The Royalty Interest Agent in Pharmaceutical Royalty and Revenue Interest Transactions

The term "Royalty Interest Agent" does not appear as a standardised designation in pharmaceutical royalty financing documentation. Instead, the role is expressed through a set of functionally equivalent but terminologically inconsistent defined terms that vary by transaction, by investor, and by deal counsel. Understanding what this role entails—how it is defined, what powers it carries, what liabilities it excludes, and how it differs across transaction types—requires attention to the specific contractual language in which it is embedded.

This analysis examines the agent designation as it appears across recent SEC filings, identifies the core provisions that define the role, and traces the structural adaptations that distinguish the agent in royalty purchase agreements and revenue interest financing agreements from its better-known counterpart in syndicated lending.

Why This Matters

The agent designation determines who receives payments, who holds collateral, who processes amendments, and who pulls the trigger on enforcement. In a bilateral transaction none of this requires a separate role. But the pharmaceutical royalty market has moved well beyond bilateral structures—and the agent question now carries consequences that flow through to economics, operational flexibility, and downside protection.

For the company making payments, the agent is the sole operational counterparty for what may be a 10-to-15-year financial relationship. The quarterly compliance certificate goes to the agent. Default notices come from the agent. Amendment requests are processed—or delayed—by the agent. When Verona Pharma needed to restructure its $650 million financing in March 2025—repaying the RIPSA, amending the debt facility, renegotiating the intercreditor arrangements—that entire process ran through the agent. The speed and competence with which the agent coordinates investor approvals directly affects the company's ability to execute.

For investors, particularly minority co-investors, the agent provisions define the structural limits of their protection. When the agent is also the majority investor—as in the OrbiMed/Adaptive Biotechnologies structure—the graduated consent mechanics and "sacred rights" protections are the contractual barrier between minority interests and adverse action. Understanding which decisions require unanimity versus majority direction is not academic—it determines whether a minority investor can block a payment reduction, a collateral release, or a maturity extension it did not agree to.

For deal counsel, the absence of a standardised defined term—and the inconsistency in how these provisions are drafted across transactions—means that assumptions drawn from one deal's documentation may not hold in another. The agent designated as "Purchaser Agent" in an OrbiMed structure holds different authority, under different exculpation standards, than the "Investor Representative" in an HCRx structure. The terminology matters because the contractual architecture varies with it.

Terminology: A Taxonomy

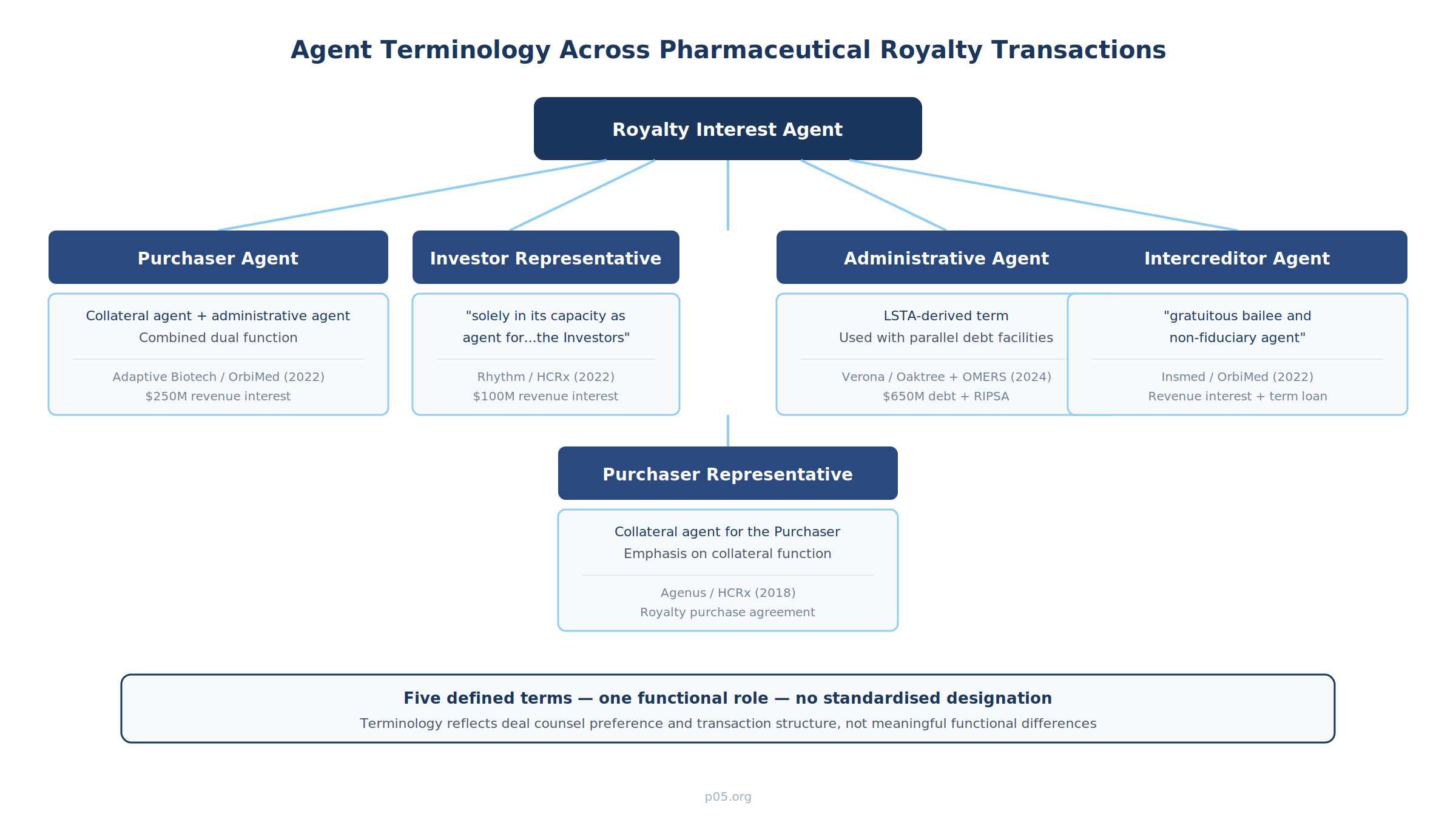

The agent role in pharmaceutical royalty transactions appears under at least five distinct defined terms in recent filings. The terminology reflects the preferences of deal counsel and the structural nuances of the underlying transaction, not meaningful functional differences.

"Purchaser Agent." Used in revenue interest purchase agreements where the agent serves dual functions as collateral agent and administrative agent. In Adaptive Biotechnologies' $250 million agreement with OrbiMed (September 2022), the defined term is:

"OrbiMed Royalty & Credit Opportunities IV, LP, as collateral agent and administrative agent for the Purchasers (the 'Purchaser Agent')"

This formulation combines two distinct functions—collateral administration and administrative agency—into a single defined term. The dual-hatted structure means the Purchaser Agent both manages day-to-day payment mechanics and holds perfected security interests in the collateral package on behalf of the purchasing group.

"Investor Representative." Used in revenue interest financing agreements, particularly those structured by HealthCare Royalty. In the Rhythm Pharmaceuticals $100 million agreement (June 2022), the defined term is:

"HCR Collateral Management, LLC, a Delaware limited liability company (the 'Investor Representative'), solely in its capacity as agent for, and representative of, the Investors"

The qualifier "solely in its capacity" is significant. It cabins the entity's authority to the specific role defined in the agreement, preventing any inference of broader agency or fiduciary obligations that might arise under general partnership or agency law.

"Purchaser Representative." Used in royalty purchase agreements, particularly for traditional royalty monetisations. In the Agenus/HealthCare Royalty royalty purchase agreement, the defined term is:

"HealthCare Royalty Partners III, L.P., as collateral agent for the Purchaser"

Here the defined term emphasises the collateral function. The administrative agency functions are implied rather than explicitly named—the Purchaser Representative receives payments, manages escrow accounts, and coordinates notices, but these are not separately defined roles.

"Administrative Agent." Borrowed directly from syndicated lending, this term appears when royalty or revenue interest transactions are structured alongside term loan facilities. In the Verona Pharma $650 million financing with Oaktree and OMERS (May 2024), Oaktree served as administrative agent across both a $400 million term loan and a $250 million revenue interest purchase and sale agreement (RIPSA). When both debt and royalty components share the same agent, the term typically follows the lending convention.

"Intercreditor Agent." A specialised designation for transactions where the royalty interest sits alongside senior secured debt held by a different creditor group. In the Insmed/OrbiMed revenue interest purchase agreement (October 2022), the agreement introduces:

"BioPharma Credit PLC, acting as gratuitous bailee and non-fiduciary agent on behalf of, and for the benefit of, the Purchaser"

The "gratuitous bailee" formulation is borrowed from intercreditor structures in leveraged finance, where a first-lien agent holds collateral for the benefit of both first-lien and second-lien creditors. The "non-fiduciary" qualifier expressly negates any duty of loyalty owed to the party on whose behalf the agent holds collateral—a critical distinction when the intercreditor agent's primary relationship is with the term loan lenders.

Structural Provenance: From Syndicated Lending to Royalty Finance

The agent provisions in pharmaceutical royalty agreements are adapted—not directly transplanted—from the LSTA (Loan Syndications and Trading Association) model agency provisions used in syndicated credit facilities. The adaptation is well-documented in legal commentary. Mayer Brown's 2019 analysis of administrative agent issues in syndicated lending identifies the core framework from which the royalty agent's role derives: formal appointment establishing authority, express limitation to duties stated in the agreement, disclaiming fiduciary status, exculpation to a gross negligence/willful misconduct standard, lender-side indemnification, and defined resignation/removal mechanics.

Royalty finance transactions retain this framework but adapt it in several technically significant ways.

Variable payment streams. In a syndicated loan, the agent processes fixed interest payments and scheduled amortisation. In a royalty or revenue interest transaction, the payment stream is a percentage of net sales—recalculated quarterly, subject to adjustments for deductions (rebates, chargebacks, returns, distribution fees), and potentially subject to tiered rates that change as cumulative payments cross defined thresholds. The agent must verify these calculations against the company's quarterly compliance certificates, a task that requires pharmaceutical-specific knowledge (understanding of gross-to-net adjustments, channel dynamics, and government programme deductions) that has no equivalent in loan administration.

True sale characterisation. Where the transaction is documented as a true sale rather than a secured financing, the agent's position involves a structural tension. Covington's 2024 analysis found that 95% of royalty monetisations from 2019–2023 were documented as true sales. In a true-sale structure, the purchaser owns the royalty interest outright—it is not collateral securing a loan. Yet the agreements routinely include "backup" security interests (filed as precautionary UCC financing statements) in case a court subsequently recharacterises the sale as a secured loan. The agent files and maintains these backup security interests, creating a collateral administration role that exists only as a contingency against recharacterisation risk.

Absence of revolving mechanics. Syndicated loan agents manage borrowing base certificates, swingline loans, letter of credit drawings, and revolving commitment reductions. None of these exist in a pure royalty purchase. The agent's role is therefore narrower in some respects (no draw mechanics) but more complex in others (product-level commercial verification).

Milestone-contingent funding. Revenue interest financing agreements frequently include tranche structures where subsequent funding is contingent on regulatory or commercial milestones—FDA approval, first commercial sale, achievement of specified net sales thresholds. In the Adaptive Biotechnologies/OrbiMed deal, the $125 million first payment was unconditional, but the subsequent $75 million second payment and $50 million third payment were subject to funding conditions and had to be requested by the company no later than September 2025. The agent must verify milestone satisfaction before releasing subsequent tranches, a function that parallels the conditions-precedent verification in delayed-draw term loans but applies pharmaceutical-specific criteria.

The Agent Provision: Core Contractual Architecture

The agent section of a royalty purchase agreement or revenue interest financing agreement typically runs 5–10 pages and contains a defined set of provisions. Drawing on the framework established in LSTA form documentation and adapted for royalty-specific mechanics, the standard architecture includes the following elements.

Appointment and Authority

The investors irrevocably appoint the agent and authorise it to take actions and exercise powers expressly set forth in the transaction documents. The operative word is "expressly"—the agent has no implied authority and no duties not specifically enumerated.

Exculpation

The exculpation provision limits the agent's liability to losses caused by its own gross negligence, willful misconduct, or (in some formulations) bad faith. The agent is not liable for actions taken or omitted in reliance on the advice of legal counsel, accountants, or other experts. The agent is not deemed to have knowledge of any default unless it receives actual written notice from the company or an investor. The agent has no duty to inquire, investigate, or monitor the company's business, financial condition, or compliance—unless the agreement expressly requires specific monitoring actions.

This exculpation standard tracks the framework described in Eaton Vance Management v. Wilmington Savings Fund Society (N.Y. Sup. Ct. 2018), where claims against an administrative agent were dismissed on the basis that the agent acted within its contractual authority and the claimant failed to demonstrate gross negligence or willful misconduct.

No Fiduciary Duty

This provision—universal in royalty financing agent clauses—expressly disclaims any fiduciary relationship between the agent and the investors, the agent and the company, or the agent and any third party. The agent acts in a contractual capacity only. This is not merely defensive boilerplate: without the disclaimer, an agent holding collateral and making discretionary enforcement decisions could potentially be characterised as a fiduciary under state common law, which would impose duties of loyalty and care beyond those defined in the agreement.

Individual Capacity

Where the agent is also an investor in the transaction—as in the OrbiMed/Adaptive structure, where OrbiMed Royalty & Credit Opportunities IV served as both Purchaser Agent and a purchaser—the agreement includes a provision recognising the agent's right to act in its individual capacity as though it were not the agent. This permits the agent-investor to vote on amendments, participate in enforcement decisions, and exercise its economic rights without being constrained by its agency role.

Indemnification

The investors indemnify the agent for losses, claims, and expenses incurred in performing its duties, pro rata by their respective shares of the invested amount. This indemnification is typically "to the extent not reimbursed by the Company"—meaning the company's indemnification obligation is the primary source, with investor-side indemnification as a backstop. The indemnification survives termination of the agreement and resignation or removal of the agent.

Direction and Consent Mechanics

The agent acts at the direction of "Required Investors" (or "Required Purchasers"), typically defined as investors holding more than 50% of the aggregate invested amount. Certain actions require higher thresholds or unanimity:

- Majority required: enforcement actions, acceleration, exercise of remedies, amendments to non-economic terms

- Supermajority or unanimity required: reductions in payment percentages, extensions of payment dates, releases of all or substantially all collateral, changes to the pro rata sharing provisions, changes to the voting thresholds themselves

This graduated consent structure directly mirrors syndicated lending conventions. The "sacred rights" requiring unanimous consent protect individual investors from having their economic terms diluted by a majority vote—a particularly important protection in co-investment structures where one fund's affiliate serves as agent.

Collateral Administration

The agent perfects security interests (through UCC filings and control agreements), manages the segregated account structure (lockbox accounts, collection accounts, distribution accounts), and holds the collateral package for the benefit of the investor group. Upon an event of default, the agent may exercise remedies—including foreclosure, cash sweeps, and acceleration—but typically only at the direction of Required Investors.

The collateral package in a pharmaceutical royalty transaction typically includes: product-related intellectual property (patents, trademarks, know-how), regulatory assets (NDAs, BLAs, marketing authorisations), material contracts (license agreements, supply agreements, distribution agreements), and deposit accounts into which product revenues are swept. The agent must maintain perfection across all of these asset categories, which may involve UCC filings, patent and trademark security agreement recordings at the USPTO, and control agreements with depositary banks.

Resignation and Successor

The agent may resign upon 30 days' written notice. Required Investors appoint a successor. If no successor is appointed within the notice period, the resigning agent may appoint a successor itself or, in some formulations, the agent's resignation becomes effective without a successor—leaving the investors to coordinate among themselves until one is appointed. This creates a structural incentive for investors to promptly agree on a successor.

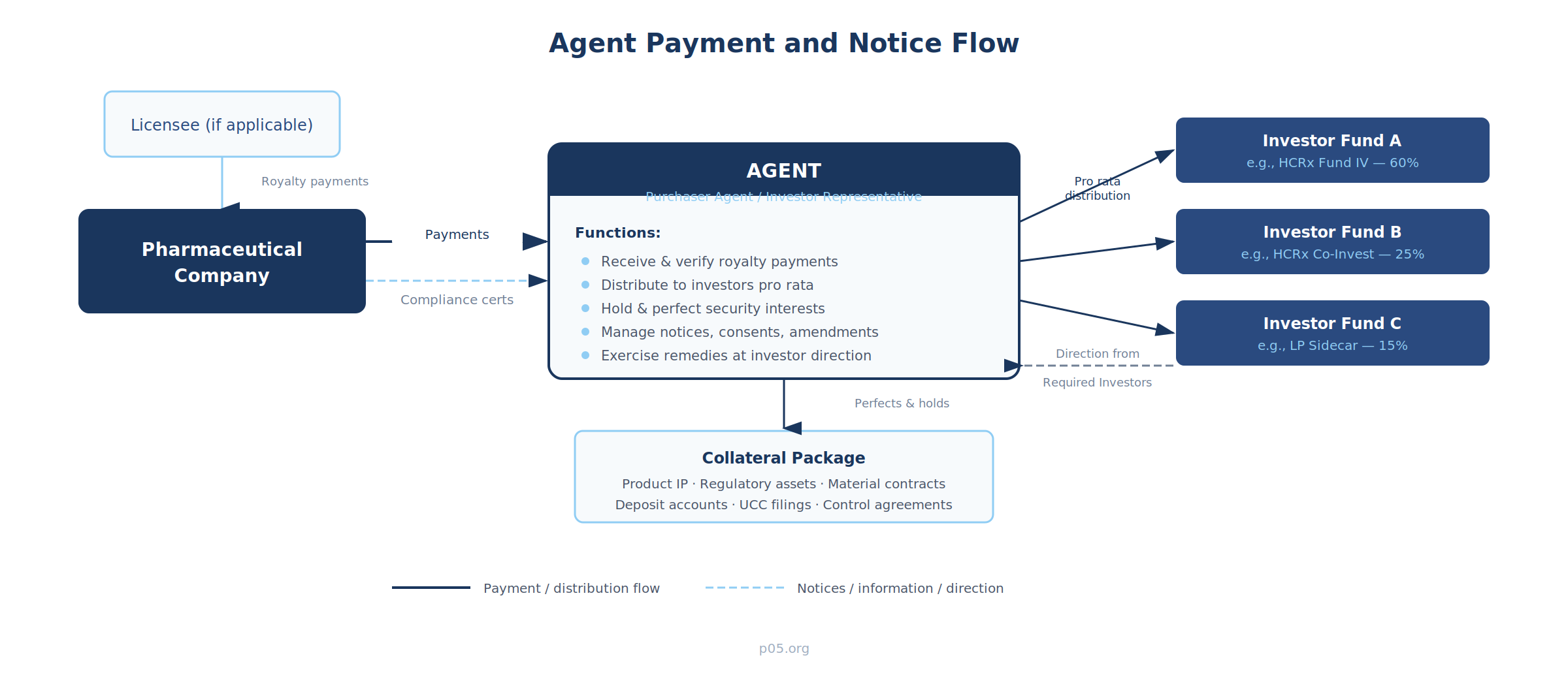

Agent Payment and Notice Flow

The agent sits at the centre of the transaction's operational infrastructure. The company makes all payments to the agent's segregated account—not directly to investors. The agent verifies the quarterly calculation, applies the contractual waterfall, and distributes proceeds to each investor according to its pro rata share. Notices, compliance certificates, and amendment requests all flow through the agent as the single point of contact. Direction from investors—enforcement decisions, consent to amendments, acceleration elections—flows back through the agent to the company.

This architecture serves two purposes. For the company, it provides a single operational counterparty regardless of how many fund vehicles participate in the investor group. For the investors, it provides a centralised mechanism for collateral administration, payment processing, and coordinated enforcement—without requiring each investor to independently monitor the company's compliance and independently pursue remedies upon default.

Deal Examples: Agent Structures in Practice

Single-Entity Agent (HCR Collateral Management / Rhythm)

HCR Collateral Management, LLC—a dedicated entity separate from the HCRx fund vehicles that serve as investors—acts as Investor Representative. This separation insulates the agent function from the economic interests of any individual fund vehicle. All notices flow to HCR Collateral Management. All payments are received by HCR Collateral Management and distributed to the HCRx fund entities. The company's sole operational counterparty is HCR Collateral Management, regardless of how many HCRx fund vehicles participate.

Key structural feature: The dedicated management entity has no economic interest in the royalty payments it administers. This eliminates the inherent conflict present when the agent is also an investor, though it introduces a dependence on the management entity's continued existence and operational capability.

Dual-Hatted Agent (OrbiMed / Adaptive Biotechnologies)

OrbiMed Royalty & Credit Opportunities IV, LP serves as both purchaser and Purchaser Agent. The "Individual Capacity" provision permits OrbiMed to participate in investor decisions (amendments, enforcement, acceleration) in its capacity as a co-investor, notwithstanding its agent role.

Key structural feature: The dual-hatted model is cost-efficient but creates inherent tension. When the agent-investor holds a majority or super-majority of the invested amount, it effectively controls both the direction given to the agent and the agent's execution of that direction. For minority co-investors, the individual capacity provision and the graduated consent structure are the primary contractual protections against adverse action.

Multi-Instrument Agent (Oaktree / Verona Pharma)

Oaktree served as administrative agent across both a term loan facility and a RIPSA. The two instruments were governed by separate agreements with an intercreditor agreement defining priority, payment waterfall, enforcement standstills, and collateral sharing. When Verona repaid the RIPSA in March 2025 and restructured the debt facility to $450 million, the agent managed the termination of one instrument, the amendment of another, and the renegotiation of the intercreditor arrangements—all within the same closing.

Key structural feature: The multi-instrument agent must operate under two separate agency mandates with potentially conflicting investor constituencies. The intercreditor agreement governs which instrument's investors have priority in enforcement, how cash is allocated during a default, and whether one set of investors can block or delay the other's exercise of remedies. The agent's contractual position becomes significantly more complex—and its potential exposure correspondingly greater—than in a single-instrument structure.

Gratuitous Bailee Agent (BioPharma Credit PLC / Insmed)

BioPharma Credit PLC—an entity affiliated with Pharmakon Advisors—acted as intercreditor agent with the express designation "gratuitous bailee and non-fiduciary agent." The "gratuitous bailee" formulation means BioPharma Credit holds collateral for OrbiMed's benefit without receiving consideration for the bailment itself (the bailee's compensation comes from its separate relationship as term loan lender). The "non-fiduciary" qualifier forecloses any claim that the bailee owes duties of loyalty to the beneficiary of the bailment.

Key structural feature: This is the most heavily disclaimed form of the agent role. The gratuitous bailee holds collateral as a mechanical function, with no discretion, no advisory obligation, and no fiduciary duty. It is structurally similar to a depositary bank holding pledged securities—a ministerial role stripped of all substantive authority.

Accounting and Tax Treatment

The agent designation has implications beyond the contractual relationship.

True sale vs. secured financing. Whether the transaction is characterised as a true sale (the purchaser owns the royalty interest) or a secured financing (the purchaser has a security interest in the royalty interest) affects the agent's UCC filing strategy, the company's balance sheet treatment, and the bankruptcy remoteness of the structure. The agent typically files precautionary UCC financing statements naming the company as debtor and the agent (for the benefit of the investor group) as secured party—regardless of the intended true-sale characterisation. This dual-track approach preserves the investor group's fallback position if recharacterisation occurs.

Withholding tax. For cross-border transactions—where non-U.S. investors hold royalty interests in products generating U.S. sales—the agent may be the entity that receives payments subject to U.S. withholding tax. The agent must manage treaty benefit claims, obtain and verify IRS Forms W-8BEN or W-8BEN-E from non-U.S. investors, and coordinate with the company's withholding obligations. Where the agent is the named payee on the licensee instruction letter (directing the licensee to pay royalties to the agent's account), the agent effectively becomes the tax reporting point for the payment stream.

Bankruptcy treatment. In a company bankruptcy, the agent's position depends on the transaction structure. If documented as a true sale, the royalty interest is not property of the estate, and the agent can continue collecting payments from the licensee. If recharacterised as a secured loan, the automatic stay applies, and the agent must seek relief from the stay before exercising remedies. The agent's backup security interest—filed precautionarily at closing—becomes the investor group's primary protection in the recharacterisation scenario. The agent's obligations in a bankruptcy context (filing proofs of claim, participating in plan negotiations, credit-bidding in asset sales) are typically defined in the agreement and exercised at the direction of Required Investors.

Conclusion

The royalty interest agent—whatever its defined term in any given transaction—is the operational nexus of the pharmaceutical royalty financing relationship. The five distinct designations identified in recent filings (Purchaser Agent, Investor Representative, Purchaser Representative, Administrative Agent, Intercreditor Agent) reflect deal counsel preferences and structural nuances rather than meaningful functional differences. But the contractual architecture behind each designation—the exculpation standards, fiduciary disclaimers, consent thresholds, collateral mechanics, and individual capacity provisions—varies in ways that carry real consequences for both companies and investors.

As multi-investor structures, multi-instrument financings, and secondary market activity continue to increase the complexity of pharmaceutical royalty transactions, the agent provisions deserve the same scrutiny that parties have long applied to the economic terms. The payment percentage and the cap multiple get negotiated; the agent designation often does not. That asymmetry is a structural vulnerability for parties who will spend a decade living with the consequences.

All information in this report was accurate as of the research date and is derived from publicly available sources including company press releases, SEC filings, regulatory announcements, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice.

Member discussion