Step-up Provisions in Pharmaceutical Royalty Financings

When Savara sold a royalty on MOLBREEVI to RTW funds in late 2025, the deal included a clause that most observers would have overlooked: if prior-year net sales fell short of a specified threshold, the investor's royalty would jump from 7.0% to 9.5% for the following calendar year. The company did not disclose what that threshold was. But the mechanism itself, a "step-up," is fast becoming one of the defining structural features of modern pharmaceutical royalty financings.

A step-up is a contractually defined, contingent increase in one or more economics that drive the investor's realised return. Most commonly this means the royalty rate. But step-ups can also apply to the cap or return multiple, the termination or buy-out amount, a minimum payment floor, or the investor's share in a waterfall. In market practice, step-ups are used to re-price risk after the fact, when observable outcomes deviate from the underwriting case. A slower-than-expected launch ramp, missed sales thresholds, regulatory timing slippage, or a delayed change of control can all trigger them. The logic is simple: deals can clear pricing today while reserving a pre-agreed mechanism to compensate the investor if performance underwhelms.

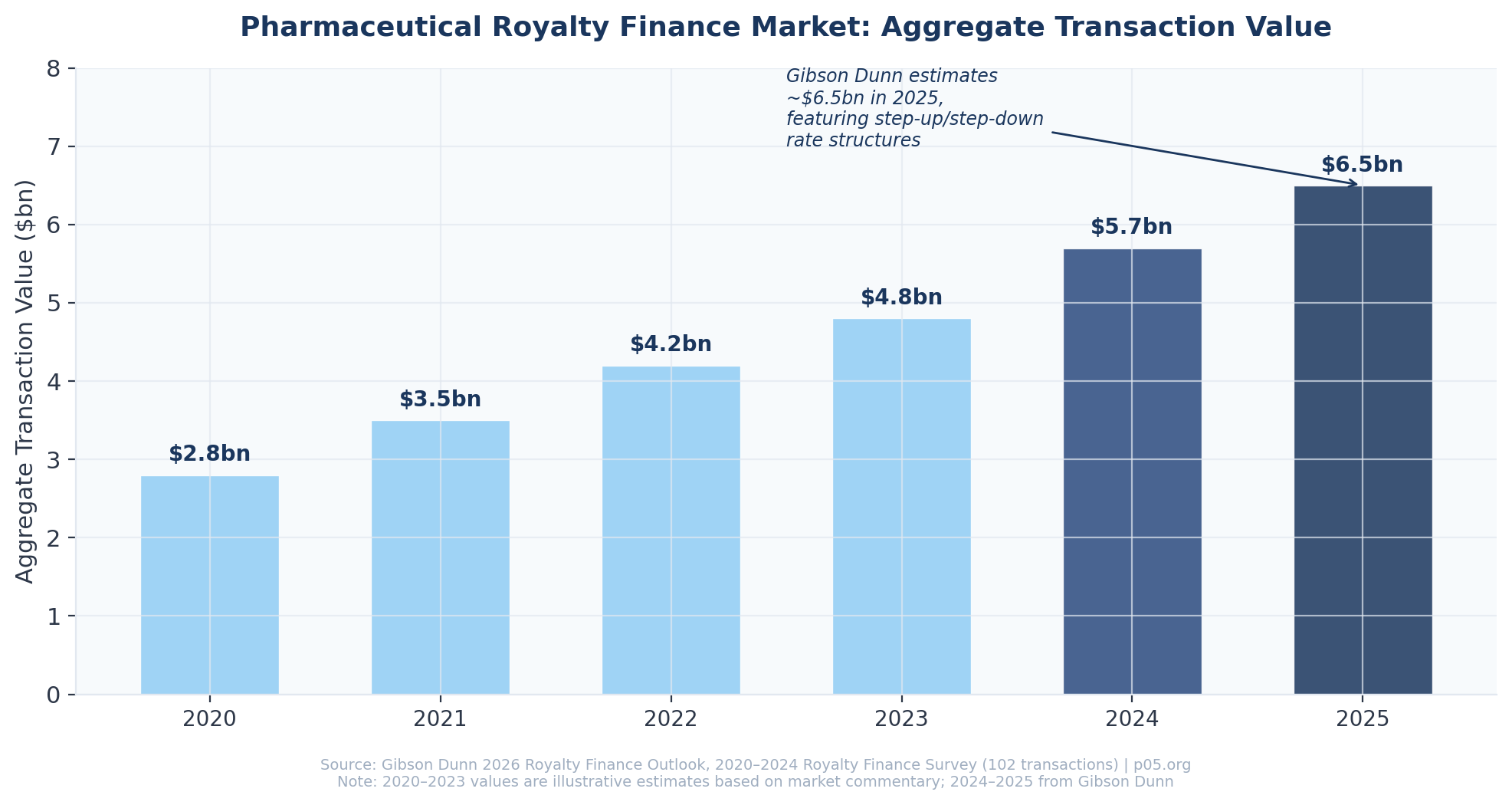

Gibson Dunn estimates that aggregate royalty finance transaction value across leading participants rose to roughly $6.5 billion in 2025, up from approximately $5.7 billion in 2024, and explicitly observes that many of the year's deals featured step-down or step-up royalty rates among other innovative structural features. Its 2020–2024 royalty finance survey of 102 publicly announced transactions reports expanding use of synthetic royalties and milestone-linked structures, as well as frequent inclusion of product liens and non-incurrence covenants in synthetic financings. A Deloitte royalty market study reported that 87% of surveyed biopharma executives expect to incorporate royalty financing into their capital-raising strategies over the next three years. Royalty Pharma alone deployed $2.6 billion on royalty transactions in 2025, with up to $4.7 billion in announced transactions including its landmark $2 billion funding arrangement with Revolution Medicines.

This market structure is naturally conducive to step-ups. When financings are non-recourse to a single asset or a narrow basket and covenant-heavy, step-ups provide an additional contractual tool to preserve investor returns without requiring renegotiation. Gibson Dunn highlights a particularly creative 2025 transaction: XOMA Royalty Corporation's strategic royalty share agreement with Takeda, under which Takeda's royalty and milestone payment obligations related to Mezagitamab were reduced while XOMA received royalty and milestone payments across a basket of nine development-stage assets from Takeda's externalized portfolio. In parallel, hybrid financing structures that blend traditional royalty economics with elements of term debt or structured credit are becoming increasingly prevalent, incorporating caps on total returns, milestones, debt-like covenants, or make-whole payments at a maturity date.

Recent SEC filings reveal at least six distinct step-up archetypes operating in practice. This article examines each, explains the economic logic, analyses the clause architecture and trigger design, and works through a quantitative model showing how step-ups affect investor returns.

The six archetypes

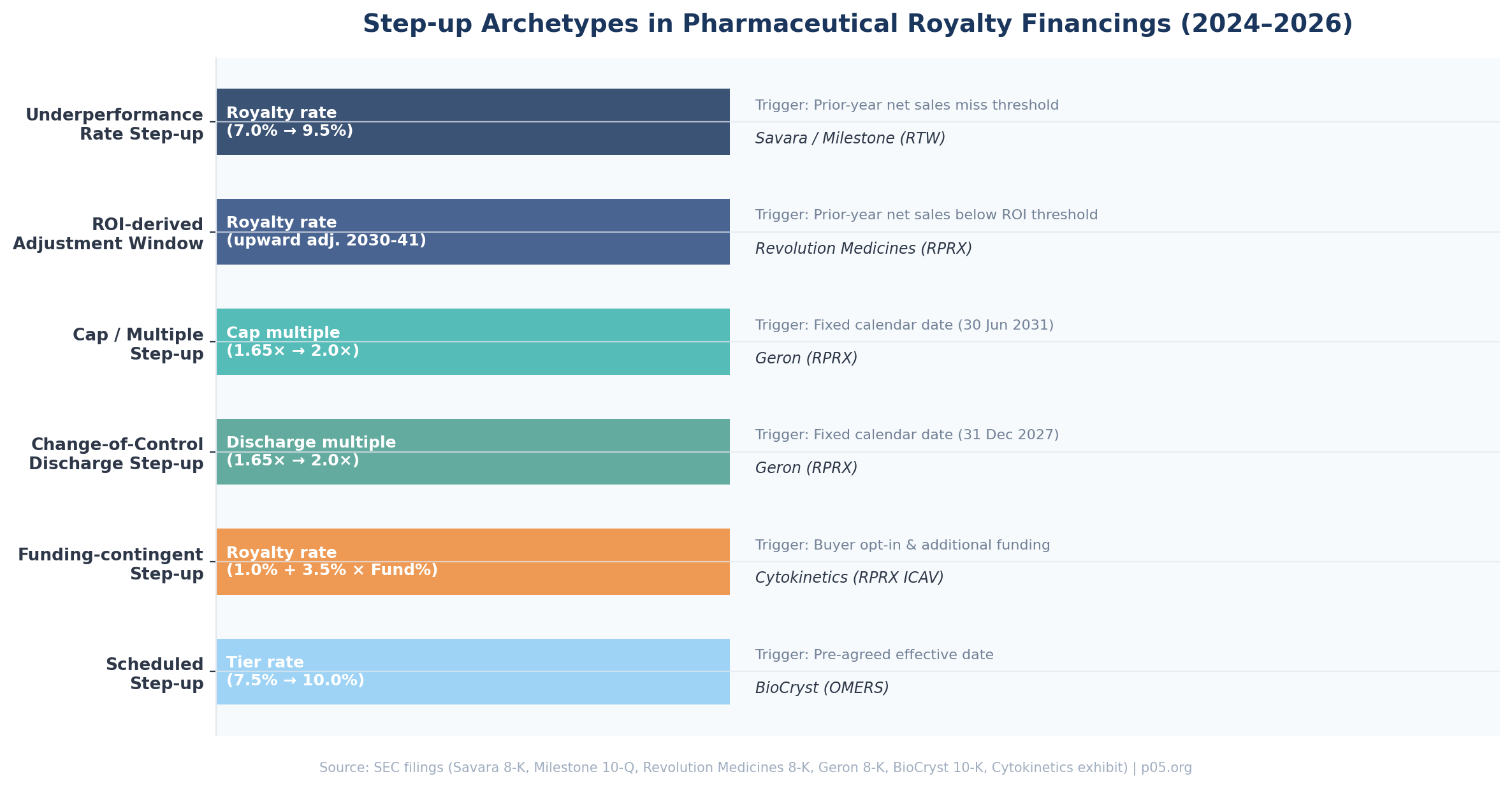

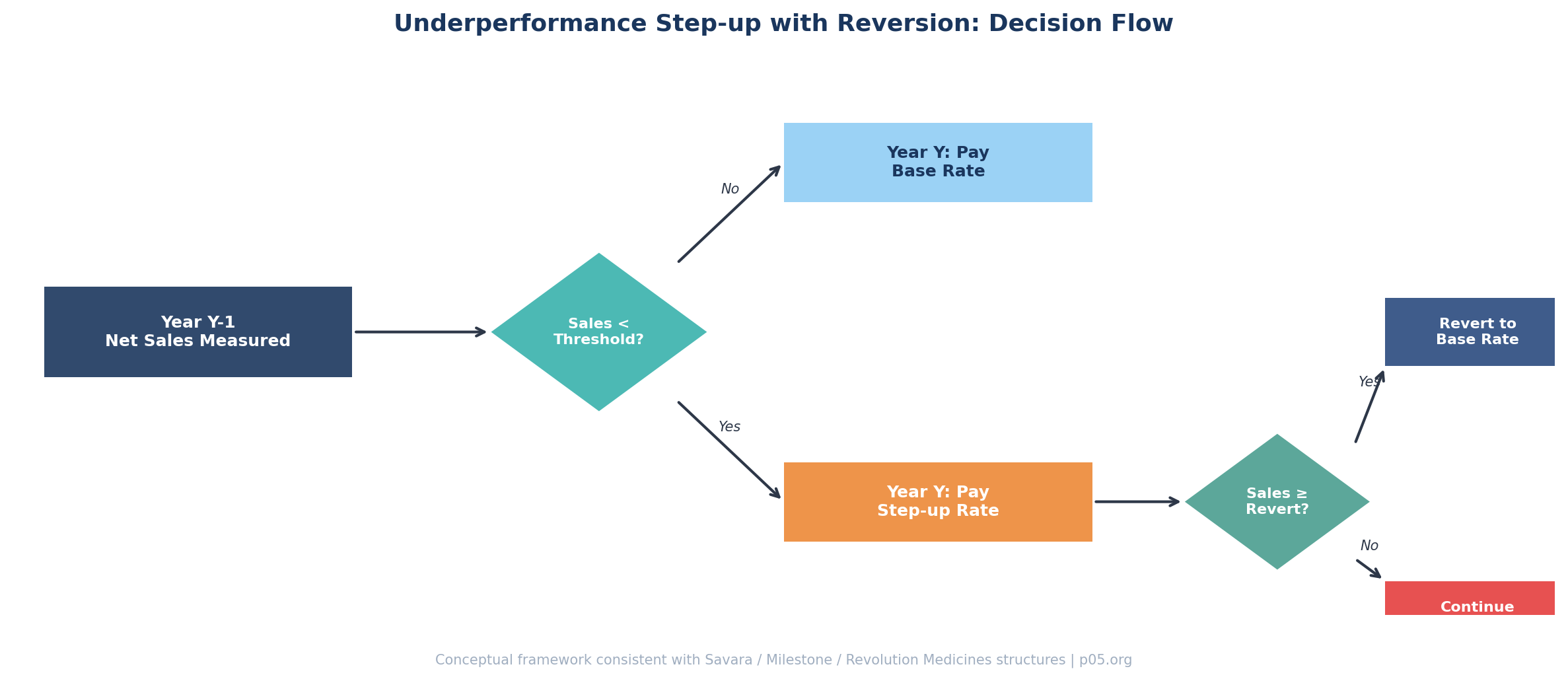

Underperformance rate step-up with reversion

The most common variant. Savara's 2025 RTW royalty sale discloses that a 7.0% tier can increase to 9.5% for a calendar year if the prior year's net sales do not achieve a specified level. A structurally similar feature appears in Milestone Pharmaceuticals' RTW deal: if certain annual net sales thresholds are not met, the "Initial Tier Royalty" increases to 9.5% and then reverts once a later threshold is achieved. In both cases, the step-up is temporary, contingent on underperformance, and designed to revert when the product returns to its expected trajectory.

ROI-derived "upward adjustment" window

Revolution Medicines' 2025 Royalty Pharma transaction takes a different approach. It provides for an upward adjustment to royalty payment rates from 2030 to 2041 if annual net sales in the immediately prior year are below an agreed-upon threshold. The adjustment reverts if annual net sales exceed a different threshold. What distinguishes this structure is that the company explicitly states the threshold was "derived from return-on-investment calculations." The trigger is calibrated not as a commercial key performance indicator but as an ROI stabiliser for the investor.

Time-based cap and buy-out multiple step-up

Rather than raising the royalty rate, Geron's 2024 Royalty Pharma agreement caps payments at 1.65 times the purchase price if that amount is achieved by 30 June 2031, but allows payments to continue up to 2.0 times thereafter. The same agreement steps up the change-of-control discharge multiple from 1.65 times to 2.0 times after 31 December 2027. This is economically equivalent to a step-up in the investor's make-whole if the company is sold after more time risk and opportunity cost have accrued.

Funding-contingent step-up

Cytokinetics' CK-586 revenue participation agreement defines a product royalty rate that starts at 1.00%. If the buyer exercises an opt-in and funds additional development, the rate becomes 1.00% plus 3.50% multiplied by the Funding Percentage, where that percentage is defined as additional investment payments divided by $150 million. The economic logic is that the buyer receives higher participation only if it funds more of the development budget. This is development-linked "pay more, get more" economics. The agreement is governed by New York law, a common choice for these financings.

Scheduled step-up at a fixed effective date

BioCryst's OMERS royalty purchase agreement discloses that OMERS' tiered royalty on ORLADEYO direct sales changed beginning 1 January 2024, increasing the first tier from 7.5% to 10.0% and adjusting the second tier from 6.0% to 3.0%. This is not contingent in the strictest sense but requires careful modelling of effective dates, measurement windows, and partial-year proration. Scheduled step-ups are common in synthetic or semi-synthetic structures as back-end return accelerators.

What step-ups are doing economically

Across these archetypes, step-ups are tools for intertemporal risk transfer. Three functions stand out.

First, they shift launch-ramp downside from the investor to the originator by increasing the investor's share when sales are weak. The Savara, Milestone, and Revolution Medicines structures all do this explicitly.

Second, they protect the investor's ability to reach a target return multiple or internal rate of return within a bounded time horizon. This can be accomplished either by increasing the rate (which accelerates cashflow) or by increasing the cap (which extends the tail). Geron's deal demonstrates both levers.

Third, they create pre-agreed, contractual path-dependent convexity. If sales are strong, the step-up may never be triggered, or may revert, leaving the originator with more residual value. If sales underperform, the investor's economics improve automatically. Neither party needs to renegotiate.

In formal terms, the base cashflow mapping in a royalty financing is:

Royalty Payment = Royalty Rate × Royalty Base (Net Sales)

A step-up mechanism changes the royalty rate, the royalty base, or the termination condition as a function of a trigger event. Most commonly:

- If trigger is not satisfied → base rate applies (e.g. 5.0%)

- If trigger is satisfied → step-up rate applies (e.g. 7.0%)

with reversion logic determining whether the step-up persists for one period, until a reversion threshold is crossed, or permanently.

Clause architecture and drafting variants

Step-up economics are only as reliable as their drafting. For royalty-finance specialists, the core design problem is to create a clause that is machine-calculable, auditable, bankruptcy-resilient, and compatible with other deal documents including credit agreements, intercreditors, securitisations, and licence agreements.

Drafting primitives

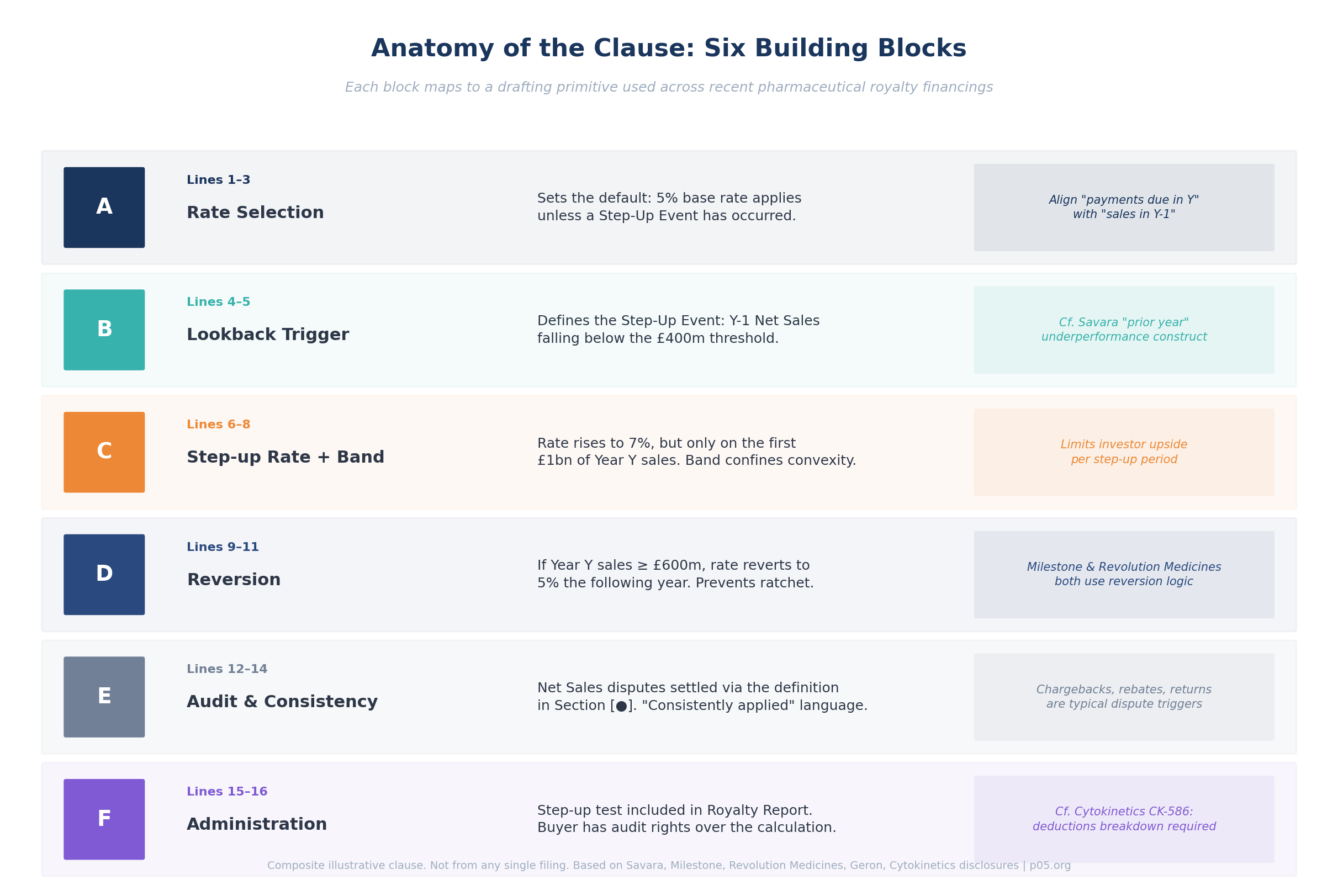

Most step-up clauses are constructed from a small number of building blocks.

State variable definition determines what is measured: annual net sales, cumulative net sales, cumulative receipts, regulatory status, time from first commercial sale, and so on.

Observation window determines when it is measured: prior calendar year, trailing twelve months, cumulative from launch, or another period.

Trigger test sets the threshold and comparator: "if less than X," "if equal to or greater than X," or "if not achieved by date D."

Economic switch determines what changes: the rate, cap, floor, or termination payment.

Reversion or reset determines how long the change lasts: for one period only, until crossing a reversion threshold, or permanently.

Anti-gaming and administration provisions address reporting, audits, dispute resolution, treatment of restatements and chargebacks, late payments, and offsets.

Cytokinetics' CK-586 agreement illustrates how these primitives are embedded in definitional architecture. The "Product Royalty Rate" definition houses multiple states (pre-opt-in, post-opt-in) and uses the defined Funding Percentage, itself formula-based, as the scaling variable.

Common legal drafting variants

Definition-level rate tables versus operative covenants. A frequent pattern is to embed step-ups inside the definition of "Royalty Rate," "Product Royalty Rate," or "Applicable Percentage" rather than in an operative clause. This reduces interpretive ambiguity and allows the calculation to be a matter of applying definitions. Cytokinetics uses this approach: the Product Royalty Rate is defined as 1.00% initially, becoming 1.00% plus 3.50% multiplied by Funding Percentage after opt-in.

Single-period versus multi-period applicability. Savara describes a mechanism where the 7.0% tier increases for a single calendar year if the prior year misses a level. Revolution Medicines describes adjustments in a specific future window (2030 to 2041) tied to the immediate prior year, with upward adjustments that can later revert. These are different persistence choices with different path dependency.

Rate step-up versus cap step-up. Geron's transaction shows a pure cap-multiple step-up: cease at 1.65 times if achieved by a date, otherwise cease at 2.0 times thereafter. This avoids altering the royalty rate itself but extends duration and increases total possible receipts.

Step-up with explicit reversion thresholds. Reversion is critical to prevent step-up economics from becoming a one-way ratchet. Milestone's agreement states that the initial tier royalty increases to 9.5% until a later threshold is attained, at which point it reverts to 7%. Revolution Medicines similarly states upward adjustments revert if annual net sales exceed a different threshold.

Step-up embedded in change-of-control economics. Change-of-control provisions often combine a buy-back option with a variable discharge amount. Geron's buy-out payment definition steps up from 1.65 times to 2.0 times after a specified date.

Sample step-up clause (illustrative)

The sample below is not copied from any filing. It is a composite drafting pattern reflecting common structures disclosed in recent transactions.

Trigger design in practice

Step-ups must be triggered by events that are objectively verifiable, hard to manipulate, and timely enough to protect the investor while not unduly penalising the originator.

Sales and revenue thresholds

Prior-period sales tests (miss triggers). Savara's disclosure is a canonical example: a tier of 7.0% increases to 9.5% for a year if the prior year's net sales do not meet a specified level. Milestone discloses an analogous "miss then step-up until later threshold" mechanism.

Prior-period sales tests (ROI-derived thresholds, with reversion). Revolution Medicines explicitly states that its adjustment threshold was derived from return-on-investment calculations, and that the upward adjustment applies only to one tier and stays in the single digits. This framing is important: the threshold may be set not as a commercial KPI but as an ROI stabiliser.

Time-based triggers

Time-based step-up of cap or multiple. Geron's deal uses a time cut-off: the cap is 1.65 times if achieved by a date, otherwise it becomes 2.0 times. This is a straightforward way to compensate investors for time value if sales ramp slower than projected, without changing the rate structure.

Scheduled effective date step-ups. BioCryst discloses a change effective 1 January 2024 to OMERS' tiered royalty rates on direct sales. While not contingent in the strictest sense, scheduled step-ups are common in synthetic or semi-synthetic structures to create a back-end return accelerator.

Regulatory events and clinical milestones

In pharmaceutical royalty financings, step-ups are often keyed to development or approval events, especially for pre-approval assets. The Cytokinetics collaboration illustrates several milestone-conditioned economics, including expansion funding and post-approval payments and royalties in certain scenarios. A particularly important variant is funding-contingent step-up tied to clinical progression: the CK-586 product royalty rate steps up when the buyer opts in and funds additional development.

Change-of-control triggers and corporate events

Change-of-control triggers are used to prevent leakage of value to sellers or acquirers while the investor is under-returned, and to handle diligence and assignment issues of the underlying royalty streams.

Geron's change-of-control discharge amount steps up after 31 December 2027 from a 1.65 times to a 2.0 times basis. Savara discloses a buy-back option tied to certain changes of control within two years of receiving the purchase price.

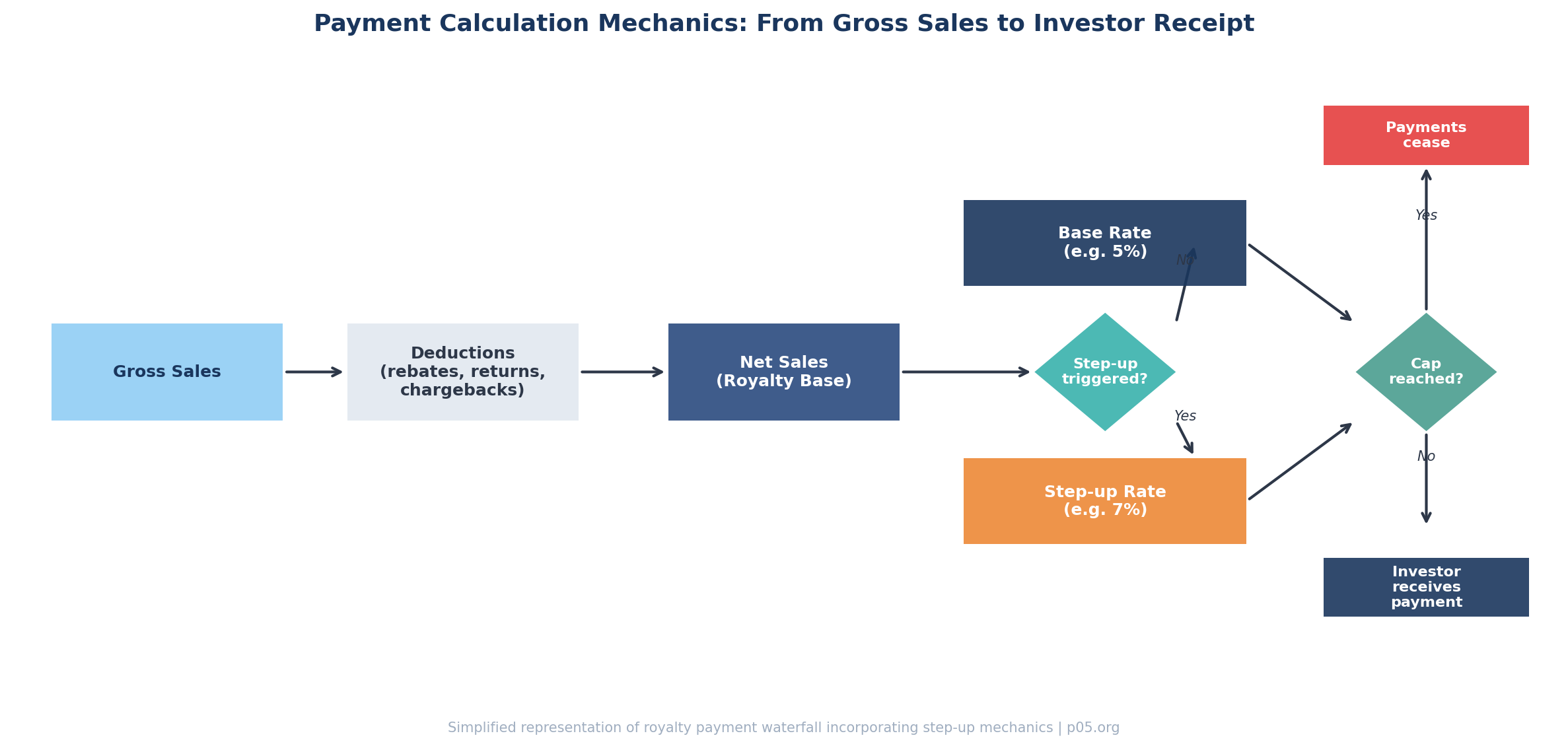

Payment calculation mechanics and waterfall interactions

For specialists, the practical difficulty of step-ups is rarely the concept. It is the calculation base, the measurement window, and their interaction with caps, floors, and other deal features.

Net Sales versus gross sales, and why step-ups amplify definitional risk

In most synthetic royalty financings, the payment base is Net Sales or "Annual Net Sales." Step-up provisions increase the multiplication factor on Net Sales, which makes Net Sales definitional disputes more valuable in underperformance scenarios (when the step-up is active) and therefore more likely.

Cytokinetics' CK-586 agreement illustrates how deals operationalise this. The seller must deliver a royalty report including units, gross sales, and a breakdown of all permitted deductions from gross sales used to determine net sales and the royalty payment. However, the publicly filed exhibit shows that the Net Sales definition itself is redacted. This is common in SEC exhibits for competitive reasons. It also means external analysts often cannot fully reconstruct what counts as net sales without confidential schedules.

Step-up interactions with caps, floors, and effective rate reporting

Caps and multiples. Step-ups can accelerate reaching a cap (rate step-up) or extend total receipts (cap step-up). Geron's structure is explicit: payments cease at 1.65 times if achieved by a date, otherwise 2.0 times thereafter. The cap itself is a state variable that can be stepped up.

Floors. While floors are not always disclosed in short-form descriptions, Cytokinetics' 2024 development funding loan scenario illustrates minimum floor payment concepts (floor amounts in early quarters) in a related structured funding arrangement, demonstrating how floors are used to guarantee a minimum cash return in certain windows.

Effective rate disclosure. Savara notes that although headline tiers range from 7.0% to 1.0% (with a 9.5% step-up possibility), the company expects the effective royalty rate over the life of the agreement to be low single digits. For modelling, specialists should reconcile disclosed tiers with the cap, expected sales trajectory, and potential step-up activation frequency.

Lookbacks, true-ups, and clawbacks

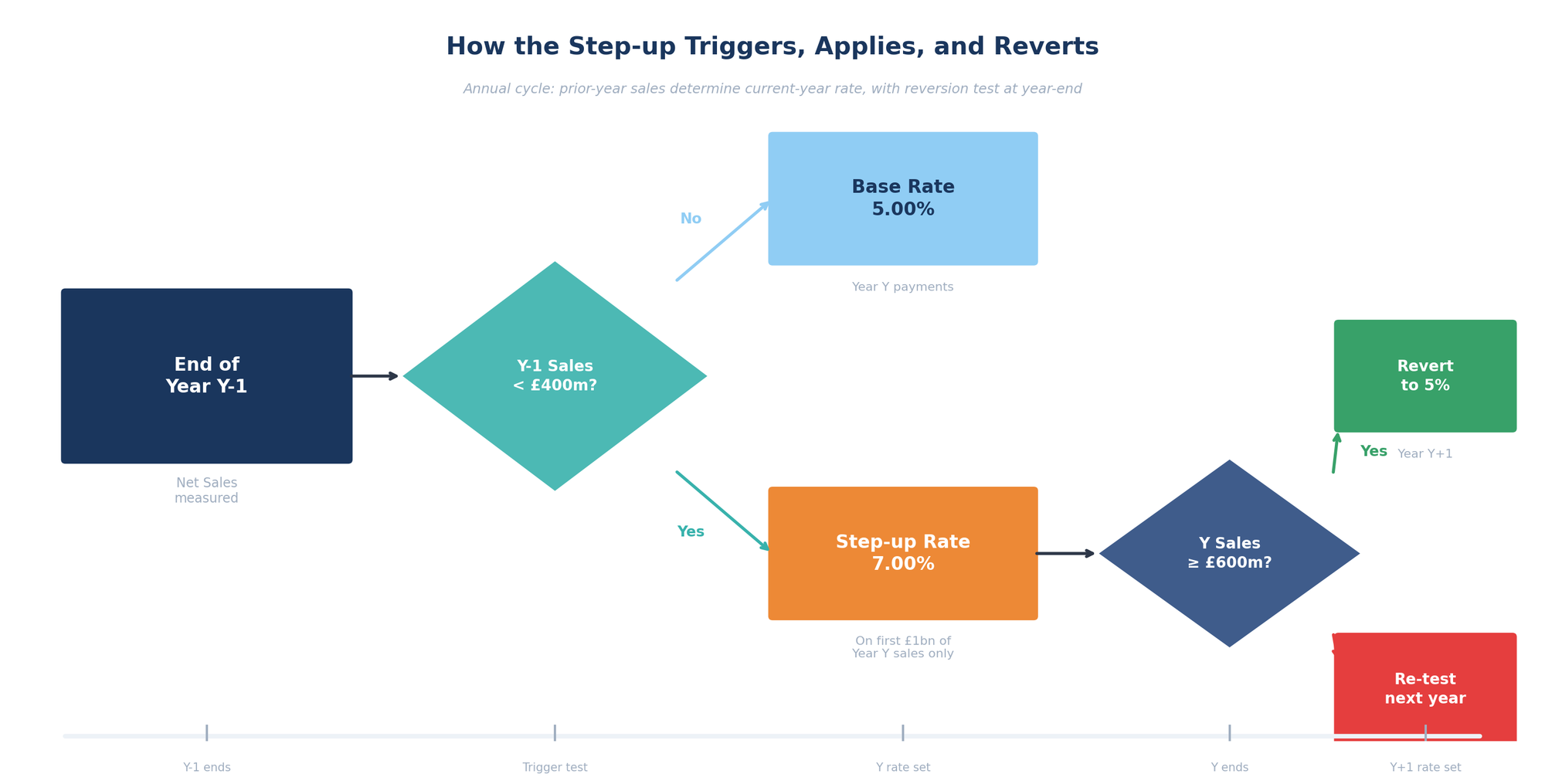

Step-ups commonly depend on prior-period performance, with sales in year Y-1 determining the rate in year Y. This creates three technical issues.

Restatements and commercial adjustments (rebates, chargebacks, returns) may be finalised after the measurement period, requiring true-up protocols. Audit rights must be aligned to step-up disputes, or the step-up becomes litigable rather than calculable. Clawbacks may be required if a step-up was applied based on preliminary data and later data indicates the threshold was actually met.

While specific clawback language is often redacted, the CK-586 agreement's reporting and audit framework, plus interest on certain overdue amounts, shows the administrative scaffolding typically used to manage these risks.

Waterfall complexity with hybrid capital stacks

Step-ups must be analysed at two levels: the royalty calculation level (how much is owed in a period) and the cash waterfall level (who receives what cash when multiple claims exist).

The CK-586 agreement contains language contemplating proceeds waterfalls in scenarios where senior lenders have liens on certain product assets, with a formula based on the then-applicable Product Royalty Rate relative to other sold revenue interests. This illustrates how step-ups can change intercreditor economics: if the product royalty rate increases, the relative sharing formula can change as well.

Accounting, tax, and disclosure implications

Step-ups can materially affect both classification and measurement. They change expected cashflow timing and amounts, which feed effective interest rates and fair value estimation.

Accounting treatment under US GAAP

Liability treatment with effective interest method. BioCryst records consideration received under its royalty purchase agreements as "royalty financing obligations" on the balance sheet and imputes interest expense using the effective interest method. It reassesses expected royalty payments each reporting period and adjusts the effective interest rate prospectively. BioCryst further discloses that fair value and carrying value are measured using Level 3 estimates of future payments, using a prospective method for changes in estimates.

Geron similarly discloses that it accounted for its Royalty Pharma agreement as a financing liability because of "significant continuing involvement" in generating the future revenue on which royalty payments are based, and measures the liability and interest expense based on current estimates of expected future payments.

Why step-ups matter for accounting. Step-ups increase the dispersion of potential cashflows and can cause periodic re-estimation to swing effective interest rates. BioCryst's disclosure highlights that changes in projected net product sales impact both the amount and timing of expected royalty payments and can lead to prospective adjustments of amortisation and effective interest. Step-ups that activate on underperformance, precisely when forecasts are being revised downward, can partially offset declines in expected receipts, making the effective interest recalibration less severe. But they also increase model complexity.

Disclosure and SEC exhibit redactions

A recurring practical limitation in 2024 to 2026 primary sources is that key economic definitions are partially redacted. The CK-586 exhibit displays the Net Sales definition as redacted content. Revolution Medicines discloses the existence of thresholds and their conceptual derivation from ROI calculations but does not disclose the numeric thresholds. Savara discloses the step-up to 9.5% but not the specified level of net sales that triggers it. Specialists should therefore treat some public-market modelling as structural rather than fully parametric unless confidential schedules are accessible.

Tax consequences and characterisation risk

Royalty financing contracts often articulate intended tax treatment, particularly where the parties want sale treatment rather than indebtedness.

Cytokinetics' CK-586 revenue participation right purchase agreement includes an explicit "Tax and Accounting Treatment" clause stating that the parties agree to treat the transaction as a contractual sale arrangement, not indebtedness, and to treat purchase price and royalty payments as taxable transactions (and not a partnership). It also includes withholding mechanics tied to delivery of IRS forms such as W-8BEN-E.

From a tax perspective, step-ups can be relevant because they change the expected payments profile. If a transaction were recharacterised as debt, stepped economics may resemble contingent interest or original issue discount features. Even where the parties' agreement controls their reporting position, step-ups increase the need for consistent tax positions across the originator, the royalty SPV or fund, and any securitisation noteholders.

Deal summary table: step-ups in practice (2024–2026)

| Company (counterparty) | Investor / buyer | Asset | Step-up mechanic | Trigger type |

|---|---|---|---|---|

| Savara (SVRA) | RTW funds | MOLBREEVI (molgramostim) U.S. Net Sales royalty | Initial tier increases: 7.0% → 9.5% for a calendar year | Underperformance: prior-year Net Sales below a specified level (level not disclosed); described as "true sale" with cap ($187.5m) |

| Milestone Pharmaceuticals (MIST) | RTW | Etripamil U.S. annual net sales royalty | Initial Tier Royalty increases: 7% → 9.5%; reverts to 7% later | Underperformance: if certain annual net sales thresholds not met; step-up applies until subsequent threshold attained (thresholds not disclosed) |

| Revolution Medicines (RVMD) | Royalty Pharma | RMC-6236 / RMC-9805 worldwide Net Sales tiers | Upward adjustment to royalty rates (limited to $0–$2bn tier) during 2030–2041; reverts | Underperformance / ROI-derived: prior-year Annual Net Sales below threshold; thresholds not disclosed; adjustment "derived from ROI calculations" |

| Geron (GERN) | Royalty Pharma Development Funding | RYTELO U.S. net sales revenue interest | Cap multiple steps up: cease at 1.65× if achieved by 30 Jun 2031, otherwise 2.0× thereafter; change-of-control discharge multiple steps up after 31 Dec 2027 | Time-based: crossing fixed calendar dates changes the cap / discharge multiple; includes tiered rates (7.75% / 3% / 1%) |

| BioCryst (BCRX) | OMERS (affiliate) | ORLADEYO direct sales royalties | Scheduled rate change: on 1 Jan 2024, tiered direct sales royalty changes (first tier 7.5% → 10.0%) | Time-based step-up effective date embedded in agreement; payments cease at a defined aggregate multiple of purchase price (155%) |

| Cytokinetics (CYTK) | Royalty Pharma Investments 2019 ICAV | CK-586 worldwide Net Sales revenue participation | Funding-contingent step-up: Product Royalty Rate = 1.00%, then (after opt-in) 1.00% + (3.50% × Funding Percentage) | Trigger is buyer's opt-in / additional investment payments (Funding Percentage = additional payments / $150m); governed by New York law |

Worked modelling example with step-up and sensitivity

This worked example is illustrative but calibrated to step-up patterns seen in filings: an underperformance lookback step-up with reversion logic and a cap multiple where the step-up accelerates reaching the cap, similar in spirit to the capped and reversion structures described by Savara and Milestone.

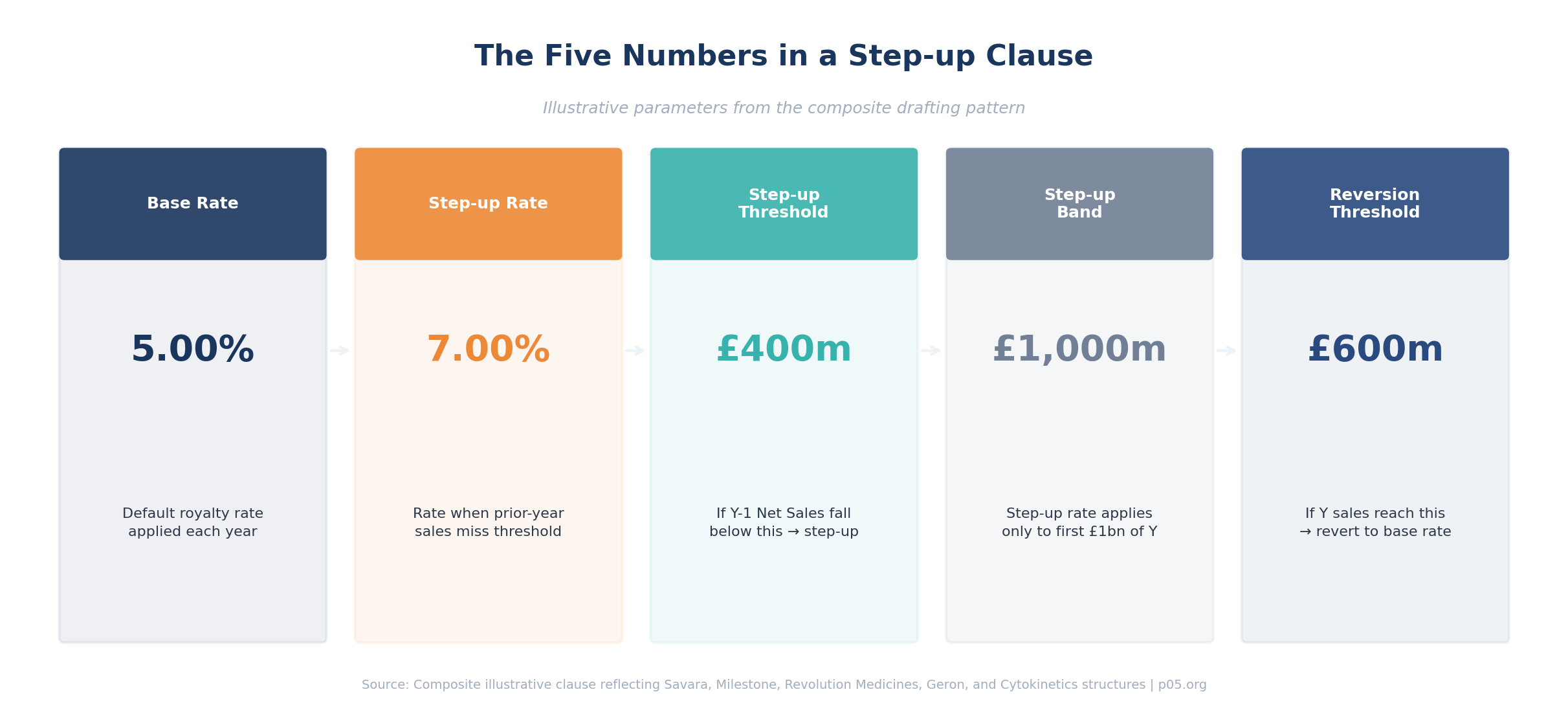

Assumptions (investor view)

The upfront purchase price is £150 million. The cap allows the investor to receive up to £255 million total (a 1.7 times multiple, consistent with capped structures used in practice). The base royalty rate is 5.0% of annual net sales. The step-up rate is 7.0% of annual net sales in any year where prior-year net sales were below £400 million. The rate reverts when sales are above the threshold in the prior year.

The assumed net sales trajectory (in £ millions) is: 150, 250, 350, 450, 550, 650, 650, 550, 450, 350, 250, 200, 150, 100, 50.

Cashflows with step-up (cap at £255m)

| Year | Net sales (£m) | Applicable rate | Royalty paid (£m) | Cumulative paid (£m) |

|---|---|---|---|---|

| 1 | 150 | 5.0% | 7.5 | 7.5 |

| 2 | 250 | 7.0% | 17.5 | 25.0 |

| 3 | 350 | 7.0% | 24.5 | 49.5 |

| 4 | 450 | 7.0% | 31.5 | 81.0 |

| 5 | 550 | 5.0% | 27.5 | 108.5 |

| 6 | 650 | 5.0% | 32.5 | 141.0 |

| 7 | 650 | 5.0% | 32.5 | 173.5 |

| 8 | 550 | 5.0% | 27.5 | 201.0 |

| 9 | 450 | 5.0% | 22.5 | 223.5 |

| 10 | 350 | 5.0% | 17.5 | 241.0 |

| 11 | 250 | 7.0% | 14.0 (truncated to cap) | 255.0 |

| 12–15 | — | — | 0.0 | 255.0 |

Results

With the step-up, the investor's annual IRR (based on end-of-year receipts) is approximately 9.64%, and the cap is reached in Year 11.

Without the step-up, applying a flat 5.0% rate under the same cap and sales path, the investor's IRR falls to approximately 8.49%, and the cap is not reached until Year 14.

The step-up improves IRR by roughly 115 basis points and shortens expected duration by approximately three years. This is precisely the economic purpose of underperformance step-ups described in recent deals: compensate the investor for a slower ramp by increasing participation when sales are weak, yet allow reversion once sales recover.

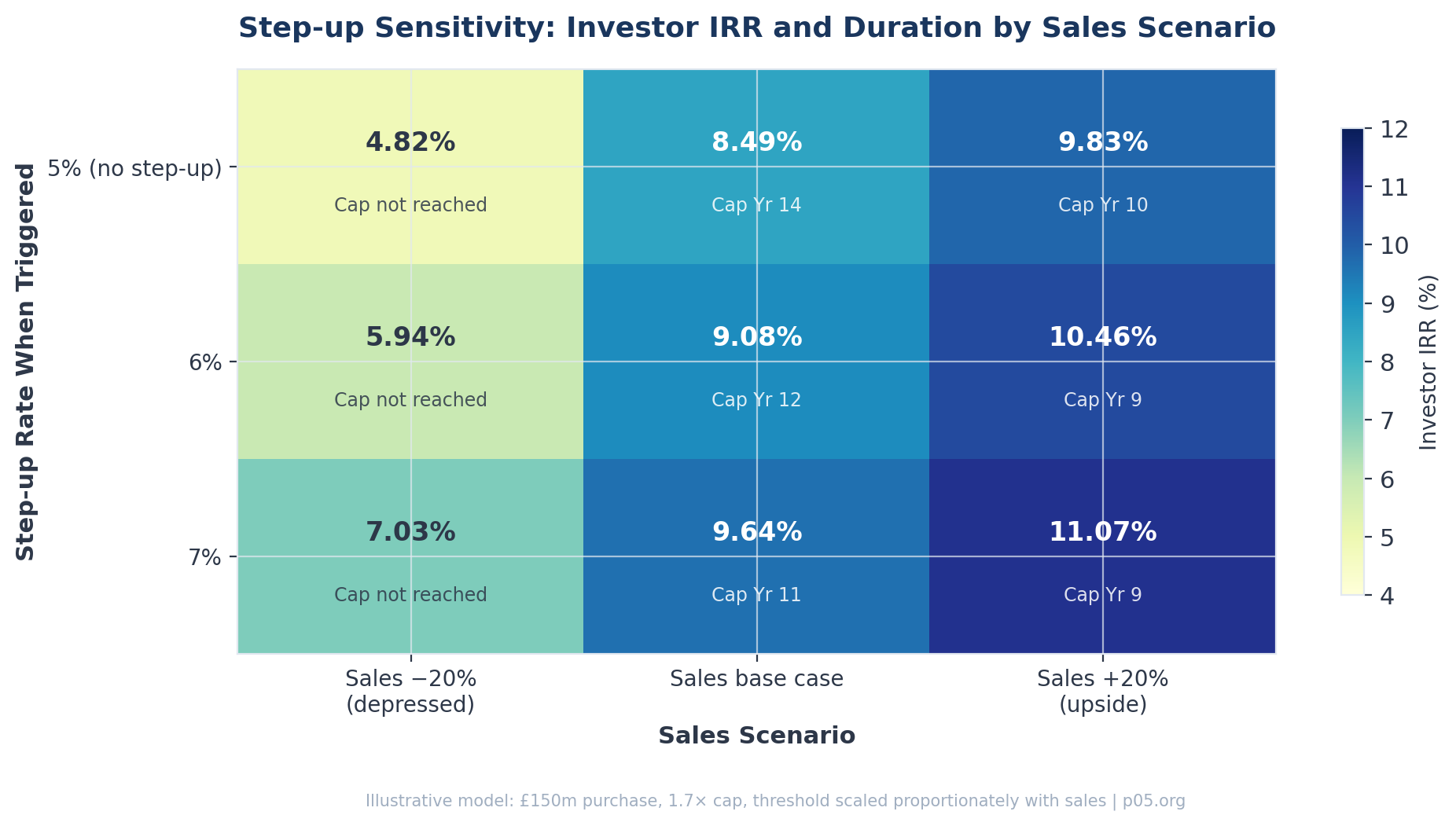

Sensitivity analysis

The table below varies the sales level by plus or minus 20% (with the threshold scaled proportionately to preserve commercial meaning) and the step-up rate between 5% (no step-up), 6%, and 7%.

| Step-up rate when triggered | Sales −20% | Sales base | Sales +20% |

|---|---|---|---|

| 5% (no step-up) | IRR 4.82%; cap not reached by Year 15 | IRR 8.49%; cap Year 14 | IRR 9.83%; cap Year 10 |

| 6% | IRR 5.94%; cap not reached by Year 15 | IRR 9.08%; cap Year 12 | IRR 10.46%; cap Year 9 |

| 7% | IRR 7.03%; cap not reached by Year 15 | IRR 9.64%; cap Year 11 | IRR 11.07%; cap Year 9 |

Two points are worth emphasising.

Step-ups are most valuable in the "marginal" region where the base case nearly reaches the cap but slower sales threaten duration. In these scenarios, step-ups can restore duration and IRR without renegotiation. This is the zone where they most efficiently fulfil their economic function.

Step-ups may not rescue deep downside. If sales are sufficiently depressed, even an aggressive step-up might not reach the cap within a typical projection horizon. This is why some deals combine step-up rates with cap step-ups, floors, or change-of-control make-wholes. Geron's time-based multiple step-up is an example of combining the cap lever with the rate lever.

All information in this article is derived from publicly available sources including SEC filings, regulatory announcements, and industry reports. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.

Several 2024 to 2026 filings identify step-up mechanics but do not provide full quantitative parameters. The specific net sales thresholds in Savara, Milestone, and Revolution Medicines are not disclosed. The Net Sales definition in Cytokinetics' CK-586 exhibit is redacted. Where those data are unavailable in primary sources, any external model should be treated as a scenario framework rather than a single-point estimate.

Member discussion