Anti-Dilution Mechanics in Synthetic Royalty Agreements: Protecting Investor Economics When the Underlying Asset Gets Sublicensed, Reformulated, or Combined

When Royalty Pharma commenced dispute resolution proceedings against Vertex Pharmaceuticals over the royalty treatment of Alyftrek — arguing that deutivacaftor is "the same as" ivacaftor and therefore royalty-bearing at approximately 8%, while Vertex paid only approximately 4% — the dispute crystallised something that synthetic royalty practitioners have long understood but rarely confronted so publicly: the single most dangerous risk to a royalty investor is not clinical failure or patent expiry.

It is definitional erosion — the slow or sudden narrowing of the royalty base through commercial decisions that the operating company controls and the investor does not.

Alyftrek is a combination of vanzacaftor, tezacaftor, and deutivacaftor, approved by the FDA in January 2025 as a next-generation cystic fibrosis therapy intended to succeed Trikafta. The contractual question — whether a deuterated analogue of a royalty-bearing compound remains royalty-bearing — is worth hundreds of millions of dollars over the product's commercial life and illustrates the three fundamental vectors through which royalty economics can be diluted: sublicensing, reformulation, and combination.

This article maps the anti-dilution problem set in synthetic royalty agreements, examines the contractual architecture that sophisticated investors deploy to protect their economics, and grounds each mechanism in recent transaction practice from 2025 and 2026.

The synthetic royalty as a contractual asset: why anti-dilution is structural, not cosmetic

A synthetic royalty is not a licence royalty. In a traditional royalty monetisation, the investor acquires a pre-existing payment obligation — a licensee already owes a licensor a percentage of net sales, and the investor buys the right to receive that stream. The payment obligation and its definitions were negotiated between licensor and licensee, often years earlier, with their own commercial logic.

A synthetic royalty, by contrast, is manufactured by the financing transaction itself. The operating company creates a new contractual obligation to pay a percentage of its own product's net sales to the investor, in exchange for upfront capital. There is no upstream licensor dictating terms.

The definitions — what counts as "the product," what counts as "net sales," what happens when the product is sublicensed or reformulated or combined — are negotiated between the company and the investor, and they are the entire architecture on which the investor's return depends.

From 2020 through 2024, royalty financings in biopharma totalled approximately $29.4 billion, more than double the amount raised in the preceding five years, with synthetic structures gaining prominence within that trend. Royalty Pharma alone deployed nearly $2.8 billion in capital in 2024, including a $950 million royalty acquisition on Amgen's Imdelltra and a $2 billion funding arrangement with Revolution Medicines encompassing $1.25 billion in synthetic royalty funding and up to $750 million in secured debt. As recently as April 2026, Apnimed secured up to $150 million from HealthCare Royalty Partners with a synthetic royalty component equal to a low single-digit percentage of AD109 net sales.

At these capital magnitudes, the anti-dilution question is not a drafting nicety. It is the structural determinant of whether the investor receives its target return.

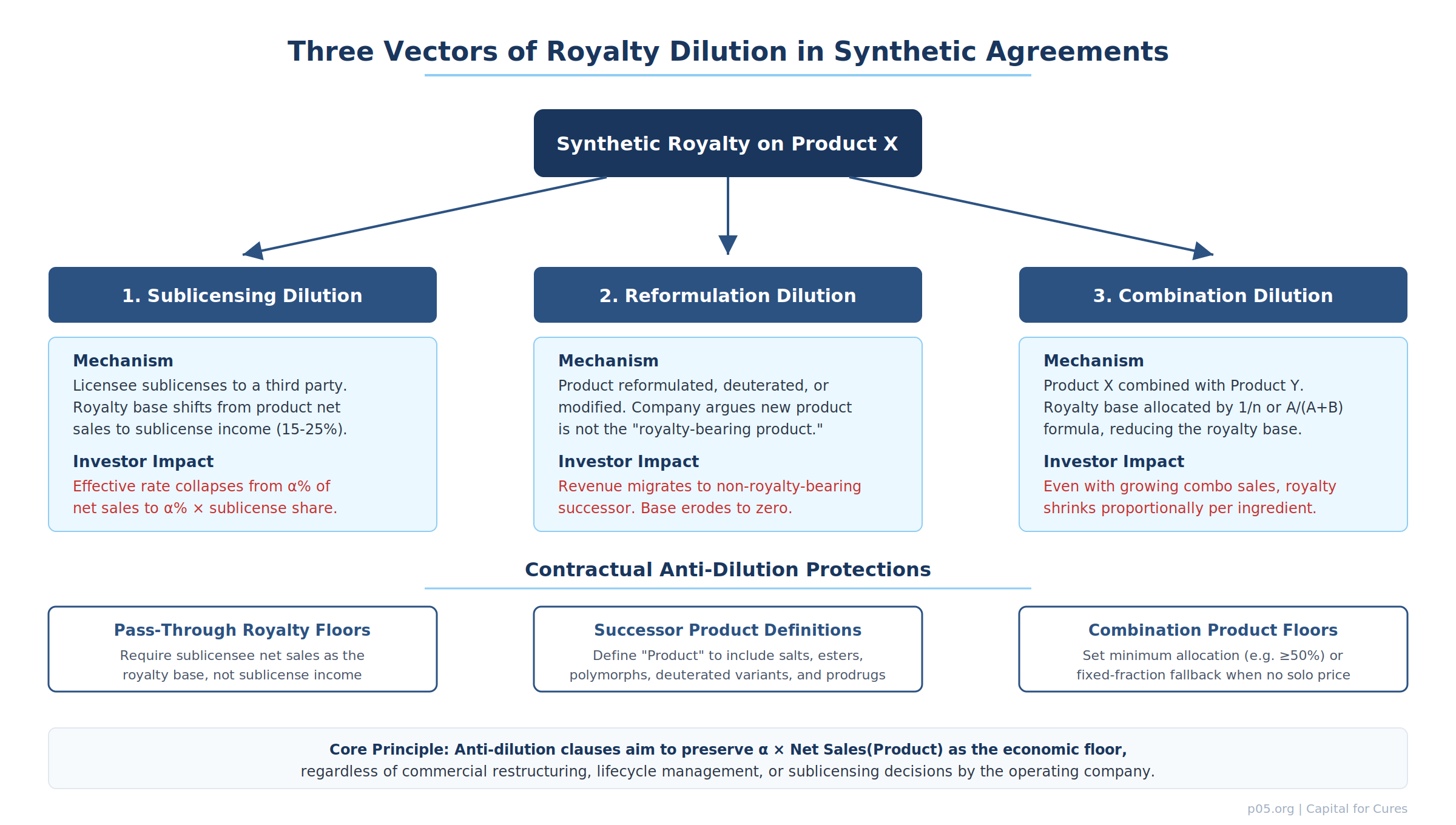

Three vectors of royalty dilution

The conceptual framework for anti-dilution in synthetic royalties can be organised around three distinct mechanisms by which the effective royalty base — and therefore the investor's absolute dollar return — can shrink without any decline in the underlying product's therapeutic or commercial value.

1. Sublicensing dilution

The operating company sublicenses commercialisation rights to a third party. If the synthetic royalty agreement calculates the investor's payment based on "net sales of the product," the question becomes: whose net sales? The sublicensee's sales to end customers, or the sublicense income (upfront, milestones, and running royalties) received by the operating company from the sublicensee?

The distinction is enormous. If the sublicensee pays the operating company a 15–25% royalty on net sales (a common range for sublicensing consideration in pharmaceutical agreements), and the investor's synthetic royalty is calculated on that sublicense income rather than on the sublicensee's product sales, the effective royalty rate collapses. A 7% synthetic royalty on $1 billion in sublicensee net sales yields $70 million; a 7% royalty on 20% sublicense income from the same $1 billion yields $14 million.

The Covington guide to synthetic drug royalty dealmaking identifies negative covenants that "concentrate on protecting the purchaser's right to net sales payments through restrictions on sales and licences of, and liens on, product assets" as a core feature of the covenant architecture. The sublicensing vector is precisely why those restrictions exist: without them, the operating company can lawfully redirect the economic value of the product into a sublicensing relationship that the investor cannot reach at the same rate.

2. Reformulation dilution

The operating company reformulates, deuterates, pegylates, or otherwise modifies the royalty-bearing compound and argues that the new product is a distinct molecule, not the "product" as defined in the synthetic royalty agreement. Revenue migrates from the royalty-bearing original to the non-royalty-bearing successor.

The Vertex/Royalty Pharma dispute over Alyftrek is the canonical 2025 illustration. Royalty Pharma's position, as stated in its Q4 2024 10-K, is that deuterated ivacaftor (deutivacaftor) is "the same as" ivacaftor and is therefore royalty-bearing, which would yield a blended royalty of approximately 8% on Alyftrek sales. Vertex's position is that deutivacaftor is a distinct compound, yielding a blended royalty of approximately 4%. The combination product's allocation formula (sales allocated equally to each active pharmaceutical ingredient) then determines whether the ivacaftor-lineage component carries royalty obligations.

This is not an academic distinction. By late 2025, Royalty Pharma disclosed that Vertex had not paid the full amount of royalty receipts on Alyftrek net sales to which RPRX believed it was contractually entitled, and that RPRX had commenced the dispute resolution process contemplated by the agreements. The outcome will set market precedent for how reformulation language is drafted in every future synthetic royalty agreement.

3. Combination dilution

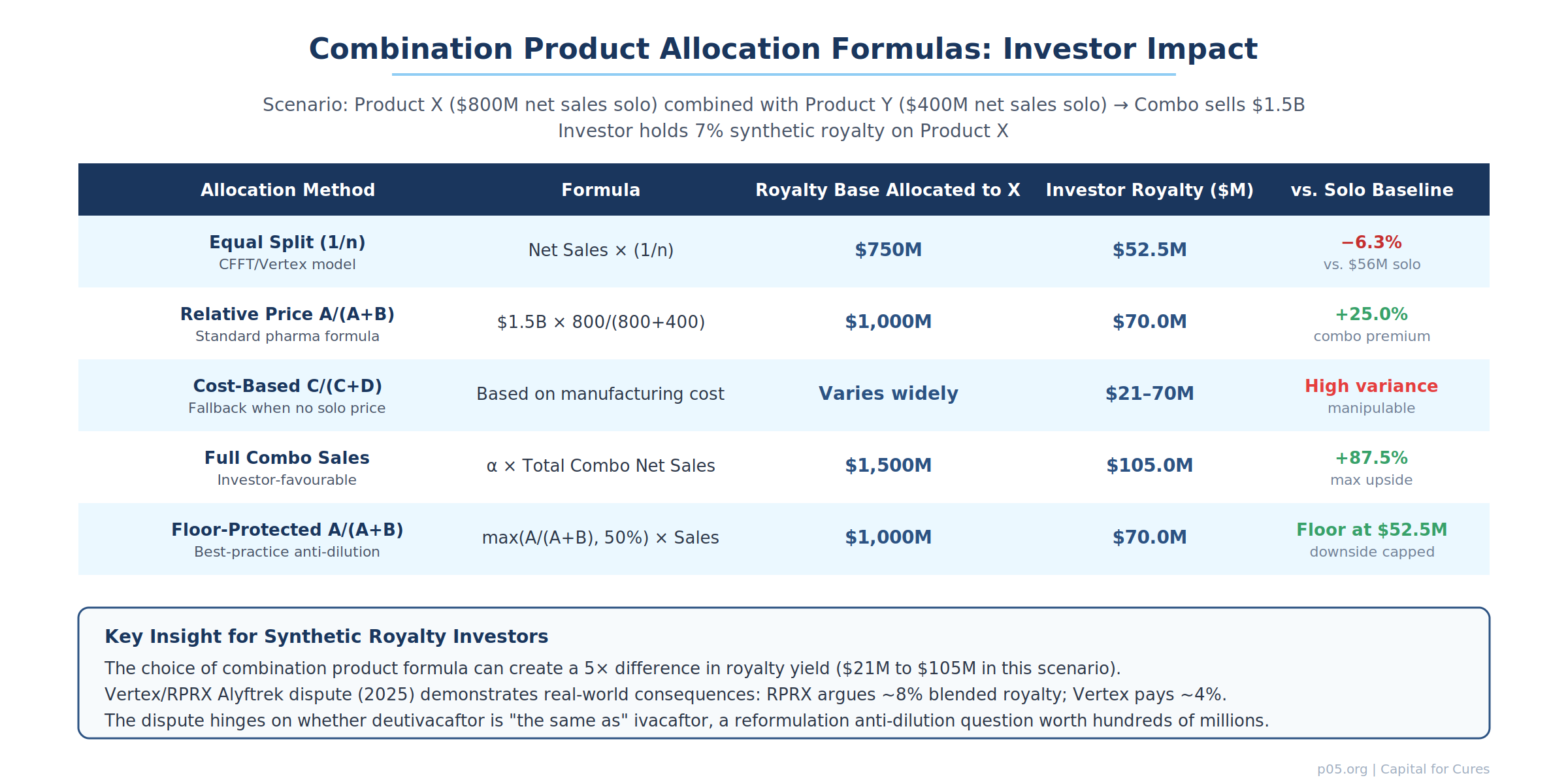

The royalty-bearing product is combined with one or more additional active ingredients into a fixed-dose combination. Even if the combination sells more than the standalone product ever did, the royalty base is allocated across ingredients, potentially halving or thirding the investor's effective base.

The standard pharmaceutical industry approaches to combination product allocation, visible across dozens of SEC-exhibited licence agreements, follow a hierarchy: the relative-price formula A/(A+B) when both components are sold separately; the cost-based formula C/(C+D) when only one is sold separately; and the equal-split formula 1/n when neither is sold separately. The CFFT/Vertex CF agreements, for example, used the 1/n equal-split method, allocating net sales equally to each active pharmaceutical ingredient, with no royalty paid on portions allocated to non-royalty-bearing components.

For investors, the allocation formula is not neutral. As the diagram below illustrates, the choice of method can produce a 5× difference in effective royalty yield on identical underlying commercial performance.

The Imdelltra template: how BeOne/Royalty Pharma addressed reformulation risk in 2025

The BeOne Medicines/Royalty Pharma transaction, announced in August 2025, provides the most instructive public example of how sophisticated parties are now drafting product definitions to pre-empt reformulation dilution.

The SEC-exhibited Royalty Purchase Agreement defines the royalty-bearing asset as "any and all products that consist of the monoclonal antibody Imdelltra (tarlatamab), in any strengths, forms (including pegylated versions), formulations (whether short-acting or long-acting), administrations or delivery routes." This is not accidental verbosity. The parenthetical inclusions — pegylated versions, short-acting or long-acting formulations, all delivery routes — are each a specific anti-dilution defence against lifecycle management strategies that Amgen might pursue.

Consider the implications: if Amgen develops a long-acting subcutaneous formulation of tarlatamab to replace the current intravenous infusion (a common lifecycle strategy for monoclonal antibodies), the investor's royalty base is explicitly preserved. If Amgen pegylates tarlatamab for extended half-life, the royalty base is explicitly preserved. The definition anticipates the reformulation playbook and closes it contractually.

The transaction also structures territorial anti-dilution: Royalty Pharma receives royalties on worldwide net sales excluding China, where BeOne retains commercial rights. Critically, the seller retains a share of royalty payments on annual Imdelltra ex-China net revenue above $1.5 billion — a tiered structure that aligns interests while protecting the investor's base economics below the threshold.

The deal's total consideration of up to $950 million, with a 15–18 year duration and tiered declining royalty rates, reflects the capital markets' pricing of both the clinical opportunity (Imdelltra received FDA accelerated approval in May 2024 for small-cell lung cancer) and the contractual robustness of the anti-dilution architecture.

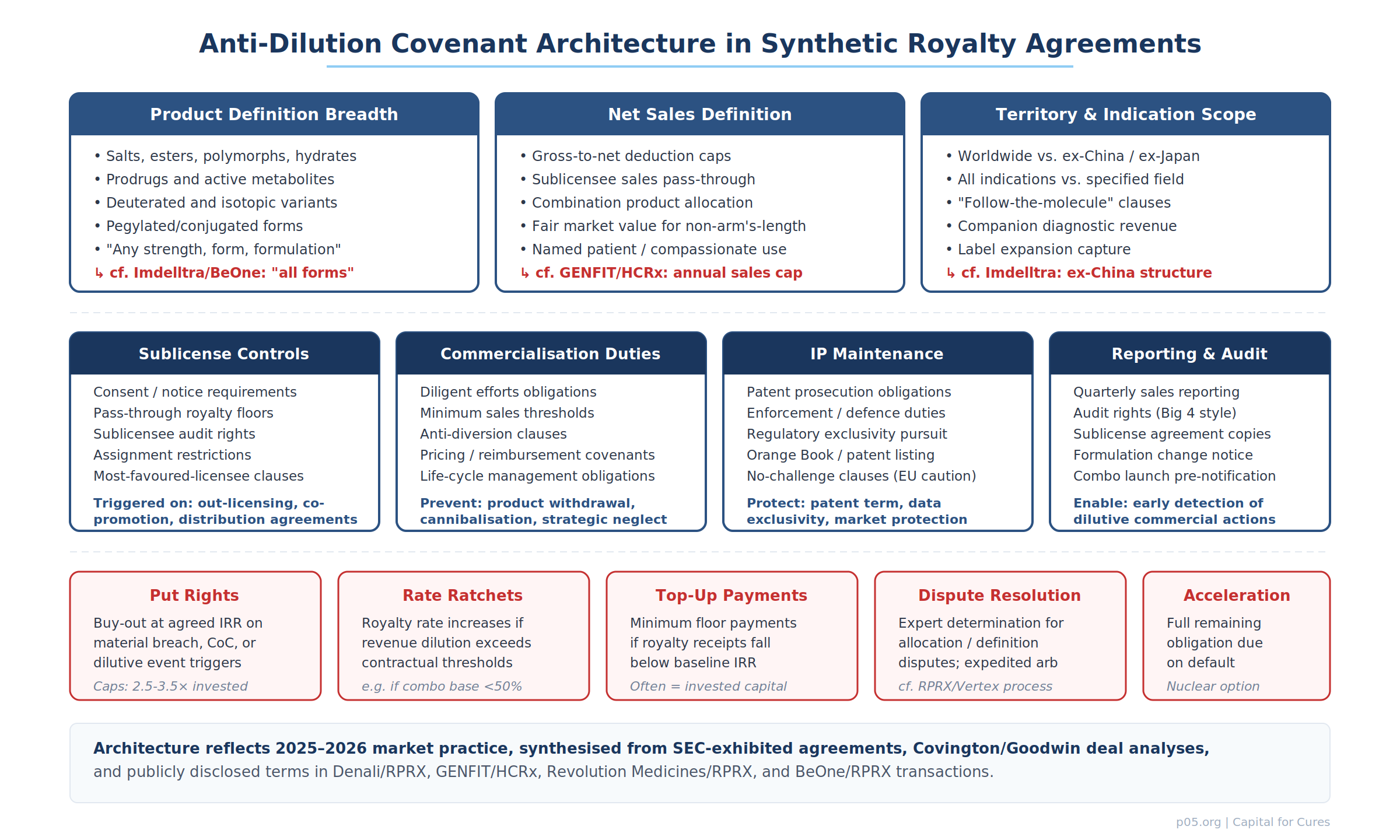

Anti-dilution covenant architecture: three layers of protection

Modern synthetic royalty agreements deploy anti-dilution protections across three nested layers: definitional, operational, and remedial.

Layer 1: Definitional protections

The first line of defence is definitional breadth. Product definitions in well-drafted synthetic royalty agreements now routinely include salts, esters, polymorphs, hydrates, solvates, prodrugs, active metabolites, deuterated variants, pegylated conjugates, antibody-drug conjugates, bispecific formats, and any other modification of the active pharmaceutical ingredient. The goal is to define the "product" as the therapeutic franchise, not the specific molecule as filed in the original NDA/BLA.

Net sales definitions carry their own anti-dilution mechanics: caps on gross-to-net deductions (preventing artificial inflation of discounts, rebates, or chargebacks to reduce the royalty base), fair market value imputation for non-arm's-length transfers, inclusion of sublicensee sales on a pass-through basis, and specified allocation formulas for combination products with minimum floors.

Territory and indication definitions must similarly anticipate expansion: "follow-the-molecule" clauses that capture revenue from new indications, supplemental approvals, paediatric extensions, and geographic launches not contemplated at the time of the original financing.

Layer 2: Operational covenants

The second layer constrains the operating company's commercial discretion in ways that protect the royalty base.

Sublicense controls typically require investor consent for, or at minimum advance notice of, any sublicensing, out-licensing, co-promotion, or distribution arrangement that would alter the identity of the entity generating product net sales. The most protective formulations require that any sublicensee's net sales be included in the royalty base on a pass-through basis — that is, the investor's royalty is calculated on the sublicensee's sales to end customers, not on the sublicense consideration flowing to the operating company.

Commercialisation duties impose affirmative obligations: diligent efforts to commercialise, minimum sales thresholds (sometimes linked to consensus forecasts), anti-diversion clauses preventing strategic cannibalisation of the royalty-bearing product by a non-royalty-bearing successor, and lifecycle management obligations requiring the company to pursue label expansions, geographic launches, and formulation improvements that sustain or grow the revenue base.

IP maintenance covenants require the company to prosecute and defend relevant patents, pursue regulatory exclusivity (orphan, paediatric, data exclusivity), maintain Orange Book listings, and — critically — not settle patent challenges on terms that would accelerate generic entry without investor consent.

Reporting and audit rights enable early detection of dilutive actions: quarterly sales reporting with sublicensee breakouts, copies of sublicense agreements, advance notice of formulation changes or combination product launches, and Big 4-style audit rights exercisable at the investor's discretion.

Layer 3: Remedial protections

When covenants are breached or dilutive events occur, the agreement must provide enforceable remedies.

Put rights allow the investor to require the operating company to repurchase the royalty at an agreed price — typically a multiple of invested capital (2.5–3.5× is the current market range for pre-approval assets, 1.5–2.0× for marketed products) — upon the occurrence of specified trigger events. These triggers commonly include change of control, material breach of commercialisation covenants, bankruptcy, and (in the most investor-protective formulations) material dilutive events such as an unapproved sublicensing or product reformulation.

Rate ratchets automatically increase the royalty rate if the effective revenue base falls below a contractual threshold — for example, if combination product allocation reduces the royalty base below 50% of standalone product net sales, the royalty rate on the allocated base increases to compensate.

Top-up payments serve as a floor for the investor's return: if cumulative royalty receipts fall below a baseline amount (often equal to invested capital) by a specified date, the operating company must make a cash payment to cover the shortfall.

Dispute resolution mechanisms — expert determination, expedited arbitration, or structured escalation protocols — are not merely procedural. They are functional anti-dilution tools because they provide a forum for resolving definitional disputes (is deutivacaftor the same as ivacaftor?) without the cost and delay of full-scale litigation.

The GENFIT/HCRx template: capped royalty financing with structural guardrails

The GENFIT/HealthCare Royalty transaction, signed in January 2025 and closed in March 2025, demonstrates a different anti-dilution architecture: the capped pass-through model.

HCRx provided up to €185 million (€130 million upfront, with two additional milestone-contingent tranches of €30 million and €25 million) in exchange for a portion of the royalties GENFIT receives from Ipsen on global sales of Iqirvo (elafibranor). The structure has several distinctive anti-dilution features.

First, cumulative payments to HCRx are capped at €277.5 million to €453.25 million depending on timing and occurrence of future events, and are subject to a time-limit of no later than March 2045. Once the cap or time-limit is met, all future royalties revert to GENFIT. This is cap-as-anti-dilution: because the investor's return is bounded, both parties have reduced incentive to litigate definitional boundaries at the margin.

Second, the portion of royalties that HCRx receives is subject to an annual cap equal to the amount of royalties based on annual maximum net sales of €600 million. Above that level, GENFIT retains the incremental royalty. This is anti-dilution in reverse: it protects the company from over-transferring value in an upside scenario, while simultaneously ensuring that the investor's base return is protected by the uncapped obligation below the threshold.

Third, the royalty obligation is secured by a fiducie-sûreté — a French-law trust structure that ring-fences the royalty receivables for the benefit of HCRx. This is a structural anti-dilution mechanism: it places the cash flows beyond the reach of GENFIT's other creditors and beyond the company's unilateral control, creating a bankruptcy-remote channel for royalty payments.

Fourth, GENFIT retains rights to all regulatory, commercial, and sales-based milestone payments from Ipsen — separating the royalty stream (partially monetised) from the milestone stream (fully retained). This preserves the company's incentive to pursue label expansions and geographic approvals that would grow the royalty base from which HCRx is paid.

The sublicensing problem in depth: pass-through versus income-share models

The sublicensing anti-dilution question deserves detailed treatment because it is the mechanism most commonly underestimated by first-time synthetic royalty investors and most commonly exploited by operating companies seeking to restructure their commercial arrangements.

There are two basic models for handling sublicensee economics in a synthetic royalty agreement.

In the pass-through model, the royalty base is defined as the net sales of the product regardless of who makes the sale. If the operating company sublicenses commercialisation to a third party, the sublicensee's net sales to end customers are included in the royalty base, and the investor receives its percentage on those sales. The sublicensing event does not reduce the investor's effective rate.

In the income-share model, the royalty base shifts to the sublicense consideration received by the operating company — the sublicense royalty, the upfront payment, the milestones. Because sublicense consideration is typically a fraction of end-customer net sales (15–25% is a common running royalty range for pharmaceutical sublicenses, with lower effective rates when upfronts and milestones are amortised over the product life), the investor's effective rate on end-customer sales is dramatically reduced.

The pass-through model is unambiguously investor-favourable. But it creates operational complexity: the investor needs reporting visibility into the sublicensee's sales, audit rights over the sublicensee (or flow-through audit rights via the operating company's sublicence agreement), and mechanisms to ensure that the sublicensee's net sales definitions match the synthetic royalty agreement's definitions.

The income-share model is operationally simpler but economically punitive to the investor. It is also strategically manipulable: the operating company can structure the sublicence to minimise royalty income (for example, by accepting a larger upfront and smaller running royalty) in ways that reduce the synthetic royalty payments without reducing the total value of the sublicensing transaction.

Best practice in 2025–2026 synthetic royalty agreements is a hybrid: the pass-through model as the default, with income-share as a fallback only where pass-through reporting is genuinely impracticable (for example, in certain ex-US territory sublicenses where the sublicensee is a distributor rather than a marketer), and with investor consent required for any sublicensing arrangement that would trigger the income-share fallback.

The combination product problem: allocation formulas and their investor consequences

The combination product allocation formula is the single most technically consequential anti-dilution provision in a synthetic royalty agreement, because it determines how much of a combination product's net sales are attributed to the royalty-bearing active ingredient.

The standard pharmaceutical industry hierarchy, visible in dozens of SEC-exhibited agreements, operates as follows:

Relative price method — A/(A+B). If both the royalty-bearing product and the other active ingredient(s) are sold separately in the same country, net sales of the combination are multiplied by the fraction A/(A+B), where A is the weighted average sale price of the royalty-bearing product when sold alone, and B is the weighted average sale price of the other ingredient(s) when sold alone. This method is economically rational when solo prices exist and are commercially meaningful, but it can be manipulated through strategic pricing of the standalone product.

Cost-based method — C/(C+D). If one or both components are not sold separately, the allocation is based on fully absorbed manufacturing costs. This method is easily manipulable because manufacturing costs are internal to the operating company and bear little relationship to the therapeutic or commercial value of each ingredient.

Equal-split method — 1/n. Net sales are allocated equally among all active pharmaceutical ingredients, regardless of their relative contribution to efficacy or commercial value. This is the simplest method but can be the most dilutive to investors: if the royalty-bearing ingredient is the primary driver of efficacy and sales (as ivacaftor was for the original CF modulator franchise), equal allocation with non-royalty-bearing co-ingredients systematically undervalues its contribution.

Mutual agreement / expert determination. Where no formula produces a result, the parties negotiate or refer the allocation to an independent expert. This is the most uncertain outcome for investors and should be treated as a drafting failure rather than a viable allocation mechanism.

For synthetic royalty investors, the anti-dilution implications are clear: the allocation formula must be specified at the time of the financing, not left to future negotiation; minimum allocation floors (e.g. no less than 50% of combination net sales attributed to the royalty-bearing product) should be included as a structural protection; and the operating company's ability to launch a combination product that includes the royalty-bearing ingredient without investor consent should be subject to covenant restrictions.

Recent transaction landscape: anti-dilution features in practice

The 2025–2026 transaction landscape illustrates the rapid evolution of anti-dilution practice.

The Denali Therapeutics/Royalty Pharma transaction (December 2025) — $275 million for a 9.25% synthetic royalty on tividenofusp alfa — deployed a multiple-based cap structure (3.0× invested capital, reducing to 2.5× if reached by Q1 2039) that implicitly addresses anti-dilution by bounding the investor's maximum payment obligation. The cap functions as a mutual anti-dilution mechanism: it protects the company from over-paying in an upside scenario while ensuring the investor's returns are secured within a defined multiple, regardless of how the royalty base might be restructured over the product's commercial life.

The Revolution Medicines/Royalty Pharma arrangement (June 2025) — $2 billion total, including $1.25 billion in synthetic royalty funding — represents the largest synthetic royalty financing to date and reportedly includes tiered royalty rates keyed to sales thresholds, change-of-control put rights, and acceleration provisions. The scale of the transaction implies a correspondingly sophisticated anti-dilution architecture, though the full covenant package has not been publicly exhibited.

The SWK Holdings/Runway Growth Finance merger, which closed in April 2026, illustrates a different dimension of anti-dilution risk: what happens to the synthetic royalty investor's protections when the financing entity itself undergoes a change of control. SWK's portfolio included structured debt, traditional royalty monetisations, and synthetic royalty transactions, and the merger required careful treatment of existing royalty holder rights under the combined entity — including a supplemental indenture adding restrictive covenants and an additional event of default to comply with Investment Company Act requirements.

For synthetic royalty investors in SWK's portfolio companies, the merger raised questions about whether covenant enforcement posture, audit practices, and dispute resolution approaches would change under Runway Growth's management.

Valuation implications: how anti-dilution clauses affect pricing and discount rates

The anti-dilution architecture of a synthetic royalty agreement directly affects its risk-adjusted valuation. The investor's expected return is a function of:

E[NPV] = Σ [α(t) × Base(t)] / (1 + r)^t

where α(t) is the royalty rate (potentially time-varying if tiered), Base(t) is the net sales base allocated to the royalty-bearing product (potentially subject to combination product allocation, sublicense pass-through mechanics, and reformulation definitions), and r is the discount rate reflecting clinical, commercial, regulatory, and contractual risk.

Anti-dilution protections compress the discount rate by reducing the variance of Base(t). A synthetic royalty with a broad product definition (all salts, forms, formulations, conjugates), pass-through sublicensing mechanics, a minimum combination product allocation floor, and investor-favourable put rights on dilutive events will price at a lower discount rate — and therefore a lower royalty rate for the same upfront capital — than an otherwise identical royalty without those protections.

The practical implication for operating companies is counterintuitive: stronger anti-dilution protections can reduce the cost of capital. By giving the investor greater certainty that the royalty base will not be eroded by commercial decisions, the company can negotiate a lower royalty rate, a higher upfront payment, or a lower cap multiple.

The practical implication for investors is equally important: anti-dilution protections are not free optionality. They constrain the operating company's commercial flexibility. A company with aggressive lifecycle management plans — a combination product strategy, a reformulation pipeline, a sublicensing-heavy commercial model — may resist broad product definitions and pass-through sublicensing requirements. The negotiation is a pricing exercise: more protection for the investor means more constraint on the company, and the equilibrium royalty rate reflects the balance.

Emerging frontiers: biosimilar substitution, ADC payload swaps, and AI-designed successors

Three emerging frontiers are testing the limits of current anti-dilution drafting.

Biosimilar substitution and interchangeability. As reference biologics face biosimilar competition, operating companies may shift commercial emphasis to next-generation biologics that are not biosimilar-substitutable. If the synthetic royalty covers the reference biologic but not the next-generation successor, revenue migration can erode the royalty base even without formal reformulation. Anti-dilution clauses must now address not only what the product is but what the product competes with — a subtle but commercially significant distinction.

ADC payload swaps and bispecific reformatting. Antibody-drug conjugates are increasingly subject to payload optimisation (swapping one cytotoxic payload for another on the same antibody chassis) and format changes (converting a monospecific antibody into a bispecific). The BeOne/Royalty Pharma Imdelltra definition — covering "any strengths, forms (including pegylated versions), formulations" — is a strong template, but it may not clearly address whether a bispecific variant of tarlatamab with a different second target constitutes the "same" product. The next generation of product definitions will likely need to specify that any product incorporating or derived from the defined antibody sequence, regardless of format, valency, or conjugation, remains royalty-bearing.

AI-designed molecular successors. As AI-driven drug design accelerates, operating companies may increasingly develop follow-on molecules that are structurally distinct from the royalty-bearing compound but functionally equivalent — designed to replace the original product while falling outside the product definition. This is reformulation dilution at scale: not a deuterated analogue but a computationally designed successor with a different scaffold, different IP, and no contractual nexus to the original royalty agreement. The anti-dilution response will likely be "anti-cannibalisation covenants" — affirmative obligations not to develop or launch products intended to replace the royalty-bearing product without investor consent — combined with broader economic-interest definitions that capture successor products within a defined therapeutic niche.

Practical takeaways for dealmakers and royalty investors

The anti-dilution problem in synthetic royalty agreements is, at bottom, a question of who controls the definition of value. The operating company controls the product, the commercial strategy, the lifecycle management decisions, and the sublicensing relationships. The investor controls a contractual entitlement whose value depends on those decisions. Anti-dilution clauses are the mechanism by which the investor's economic interest is insulated from the operating company's unilateral discretion.

For investors, the hierarchy of priorities is: (1) product definition breadth — define the franchise, not the molecule; (2) net sales base integrity — pass-through sublicensing, combination product floors, gross-to-net caps; (3) operational covenants — diligent commercialisation, sublicense consent, formulation change notice; (4) remedial architecture — put rights, rate ratchets, top-up payments, and expedited dispute resolution.

For operating companies, the strategic calculation is: (1) broader anti-dilution protections reduce the cost of capital by compressing the investor's discount rate; (2) but they constrain commercial flexibility in ways that may conflict with lifecycle management strategy; (3) the negotiation equilibrium is a function of the company's commercial plans, the investor's return requirements, and the competitive intensity of the royalty financing market.

For deal counsel, the drafting imperative is precision. The Vertex/Royalty Pharma Alyftrek dispute demonstrates that ambiguity in product definitions — is a deuterated analogue "the same as" the parent compound? — creates litigation risk worth hundreds of millions. Every reformulation strategy, every combination product plan, every sublicensing scenario that is foreseeable at the time of the financing should be addressed explicitly in the agreement. The cost of additional definitional specificity at drafting is trivial relative to the cost of a dispute over whether the royalty base has been diluted.

The synthetic royalty market is maturing rapidly. As transaction sizes grow — the Revolution Medicines/Royalty Pharma deal alone exceeded $2 billion — and as product lifecycle strategies grow more sophisticated, the anti-dilution architecture of synthetic royalty agreements will increasingly determine not just whether investors are protected, but whether the asset class retains the risk-return profile that has made it attractive to institutional capital.

All information in this report was accurate as of the research date and is derived from publicly available sources including SEC filings, press releases, regulatory guidance, practitioner publications, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.