Will GLP-1 Royalties Deliver What They Promised? Deal Economics Under a Repricing Regime

The GLP-1 class is the largest pharmaceutical revenue event of the decade. Combined 2024 sales of Wegovy and Ozempic reached $26 billion, with Mounjaro and Zepbound adding approximately $16 billion. For 2025, tirzepatide alone reached $36.5 billion, making it the world's best-selling drug, with semaglutide close behind at $33 billion. Every royalty fund, every late-stage biotech with an incretin or amylin asset, and every licensor sitting on an upstream contract has been priced against this trajectory.

The thesis was simple: buy a percentage of net sales of an asset compounding at 30% to 50% annually, hold for a decade, collect. The execution is becoming considerably less simple.

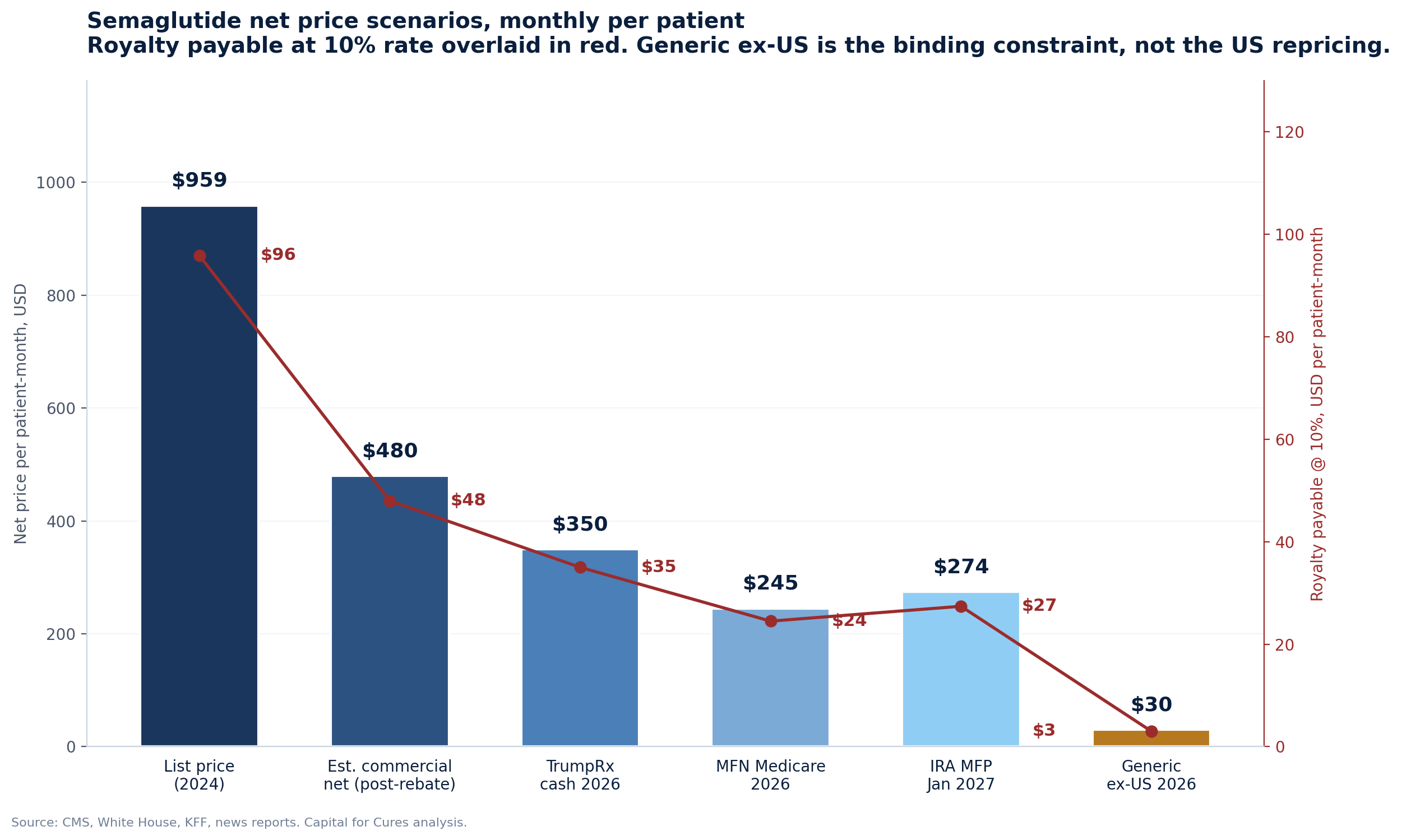

In November 2025 the Trump administration announced Most-Favored-Nation pricing agreements with Eli Lilly and Novo Nordisk that drop Medicare prices for semaglutide and tirzepatide to $245 per month and bring TrumpRx cash prices to roughly $350. Two weeks later, CMS published the IRA Maximum Fair Price for semaglutide at $274 per month, effective January 2027, a 71% discount to the prior list price of $959. Liraglutide is now generic in major markets, with Biocon receiving FDA approval for generic Saxenda in February 2026. Indian and Chinese suppliers are preparing semaglutide generics for non-US, non-EU launches in 2026.

The royalty stack on these molecules now runs through a different price reality than the one used at deal signing.

This piece works through the four structural archetypes of GLP-1 royalty exposure, the underwriting assumptions each one embeds, what the sell side actually thinks about market size, and what the repricing event means for whether the deals will deliver. The conclusion varies sharply by archetype.

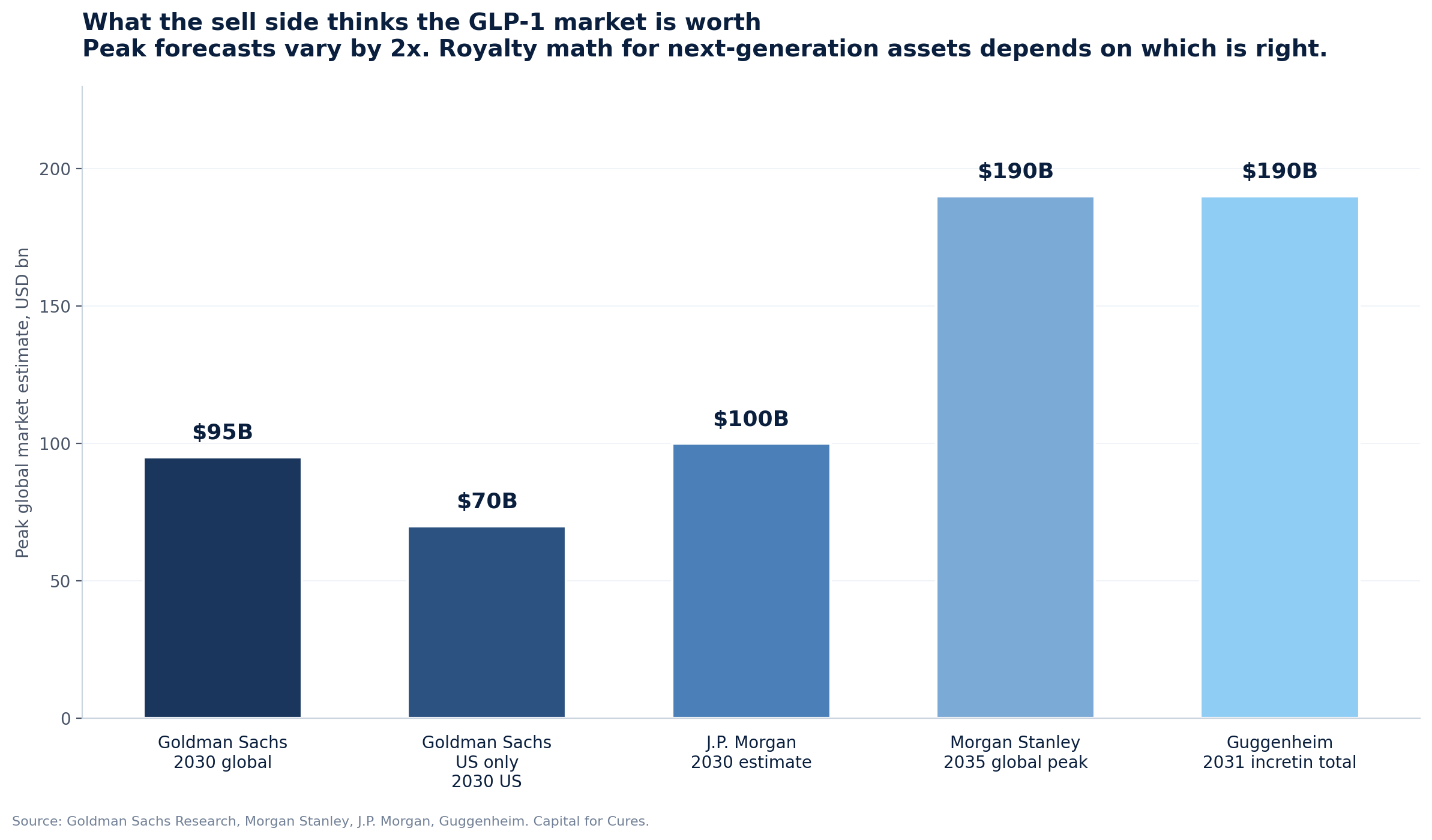

What the analysts actually think

Before walking through the royalty mechanics, it is worth surfacing the dispersion in sell-side forecasts. The royalty math depends entirely on which of these views turns out to be right.

Goldman Sachs cut its forecast in May 2025, moving the global anti-obesity market estimate from $130 billion to $95 billion by 2030. The cut was driven by lowering Medicare unlock probability from 70% to 50% (since reversed by the November 2025 deals) and shorter-than-assumed treatment duration. Goldman's US-only peak forecast is $70 billion, ex-US is $50 billion. The Goldman view was the most cautious of the major sell-side desks at the time, and on key dimensions it has been overtaken by events: Medicare coverage is now happening, MFN cuts list prices but expands volume.

Morgan Stanley moved the other direction. In April 2026, Morgan Stanley raised its peak global market estimate to $190 billion by 2035, $40 billion above its prior estimate. The Morgan Stanley base case has approximately 30% of obese or diabetic Americans on GLP-1 therapy by 2035 versus 6% in 2025, and 10% globally outside the US. Morgan Stanley estimates 25 million Americans will be on GLP-1 treatment by 2030, up from 10 million in 2025. The forecast specifically incorporates ex-US generic erosion, projecting Brazil's GLP-1 market to "more than quadruple" with generic competition reducing prices by up to 70%. Morgan Stanley is therefore bullish on volume and explicit about the price compression.

J.P. Morgan's forecast for 2030 is approximately $100 billion globally with 25 to 30 million Americans on treatment, and JPM has been first to flag the second-order effects on adjacent industries: a $30 to $55 billion annual revenue reduction for food and beverage companies by 2030 to 2034, and so far minimal impact on medtech volumes. Guggenheim is the most aggressive, with Seamus Fernandez forecasting $50 billion in diabetes incretin sales plus $140 billion in obesity sales by 2031, and his thesis that GLP-1 incretins will become the most prescribed drugs ever by or before 2031.

The most informative view is not from the sell side but from the manufacturers themselves.

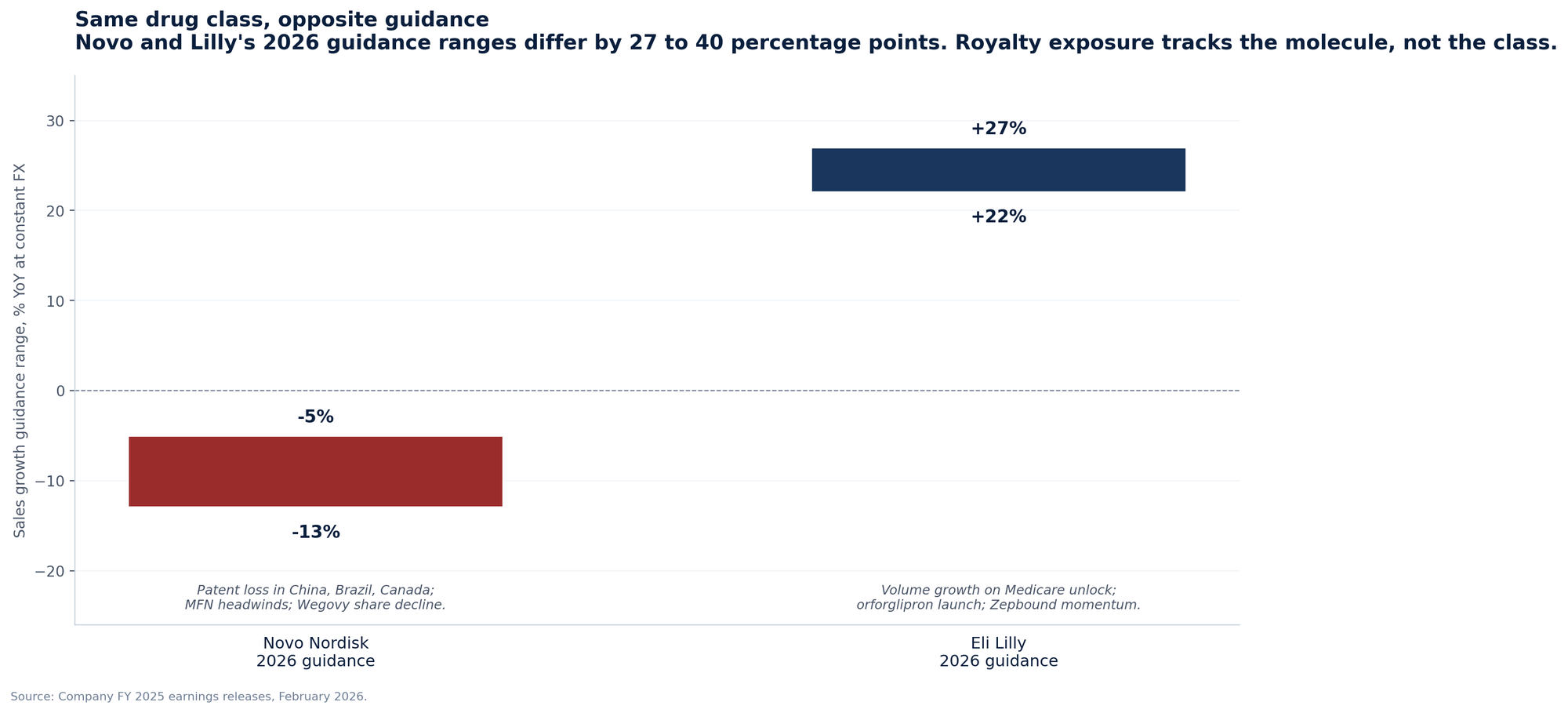

Novo Nordisk guided 2026 sales and operating profit to decline 5% to 13% at constant FX, citing pricing pressure in the US, intensifying competition, and patent loss in China, Brazil, Canada, and Turkey. Eli Lilly guided 2026 revenue to $80 to $83 billion, growth of 22% to 27%, with CFO Lucas Montarce explicitly saying "price is expected to be a drag on growth in the low- to mid-teens." Both companies face the same MFN agreement, the same IRA negotiation framework, and the same ex-US patent landscape.

The divergence comes from where they sit in the molecular hierarchy: Zepbound has demonstrated superior weight loss to Wegovy in head-to-head data, Mounjaro is taking share in diabetes, and orforglipron is launching in 2026. The implication for royalty holders is straightforward: in the post-2025 environment, your exposure tracks the molecule, not the class. A holder with royalty rights on semaglutide-derived assets is in a worse position in 2026 than a holder with royalty rights on tirzepatide-derived or next-generation assets.

The four archetypes of GLP-1 royalty exposure

There is no single "GLP-1 royalty market." There are four distinct claim types on GLP-1 cash flows, each with different sensitivity to price, volume, and substitution risk.

Type 1: Contractual licensing royalties

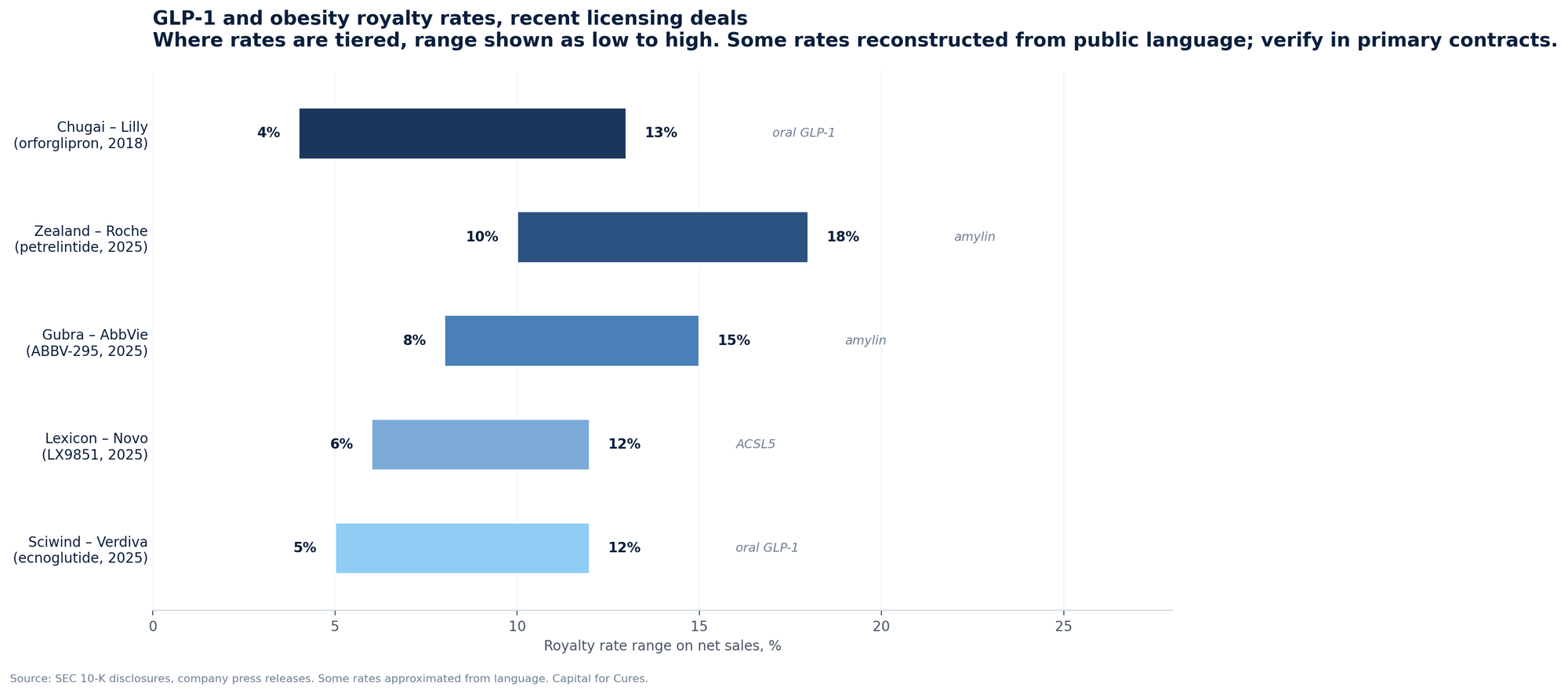

A discoverer licenses a molecule to a commercialiser and retains a tiered royalty on net sales. These are operating-company-to-operating-company deals, governed by license agreements that pre-date any pricing reform. The economics are documented in 10-K disclosures because they are material to the licensee.

The clearest example is Chugai's royalty on orforglipron. Lilly licensed OWL833 from Chugai in 2018 for a $50 million upfront payment, up to $390 million in milestones, and "tiered royalty payments on future worldwide net sales from mid single digits to low teens." Orforglipron was approved by the FDA in April 2026. Chugai's economic interest in the asset is now a live royalty stream, the rate of which sits inside Lilly's licensing footnote rather than on Chugai's balance sheet as a financial instrument.

Recent comparable deals in this category:

| Discoverer | Commercialiser | Asset | Class | Year | Upfront | Total deal value | Royalty rate |

|---|---|---|---|---|---|---|---|

| Chugai | Eli Lilly | Orforglipron | Oral GLP-1 | 2018 | $50M | $440M | Mid SD to low teens |

| Gubra | AbbVie | ABBV-295 | LA amylin | 2025 | $350M | $2.225B | Tiered, undisclosed |

| Zealand Pharma | Roche | Petrelintide | Amylin | 2025 | $1.65B | $5.3B + 50/50 US-EU | Double digit to high teens, RoW |

| Lexicon | Novo Nordisk | LX9851 | ACSL5 oral | 2025 | $75M near-term | $1B | Tiered, undisclosed |

| Sciwind | Verdiva | Ecnoglutide | Oral GLP-1 | 2025 | $70M | $2.47B | Tiered, ex-Greater China/Korea |

| Hansoh Pharma | Regeneron | HS-20094 | GLP-1/GIP | 2025 | $200M | $2B | Tiered, ex-Greater China |

| United Labs | Novo Nordisk | UBT251 | Triple agonist | 2025 | $200M | $2B | Tiered, ex-Greater China |

Sources: SEC filings, Contract Pharma, Zealand investor presentation March 2025, Lexicon press release, Sciwind press release.

The economic feature these contracts share is that the royalty is paid out of net sales, the line item that bears the full impact of the 2026 to 2027 repricing. Mid-single-digit to low-teens royalty rates do not compress when the net price compresses; they apply to whatever the post-rebate, post-MFN, post-MFP number turns out to be.

Type 2: Acquired royalty streams

A discoverer or original licensee monetises a future royalty for upfront cash to a royalty financing firm, which then sits in the position of a non-operating investor in the asset. The clearest GLP-1 example is Royalty Pharma's $205 million acquisition of Zealand Pharma's interest in Sanofi's Soliqua and Lyxumia franchise in September 2018. That deal acquired the future royalty stream and $85 million of potential commercial milestones for $205 million in cash.

Lyxumia is lixisenatide, a short-acting GLP-1 receptor agonist. Soliqua is a fixed-dose combination of insulin glargine and lixisenatide. Neither is a top-tier obesity asset.

The Zealand-Royalty Pharma transaction is the largest publicly disclosed pure GLP-1 royalty monetisation, and it predates the obesity boom. There has been no comparable monetisation of a Wegovy, Ozempic, Zepbound, or Mounjaro royalty for a simple reason: Novo and Lilly developed and own those products outright, and they are too profitable to monetise. The third-party royalty stack on the dominant GLP-1 brands is essentially empty. This is why the GLP-1 class is structurally underrepresented in royalty fund portfolios despite being the largest single pharmaceutical class by revenue.

Type 3: Synthetic royalties

Synthetic royalties are post-launch financings in which a biotech sells a percentage of future net sales of its own product for upfront capital, without transferring underlying IP. The instrument is now standard for commercial-stage biotechs needing non-dilutive growth capital. There is no mature GLP-1 example because the assets that would carry one (aleniglipron from Structure Therapeutics, Viking's VK2735, ecnoglutide via Verdiva) are pre-launch.

The synthetic royalty issuance window for GLP-1 assets opens in 2027 to 2029, when next-generation incretins and amylin programs reach launch. The repricing event is highly relevant to that window: synthetic royalty issuers will need to price against post-MFN, post-IRA net sales reality, and the historical 2024 to 2025 list-price benchmarks will no longer be the right comparator. Buy-side discount rates applicable to these instruments already reflect post-reform price uncertainty, which means deals priced from 2027 onwards may carry tighter spreads relative to other late-stage launch financings, not wider.

Type 4: M&A embedded royalty rights

Contingent value rights and earn-outs embedded in acquisitions function as royalty-like instruments tied to specific clinical or commercial milestones. The Pfizer-Metsera deal closed in November 2025 with a $47.50 per share cash payment plus a non-transferable CVR worth up to $22.50 per share:

| CVR trigger | Payment per share | Asset state |

|---|---|---|

| Phase 3 start of MET-097i + MET-233i | $5.00 | Pre-pivotal |

| FDA approval of monthly MET-097i monotherapy | $7.00 | NDA review |

| FDA approval of MET-097i + MET-233i combination | $10.50 | NDA review |

Source: Marketscreener, Pfizer-Metsera completion announcement, November 2025.

Roche's 2023 acquisition of Carmot included up to $400 million in earn-outs tied to obesity pipeline milestones. These are not strictly royalties. They are options on regulatory and commercial outcomes that look like royalty rights from the holder's perspective: capped, milestone-driven, non-recourse to the operating business. They sit on the same valuation curve as Type 1 royalties for analytical purposes, with the additional dimension that the acquirer controls the development timeline and can affect milestone achievement. The Pfizer-Metsera CVR economics are largely binary, regulatory-event-driven, and therefore substantially more robust to the repricing event than royalties on net sales.

The first negative datapoint on the Metsera asset arrived in February 2026: Phase 2b VESPER-3 data on PF-08653944 (formerly MET-097i) showed maximum weight loss of 10.5% after six months, below market expectations and well below the 20%-plus benchmarks set by tirzepatide. The CVR is not yet impaired, but the Phase 3 trigger now carries higher execution risk than at deal close.

The repricing event: what changed in November 2025

Three regulatory developments in 2025 reset the price assumptions underlying every GLP-1 royalty.

First, on November 6, 2025, the White House announced MFN agreements with Lilly and Novo. The headline numbers:

| Channel | Product | Pre-deal | Post-deal | Effective |

|---|---|---|---|---|

| Medicare/Medicaid | Ozempic, Wegovy, Mounjaro, Zepbound | ~$1,000 list | $245/month | Mid-2026 |

| TrumpRx self-pay | Wegovy injectable | ~$1,350 list | $350/month | 2026 |

| TrumpRx self-pay | Zepbound multi-dose pen | $1,086 list | $299–$449/month | 2026 |

| TrumpRx self-pay | Oral GLP-1 (orforglipron, oral semaglutide) | n/a | $150/month starting dose | 2026 |

| Medicare BALANCE pilot | All covered GLP-1s | n/a | $50/month copay | April 2026 |

Sources: White House announcement, AJMC coverage, Premera Producers summary, Lilly press release.

The agreements include three years of tariff relief for both companies. The MFN price applies only to federal programs and to the new TrumpRx channel; commercial insurance is not directly affected, though both companies have stated they will lower commercial prices over time.

Second, on November 25, 2025, CMS published the IRA Maximum Fair Price for semaglutide at $274 per month, taking effect January 2027:

| Form | Pre-IRA list | IRA MFP (Jan 2027) | Discount |

|---|---|---|---|

| Rybelsus 30-pill supply | ~$960 | $276.78 | 71% |

| Ozempic 3mL syringe | ~$960 | $276.67 | 71% |

| Wegovy 4 × 0.5mL syringes | ~$1,350 | $385.63 | 71% |

Source: Health Affairs Forefront, December 2025.

CMS aggregated Ozempic, Wegovy, and Rybelsus into a single negotiation despite Novo's objection. The KFF analysis notes the interaction between the IRA $274 price and the MFN $245 price has not been clarified; both apply to overlapping populations and there is no public guidance on which takes precedence.

Third, the FDA removed semaglutide from the shortage list in February 2025 and tirzepatide had already been removed in December 2024, ending the period of lawful 503A and 503B compounding that had created a parallel low-cost market. The compounding crackdown was reinforced by the March 2026 Hims-Novo settlement and FDA warning letters. Compounded prescribing has not fully abated; Novo's own Q3 2025 disclosures cite "over 1 million patients on compounded GLP-1s in the US," but the regulated channel is now the main pathway.

Combined, these three changes produce a structural compression of US net price for the dominant brands of approximately 50% to 75% from the 2024 list-price baseline, depending on channel mix. Crucially, the manufacturers themselves describe the IRA impact as "low single-digit impact on global sales growth" because (a) commercial rebates were already large (b) Medicare's share of the GLP-1 obesity population was historically zero (c) volume offset is real.

The royalty payable on $1 of US net sales is unchanged in rate but reduced in absolute amount in lockstep with net price.

The patent geography problem

Most GLP-1 royalty contracts apply to "global net sales" with no carve-outs for jurisdictions where the underlying patent is invalid or expired. This was a non-issue when patent geography mapped cleanly to revenue geography. It becomes a material problem in 2026 onwards because the patent cliff is regional and the revenue mix is becoming more global.

Liraglutide's composition-of-matter patent expired in major markets in 2024, and Biocon's generic Saxenda received FDA approval in February 2026. Semaglutide's US and EU patents run to 2031 to 2032. Semaglutide patents in China and India are weaker and shorter, with multiple suppliers preparing for 2026 launches.

| Molecule | US/EU patent expiry | China/India/Brazil expiry | Generic competition risk |

|---|---|---|---|

| Liraglutide | 2024 (expired) | Expired | Active in all markets |

| Exenatide | Expired | Expired | Active |

| Semaglutide | 2031–2032 | 2026 onwards | Imminent ex-US |

| Tirzepatide | 2036–2038 | 2031+ (formulation patents extend) | Mid-2030s |

| Petrelintide, orforglipron, ABBV-295, LX9851 | Late 2030s to early 2040s | Same | Low |

Sources: C&EN, GeneOnline, company filings.

The Indian and Chinese semaglutide pipeline is wide. Dr. Reddy's, Alkem, Biocon, Sun Pharma, Jiangsu Hengrui, and Sandoz all have generic semaglutide in development. Brazil's Biomm has signed manufacturing arrangements. Morgan Stanley specifically forecasts that Brazilian generic semaglutide will price 70% below branded.

For a royalty holder with a contract sized in 2018 to 2022 that assumed a flat global price of approximately $1,000 per patient-month, the 2026 to 2030 reality of the same molecule selling at $20 to $50 per month in middle-income markets and $250 in high-income markets is a structural mispricing of the underlying instrument. The modelling response is not to apply a uniform rate to global net sales but to disaggregate by jurisdiction and by year, applying different price assumptions and patent end-dates to each. Few royalty deal models I have seen do this rigorously.

Tirzepatide and other next-generation incretins benefit from a longer patent runway. The patent geography risk for next-generation royalties is therefore concentrated in the policy compression channel (MFN, IRA negotiation in subsequent cycles) rather than the generic substitution channel.

Substitution risk inside the class

The second-order risk is intra-class substitution. The GLP-1 category is the most actively contested space in pharmaceutical R&D. There are six oral GLP-1 candidates in Phase 2 or beyond. Three different mechanism classes (incretins, amylin analogs, ACSL5 inhibitors) are now in late-stage development. Royalty holders on a specific molecule own a position in a class where the molecular share will be redistributed multiple times during the life of the royalty.

The relevant late-stage 2024 to 2026 deal data points:

| Date | Buyer | Target/asset | Mechanism | Deal value | Status |

|---|---|---|---|---|---|

| Dec 2023 | Roche | Carmot | GLP-1/GIP + oral GLP-1 | $2.7B + $400M | Closed |

| Mar 2025 | AbbVie | Gubra (license) | LA amylin | $350M + $1.875B | Closed |

| Mar 2025 | Roche | Zealand (collaboration) | Amylin | $1.65B + $3.6B | Closed Q2 2025 |

| Mar 2025 | Novo | Lexicon (license) | ACSL5 oral | $75M + $925M | Phase 1 active |

| Mar 2025 | Novo | United Labs (license) | Triple agonist | $200M + $1.8B | Phase 2 |

| Jun 2025 | Regeneron | Hansoh (license) | GLP-1/GIP | $200M + $1.8B | Phase 3 |

| Sep 2025 | Pfizer | Metsera | LA GLP-1 + amylin | $4.9B + $5.1B CVR | Closed Nov 2025 |

| Dec 2025 | Genentech | Structure (Gasherbrum, license) | Oral GLP-1 (CT-996) | $100M + tiered | Closed |

Sources: SEC filings; BioSpace, Fierce Biotech, Labiotech.

The aggregate contracted value of these deals is sized against an outcome where each asset captures 5% to 15% market share of an $80 billion to $150 billion 2032 global obesity market. The contracted milestone payments and royalty rates are predicated on each asset achieving its share. The mathematical reality is that not all of them can. There are now five large pharma sponsors (Lilly, Novo, Roche, Pfizer, AbbVie) plus several mid-cap challengers, each with at least one late-stage program. The volume-weighted average market share these programs need to clear their commercial milestones substantially exceeds 100% of the addressable obesity market. Some royalty positions will deliver, others will not, and the dispersion across royalty contracts in the same therapeutic area will be unusually wide.

The discriminating factors are not what they were in earlier therapeutic areas. Patent-protected exclusivity is necessary but no longer sufficient because intra-class substitution between molecules with overlapping patent cliffs erodes pricing power for all of them. Differentiated efficacy at the 20%-plus weight loss level, demonstrated cardiovascular or renal outcomes, oral formulation, and once-monthly dosing are the dimensions on which winners will be decided. Pfizer's Phase 2b VESPER-3 readout in February 2026 on PF-08653944 at 10.5% maximum weight loss is the first concrete signal that not every Phase 3 obesity asset will clear the bar, and that several Phase 2/3 programs currently sized as future blockbusters will end up sub-scale or discontinued.

Outlook by archetype

Type 1: Contractual licensing royalties

Type 1 royalties on next-generation assets are the most exposed to the repricing event because they were sized in 2024 to 2025 against unreformed pricing assumptions and apply to assets that will launch into the post-reform market.

Within Type 1, royalties on assets with structural differentiation (oral formulations, once-monthly dosing, amylin or non-incretin mechanisms with distinct efficacy profiles) will compress less than royalties on me-too injectable GLP-1s. The Chugai-orforglipron position is partially insulated by the oral formulation and the BALANCE-driven volume lift. The Gubra-ABBV-295 and Zealand-petrelintide positions are insulated by the amylin mechanism's differentiation. The Lexicon-LX9851 position is insulated by ACSL5 being non-incretin and potentially synergistic with semaglutide.

Quantitative back-of-envelope on Chugai's orforglipron royalty: at an 8% midpoint rate (mid-single-digit to low-teens) and a blended $200 per patient-month US net price on the launch dose, royalty per US patient-month is approximately $16. Pre-MFN, a list price near $1,000 with rebates implying $400-plus net would have yielded $32-plus per patient-month. The compression for Chugai is approximately 50%, with offsetting volume upside from the $150 starting-dose price stimulating new patient starts. This is a coherent thesis but it is not what the 2018 underwriting case would have produced.

Type 2: Acquired royalty streams

Not materially exposed to GLP-1 repricing because the largest publicly disclosed position (Royalty Pharma on Lyxumia/Soliqua) is on a non-blockbuster franchise that was already in commercial decline before the reforms. There is no Type 2 position on the dominant brands. The category itself is structurally undertraded relative to oncology, multiple sclerosis, and immunology, where royalty financing has decades of precedent. The 2026 to 2030 window may produce the first meaningful Type 2 transactions on next-generation GLP-1 assets, particularly out of mid-cap European biotechs that licensed Chinese GLP-1 IP and need to monetise contracted milestone tails ahead of launch.

Type 3: Synthetic royalties

Do not yet exist in the GLP-1 class. The issuance window is 2027 to 2029, and deals that get done will be priced against post-reform reality. The instrument may turn out to be more attractive than Type 1 from the buy side because the discount rates applicable to post-launch synthetic royalties already incorporate the 2027 to 2030 net price uncertainty. From the issuer side, synthetic royalty financing on a GLP-1 launch in 2028 will likely command tighter spreads than equity given the visibility on near-term sales.

Type 4: M&A embedded royalty rights

CVRs and earn-outs benefit from the optionality dynamic. CVR holders are short the molecule's regulatory and commercial outcomes; price compression reduces the in-the-money value of the option but does not eliminate it. The Pfizer-Metsera CVR triggers are predominantly binary regulatory milestones, not commercial sales thresholds, which makes them substantially more robust to the repricing event than royalties on net sales. The risk for Type 4 holders is execution: Phase 2b data on Metsera assets has already underperformed expectations, and the CVR's value is now meaningfully lower than at deal close even with no regulatory denial.

What this means for new deals

The deals signed between 2025 and 2026 will set the new baseline for what GLP-1 royalty pricing looks like in the post-reform era. The 2018 Chugai-Lilly contract, sized against a market that no longer exists, will end up being the cautionary tale that closed an era. The 2025 Zealand-Roche, Gubra-AbbVie, and Lexicon-Novo contracts are the first to reflect a more realistic picture, and even they were signed before the November 2025 announcements. The next batch will price differently again.

For lawyers and bankers structuring these deals, the 2026 negotiating dynamic includes:

| Deal feature | Pre-2025 default | Post-2025 default |

|---|---|---|

| Royalty rate basis | Flat % of global net sales | Jurisdiction-specific tiers |

| Price-floor mechanism | None | Contractual reset on MFN/MFP outcome |

| Patent expiry handling | Single end-date | Country-by-country, year-by-year |

| Milestone tails | Concentrated at approval | Extended through Year 5 of launch |

| Audit and information rights | Standard quarterly | Expanded, with right to revisit assumptions |

| CVR design (M&A) | Sales-based triggers | Regulatory-event-based triggers |

| Combination product treatment | Pro-rata | Explicit allocation rules |

None of these are novel in royalty financing. The GLP-1 class will be the first major pharmaceutical category where they become the deal norm rather than the deal exception.

The verdict

The overall answer to whether GLP-1 royalties will deliver what they promised: most will not deliver against the 2024 underwriting case, some will compensate via volume offsets, and the dispersion across positions will be wider than the dispersion in any previous mega-class.

The royalty holder's job over the next 24 months is to disaggregate. A "GLP-1 royalty portfolio" is a misleading construct. What matters is the molecule, the licensee, the geographic exposure, the patent runway, and the substitution profile within the class. The class-level narrative is now too coarse for analytical purposes.

The best-positioned holders are those with royalties on differentiated next-generation assets (oral, monthly, amylin, non-incretin) with patent runway through the late 2030s, partnered with sponsors that have pricing power and US commercial scale. The worst-positioned are those with royalties on first-generation injectable GLP-1s in markets exposed to 2026 to 2031 generic competition.

The sell side knows this. The 2x dispersion in peak market forecasts, from Goldman's $95 billion to Morgan Stanley's $190 billion, is not a measurement problem. It is a coherent expression of structural uncertainty about price, volume, geography, and intra-class substitution. Royalty pricing should reflect the same uncertainty. Where it does not, the gap will be revealed in the next two reporting cycles.

This article reflects publicly available information as of April 2026. It does not constitute investment, legal, or tax advice. Economics and structural mechanics described are derived from SEC filings, company press releases, and CMS publications. Royalty holders and counsel evaluating specific positions should rely on the underlying contracts and counsel.