Anti-Pledge Provisions in Pharmaceutical Royalty Financing: How They Work, How They Reshape the Stack

Anti-pledge provisions are the most underestimated structural friction in pharmaceutical royalty finance.

They sit in the assignment, encumbrance, or change-of-control clauses of nearly every modern license agreement, framed in one or two lines of dense contractual prose: "Neither party may assign this Agreement or any rights hereunder without the prior written consent of the other party." Read in isolation, the language looks like boilerplate. In practice, it determines whether a royalty stream can be monetized at all, how long the transaction will take, and how much value transfers from licensor to financier versus dissipates into restructuring friction.

The clause also reaches further than its drafters often realize. It governs not just outright sale of the receivable but also the pledge of the receivable as security for a royalty-backed note, the participation in a synthetic royalty financing, and (in some recent drafts) the transfer of economic rights to a financing vehicle even without legal title passing.

This piece works through the mechanics of anti-pledge provisions as they appear in modern pharmaceutical license agreements, the resulting impact on royalty monetization economics, the recent transactional cohort that illustrates the variation in resolution, the statutory architecture under Article 9 of the Uniform Commercial Code, and the practical drafting and diligence considerations for licensors, royalty financiers, and counsel.

What an anti-pledge provision actually is

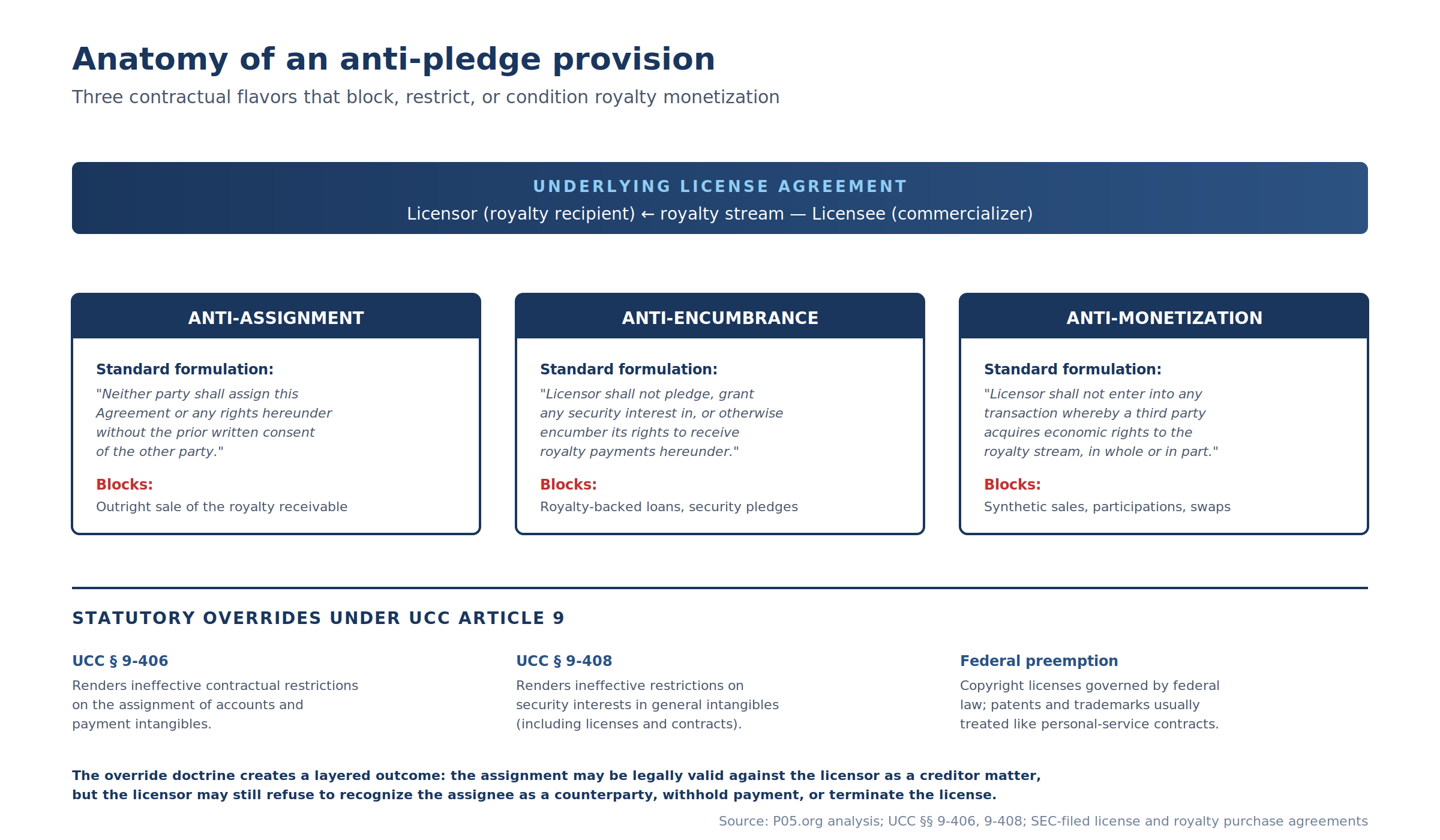

An anti-pledge provision is a contractual restriction on the licensor's (or licensee's) ability to transfer, assign, encumber, or otherwise dispose of its rights and obligations under a license agreement. The provision sits at the intersection of three distinct legal disciplines: contract law (which governs the parties' bilateral obligations), intellectual property law (which governs the underlying patent or copyright rights), and secured transactions law (which governs the priority of competing claims to the same asset stream).

The terminology is not consistent across the industry. The same restriction may be described as an anti-assignment clause, a no-encumbrance covenant, an anti-monetization provision, a transfer restriction, or simply an "assignment" clause. The substance varies more than the label, and three distinct clause flavors recur with enough frequency to be treated separately.

Anti-assignment. The licensor agrees not to transfer the license agreement or its rights thereunder to any third party without consent. The clause typically reads: "Neither party shall assign this Agreement or any rights hereunder, in whole or in part, without the prior written consent of the other party, and any purported assignment without such consent shall be void and of no effect."

The clause is found in nearly every license agreement filed with the SEC since 2000. Skadden's analysis of IP license restrictions summarizes the position succinctly: "In its simplest form, an anti-assignment provision states that the prior consent of the licensor is required for the licensee's assignment of the agreement."

Anti-encumbrance. The licensor agrees not to grant any security interest, lien, or other encumbrance on its rights to receive royalty payments. The clause typically reads: "Licensor shall not pledge, grant any security interest in, hypothecate, or otherwise encumber its rights to receive royalty payments hereunder without the prior written consent of Licensee."

The anti-encumbrance flavor is more common in pharma-to-pharma collaboration agreements than in university-to-biotech license agreements, and it specifically targets royalty-backed loan structures rather than outright sales.

Anti-monetization. The most recently-drafted variant explicitly prohibits any transaction whereby a third party acquires direct or indirect economic rights to the royalty stream, regardless of whether the transaction is structured as an assignment, a security pledge, a participation, or a synthetic payment obligation.

The Arrowhead-Royalty Pharma 2023 olpasiran royalty purchase agreement contains the textbook drafting: "The Seller shall not, without the prior written consent of the Buyer (such consent to be granted or withheld in the sole discretion of the Buyer), exercise any right to terminate, agree with Licensee to terminate, or take, or permit any Affiliate or Visirna or any sublicensee of any Affiliate or Visirna to take, any action that would reasonably be expected (with or without the giving of notice or passage of time, or both) to give Licensee the right to terminate, the License Agreement in its entirety."

The same agreement defines "Monetization" expansively to mean "any assignment, conveyance, monetization, or imposition of a Lien by the Seller on, following the Closing, any percentage of the Royalty."

For royalty finance, this distinction is not academic.

It determines whether a buyer can underwrite the royalty asset as a clean financial instrument or must structure around the underlying license. It determines whether a synthetic royalty transaction can be done with or without the licensee's knowledge. And it determines whether the entire royalty financing market for a particular asset is functionally open or closed.

Three properties define the modern anti-pledge regime.

Personal-services treatment. Under U.S. federal law, patent and copyright licenses are typically treated as personal-services contracts. Absent express contrary language, they are not freely assignable by the licensee. The licensor's identity is deemed material, and federal policy favors the licensor's ability to control who exercises the licensed rights. The default rule cuts against royalty monetization in the same way that it cuts against any other transfer; both require contractual permission or statutory override.

The UCC override. Both UCC § 9-406 and UCC § 9-408 render certain contractual restrictions on assignment or encumbrance ineffective as a matter of state commercial law. Section 9-406 applies to accounts and payment intangibles (which is what most royalty receivables are characterized as) and overrides outright restrictions on assignment. Section 9-408 applies to general intangibles (which includes license rights and contracts) and overrides restrictions on the creation of security interests.

The override doctrine is powerful but limited in scope. It validates the assignment or security interest as between the assignor (licensor) and the assignee (royalty fund) but does not always force the obligor (licensee) to recognize the assignee as a counterparty, deliver royalty reports to it, or refrain from terminating the license.

The bilateral nature of the bargain. Even where UCC override applies, the licensee retains substantial leverage. It can refuse to provide royalty reports to the assignee, refuse to engage in audit cooperation, refuse to accommodate change-of-control diligence, and decline to consent to amendments necessary to support the financing structure. The override doctrine wins the legal battle in the abstract; the licensee often wins the practical war.

Goodwin's October 2025 royalty deals report characterizes the resulting market in plain terms. The continued growth of royalty finance has been driven in part by an increase in deal structures that work within or around restrictive license terms, including "tiered royalties, milestone-based arrangements, capped or hybrid instruments, territory or indication splits, multiproduct deals, and tranched funding." Each of these structural options is, in part, a response to anti-pledge friction in the underlying license.

The five-position spectrum of pledge restrictions

Anti-pledge provisions exist on a continuum from no restriction at all (the license is silent on assignment, and royalty rights flow freely) to absolute prohibition (any purported transfer is void as of its inception). Each position implies a different monetization timeline, a different buyer-side discount, and a different probability of getting the deal done at all.

The spectrum collapses into five identifiable positions.

Freely assignable. The license is silent on assignment, or contains express language permitting assignment without consent. The royalty receivable can be monetized as a clean financial instrument with no licensor involvement.

This position is rare in modern pharmaceutical licenses, accounting for roughly 10% of agreements signed since 2024. Where it appears, it typically reflects either (i) pharma-to-pharma deals between counterparties of equal sophistication where neither side wanted asymmetric restrictions, or (ii) older agreements (pre-2010) drafted before royalty monetization was a mainstream financing technique.

Notice only. The licensor must provide written notice to the licensee of the assignment but does not require consent. The licensee may have a right to refuse to deal with the new counterparty, but it cannot block the transfer of economic rights.

This position is found in approximately 15% of recent agreements and is most common in arm's-length biotech-to-biotech deals where neither party expects to need the comfort of a consent right. The monetization timeline is short (two to four weeks for notice mechanics) and the buyer-side discount is modest (50 to 100 basis points relative to the freely-assignable benchmark).

Reasonable consent. The licensee's consent is required but cannot be unreasonably withheld. This is the modal clause in modern license agreements, accounting for roughly 35% of deals.

The phrase "such consent not to be unreasonably withheld" imposes a meaningful constraint on the licensee. The licensee must articulate a legitimate business reason for refusing consent, and courts in Delaware, New York, and California have generally been willing to scrutinize the reasonableness of refusals.

The monetization timeline at this position is one to three months (consent letter negotiation plus licensee diligence) and the buyer-side discount is 100 to 250 basis points to reflect the residual risk that consent is withheld or conditioned.

Discretionary consent. Consent is required and may be "granted or withheld in the sole discretion" of the licensee, with no reasonableness standard. The licensee can refuse without justification.

This position is now equally common as reasonable consent, also accounting for roughly 35% of deals, and is increasing in frequency. It is the modal position when big pharma is the licensee, because big pharma has the leverage to insist on unilateral discretion. The Arrowhead-Royalty Pharma olpasiran deal documents the practice: consent is "to be granted or withheld in the sole discretion of the Buyer".

The monetization timeline at this position is three to nine months and the buyer-side discount is 300 to 600 basis points. In approximately 15% of cases at this position, the consent is ultimately not obtained at all, and the monetization either does not proceed or is restructured as a synthetic financing that does not require licensee consent.

Absolute prohibition. Any purported assignment is void and of no effect. The license has no consent mechanic at all; the prohibition is unconditional.

This position is rare in commercial license agreements, accounting for roughly 5% of deals, but it is common in (i) foundation grants where the foundation insists on perpetual control over the licensed technology, and (ii) government-funded research agreements where the Bayh-Dole Act framework restricts assignment.

At the absolute prohibition position, the royalty financing market for the underlying asset is functionally closed. The seller must restructure into an SPV that holds only the economic rights (not the license), and even then the SPV's ability to deliver royalty cashflow to the buyer depends on continued licensee performance. Buyer-side bids typically withdraw.

The spectrum collapses to a single economic principle: the further rightward a license sits, the longer the monetization timeline, the higher the buyer-side discount, and the lower the probability of execution. The rightward positions are gated by the relative bargaining power of licensor and licensee at the time of the original license signing, and that bargaining power often does not reflect the licensor's eventual interest in monetizing the royalty stream years later.

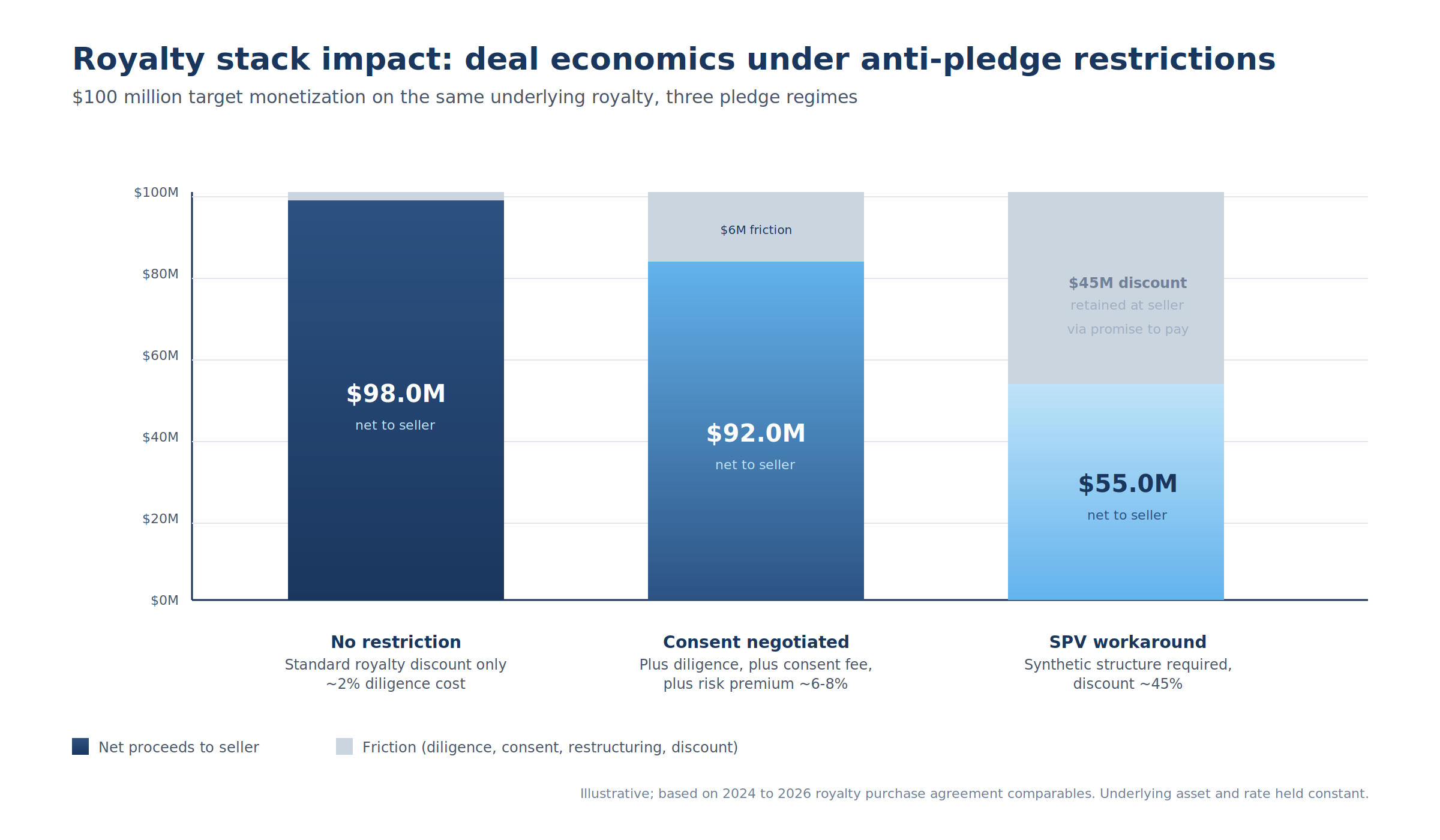

Royalty stack impact: where the value actually goes

The economic distinction between these positions becomes vivid when traced through a representative $100 million royalty monetization target. Assume a single licensor with a Phase 3-stage royalty entitlement attempting to sell or finance against $100 million of expected royalty value, and compare three pledge regimes: no restriction (license silent or freely assignable), consent successfully negotiated (typically with a fee), and absolute prohibition requiring an SPV workaround.

In the no-restriction case, the seller receives $98 million net of approximately $2 million in standard transaction costs (diligence, legal, escrow setup). The deal closes in roughly 30 days from signed term sheet. The buyer underwrites the asset as a pure financial instrument and prices the royalty stream against its actuarial expected value plus required risk premium.

In the consent-negotiated case, the seller receives $92 million net of approximately $6 million in incremental friction costs. The friction breaks down into roughly $1.5 million of licensee consent fees (paid as a transaction expense to the licensee in exchange for consent and any necessary license amendments), $2 million of additional legal and tax diligence (the negotiation of the tripartite consent letter is a meaningful undertaking), and approximately $2.5 million of residual buyer discount for the new payment direction and audit cooperation requirements. The deal closes in roughly 90 to 120 days.

In the SPV workaround case, the seller receives $55 million net, reflecting a roughly 45% buyer discount on the gross expected value. The seller retains nominal title to the royalty stream and grants the buyer a promise-to-pay obligation backed by a security interest in an SPV that holds only the economic rights. The structure is monetizable but at a substantial economic discount because (i) the buyer cannot perfect a direct security interest in the underlying license, (ii) the licensee remains free to terminate the license for cause without consulting the buyer, and (iii) the bankruptcy treatment of the structure is uncertain.

The mechanical conclusion is that anti-pledge friction is highly nonlinear. A clean license with no restriction trades at a small premium to the consented case; the consented case trades at a modest discount; the SPV workaround case trades at a very substantial discount. The 45% gap between the consented case and the SPV workaround case is the price the licensor pays for failing to negotiate appropriate consent mechanics into the original license.

Three specific second-order effects on the royalty stack are worth noting.

Cross-default complications. If the licensee terminates the underlying license for cause (typically a material breach by the licensor that is not cured within the contractual cure period), the royalty stream stops. The financing buyer, having underwritten the asset as a payment intangible, finds itself holding a receivable against a now-defunct contract. This risk is mitigated in most royalty purchase agreements by detailed seller covenants requiring the seller to perform its license obligations, but the covenant is only as good as the seller's ability to perform.

The Eclat-Broadfin Healthcare 2013 royalty agreement is representative on this point: "The Payor shall not enter into, or amend, any Contract of it or its Affiliates after the date hereof the effect of which is to place any restrictions or limitations on the Payor's ability to make the payments that are required to be paid to the Buyer under this Agreement."

Audit cooperation and information rights. Royalty agreements typically grant the royalty recipient audit rights over the licensee's books to verify royalty calculations. When the royalty stream is monetized, the question is whether those audit rights pass to the financier. Most license agreements are silent on this point, and the licensee can take the position that audit rights are personal to the original licensor.

The Reata Pharmaceuticals 2021 amendment to the Dartmouth license illustrates the workaround: in connection with Dartmouth's intended monetization, the parties amended the license to require that "all reports (including, without limitation, royalty reports) and correspondence to be delivered by the LICENSEE to UTMDACC in connection with the License Agreement are to also be concurrently delivered by the LICENSEE directly to DARTMOUTH." The amendment created parallel reporting obligations that survive Dartmouth's eventual royalty sale.

Change-of-control triggers. Many license agreements include change-of-control provisions that allow the licensee to terminate or renegotiate on a change of control of the licensor. A royalty monetization that is structured as a sale of substantially all of the licensor's economic interest in the asset may, in the licensee's view, constitute a constructive change of control that triggers these provisions.

The Royalty Pharma 2005 royalty sale documentation addresses this risk by carving out affiliate transfers: "nothing herein shall prohibit or restrict Royalty Pharma from assigning any of its rights and obligations hereunder to any Affiliate of Royalty Pharma or to any collateral agent under any financing arrangement entered into by Royalty Pharma or any of its Affiliates."

The carveout is one-sided; it protects the buyer's flexibility to assign without protecting the seller's flexibility to do the same.

Recent deal evidence: 2020 to 2026

The 2020 to 2026 transactional cohort shows that anti-pledge provisions are now central to royalty deal structuring at every stage. Seven representative transactions illustrate the range of outcomes, from clean consent negotiation to outright structural workaround.

The AGA Medical 2008 consent letter is the historical template. Inventor Dr. Curtis Amplatz had granted AGA Medical a license to certain cardiac occluder technology and held the right to receive royalty payments under the license. The license contained a standard anti-assignment clause: "C. Amplatz's rights and obligations under the agreements may not be assigned without the written consent of AGA."

When Amplatz wished to assign his royalty receipt rights to Carina Royalty, LLC (a personal LLC structured for estate-planning purposes), AGA's consent was required. The consent was granted via a one-page tripartite letter that (i) consented to the assignment of the royalty receipt rights only (not the underlying license), (ii) explicitly preserved Amplatz's retention of all non-economic rights under the license, (iii) directed AGA to send future royalty payments to Carina's address, and (iv) imposed confidentiality obligations on Carina. The structure became the modern model for royalty monetization consent letters.

The PDL BioPharma November 2009 securitization illustrates the SPV-isolation approach to anti-pledge friction. PDL held license rights from Genentech for royalties on Avastin, Herceptin, Lucentis, and Xolair. The Genentech licenses contained anti-encumbrance clauses that would have impeded a direct pledge of the royalties.

PDL's solution was to transfer 60% of the royalty receivables to a wholly-owned SPV, QHP Royalty Sub LLC, and have the SPV issue $300 million of senior secured notes backed by those receivables under Rule 144A. The transaction was structured to operate beneath the anti-encumbrance threshold by transferring only the economic rights to receive royalties rather than the underlying license itself. The Genentech license was not assigned or encumbered; only the receivables were.

The transaction set the modern template for royalty securitization structures.

The Reata Pharmaceuticals 2021 Dartmouth-UTMDACC amendment is the textbook university-license workaround. Dartmouth held license rights to receive running royalties under a license agreement governed by both Dartmouth's tech-transfer office and UTMDACC's (M.D. Anderson's). Both licensors' consent was required for assignment under Section 10.03 of the license agreement.

Dartmouth wished to monetize "all or a portion of its rights to receive running royalties... including by means of an assignment of such Receivables." The amendment process required (i) a parallel consent from UTMDACC to the assignment of the license to Reata Sub (a subsidiary), (ii) an amendment to permit Dartmouth's intended monetization, and (iii) an amendment to require concurrent royalty reporting directly to Dartmouth so that the monetization buyer would have direct visibility into the licensee's performance.

The whole process took approximately nine months from initial term sheet to executed amendment, illustrating the timeline impact of university-license consent mechanics.

The Arrowhead-Royalty Pharma 2023 olpasiran agreement shows the asymmetric drafting of modern synthetic royalty agreements. Arrowhead held its olpasiran license out to Amgen and had agreed to share royalty proceeds with Royalty Pharma in exchange for upfront capital.

The royalty purchase agreement contains extensive anti-monetization restrictions running against Arrowhead (the seller) but explicit permission for Royalty Pharma (the buyer) to further assign its rights. Specifically, the seller cannot exercise termination rights under the Amgen license without Royalty Pharma's "sole discretion" consent, cannot consent to changes that affect the royalty, and cannot enter into any subsequent monetization of the same royalty stream. The buyer, by contrast, retains broad flexibility to assign to affiliates, collateral agents, and successors.

The structural asymmetry is now standard in modern royalty purchase agreements and creates a one-way ratchet: the buyer can move the asset within its financing structure freely, but the seller is locked into the relationship.

The Pharvaris-BRAIN Biotech-Royalty Pharma October 2024 cross-border transaction illustrates the European tripartite consent letter mechanism. The underlying license agreement was between BRAIN Biotech (a German licensor that had acquired the license from AnalytiCon by merger) and Pharvaris (a Dutch biotech with U.S. listed status).

BRAIN Biotech wished to sell its royalty receipt rights to Royalty Pharma Investments 2019 ICAV, an Irish collective asset-management vehicle. The license amendment recital is explicit on the structure: "BRAIN Biotech has proposed to sell, transfer and assign its right, title and interest in the payments BRAIN Biotech receives from Pharvaris... on terms and conditions customary for such a monetization transaction, including the grant for the benefit of Royalty Pharma of a security interest in the License Agreement."

The deal closed only after Pharvaris executed a separate consent letter (Exhibit D-2 to the royalty purchase agreement) and the license itself was amended in parallel to clarify the duration of Pharvaris's payment obligations. The cross-border structure layered German contract law, Dutch corporate law, U.S. SEC disclosure obligations, and Irish vehicle law into a single transaction; the consent letter was the integration mechanism.

The Royalty Pharma-Revolution Medicines June 2025 daraxonrasib agreement is the largest synthetic royalty transaction to date, with up to $2 billion of committed funding priced on Phase 1 clinical data. The transaction is structured as a synthetic royalty rather than a traditional royalty purchase, meaning that there is no third-party license in the deal stack. Revolution Medicines owns the daraxonrasib asset and grants Royalty Pharma a direct contractual right to receive a percentage of future net sales of the product.

The structural choice is partly a response to anti-pledge friction at the licensee level: by structuring the deal as a synthetic royalty against a wholly-owned asset, Royalty Pharma avoids the consent requirements of any third-party license. The largest synthetic royalty deals in 2024 to 2026 are largely those where the seller owns the asset outright, precisely because synthetic structures sidestep the anti-pledge problem entirely.

The BeOne Medicines August 2025 IMDELLTRA monetization of up to $950 million is a traditional royalty monetization on tarlatamab. BeOne held its IMDELLTRA royalty rights through its underlying agreement with Amgen, and the transaction required Amgen consent under the standard anti-assignment provisions of the license.

The consent process was handled in pre-signing diligence rather than as a post-signing closing condition, which is the recommended best practice for transactions in the consent-required range of the spectrum: the buyer would not have committed capital without certainty that Amgen would consent, and BeOne could not have signed without first securing the consent.

The pattern across this cohort is clear. Anti-pledge provisions are universal in modern license agreements, and the question for any royalty financing is not whether they exist but how they will be navigated. The available workarounds are well-developed: tripartite consent letters, SPV isolation, synthetic structures, and license amendments. The choice among them is driven by the position on the spectrum, the relative leverage of the parties, and the buyer's appetite for residual structural risk.

The legal architecture: UCC, federal preemption, and consent mechanics

The interaction between contractual anti-pledge provisions and the UCC's anti-assignment-override provisions is the central legal puzzle of royalty finance.

For royalty financiers diligencing an asset, for counsel structuring a transaction, and for licensors evaluating their monetization options, these are the doctrines and clauses that determine the shape of the deal.

UCC § 9-406. Section 9-406 applies to accounts and payment intangibles. A "payment intangible" is a general intangible under which the account debtor's principal obligation is a monetary obligation. Royalty receivables are typically characterized as payment intangibles.

The section provides that a contractual term prohibiting, restricting, or requiring consent for the assignment or transfer of a payment intangible is ineffective. The override means that, as between the assignor (licensor) and the assignee (royalty fund), the assignment is valid even if the license agreement purports to prohibit it.

The override has limits. It does not force the licensee to recognize the assignee as a counterparty in the same way that the original licensor was. It does not transfer non-monetary rights (such as audit rights, change-of-control rights, or termination rights). And it does not preempt federal law, which (as discussed below) treats some IP licenses differently.

UCC § 9-408. Section 9-408 applies to general intangibles, which includes the broader category of contractual rights under license agreements. The section provides that contractual terms prohibiting, restricting, or requiring consent for the creation, attachment, or perfection of a security interest in a general intangible are ineffective to the extent that they would impair such creation, attachment, or perfection.

The override is narrower than § 9-406. It enables the creation of a security interest but does not necessarily enable enforcement of that security interest. In other words, the royalty financier can take a security interest in the license rights, but in a default scenario the financier may not be able to step into the licensor's shoes and assert the license rights against the licensee without the licensee's separate consent.

The American Bankruptcy Institute frames the practical consequence: "Outside of bankruptcy, [the security interest] could have value if the licensor is willing to recognize the security interest and consent to an assignment to the purchaser at the UCC foreclosure sale... However, in bankruptcy, the security interest may suddenly have a great deal of value." The bifurcation matters enormously for royalty financing structuring.

Federal preemption. The UCC override doctrine is a creature of state commercial law. Where federal law speaks separately to the transferability of IP licenses, federal law preempts the UCC.

The most important federal preemption is in copyright. The Ninth Circuit's decision in Cybernetic Services and earlier decisions in Peregrine and Avalon establish that perfection of security interests in copyrights is governed by federal law, not the UCC. A royalty financier taking a security interest in a copyright-based royalty stream (most relevant in the digital health and software-as-a-medical-device space) must file with the Copyright Office in addition to (or instead of) filing a UCC financing statement.

For patents and trademarks, the consensus position is that UCC filing is sufficient for perfection against lien creditors and bankruptcy trustees, but careful counsel will often file in both venues (USPTO and state UCC) to provide maximum protection.

The consent letter. The practical mechanism for working around contractual anti-pledge restrictions is the consent letter (sometimes called the acknowledgment letter or the comfort letter). The consent letter is a separate three-party agreement among the licensor (seller), the licensee (obligor), and the royalty financier (buyer) in which the licensee acknowledges and consents to the proposed monetization.

The standard consent letter contains the following elements: (i) consent to the assignment of the royalty receipt rights, (ii) confirmation that the assignment does not trigger any termination right, change-of-control, or anti-assignment remedy, (iii) direction to the licensee to deliver future royalty payments and reports to the new recipient, (iv) confirmation that the licensee will not amend the license in ways that impair the royalty without the buyer's consent, (v) a confidentiality undertaking, and (vi) (in some structures) a step-in right allowing the buyer to assume the licensor's role in defined default scenarios.

The Pharvaris consent letter referenced as Exhibit D-2 to the BRAIN Biotech royalty purchase agreement is a representative modern example. The license amendment runs in parallel with the consent letter and the two documents are economically interdependent: "This Amendment 2 shall only come into effect (and, subject to the terms and conditions of the License Agreement, remain in effect) upon the condition that the Consent Letter, as specified in Exhibit D-2 to the Royalty Purchase Agreement between Brain Biotech and Royalty Pharma, is duly executed and becomes effective among Brain Biotech, Pharvaris, and Royalty Pharma."

Change-of-control treatment. Anti-pledge provisions are often paired with change-of-control provisions that treat certain assignments (and certain transactions short of assignment) as constructive transfers. A reverse triangular merger of the licensor, for example, may trigger an anti-assignment clause even though no contract is formally transferred. Modern license drafting often explicitly addresses this by either (i) including merger and corporate reorganization within the assignment definition or (ii) carving them out.

The royalty financier should diligence both the assignment clause and the change-of-control clause separately, because the practical effect of monetization may fall under either or both.

Choice of law and governing jurisdiction. Anti-pledge provisions are typically governed by the law of the jurisdiction specified in the license agreement (usually New York, Delaware, California, or the licensor's home jurisdiction). The UCC override applies based on the location of the debtor (the licensor), which is determined under UCC § 9-301.

For cross-border deals (like Pharvaris-BRAIN-Royalty Pharma), the choice-of-law analysis becomes layered: the license governance law, the royalty purchase agreement governance law, the UCC override jurisdiction, and the local insolvency law all interact. The integration mechanism is typically a comprehensive consent letter that anticipates each jurisdiction's procedural requirements.

Accounting and financing consequences

The accounting and financing treatment of anti-pledge provisions affects how the underlying transaction is structured, characterized for tax purposes, and presented in financial statements.

True sale versus secured loan characterization. A royalty monetization can be characterized either as a true sale of the underlying receivable (in which case the buyer takes title to the receivable and the seller derecognizes the asset) or as a secured loan (in which case the seller retains the asset and recognizes a financing liability). The characterization has substantial tax, accounting, and bankruptcy consequences.

Anti-pledge provisions affect the characterization because, where the underlying license restricts assignment, the buyer may not actually receive clean title to the receivable. The transaction may be re-characterized as a secured loan even if structured as a sale.

Gibson Dunn's analysis of synthetic royalty financing notes that "under Article 9 of the New York UCC, a synthetic royalty sale is treated as a transfer of an account, defined as a right to payment for property sold." The synthetic structure is designed to operate as an account transfer rather than as a transfer of license rights, precisely to avoid the anti-pledge problem.

The characterization analysis is most acute in bankruptcy. If the transaction is characterized as a true sale, the receivable is removed from the seller's bankruptcy estate. If it is characterized as a secured loan, the receivable remains in the estate and is subject to the rights of other creditors and the bankruptcy court's exercise of cramdown and discharge powers.

Lien perfection mechanics. Perfection of a security interest in a royalty receivable involves filing a UCC-1 financing statement in the state of the debtor's organization. The filing perfects the security interest as to lien creditors and bankruptcy trustees.

For royalty financiers, the question is whether the security interest will also be perfected as to the licensee. The answer turns on the interaction between UCC § 9-406, UCC § 9-408, and any contractual notice requirement in the license. Best practice is to (i) file the UCC-1 financing statement, (ii) deliver written notice of the assignment to the licensee, and (iii) obtain a separate acknowledgment of the assignment from the licensee in the form of a consent letter.

Disclosure obligations. Royalty monetizations by publicly-traded sellers are typically disclosed on Form 8-K and described in subsequent 10-Q and 10-K filings. Where the transaction was conditioned on a license amendment or consent letter, the existence and substance of those agreements should also be disclosed. The Pharvaris filing is the standard pattern: the license amendment, the royalty purchase agreement, and the consent mechanism are all referenced and (in part) filed as exhibits.

For publicly-traded licensees, the question is whether the licensor's monetization triggers any disclosure obligation on the licensee's part. Generally the answer is no (the licensee's economics are unchanged by the licensor's monetization), but where the monetization is paired with a license amendment that materially affects the licensee, separate disclosure may be required.

Tax considerations. Cash proceeds of a true-sale royalty monetization are typically taxable as ordinary income to the seller (because the royalty payments themselves would have been taxed as ordinary income when received). Cash proceeds of a secured-loan-characterized transaction are not immediately taxable but the seller's basis in the receivable is unchanged.

The tax characterization is independent of the accounting characterization, and the two can diverge. A transaction may be accounted for as a sale (with derecognition of the asset on the seller's balance sheet) but characterized as a financing for tax purposes (with no taxable gain recognized at closing). The optimal tax characterization depends on the seller's tax position, the timing of expected royalty receipts, and the applicable tax rate regime.

Capital structure implications for licensees. When a licensor monetizes its royalty stream, the licensee gains a new counterparty (the financing buyer) that has different incentives than the original licensor. The original licensor's incentive was typically to maximize total royalty receipts over the patent life. The buyer's incentive is to maximize the present value of the royalty stream during the buyer's investment horizon, which may be shorter.

This counterparty shift is one of the primary reasons that licensees insist on consent rights in the first place. The consent mechanic is, in part, a defense against an unwanted counterparty change. Licensees that are reasonable about granting consent are typically those that have already negotiated robust audit rights, anti-amendment provisions, and other protections that survive the monetization. Licensees that are restrictive about granting consent are typically those that have not.

What this means for new deals

Four implications follow for the drafting, negotiation, and diligence of license agreements and royalty financings in 2026 and beyond.

For licensors with future financing needs. The anti-pledge clause in a license agreement signed today will determine the licensor's monetization optionality five to fifteen years from now. The negotiating moment to address this is at license signing, not at monetization closing.

Licensors should specifically negotiate for (i) a reasonableness standard on consent rather than sole discretion, (ii) an explicit carveout permitting assignment of the royalty receivables (as distinct from assignment of the license itself), (iii) parallel reporting and audit rights that survive any monetization, and (iv) advance language confirming that any monetization will not be deemed a constructive change of control.

The Reata-Dartmouth amendment provides a usable template for licensors that want to retrofit these protections after the original license has been signed: an amendment that adds parallel reporting, expressly permits monetization, and confirms confidentiality protections for the buyer's diligence process can be negotiated as part of the broader license-amendment process even years after original signing.

For royalty financiers diligencing license agreements. Pre-signing diligence on the underlying license is the most important workstream in any royalty financing. The diligence should specifically address (i) the assignment and change-of-control clauses, (ii) whether reasonable-consent or sole-discretion standards apply, (iii) the existence of any tail provisions, ROFRs, or co-promotion options that would survive the monetization, (iv) the audit and information rights and whether they are personal to the licensor, and (v) the change-of-control treatment of corporate reorganizations.

In the consent-required range of the spectrum, pre-signing engagement with the licensee is essential. The BeOne-IMDELLTRA model, in which Amgen's consent was secured before the royalty purchase agreement was signed, is the recommended best practice. Securing consent as a post-signing condition introduces meaningful execution risk and delays closing.

For licensees evaluating consent requests. A licensee approached for consent to a royalty monetization has substantial leverage to extract value, but excessive aggressiveness is short-sighted. The licensor will eventually monetize one way or another; the only question is whether the structure preserves the bilateral relationship or substitutes a worse counterparty (an SPV with limited operational visibility, for example).

The reasonable licensee position is to grant consent in exchange for (i) confirmation that the buyer is a financial institution with sufficient sophistication, (ii) a confidentiality undertaking from the buyer, (iii) preservation of the licensee's existing audit and termination rights, and (iv) a modest consent fee (typically $250,000 to $1 million depending on transaction size). The unreasonable position is to demand fees so large or conditions so restrictive that the licensor walks away from the consent process and structures into an SPV workaround, which leaves the licensee with a less-cooperative counterparty over the long term.

For counsel structuring synthetic royalties. Where the underlying license carries discretionary-consent or absolute-prohibition restrictions, the synthetic royalty structure is often the only viable monetization route.

The Royalty Pharma-Revolution Medicines daraxonrasib deal is the modern template: the seller owns the underlying asset outright and grants the buyer a direct synthetic obligation, bypassing any third-party license entirely. This structure works only when the seller does in fact own the asset; it is not available where the royalty stream depends on a third-party license that cannot be amended.

Counsel structuring a new synthetic royalty should specifically address (i) the obligation's characterization as a true sale versus a secured loan, (ii) the perfection mechanics in the appropriate UCC jurisdiction, (iii) the bankruptcy treatment of the structure, particularly in light of post-Mallinckrodt jurisprudence, and (iv) the disclosure regime that will apply to the synthetic obligation in the seller's subsequent SEC filings.

The verdict

Anti-pledge provisions are the most consistently underestimated structural friction in pharmaceutical royalty finance. They impose a tax on monetization that few buy-side models price correctly and that most sell-side preparation efforts address too late in the deal cycle.

Each step rightward on the pledge-restriction spectrum lowers the speed of monetization, raises the buyer-side discount, and raises the probability that the transaction must be restructured into a synthetic or SPV-isolated form that delivers materially worse economics than a clean assignment would have.

The 2020 to 2026 transactional cohort shows that the modal modern license sits in the reasonable-consent or sole-discretion range of the spectrum, and that the modal royalty monetization therefore requires a consent letter or license amendment as a condition to closing. The processes are well-developed and the timelines are well-understood, but the diligence and structuring effort required is non-trivial and the residual execution risk is meaningful.

For royalty financiers, the practical response is to make pre-signing license diligence the first workstream of every transaction, to engage the licensee early where consent is required, and to model the consent-friction cost into the buyer-side price. For licensors, the practical response is to recognize that the anti-pledge clause in tomorrow's license agreement will determine the monetization economics in next decade's financing, and to negotiate accordingly. For licensees, the practical response is to recognize that the consent right is a tool for preserving relationship quality rather than a fee-extraction mechanism, and to use it accordingly. For counsel, the practical response is to draft consent and assignment clauses with the eventual monetization in mind, to structure synthetic royalties where the underlying license is too restrictive to support a traditional structure, and to integrate the consent letter, license amendment, and royalty purchase agreement into a single coordinated closing.

The next two to three years of royalty financing volume will reveal whether the current standardization of consent-letter mechanics holds up as more deals move into the consent-required range of the spectrum. The volume of royalty deals signed in 2024 to 2025 (with more than $29.4 billion in biopharma royalty financings from 2020 to 2024) suggests that the market has substantially absorbed the friction.

The structural advantages of getting the anti-pledge architecture right at license signing are substantial enough that, once the discipline takes hold among sophisticated licensors, the friction at monetization should compress meaningfully.

This article reflects publicly available information as of May 2026. It does not constitute investment, legal, or tax advice. Mechanics and structural details described are derived from SEC filings, royalty purchase agreements, license agreement amendments, and published legal analysis. Royalty financiers, licensors, licensees, and counsel evaluating specific transactions should rely on the underlying contracts and counsel.This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.