What Happens to Royalties When a Drug Gets a Label Expansion

When a royalty deal is struck, both parties are pricing a specific future. The investor models a particular patient population, a particular market, a particular competitive backdrop. The company monetises a revenue stream it believes it can forecast with reasonable confidence. Then the FDA approves a new indication, and everything changes — sometimes by billions of dollars.

Label expansion is one of the most consequential and least-discussed dynamics in pharmaceutical royalty financing. The question of who captures that upside — or who absorbs the structural risk — depends entirely on contract language that was drafted years before the approval came through. In most cases, those contracts were not written with a $6 billion indication in mind.

This article examines the mechanics of what happens to royalty streams when a drug's label grows, how different deal structures handle the resulting windfall or mismatch, and what investors and issuers should be doing differently when pricing deals in the era of platform biologics.

The Scale of the Problem

To understand why label expansion matters to royalty investors, consider the trajectory of two drugs that have defined the last decade of pharmaceutical finance.

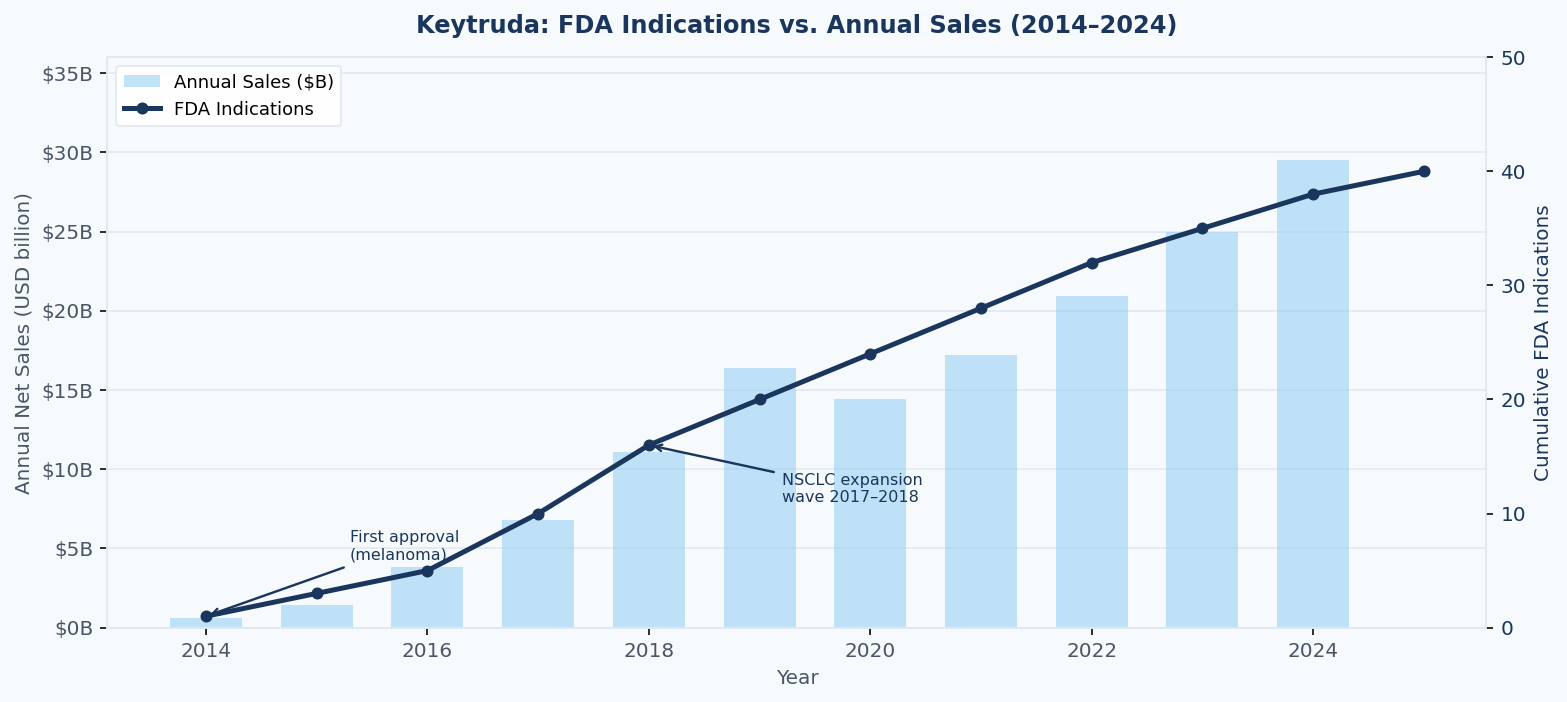

Keytruda (pembrolizumab) received its first FDA approval in September 2014 for unresectable or metastatic melanoma. At that point, it was a high-interest oncology asset, but its market was defined. A royalty investor pricing a deal in 2014 or 2015 was underwriting exposure to melanoma — a meaningful but ultimately bounded indication.

What actually happened is now pharmaceutical history. By the end of 2024, Keytruda held approximately 40 FDA-approved indications across 19 cancer types, generated $29.5 billion in annual net sales (Merck 8-K filed February 4, 2025), and accounted for nearly half of Merck's total revenue. Each approval added a new patient population, each combination regimen opened a new reimbursable use case, and each label expansion compounded on the last.

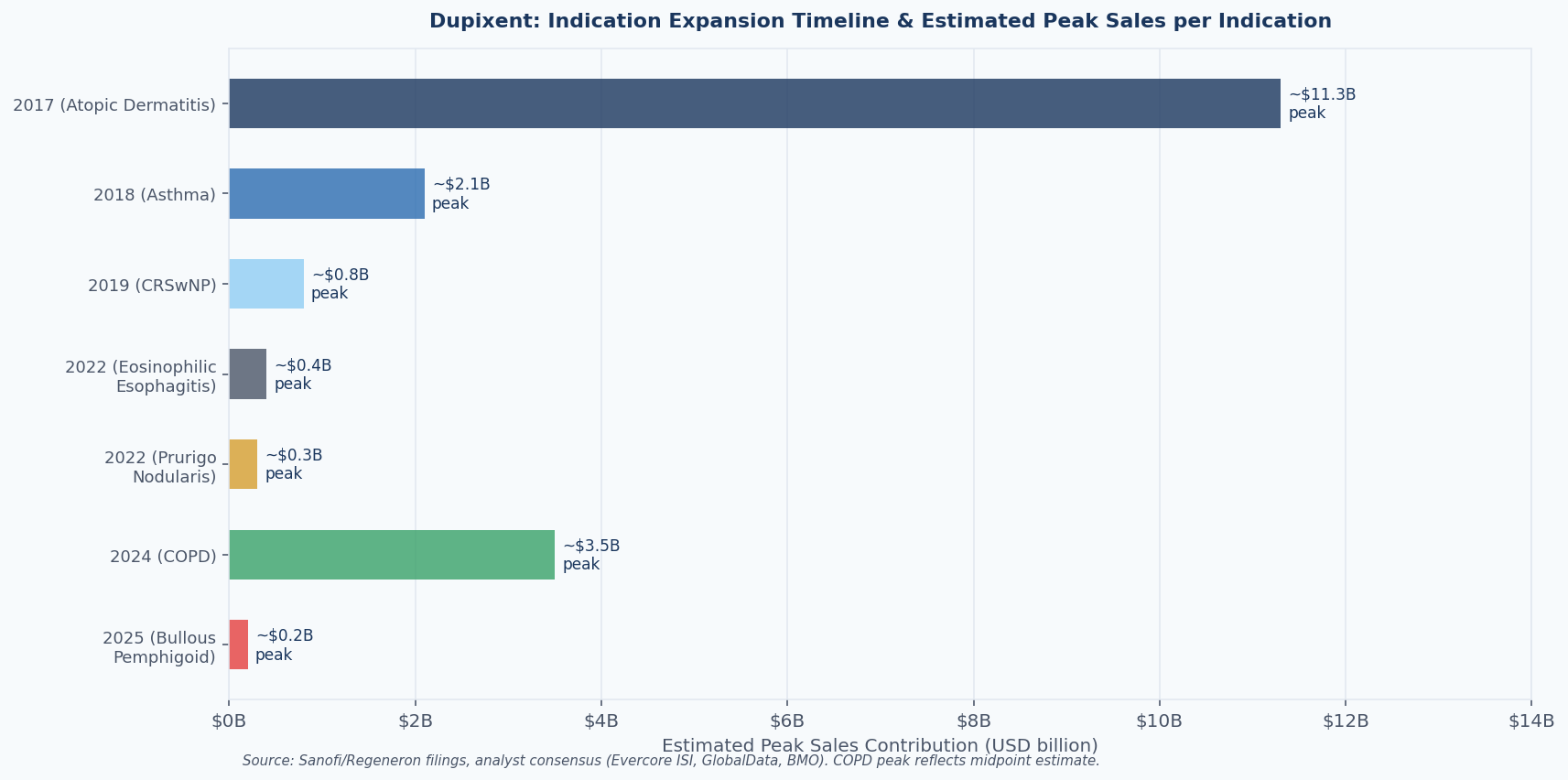

The same dynamic, playing out in immunology rather than oncology, can be observed in Dupixent (dupilumab). First approved in 2017 for atopic dermatitis, the IL-4/IL-13 inhibitor from Sanofi and Regeneron now carries nine indications as of early 2026.

In September 2024, it became the first biologic approved for COPD — a $30 billion addressable respiratory market — and analysts at Evercore ISI projected that indication alone would add $3.5 billion in peak global sales. GlobalData modelled an even more bullish case, estimating the COPD indication could contribute $6.57 billion by 2033.

Figure 1: Keytruda's cumulative FDA indications and annual net sales, 2014–2024. The correlation between indication count and revenue growth illustrates why label expansion is a primary driver of royalty asset value — and why deals priced on early-stage label assumptions frequently misvalue the underlying stream. Sources: Merck annual reports; FDA approval history via NCI SEER.

For a royalty investor who bought into either of these assets in their early years, the question of contract scope is not academic. It is the difference between capturing a modest return on a single-indication drug and participating in a platform franchise worth tens of billions.

What Royalty Contracts Actually Say

Most standard royalty agreements define the royalty base by reference to "Net Sales of the Licensed Product." The critical variable is how "Licensed Product" and "Net Sales" are defined, because these definitions — often buried in pages of boilerplate — determine whether new indications flow through to the investor's royalty calculation or not.

There are three primary structures in use, and they produce radically different outcomes at label expansion.

The Broad Product Royalty

In this structure, the royalty is calculated on total net sales of the product, regardless of indication. This is the dominant structure in traditional royalty buyouts, where an investor acquires a portion of existing royalty rights from a licensor who already holds them under a licensing agreement with a pharmaceutical company.

Because the underlying licence is typically broad — the pharma licensee has rights to the entire product — the royalty stream naturally captures all sales, across all uses.

Under this structure, label expansion is pure upside for the investor. When Keytruda received its NSCLC approvals in 2015 and 2016, or its adjuvant NSCLC approval in January 2023, every incremental sales dollar from those new populations flowed through the same royalty calculation. No contractual mechanism was needed. The investor's rate applied to a growing base.

This is the structure Royalty Pharma typically acquires when it purchases royalties from academic institutions or from biotech licensors. The University of Zurich's royalty on emicizumab (Hemlibra), for example, flows on all net sales of the product globally — it is not carved to haemophilia A alone.

When Roche pursued additional approvals for emicizumab in inhibitor-negative patients and in paediatric populations, Royalty Pharma's position benefited automatically.

The Indication-Specific Royalty

In synthetic royalty financings — deals where a company sells an investor a royalty on its own product's future sales in exchange for upfront capital — the royalty is frequently defined by reference to a specific approved use. The investor is providing development capital tied to a particular indication, and the royalty is scoped accordingly.

Under this structure, label expansion to new indications does not flow through to the royalty calculation unless the contract explicitly provides for it. The investor holds a royalty on Indication A. When Indication B is approved and generates $2 billion in additional revenue, the investor receives nothing. The entire value of the expansion accrues to the company.

This creates what might be called the label expansion gap — a structural mismatch between the asset's actual commercial trajectory and the investor's economic participation in it. The company used the investor's capital to develop and approve Indication A, but once the platform is de-risked, subsequent indications represent largely costless upside that the company captures in full.

From a company's perspective, this is entirely intentional. Synthetic royalty financings are designed to monetise a defined revenue stream while preserving the company's optionality on future value. Giving an investor a broad product royalty on a platform molecule at early-stage pricing would be extraordinarily expensive in hindsight.

The Anti-Substitution / Overlap Clause

A third structure, increasingly common in deals involving platform biology or pipeline molecules with multiple active programmes, uses explicit anti-substitution language to address the label expansion question directly.

The clearest recent example is Royalty Pharma's $2 billion funding agreement with Revolution Medicines, announced June 24, 2025 (Revolution Medicines 8-K, filed June 24, 2025). The deal centred on a synthetic royalty on daraxonrasib, Revolution's lead RAS(ON) inhibitor, for its cancer indications — primarily pancreatic ductal adenocarcinoma (PDAC). Revolution also had a second RAS inhibitor, zoldonrasib, in clinical development.

The agreement included an explicit provision: if zoldonrasib receives approval for the same indications as daraxonrasib, zoldonrasib's sales in those indications are folded into the royalty base. If zoldonrasib is approved only in different indications, it remains outside the royalty.

The clause is designed to prevent a scenario where Revolution effectively substitutes one molecule for another — using the investor's capital to de-risk the first asset, then migrating commercial activity to the second once it is approved, leaving the royalty holder with a degraded base.

The royalty rates are tiered: 4.55% on the first $2 billion in annual net sales, 2.50% on $2–4 billion, 1.00% on $4–8 billion, and zero above $8 billion. This anti-substitution clause is directionally sensible, but it only protects against one specific risk: product substitution within the same indication. It does not address the broader label expansion question for daraxonrasib itself — a meaningful consideration given that RAS inhibitors are under investigation across multiple solid tumour types beyond pancreatic cancer.

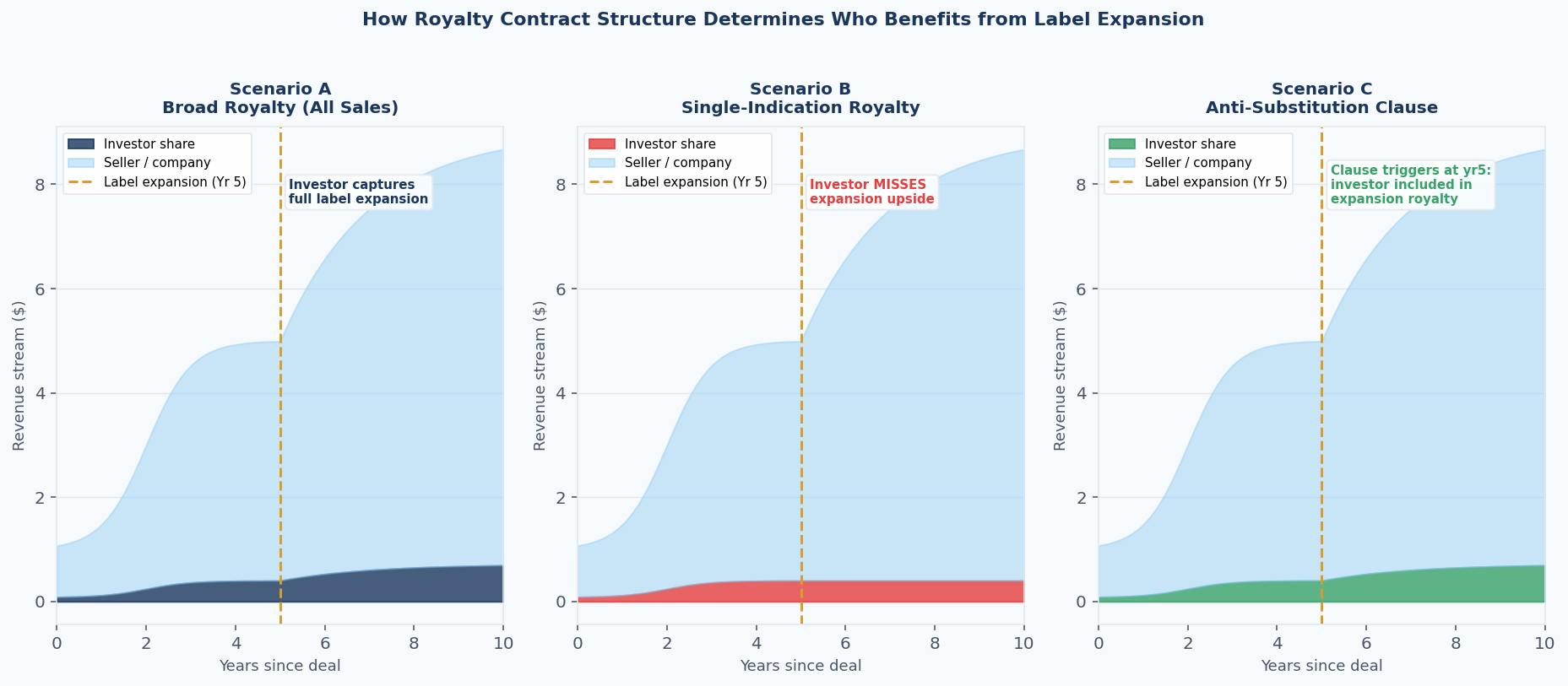

Figure 2: How three royalty contract structures perform when a new indication is approved at Year 5. Scenario A (broad product royalty) captures the expansion automatically. Scenario B (indication-specific royalty) misses it entirely. Scenario C (anti-substitution clause) provides partial protection by triggering inclusion at the point of approval. Note: figures are illustrative.

Dupixent: A Masterclass in Indication Stacking

No drug illustrates the compounding dynamics of label expansion better than Dupixent. Because dupilumab's IL-4/IL-13 mechanism is relevant to any condition driven by type 2 inflammatory pathways, its indication runway was always unusually long — but its commercial magnitude was not obvious at the time of early financing deals.

Dupixent was first approved in March 2017 for moderate-to-severe atopic dermatitis in adults. By any reasonable standard at the time, it was a significant but bounded opportunity: a biologic for eczema in a market where biologics had struggled with reimbursement.

Sanofi's collaboration with Regeneron was already in place from 2014, with Regeneron retaining co-commercialisation rights in the US and receiving a share of profits on sales from Sanofi's territory. That collaboration structure was designed around what dupilumab then was — not what it would become.

What it became is now one of the most important royalty assets in biopharma. Global net sales reached $14.15 billion in 2024, a 22% increase over 2023 (Regeneron 8-K, filed February 4, 2025; SEC EDGAR accession 0001804220-25-000007).

The September 2024 approval for COPD — the seventh indication, and the first biologic ever approved for that disease — opened a patient population estimated at 300,000 in the US alone for the eosinophilic phenotype. By early 2026, Dupixent carries nine indications including bullous pemphigoid (approved June 2025), with chronic spontaneous urticaria (CSU) having been under FDA review through mid-2025.

Figure 3: Dupixent's indication expansion timeline and estimated peak sales contribution per indication, based on analyst consensus and company guidance. Atopic dermatitis remains the dominant revenue driver, but COPD is the highest-value expansion. Sources: Sanofi FY2024 results; Regeneron FY2024 8-K (SEC EDGAR); Evercore ISI via FiercePharma; GlobalData via BioSpace.

For Regeneron, which receives a share of profits on Dupixent sales from Sanofi outside the US co-commercialisation territory, each new indication is incremental revenue with effectively zero incremental development cost at the royalty level — the investment was made once at the compound level, and the indication-by-indication approvals harvest the value of that earlier scientific bet.

For any investor who had purchased a royalty on Dupixent scoped only to atopic dermatitis, the picture would be quite different. Atopic dermatitis accounted for 73.3% of Dupixent's revenue share in 2024 — a declining fraction year by year as COPD, CSU, and other new indications ramp. An atopic dermatitis-only royalty would have missed roughly one quarter of 2024 revenues already, with more dilution coming.

How the Market Values Indication Optionality

The central challenge in pricing a royalty deal involving a platform molecule is that future indications are probabilistic, not guaranteed. An investor cannot simply buy a broad product royalty and assume all possible future label expansions materialise — some will fail in Phase III, some will not achieve commercial reimbursement, and some will face competition before they reach meaningful sales.

What the market has increasingly done is attempt to price indication optionality explicitly, rather than ignore it or absorb it implicitly.

In practice, this takes several forms.

Tiered royalty rates with indication floors. Some deals use a base royalty rate that steps down if additional indications are approved, on the logic that the investor's risk-adjusted return was calibrated to a specific commercial scenario, and that extraordinary success should be shared more equitably.

The BioCryst/Royalty Pharma deal for Orladeyo, announced December 7, 2020, is the canonical example (BioCryst 8-K, filed December 7, 2020; SEC EDGAR): 8.75% on first $350 million in sales, stepping to 2.75% on the next tranche, and zero beyond $550 million. The structure acknowledges that peak success should benefit the company more than the investor, since the investor's return model was not built on a blockbuster scenario.

Milestone-gated tranches tied to new indication approvals. In development-stage financings, tranches of capital are often conditioned on regulatory milestones — including new indication approvals. This allows the investor to commit initial capital at lower risk while retaining the right to participate in an expanded programme if it materialises.

The Revolution Medicines/Royalty Pharma structure follows this logic precisely: $250 million pre-approval, a second $250 million tranche contingent on positive Phase 3 PDAC data, and three further optional tranches of $250 million each post-approval.

Each additional tranche is effectively priced on the probability of the next indication clearing, rather than on a single upfront assessment of the entire opportunity.

Explicit indication expansion rights. A small but growing number of deals include explicit contractual rights for the royalty holder to include future indications in the royalty base upon approval, at a pre-agreed economics. These are difficult to negotiate because companies are understandably reluctant to pre-commit the economics of future indications at the point of initial deal-signing — the leverage dynamics change considerably once a platform is de-risked.

But they are appearing in deals where the investor is providing substantial early capital and where the compound's mechanism strongly suggests multi-indication potential.

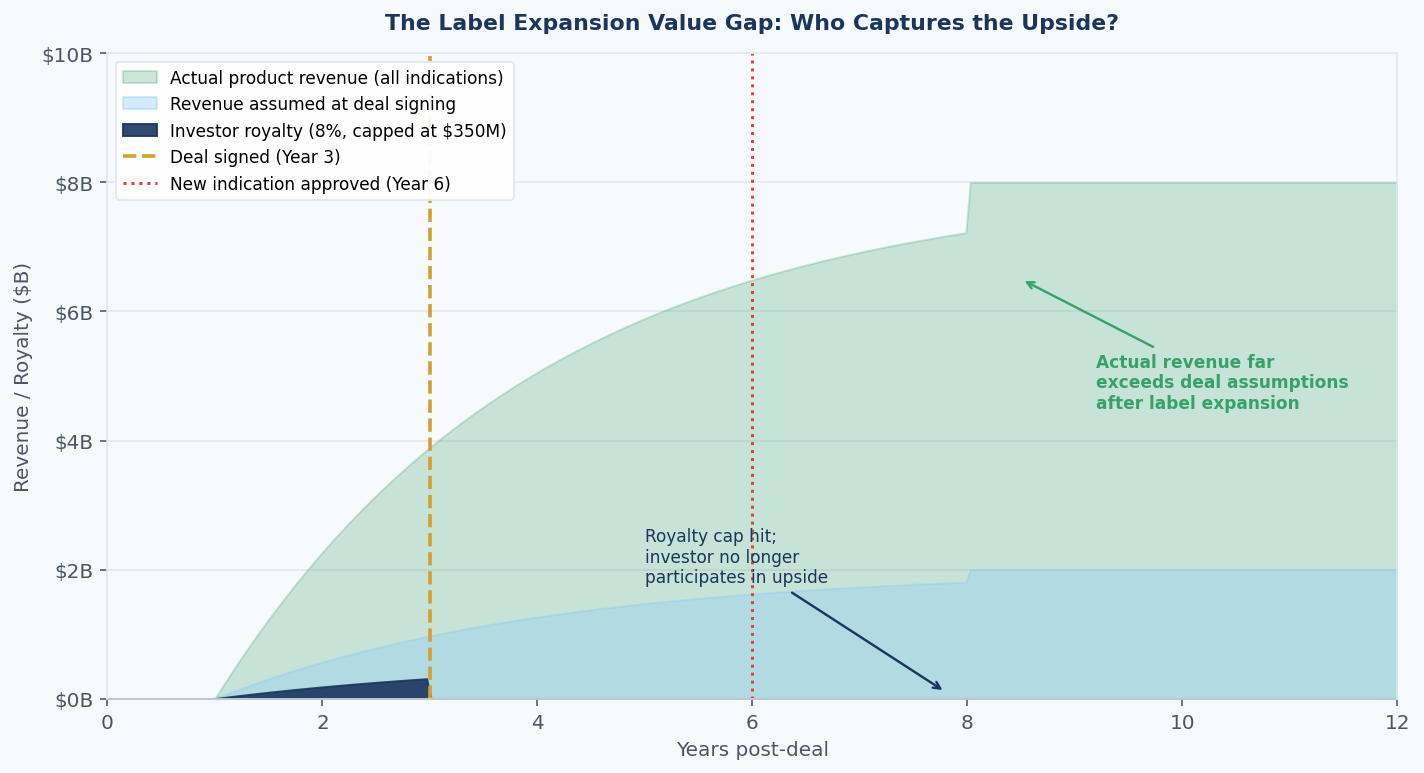

Figure 4: Illustrative value gap between assumed revenue at deal signing, actual revenue following label expansion, and the royalty investor's economically-capped participation. When a royalty is structured with a hard cap and indication scope, the investor's share of total value declines sharply after approval of new indications. Note: figures are illustrative.

The Modelling Problem

From a valuation standpoint, label expansion creates a compound uncertainty that most royalty models handle poorly. Standard royalty valuation methodology — discounted cash flow on a probability-weighted revenue forecast for the known indication — is not designed to capture the option value of indications that do not yet have Phase 3 data.

The academic literature on royalty valuation has begun to address this, using real options approaches to model indication pipelines as sequential options with interdependent probabilities. If a compound receives approval for Indication A, that event materially updates the probability of approval for Indication B (particularly where the same mechanism is relevant), and any royalty valuation model that does not account for this correlation will systematically undervalue broad-spectrum assets in early licensing.

In practice, the more relevant question for deal structuring is not how to model the full option value — it is how to allocate it between the parties. A few working principles have emerged from market practice.

First, investors who provide capital at early clinical stages should expect to participate meaningfully in the product's commercial success, including expansion to additional indications, if the royalty is to compensate appropriately for the risk taken. Early-stage royalty rates in the 8–12% range are calibrated on binary risk (approve or fail), not on a scenario where the compound becomes a multi-indication platform.

If the latter scenario materialises but the royalty is indication-specific, the investor has effectively subsidised a franchise they do not own.

Second, companies should expect to pay a premium — either in rate or in breadth — when seeking capital from royalty investors on platform compounds. The investor community has learned from Keytruda's 40-indication trajectory, Dupixent's nine-indication expansion, and AbbVie's Skyrizi — which grew 50.9% to $11.7 billion in 2024 driven by multiple inflammatory indications — that type 2 immunology and immuno-oncology compounds can compound their indications faster than any single deal modelled.

Pricing deals as if the current indication is the last one is not credible, and sophisticated investors will reflect the indication optionality in their return requirements.

Third, the gap between these two positions — investor wanting broad participation, company wanting to preserve optionality — is precisely where deal structuring has become more creative. Anti-substitution clauses, milestone-gated indication inclusions, and IRR-based waterfalls that reset upon material label expansion are all mechanisms designed to bridge this gap without requiring either party to solve the probability problem at signing.

Practical Implications for Deal Structuring

For practitioners on both sides of royalty transactions involving platform compounds, the label expansion question should be addressed explicitly in term sheets rather than left to interpretation of standard product royalty definitions.

On the investor side, the key questions at due diligence are: what is the mechanism, and how many disease states does it plausibly address?

For a narrow-spectrum small molecule with a single addressable indication, the scope question matters little. For a biologic targeting a pathway implicated in multiple inflammatory conditions — or a checkpoint inhibitor being evaluated across 30+ tumour types — the scope of the royalty base is material to any credible return model.

On the company side, the relevant question is not simply what you are willing to give but what expansion scenarios you would be comfortable sharing with an investor.

If the company's internal view is that the compound has realistic probability of approval in two or three additional indications within the royalty's life, pre-agreeing the economics of that expansion at current pricing is almost always cheaper than raising equity later at a higher valuation.

The investor takes the indication risk; the company retains operational control.

The deals that have aged worst for investors are those where the product succeeded spectacularly in its first indication, rapidly became commercially de-risked, and then collected multiple additional indications with no benefit flowing to the royalty holder who provided the original capital.

The deals that have aged worst for companies are those where a broad product royalty was granted at an early-stage rate that was never repriced, and which proved extraordinarily expensive once the compound became a platform.

The market is slowly building the contract language to avoid both failure modes. But slowly is the operative word — most deals are still being written with inadequate treatment of the label expansion scenario, often because addressing it explicitly requires both parties to commit to positions on probability and value that neither is comfortable disclosing.

What Investors Should Watch in 2026

As of early 2026, the drugs most likely to generate significant royalty-relevant label expansions in the near term include:

- Dupixent: CSU decision was targeted for April 18, 2025, with additional pipeline indications in lichen simplex chronicus and food allergy in development per Regeneron's FY2024 8-K. Projections from GlobalData suggest revenue could reach $23.6 billion by 2030.

- Keytruda Qlex: The subcutaneous formulation, approved September 19, 2025 across 38 solid tumour indications, represents lifecycle management ahead of the IV formulation's compound patent expiry in December 2028. Merck received a new indication for HER2-positive gastric/GEJ cancer with PD-L1 CPS ≥ 1 on March 19, 2025, and more approvals are expected.

- GLP-1/GIP agonists: Semaglutide and tirzepatide continue to expand their labels across cardiovascular, renal, and additional metabolic indications. Ozempic generated $17.5 billion in sales in 2024 and Mounjaro $11.5 billion; any royalty deal tied to a single indication within these franchises carries material scope risk.

- daraxonrasib (Revolution Medicines): Phase 3 PDAC results are expected in 2026 per Revolution Medicines' Q4 2025 8-K (SEC EDGAR). The RAS(ON) programme spans pancreatic, lung, and colorectal cancer — a breadth of indication potential that makes the scope of the Royalty Pharma deal's anti-substitution clause a live question.

For royalty investors already holding positions in any of these assets, the practical question is whether existing deal documentation captures the expansion or not. For investors considering new positions, the question is how to structure a deal that reflects the actual risk-return profile of a platform asset rather than the single-indication proxy.

The answer will vary by asset and by transaction type. But the principle is consistent: in an era of platform biology, treating royalty scope as a boilerplate matter is the fastest way to price yourself out of your own thesis.

All information in this report was accurate as of the publicattion date and is derived from publicly available sources including company press releases, SEC filings, regulatory announcements, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice.

Member discussion