The Warrant Sweetener: How Equity Kickers Are Reshaping Pharmaceutical Royalty Deals

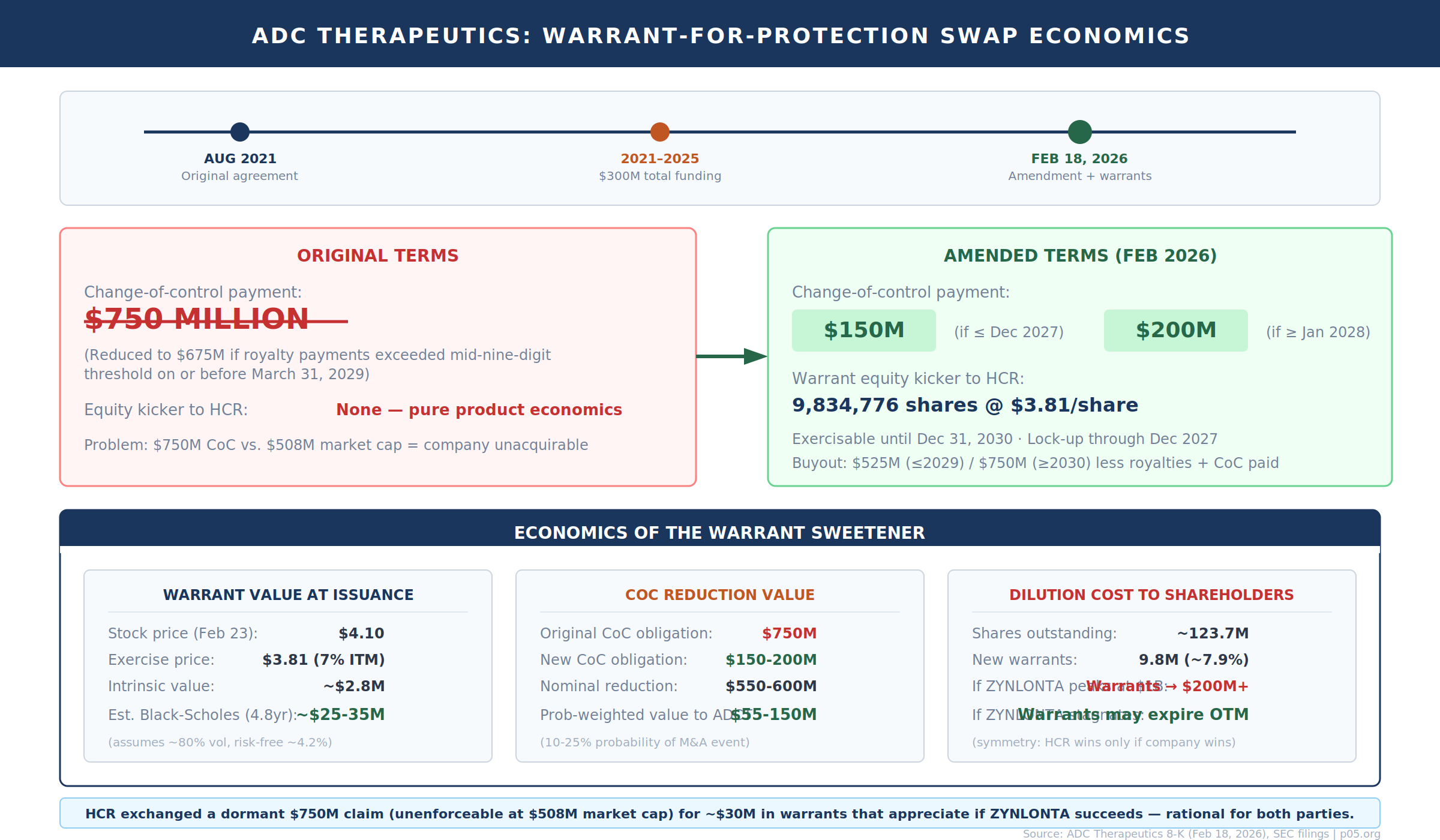

When ADC Therapeutics filed an 8-K on February 23, 2026, the headline was the dramatic reduction of its change-of-control payment to HealthCare Royalty from $750 million to as little as $150 million. Buried in the exhibits was a detail that tells you far more about where royalty financing is headed: in exchange for loosening the leash, HCR received warrants to purchase approximately 9.8 million common shares at $3.81 per share, exercisable through December 2030.

The warrants are not incidental. They represent a shift in how royalty investors structure downside protection, moving from fixed contractual floors towards equity-linked optionality that rises and falls with the company's success. They arrive at a moment when warrant inducements, a related but distinct mechanism, have become the survival financing of choice for capital-constrained biotechs, generating billions in aggregate proceeds through 2024-2026.

This article examines both phenomena: warrants as sweeteners within royalty financing restructurings, and standalone warrant inducements as primary capital-raising tools. Though they share a common instrument, their strategic logic and the types of companies that use them could not be more different.

What Is a Warrant Inducement?

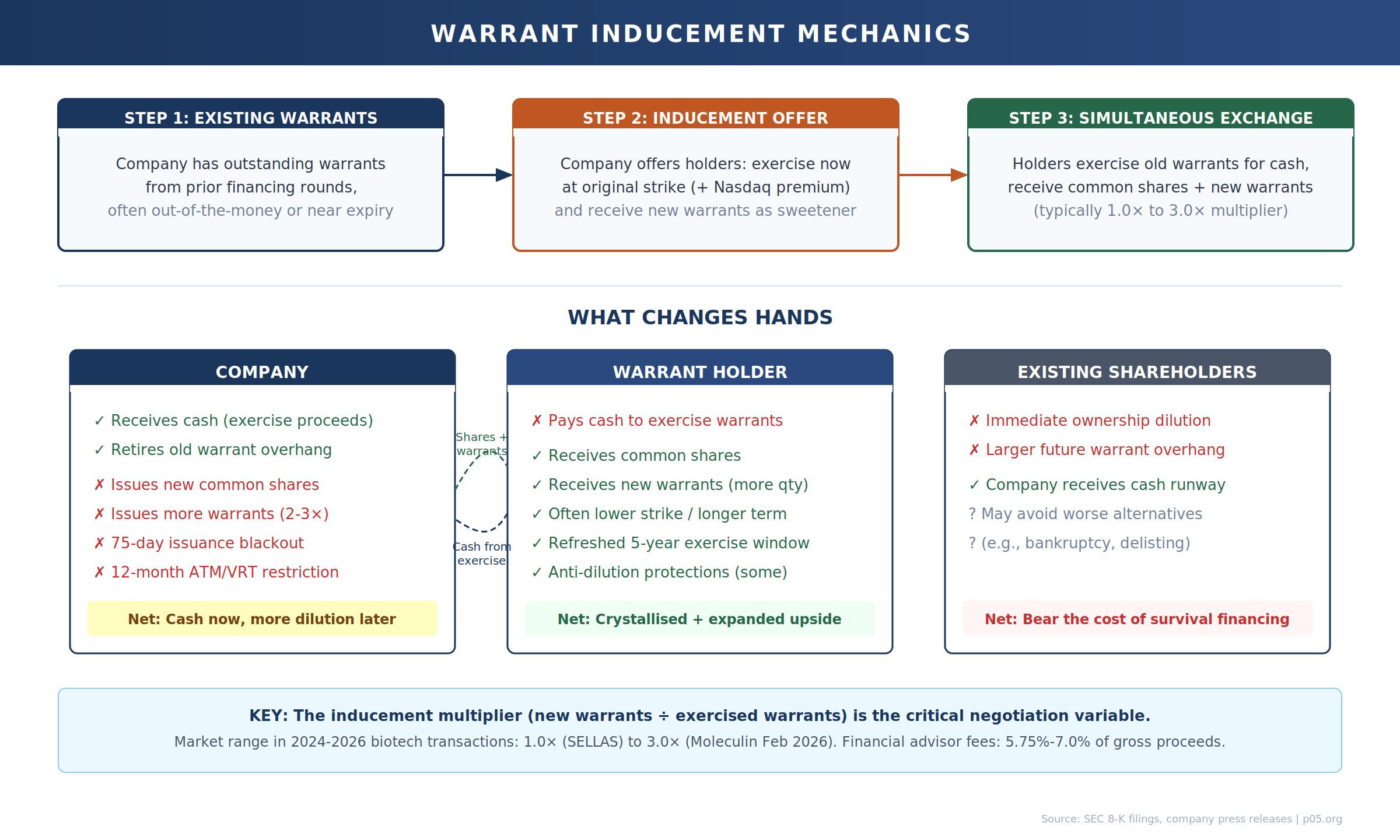

A warrant inducement is a transaction in which a company persuades existing warrant holders to exercise immediately, generating cash, by offering new warrants as compensation. The holder surrenders old warrants, pays the exercise price in cash, receives common shares, and simultaneously receives a fresh batch of warrants with new terms: typically a longer duration, sometimes a lower strike price, and almost always in greater quantity than the warrants surrendered.

The company converts a contingent equity obligation into immediate cash. The warrant holder crystallises their position and receives refreshed equity exposure, often on more favourable terms. Existing shareholders absorb the cost: immediate dilution from the exercise plus a larger warrant overhang.

The multiplier, the ratio of new warrants issued to old warrants exercised, is the critical negotiation variable. In recent biotech transactions multipliers have ranged from 1.0× (one new warrant per exercised warrant, as in the SELLAS Life Sciences October 2025 transaction) to 3.0× (as in Moleculin Biotech's February 2026 inducement). The equilibrium reflects a simple tension: lower multipliers generate less participation; higher multipliers generate more dilution than the cash proceeds justify.

The Spectrum: From Survival Financing to Strategic Restructuring

Warrant inducements sit along a spectrum defined by context and counterparty sophistication. At one end are micro-cap biotechs using serial inducements to avoid delisting. At the other are multi-hundred-million-dollar royalty restructurings where warrants serve as consideration in complex negotiations between commercial-stage companies and institutional investors.

Serial Inducements: The Distressed End

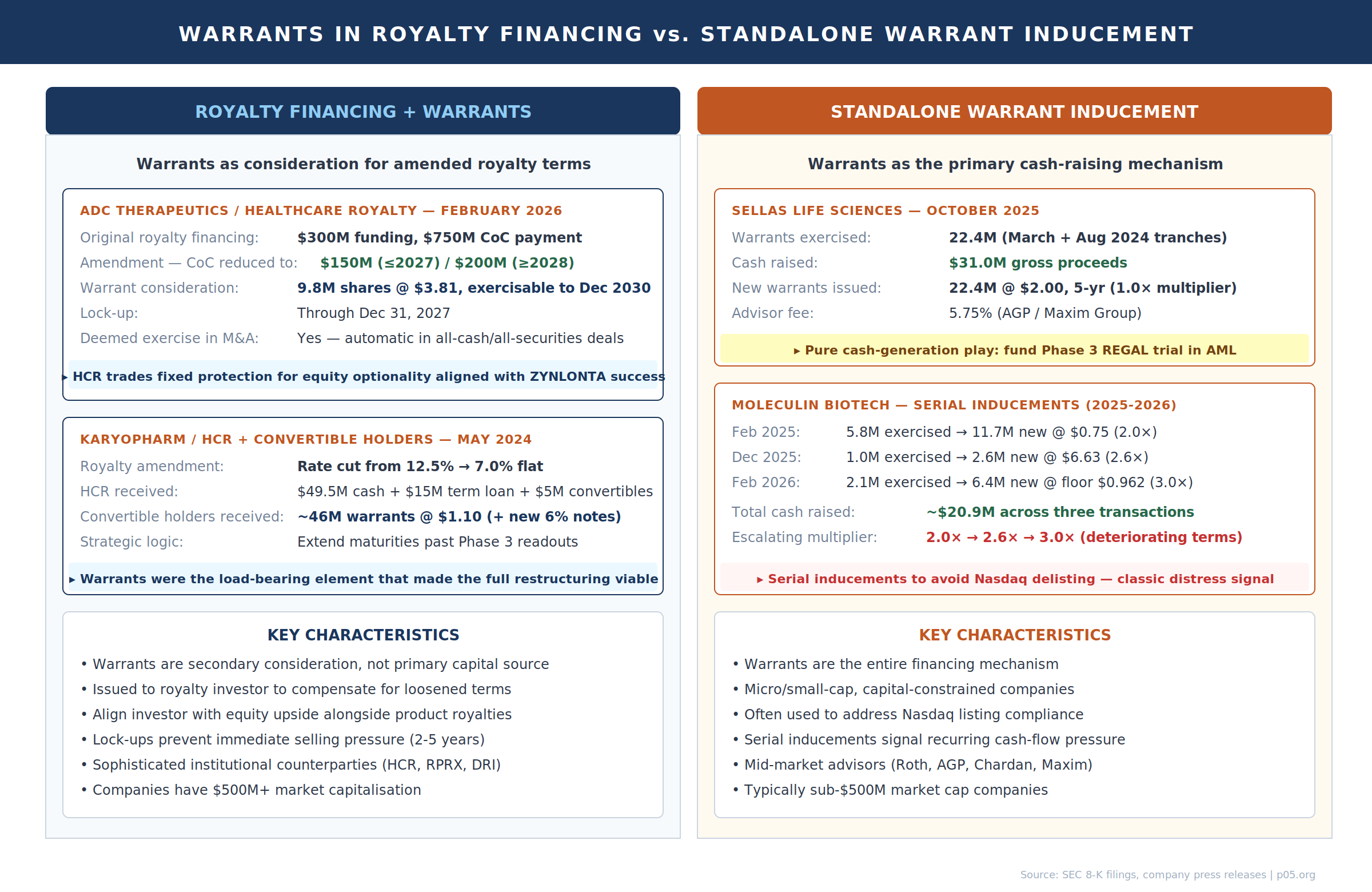

Moleculin Biotech provides the textbook case of warrant inducement as survival mechanism. The company executed three separate inducement transactions within twelve months:

| Transaction | Date | Warrants Exercised | Cash Raised | New Warrants | Multiplier |

|---|---|---|---|---|---|

| First inducement | Feb 2025 | 5,800,000 | $5.8M | 11,700,000 | 2.0× |

| Second inducement | Dec 2025 | 1,000,000 | $6.8M | 2,600,000 | 2.6× |

| Third inducement | Feb 2026 | 2,122,652 | $8.3M | 6,367,956 | 3.0× |

Each successive inducement required a higher multiplier, reflecting deteriorating leverage as the warrant overhang expanded. The December 2025 transaction was explicitly undertaken to address Nasdaq's minimum stockholders' equity requirement of $2.5 million; the company had received a delist determination letter weeks earlier. By February 2026, the new Series H warrants included anti-dilution price-reset protections with a floor of $0.962, reflecting investors' demand for protection against the very dilution the inducement itself was creating.

This is the warrant inducement death spiral in miniature. Each round of financing creates the conditions that necessitate the next, at progressively worse terms for existing shareholders.

Clinical-Stage Financing: The Middle Ground

SELLAS Life Sciences raised $31 million in October 2025 by inducing exercise of warrants originally issued in March and August 2024. Holders exercised at their original strike prices plus a $0.125 per share premium (a Nasdaq requirement for inducement pricing), receiving new warrants at $2.00 on a 1.0× basis. The proceeds were earmarked for the Phase 3 REGAL trial in acute myeloid leukaemia.

iBio raised $6.2 million in April 2025 through an inducement where 5.6 million existing warrants were exercised at $1.11, with investors receiving 11.25 million new warrants at $0.86: a 2.0× multiplier with a lower strike than the original instruments.

These transactions differ from the Moleculin pattern in that they represent planned capital deployment rather than emergency liquidity events. But they share the fundamental characteristic that the warrant itself is the primary financing instrument. There is no underlying product royalty, no asset-specific cash flow being monetised, and no institutional counterparty with a long-term strategic relationship. These are equity market transactions, pure and simple.

Warrants Within Royalty Restructurings: The Strategic End

At the opposite end sit transactions like ADC Therapeutics and HealthCare Royalty, where warrants function not as the primary financing mechanism but as consideration in a negotiated restructuring. The economics, strategic logic, and implications differ fundamentally from standalone inducements, and this distinction matters for understanding how the asset class is evolving.

ADC Therapeutics: Anatomy of a Royalty-Linked Warrant

The ADC Therapeutics amendment restructured a royalty purchase agreement dating to August 2021 under which HCR had provided $300 million in total funding. The original agreement required a $750 million payment upon any change of control (reduced to $675 million if royalty payments exceeded a mid-nine-digit threshold before March 2029), less royalties already paid.

That $750 million obligation was, in effect, a poison pill. With a market capitalisation of roughly $508 million, any acquirer would face a royalty buyout potentially exceeding the company's entire equity value. The provision gave HCR ironclad protection on paper but rendered the company essentially unacquirable, destroying strategic optionality for both management and shareholders.

The amendment solved this through a value exchange. ADC Therapeutics' change-of-control payment dropped to $150 million if triggered through December 2027, or $200 million thereafter. Royalty obligations continue post-acquisition until the original cap is reached, and the company retains optional buyout rights at $525 million (before 2030) or $750 million (from 2030 onward), minus royalties paid and the CoC payment. In return, HCR received warrants to purchase 9,834,776 common shares at $3.81 per share, exercisable through December 31, 2030, with a lock-up through the end of 2027. The warrants include deemed-exercise provisions in all-cash or all-securities acquisitions, ensuring HCR captures equity value even in change-of-control scenarios.

The economic logic is clean. HCR surrendered a large portion of its fixed downside protection (a $750 million CoC payment that no acquirer would willingly pay) in exchange for equity-linked upside that becomes valuable precisely when the company succeeds. If ZYNLONTA achieves the $600 million to $1 billion in peak US revenue that management projects, the warrants could be worth multiples of the CoC reduction. If the company stagnates, HCR still holds its royalty stream plus warrants that might expire worthless, but the alternative, an unexercisable $750 million clause, was not generating value either.

By converting fixed protection into equity optionality, HCR transformed itself from a passive creditor into an aligned equity participant. That alignment may prove more valuable than any contractual floor if ADC Therapeutics becomes an acquisition target. HCR would benefit from both the continued royalty stream and the appreciation of its warrant position.

Karyopharm: The Layered Restructuring

Karyopharm's May 2024 refinancing demonstrated a more complex integration of warrants into royalty restructuring. The company simultaneously addressed three capital structure problems: approaching convertible note maturities, an expensive royalty agreement with HCR, and the need for fresh secured debt.

The royalty component saw HCR receive a $49.5 million cash payment, a $15 million term loan note, and $5 million in new convertible notes in exchange for reducing the royalty rate on XPOVIO (selinexor) from a tiered schedule reaching 12.5% to a flat 7.0%. The warrant component appeared in the adjacent convertible note exchange: the top four holders of Karyopharm's 3.0% convertible notes due 2025 exchanged $148 million in principal for $111 million of new 6.0% convertible notes due 2029 plus warrants to purchase approximately 46 million shares at $1.10.

The warrants served as the inducement that made the exchange economically viable for noteholders being asked to accept a 25% haircut on principal. Without the equity kicker, no rational bondholder would voluntarily convert performing debt into less debt. The 46 million warrants at $1.10, representing substantial potential dilution, were the price Karyopharm paid to extend its maturity profile past the critical Phase 3 data readouts.

This layered structure illustrates how equity kickers have become load-bearing elements in pharmaceutical restructurings. Remove the warrants and the entire edifice collapses: noteholders refuse the exchange, maturities hit before data readouts, and the company faces potential bankruptcy, which would itself trigger consequences under the royalty agreement.

Why Royalty Investors Accept (and Demand) Warrants

Traditional royalty financing was built on a clean division. The investor provided capital in exchange for a fixed percentage of product sales, with no equity exposure and no governance rights. The entire return depended on commercial execution of a specific drug.

Three forces have disrupted this model.

First, the proliferation of change-of-control clauses that are nominally protective but practically unenforceable. A $750 million CoC payment against a $500 million market capitalisation is a theoretical protection that no acquirer will honour. As I discussed in Royalties That Wake Up, the La Jolla Pharmaceutical experience showed that even carefully drafted triggers can be structured around. Warrants offer a different kind of protection: instead of a binary trigger that may never fire, they provide continuous equity exposure that increases in value as the company's prospects improve.

Second, many commercial-stage biotechs now trade well below the valuations implied by their royalty agreements. When a company's stock trades at a fraction of the net present value of its product royalties, a pure royalty interest may be overexposed to execution risk with no participation in the equity recovery that would occur if the company navigates its challenges. Warrants give the royalty investor a call option on that recovery.

Third, the increasing complexity of pharmaceutical balance sheets, where royalty obligations interact with convertible notes, secured debt, ATM facilities, and equity kickers from prior financings, creates situations where royalty amendments are part of broader restructurings. In these contexts, warrants serve as fungible currency that can be allocated across creditor constituencies to build consent for the overall package.

The Cost of Capital Calculus

Understanding why warrants appear in certain structures requires comparing the true cost of capital across available alternatives. Covington & Burling's May 2025 overview catalogued the spectrum from venture lending through synthetic royalties to royalty monetisations, each involving different risk/return profiles and contractual restrictions.

The comparison:

| Financing Type | Cost to Company | Dilution | Revenue Requirement |

|---|---|---|---|

| Pure royalty monetisation | 8-15% implied yield | None | Strong, growing product sales |

| Royalty + warrant hybrid | 8-12% implied + equity | Moderate (5-10%) | Moderate product sales |

| Venture debt + warrants | 11-15% coupon + 2-8% coverage | Low-moderate | Any (covenant-driven) |

| Warrant inducement | 100% equity | Severe (2-3× multiplier) | None required |

The ADC Therapeutics amendment falls in the second category. HCR's willingness to accept warrants instead of maintaining the $750 million floor reflects a pragmatic understanding that a nominal protection which can never be enforced is worth less than a smaller, achievable claim paired with equity upside. The same logic applies in contexts where the underlying revenue base is structurally constrained, as I explored in the context of biosimilar royalty financing, where compressed margins and price erosion limit the economics available for pure royalty payments.

Accounting: Classification Determines Everything

Warrant accounting is a strategic variable, not a technicality. It can determine whether a company maintains listing compliance, how its financials present to acquirers, and whether the instruments create mark-to-market volatility in earnings.

Under ASC 815-40, the critical question is whether warrants qualify for equity classification or must be recorded as liabilities. Deloitte's March 2025 analysis noted that the SEC staff has observed "widespread diversity in practice" in how issuers evaluate whether warrant provisions preclude equity classification. The distinction turns on two sequential tests under ASC 815-40-15 and 815-40-25: first, whether the instrument is indexed to the entity's own stock; second, whether it meets the equity classification conditions. The most common disqualifier is a fundamental transaction provision giving holders the right to receive Black-Scholes value in cash upon certain corporate events.

Moleculin's February 2026 Series H warrants include exactly such a provision, almost certainly requiring liability classification. The warrants appear on the balance sheet at fair value with changes flowing through the income statement each quarter. The irony is acute: Moleculin undertook the December 2025 inducement specifically to boost stockholders' equity for Nasdaq compliance. But if new warrants require liability classification, they increase total liabilities, potentially undermining the very objective the transaction was designed to achieve. The company addressed this by simultaneously amending its earlier Series E and F warrants to reclassify them from liabilities to equity, removing the problematic provisions.

For warrants issued within royalty amendments, like those to HCR, the analysis differs. ADC Therapeutics is a Swiss corporation; its warrants are governed by Swiss law and include specific provisions around treasury stock and exercise mechanics that may affect classification under both US GAAP and IFRS. The lock-up through December 2027 reduces near-term volatility but does not affect classification.

The broader point for analysts: every warrant inducement or issuance requires careful analysis of the classification consequences. A headline reading "company raises $8 million through warrant exercise" may conceal a simultaneous increase in warrant liabilities of $15 million if the new warrants are marked to market at fair value exceeding intrinsic value.

Regulatory and Structural Guardrails

Nasdaq Pricing Rules

Nasdaq Rule 5635(d) requires stockholder approval for transactions issuing 20% or more of outstanding common stock below market price. New warrants are therefore often issued subject to stockholder approval, becoming exercisable only after affirmative vote. Both Moleculin's February 2026 Series H warrants and bioAffinity Technologies' inducement warrants followed this structure.

Additionally, Nasdaq requires that inducement warrant exercise prices be at least equal to the original exercise price. The SELLAS 8-K specifically noted holders exercised at their original prices "plus $0.125 per share in accordance with the rules and regulations of The Nasdaq Capital Market."

Standstill Provisions

Inducement agreements typically include 75-to-90-day blackouts on additional equity issuances and 12-month prohibitions on variable rate transactions (ATM facilities, equity lines of credit). For a company burning cash to fund clinical trials, a 12-month ATM restriction is a significant constraint that must be weighed against the immediate cash benefit.

In royalty contexts, lock-ups serve a different purpose. ADC Therapeutics' warrants to HCR include a lock-up through December 2027, not to prevent dilution, but to signal that HCR is a long-term aligned holder rather than a short-term trader.

Financial Advisor Fees

Placement agents, typically mid-market banks like Roth Capital Partners, A.G.P./Alliance Global Partners, Maxim Group, and Chardan, charge 5.75% to 7.0% of gross proceeds. On a $6.8 million Moleculin transaction, that consumes nearly $500,000, a significant percentage for a company using the proceeds to avoid delisting.

Market Data: 2024-2026 Transactions

| Company | Date | Gross Proceeds | Old Warrants | New Warrants | Multiplier | Advisor |

|---|---|---|---|---|---|---|

| SELLAS Life Sciences | Oct 2025 | $31.0M | 22,363,714 | 22,363,714 | 1.0× | AGP / Maxim |

| Moleculin Biotech | Feb 2026 | $8.3M | 2,122,652 | 6,367,956 | 3.0× | Roth Capital |

| Moleculin Biotech | Dec 2025 | $6.8M | 1,000,000 | 2,600,000 | 2.6× | Roth Capital |

| Moleculin Biotech | Feb 2025 | $5.8M | 5,800,000 | 11,700,000 | 2.0× | n/a |

| iBio | Apr 2025 | $6.2M | 5,626,685 | 11,253,370 | 2.0× | Chardan |

| bioAffinity Tech | Feb 2025 | $1.4M | 2,438,473 | 2,926,168 | 1.2× | WallachBeth |

| ZyVersa | Jul 2025 | $2.0M | 3,000,000 | 6,100,000 | 2.0× | n/a |

Warrants within royalty restructurings:

| Company | Royalty Investor | Date | Warrants Issued | Strike | Context |

|---|---|---|---|---|---|

| ADC Therapeutics | HealthCare Royalty | Feb 2026 | 9,834,776 | $3.81 | CoC reduction ($750M → $150-200M) |

| Karyopharm | Convertible holders / HCR | May 2024 | ~46,000,000 | $1.10 | Convertible exchange + royalty rate cut |

The two categories serve fundamentally different markets. Standalone inducements are concentrated in micro-cap biotechs with constrained financing alternatives. Royalty-linked warrants appear in mid-cap companies with substantial product revenue and sophisticated institutional counterparties. The instruments may be identical on paper, but their economic significance diverges completely.

Implications

For Companies

Companies with monetisable product revenue should generally prefer pure royalty financing, which preserves equity but dedicates product cash flows to the investor. The critical question for any company considering a warrant inducement is whether it breaks the cycle or perpetuates it. SELLAS used its $31 million to fund definitive clinical programmes with potential for inflection. Moleculin's serial inducements have generated cash without meaningfully changing the company's trajectory, creating a widening gap between dilution absorbed and value created.

For Royalty Investors

The ADC Therapeutics precedent opens a new dimension of deal structuring. The logical extension is bespoke structures where the initial royalty financing itself includes warrant components, effectively creating a hybrid between traditional royalty monetisation and venture lending. This would unlock transactions that neither pure royalty nor pure equity structures can reach: early-stage companies where product revenue alone cannot generate attractive royalty returns, or distressed situations where existing obligations need restructuring.

As I noted in the context of biosimilar royalty financing, the same economic forces that push companies with structurally declining revenue trajectories towards hybrid credit-plus-royalty structures could push a broader class of companies towards royalty-plus-warrant hybrids. When the product economics alone cannot support the investor's required return, equity optionality fills the gap.

For Acquirers

Any acquirer must now map the full landscape of equity-linked obligations, including warrants held by royalty investors. ADC Therapeutics' warrants include deemed-exercise provisions in M&A scenarios, meaning an acquirer would need to either assume the warrants or cash them out at Black-Scholes value. Under the amended agreement, an acquirer closing in 2028 would face a $200 million CoC payment to HCR plus the value of 9.8 million warrants (deemed exercised in an all-cash deal). If the stock has appreciated significantly, the warrant component could rival the CoC payment itself.

Conclusion

The warrant, a simple call option on the issuer's common stock, has emerged as a versatile instrument in pharmaceutical financing. At the distressed end it powers inducement transactions that keep companies alive long enough to reach their next milestone, often at devastating cost to existing shareholders. At the strategic end it serves as sophisticated amendment consideration that aligns royalty investors with equity outcomes.

The signalling value depends entirely on context. When HCR accepts warrants from ADC Therapeutics, the market reads confidence. When Moleculin issues its third inducement in twelve months, the market reads distress.

The Gibson Dunn Royalty Report documented $29.4 billion in life sciences royalty financings from 2020 to 2024, overwhelmingly structured as pure product-economics transactions with no equity component. If the market moves towards hybrid structures that combine royalty streams with warrant kickers, as the Covington and Goodwin analyses suggest is increasingly possible, the result will be a new asset class sitting between traditional royalty investing and healthcare venture lending.

The next time a commercial-stage biotech approaches its royalty counterparty for an amendment, the conversation will almost certainly include a new question: what's the warrant worth?

All information in this report was accurate as of the research date and is derived from publicly available sources including company press releases, SEC filings, regulatory announcements, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice.

Member discussion