Best-Efforts Placements in Pharmaceutical Royalty Finance: How They Work, How They Reshape the Stack

Best-efforts placements are the most procedurally important and economically misunderstood capital-raising structure in modern royalty finance.

They sit on the cover page of almost every micro-cap and small-cap biotech offering memorandum since 2023, framed in three lines of stock language: "the placement agent shall serve as the exclusive placement agent for the Company, on a reasonable best-efforts basis." That phrase governs the way that future royalty originators (the licensors that any royalty fund underwrites) get their bridge capital between deal events.

The structure also appears, more selectively, in the documentation of certain royalty-backed bond placements, in the 144A offerings of synthetic royalty notes, and in the equity raises of royalty aggregators themselves. The mechanism is the same in each case. The economic consequences for a buy-side underwriter looking at the issuer's future royalty stream are not.

This piece works through the mechanics of best-efforts placements as they appear in modern pharmaceutical capital markets, the resulting impact on the royalty stack at the originator level and at the platform level, the recent placement cohort that illustrates the variation in structure, and the legal architecture that royalty financiers and counsel should attend to when evaluating an issuer that has just closed (or is about to close) a best-efforts deal.

What a best-efforts placement actually is

A best-efforts placement is a securities offering in which the placement agent (an investment bank, typically a small or mid-tier firm) agrees to use commercially reasonable efforts to solicit purchases of the issuer's securities. The agent does not commit its own balance sheet to acquiring those securities. The agent acts as agent, not as principal.

The legal cornerstone is the placement agency agreement, a one-to-two-page exhibit filed alongside the prospectus supplement or the 8-K announcing closing.

The standard formulation, repeated almost verbatim across hundreds of 2024 to 2026 filings, runs as follows: "the Company expressly acknowledges and agrees that the Placement Agent's obligations hereunder are on a reasonable best efforts basis only and that the execution of this Agreement does not constitute a commitment by the Placement Agent to purchase the Securities and does not ensure the successful placement of the Securities or any portion thereof or the success of the Placement Agent with respect to securing any other financing on behalf of the Company."

That sentence does almost all of the work. The agent is not buying anything, the agent is not guaranteeing anything, the agent earns a commission only on what actually clears, and the issuer absorbs the entire residual marketing risk.

The distinction is sharp against firm commitment underwriting. In a firm commitment offering, the underwriter purchases the entire issue from the company at a negotiated price and then resells it into the market. The underwriter is the principal, and the underwriter bears the inventory risk.

FINRA-published guidance and standard FINRA Series materials describe the contrast succinctly: the firm commitment underwriter buys the entire issue from the issuer and then resells it to investors, whereas the best-efforts underwriter agrees to use its best efforts to sell the offering but does not guarantee that all securities will be sold. Any unsold units or shares are returned to the issuer.

For royalty finance, this distinction is not academic.

It determines whether the licensor that originated the future royalty stream actually receives the capital it was attempting to raise. It determines whether the platform that just monetized a royalty actually closes the matching debt facility. It determines whether the synthetic royalty financing vehicle that is supposed to bring a bond to market actually clears the issuance window.

Three properties define the structure.

Agency, not principal. The agent never takes title to the securities. There is no inventory risk on the agent's balance sheet and no warehousing of unsold paper. If the offering clears 60% of target, the issuer receives 60% of target proceeds (less fees on that amount only) and the remaining securities are simply withdrawn from the offering. The agent's role is functionally that of a finder and a solicitor.

Commission, not spread. The agent earns a cash fee, almost universally in the 6% to 8% range on gross proceeds raised, plus a management fee of approximately 1% and warrant coverage of 5% to 7% of the shares actually sold. The compensation is contingent on what closes, not on what is offered.

By contrast, firm commitment underwriters earn a spread (the difference between the price paid to the issuer and the price at which the securities are sold to investors), which is generally lower in percentage terms (5% to 7%) but applies to the entire issue.

Conditional close. Best-efforts offerings frequently contain closing conditions that further constrain capital certainty.

The two most common are the "all-or-none" structure (the offering closes only if the entire targeted amount is subscribed, otherwise all investor funds are returned from escrow) and the "part-or-none" or "minimum-maximum" structure (a defined minimum amount must be cleared for closing, with a defined maximum cap above that). The presence or absence of these conditions changes the economic profile of the deal materially.

FINRA Rule 5110 treats best-efforts offerings under a distinct regulatory regime. The applicable review period runs from 180 days before the required filing date through 60 days after the final closing. Any payment, right, or interest received by participating members during that window is presumptively underwriting compensation. The implementation regime took effect through FINRA Regulatory Notice 20-10 in 2020.

The filing disclosure obligations are heavier than for firm commitment offerings, the lock-up periods are typically shorter, and the tail-financing provisions (the right of the agent to earn fees on subsequent capital raised from introduced parties) are explicit in almost every placement agency agreement filed with the SEC since 2020.

The Virpax Pharmaceuticals 2024 S-1/A is representative on the tail point. The placement agent was entitled to a 2.5% cash fee on any financing consummated within six months of engagement expiration with any party "actually introduced by Placement Agent to the Company" during the engagement period.

Royalty financiers approaching a recently-placed issuer should be alert to these tails. They can affect how a subsequent royalty monetization is priced and structured.

The five-position spectrum of placement structures

Securities placements exist on a continuum from pure agency (issuer bears every dollar of shortfall risk) to firm commitment (underwriter bears the entire risk and the issuer is guaranteed its check). Best-efforts sits in the middle.

But the precise position on that spectrum determines whether the placement is the kind of instrument a royalty financier can rely on as a meaningful liquidity event for the issuer, or whether it is essentially a probability-weighted hope.

The spectrum collapses into five identifiable structures.

Pure best-efforts. No minimum subscription, no escrow requirement, no all-or-none condition. The agent solicits indications of interest, the issuer prices the offering, and whatever clears clears.

Examples in 2025 to 2026 are numerous: the April 2025 CNS Pharmaceuticals offering with A.G.P./Alliance Global Partners, the January 2025 Processa Pharmaceuticals offering, the September 2025 Reviva Pharmaceuticals offering. All used the standard reasonable best-efforts language and closed on whatever subscription was available.

The capital certainty for the issuer is the lowest on the spectrum. The underwriting spread (combined cash fee plus management fee plus warrant coverage value) is typically 8% to 10% on gross proceeds. This is the modal structure for micro-cap biotech equity in 2025 to 2026 and the structure under which most pre-revenue royalty originators raise their pre-monetization runway.

Part-or-none. A defined threshold subscription (commonly 40% to 60% of target) must be cleared in escrow before closing. Below the threshold, all investor funds are returned and the offering is withdrawn. Above the threshold, the offering closes at whatever level was actually subscribed up to the maximum.

The capital certainty is binary at the threshold but linear above it. This structure is more common in Regulation A+ offerings than in registered direct offerings, but it appears in both. The underwriting spread is similar to pure best-efforts (6% to 8% cash plus extras).

All-or-none. The offering closes only if the entire targeted amount is subscribed. Below 100%, all funds return from escrow and the deal is dead.

This structure is rare in pharmaceutical capital markets (issuers are usually willing to accept partial subscription rather than risk no proceeds at all) but it appears occasionally in Regulation A+ deals and in some Form S-1 offerings where the issuer has a discrete capital need that cannot be met partially. The compensation typically rises to 7% to 9% to reflect the binary structural risk.

Minimum-maximum. A banded structure with a defined floor and ceiling. The offering closes if subscription clears the floor; pricing and final size are settled within the band.

This structure is more common in 144A bond placements (where royalty-backed notes have used minimum-maximum structures since the original NPS Pharmaceuticals 2004 Sensipar securitization) than in equity raises. The 2008 Indevus Pharmaceuticals $105 million non-recourse note placement on SANCTURA royalties used a closely related banded structure.

Firm commitment. The underwriter buys the entire issue at a negotiated price and resells it. The issuer knows on signing exactly how much capital it will receive net of the spread. The spread is typically 5% to 7%, lower than best-efforts compensation in percentage terms.

This is the structure used by established royalty platforms when accessing the bond market. The Royalty Pharma September 2020 issuance of $6 billion in senior unsecured notes in six tranches was a firm-commitment 144A deal led by BofA, Citi, JPMorgan, and Morgan Stanley as joint book-runners. It is also the structure for marketed follow-on offerings by mid-cap and large-cap public companies.

The spectrum collapses to a single economic principle: the further rightward an issuer can push its placement, the more capital certainty it acquires and the lower the percentage cost of capital it pays.

But the rightward positions are gated by issuer quality (market capitalization, public float, trading volume, audit history, and management track record). Most pre-revenue or early-commercial royalty originators are gated at the pure best-efforts position whether or not they would prefer otherwise.

Royalty stack impact: where the cash actually lands

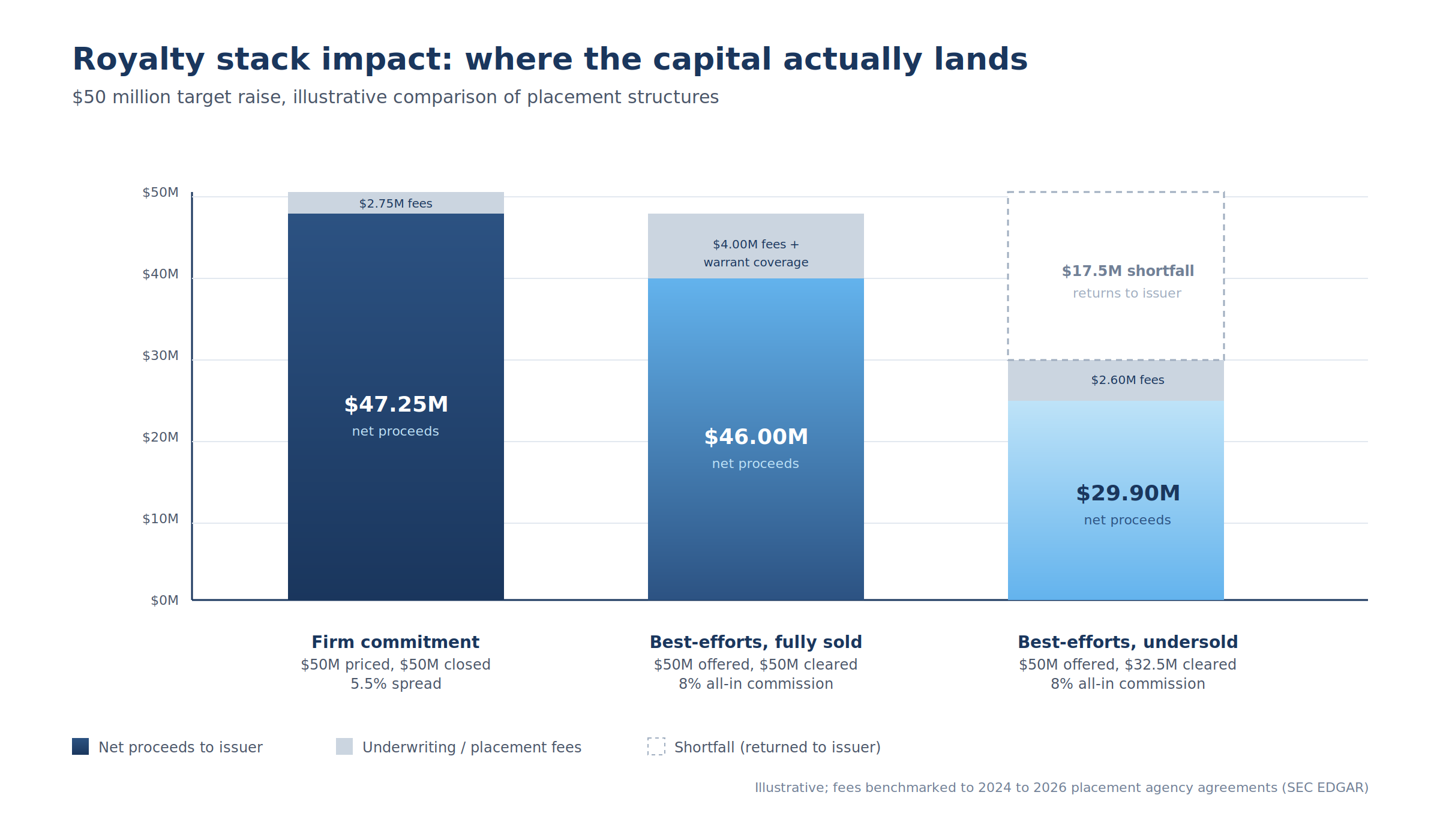

The economic distinction between these positions becomes vivid when traced through a representative $50 million capital target.

Assume a single issuer attempting to raise $50 million to fund Phase 3 trial completion (the milestone after which the asset becomes royalty-eligible), and compare three structures. The three are: firm commitment with a 5.5% spread, best-efforts with full subscription at an 8% all-in cost, and best-efforts with 65% subscription at the same 8% all-in cost on the cleared portion.

In the firm commitment case, the issuer receives $47.25 million net of a $2.75 million spread.

In the best-efforts fully-sold case, the issuer receives $46.00 million net of $4.0 million in cash fees and warrant coverage value. The economic difference, roughly $1.25 million or 2.5% of the target, is the price of the lower capital certainty. The placement agent earned a higher percentage fee, but the issuer pre-positioned for a market in which firm commitment was not available.

In the best-efforts undersold case (which is the modal outcome at the micro-cap segment of the market in 2024 to 2026, where pure best-efforts offerings frequently close at 50% to 75% of target), the issuer receives $29.90 million net.

The $17.5 million shortfall returns to the issuer not as cash but as withdrawn capacity: the offering is reduced in size and the unsold securities are simply not issued. The royalty originator that was modeling $50 million in proceeds against a $30 million Phase 3 budget plus $20 million in working capital now has $29.9 million against a $50 million spend. The gap is either filled with a follow-on raise (often at lower price) or absorbed by program delay.

The mechanical conclusion is that the gross-to-net capital wedge is small (a few percentage points), but the certainty-to-realized wedge can be very large (15% to 50% of the target).

For royalty financiers underwriting an issuer's ability to reach commercial launch on the basis of its disclosed capital position, the difference between a "$50 million best-efforts placement" headline and the actual closed amount matters substantially. Three specific second-order effects on the royalty stack are worth noting.

Reduced downstream royalty financing capacity. A royalty originator that closed an undersubscribed best-efforts placement carries more dilution per dollar raised, has consumed more of its registration capacity (S-1 or S-3 shelf), and is more likely to be running its operations on negative working capital by the time the royalty event triggers (Phase 3 readout, NDA filing, commercial launch).

The royalty financing buyer at that event prices the deal accordingly. A licensor that just closed a clean firm commitment offering presents very differently in royalty diligence from one that just closed a 50%-subscribed best-efforts deal at a 30% discount to the prior trading price.

Warrant overhang. Best-efforts placements almost universally include warrant coverage to the agent (5% to 7% of shares sold) and frequently include investor warrants attached to the units sold.

A typical 2025 micro-cap best-efforts offering issues common stock plus pre-funded warrants plus Common Warrants exercisable at 100% to 125% of the unit price, plus placement agent warrants at 125% of the unit price. The aggregate warrant coverage on a fully-converted basis can exceed 200% of the shares actually sold for cash.

The royalty financing buyer that later acquires a royalty stream from this same issuer must understand the post-money capitalization with full warrant dilution modeled in. That capitalization determines change-of-control thresholds, anti-dilution triggers in the royalty agreement, and the licensor's incentive to accept versus reject a takeout.

Tail-period encumbrance. As noted above, placement agency agreements almost universally contain tail provisions giving the agent the right to a cash fee on any financing arranged with an introduced party for six to twelve months after engagement expiration.

For royalty originators that close a best-efforts equity placement and then attempt to monetize a royalty within the same year, the tail provision can apply. If the royalty financier first contacted the issuer through the placement agent's introduction (or even attended an agent-organized non-deal roadshow), the agent may have a contractual claim on a percentage of the royalty proceeds.

The risk is mitigated by careful drafting in the royalty purchase agreement: a representation that no broker, finder, or placement agent claims compensation; an indemnity from the issuer for any such claim; a closing condition that the issuer deliver a waiver from any placement agent with a potentially applicable tail. But it requires deliberate attention.

The two placement types are not interchangeable for any of the analytical or financing purposes that royalty fund analysts care about.

Recent placement evidence: 2024 to 2026

The 2024 to 2026 placement cohort shows that best-efforts is overwhelmingly the modal structure at the micro-cap and small-cap segments of the pharmaceutical equity market, while firm commitment remains the modal structure at the established royalty platform level.

Seven representative transactions illustrate the variation.

The Royalty Pharma 2020 notes issuance is the platform-level benchmark. Royalty Pharma priced $6 billion of senior unsecured notes in September 2020 in six tranches ranging from three to thirty years, in a firm-commitment 144A offering with joint book-runners. The proceeds refinanced existing Term Loan A and Term Loan B facilities and rebalanced the capital structure of the platform.

The relevant point for this discussion is that established royalty platforms with diversified portfolios and investment-grade credit profiles can access firm-commitment capital at the bond level. The same is not true for the licensors that originate the royalty streams those platforms eventually buy.

The January 2025 Processa Pharmaceuticals placement is the textbook small-cap best-efforts equity raise. A.G.P./Alliance Global Partners served as exclusive placement agent on a reasonable best-efforts basis for an offering of common stock, common warrants, and pre-funded warrants.

The placement agency agreement included the standard 7% cash fee plus 1% management fee, a 90-day exclusive engagement (later extended), and explicit tail-financing provisions. The offering closed at approximately $3 million in gross proceeds against a larger initial target.

The April 2025 CNS Pharmaceuticals placement used the same A.G.P. template at higher size, with the standard 7% cash fee, 1% management fee, warrant coverage to the placement agent, and reasonable best-efforts language.

CNS is a clinical-stage oncology company whose lead asset, if commercialized, would represent a future royalty origination opportunity. Royalty financiers tracking CNS in 2026 should note that the company has done multiple best-efforts placements in 12 months (April 2025, May 2025, and others), each at smaller size than the last. The pattern of repeat fundings indicates chronic undersubscription rather than discrete capital events.

The June 2025 Adial Pharmaceuticals placement is structurally identical. A.G.P. served as exclusive placement agent on reasonable best-efforts, 7% cash plus 1% management fee, common stock and warrants offered under an effective S-1. Adial's lead AUD therapeutic, if successful in Phase 3, would be a textbook out-licensing candidate with potential royalty originator status.

The September 2025 Reviva Pharmaceuticals placement illustrates the tail-end-of-engagement pattern. The placement agency agreement specified a hard close date of September 29, 2025, after which the engagement automatically terminated.

This kind of "use it or lose it" closing window is common at distressed micro-caps and reflects the agent's unwillingness to maintain exclusive engagement indefinitely on an offering that may not close. The royalty relevance is that Reviva, like many micro-caps in this cohort, is using equity proceeds primarily to fund cash runway rather than program advancement. Any future royalty event is being pushed further out in time.

The January 2026 Park Ha Bio follow-on introduces the cross-border dimension. Park Ha is a Cayman Islands exempted company, and the best-efforts follow-on placement of approximately $2.45 million with D. Boral Capital as sole placement agent closed in January 2026 with a 7% cash fee.

The Cayman SPV structure is common for Asian and Israeli biotechs accessing U.S. capital markets. It complicates any subsequent royalty pledge. A royalty financier acquiring rights from a non-U.S. parent through a U.S. subsidiary must navigate cross-border perfection, tax treaty considerations, and UCC Article 9 versus local law conflicts.

The April 2026 FibroBiologics placement closed on April 2, 2026, with H.C. Wainwright as exclusive placement agent on a reasonable best-efforts basis. The economic terms were the now-standard 7% cash fee, 1% management fee, and 7% warrant coverage at $1.65 per share exercise price. Net proceeds were approximately $2.5 million.

FibroBiologics is a pre-IND cell therapy company whose future royalty origination capacity is highly speculative. The company is included here as a representative of the very-early-stage placement segment where best-efforts is essentially the only available capital-raising structure.

The pattern across this cohort is clear. Best-efforts placements at the micro-cap and small-cap level have become highly standardized.

The same three or four placement agents recur: A.G.P./Alliance Global Partners, H.C. Wainwright, D. Boral Capital, Aegis Capital. The same fee structure recurs: 7% cash, 1% management, 7% warrants. The same warrant overlays recur: common warrants at par or near par to unit price, pre-funded warrants at $0.0001 to $0.001 exercise price. The same lock-up and tail provisions recur across deals.

The standardization has reduced execution friction for issuers but has not changed the fundamental economic property of the structure: capital certainty is low, fee burden is high on a relative basis, and the resulting capitalization is more dilutive per dollar raised than any of the higher-certainty alternatives.

The legal architecture: what to look for in the placement agency agreement

The detail of best-efforts placement provisions varies modestly by deal and by agent, but the same set of clauses recurs.

For royalty financiers diligencing an issuer that has recently closed a placement, for counsel structuring an issuer's next financing, and for licensors evaluating their post-placement royalty monetization options, these are the provisions that determine the shape of the asset.

The reasonable best-efforts standard. The phrase "reasonable best efforts" (or "best efforts," or occasionally "commercially reasonable best efforts") appears in nearly every placement agency agreement filed since 2020. The phrase is a term of art borrowed from contract law: it imposes a duty of diligent effort short of a fiduciary duty or a guarantee of outcome.

The agent must actually market the offering, must conduct compliant solicitation activity, must maintain customary records and customary marketing infrastructure. But the agent is not liable for the outcome.

Disputes over what constitutes "reasonable best efforts" in a failed offering are rare in pharmaceutical capital markets (issuers almost never sue placement agents over undersubscription). But the standard does have practical content: an agent that signs a placement agency agreement and then takes no meaningful marketing action could be in breach.

Exclusivity and engagement period. Almost all placement agency agreements grant the agent exclusive engagement for a defined period, commonly 30 to 90 days, sometimes extendable by mutual agreement.

During the exclusivity period the issuer may not engage another agent for the same securities or solicit purchasers directly outside the offering. The exclusivity is the agent's primary protection against issuer free-riding on the agent's marketing effort.

Compensation structure. The dominant 2025 to 2026 compensation pattern is 7.0% cash fee on gross proceeds, 1.0% management fee on gross proceeds, and warrant coverage of 5.0% to 7.0% of the shares sold at exercise prices typically 25% above the offering price.

Some deals include a non-accountable expense allowance of 1.0% to 2.0% in lieu of detailed expense reimbursement. Some include reimbursement of agent legal fees up to a defined cap ($30,000 to $100,000). The aggregate all-in cost of a typical best-efforts placement at the micro-cap level is 9% to 11% of gross proceeds when warrant coverage is valued at Black-Scholes.

The FINRA-published guidance on aggregate underwriting compensation treats compensation equal to or greater than 9% of offering proceeds in connection with an initial public offering, and 8% in all other offerings, as the threshold at which fairness review intensifies. Most 2024 to 2026 micro-cap placements sit at or just below those thresholds when warrant value is included.

Tail period. The tail provision is the most consequential clause for royalty financiers diligencing post-placement issuers.

The typical tail runs six to twelve months after engagement expiration and gives the agent the right to a defined percentage (commonly equal to the cash fee, 6% to 8%) of any financing arranged during that window with parties introduced by the agent during the original engagement.

For royalty financiers, the practical risk is that the placement agent introduced the royalty fund to the issuer (through investor day attendance, non-deal roadshow, or direct introduction during the placement marketing period) and then claims a tail fee on the royalty proceeds.

The risk is mitigated by careful drafting in the royalty purchase agreement: a representation that no broker, finder, or placement agent claims compensation; an indemnity from the issuer for any such claim; a closing condition that the issuer deliver a waiver from any placement agent with a potentially applicable tail. But it requires deliberate attention.

Right of first refusal on future financings. Many placement agency agreements grant the agent a right of first refusal to serve as lead agent on subsequent financings within a defined period (commonly 12 to 18 months). FINRA Rule 5110 limits ROFR to no more than three years and requires that the issuer have only one opportunity to waive or terminate this right.

The ROFR is rarely exercised on royalty monetization transactions (royalty deals are private, structured trades that are not within the agent's customary product), but the existence of the ROFR can complicate the negotiation of those trades.

Closing conditions. The placement agency agreement specifies the conditions to closing: the registration statement effective; no stop order; representations and warranties true; opinions of counsel delivered; comfort letter from accountants; and the agent's satisfaction with the due diligence investigation.

The last condition is the agent's primary protection against post-engagement issuer adverse events. Several 2025 placement agency agreements explicitly include the right of the agent to terminate the engagement prior to closing "if it reasonably determines that it is unsatisfied with the results of its due diligence investigation," which is broader than the customary materially-adverse-change clause.

Indemnification and contribution. Best-efforts placement agency agreements include broad issuer indemnification of the agent for liabilities arising from the offering (other than the agent's own willful misconduct or gross negligence), reciprocated by a narrower agent indemnification of the issuer for information the agent specifically supplied.

The indemnity scope and the contribution mechanics are largely standard and are rarely negotiated outside the largest deals.

Lock-up provisions. The issuer (and frequently its officers and directors) is locked up from issuing additional securities or selling existing securities for a period (typically 60 to 90 days, sometimes longer) following the closing.

The lock-up is designed to prevent the issuer from immediately diluting investors who purchased in the placement.

Choice of law and dispute resolution. Placement agency agreements are typically governed by New York law (occasionally Delaware), with disputes submitted to New York courts. The choice is conventional and rarely consequential for the kinds of disputes that do arise (compensation disputes, tail-fee claims, and post-closing indemnification claims).

Accounting and financing consequences

The accounting treatment of best-efforts placement proceeds at the issuer level is straightforward. Proceeds net of placement costs are credited to the appropriate equity or debt accounts under ASC 470 or ASC 718 as applicable. But two more subtle considerations affect royalty financing analytics.

Capitalization quality. Securities issued in best-efforts placements at micro-cap and small-cap issuers in 2025 to 2026 carry substantial warrant overhang.

A typical structure issues common stock at a unit price of $1.50, with attached common warrants exercisable at $1.65 (10% above unit price) and placement agent warrants exercisable at $1.875 (25% above unit price). If the issuer's stock trades flat or below the unit price for the warrant term (typically five years), the warrants expire unexercised and the capitalization stabilizes at the cash-raised level. If the stock trades above the warrant exercise prices, warrant exercise generates additional cash for the issuer but also additional dilution.

For royalty financing buyers underwriting the issuer's future royalty stream, this warrant overhang affects the change-of-control calculation. Many royalty agreements include a change-of-control trigger that gives the royalty holder a call right or a put right on a defined event (typically a 50% change in beneficial ownership, an asset sale, or a merger).

If the issuer has a heavily warranted capitalization, the post-money-equivalent ownership thresholds for the trigger can be reached at very different cash-investment thresholds than the as-reported share counts suggest. The royalty financier should model post-money capitalization with full warrant exercise to understand the actual trigger geometry.

Going-concern signaling. A series of repeated best-efforts placements at declining size and declining price is the strongest available going-concern signal for a public micro-cap biotech.

Royalty financiers approaching such an issuer must adjust their probability of survival assumptions downward. A licensor that closes three placements of $5 million, $4 million, and $3 million in successive quarters is signaling that public capital markets are progressively losing appetite for its securities, that the cash burn rate is not improving, and that the next financing event (if any) will be at lower price, larger dilution, or both.

The royalty financing alternative is increasingly attractive to such issuers (non-dilutive, no warrant overhang, structurally subordinated to operations rather than to share count). This is why the population of royalty-monetization candidates is correlated with the population of repeat best-efforts issuers.

The diligence question for the buyer is whether the asset itself supports a clean royalty financing or whether the asset is collateralized to a degree that complicates the trade.

Article 9 perfection on subsequent royalty pledges. When an issuer that has just closed a best-efforts equity placement subsequently sells a royalty interest to a royalty fund, the royalty purchase agreement and the related security agreement (if the structure includes a back-up security interest) must be perfected under Article 9 of the UCC of the relevant state.

The recent equity placement does not directly affect the royalty perfection, but it does affect the senior debt position of any lender that took a blanket lien on the issuer's assets at or before the placement. A blanket lien on "all assets" perfected before the royalty sale will, absent a release, encumber the royalty interest the fund is attempting to acquire.

Royalty financiers should require lien searches that postdate the most recent best-efforts placement and should obtain releases or subordination agreements from any senior lender as a closing condition.

Tax considerations. Cash proceeds of a best-efforts equity placement are not taxable to the issuer. Cash proceeds of a debt placement (including a royalty-backed note placement) are not taxable but generate interest deductions over the life of the debt. Cash proceeds of a synthetic royalty sale that is characterized as a debt transaction for tax purposes are similarly treated.

The accounting and tax treatment is well-settled and rarely the source of post-closing surprise. The more subtle question (whether a synthetic royalty sale is characterized as a true sale of intellectual property for tax purposes or as a financing) is unaffected by the placement structure of the issuer's prior equity raises.

A representative example of a royalty-backed note placement using a banded structure is the 2009 PDL BioPharma $300 million senior secured notes deal, in which QHP Royalty Sub LLC issued notes secured by 60% of PDL's royalties on Avastin, Herceptin, Lucentis, and Xolair. The transaction used Rule 144A and Regulation S as the offering venue and was structured as a firm-commitment underwriting at the bond level, with the marketing risk borne by the underwriters rather than the issuer.

The 2008 Indevus Pharmaceuticals $105 million non-recourse note placement on SANCTURA royalties is similar in concept. Both transactions illustrate that established royalty assets can support firm-commitment bond placements. The best-efforts structure is reserved for issuers and assets without the credit profile to attract that commitment.

What this means for new deals

Four implications follow for the negotiation and diligence of best-efforts placements in 2026 and beyond, for the issuers that use them and the royalty financiers that evaluate the issuers afterwards.

For licensors with future royalty potential. Best-efforts equity placements are appropriate for capital needs that cannot be met more efficiently through royalty monetization, project financing, or other non-dilutive structures. But the decision to use a best-efforts equity raise rather than a royalty financing should be deliberate, not default.

A licensor with a Phase 3 asset that will generate royalty income within 12 to 24 months can frequently raise as much capital through a synthetic royalty sale (with no dilution, no warrant overhang, and no tail encumbrance) as through a series of best-efforts equity placements.

The royalty financing alternative has been historically underused because of perceived complexity and longer execution timeline. The 2024 to 2026 cohort of established royalty fund counterparties has shortened both materially.

For royalty financiers diligencing recently-placed issuers. A clean royalty financing diligence on a recently-placed issuer requires close reading of the placement agency agreement.

The five specific items to look for are:

(i) the tail-period scope and whether the royalty fund could plausibly be characterized as an introduced party;

(ii) the right of first refusal scope and whether it covers royalty transactions (almost always no, but worth confirming);

(iii) the lock-up provisions and whether they apply to royalty sales (typically not, but ambiguous in some recent drafts);

(iv) the placement agent warrant coverage and whether warrant exercise affects change-of-control thresholds in the royalty agreement; and

(v) the senior lender lien position, particularly if the placement was paired with a venture debt facility.

None of these is typically a deal-breaker, but each requires explicit treatment in the royalty purchase agreement closing checklist.

For royalty platforms accessing the bond market. Established royalty platforms with diversified portfolios and investment-grade credit profiles continue to access capital through firm-commitment bond placements, and that capacity is not at risk.

The capital flowing through best-efforts placements at the micro-cap segment is a fundamentally different market: smaller, more dilutive, more episodic, more reliant on retail-influenced investor demand. Platform-level capital strategy should not be confused with the financing patterns of pre-commercial licensors.

For counsel structuring synthetic royalty notes. Synthetic royalty bond placements (including those done under Rule 144A) sit between the two ends of the spectrum.

The 2024 to 2026 cohort suggests that synthetic royalty notes backed by single-asset royalty streams (the Indevus, NPS, PDL templates) and notes backed by diversified portfolios (the Royalty Pharma template) both clear the bond market, but the placement structure differs.

Single-asset notes more frequently use 144A private placement with a banded or minimum-maximum subscription structure. Portfolio notes use firm commitment. The choice is driven by the underlying asset risk profile and the available investor base, not by the placement agent's preference.

Counsel structuring a new synthetic royalty note should benchmark to the closest comparable transaction by asset profile rather than to the most recent transaction by date.

The verdict

Best-efforts placements are the dominant equity financing structure for the licensor population that originates pharmaceutical royalty streams, but they impose a structural cost on the royalty stack at the originator level that few buy-side models price correctly.

Each step leftward on the spectrum from firm commitment to pure best-efforts lowers the licensor's capital certainty, raises the per-dollar dilution, raises the per-share warrant overhang, and raises the probability that the issuer arrives at the royalty financing table with a depleted balance sheet and a complicated capitalization.

The 2024 to 2026 placement cohort shows that the modal mid- and late-stage pre-revenue licensor finances itself through repeated best-efforts placements at progressively declining size, with a stable set of micro-cap focused placement agents using highly standardized fee structures.

The population of clean firm-commitment-eligible issuers is small and concentrated in the platform tier (Royalty Pharma, Healthcare Royalty, the largest mid-caps). Below that tier, best-efforts is the only available structure.

For royalty financiers, the practical response is to read the placement agency agreement in addition to the royalty agreement, to model post-money capitalization with full warrant exercise, and to require placement-agent waivers as a closing condition where the tail period overlaps the royalty financing.

For licensors, the practical response is to evaluate whether non-dilutive royalty monetization could substitute for the next planned best-efforts equity raise. The answer is increasingly yes.

For counsel, the practical response is to draft tail provisions narrowly, to draft ROFR provisions to exclude royalty transactions explicitly, and to draft change-of-control triggers in royalty agreements with full warrant dilution in mind.

The next two to three years of pharmaceutical capital formation will reveal whether the best-efforts equity treadmill that has characterized the micro-cap segment since 2023 gives way to broader royalty monetization adoption among pre-revenue licensors. The volume of royalty deals signed in 2025 to early 2026 suggests it is beginning to.

The structural advantages of royalty financing over repeated best-efforts equity (non-dilutive, no warrant overhang, no tail encumbrance, capital certainty at signing) are substantial enough that the shift, once it gathers pace, is unlikely to reverse.

This article reflects publicly available information as of May 2026. It does not constitute investment, legal, or tax advice. Mechanics and structural details described are derived from SEC filings, FINRA rules and notices, placement agency agreements, and published bond offering memoranda. Royalty financiers, licensors, and counsel evaluating specific transactions should rely on the underlying contracts and counsel. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.