The Overriding Royalty Interest in Pharmaceutical Royalty Financing

The overriding royalty interest has been a standard instrument in oil and gas financing for over a century. It has funded drilling programmes, compensated geologists, settled disputes, and structured billions of dollars in production payment transactions across North American mineral properties. It has also generated a substantial body of case law — particularly around bankruptcy characterisation — that remains almost entirely unknown to the pharmaceutical royalty market.

This article examines the ORRI in detail: what it is, how it works mechanically, how courts have treated it, and how its structure compares to the instruments currently used in pharmaceutical royalty financing. It then asks a question that, as far as I can determine, has not been seriously explored in the life sciences financing literature: could the ORRI concept be adapted for pharmaceutical transactions, and if so, what would that look like?

Definition and Legal Nature

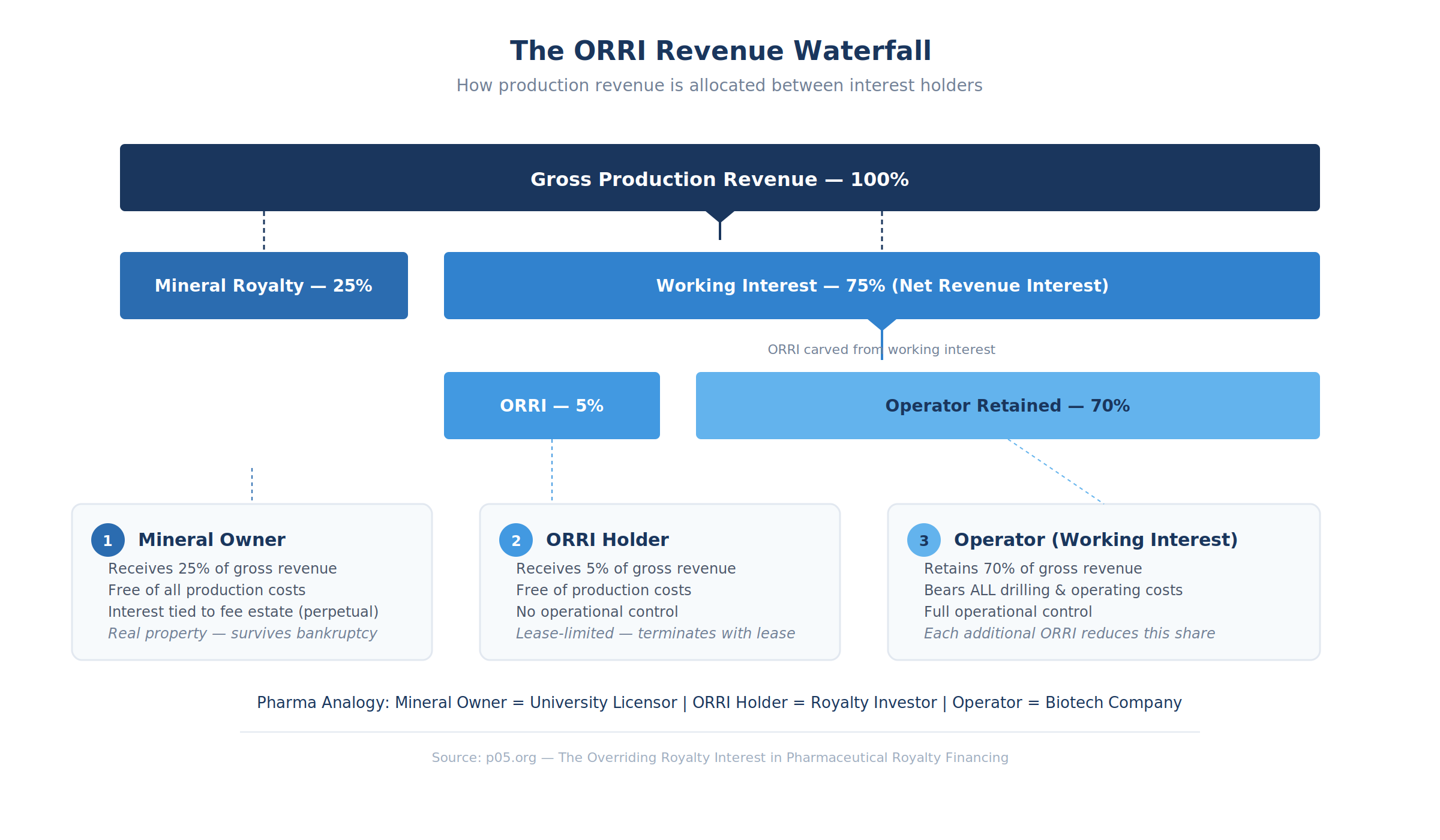

An overriding royalty interest (ORRI) is a fractional, undivided interest in the gross production revenue from a mineral property, carved out of the lessee's working interest rather than from the mineral estate itself. The holder receives a stated percentage of production proceeds — free and clear of drilling, completion, and operating costs — for as long as the underlying lease remains in force. When the lease terminates, the ORRI terminates with it.

Several elements of this definition are worth unpacking.

Carved from the working interest, not the mineral estate. The ORRI does not convey ownership of the underlying resource. It is a right to a share of proceeds, not a right to a share of production in situ. The mineral owner retains their royalty interest. The working interest holder (typically the operator or E&P company) bears all costs and retains operational control. The ORRI holder sits between them: entitled to revenue, carrying no cost burden, exercising no operational authority.

Non-possessory and non-operating. The ORRI holder has no right to participate in decisions regarding development, drilling schedules, well spacing, production rates, or abandonment. As the Akers Law Firm analysis puts it, an overriding royalty interest is "a nonpossessory interest" that gives the owner "no right, absent an agreement to the contrary, to participate in decisions with regard to the development and operation of the burdened lease."

Lease-limited duration. Unlike a mineral royalty interest — which attaches to the fee estate and endures in perpetuity — the ORRI is coterminous with the lease from which it was carved. If the lease expires, is released, or is terminated for non-production, the ORRI ceases to exist. The holder's economic interest reverts to zero regardless of remaining resource potential.

How ORRIs Are Created

ORRIs are typically created through one of three mechanisms, each carrying distinct legal and tax consequences.

Reservation in a lease assignment. When an oil and gas company assigns its leasehold working interest to another party, it may reserve an ORRI in the assignment instrument. The assignor retains a revenue participation without retaining any operating obligation. In a well-documented example from the Delta Petroleum bankruptcy, Whiting granted BWAB "an overriding royalty consisting of an undivided 3.5% interest in Whiting's Net Revenue Interest from the Subject Properties." A subsequent conveyance to Delta Petroleum included a 1% ORRI reserved for the company's CEO. Neither was recorded in real property records due to concerns about co-tenant objections — a decision that created significant complications when Delta later filed for Chapter 11.

Grant as compensation. Geologists, landmen, petroleum engineers, and attorneys who contribute to assembling or evaluating a prospect are frequently compensated with ORRIs carved from the working interest. The ORRI functions as deferred compensation tied to production success — no production, no payment. As Blue Mesa Minerals notes, "a landman may agree to acquire leases for XYZ Oil and Gas Company in exchange for 50% cash and 50% ORRI on future wells drilled on a specific tract of lands."

Conveyance as a financing mechanism. E&P companies use ORRIs to raise capital without incurring debt or diluting equity. An investor provides cash in exchange for a carved-out percentage of future production revenue. A 2011 SEC filing by GMX Resources documented a term overriding royalty interest conveyance in which the working interest owner warranted title and assigned a specified percentage of crude oil production to the royalty owner, complete with division order mechanics, audit rights, and protective mortgage provisions. SandRidge Permian Trust's ORRI conveyances, also filed with the SEC, show how term and perpetual ORRIs can be layered alongside net profits interests in a single transaction — illustrating the kind of multi-instrument financing structure that pharmaceutical deal architects are only beginning to explore.

The ORRI Calculation

The arithmetic is straightforward. An ORRI is calculated as:

ORRI Value = ORRI Rate × Working Interest × Mineral Interest × Tract Participation Factor

Consider a simplified example. A landowner owns 100% of the mineral rights on a tract and leases them to an operator, reserving a 25% royalty. The operator's net revenue interest is 75%. The operator then grants a 5% ORRI to a geologist. The revenue allocation becomes: landowner receives 25%, geologist receives 5%, operator retains 70%. All three interests sum to 100% of production revenue.

The calculation looks simple, but in practice it becomes complex quickly. Multiple ORRIs can be stacked on a single lease. Proportionate reduction clauses can reduce the ORRI if the operator does not control 100% of the working interest. And post-production cost allocation — whether the ORRI holder bears a share of gathering, processing, and transportation expenses — has been one of the most litigated issues in oil and gas law, with treatment varying by state and by the specific language of the conveyance instrument.

Term ORRIs vs. Perpetual ORRIs

ORRIs come in two fundamentally different forms, and the distinction between them carries legal consequences that extend well beyond the oil and gas context.

A perpetual ORRI pays a fixed percentage of production for the life of the lease. There is no cap, no target return, and no reversion. The holder's economics are entirely tied to production volume and commodity prices. If the well produces for fifty years, the ORRI pays for fifty years.

A term ORRI (or dollar-denominated production payment) provides the holder with a stated dollar amount, paid from a percentage of production, after which the interest reverts to the grantor. As Mayer Brown described in their analysis, "dollar-denominated, or volumetric production, payments generally provide for the reversion to the grantor of the interest conveyed, upon receipt by the purchaser of an amount equal to the specified sum advanced by the purchaser along with, typically, an additional amount such that the total amount received produces a targeted internal rate of return."

This is a critical distinction. The perpetual ORRI is an economic interest in the property. The term production payment is, for federal tax purposes, treated as a loan. Under IRC § 636(a), "a production payment carved out of mineral property shall be treated, for purposes of this subtitle, as if it were a mortgage loan on the property, and shall not qualify as an economic interest in the mineral property." Congress added Section 636 through the Tax Reform Act of 1969 specifically to shut down ABC transaction abuses where borrowers in retained production payments were effectively repaying loans with pre-tax dollars.

Bankruptcy Treatment: The Central Legal Question

The characterisation of an ORRI in bankruptcy is the highest-stakes legal question in ORRI transactional practice.

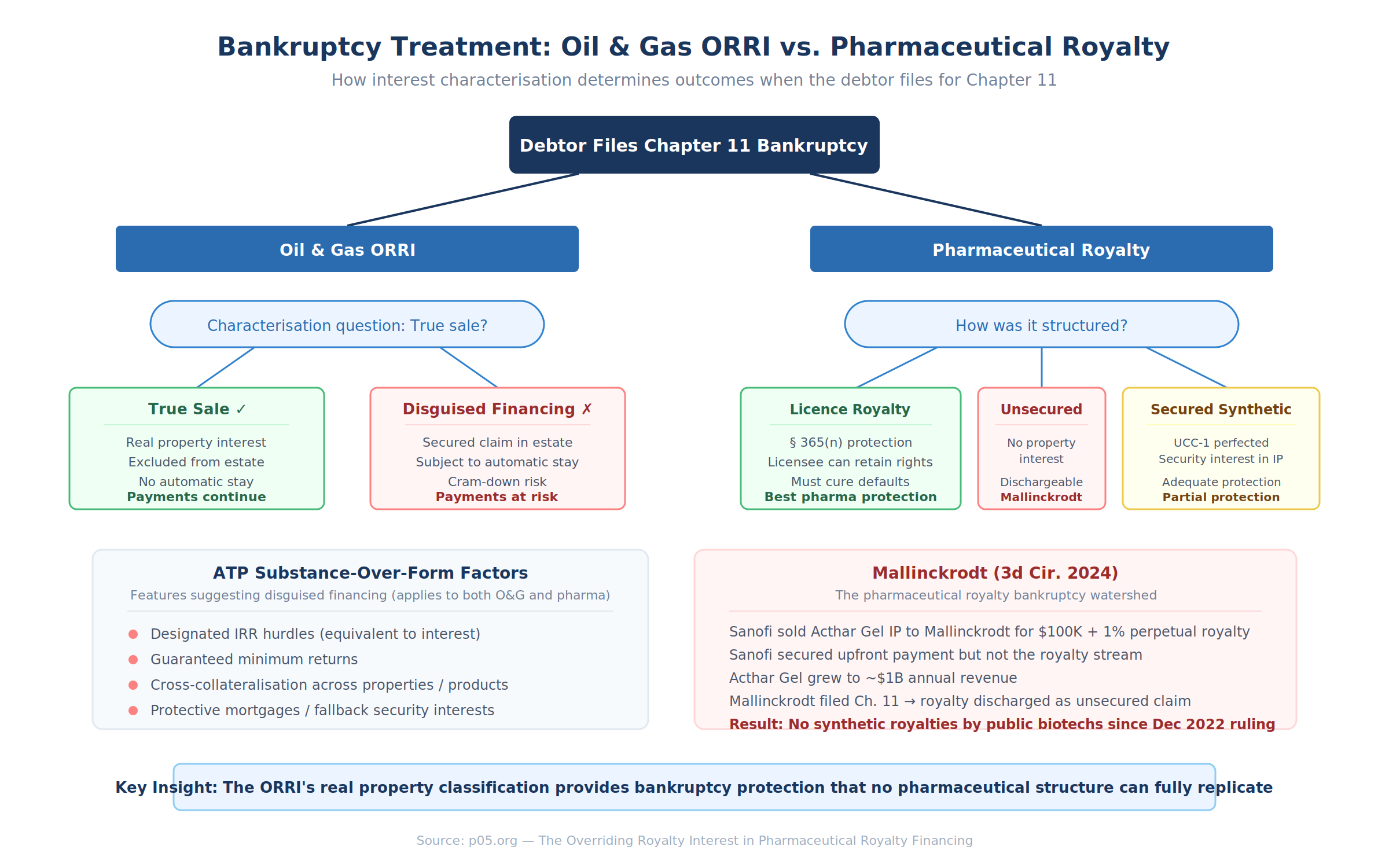

True Sale vs. Secured Financing

If an ORRI constitutes an absolute conveyance of a real property interest — a "true sale" — the interest is excluded from the debtor's bankruptcy estate. The ORRI holder continues receiving production payments regardless of the bankruptcy proceeding. The automatic stay does not apply. The interest is not property of the estate.

If the ORRI is recharacterised as a secured financing — collateral securing a loan rather than a conveyance of a property interest — the interest falls into the bankruptcy estate and is subject to the automatic stay. The ORRI holder becomes a secured creditor standing in line with other claimants.

ATP Oil & Gas: The Watershed Case

The In re ATP Oil & Gas Corp. litigation in the Southern District of Texas fundamentally changed the risk calculus for ORRI investors. ATP had entered into numerous production payment transactions involving properties on the Outer Continental Shelf, transferring term ORRIs to investors in exchange for cash. When ATP filed for bankruptcy, ORRI holders argued their interests constituted real property excluded from the estate.

Judge Marvin Isgur denied summary judgment, applying a substance-over-form analysis. He cited the Louisiana Supreme Court's holding in Howard Trucking Co. v. Stassi that the best evidence of the parties' intent is "what the parties agreed to do" — the economic substance, not the legal label. The court identified several features suggesting disguised financing:

The transactions included designated IRR hurdles payable on top of the purchase price — analytically equivalent to interest on a loan. In certain instances, ATP guaranteed that buyers would achieve their designated returns. Some transactions provided for conditional increases in royalty percentages if ATP missed development milestones. Cross-collateralisation provisions entitled buyers to receive payments across multiple leases even where one lease ceased production. And protective mortgages would take effect if a court found the interests did not constitute real property — a provision that itself suggested the parties doubted the real property characterisation.

As Mayer Brown concluded, "capital providers that are considering entering into term ORRI transactions must take into consideration the possibility that the interest they acquire may be similarly treated in the event of the bankruptcy of the lessee."

Mallinckrodt: The Pharmaceutical Mirror Image

The pharmaceutical market has its own watershed bankruptcy case, and it illustrates precisely the problem that the ORRI's real property classification is designed to solve.

In In re Mallinckrodt PLC, the Third Circuit affirmed that Sanofi's perpetual 1% royalty on Acthar Gel — owed under a 2001 asset purchase agreement — was a dischargeable unsecured claim. Sanofi had sold the Acthar Gel intellectual property outright to Mallinckrodt for $100,000 upfront plus the perpetual royalty. Critically, Sanofi took a security interest in the IP to secure the $100,000 payment but not the royalty stream. When Mallinckrodt filed for Chapter 11 nearly twenty years later, with Acthar Gel generating close to $1 billion in annual sales, the court held that the royalty obligation could be discharged. Mallinckrodt could continue selling the drug without paying Sanofi anything.

The Third Circuit's reasoning was stark: Sanofi "kept no property or security interest in Acthar Gel, but only a contractual right to a royalty. Because that contingent claim arose before Mallinckrodt went bankrupt, it is dischargeable in bankruptcy." The court noted explicitly that Sanofi could have structured the deal differently — licensing rather than selling the IP, taking a security interest to secure the royalty, or forming a joint venture to retain ownership.

Covington's post-Mallinckrodt analysis noted that "no unsecured synthetic royalty financings by public biotech companies have hit the market since the Mallinckrodt district court decision came down in December 2022." The case effectively demonstrated that an unsecured pharmaceutical royalty — the contractual right to receive a percentage of future revenue — is among the weakest forms of creditor protection available.

Here is where the ORRI comparison becomes instructive. In oil and gas, a properly structured perpetual ORRI — conveyed as a real property interest, recorded in county records, characterised as an absolute conveyance rather than a security interest — sits outside the bankruptcy estate entirely. The ORRI holder is not a creditor. The holder is a property owner whose interest is not subject to the automatic stay, not dischargeable, and not within the jurisdiction of the bankruptcy court. The Mallinckrodt outcome — a royalty holder left with pennies on the dollar after the debtor's plan discharged its claim — could not happen to a properly structured ORRI holder in an oil and gas bankruptcy (though the ATP case shows that the characterisation is not always straightforward).

The pharmaceutical market cannot replicate this protection because IP is personal property, not real property. But the Mallinckrodt case demonstrates how much is at stake in the characterisation question, and why the ORRI case law — particularly the ATP factors courts use to distinguish true conveyances from disguised financings — deserves close attention from pharmaceutical royalty practitioners.

Property Classification and Perfection

In most U.S. jurisdictions, perpetual ORRIs are classified as interests in real property. Revenue Ruling 72-117 confirmed that an overriding royalty carved out of a lease is real property for federal tax purposes. This classification means ORRIs are perfected through recording in county real property records, qualify for Section 1031 like-kind exchanges, and — critically — are generally excluded from the bankruptcy estate as absolutely conveyed property interests.

An ORRI that is properly recorded runs with the land. It binds all subsequent holders of the burdened working interest. No UCC filing is required.

The tax treatment is also distinctive. ORRI holders qualify for percentage depletion — a statutory deduction of 15% of gross income from the property for oil and gas, available even in excess of the holder's adjusted basis. Under IRC § 1.614-1(a)(2), ORRIs are classified as "economic interests" in mineral property alongside working interests and royalty interests. However, as HoganTaylor documented, the tax treatment varies significantly depending on how the ORRI was created. ORRIs received as compensation for services may be subject to self-employment tax. ORRIs reserved upon lease assignment are treated as sub-leases rather than sales, preventing the assignor from immediately offsetting income against leasehold costs.

The Protective Provisions

ORRI holders in oil and gas have, through decades of litigation, developed a set of contractual protections that address the inherent vulnerabilities of non-operating interests.

Anti-washout clauses. Without contractual protection, an operator can allow a lease burdened by an ORRI to expire, then take a new lease on the same property free and clear of the override. Courts have repeatedly addressed this scenario. The Akers Law Firm analysis recounts "thousands of sad stories of landmen and geologists who assigned a lease to an operator in exchange for an overriding royalty interest, then watched helplessly as their lease expired, without any effort on the part of the operator to develop it, only to discover that the operator had taken a new lease from the same lessor, covering the same lands, but free and clear of their overriding royalty interest." Anti-washout provisions prevent this by requiring that any new lease on the same lands remain burdened by the original ORRI.

Continuous development obligations. ORRI agreements may require the operator to maintain minimum drilling activity, ensuring the lease is held by production and the ORRI continues to generate revenue.

Consent-to-assignment provisions. Restrictions on the operator's ability to assign the burdened lease without the ORRI holder's consent, preventing dilution of the revenue base through farm-out transactions to operators with less incentive to develop.

Post-production cost allocation. Whether ORRI holders bear their proportionate share of gathering, processing, transportation, and compression costs is determined by the conveyance language. The default rule in most jurisdictions is that overrides are free of production costs but may bear post-production expenses — though the distinction between "production" and "post-production" costs has generated extensive litigation.

The Royalty Stack Problem

In oil and gas, stacking ORRIs on a single lease creates a straightforward economic problem. If the mineral owner retains a 25% royalty and the working interest holder carves out cumulative ORRIs of 10%, the operator's net revenue interest drops to 65%. Each additional override reduces the operator's economic incentive to invest in the property.

CelforPharma's analysis of the pharmaceutical royalty stack describes an identical dynamic. A company that in-licences a compound from a university, pays royalties to a technology platform provider, compensates a contract manufacturer with a revenue share, and out-licences to a commercial partner can find that cumulative royalty obligations consume a substantial portion of the product's revenue before anyone calculates profit. When a synthetic royalty investor enters the picture, the stack grows further.

The ORRI framework provides an explicit hierarchy for addressing this. In oil and gas, the mineral royalty comes off the top before the working interest is calculated. ORRIs then take their share from the working interest holder's portion. Each interest has a defined position in the waterfall. Pharmaceutical royalty agreements do not always define the stacking order with equivalent clarity — a problem that becomes acute when multiple royalty obligations, each calculated against "net sales" with varying definitions, sit on the same product.

Has This Been Done in Pharma?

No pharmaceutical transaction has, to my knowledge, been explicitly structured as an overriding royalty interest. The term does not appear in the Covington synthetic royalty studies, the Gibson Dunn Royalty Report covering $29.4 billion in life sciences royalty transactions from 2020 to 2024, or the Goodwin analysis of the synthetic royalty market's continued rise.

But several recent pharmaceutical transactions are functionally equivalent to ORRIs, even if the parties did not use the term.

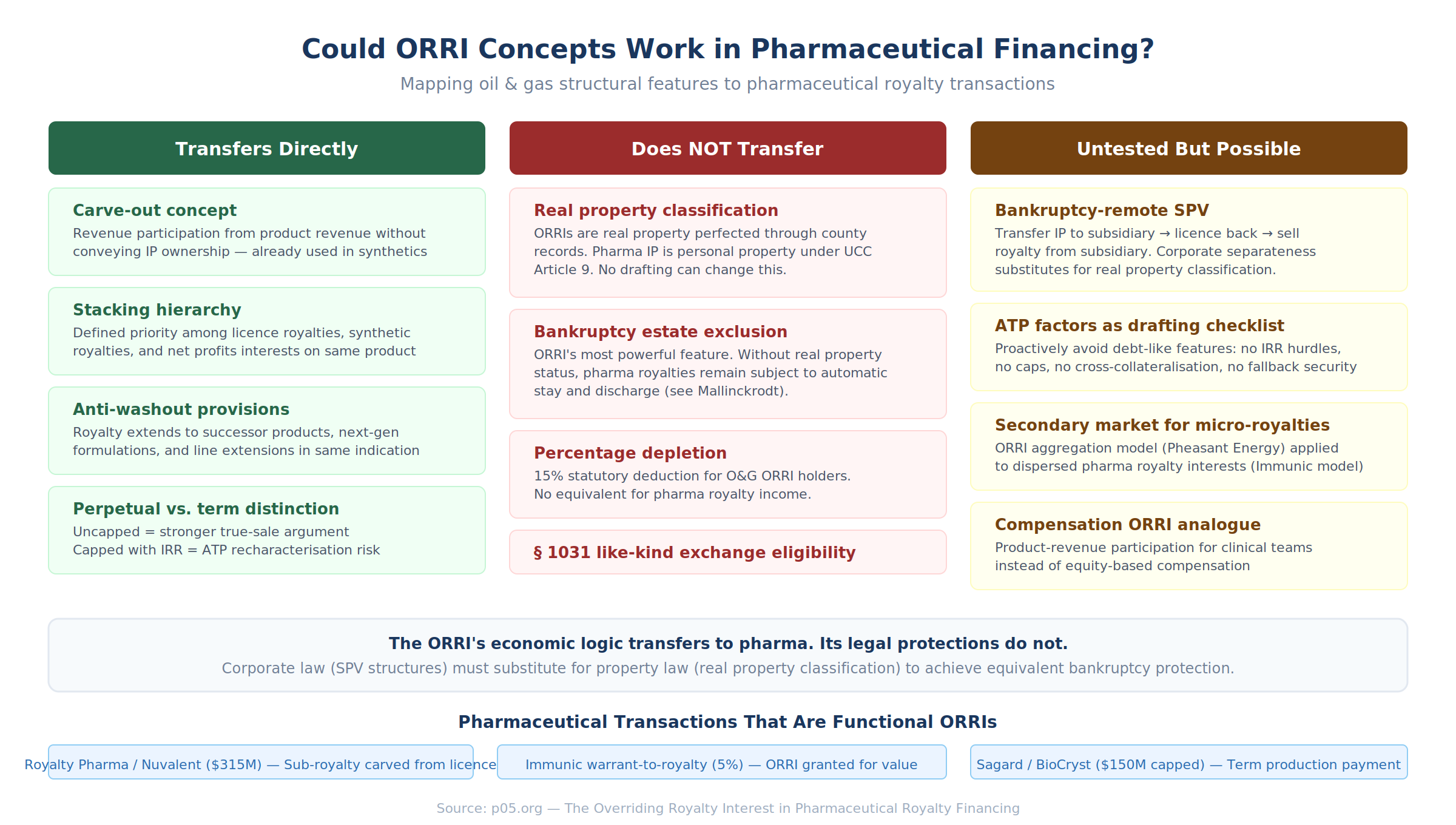

When Royalty Pharma acquired a pre-existing royalty interest in Nuvalent's neladalkib and zidesamtinib from an undisclosed third party for up to $315 million, the seller was monetising a portion of a licence royalty — carving a revenue interest out of an existing entitlement and conveying it to a third party for cash. Structurally, this is an ORRI reservation upon lease assignment: the original royalty holder assigns a sub-interest to an investor.

When Immunic created a 5% synthetic royalty on vidofludimus calcium in exchange for the cancellation of 51 million warrants — a transaction I examined in The Royalty Swap — it carved a revenue participation out of its own product economics and conveyed it to former warrant holders. That is, structurally, an ORRI granted in exchange for value, where the "working interest" is the company's ownership of the product's commercial revenue and the "value" is warrant cancellation rather than cash.

The Sagard Healthcare / OMERS Life Sciences transaction involving a capped, tiered, declining royalty on BioCryst's ORLADEYO for $150 million echoes the term production payment structure — a revenue participation that steps down as the investor achieves its target return. Under oil and gas law, this structure would be analysed as a dollar-denominated production payment subject to IRC § 636 loan treatment.

In each case, the economic substance matches the ORRI framework even though the legal documentation follows the pharmaceutical synthetic royalty template.

Could an ORRI Structure Work in Pharma?

The honest answer is: partially. The ORRI's legal architecture is built on a foundation of real property law that does not translate directly to intellectual property. But the economic logic does translate, and certain structural features of the ORRI could address problems that pharmaceutical royalty practitioners currently handle through more complicated means — or do not address at all.

What Would Transfer Directly

The carve-out concept. An ORRI is carved from the working interest, not from the mineral estate. In pharma, a company could carve a revenue participation from its own product revenue (the "working interest") without conveying any ownership of the underlying patents or regulatory exclusivity (the "mineral estate"). This is already what synthetic royalties do — but the ORRI framework provides a more precise vocabulary for describing the relationship between the carved-out interest and the retained interest. The distinction matters in bankruptcy. As the Covington synthetic royalty guide documented, synthetic royalties "also purport to be structured as a 'true sale' of the revenue stream at issue" but the characterisation has not been tested in court. Oil and gas ORRI practitioners have spent decades refining the drafting that supports true-sale characterisation. Pharmaceutical practitioners could borrow that precision.

The stacking hierarchy. Oil and gas law has developed clear priority rules for how mineral royalties, ORRIs, and net profits interests relate to each other. Pharmaceutical transactions would benefit from adopting an equivalent hierarchy, explicitly defining which obligations sit senior in the waterfall and how cumulative royalties are calculated. When Royalty Pharma's 2024 10-K describes acquiring synthetic royalties, third-party royalties, and earn-outs on the same products, the stacking question becomes material. In oil and gas, a 5% ORRI always sits behind the mineral royalty and ahead of the net profits interest. No equivalent convention exists in pharma.

The protective provisions. Anti-washout clauses, continuous development obligations, and consent-to-assignment restrictions are proven protective mechanisms with decades of judicial enforcement behind them. Pharmaceutical royalty agreements already include analogous provisions (commercialisation diligence covenants, change-of-control protections), but the oil and gas versions are more specific and more thoroughly tested. Of particular relevance is the anti-washout clause. In oil and gas, the Oklahoma rule recognises a "confidential relationship" between an ORRI assignor and the lessee, giving courts equitable grounds to extend an override to new leases even without an explicit anti-washout provision. In pharma, the equivalent scenario is a company allowing a product to languish, then acquiring or developing a competing compound in the same therapeutic area, effectively shifting revenue away from the burdened product. A pharmaceutical anti-washout clause — explicitly tying the royalty to any successor product, next-generation formulation, or replacement therapy developed by the same entity — would address this risk. I am not aware of any pharmaceutical royalty agreement that uses this language.

The perpetual vs. term distinction. Explicitly categorising a pharmaceutical royalty as "perpetual" (uncapped, life-of-patent) or "term" (capped at a specified dollar amount or multiple of invested capital) would clarify the true-sale analysis and the accounting treatment. The oil and gas case law demonstrates that term interests with dollar caps and IRR hurdles face substantially greater risk of recharacterisation as debt. The Covington study of 39 synthetic royalty deals found a median capped return of 2.25× invested capital — a structure that, under oil and gas law, would be analysed as a term production payment subject to IRC § 636 loan treatment rather than a true-sale conveyance. Pharmaceutical deal architects may not fully appreciate how much these structural choices affect bankruptcy characterisation.

What Would Not Transfer

Real property classification. The ORRI's most powerful feature — its classification as real property, which provides bankruptcy exclusion, perfection through county recording, and eligibility for percentage depletion — depends on the interest being tied to mineral estates and governed by state oil and gas law. Pharmaceutical intellectual property is personal property under Article 9 of the UCC. No amount of creative drafting will convert a pharmaceutical royalty into real property.

Bankruptcy estate exclusion. The ORRI's ability to survive the debtor's bankruptcy as an excluded real property interest is the feature that pharmaceutical royalty investors would most like to replicate. But this protection arises from the property classification, and without it, pharmaceutical royalties remain subject to the same bankruptcy risks that the Covington analysis has documented. The Mallinckrodt outcome makes this concrete: Sanofi's perpetual 1% royalty on a product generating close to $1 billion in annual revenue was discharged for pennies on the dollar. Had the same economics been structured as an ORRI on a mineral lease, the holder would have continued receiving payments throughout the bankruptcy without interruption.

Percentage depletion. The tax deduction available to ORRI holders has no pharmaceutical equivalent. Pharmaceutical royalty income is ordinary income, full stop.

Rule against perpetuities risk. Anti-washout clauses in oil and gas have their own vulnerabilities that pharmaceutical practitioners should understand before importing them. In Yowell v. Granite Operating Co., the Texas Supreme Court held that an anti-washout provision extending an ORRI to "future leases" violated the rule against perpetuities because the interest was subject to multiple contingencies not certain to occur within the perpetuities period. The court required reformation. A pharmaceutical anti-washout clause tying a royalty to successor products would face similar durational challenges if drafted without care.

What Remains Untested But Could Be Attempted

Bankruptcy-remote SPV structures borrowing ORRI economics. The Covington synthetic royalty guide describes — without reporting any completed transactions — a structure in which "many companies house their intellectual property in a subsidiary separate from the legal entities that commercialise the relevant product. This subsidiary could act as the seller in a synthetic deal, enter into a licence agreement with the operating company, and royalty payments under the licence agreement would fund payments under the synthetic deal." Sidley Austin confirms that it has advised "a privately held biotechnology company on the negotiation and documentation of a royalty financing transaction using a bankruptcy-remote vehicle."

This is, in effect, the pharmaceutical analogue to the ORRI's real property exclusion — using corporate separateness rather than property classification to achieve bankruptcy remoteness. The biotech company would transfer its IP to a newly formed subsidiary, the subsidiary would licence the IP back to the parent for commercialisation, and the subsidiary would sell a royalty on the licence revenue to the investor. If the parent files for bankruptcy, the IP sits in the subsidiary (which is structured to be bankruptcy-remote), the licence remains in force, and the investor's royalty continues to be funded from licence payments.

The challenge, as Covington notes, is that this structure "could be subject to challenge, particularly if the subsidiary is" not genuinely independent. Courts can pierce the corporate veil or substantively consolidate the subsidiary with the parent in bankruptcy if the subsidiary lacks genuine operational independence. The oil and gas ORRI avoids this problem entirely because the interest is a property right, not a corporate structure. But for pharmaceutical deals, the SPV approach may be the closest available approximation — and the ORRI case law on true-sale vs. disguised-financing provides a useful analytical framework for drafting the SPV's governing documents to maximise the probability that the structure survives judicial scrutiny.

Applying ATP's substance-over-form factors proactively. The ATP court identified specific features that suggested disguised financing: designated IRR hurdles, guaranteed returns, conditional royalty percentage increases, cross-collateralisation, and protective mortgages. A pharmaceutical royalty practitioner could use these factors as a drafting checklist — deliberately avoiding each one. An uncapped, perpetual royalty with no guaranteed return, no cross-collateralisation across products, no reversion upon payment of a specified amount, and no fallback security interest would score well on every ATP factor. The Covington study found that 95% of synthetic royalties are documented as "true sales" but most include features — caps, milestone adjustments, put options — that the ATP analysis would flag as debt-like. The gap between documentation and economic substance is precisely the gap that the ATP court exploited.

Secondary market development. In oil and gas, ORRIs are freely assignable unless the conveyance restricts transfer. Companies like Pheasant Energy actively acquire ORRIs from individual holders, aggregating small interests into portfolios. This creates liquidity for original holders and concentration for investors who want meaningful exposure.

The pharmaceutical market has no equivalent secondary market for sub-royalty interests. But the building blocks exist. The Immunic warrant-to-royalty exchange dispersed a 5% royalty among multiple former warrant holders. If those interests are transferable, an aggregator could assemble them. Royalty Pharma already functions as an aggregator of licence royalties — acquiring interests from universities, individual inventors, and biotech companies. The extension to acquiring sub-royalty interests carved from existing synthetic royalties is conceptually straightforward, though it requires that the original agreements permit assignment without the seller's consent. Most currently do not.

The compensation ORRI analogue. In oil and gas, geologists and landmen routinely receive ORRIs as deferred compensation tied to production success. The pharmaceutical equivalent would be granting clinical development teams, regulatory affairs specialists, or commercial launch executives a revenue participation in the products they help bring to market — payable only upon commercial success. This is not stock options or restricted stock units. It is a direct claim on product revenue, senior to equity, with no cost burden. No pharmaceutical company currently structures compensation this way, but the ORRI framework provides a model that ties compensation directly to value creation at the product level rather than at the corporate level. For a clinical-stage biotech developing multiple assets, this could align incentives more precisely than equity-based compensation, which dilutes across the entire enterprise.

Cross-industry characterisation precedent. If a pharmaceutical royalty were challenged in bankruptcy, would a court look to the ORRI case law for guidance? The ATP analysis — substance over form, looking at economic features rather than legal labels — is a general principle of bankruptcy law, not specific to oil and gas. A pharmaceutical synthetic royalty with a capped return, milestone-based acceleration, and cross-collateralisation across multiple products would present the same analytical questions that ATP's term ORRIs presented. The Womble Bond Dickinson analysis of Mallinckrodt advised pharmaceutical IP sellers to consider licensing rather than selling outright, taking security interests, or forming joint ventures — each of which corresponds to a structural feature that has been tested and refined in ORRI practice. Whether courts would explicitly apply oil and gas ORRI precedent to pharmaceutical transactions remains an open question, but the analytical framework is already being imported implicitly through the Covington and Mintz analyses.

Structural Comparison

| Feature | Oil & Gas ORRI | Traditional Pharma Royalty | Synthetic Pharma Royalty |

|---|---|---|---|

| Source of right | Carved from working interest | Reserved in licence agreement | Created by new agreement |

| Underlying asset | Mineral lease | Patents / regulatory exclusivity | Patents / product revenue |

| Cost burden | Free of production costs | Free of development costs | Free of development costs |

| Duration | Life of lease | Term of licence / patent life | Specified term or cap |

| Property classification | Real property (most states) | Personal property (UCC Art. 9) | Personal property (UCC Art. 9) |

| Perfection | County real property records | UCC-1 financing statement | UCC-1 financing statement |

| Bankruptcy treatment | Estate-excluded if true sale | Licensee protections (§ 365(n)) | Untested; likely secured claim |

| Tax treatment | Depletion-eligible | Ordinary income | Ordinary income / debt |

| Transferability | Freely assignable (default) | Subject to licence consent | Subject to agreement terms |

| Termination trigger | Lease expiry / release | Patent expiry / licence term | Cap reached / term expires |

| Anti-washout protection | Available by contract | Not standard | Not standard |

| Stacking convention | Defined priority hierarchy | Variable / inconsistent | Variable / inconsistent |

What Would Have to Change

For the ORRI concept to gain traction in pharmaceutical financing, several things would need to happen.

Pharmaceutical royalty agreements would need to adopt explicit stacking conventions that define priority among multiple royalty obligations on the same product. Today, many synthetic royalty agreements calculate payments based on "net sales" without clearly specifying how the definition interacts with pre-existing licence royalties owed to upstream partners. The oil and gas framework — where each interest has a defined position in the revenue waterfall — provides a template.

Anti-washout provisions would need to become standard, drafted with attention to the rule against perpetuities limitations exposed in Yowell. The oil and gas experience demonstrates that non-operating interest holders are vulnerable to strategic behaviour by the entity controlling the underlying asset. In pharma, the equivalent risk is that a company allows a product to languish while developing a competing compound, or structures an acquisition in a way that shifts revenue away from the burdened product. A pharmaceutical anti-washout clause — extending the royalty to successor products, next-generation formulations, and line extensions developed within the same therapeutic indication — would address this risk within existing contract law frameworks.

The true-sale analysis would need further development in the pharmaceutical context. The ATP case law provides a detailed analytical framework for distinguishing between true conveyances and disguised financings. Pharmaceutical royalty practitioners could use this framework proactively — structuring transactions to avoid the features that ATP courts identified as indicative of debt (IRR hurdles, guaranteed returns, cross-collateralisation, protective mortgages) and to emphasise the features that support true-sale treatment (uncapped revenue participations, absence of recourse, no reversion upon payment of a specified sum). The Mintz analysis of Mallinckrodt confirmed that "security and ownership" are the key variables in bankruptcy characterisation — and that licensing, security interests, and retained ownership stakes each provide incrementally stronger protection. Each of these corresponds to a structural feature well-established in ORRI practice.

Bankruptcy-remote SPV structures would need to move from theoretical possibility to market standard. The Covington guide describes the concept, Sidley has executed at least one transaction using this approach, but the structure has not yet been tested in a pharmaceutical bankruptcy. Given the Mallinckrodt precedent — which demonstrated that unsecured pharmaceutical royalties can be discharged entirely — there is a strong incentive for investors to push for bankruptcy-remote structures. The ORRI analogy is useful here: in oil and gas, the ORRI's bankruptcy protection comes from property law (real property classification); in pharma, the equivalent protection would come from corporate law (SPV separateness and the true-sale doctrine). Different legal mechanism, same economic objective.

And ultimately, someone would need to test the structure. The pharmaceutical royalty market is built on precedent. Each new structural innovation — from Royalty Pharma's first traditional monetisations in the 1990s to the emergence of synthetic royalties in the 2010s to the warrant-to-royalty exchange I documented at Immunic — began as an experiment before becoming a template. The ORRI concept, adapted for pharmaceutical intellectual property, would require the same willingness to try something new. Whether any transaction participant is willing to be first remains the open question.

I am not a lawyer or financial adviser. This content is for informational purposes only and does not constitute investment, legal, or financial advice. All information is derived from publicly available sources including legal analyses, SEC filings, court opinions, and academic publications. Information may have changed since publication.

Member discussion