Waterfall Disputes in Stacked Royalty Deals: When Multiple Holders Go to War Over the Same Revenue Stream

In April 2022, a Texas jury needed two hours to decide that Daiichi Sankyo owed Seagen $41.8 million in back royalties on Enhertu — plus an 8% running rate on all future US sales of what was already a multi-billion dollar oncology franchise. Three years later, the Federal Circuit reversed the verdict entirely, invalidating Seagen's patent and vacating every dollar of the award.

Between those two dates, the economics of Enhertu's entire royalty stack were in limbo. AstraZeneca, which had paid $1.35 billion upfront in 2019 to co-develop the drug, could not know what its effective royalty burden would be. Daiichi Sankyo could not determine whether the 8% Seagen claim would push its aggregate royalty obligations past the point of commercial viability. And anyone attempting to value, trade, or lend against Enhertu's revenue stream had to model a binary legal outcome with hundreds of millions of dollars on either side.

This is what a waterfall dispute looks like in practice: not a clean legal question, but a multi-year period of structural uncertainty that cascades through every layer of a drug's royalty stack.

In a previous analysis, we examined the structural mechanics of stacked royalty financings — intercreditor agreements, synthetic seniority, leakage risks, and anti-stacking covenants. This article turns to what happens when those structures are tested: the real-world disputes that arise when multiple royalty holders claim priority over the same cash flows, and the patterns those disputes follow.

The Dispute Landscape Has Changed

The pharmaceutical royalty market has grown from a niche corner of life sciences finance into a $10+ billion annual market. Gibson Dunn's H1 2025 data showed aggregate volume annualising at $5.42 billion, with average transaction sizes exceeding $225 million. As Goodwin observed in October 2025, the momentum continued to accelerate, driven by demand for non-dilutive capital in a challenging equity environment.

That growth has a structural consequence: more drugs now carry more layers of royalty obligations than at any previous point. University patent royalties, technology platform licenses, co-development agreements, synthetic royalty monetisations, and litigation settlement royalties stack on top of each other, frequently governed by bilateral contracts negotiated years apart with no cross-references between them.

The stacking mechanics are well-understood. What remains poorly understood is the conflict surface — the specific points where these stacked structures generate disputes between holders who each believe they have a valid claim on the same dollars.

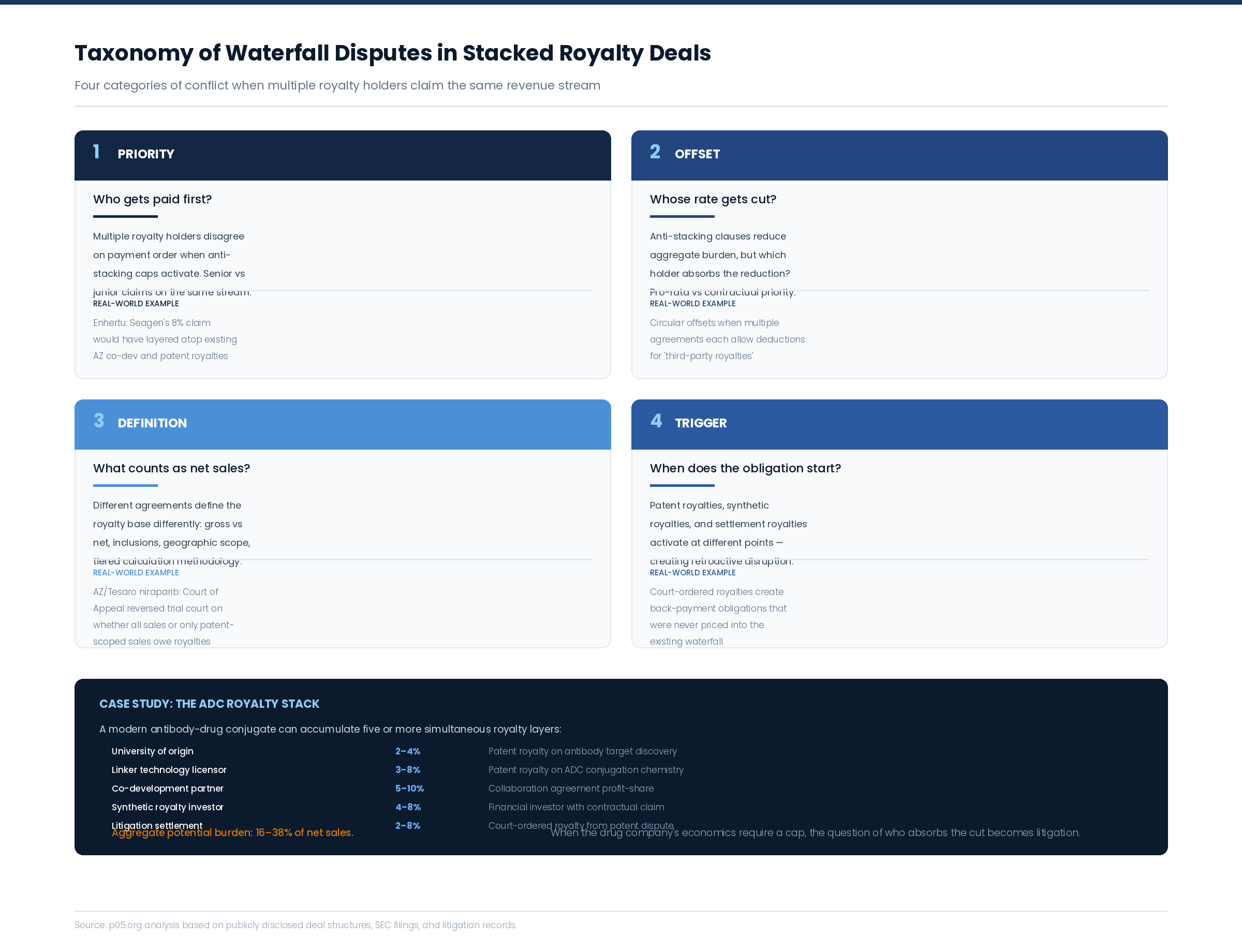

Pattern 1: The Retroactive Layer — Litigation That Rewrites the Stack

The most disruptive category of waterfall dispute is the retroactive royalty — a claim imposed on an existing stack by a court or arbitration panel, forcing all other holders to absorb a layer they never priced into their original economics.

Enhertu: Five Years of Stack Uncertainty

Enhertu's royalty dispute is the most financially significant example in recent memory. The drug's licensing chain begins with Daiichi Sankyo's in-house discovery of the DXd ADC platform, proceeds through a 2008 collaboration with Seagen (then Seattle Genetics) that ended in 2015, and arrives at a $6.9 billion co-development agreement with AstraZeneca in 2019. When Seagen argued in 2020 that its '039 patent covered the linker technology used in Enhertu, it was claiming a royalty layer that post-dated every other commercial arrangement on the drug.

The district court's 2022 ruling ordered an 8% running royalty from April 2022 through the patent's November 2024 expiry. On a drug that generated $3.75 billion in combined 2024 sales, that represented a potential annual transfer of $300 million — not to a party that had funded Enhertu's development or taken clinical risk, but to a former collaborator asserting a patent claim.

The waterfall disruption was not limited to the direct litigants. Any investor holding or considering a position in Enhertu-adjacent royalty streams had to model two futures: one in which the stack included an 8% Seagen layer, and one in which it did not. The Federal Circuit's December 2025 reversal resolved the uncertainty — but only after five years of litigation and a parallel USPTO post-grant review that independently invalidated the patent.

The lesson is not about Enhertu specifically. It is that any drug with a complex licensing history and multiple technology contributors is vulnerable to a retroactive claim that reorders the entire waterfall. ADCs are particularly exposed — a single drug can incorporate antibody, payload, and linker technologies from separate licensors, any of whom may later assert that the product falls within their patent claims.

What Retroactive Claims Do to Existing Holders

When a court imposes a new royalty layer, the drug company's aggregate royalty burden increases. If anti-stacking provisions exist in any of the prior agreements, the increase may trigger offsets that reduce payments to existing holders — holders who had no role in the litigation, no voice in the proceedings, and no contractual mechanism to protect their position.

This is the gap that separates pharmaceutical royalty stacks from corporate debt structures. In corporate debt, a new creditor claim requires either the consent of existing creditors (through negative pledge covenants) or subordination to existing claims. In pharmaceutical royalty stacks, a court can impose a new claim that sits alongside or ahead of existing obligations, with no formal mechanism for existing holders to object or protect their priority.

Pattern 2: The Anti-Stacking Collision — When Offset Clauses Fight Each Other

Anti-stacking clauses are the pharmaceutical royalty market's primary defence against excessive aggregate burdens. A typical clause allows the licensee to deduct a portion of third-party royalties from the primary licensor's rate, subject to a floor — often 50% of the original rate.

The problem emerges when multiple agreements on the same drug each contain anti-stacking clauses, and those clauses were drafted without knowledge of each other.

The Circular Offset Problem

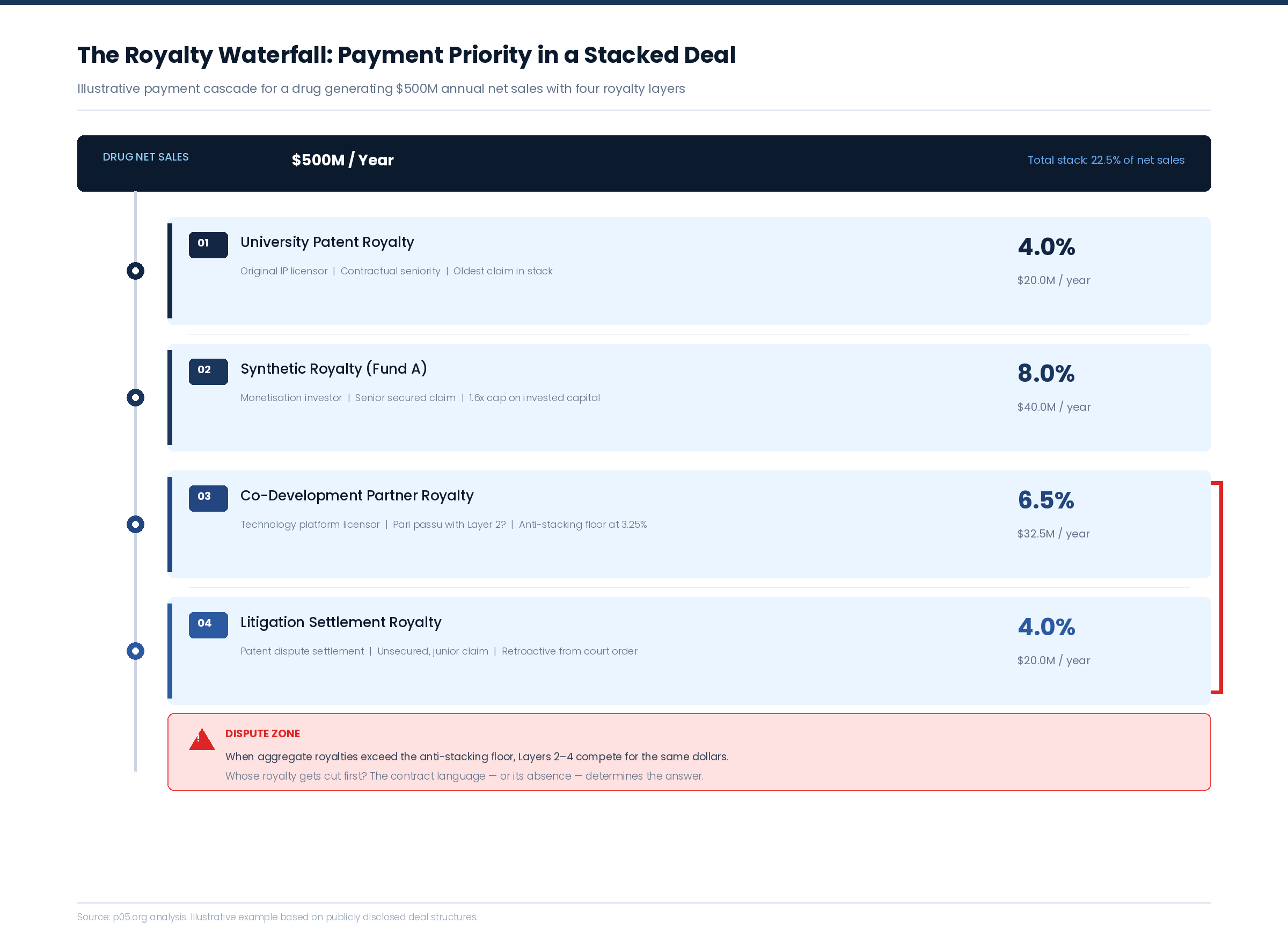

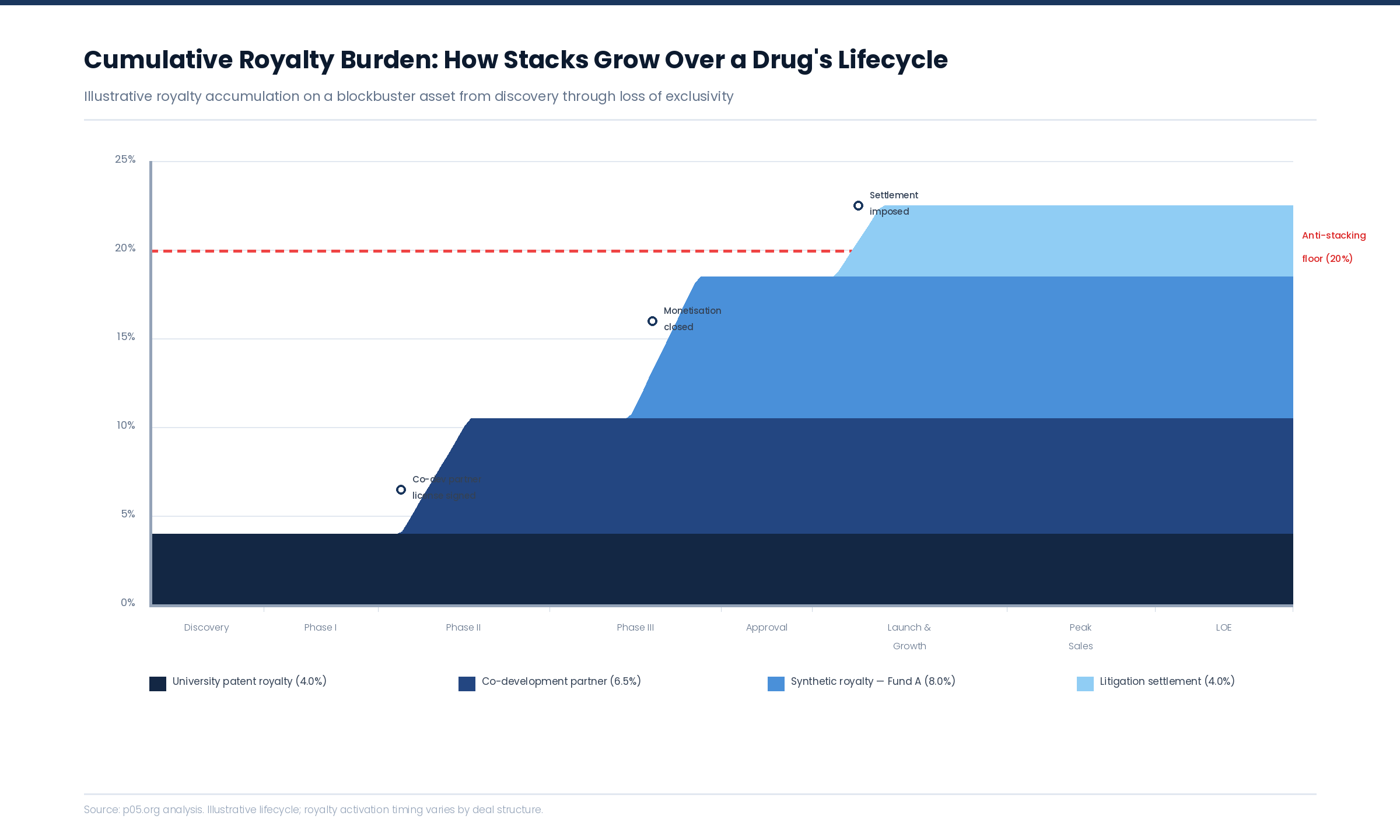

Consider a drug carrying three royalty obligations: a 4% university patent royalty, a 6.5% co-development royalty, and an 8% synthetic royalty from a monetisation transaction. Each agreement contains an anti-stacking clause allowing up to 50% offset for third-party royalties, subject to a floor of 50% of the original rate.

When the total stack reaches 18.5%, the licensee invokes each anti-stacking clause simultaneously. The university's 4% can be reduced by offsets for the co-development and synthetic royalties — but the co-development agreement's clause can also be invoked to offset the university and synthetic royalties. If each holder's rate is reduced to its floor, the aggregate burden drops — but the question of which holder absorbs the reduction first, and how the offsets interact, is not answered by any of the three agreements individually.

This is not a hypothetical. As IP Draughts has documented, "whatever the clause says, if enough money is at stake its correct interpretation may be litigated." The leading UK precedent, Cambridge Antibody Technology v Abbott, turned precisely on the interaction between anti-stacking provisions in overlapping agreements.

The financial stakes are large. A 2% difference in offset allocation on a drug generating $2 billion annually is a $40 million annual dispute — recurring every quarter for as long as the royalty obligations persist.

The Floor Collision

Anti-stacking floors create a separate category of dispute. If Licensor A's floor is 2% and Licensor B's floor is 3.25%, and the licensee's maximum economically viable royalty burden is 10%, the guaranteed minimum payments to A and B alone consume 5.25% — leaving only 4.75% for all other royalty holders in the stack, regardless of what their contracts nominally entitle them to.

When a new holder enters the stack (through a monetisation transaction or litigation settlement), the floor commitments may be contractually senior to the new holder's claim, even if the new holder believed it was acquiring a percentage of gross sales without reference to floors in agreements it has never seen.

Pattern 3: The Definition War — What Counts as 'Net Sales'

The most technically complex waterfall disputes arise from definitional mismatches between royalty agreements on the same drug.

The AstraZeneca/Tesaro Precedent

The UK Court of Appeal's ruling on AstraZeneca's sub-licences to Tesaro for niraparib (a PARP inhibitor) illustrates the problem. The dispute centered on whether royalties were owed on all sales in countries where licensed patents existed, or only on sales that would be covered by the patent claims.

The trial court adopted a broad interpretation: all sales in patent-covered countries generated royalty obligations. The Court of Appeal reversed, holding that the drafting indicated royalties were payable only on usage within patent scope. The difference between the two interpretations represented a substantial reallocation of revenue between the parties.

In a stacked structure, this type of definitional dispute cascades. If one royalty agreement calculates on "worldwide net product sales" and another on "net sales of licensed products in the territory," the royalty bases differ. Tiered structures amplify the mismatch: Evrysdi's royalty, for example, steps from 8% to 16% across four tiers based on aggregate sales levels. If two holders calculate tiers from different bases, they can disagree on the applicable rate even when they agree on the underlying revenue.

Net Sales Adjustments as a Conflict Surface

The definition of "net sales" itself varies between agreements. Returns, rebates, chargebacks, distribution fees, IRA negotiated prices, 340B discounts — each agreement may include or exclude these adjustments differently. A drug company making quarterly royalty payments to four holders, each with different net sales definitions, must calculate four different royalty bases from the same gross revenue. Any error or ambiguity in those calculations becomes a potential dispute.

Post-IRA, this surface has expanded. The Inflation Reduction Act's price negotiation provisions create a new category of price adjustment that most pre-2022 royalty agreements did not contemplate. Whether a CMS-negotiated price reduction constitutes a "rebate" (typically deducted from net sales) or a "price" (which may not be) is an open question that has not yet been litigated in the royalty context.

Pattern 4: The Fragmented Stack — When No One Knows the Full Picture

Perhaps the most insidious category of waterfall dispute arises from information asymmetry: situations where no single party has visibility into the complete royalty stack.

The Xtandi Example

Xtandi (enzalutamide) illustrates how a royalty stack can fragment across multiple holders over time. The drug was discovered at UCLA under federal grants, licensed to Medivation in 2005, co-developed with Astellas, and approved in 2012. The royalty stack included UCLA (43.875% of a 4% royalty on worldwide net sales), the Howard Hughes Medical Institute, and the original researchers — each with co-ownership of the royalty interest. When Royalty Pharma acquired rights to a portion of those royalties for $1.14 billion in 2016, and Pfizer subsequently acquired Medivation for $14 billion, the ownership of the royalty interest was distributed across multiple institutional and individual holders.

The fragmentation creates an information problem. A new investor considering a position adjacent to Xtandi's royalty stream — through a synthetic royalty on related enzalutamide indications, for example — would need to reconstruct the full ownership stack from SEC filings, university licensing records, and (for the individual inventor shares) potentially private records that are not publicly accessible.

The Private Company Gap

The information asymmetry is most acute in private company transactions. When a publicly traded biotech monetises a royalty, the terms are typically disclosed in SEC filings. When a private company does the same, the transaction may generate no public record at all — meaning that a subsequent investor has no visibility into existing royalty obligations unless the company voluntarily discloses them during due diligence.

This is the gap that Capital for Cures is building systematic infrastructure to close. The platform's AI-powered extraction pipeline processes SEC filings, licensing agreements, court records, and international regulatory filings to create a comprehensive database of royalty deal terms — including the private company transactions and smaller deals that no existing data provider covers. In a market where waterfall disputes arise precisely because parties lack visibility into the total stack, a centralised deal database functions as a dispute prevention mechanism, giving incoming investors the information they need to assess the full stack before committing capital.

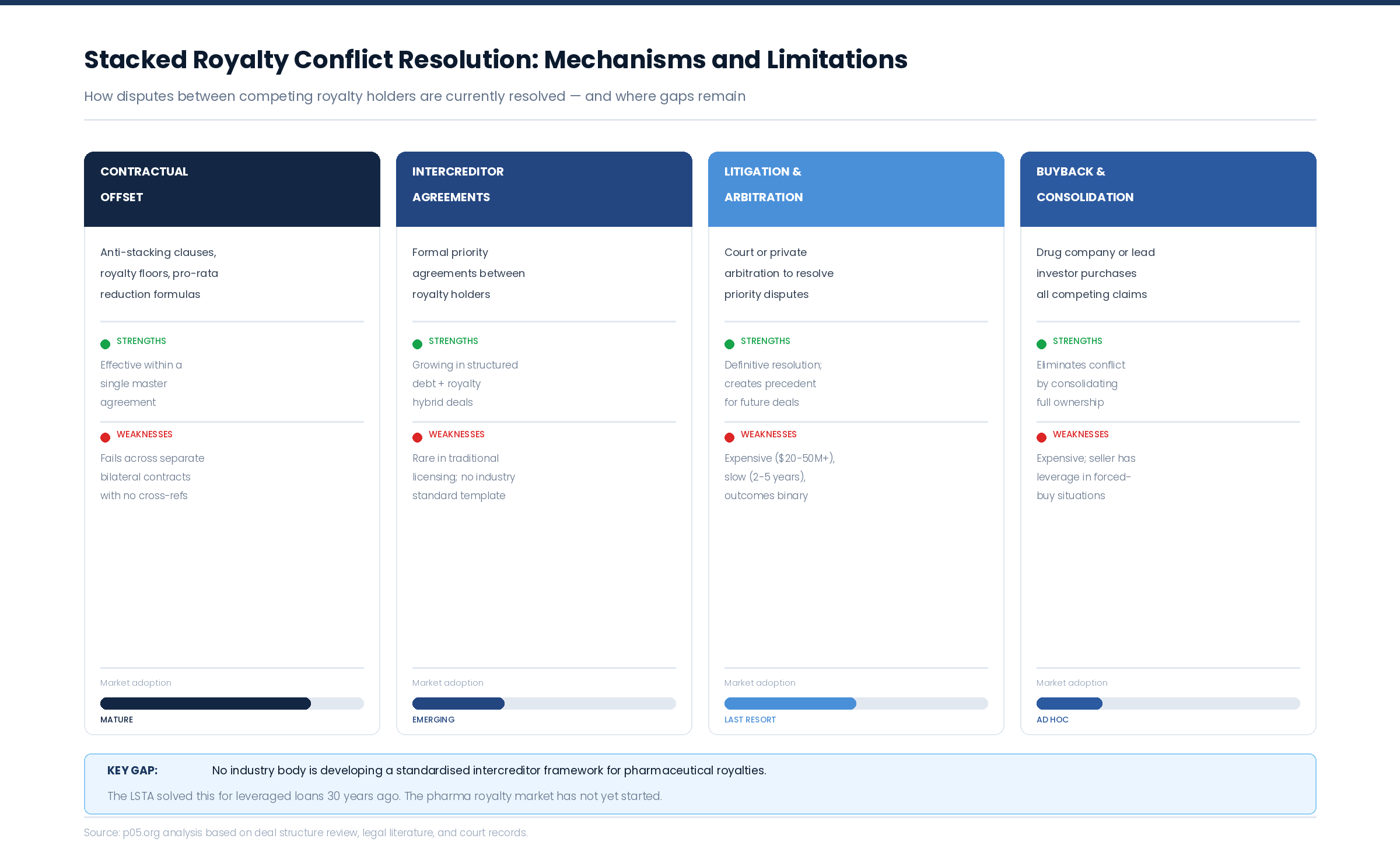

The Resolution Deficit

When waterfall disputes arise, the pharmaceutical royalty market has four resolution mechanisms — all of them inadequate relative to the stakes involved.

Litigation

The Seagen/Daiichi dispute is the archetype: five years, multiple courts, a parallel USPTO proceeding, and resolution on a technicality (patent validity) rather than on the substantive question of waterfall priority. The cost of litigating a royalty priority dispute through the federal court system — including discovery, expert witnesses, trial, and appeals — can easily reach $20-50 million per side, making it economically irrational for any dispute below that threshold.

Arbitration

Many licensing agreements contain arbitration clauses, but the scope of those clauses typically covers disputes between the parties to the agreement — not disputes between one party and a holder whose claim arises under a different agreement entirely. A synthetic royalty investor and a university patent holder, for example, may have no contractual relationship and no shared arbitration mechanism.

Contractual Negotiation

The most common resolution is private negotiation, which works when the number of holders is small and the parties have aligned incentives. Royalty Pharma's consolidation of the Evrysdi stack — acquiring 100% of the tiered 8-16% royalty through sequential purchases from PTC Therapeutics — is the clearest example. But consolidation requires a buyer with the balance sheet and strategic interest to acquire every layer, and it works only for stacks where all holders are willing to sell.

Buyback by the Drug Company

The drug company paying the royalties can resolve waterfall disputes by buying back the conflicting claims. But this is expensive — the seller in a forced-buy situation holds significant leverage — and it addresses the symptom (the dispute) rather than the cause (the absence of a coordination mechanism between holders).

What the Market Needs and Does Not Have

The corporate credit market solved this class of problem thirty years ago with intercreditor agreements. The pharmaceutical royalty market has not.

The specific gaps are identifiable and, in principle, addressable.

First: a standard intercreditor template for pharmaceutical royalties. The Loan Syndications and Trading Association transformed the leveraged loan market by developing documentation that addressed assignment, subordination, consent, and payment priority in a standardised form. A pharmaceutical royalty equivalent would need to address anti-stacking offset allocation, definitional harmonisation across agreements, treatment of retroactive claims, and dispute resolution mechanisms that bind all holders in the stack — not just bilateral pairs. No industry body is working on this.

Second: a centralised royalty burden registry. Today, the full royalty stack on any given drug can be reconstructed only through labour-intensive analysis of SEC filings, court records, and voluntary disclosures. A registry — whether maintained by an industry association, a data provider, or a regulatory requirement — would allow all parties to see the complete picture before disputes arise. Capital for Cures' database of 50,000+ deals with royalty rates represents the most comprehensive effort in this direction, but the gap between a transaction database and a real-time burden registry remains significant.

Third: a body of precedent. The Seagen/Daiichi outcome was decided on patent validity grounds, not waterfall priority principles. The AstraZeneca/Tesaro ruling addressed definitional scope, not inter-holder priority. The market needs cases — or, ideally, published arbitration decisions — that establish norms for how anti-stacking offsets are allocated among competing holders, how retroactive claims interact with existing stacks, and how definitional mismatches are resolved when multiple agreements attach to the same revenue.

Implications for Different Market Participants

The waterfall dispute problem affects each participant in the royalty ecosystem differently.

For royalty investors, the implication is that structural due diligence — the analysis of intercreditor arrangements, anti-stacking interactions, and definitional consistency across the full stack — is now as important as commercial due diligence on the drug itself. An investor acquiring an 8% synthetic royalty on a drug generating $1 billion in net sales is not acquiring $80 million per year; they are acquiring $80 million minus whatever adjustments, offsets, and priority claims exist in the other layers of the stack. Those adjustments are not visible from the drug's sales trajectory alone.

For drug companies, the implication is that each new monetisation transaction increases the complexity of the company's royalty administration and the probability of an inter-holder dispute that the company will be drawn into — often as the entity responsible for calculating and distributing royalty payments under multiple inconsistent agreements.

For universities and research institutions — the original royalty holders whose patent royalties typically occupy the oldest layer of the stack — the deepening of structures above their position creates a risk that was barely contemplated when their licensing agreements were drafted decades ago. A university holding a 4% royalty negotiated in 2005 may find that rate effectively reduced by anti-stacking offsets triggered by monetisation transactions it had no role in negotiating.

For legal advisors, the opportunity is clear: the next generation of royalty agreements needs to be drafted with explicit awareness of the full stack, not as bilateral contracts that ignore the other claims on the same revenue. The era of the standalone royalty agreement is over. Every new royalty must be drafted as a layer in a multi-party structure, with provisions that anticipate interaction with existing and future claims.

Conclusion

The pharmaceutical royalty market is generating deeper, more complex stacks on individual drugs than at any point in its history. The structural mechanics of those stacks — priority waterfalls, anti-stacking covenants, synthetic seniority, true sale isolation — are increasingly sophisticated. But the mechanisms for resolving disputes between holders in those stacks remain primitive: bilateral litigation, private negotiation, or expensive consolidation.

The Enhertu case demonstrates the cost of that gap: five years of uncertainty, hundreds of millions in disputed royalties, and resolution on a technicality rather than on principle. As the market continues to grow — with new entrants like KKR (through HealthCare Royalty Partners), H.I.G., and others joining the established funds — the frequency of waterfall disputes will increase mechanically. More layers mean more interaction surfaces. More interaction surfaces mean more points of failure.

The infrastructure to manage that complexity is not optional. It is the difference between a market that scales efficiently and one that scales into litigation.

All information in this report was accurate as of the research date and is derived from publicly available sources including company press releases, SEC filings, court records, regulatory announcements, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. Sebastian Gensior is not a lawyer or financial adviser.