The Weekly Term Sheet (2026-W10)

Visual Summary

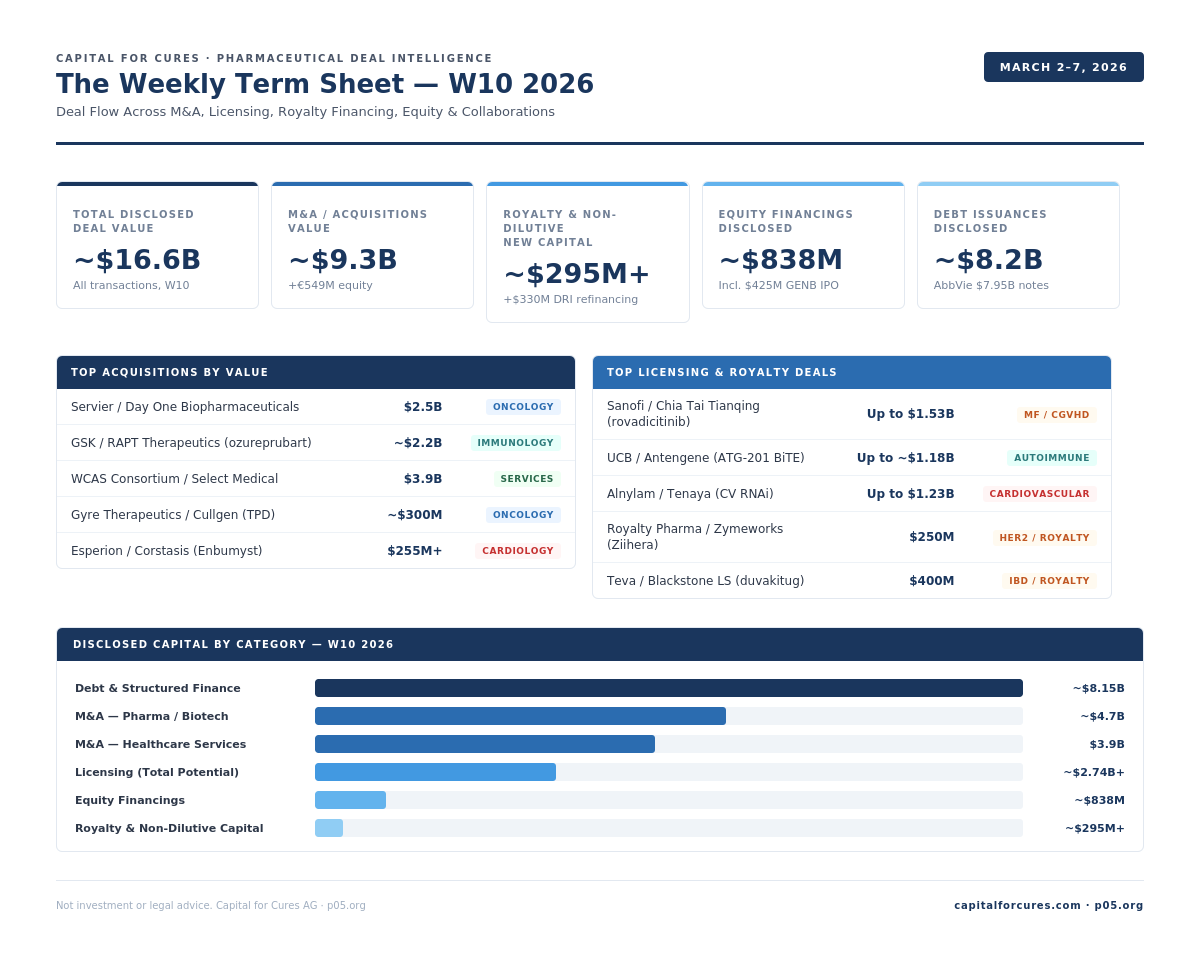

Week in Numbers: $16.6B total disclosed value, $9.3B M&A, $295M+ royalty and non-dilutive capital, $838M equity financings, $8.2B debt issuances

Royalty League Table: Seven royalty and non-dilutive financing transactions: Teva/Blackstone ($400M), Royalty Pharma/Zymeworks ($250M), Heidelberg/HCRx+Soleus ($45M), and DRI Healthcare ($330M+ refinancing)

M&A and Licensing League Tables: WCAS/Select Medical $3.9B through Esperion/Corstasis $255M+) and licensing ranking (Chia Tai Tianqing/Sanofi $1.53B through Pierre Fabre/Eton Pharma

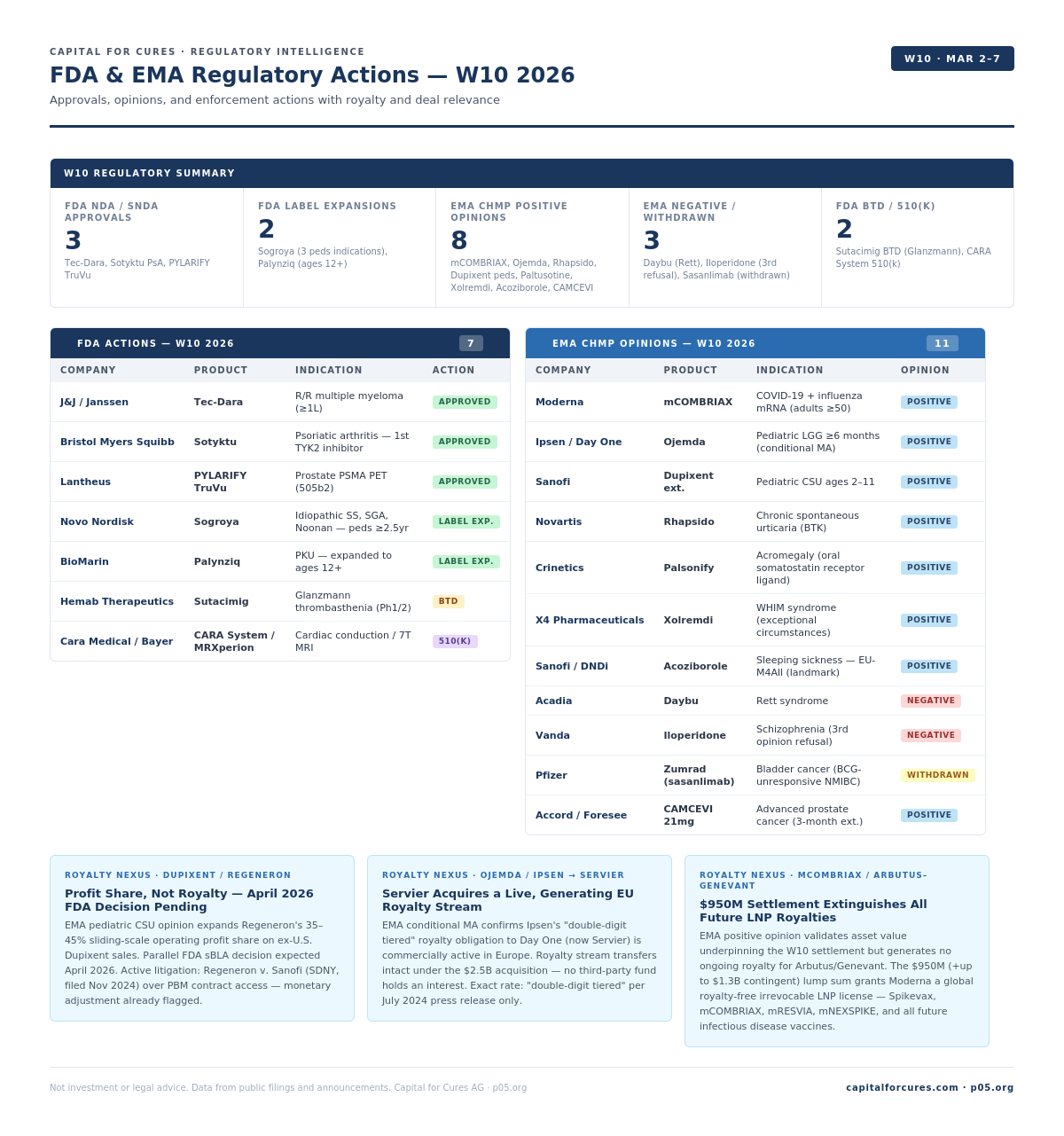

FDA and EMA Regulatory Overview: 3 FDA approvals, 2 label expansions, 8 EMA positive opinions, 3 EMA negative/withdrawn, 2 FDA BTD/510k)

Week in Review

Week 10 produced two transactions with direct implications for the pharmaceutical royalty and financing ecosystem: AstraZeneca's royalty monetization with Compugen for rilvegostomig surfacing in earnings disclosures, and Teva's $400M strategic growth capital agreement with Blackstone Life Sciences for duvakitug — the week's most direct example of a dedicated life sciences royalty investor providing development capital in exchange for a future royalty interest. Together they illustrate two sides of the royalty deal spectrum: monetising receivables during Phase 3, and creating new royalty obligations to fund pipeline advancement.

EMS/NC Group's $600M acquisition of Sanofi's Brazilian generics unit Medley (signed March 6) was the week's most significant Latin American pharmaceutical transaction and Sanofi's full exit from Brazilian generics. Other notable developments included UniQure's ~40% stock decline following FDA's rejection of its BLA filing plan for AMT-130, Novo Nordisk's €432M Irish factory expansion and its Hims & Hers platform deal (which sent Hims shares up ~40%), Bayer's $7.25B Roundup settlement receiving preliminary court approval, and DRI Healthcare's $330M+ in combined refinancing alongside a new $800M–$1B five-year deployment target against a ~$3B pipeline.

Total disclosed deal value this week: ~$16.6B

Feature: Moderna / Arbutus Biopharma–Genevant Sciences — Up to $2.25B LNP Patent Settlement

Moderna / Arbutus Biopharma–Genevant Sciences | Patent Settlement + License | LNP Delivery Technology | Platform | March 3, 2026

| Parameter | Detail |

|---|---|

| Announced | March 3, 2026 |

| Structure | Consent to judgment of infringement + global perpetual royalty-free license |

| Non-contingent payment | $950M lump sum, due July 8, 2026 |

| Contingent payment | $1.3B contingent on outcome of Moderna's Federal Circuit appeal (Section 1498 government-contractor immunity defense) |

| Total maximum | Up to $2.25B |

| Ongoing royalties | None — royalty-free license |

| Patents covered | U.S. 8,492,359; 9,364,435 (survived Moderna's IPR challenge at PTAB); 11,141,378; 9,504,651 (four LNP molar ratio / method patents) |

| Products licensed | Spikevax, mNEXSPIKE, mRESVIA, mCOMBRIAX, and all future infectious disease vaccines using SM-102 LNP |

| Proceeds allocation | Arbutus ~20% (net of litigation costs, subject to tiered low single-digit royalty cap; evaluating return of capital to shareholders in Q3 2026); Genevant/Roivant ~80% |

| Scope | Global, non-exclusive, perpetual, irrevocable |

| Court | Arbutus Biopharma Corp. v. Moderna Inc., D. Del., No. 22-cv-252; consent judgment issued March 4, 2026 |

| Arbutus legal counsel | Morrison & Foerster (Adam Brausa, Eric Wiener, Daralyn Durie); Shaw Keller LLP (Delaware local) |

| Genevant legal counsel | Williams & Connolly (David Berl, lead); Shaw Keller LLP (Delaware local) |

| Moderna legal counsel | Kirkland & Ellis (James Hurst, Jeanna Wacker); Morris, Nichols, Arsht & Tunnell (Delaware local) |

| Roivant capital return | $1.0B share buyback authorized post-settlement |

Announced March 3, 2026, this settlement resolves all worldwide LNP patent enforcement actions between Moderna and Arbutus/Genevant — potentially the largest disclosed patent settlement in pharmaceutical industry history. The original 2022 complaint asserted six patents; the case narrowed to four by trial, all covering LNP molar ratios and formulation methods. Moderna consented to judgment of infringement on all four, receiving in return a global, non-exclusive, perpetual, royalty-free license covering its entire infectious disease vaccine portfolio using SM-102 lipid nanoparticle technology. The consent judgment was issued March 4, 2026 by Judge Joshua Wolson (E.D. Pa., sitting by designation in D. Del.).

The $950M non-contingent payment is due July 8, 2026. The additional $1.3B is contingent on the outcome of Moderna's Federal Circuit appeal of the Section 1498 government-contractor immunity defense — a legal theory under which Moderna argued that its COVID-19 vaccine production, carried out under U.S. government contracts, was shielded from patent infringement claims. Judge Wolson ruled February 4, 2026 that Section 1498's "for the Government" language requires actual government benefit, not merely public benefit through patients, preserving Moderna's right to appeal. If the Federal Circuit affirms, the $1.3B is due within 90 days; if Moderna ultimately prevails, Arbutus/Genevant must refund the full amount plus interest. Moderna has recorded no accrual for this contingency.

The proceeds split is asymmetric: Arbutus receives approximately 20% of net settlement proceeds (after litigation costs), subject to a cap of tiered low single-digit royalties on net sales, while Genevant/Roivant receives approximately 80%. Roivant authorized a $1.0B share buyback following the announcement.

The elimination of ongoing royalties is commercially significant: Moderna had faced the prospect of paying royalties on all future SM-102 LNP-based vaccine sales — a potentially multi-billion-dollar long-term liability — in exchange for the lump-sum resolution. Arbutus and Genevant exchanged that royalty stream for immediate capital certainty. The structure is a clean royalty monetization in reverse: the royalty obligor (Moderna) paid to extinguish rather than the royalty holder selling forward.

Feature: AstraZeneca / Compugen Royalty Monetization — rilvegostomig

AstraZeneca / Compugen | Royalty Financing | Lung, GI, and Endometrial Cancers | Phase 3

| Parameter | Detail |

|---|---|

| Upfront | $65M |

| Additional milestone (BLA acceptance) | $25M |

| Total maximum disclosed | $90M |

| Royalty rate retained by Compugen | Up to mid-single digits (majority retained) |

| Remaining milestone eligibility | Up to $195M |

| Deal announced | December 17, 2025 |

| Earnings confirmation | March 2, 2026 |

The AstraZeneca/Compugen deal originally closed in December 2025 but came into focus this week through Compugen's Q4 2025 earnings disclosure on March 2, confirming receipt of the $65M upfront payment. The structure is a canonical royalty monetization: Compugen sold a small portion of its future royalty interest in rilvegostomig — AstraZeneca's PD-1/TIGIT bispecific — in exchange for non-dilutive upfront capital, while retaining the majority of the royalty stream and all future milestone eligibility.

Rilvegostomig is an Fc-reduced PD-1/TIGIT bispecific antibody currently advancing across 10 ongoing Phase 3 trials in patients with lung, gastrointestinal, and endometrial cancers. The TIGIT component derives from Compugen's wholly owned COM902 antibody, licensed to AstraZeneca under a 2018 agreement. For Compugen, the transaction extended the expected cash runway to 2029 with no debt incurred, and the company turned profitable in 2025 — reporting $72.8M in full-year revenues versus $27.9M in 2024 — largely on the back of the AstraZeneca payment and earlier Gilead license fees.

The deal is structurally notable for the retained economics. Compugen gave up a minority slice of royalty flow to access immediate capital during Phase 3, rather than monetizing the entire royalty interest. As rilvegostomig approaches potential approval and commercialization, the residual royalty position could represent significant value — the company separately holds up to $758M in milestones from its Gilead partnership for GS-0321.

The term sheet value cited in the source data ($260M total) appears to reflect an estimate of broader royalty value rather than the $90M maximum disclosed in the official agreement. The $65M upfront and up to $195M in future milestones are the confirmed contractual figures.

Royalty Financing: Teva / Blackstone Life Sciences — duvakitug | $400M

Teva Pharmaceuticals / Blackstone Life Sciences | Royalty Financing / Strategic Growth Capital | Inflammatory Bowel Disease (Ulcerative Colitis, Crohn's Disease) | Phase 3

| Parameter | Detail |

|---|---|

| Announced | March 3, 2026 |

| Financing amount | $400M, disbursed over four years |

| Funder | Blackstone Life Sciences (BXLS) |

| Asset | Duvakitug (TEV-'574 / SAR447189), anti-TL1A human monoclonal antibody |

| Indications | Ulcerative colitis (SUNSCAPE-1), Crohn's disease (STARSCAPE-1) |

| Phase 3 enrollment | >3,000 patients combined; follow-up up to 40 weeks |

| Phase 3 completion | SUNSCAPE-1 (UC): expected 2028; STARSCAPE-1 (CD): expected 2029 |

| BXLS consideration | FDA-approval milestone (undisclosed size) + commercial milestones + low single-digit royalties on worldwide net sales |

| Royalty rate | Low single-digit (global, all territories) |

| Co-development partner | Sanofi (separate October 2023 agreement; equal cost/P&L share in major markets; Sanofi leads Phase 3 and North America/Asia commercialization; Teva leads Europe/Israel) |

| Sanofi upfront to Teva (2023) | €469M (~$500M) |

| Sanofi milestones to Teva (2023) | Up to €940M (~$1B) in development and launch milestones |

| Phase 2b LTE data | Reported February 17, 2026: 58% UC patients, 55% CD patients in clinical remission at 44 weeks maintenance |

| Key BXLS spokespeople | Paris Panayiotopoulos, Senior Managing Director, BXLS; Dr. Nicholas Galakatos, Global Head, BXLS |

| Key Teva spokesperson | Evan Lippman, EVP Business Development, Teva |

| BXLS legal counsel | Ropes & Gray LLP |

| Teva legal counsel | Not disclosed |

| Financial advisors | Not disclosed |

Announced March 3, 2026, Teva's agreement with Blackstone Life Sciences provides $400M in four-year staged funding to cover ongoing and future duvakitug development costs, in exchange for a contingent FDA-approval milestone payment, additional commercial milestones, and low single-digit royalties on worldwide net sales. Ropes & Gray LLP acted as legal counsel to Blackstone Life Sciences — consistent with the firm's standing role advising BXLS on its life sciences financing transactions, having also represented BXLS on its Moderna and Alnylam growth capital agreements. Teva's legal counsel and any financial advisors were not disclosed in the public announcement.

The asset: duvakitug and TL1A biology

Duvakitug is a fully human monoclonal antibody targeting TL1A (TNF-like cytokine 1A, also called TNFSF15), a member of the TNF superfamily expressed primarily by macrophages, dendritic cells, and endothelial cells in inflamed tissue. TL1A drives both inflammatory and fibrotic pathways in the intestinal wall through its receptor DR3 (Death Receptor 3), which is expressed on T cells, innate lymphoid cells, and stromal cells. The dual mechanism distinguishes TL1A inhibition from anti-TNF, IL-12/23, and gut-selective integrin therapies, which primarily suppress inflammatory cascades but have limited impact on the fibrotic process that drives stricturing disease, obstruction, and surgical intervention.

In Phase 2b, duvakitug at 900mg demonstrated clinical remission in 58% of UC patients and 55% of CD patients at the end of a 44-week maintenance period — durability data reported February 17, 2026, two weeks before the Blackstone financing. Phase 3 comprises two studies: SUNSCAPE-1 (ulcerative colitis, expected data 2028) and STARSCAPE-1 (Crohn's disease, expected data 2029), together enrolling over 3,000 patients.

The competitive TL1A landscape

Duvakitug is not alone in Phase 3. Merck & Co. acquired tulisokibart via its $10.8B purchase of Prometheus Biosciences in 2023 and expects Phase 3 data later in 2026. Roche's afimkibart, acquired as part of a $7B deal for Telavant, is also in pivotal testing.

AbbVie is developing an additional TL1A program. The class is therefore crowded at the most critical juncture, and payer positioning — step therapy placement relative to anti-TNF, IL-23, JAK inhibitors, and gut-selective agents — will depend heavily on head-to-head data or differentiated trial design that Phase 3 may or may not deliver.

The prior Sanofi collaboration and the stacked royalty architecture

In October 2023, Sanofi paid €469M (~$500M) upfront to co-develop and co-commercialize duvakitug globally, with up to €940M in additional development and launch milestones to Teva. The agreement splits global development costs equally, shares major-market net P&L on a 50/50 basis, and designates Sanofi as Phase 3 lead and North American/Asian commercial lead, with Teva leading European and Israeli commercialization. Non-major markets operate under a separate royalty arrangement between Teva and Sanofi.

The BXLS low single-digit global royalty now sits on top of this co-commercialization structure. Blackstone's royalty runs on worldwide net sales regardless of territory, meaning it applies across both the Sanofi-led and Teva-led commercial geographies simultaneously. The combined effect is a layered royalty burden: in North American and Asian markets, Sanofi's 50/50 P&L split and Teva's royalty obligation to BXLS both reduce Teva's net economic participation; in European and Israeli markets where Teva leads commercialization, the BXLS global royalty still applies as a first claim on revenue.

Analysts have flagged that this stacked structure compresses net pricing power in formulary negotiations, particularly against IL-23 inhibitors that reach the market with lighter royalty stacks. The undisclosed size of the FDA-approval milestone owed to BXLS adds a further contingent capital commitment at the point of regulatory success.

BXLS's strategic pattern

Blackstone Life Sciences has signed structurally similar development capital agreements with Moderna, Alnylam Pharmaceuticals, and Autolus Therapeutics — a pattern of providing staged research and development funding to Phase 3-stage assets in exchange for royalties and milestone-linked returns rather than equity ownership. The model functions as a hybrid between venture lending and royalty acquisition, providing pharmaceutical companies with non-dilutive capital while creating royalty-like economic exposure for the investor without requiring asset ownership. The Teva/duvakitug transaction extends this model to a co-commercialized asset, creating a three-party royalty structure: BXLS (global royalty), Sanofi (major-market P&L split), and Teva (residual after both).

The duvakitug deal is Teva's second consecutive non-dilutive pipeline financing in early 2026. In January 2026, Teva secured up to $500M from Royalty Pharma to fund the clinical development of TEV-'408, an anti-IL-15 monoclonal antibody in Phase 2 for celiac disease and Phase 1b for vitiligo. The back-to-back transactions — Royalty Pharma in January, BXLS in March — reflect Teva's stated "Pivot to Growth" capital strategy: funding Phase 2 and Phase 3 pipeline advancement through royalty-based and growth capital instruments rather than equity dilution or balance sheet drawdown. Both deals create royalty obligations that will sit above Teva's net sales economics if either asset reaches market.

Acquisitions

| # | Acquirer | Target / Asset | Value | Type | Stage | Date |

|---|---|---|---|---|---|---|

| 1 | Servier | Day One Biopharmaceuticals (Ojemda + pipeline) | $2.5B | Cash tender offer | Marketed / Ph 3 | March 6 |

| 2 | Rallybio | Candid Therapeutics (T-cell engager platform) | Undisclosed + CVR | Reverse merger + financing | Ph 1 / Ph 2 | March 3 |

| 3 | Gyre Therapeutics | Cullgen (protein degradation platform) | ~$300M all-stock | All-stock | Clinical | March 2 |

| 4 | Esperion | Corstasis (Enbumyst) | $75M upfront + up to $180M milestones + royalties | Cash + royalty obligation | Marketed | March 3 |

| 5 | GSK | RAPT Therapeutics (ozureprubart) | ~$2.2B (~$1.9B net cash) | Cash tender offer completion | Ph IIb | March 3 |

| 6 | RadNet / DeepHealth | Gleamer SAS (radiology AI) | Up to €230M | Cash + milestone | Marketed | March 2 |

| 7 | WCAS Consortium | Select Medical Holdings | $3.9B | Take-private | Commercial | March 2 |

| 8 | Grünenthal | Kyowa Kirin International EMEA JV stake | Undisclosed | Stake buyout | Commercial | March 2 |

| 9 | Intuitive Surgical | ab medica / Abex / Excelencia Robótica | ~€319M | Completion | Commercial | March 1–2 |

| 10 | Sectra | Oxipit (chest X-ray AI) | Undisclosed | Acquisition | Marketed | March 2026 |

| 11 | BioSyent | Oral Science | $25.5M + up to $6M contingent royalties | Cash + equity + royalty | Commercial | March 2 |

| 12 | VERAXA Biotech | Voyager Acquisition Corp. | Undisclosed | SPAC shareholder approval | Clinical | W10 |

Section total (disclosed values): ~$9.3B cash/equity + €549M + undisclosed elements. Servier/Day One ($2.5B) and GSK/RAPT (~$2.2B) account for ~$4.7B of disclosed pharma deal value. Select Medical ($3.9B) is healthcare services.

Royalty notes: Servier/Day One carries a layered royalty structure (mid-teens Ipsen receivable ex-U.S. inbound; undisclosed Takeda liability on U.S. sales outbound). BioSyent/Oral Science carries a seller-retained contingent royalty capped at $6M through 2033 on one undisclosed product (rate not disclosed). GSK/RAPT: no royalty obligation disclosed; Esperion/Corstasis: Otsuka Japan royalty (15–30% tiered) being monetized via Athyrium/HCRx to finance acquisition; Corstasis sellers receive low double-digit royalties on worldwide Enbumyst net sales going forward.

Acquisition: Servier / Day One Biopharmaceuticals — Ojemda + Oncology Pipeline | $2.5B

Servier / Day One Biopharmaceuticals | Acquisition (Cash Tender Offer) | Pediatric Low-Grade Glioma, Rare Oncology (Adult and Pediatric) | Marketed / Phase 3 | March 6, 2026

| Parameter | Detail |

|---|---|

| Announced | March 6, 2026 |

| Deal value | $2.5B (total equity value) |

| Price per share | $21.50 per share, all-cash |

| Premium to last close (March 5, 2026) | ~68% |

| Premium to 1-month VWAP (March 5, 2026) | ~86% |

| Structure | Cash tender offer; second-step merger for any untendered shares at same consideration |

| Closing conditions | Majority tender of DAWN shares; U.S. antitrust (HSR) clearance |

| Expected close | Q2 2026 |

| Financing | Servier existing cash and investments (no financing condition) |

| Servier advisors | Goldman Sachs Bank Europe SE (financial); Baker McKenzie (legal) |

| Day One advisors | Centerview Partners LLC (financial); Fenwick & West LLP (legal) |

| Day One ticker | NASDAQ: DAWN |

Announced March 6, 2026, Servier's acquisition of Day One Biopharmaceuticals is the largest biopharma deal announced this week, and the most significant oncology acquisition by a European private pharmaceutical company in recent years. Servier is a French foundation-governed group with €6.9 billion in revenues in the 2024/25 financial year, more than 20,000 employees, and medicines distributed across 130 countries. Despite its scale, it is privately held and foundation-governed — not publicly traded — making its deployment of $2.5 billion in existing balance sheet cash a significant strategic commitment to its oncology build.

The deal centerpiece is Ojemda (tovorafenib), a RAF kinase inhibitor that received FDA approval in April 2024 as the first oral, once-weekly targeted therapy for relapsed or refractory pediatric low-grade glioma (pLGG). pLGG is the most common form of brain cancer in children and adolescents; BRAF alterations — either the BRAF V600E mutation or BRAF fusions — drive approximately 50% of cases and have historically lacked approved oral targeted options. Ojemda's approval was based on the FIREFLY-1 Phase 2 study, which demonstrated a 67% overall response rate by independent review in BRAF-altered pLGG. The FDA granted Priority Review and Rare Pediatric Disease designation; a Pediatric Priority Review Voucher was awarded at approval.

Beyond Ojemda, the acquisition captures the pipeline assets Day One assembled through its January 2026 acquisition of Mersana Therapeutics: most notably XMT-2056, an antibody-drug conjugate targeting HER2 in advanced solid tumors, which entered Phase 1 in 2024 and represents a differentiated ADC payload mechanism. Day One's full pipeline spans early stage through Phase 3, with programs covering both pediatric and adult rare cancers — a strategic fit with Servier's stated 2030 objective of building leadership in rare oncology targeted therapies.

The premium — 68% to last close, 86% to the 30-day VWAP — is consistent with control premiums in competitive rare disease oncology acquisitions and reflects both the near-term commercial ramp of Ojemda and the option value in the broader pipeline. DAWN shares rose approximately 65% on announcement day, confirming a clean arb setup for the cash tender.

Goldman Sachs Bank Europe SE acted as exclusive financial advisor to Servier, with Baker McKenzie as legal counsel. Centerview Partners served as Day One's exclusive financial advisor, with Fenwick & West LLP as legal counsel.

Royalty Architecture

The Servier/Day One transaction carries a layered royalty structure that is material to understanding the deal's economics. Servier is simultaneously acquiring a royalty receivable and assuming a royalty liability — two flows running in opposite directions through the same asset.

Downstream — Ipsen royalty receivable (ex-U.S.): In July 2024, Day One licensed all ex-U.S. commercialization rights for tovorafenib to Ipsen for $111M upfront (including a $40M equity investment), up to $350M in milestone payments, and tiered double-digit royalties starting at mid-teens percentage on net sales. The royalty obligations run on a country-by-country basis for no less than ten years from first commercial sale in each territory. Servier acquires this receivable in full — Ipsen will pay mid-teens royalties on every dollar of ex-U.S.

Ojemda revenue directly to Servier going forward. The timing is favorable: Ojemda received a positive CHMP opinion from the EMA in February 2026, meaning the European royalty stream is about to become commercially live, potentially in the months immediately following deal close. No third-party royalty fund (Royalty Pharma, HCRx, OMERS, DRI Healthcare, or similar) holds a purchased interest in this stream — Day One never monetized the Ipsen receivable, so it transfers to Servier intact.

Upstream — Takeda royalty liability (U.S.): Tovorafenib was originally discovered in a Sunesis Pharmaceuticals / Biogen Idec collaboration that later expanded to include Millennium Pharmaceuticals, a Takeda affiliate. Day One acquired Takeda's rights in the compound in 2020 under a license from Takeda Oncology. That license almost certainly carries upstream royalty obligations on U.S.

Ojemda net sales payable back to Takeda — and potentially residual obligations to Biogen's successors or former Sunesis holders. The specific rate has never been publicly disclosed. Servier assumes these upstream obligations with the acquisition.

Industry analysts flagged this liability at the time of Ojemda's FDA approval: the exact royalty owed to Biogen, Takeda, Viracta, and/or former Sunesis holders remains an open question, and the molecule's lengthy pre-commercialization development history means multiple parties may hold a claim on the revenue stack. The net economic spread — mid-teens ex-U.S. inbound from Ipsen, offset by an undisclosed upstream rate outbound to Takeda on U.S. sales — is a key variable in Servier's actual Ojemda return on invested capital that the $2.5B headline does not surface.

Acquisition / Reverse Merger: Rallybio / Candid Therapeutics — T-Cell Engager Autoimmune Platform

Rallybio Corporation / Candid Therapeutics | Acquisition / Reverse Merger + Concurrent Financing | Autoimmune Diseases (Myasthenia Gravis, ILD, SLE, RA, and others) | Phase 1 / Phase 2

| Parameter | Detail |

|---|---|

| Announced | March 2, 2026 |

| Structure | All-stock reverse merger (Rallybio acquires Candid) |

| Concurrent financing | >$505M (oversubscribed and upsized) |

| Pro-forma cash at close | ~$700M |

| Runway | Through 2030 |

| Expected close | Mid-2026 |

| Post-merger name | Candid Therapeutics, Inc. |

| Post-merger ticker | NASDAQ: CDRX |

| Ownership split | Candid/new investors ~96.35%; legacy Rallybio ~3.65% |

| Rallybio CVRs | Tied to proceeds from legacy asset monetization (REV102 + others) |

| Key investors | RA Capital Management, Venrock Healthcare Capital Partners, Cormorant Asset Management, Foresite Capital, Janus Henderson Investors |

| Candid advisors | Wedbush Securities (financial); Cooley LLP (legal) |

| Rallybio advisors | Evercore (lead financial); Citizens Capital Markets & Advisory (co-financial); Ropes & Gray LLP (legal) |

| Placement agents ($505M financing) | Jefferies, BofA Securities, TD Cowen, Cantor Fitzgerald |

| Placement agent legal counsel | Latham & Watkins LLP |

Announced March 2, 2026, the Rallybio/Candid transaction is a classic reverse merger used to take a well-funded private clinical-stage company public: Rallybio (NASDAQ: RLYB), a New Haven-based rare disease biotech with a diminished pipeline following the Phase 2 failure of its lead FNAIT program in 2024, serves as the public shell, while Candid — the clinical and commercial substance — survives as the operating entity under its own name. The exchange ratio is determined by relative valuations at closing. The mechanics leave Rallybio stockholders with 3.65% of the combined company plus CVRs linked to monetization of legacy Rallybio assets; the remaining 96.35% accrues to Candid shareholders and the new financing round participants.

The concurrent $505M private financing was oversubscribed and upsized, with a syndicate of prominent healthcare institutional investors and mutual funds. The combined pro-forma cash position of approximately $700M is intended to fund operations through 2030, covering multiple Phase 2 readouts and pipeline advancement across Candid's T-cell engager (TCE) portfolio.

What Candid brings: T-cell engagers for autoimmune disease

Candid Therapeutics is a San Diego-based company that has assembled what it describes as the most advanced and diversified TCE pipeline in autoimmune disease. T-cell engagers are bispecific antibodies engineered to physically bridge a T cell (typically via a CD3-binding arm) to a pathogenic target cell, redirecting cytotoxic T-cell activity against disease-driving B cells or plasma cells — an approach that has proven transformative in hematologic oncology and is now being applied systematically to autoimmune disease. Candid's assets were acquired via two deals with Chinese biotechnology firms in 2024, giving the company a China-originated but globally rights-held portfolio.

The lead asset, cizutamig, is a BCMA-directed TCE. BCMA (B-cell maturation antigen) is expressed on long-lived plasma cells, which are the primary source of pathogenic autoantibodies in diseases such as myasthenia gravis, systemic lupus erythematosus, and IgG4-related disease. By depleting BCMA-expressing plasma cells, cizutamig aims to eliminate the autoantibody-producing cells responsible for disease maintenance.

With 87 total patients dosed including 47 autoimmune patients across more than 10 indications, cizutamig has demonstrated favorable tolerability with low rates of mild cytokine release syndrome. Phase 2 studies in myasthenia gravis and interstitial lung disease are planned for 2026.

CND261 is a CD19-directed TCE targeting B cells upstream of plasma cell differentiation, with initial clinical data expected in the first half of 2026. CND319 is a dual CD19/CD20 TCE designed to reduce antigen escape through dual B-cell surface targeting, with Phase 1 planned for mid-2026. CND460 is a preclinical dual BCMA/CD19 TCE expected to enter the clinic in the first half of 2027.

The autoimmune TCE space is rapidly crowding — Cullinan Therapeutics' CLN-978 (CD19 TCE) is approaching Phase 1 data in rheumatoid arthritis and SLE in 2026, and multiple other companies are pursuing overlapping targets. Candid's differentiation lies in the breadth of the pipeline, the clinical head start of cizutamig with data across a wide indication set, and the $700M capitalization enabling simultaneous multi-indication development.

The deal is included here for completeness as a major structural transaction in the autoimmune biologics space. It does not carry direct royalty financing implications at announcement, though the CVR structure for Rallybio legacy asset monetization (including REV102 rights) adds a royalty-adjacent element for legacy shareholders.

Acquisition: Gyre Therapeutics / Cullgen — Targeted Protein Degradation Platform | ~$300M All-Stock

Gyre Therapeutics / Cullgen | Acquisition | Fibrosis, Oncology, Pain | Clinical-Stage

| Parameter | Detail |

|---|---|

| Deal value | ~$300M (all-stock) |

| Structure | Tax-free reorganization; Cullgen becomes wholly owned subsidiary |

| Consideration | Gyre common stock + new Series B Convertible Preferred Stock (5:1 conversion ratio to common, post-stockholder approval; individual ownership capped below 19.99%) |

| Seller | Cullgen Inc. (privately held, San Diego) |

| Acquirer | Gyre Therapeutics, Inc. (Nasdaq: GYRE) |

| Leadership change | Cullgen CEO Dr. Ying Luo becomes President and CEO of combined company; Ping Zhang remains Executive Chairman; two Gyre directors resign at close |

| Regulatory conditions | HSR review; Cullgen stockholder approval; NYSE (GYRE) stockholder approval for share issuance |

| Expected close | Early Q2 2026 |

| Financial advisor | None disclosed |

| Announced | March 2, 2026 |

Gyre Therapeutics, a commercial-stage fibrosis-focused biopharma with $105.8M in 2024 net sales from ETUARY (pirfenidone) in China and a Hydronidone NDA approaching submission for CHB-associated liver fibrosis, agreed on March 2 to acquire Cullgen in a $300M all-stock deal. The transaction ends a prior reverse-merger agreement between Cullgen and Pulmatrix (terminated prior to signing) and delivers Cullgen's targeted protein degradation (TPD) and degrader-antibody conjugate (DAC) platform into Gyre's pipeline.

Cullgen's lead clinical asset is CG001419, an oral pan-TRK protein degrader targeting acute pain (post-bunionectomy Phase 2 planned for H1 2026) and solid tumors (Phase 1 ongoing). A second clinical-stage asset is a GSPT1 degrader for blood cancers. The DAC platform represents an emerging modality combining targeted degradation with antibody-directed delivery, extending the therapeutic scope well beyond Gyre's existing fibrosis franchise.

The combined entity will operate with U.S.- and China-based capabilities spanning discovery, manufacturing, and commercialization across inflammatory diseases, oncology, and pain. The all-stock structure preserves Gyre's cash for integration and pipeline investment. The Series B preferred share mechanism — designed to stay below 19.99% common stock issuance before stockholder conversion approval — is a standard structural solution for deals where dilution limits require bridging.

Acquisition: Esperion Therapeutics / Corstasis Therapeutics — Enbumyst | $255M + Royalties | CHF

Esperion Therapeutics / Corstasis Therapeutics | Acquisition | Edema / Congestive Heart Failure, Hepatic and Renal Disease | Marketed

| Parameter | Detail |

|---|---|

| Announced | March 3, 2026 |

| Upfront | $75M cash |

| Milestones | Up to $180M (regulatory and commercial) |

| Royalties to sellers | Low double-digit on worldwide Enbumyst sales and follow-on products |

| Total potential value | Up to $255M + ongoing royalties |

| Expected close | Q2 2026 |

| Esperion advisor | Jefferies LLC (financial); Gibson, Dunn & Crutcher LLP (legal) |

| Corstasis advisor | PJT Partners (financial); Arnold & Porter Kaye Scholer LLP (legal) |

| Financing | Esperion existing credit facilities + royalty monetization of Japanese bempedoic acid royalties via Athyrium Capital Management and HealthCare Royalty (KKR) |

| Japanese royalty payer | Otsuka Pharmaceutical Co., Ltd. (Japan-exclusive commercialization rights holder for NEXLETOL/NEXLIZET) |

| Japan royalty rate (underlying) | 15–30% tiered on net sales in Japan |

Announced March 3, 2026, Esperion Therapeutics (NASDAQ: ESPR) agreed to acquire all outstanding stock of Corstasis Therapeutics, a privately held commercial-stage company based in Henderson, Nevada, adding Enbumyst (bumetanide nasal spray) to its cardiovascular franchise. Enbumyst received FDA approval in September 2025 as the first and only nasal spray loop diuretic approved for edema associated with congestive heart failure, hepatic disease, and renal disease in adults. The stock fell 13.1% on announcement day, reflecting market skepticism about the cost of monetizing a newly commercial royalty stream to fund the deal.

Enbumyst: the clinical rationale

Loop diuretics — of which bumetanide is one — are the cornerstone of fluid management in heart failure, but existing delivery routes each have a meaningful limitation. Oral bumetanide and furosemide suffer from erratic gastrointestinal absorption in decompensated patients, precisely because gut wall edema impairs uptake when it is most needed. Intravenous administration is reliably effective but requires hospital or infusion center access, driving a significant proportion of CHF hospitalizations — patients who are fluid-overloaded at home but cannot achieve therapeutic diuresis orally cycle into the hospital for IV treatment and are discharged once stable.

Intranasal delivery bypasses the gut entirely, achieving faster and more consistent absorption than oral while remaining self-administered at home. Corstasis is also advancing a subcutaneous multidose pen injector pipeline as a further option for patients who cannot reliably self-administer nasal spray. Esperion cites a U.S. addressable market exceeding $4.6 billion, anchored by approximately 6.7 million American adults living with CHF.

The Otsuka Japan royalty stream — background

Otsuka is not the acquirer; it is the entity whose royalty payments to Esperion are being monetized to finance the deal. In April 2020, Esperion granted Otsuka Pharmaceutical Co., Ltd. exclusive rights to develop and commercialize NEXLETOL (bempedoic acid) and NEXLIZET (bempedoic acid/ezetimibe) in Japan, receiving a $60M upfront payment, up to $450M in development and sales milestones, and tiered royalties of 15–30% on all net sales in Japan. Otsuka was responsible for all Japan-specific development costs, regulatory submissions, and commercialization activities.

NEXLETOL received Japanese Ministry of Health, Labour and Welfare approval in September 2025 — just months before the Corstasis deal — with National Health Insurance pricing following shortly after. Otsuka deployed a dedicated field force of 600–800 sales representatives to support the launch. The Japan royalty stream was therefore brand new at the time Esperion chose to monetize it: commercially live for only a matter of months, with the full revenue ramp still ahead.

Athyrium Capital Management and HealthCare Royalty — who they are

Athyrium Capital Management is a New York-based specialized healthcare asset manager founded in 2008, with over $4.6 billion in committed capital. Athyrium invests across healthcare verticals — biopharma, medical devices, healthcare services, health IT — and across the capital structure, including royalties, structured debt, and equity. It has been an active participant in royalty monetization transactions for mid-cap commercial-stage biotechs, providing lump-sum liquidity against future royalty receivables in exchange for the right to collect those cash flows up to a negotiated return threshold, after which flows revert to the originator.

Athyrium's participation here signals the transaction was sized and structured as a conventional royalty purchase agreement layered on top of Esperion's existing credit facilities rather than a pure debt instrument.

HealthCare Royalty (HCRx) is a Greenwich, Connecticut-based royalty acquisition firm founded in 2006, majority owned by KKR & Co. (NYSE: KKR). HCRx has committed over $7 billion across more than 100 transactions in commercial-stage and near-commercial-stage biopharmaceutical royalties. It is one of the three dominant dedicated royalty acquirers in the life sciences space alongside Royalty Pharma and OMERS Life Sciences (which separately holds Esperion's European royalty stream monetized in July 2024 in a $304.7M transaction).

The co-participation of Athyrium and HCRx in the Japan monetization suggests the deal was either syndicated across both vehicles or structured as a co-investment — consistent with how larger royalty monetization facilities are often assembled when the underlying asset is a single-country royalty stream requiring diversification of funder exposure.

The circular royalty economy — one transaction, four layers

This deal is structurally notable for compressing the full pharmaceutical royalty lifecycle into a single announcement:

- Esperion holds a royalty receivable from Otsuka on Japan bempedoic acid net sales (15–30% tiered, newly commercial as of late 2025)

- Esperion monetizes a portion of that receivable to Athyrium/HCRx today, receiving a present-value lump sum in exchange for future Japan royalty cash flows up to an agreed return threshold

- Esperion deploys that lump sum as the $75M acquisition payment for Corstasis

- Corstasis shareholders receive in return low double-digit royalties on worldwide Enbumyst net sales going forward

The acquirer simultaneously holds a royalty receivable (Japan), converts it to present value via a royalty purchase, deploys the proceeds as acquisition currency, and creates a new royalty obligation to the sellers — all in one transaction. The Japan royalty stream is the collateral, the repayment mechanism, and the enabling instrument. The market's 13% negative reaction on announcement day likely reflects the cost of selling a newly-launched, high-potential royalty stream at early-commercial multiples to fund an acquisition in an adjacent but unproven indication, combined with the new ongoing royalty obligation to Corstasis shareholders reducing future Enbumyst free cash flow.

Acquisition Completion: GSK / RAPT Therapeutics — ozureprubart | ~$2.2B | Atopic Dermatitis / Food Allergy

GSK / RAPT Therapeutics | Acquisition Completion | Atopic Dermatitis; Food Allergy | Phase IIb | March 3, 2026

| Parameter | Detail |

|---|---|

| Transaction type | Tender offer completion — previously announced January 20, 2026 |

| Acquirer | GSK plc (LSE/NYSE: GSK) |

| Target | RAPT Therapeutics, Inc. (Nasdaq: RAPT) — delisted March 3, 2026 |

| Price | $58.00 per share (cash) |

| Equity value | ~$2.2B |

| Net of cash | ~$1.9B |

| Shares tendered | ~93% as of offer expiration |

| Delisting | Nasdaq; RAPT common stock ceased trading March 3, 2026 |

| Key asset | Ozureprubart (RPT193), long-acting anti-IgE monoclonal antibody |

| Mechanism | Anti-IgE; similar class to omalizumab (Xolair) but engineered for extended half-life and subcutaneous dosing at infrequent intervals |

| Lead indication | Food allergy prophylaxis (Phase IIb; data expected 2027) |

| Additional indication | Atopic dermatitis (Phase IIb) |

| Differentiation vs. omalizumab | Longer dosing interval (potential quarterly dosing vs monthly); designed for higher-affinity IgE suppression at lower doses |

| Strategic rationale | Bolt-on to GSK's immunology/allergy franchise; anti-IgE represents a validated mechanism; food allergy is an unmet need with no approved prophylactic oral or injectable agent |

| Original announcement | January 20, 2026 |

| Close | March 3, 2026 |

GSK closed its acquisition of RAPT Therapeutics on March 3, 2026, following a tender offer in which approximately 93% of shares were tendered at $58.00 per share. The transaction was originally announced January 20, 2026 and closed in approximately six weeks — a fast timeline consistent with the absence of major antitrust concerns and the straightforward structure of a cash tender offer for a clinical-stage company with no marketed products.

The strategic rationale centers on ozureprubart, a long-acting anti-IgE monoclonal antibody in Phase IIb for food allergy prophylaxis and atopic dermatitis. Anti-IgE is a validated mechanism — omalizumab (Xolair, Novartis/Genentech) has been approved since 2003 for allergic asthma and is now approved for IgE-mediated food allergies (2024) — but ozureprubart is engineered for a substantially extended dosing interval, potentially enabling quarterly subcutaneous administration versus the monthly schedule of omalizumab. If Phase IIb data in food allergy are positive (expected 2027), GSK would have a best-in-class convenience profile in a market where the approved Xolair label was only expanded in 2024. Food allergy affects approximately 32 million Americans, and there is no disease-modifying oral or injectable prophylactic agent approved beyond the omalizumab indication.

The $2.2B price tag for a Phase IIb-stage asset reflects both the validated mechanism and the scarcity value: the anti-IgE space is small, RAPT was the most advanced independent player, and GSK paid for optionality across two indications (food allergy and atopic dermatitis) with a single differentiated molecule.

Acquisition: RadNet / Gleamer SAS — Radiology AI, €230M | Digital Health / AI Imaging | Marketed

RadNet / Gleamer SAS | Acquisition | Radiology AI / Chest X-Ray, Thoracic CT | Marketed | March 2, 2026

| Parameter | Detail |

|---|---|

| Announced | March 2, 2026 |

| Deal value | Up to €230M, all-cash (including post-closing milestone) |

| Structure | Acquisition of 100% of Gleamer SAS; integration into RadNet's DeepHealth subsidiary |

| Target HQ | Paris, France |

| Acquirer | RadNet, Inc. (NASDAQ: RDNT), Woodland Hills, California |

| Customer base | Gleamer serves radiologists and radiology groups globally |

RadNet agreed to acquire Gleamer SAS, a Paris-based radiology AI company, for up to €230M in cash including a post-closing milestone component. Gleamer will be integrated into DeepHealth, RadNet's AI and technology subsidiary. Gleamer's platform covers AI-assisted detection across chest X-ray and thoracic CT workflows, and the deal extends DeepHealth's AI capabilities into a European-origin commercial product with existing global customer relationships.

No financial terms of the milestone structure were disclosed beyond the total envelope.

The deal is notable in the context of the broader medtech/digital health M&A wave around radiology AI: within the same week, Sectra acquired Oxipit (autonomous chest X-ray AI, Lithuania), and Siemens Healthineers expanded its distribution of Cortechs.ai's neuroimaging platform. Radiology AI is consolidating rapidly, with workflow automation, autonomous reading, and specialist imaging tools emerging as three distinct sub-segments attracting different buyer profiles. RadNet/DeepHealth's acquisition of Gleamer positions it in the middle tier: AI-assisted detection tools sold to radiology practices, rather than autonomous reading or infrastructure.

Take-Private: Select Medical Holdings / WCAS Consortium — $3.9B

Select Medical Holdings / Consortium (Ortenzio, Jackson, WCAS) — $3.9B take-private | March 2, 2026

Select Medical (NYSE: SEM), one of the largest U.S. operators of critical illness recovery hospitals and outpatient rehabilitation clinics, agreed to be taken private at $16.50 per share in cash, implying a $3.9B enterprise value. The buyer consortium is led by Executive Chairman and co-founder Robert A. Ortenzio and Senior EVP Martin F.

Jackson, alongside healthcare-focused PE firm Welsh, Carson, Anderson & Stowe. The offer represents an 18% premium to the company's unaffected share price from November 24, 2025, and a 25% premium to its 90-day volume-weighted average. Ortenzio and Jackson are rolling over equity rather than taking cash, aligning insider and PE incentives.

The transaction requires approval from unaffiliated shareholders, Hart-Scott-Rodino clearance, and other regulatory sign-offs, with closing expected mid-2026. The deal is not subject to a financing condition. Select Medical will be delisted from NYSE upon completion. Ortenzio and Jackson are rolling approximately 11.8% of shares. No go-shop provision — standard no-solicitation with fiduciary out. Company termination fee: approximately $66.5M; parent reverse termination fee: approximately $133M. Outside date: December 1, 2026, extendable to March 1, 2027.

Advisors: Goldman Sachs (financial advisor to Special Committee); Skadden, Arps, Slate, Meagher & Flom (legal counsel to Special Committee); Dechert LLP (legal counsel to Select Medical); Wells Fargo and J.P. Morgan (financial advisors to Consortium, also joint lead arrangers and bookrunners for committed debt financing); Cravath, Swaine & Moore (legal counsel to Consortium); Barclays (financial advisor to WCAS); Ropes & Gray (legal counsel to WCAS); Paul Hastings (legal counsel to debt financing sources).

Stake Buyout: Grünenthal / Kyowa Kirin International — EMEA Established Medicines JV Consolidation | Private Pharma | March 2, 2026

Grünenthal / Kyowa Kirin International | Minority Stake Buyout (JV Consolidation) | Established Medicines / Pain, Related | EMEA Commercial | March 2, 2026

| Parameter | Detail |

|---|---|

| Announced | March 2, 2026 |

| Deal value | Undisclosed |

| Structure | Grünenthal acquires Kyowa Kirin International's stake in a joint venture covering established medicines |

| Geography | EMEA (primary); Germany-led operations |

| Parties | Grünenthal GmbH (private, Aachen) acquires from Kyowa Kirin International plc (subsidiary of Kyowa Kirin Co., Ltd., Tokyo) |

Grünenthal, the privately held German pharmaceutical company best known for its pain portfolio, announced the acquisition of Kyowa Kirin International's stake in their joint venture covering established medicines across EMEA. Financial terms were not disclosed. The transaction consolidates Grünenthal's control over a commercial portfolio that had previously been managed jointly, removing a sharing partner from the economics of an established medicines franchise.

This deal is structurally representative of a category that rarely appears in Bloomberg or Dealogic deal tables: private-company JV consolidations involving established (off-patent or loss-of-exclusivity) pharmaceutical assets, with no disclosed consideration. The underlying commercial rationale is straightforward — established medicines JVs often outlive their strategic rationale as the originating companies' priorities diverge, and the party with stronger commercial infrastructure and geographic focus frequently buys out the other. Grünenthal's EMEA pain and established medicines franchise is among the largest of its kind held by a private European pharma company, making the consolidation of this JV consistent with long-term portfolio ownership strategy.

Acquisition: Intuitive Surgical / ab medica, Abex, Excelencia Robótica — ~€319M Southern European Distribution

Intuitive Surgical / ab medica, Abex, Excelencia Robótica | Acquisition | Surgical Robotics | Commercial | Completed March 1–2, 2026

| Parameter | Detail |

|---|---|

| Deal value | ~€319M |

| Completed | March 1–2, 2026 (originally announced January 2025) |

| Markets | Italy, Spain, Portugal, Malta, San Marino |

| Installed base transferred | 470+ da Vinci systems |

| Employees transferred | ~250 |

Intuitive Surgical completed the acquisition of its Southern European distribution operations from three regional distributors (ab medica in Italy, Abex in Spain/Portugal, Excelencia Robótica in Spain) covering more than 470 installed da Vinci systems across Italy, Spain, Portugal, Malta, and San Marino. The deal transitions Intuitive from third-party distribution to direct commercial operations across these markets. Originally announced January 2025, completion occurred on March 1–2, 2026. Approximately 250 employees transferred to Intuitive's direct organization.

Acquisition: Sectra / Oxipit — Autonomous Chest X-Ray AI | Digital Health / Radiology AI | March 2026

Sectra / Oxipit | Acquisition | Radiology AI (Autonomous Chest X-Ray) | Marketed | March 2026

Medical imaging IT company Sectra (STO: SECT B) agreed to acquire Lithuanian radiology AI developer Oxipit, with closing expected during March 2026. Oxipit holds the first CE Class IIb certification for autonomous AI in chest X-ray analysis — a regulatory distinction reflecting clinically validated autonomy rather than decision-support assistance. Its flagship ChestLink product automatically identifies high-confidence normal chest X-ray studies and removes them from the radiologist worklist, with 99.9% sensitivity and the capacity to automate approximately 40% of cases.

In 2026, Oxipit expanded into chest CT and musculoskeletal imaging. ChestLink was already available through Sectra's Amplifier Marketplace; the acquisition moves Sectra from distribution partner to direct owner of the underlying autonomous AI technology. No financial terms disclosed. The acquisition consolidates the radiology AI autonomy segment alongside the RadNet/Gleamer and Siemens/Cortechs.ai developments announced the same week.

Acquisition: BioSyent / Oral Science — $25.5M + Seller Royalty | Canadian Oral Health | Commercial

BioSyent / Oral Science | Acquisition | Oral Health (Dental Distribution) | Commercial | March 2, 2026

| Parameter | Detail |

|---|---|

| Purchase price at closing | $25.5M ($22.5M cash + 234,192 BioSyent common shares at $12.81/share = $3.0M) |

| RSU component | $0.2M of cash consideration settled via 12,666 RSUs to certain Oral Science employees (vest year 2) |

| Share escrow / lock-up | 167,635 shares in two-year escrow; 66,557 shares in two-year lock-up (25% released every six months) |

| Additional cash at closing | $2.0M (excess working capital above $6.3M NWC requirement) |

| Contingent earn-out | Cash payment in 2027 based on Oral Science 2025–2026 performance |

| Contingent royalties | Product-specific royalties through 2033, capped at $6.0M (single undisclosed product) |

| Total maximum consideration | ~$33.5M+ (closing + NWC + earn-out + royalty cap) |

| Acquirer | BioSyent Inc. (TSXV: RX), Mississauga, Ontario |

| Target | Oral Science Inc. (privately held; Brossard, Quebec; founded 2003) |

| Target TTM revenue | >$30M (standalone, TTM to Sept 30, 2025) |

| Funding | $16.3M cash on hand + $6.0M RBC 1-Year Senior Secured Demand Term Loan + $2.0M RBC revolving credit draw |

| Post-close net cash | >$10M retained (BioSyent) |

| Additional credit line | RBC Senior Secured Demand Revolving Credit Line up to $12.0M (combined with term loan not to exceed $12.0M) |

| Pro forma TTM revenue (combined) | >$70M |

| Pro forma TTM EBITDA (combined) | >$15.75M |

| Purchase multiple (closing) | 6.33x EBITDA (TTM Sept 30, 2025, before contingent consideration) |

| Founders / leadership | Oral Science founders and leadership team remain in place; become BioSyent shareholders |

| Exchange classification | TSXV Expedited Acquisition under Policy 5.3; subject to final TSXV approval |

| SPA signed | February 8, 2026 |

| Closed | March 2, 2026 |

BioSyent closed its acquisition of Oral Science Inc. on March 2, adding a profitable and growing Canadian dental products distributor to its pharmaceutical and oral health portfolio. Founded in 2003 and headquartered in Brossard, Quebec, Oral Science partners with dental practices across periodontal and endodontic disease, high-risk caries, dry mouth, and oral lesions. Its integrated approach is built on four pillars: diagnosis and monitoring, in-office treatments, home-care solutions, and clinical team and patient education. Revenue is split approximately 54% from dental clinics and the remainder through retail pharmacy and direct-to-consumer online channels.

Oral Science generated more than $30M in standalone trailing revenue for the twelve months ended September 30, 2025 — a business with scale, profitability, and established channel relationships. The founders and leadership team remain in place and become BioSyent shareholders through the share consideration, aligning their incentives with the combined company's performance. Oral Science continues operating from Brossard as a standalone business unit within BioSyent.

The royalty structure — why this deal is relevant to the royalty market

The contingent royalty consideration is the element of primary interest to pharmaceutical royalty participants. Under the SPA, Oral Science's former shareholders retain the right to receive product-specific royalties based on the future net sales of a single undisclosed product through 2033, capped at $6.0M in total. The specific royalty rate, the product name, and the base period are not disclosed — the $6.0M cap is the only economic boundary defined in the public filing.

This is a classic seller-retained royalty in a commercial asset acquisition: the acquirer takes ownership of the full operating business and bears commercialization risk and capital cost going forward, while the sellers retain a capped revenue-linked participation tied to the single most commercially sensitive product in the portfolio. The structure aligns the sellers' payout with the product's commercial trajectory rather than paying them a fixed earn-out that would be owed regardless of performance — a form of contingent consideration that is common in pharma and specialty healthcare M&A but less frequently seen in the dental distribution segment.

For royalty market participants, the structure raises a specific interpretive question: is the royalty tied to a branded, differentiated product with pricing power and a defensible market position — in which case the $6.0M cap may represent a meaningful floor rather than a ceiling — or to a commodity-adjacent product with limited growth and high substitution risk? The public filing does not identify the product, so this assessment must await BioSyent's next shareholder disclosure cycle. What is disclosed is that Oral Science carries proprietary products and exclusive distribution agreements alongside its branded partner portfolio, suggesting the royalty-bearing product may be on the proprietary or exclusively licensed end of the portfolio rather than a generic or white-label item.

BioSyent's capital position and deal rationale

The acquisition is funded predominantly from BioSyent's existing cash, drawing only $8.0M from the new RBC credit facilities (term loan + revolver draw), which management expects to fully retire by Q4 2026. Post-close, BioSyent retains more than $10M in net cash and investments alongside a $12.0M revolving line — a position that preserves meaningful capacity for further acquisitions or in-licensing within the coming twelve months. CEO René Goehrum described Oral Science as a "Canadian success story much like our own" and positioned the deal as delivering on BioSyent's strategic priorities of profitable growth, revenue diversification, and long-term value creation.

The combined pro forma EBITDA of more than $15.75M on more than $70M in revenue implies a blended margin of approximately 22.5%, which is healthy for a specialty healthcare distribution and marketing platform. At 6.33x EBITDA on the closing purchase price — before earn-out and royalties — the multiple is consistent with mid-market Canadian specialty healthcare acquisition comps and reflects the absence of late-stage development risk that typically commands higher multiples in biopharma M&A.

SPAC: VERAXA Biotech / Voyager Acquisition Corp. — Shareholder Approval | ADC/BiTE Oncology

VERAXA Biotech / Voyager Acquisition Corp. | SPAC Business Combination (Milestone) | ADC/BiTE Oncology | Clinical-Stage

| Parameter | Detail |

|---|---|

| VERAXA shareholder vote | 99.57% approval (12,680,593 votes at EGM, February 27, 2026) |

| Announced | March 2, 2026 |

| SPAC | Voyager Acquisition Corp. (Nasdaq: VACH); sponsored by Cantor Fitzgerald & Co., Voyager Acquisition Sponsor Holdco LLC, and Odeon Capital Group LLC |

| Target | VERAXA Biotech AG (Zurich; portfolio company of Xlife Sciences AG, SIX: XLS) |

| Transaction type | Absorption merger; Veraxa Biotech Holding AG acquires VERAXA Biotech AG and renames to Veraxa Biotech AG |

| Capital increase approved | Ordinary capital increase up to CHF 223,400 for share issuance to Voyager shareholders |

| Next gate | Voyager shareholder vote — scheduled March 12, 2026 |

| Post-close ticker | VRXA (NASDAQ) |

| Business combination agreement signed | April 22, 2025 |

| Proxy statement/prospectus filed | February 19, 2026 |

VERAXA Biotech AG, a Zurich-based oncology company focused on antibody-drug conjugates (ADCs), bispecific T cell engagers (BiTEs), and its proprietary BiTAC antibody format, cleared the final VERAXA-side prerequisite for its merger with Voyager Acquisition Corp. on February 27, 2026, with a 99.57% shareholder vote. VERAXA originates from scientific work conducted at the European Molecular Biology Laboratory (EMBL) and is developing a pipeline of next-generation antibody-based cancer therapies. The business combination agreement was originally signed in April 2025.

The March 2 announcement is a procedural milestone rather than a transaction closing — the Voyager shareholder vote remains the final gate, with trading under VRXA on NASDAQ expected to commence shortly after. VERAXA's management team, led by CEO Dr. Christoph Antz, continues unchanged. The transaction gives VERAXA access to public capital markets for clinical development of its ADC and BiTAC pipeline, consistent with the broader 2025–2026 wave of European oncology biotechs pursuing U.S. NASDAQ listings via SPAC as a route to institutional investor access.

Corporate Vote: BioMarin / Amicus Therapeutics — Merger Vote Completed March 3, 2026

BioMarin Pharmaceutical / Amicus Therapeutics | Acquisition | Rare Lysosomal Storage Disorders | Commercial | Vote March 3, 2026

| Parameter | Detail |

|---|---|

| Vote date | March 3, 2026 (virtual special meeting) |

| Deal terms | All-cash at $14.50/share (~$4.8B equity value); agreement dated December 19, 2025 |

| Shares eligible | 313,918,463 (record date January 28, 2026) |

| Shares voted | 234,785,243 (74.79% quorum) |

| Merger adoption vote | 234,593,492 FOR / 119,194 AGAINST / 72,557 abstentions (99.9%+ approval) |

| Executive compensation advisory vote | 209,150,012 FOR / 24,282,220 AGAINST (approved, non-binding) |

| HSR early termination | Granted February 11, 2026 |

| Remaining conditions | Regulatory clearances in certain European jurisdictions and Japan |

| Expected closing | Q2 2026 |

| Drop-dead date | December 19, 2026 |

| BioMarin financial advisors | Morgan Stanley, J.P. Morgan |

| BioMarin legal counsel | Jones Day (acquisition); Cooley LLP (financing) |

| Amicus financial advisors | Centerview Partners, Goldman Sachs (also provided fairness opinion) |

| Amicus legal counsel | Kirkland & Ellis |

| Debt financing | $3.7B package: $850M senior unsecured notes due 2034, $2B Term Loan B, $800M Term Loan A, $600M revolving credit facility |

| Leverage target | Gross leverage <2.5x within two years |

| Termination fee | $175M (Amicus to BioMarin) |

| Key assets acquired | Galafold (migalastat, Fabry disease; 2025 revenue $521.7M) + Pombiliti + Opfolda (Pompe disease; 2025 revenue $112.5M) |

| Pipeline acquired | DMX-200 (CCR2 inhibitor for FSGS, Phase 3 ACTION3 trial) |

| Royalty obligations inherited | Dimerix DMX-200 license: $30M upfront (paid) + up to $75M development/regulatory milestones + $35M first commercial sale milestone + up to $410M commercial milestones + up to $40M future-indication milestones = total potential ~$560M in milestones + low-teens to low-twenties % tiered royalties on U.S. net sales |

| Galafold generic entry | Teva, Aurobindo, Lupin generic license agreements permitting entry January 30, 2037 |

The Amicus Therapeutics special meeting on March 3, 2026 produced an overwhelming 99.9%+ shareholder vote in favor of BioMarin's all-cash acquisition at $14.50/share. The only remaining conditions to closing are regulatory clearances in select European jurisdictions and Japan; HSR (U.S. antitrust) clearance was obtained early in February. The transaction, first announced December 19, 2025, is expected to close in Q2 2026.

The deal carries a material inherited royalty obligation: BioMarin assumes the Dimerix license covering DMX-200, with up to approximately $560M in milestones plus low-teens to low-twenties percent tiered royalties on U.S. net sales. The acquisition also crystallizes the Galafold generic entry timeline — Teva, Aurobindo, and Lupin hold authorized generic agreements permitting market entry on January 30, 2037, providing BioMarin approximately 11 years of commercial runway on its largest acquired revenue stream.

Licensing

| # | Licensor | Licensee | Asset | Upfront | Total Potential | Royalty | Stage | Date |

|---|---|---|---|---|---|---|---|---|

| 1 | Chia Tai Tianqing (Sino Biopharma) | Sanofi | Rovadicitinib (JAK/ROCK) | $135M | Up to $1.53B | Up to double-digit tiered | Ph 3 / Approved (China) | March 4 |

| 2 | Antengene | UCB | ATG-201 (CD19/CD3 BiTE) | $60M + $20M near-term | Up to ~$1.18B | Tiered (undisclosed rate) | Ph 1 | March 3 |

| 3 | Pierre Fabre | Eton Pharmaceuticals | HEMANGEOL (propranolol) U.S. rights | $14M | $14M + royalties | 8% of U.S. net sales (patent life) | Marketed | March 2 |

| 4 | Celyn Therapeutics | Kairos Pharma | CL-273 (EGFR NSCLC) worldwide | None disclosed | $15M milestone + royalty | 2% of U.S. net revenues (IP life) | Pre-IND | March 2 |

| 5 | Orexo AB | Dexcel Pharma USA | Zubsolv (buprenorphine/naloxone) U.S. | ~$95M net | ~$111.8M total potential | Contingent consideration up to $16.8M on 2026–2027 sales | Marketed | March 3–4 |

| 6 | GAIA AG | Daiichi Sankyo Europe | Lipodia (digital therapeutic) Europe | Undisclosed | Undisclosed | Undisclosed | Approved (Germany DiGA) | March 5 |

| 7 | Helix | Alnylam | GenoSphere clinico-genomic cohort | Undisclosed | Undisclosed | N/A (data access) | Population genomics | March 5 |

| 8 | Nxera Pharma | Centessa Pharmaceuticals | ORX489 (OX2R agonist) milestone | — | $3M milestone triggered | Per collaboration agreement | Ph 1 | March 5 |

Section total (disclosed upfront): ~$209M upfront + $20M near-term = ~$229M immediately deployable. Total potential across disclosed deals: ~$2.74B+ (Sanofi $1.53B + UCB $1.18B + remainder). Orexo/Dexcel is an asset divestiture with royalty-adjacent contingent consideration.

Royalty notes: Sanofi/Chia Tai: "up to double-digit tiered" — precise floor not disclosed; publicly confirmed as double-digit but starting rate undisclosed. UCB/Antengene: tiered rate not disclosed in public filings; rate confirmation not available. Eton/Pierre Fabre: 8% explicitly disclosed — cleanest royalty rate in the section. Kairos/Celyn: 2% U.S. explicitly disclosed — low, consistent with pre-clinical asset range. Dexcel/Orexo: not a royalty per se but contingent consideration ($16.8M cap on 2026–2027 sales performance) functions as a seller-retained royalty-equivalent.

Research Collaboration: Alnylam / Tenaya Therapeutics — Up to $1.23B Cardiovascular RNAi Discovery Collaboration

Alnylam Pharmaceuticals / Tenaya Therapeutics | Research Collaboration + License | Cardiovascular Disease | Discovery | March 5, 2026

| Parameter | Detail |

|---|---|

| Announced | March 5, 2026 (agreement signed March 4) |

| Structure | Research collaboration + target-by-target exclusive license to Alnylam |

| Upfront payment | Up to $10M (payable within 30 days; subject to $500,000 reductions per target for up to 8 Tenaya-nominated targets failing agreed standards; theoretical minimum $6M) |

| Research cost reimbursement | Yes (from Alnylam to Tenaya) |

| Development and commercial milestones | Up to $1.13B |

| Royalties | Not disclosed; 8-K describes "development, regulatory and sales-based milestones" without mentioning traditional royalties — full terms expected as Tenaya Q1 2026 10-Q exhibit |

| Research structure | 24-month validation period (extendable) + 24-month evaluation period |

| Targets | Up to 15 novel genetic targets for cardiovascular disease (jointly nominated; deal is modality-agnostic, though Alnylam's core platform is RNAi) |

| Tenaya platform | iPSC-derived cardiomyocyte phenotypic screening |

| Downstream rights | Alnylam assumes all development, manufacturing, and commercialization per target; Tenaya has no co-development or co-commercialization rights |

| Termination right | Alnylam can terminate for any reason with notice |

| Advisors | No financial or legal advisors publicly disclosed for either party; consistent with research collaboration rather than M&A |

| Tenaya GC | Jennifer Drimmer Rokovich (signed Tenaya 8-K) |

| Headline figure note | "$1.23B" cited by some outlets appears to include ~$90M in estimated research reimbursement; Tenaya's 8-K cites $10M upfront plus up to $1.13B in milestones |

Alnylam Pharmaceuticals and Tenaya Therapeutics announced on March 5, 2026 a cardiovascular disease research collaboration in which Tenaya will deploy its iPSC-derived cardiomyocyte screening platform to validate up to 15 novel genetic targets over a 24-month research term. For each validated target, Alnylam receives an exclusive worldwide license and assumes all downstream development, manufacturing, and commercialization responsibilities.

The collaboration extends Alnylam's cardiovascular franchise — which already includes inclisiran (co-developed with Novartis), vutrisiran, fitusiran, and zilebesiran — into entirely new genetic target space identified through Tenaya's disease-relevant human cardiomyocyte models. The 24-month research horizon and milestone structure ($10M upfront, up to $1.13B in contingent payments) is consistent with Alnylam's established pattern of building its pipeline through platform access agreements before committing development capital. Tenaya retains no development responsibilities once targets are licensed to Alnylam.

Major Licensing: Sanofi / Chia Tai Tianqing (Sino Biopharmaceutical) — rovadicitinib | Up to $1.53B

Sanofi / Chia Tai Tianqing Pharmaceutical Group | Licensing | Myelofibrosis (China approval), Chronic Graft-versus-Host Disease (global Phase 3) | Phase 3 / Approved (China)

| Parameter | Detail |

|---|---|

| Announced | March 4, 2026 |

| Licensor | Chia Tai Tianqing Pharmaceutical Group Co., Ltd. (subsidiary of Sino Biopharmaceutical Holdings, HKEX: 1177) |

| Licensee | Sanofi |

| Rights granted | Exclusive worldwide license (development, manufacture, and commercialization) |

| Upfront payment | $135M |

| Development, regulatory, and sales milestones | Up to $1.395B |

| Total potential value | Up to $1.53B |

| Royalties | Up to double-digit tiered on annual net sales |

| Asset | Rovadicitinib (brand name: Anxu in China) — oral dual JAK/ROCK inhibitor |

| China approval | February 2026 (NMPA) — first-line treatment for intermediate-2 or high-risk PMF, PPV-MF, and PET-MF |

| Primary global target indication | Chronic graft-versus-host disease (cGVHD) |

| Phase 3 cGVHD status | NCT06682169, ongoing in China; FDA-cleared Phase 2 in the U.S. |

Announced March 4, 2026, this is the week's largest disclosed licensing transaction and the most prominent example of a China-to-West deal moving a fully approved domestic asset into a global development and commercialization program. Chia Tai Tianqing, the pharmaceutical flagship of Sino Biopharmaceutical — one of China's largest pharmaceutical groups by revenue — grants Sanofi worldwide exclusive rights to rovadicitinib, a first-in-class oral dual inhibitor of JAK1/2 (via the STAT3/5 pathway) and ROCK1/2 (via the anti-fibrotic axis). The dual mechanism is the scientific cornerstone of the asset's differentiation: most approved myelofibrosis therapies (ruxolitinib, fedratinib, pacritinib) are JAK inhibitors only, targeting the inflammatory cascade but not the fibrotic process that drives splenomegaly progression and bone marrow failure over time.

Rovadicitinib's simultaneous inhibition of ROCK1/2 adds an anti-fibrotic dimension theoretically capable of slowing the stromal remodeling underlying disease progression — a mechanistic distinction no current approved MF therapy can claim.

Rovadicitinib received NMPA approval in February 2026 under the brand name Anxu for first-line treatment of intermediate-2 or high-risk primary myelofibrosis (PMF), post-polycythemia vera MF (PPV-MF), and post-essential thrombocythemia MF (PET-MF) in adult patients — making it one of only a handful of novel MF therapies to achieve global regulatory approval. Sanofi's primary development target, however, is chronic graft-versus-host disease (cGVHD), a severe and often life-threatening complication of allogeneic hematopoietic stem cell transplantation where the JAK/STAT3/5 inflammatory and ROCK-mediated fibrotic pathways are both implicated in disease maintenance and organ damage. Sanofi's transplant and immunology franchise — which markets Enjaymo (sutimlimab) and previously commercialized Mozobil (plerixafor) — provides an established infrastructure into which rovadicitinib fits strategically.

The competitive cGVHD landscape includes ruxolitinib (Jakavi, Novartis/Incyte, FDA-approved 2021), ibrutinib (Imbruvica, J&J/AbbVie, FDA-approved 2017), and axatilimab (Niktimvo, Syndax/Incyte, FDA-approved 2024), along with several agents in later-stage development. Rovadicitinib's dual mechanism differentiates it on paper from all current approved agents in cGVHD, none of which address both inflammatory and fibrotic pathology simultaneously.

The deal economics are at the higher end of the China-to-West licensing spectrum for 2026. The $135M upfront is substantially larger than the $60M UCB paid to Antengene for ATG-201 (announced the same week), reflecting rovadicitinib's more advanced clinical status — already approved in China and in active Phase 3 in cGVHD. The up-to-double-digit tiered royalty structure, fully disclosed in public filings, places this among the more transparent royalty packages in recent China-originated out-licensing.

Competitive context in myelofibrosis: Rovadicitinib enters a global MF market anchored by ruxolitinib (Jakavi/Jakafi, Incyte/Novartis) and increasingly crowded with fedratinib (Inrebic, BMS), pacritinib (Vonjo, SOBI/CTI BioPharma), and momelotinib (Ojjaara, GSK). None of the existing approved agents have demonstrated meaningful anti-fibrotic activity at standard therapeutic doses. If Sanofi pursues an MF label expansion alongside cGVHD, rovadicitinib would compete directly in this market with a mechanistic claim no current approved competitor can make.

Major Licensing: UCB / Antengene — ATG-201

UCB / Antengene | Licensing | B Cell-Related Autoimmune Diseases | Phase 1

| Parameter | Detail |

|---|---|

| Upfront | $60M |

| Near-term milestones | $20M (on satisfaction of conditions) |

| Total upfront + near-term | $80M |

| Development/regulatory/commercial milestones | >$1.1B |

| Royalties | Tiered on future net sales |

| Equity component | None — pure license with cash payments and tiered royalties |

| Asset | ATG-201 (CD19/CD3 bispecific T-cell engager, AnTenGager™ platform) |

| CRS reduction mechanism | (1) Steric hindrance masking — cryo-EM confirmed CD3 binding site physically blocked until CD19 target engagement; (2) fast-on-fast-off CD3 binder scFv limiting activation duration; (3) bivalent 2+1 architecture (two CD19 arms, one CD3 arm) enhancing avidity while controlling T-cell engagement |

| Geography | Worldwide exclusive |

| Phase 1 execution | Antengene (China & Australia), then transfers to UCB |

| Advisors | No financial or legal advisors publicly disclosed; UCB on Euronext Brussels, Antengene on HKEX (6996) — neither SEC-registered |

Announced March 3, 2026, the UCB/Antengene deal is the week's most substantive licensing transaction. UCB gains worldwide exclusive rights to develop, manufacture, and commercialize ATG-201, a CD19/CD3 bispecific T-cell engager designed for B cell depletion in autoimmune diseases, along with access to Antengene's manufacturing technology and the underlying AnTenGager platform.

ATG-201 employs steric hindrance masking technology intended to reduce cytokine release syndrome risk — a key differentiator relative to first-generation T-cell engagers — along with a proprietary fast-on-fast-off CD3 binder designed to limit T-cell exhaustion. Preclinical data presented at ACR 2025 showed complete and sustained B cell depletion across blood, bone marrow, and spleen in humanized mouse models following a single dose.

The deal structure is characteristic of China-to-West licensing: Antengene retains responsibility for IND submissions in China and Australia in Q1 2026 and will conduct first-in-human Phase 1 studies before transferring further clinical development to UCB. The $80M upfront and near-term package and $1.1B+ milestone stack positions this among the larger China-originated autoimmune deals of early 2026.

Licensing: Eton Pharmaceuticals / Pierre Fabre — HEMANGEOL U.S. Commercialization Rights | $14M Upfront + Royalty

Eton Pharmaceuticals / Pierre Fabre | Licensing | Infantile Hemangioma | Marketed (FDA Orphan Drug)

| Parameter | Detail |

|---|---|

| Upfront payment | $14.0M |

| Royalty | 8% of U.S. net sales for patent life |

| Inventory at closing | ~$1.5M |

| Additional inventory (May 2026) | ~$0.7M est. |

| Total initial outlay | ~$16.2M |

| U.S. commercialization start | May 1, 2026 |

| Licensor | Pierre Fabre Medicament Sas (continues global ex-U.S. rights) |

| Licensee | Eton Pharmaceuticals, Inc. (Nasdaq: ETON) |

| Financing | Cash on hand; expected accretive to 2026 earnings |

| Agreement signed | February 27, 2026 |

| Announced | March 2, 2026 |

Eton Pharmaceuticals announced on March 2 the in-licensing of U.S. commercialization rights to HEMANGEOL (propranolol hydrochloride) oral solution from Pierre Fabre, the only FDA-approved systemic therapy for proliferating infantile hemangioma. The asset is a marketed Orphan Drug treating an estimated 5,000–10,000 U.S. infants annually. Pierre Fabre retains global commercialization rights excluding the U.S. and will continue U.S. distribution through April 30, 2026.

The deal gives Eton its tenth commercial rare disease product — reaching a stated long-held milestone — and fits squarely within its orphan drug-focused commercial model. Eton will deploy its Eton Cares patient support program, which includes a $0 commercial co-pay for qualifying patients, specialty distribution, benefits investigation, and patient education services tailored to the pediatric workflow.

The royalty structure (8% of U.S. net sales for patent life) is a textbook ex-U.S. originator royalty arrangement: Pierre Fabre exits U.S. commercial operations while retaining a recurring revenue stream on the market it built. For Eton, the deal converts a one-time outlay of roughly $16M into a royalty-bearing commercial asset expected to generate immediate earnings accretion, financed from existing cash.

Licensing: Kairos Pharma / Celyn Therapeutics — CL-273 Exclusive Worldwide Rights | Equity + Milestone

Kairos Pharma / Celyn Therapeutics | Asset Acquisition (Binding Terms) | EGFR-Mutant NSCLC | Pre-IND

| Parameter | Detail |

|---|---|

| Asset | CL-273 — AI-designed, reversible, wild-type-sparing pan-EGFR small-molecule inhibitor |

| Seller | Celyn Therapeutics, Inc. (privately held; backed by OrbiMed and Torrey Pines Investment) |

| Acquirer | Kairos Pharma, Ltd. (NYSE American: KAPA) |

| Equity consideration | 16.5% of Kairos on fully diluted basis at closing |

| Regulatory milestone | $15M (cash + shares mix) upon FDA NDA/BLA submission |

| Royalty | 2% of U.S. net revenues for IP life |

| Additional asset included | CL-741, a Phase 1-ready oral type IIb c-MET inhibitor |

| Upfront cash | None disclosed |

| Conditions | Shareholder approvals (both parties); no material adverse effect; NYSE American clearance if required |

| Financial advisor | D. Boral Capital, LLC (sole advisor to Kairos) |

| Announced | March 2, 2026 |

Kairos Pharma signed binding terms on March 2 to acquire exclusive worldwide rights — covering development, manufacturing, commercialization, and all related IP and regulatory rights — to CL-273 from Celyn Therapeutics. The deal also includes CL-741, a Phase 1-ready c-MET inhibitor, providing Kairos with a complementary asset targeting MET-driven resistance in NSCLC.