform. The Bloomberg Terminal analogy is apt: Bloomberg did not create liquidity in bond markets; it made existing liquidity visible, measurable, and actionable. The pharmaceutical royalty market needs that layer before it can have the next one.

The more likely near-term path is a continuation of the incremental model, with growing transaction volume in bilateral OTC secondary sales, gradually improving price transparency as more transactions are disclosed, and eventual emergence of specialist secondary advisors (analogous to Lazard or Jefferies in private equity secondaries) who can run structured processes for sellers with significant royalty portfolios.

As the Gibson Dunn 2026 outlook for royalty finance notes, aggregate transaction value reached approximately $6.5 billion in 2025, up from approximately $5.7 billion in 2024, with participation from traditional private equity deepening further. As those private equity participants approach end-of-fund-life over the next five to ten years, secondary sale pressure will increase substantially.

Implications for Primary Market Participants

The absence of secondary market liquidity has a direct effect on primary market pricing that is rarely made explicit. When a royalty investor prices a new transaction, they apply an illiquidity premium that compensates them for the probability that they will hold the asset to maturity — typically ten to fifteen years — with no meaningful ability to exit early at a fair price.

That illiquidity premium is embedded in the discount rate applied to projected cash flows, and it represents a real cost of capital for the biotech companies selling royalties.

If secondary market infrastructure were to develop, lowering the illiquidity premium by even 200-300 basis points, the cost of royalty capital for biotech companies would fall meaningfully. A royalty that currently prices at an 11-12% implied IRR (typical for approved products, per Royalty Pharma's disclosed return targets) might price at 8-9% in a world with functioning secondary market infrastructure, with substantial consequences for deal economics.

The development of secondary market infrastructure is therefore not just a capital markets abstraction — it directly determines how much non-dilutive capital is available to the biopharmaceutical ecosystem, and at what price.

Conclusion

The pharmaceutical royalty market crossed $10 billion in annual transaction volume in 2025. It has at least three dozen dedicated institutional investors, hundreds of corporate and academic sellers, and a track record of providing non-dilutive capital that has made it a mainstream instrument in the CFO's toolkit.

What it does not have is a secondary market in any meaningful sense: no quoted bid-ask spreads, no centralised price discovery, no standardised transfer documentation, and no infrastructure for buyers and sellers to find each other without bilateral negotiation through a small network of known counterparties.

The secondary transactions that do occur — Royalty Pharma acquiring pre-existing royalties from undisclosed third parties, fund managers monetising portfolio positions at end-of-life, original licensors selling rights to specialist funds — are conducted in a manner that would be familiar to anyone who has done a private M&A deal, not anyone who has traded a financial instrument on an exchange or even in a dealer market.

The five barriers to change — contractual transfer restrictions, valuation opacity, the small buyer universe, regulatory uncertainty, and the absence of standardised documentation — are significant but not insurmountable. The private equity secondaries market faced analogous barriers three decades ago and built through them.

The question is whether the pharmaceutical royalty market will build that infrastructure organically over the next twenty years, or whether deliberate intervention — by trade associations, regulators, or infrastructure investors — can compress the timeline.

The data layer has to come first. Before a market can price royalties, it needs to know what royalties have historically traded for, what their structural terms looked like, and how implied yields have moved across therapeutic areas and asset stages.

That is the infrastructure Capital for Cures is building: a systematic, AI-powered database of pharmaceutical royalty transactions extracted from thousands of SEC filings and licensing agreements, covering deal terms that have never been aggregated in a single platform. It is not a secondary exchange. It is the precondition for one — and in a market this opaque, building the data foundation is itself a material contribution to eventual price discovery.

For now, the market's version of a bid-ask spread remains the gap between a seller's internal NPV model and the offer they receive from one of eight qualified buyers, negotiated in private over several months, and disclosed in a press release that omits the seller's identity. That is not a market. It is the precondition for one.

All information in this report was accurate as of the research date and is derived from publicly available sources including company press releases, SEC filings, regulatory announcements, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. Sebastian Gensior is not a lawyer or financial adviser.

Member discussion