Company of the week: BioCryst

BioCryst Pharmaceuticals (Nasdaq: BCRX) is a Research Triangle Park, North Carolina-based commercial-stage rare disease biotechnology company anchored by ORLADEYO (berotralstat), the first oral, once-daily plasma kallikrein inhibitor approved for the prophylaxis of hereditary angioedema (HAE).

BioCryst Pharmaceuticals (Nasdaq: BCRX) is a Research Triangle Park, North Carolina-based commercial-stage rare disease biotechnology company anchored by ORLADEYO (berotralstat), the first oral, once-daily plasma kallikrein inhibitor approved for the prophylaxis of hereditary angioedema (HAE).

Founded in 1986 out of the University of Alabama at Birmingham, BioCryst has spent the past five years executing one of the most consequential capital structure transformations of any single-product commercial biotech in the rare disease category, financed through a sequence of synthetic royalty sales, a securitised credit facility, an asset divestiture, and most recently a $700 million enterprise value asset acquisition closed in January 2026.

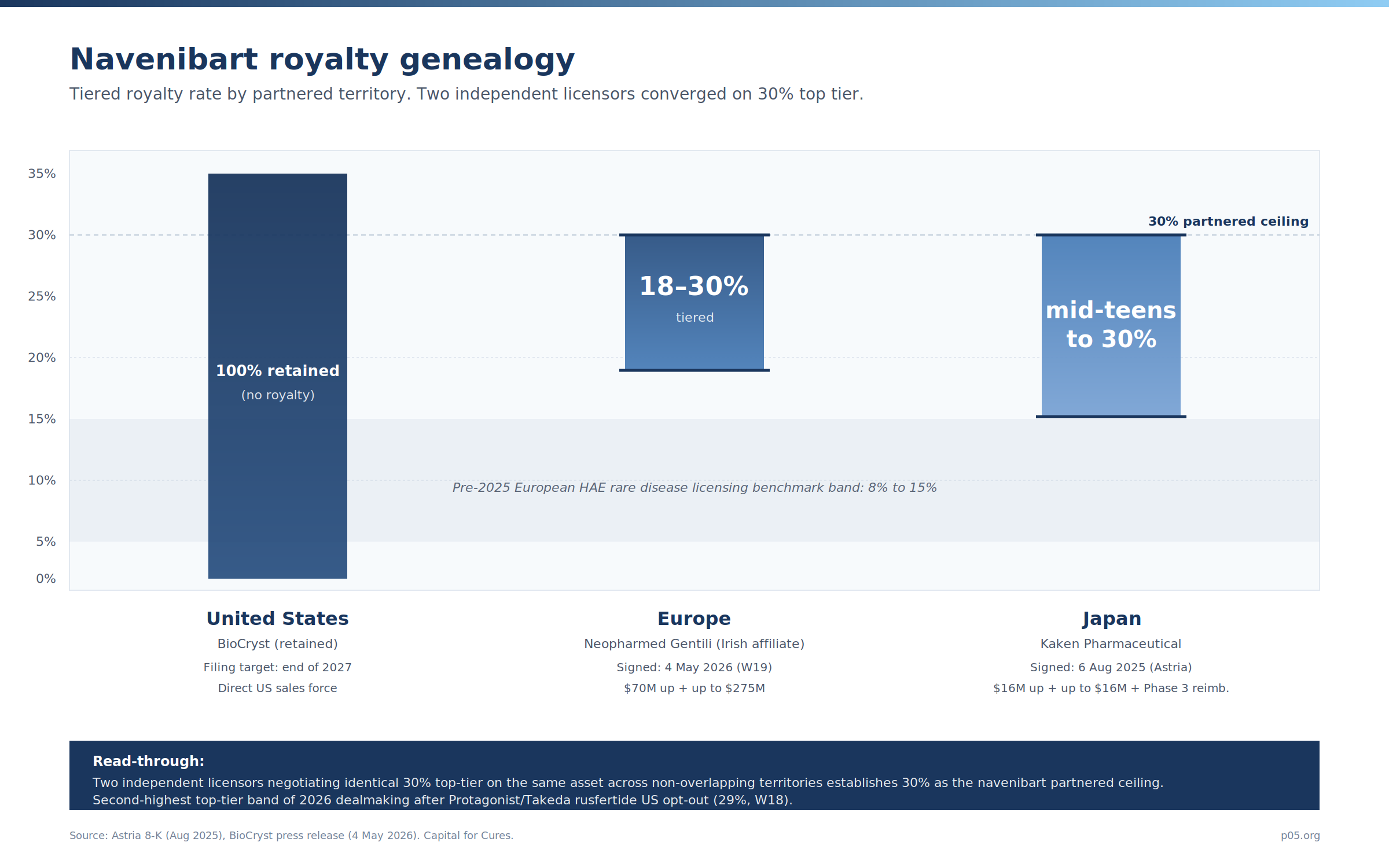

On May 4, 2026, BioCryst announced that it had granted an Irish affiliate of Neopharmed Gentili exclusive rights to commercialize navenibart for HAE in Europe in exchange for a $70 million upfront payment, up to $275 million in regulatory and sales milestones, and tiered royalties on European net sales ranging from 18% to 30%.

The announcement was the second commercial transaction between the two companies in eight months, and it completes the European deconsolidation of BioCryst's HAE franchise: the October 2025 sale of European ORLADEYO commercial rights to Neopharmed Gentili for $250 million upfront plus up to $14 million in CEE milestones; and now the corresponding navenibart European license under broadly parallel commercial logic.

The headline economics on the May 4 deal are straightforward: $70M up + up to $275M = up to $345M before royalties, with tiered royalties of 18% to 30% on European net sales. The signal in those royalty rates is, however, the more interesting feature of the transaction.

The 30% top tier sits at or near the ceiling of 2026 European HAE rare disease licensing comparables, materially above pre-2025 European royalty bands of 8% to 15%, and is now the second consecutive disclosed navenibart partner royalty band to top out at 30%, following Astria Therapeutics's August 2025 license to Kaken Pharmaceutical for Japan ($16M up, up to $16M in milestones, tiered royalties up to 30%).

Two independent licensors negotiating identical top-tier rates on the same asset across two different territories is meaningful market evidence that 30% has become the navenibart partnered-territory ceiling, and is currently the second-highest disclosed top-tier royalty band of 2026 dealmaking after the Protagonist Therapeutics opt-out from the Takeda rusfertide US collaboration (W18, 14% to 29% on worldwide net sales).

This piece examines BioCryst's origins, the ORLADEYO franchise and its layered upstream royalty stack, the January 2026 Astria Therapeutics acquisition that brought navenibart into the portfolio, the May 4 Neopharmed Gentili European license and its position in the navenibart royalty genealogy, the Blackstone facility that financed the Astria cash portion, the Phase 3 navenibart clinical program, the broader HAE prophylaxis competitive landscape, and what the cumulative capital structure now signals about BioCryst's structural cash flow profile heading into the 2027 navenibart US filing window.

The Origin Story: A Structure-Guided Drug Design Survivor

BioCryst was founded in 1986 and is one of the older independent biotechnology companies still in operation. The company built its early reputation on structure-guided drug design, a medicinal chemistry approach that crystallises target proteins to inform small-molecule inhibitor optimisation.

The platform produced RAPIVAB (peramivir, an intravenous influenza neuraminidase inhibitor approved by the FDA in 2014), galidesivir (a broad-spectrum antiviral originally developed in partnership with the US government for hemorrhagic fevers), and most consequentially berotralstat, the molecule that became ORLADEYO.

ORLADEYO received FDA approval on December 3, 2020 for the prophylaxis of HAE attacks in patients aged 12 and older, becoming the first oral, once-daily prophylactic therapy in a category that had until then been dominated by injectable and intravenous biologics.

The European Commission approved ORLADEYO in April 2021 and the product launched commercially across the EU through a BioCryst-owned commercial infrastructure originally built specifically for the European HAE market. Pediatric label expansion to ages 2 and older followed in subsequent years.

The commercial trajectory has been steep. Full-year 2024 ORLADEYO net revenue was $437 million (+34% year-on-year). Full-year 2025 ORLADEYO net revenue was $601.8 million (+38% year-on-year, +43% on a comparable basis excluding European revenue post the October 2025 sale).

Q1 2026 ORLADEYO revenue was $148.3 million (+11% year-on-year reported, +21% on a comparable basis), and management has maintained full-year 2026 ORLADEYO guidance at $625 million to $645 million.

After the European divestiture, more than 90% of ORLADEYO net revenue is now generated in the United States.

The leadership team has been substantially remade through the Astria transaction and the surrounding strategic reorientation.

Charlie Gayer, formerly President and Chief Commercial Officer, was appointed President and Chief Executive Officer in early 2026 following Jon Stonehouse's transition out of the CEO role; Anthony Doyle is Chief Financial Officer; and in April 2026 the company appointed Sandeep M. Menon as Chief Research and Development Officer, replacing Helen Thackray and signalling a deliberate move toward a more disciplined, capital-efficient development organisation focused on a narrower rare disease pipeline.

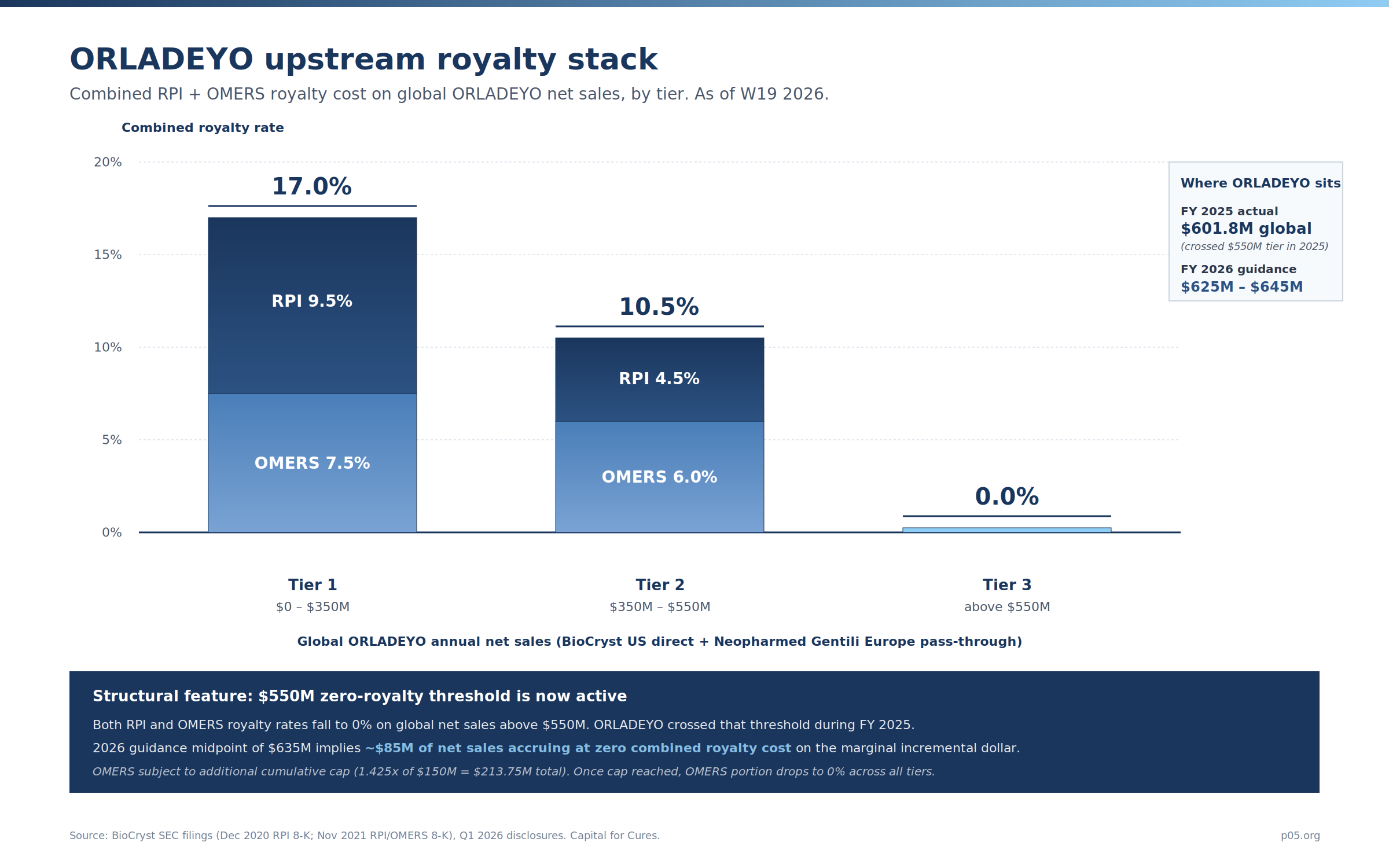

The ORLADEYO Royalty Stack: A Layered Upstream Architecture

The ORLADEYO franchise is the textbook example of a single-product commercial biotech that funded its launch and category expansion through a sequence of synthetic royalty transactions, layered against an existing commercial term loan, before subsequently restructuring the entire capital stack as the product approached commercial maturity.

Across the 2020 to 2021 financing window, BioCryst sold three distinct synthetic royalty interests to two counterparties (Royalty Pharma in two tranches; OMERS Capital Markets in one tranche) for combined upfront proceeds of $425 million. None of the three royalty interests has been retired or modified materially since then. All continue to apply against global ORLADEYO net sales (including European pass-through revenue from Neopharmed Gentili post the October 2025 divestiture).

Layer 1A: Royalty Pharma (RPI), December 2020

The original synthetic royalty transaction occurred contemporaneously with FDA approval. On December 7, 2020, Royalty Pharma acquired a tiered royalty interest in ORLADEYO and BCX9930 for a $125 million upfront cash payment. The structure was 8.75% on direct annual ORLADEYO net sales up to $350 million, 2.75% on sales between $350 million and $550 million, no royalty on sales above $550 million, and a tiered percentage of sublicense revenue in certain territories.

RPI also received a 1.0% royalty on global net sales of BCX9930 (BioCryst's then-developmental oral Factor D inhibitor) and certain related compounds. The 2020 RPI deal was paired with a $200 million credit facility from Athyrium Capital Management, of which BioCryst drew $125 million at closing.

The economic features of the 2020 RPI deal that matter for current royalty cost modelling are the tier breakpoints, which were chosen to align with management's launch-period sales forecast: $350 million was approximately the year-five base case revenue projection at the time of the transaction; $550 million was the optimistic-case ceiling above which RPI agreed not to participate.

From RPI's perspective, the structure trades a hard cap on participation upside in exchange for first-loss protection on the floor of the launch trajectory.

From BioCryst's perspective, the structure provides launch capital without dilution and without principal repayment risk, in exchange for foregone royalty economics on the first $550 million of annual net sales.

Layer 1B: Royalty Pharma expansion, November 2021

On November 22, 2021, RPI acquired an additional royalty interest for a further $150 million upfront payment, layering an incremental 0.75% royalty on direct annual ORLADEYO net sales up to $350 million, 1.75% on sales between $350 million and $550 million, no royalty on sales above $550 million, and an additional tiered percentage on sublicense revenue.

The November 2021 expansion brought RPI's combined ORLADEYO royalty position to 9.5% on direct annual net sales up to $350 million, 4.5% on sales between $350 million and $550 million, and 0% on sales above $550 million.

Worth noting on the structural shape of the 2020 + 2021 RPI position: the 2020 tier 1 rate (8.75%) is meaningfully higher than the 2021 expansion tier 1 rate (0.75%), but the 2021 tier 2 rate (1.75%) is meaningfully higher than the 2020 tier 2 rate (2.75% versus the original 2.75% — no, the 2020 tier 2 rate was already 2.75%).

The combined picture is a deal in which RPI bid for additional tier 1 economics in 2020 and additional tier 2 economics in 2021, suggesting that by November 2021 the launch trajectory was already strong enough that RPI's marginal value perception had shifted toward the higher-revenue tier rather than the floor.

Layer 2: OMERS Capital Markets, November 2021 (with Regime A / Regime B optionality)

Concurrent with the November 2021 RPI expansion, BioCryst entered into a separate $150 million synthetic royalty financing with OCM IP Healthcare Holdings Limited, an affiliate of OMERS Capital Markets, the Canadian pension plan's healthcare royalty platform. The OMERS structure is meaningfully more complex than the RPI structure, in three specific respects.

The base structure is capped, tiered, and declining. OMERS receives 7.5% on annual ORLADEYO net sales up to $350 million, 6.0% on sales between $350 million and $550 million, and 0% above $550 million. The maximum total return cap is 1.425x of $150 million invested = $213.75 million; once OMERS reaches that cumulative cap, no further royalty payments are owed under the agreement, regardless of subsequent ORLADEYO net sales.

There is a second-step cap option triggered by 2023 sales performance. If 2023 direct sales fell below a prespecified threshold, the cap would have been adjusted upward to 1.550x of $150 million = $232.5 million instead of 1.425x. This provided downstream cap-rate protection for OMERS in the scenario where launch performance fell short.

There is also a Regime A / Regime B royalty rate optionality structure. If 2023 direct sales reached the prespecified threshold, OMERS would receive what the SEC filings describe as the Regime A rates (the 7.5% / 6.0% / 0% schedule). If 2023 sales fell below the threshold, OMERS would instead receive the Regime B rates of 10.0% on the first $350 million and 3.0% on the $350M to $550M tier (with 0% above $550M), under the higher 1.550x cap.

ORLADEYO's 2023 sales performance triggered Regime A. The first OMERS royalty payment from BioCryst commenced based on Q4 2023 direct sales.

The Regime A / Regime B mechanic is unusual in synthetic royalty structuring and is worth pausing on: it functions as a mid-deal optionality reset, with the licensor (BioCryst) effectively buying lower royalty rates on the success path in exchange for accepting higher royalty rates on the failure path.

From OMERS's perspective, the Regime B option provides downside-rate protection in a scenario where the cumulative cap is unlikely to be reached on the original schedule. From BioCryst's perspective, Regime A locked in the lower royalty rate schedule once the 2023 sales hurdle cleared.

The cumulative cap mechanism is the more material consideration today. With 2025 ORLADEYO global net sales at $601.8 million, OMERS has been receiving royalty payments at the Regime A rates for roughly two years. The cap of $213.75 million has not yet been reached on current trajectory; assuming approximately 17.0% combined tier 1 royalty cost (RPI + OMERS) on the first $350 million of global net sales, OMERS's individual share of that combined rate is 7.5%, or approximately $26.25 million per year.

At that pace, the OMERS cap is reached in approximately five additional years from now, in 2030 to 2031. Beyond that point, OMERS receives no further royalty payments and BioCryst's effective royalty cost on the $0 to $350M tier drops from 17.0% to 9.5% (RPI only).

A useful related discussion of the OMERS franchise mechanics, including this transaction, appears in the Fund of the week: OMERS Life Sciences piece.

Layer 3: European Pass-Through to Neopharmed Gentili

The October 2025 sale of European ORLADEYO commercial rights to Neopharmed Gentili did not extinguish the global RPI and OMERS royalty obligations. Both royalties continue to apply against global ORLADEYO net sales (BioCryst direct sales plus Neopharmed Gentili European net sales), and European revenue is still credited to BioCryst for the purpose of determining global royalty tiers and the OMERS cumulative cap.

Under the structure, Neopharmed Gentili pays its proportionate share of the aggregate global royalty rate on its European net sales, and BioCryst pays its proportionate share on its US direct sales, with both contributions aggregating against the global tier thresholds. The mechanic preserves BioCryst's economic exposure to total global royalty progression while transferring the operational responsibility for the European portion of the obligation to Neopharmed Gentili.

This pass-through structure is non-trivial. Most regional commercial divestitures in the rare disease category result in either (i) the original synthetic royalty being restructured to apply only against the retained territory (with a corresponding reduction in royalty cap or rate); or (ii) a one-time settlement payment to the royalty holder in exchange for releasing the divested territory from the royalty obligation. Neither mechanic was used here.

Instead, BioCryst, Neopharmed Gentili, RPI, and OMERS agreed on a pass-through structure that preserves the global aggregation of net sales across the divested and retained territories. The arrangement is particularly sensible given the proximity of ORLADEYO's global net sales to the $550 million zero-royalty threshold: with ORLADEYO already crossing the $550M tier in 2025, restructuring the synthetic royalty would have required complex valuations of remaining royalty exposure in a tier 3 zero-rate environment.

The retired Pharmakon term loan

A fourth historical layer, now extinguished, is worth noting for completeness. BioCryst had a term loan with Pharmakon Advisors with an outstanding balance of approximately $249 million. The proceeds of the European ORLADEYO sale were used to retire the Pharmakon term loan, which was the explicit structural rationale BioCryst gave for the European divestiture. The retirement eliminated approximately $70 million of future interest payments over the remaining life of the loan and produced a meaningful improvement to BioCryst's free cash flow profile heading into 2026.

Synthesis: the upstream royalty stack today

The combined RPI + OMERS effective royalty cost on global ORLADEYO net sales is 17.0% on the first $350 million tier (9.5% RPI + 7.5% OMERS), 10.5% on the $350M to $550M tier (4.5% RPI + 6.0% OMERS), and 0% above $550 million (subject to the OMERS cumulative cap not having been reached). On 2026 guidance of $625 million to $645 million in global net sales, with the midpoint at $635 million:

| Tier | Net sales in tier | Combined royalty rate | Annual royalty cost |

|---|---|---|---|

| Tier 1 ($0 to $350M) | $350M | 17.0% | $59.5M |

| Tier 2 ($350M to $550M) | $200M | 10.5% | $21.0M |

| Tier 3 (above $550M) | $85M | 0.0% | $0M |

| Total | $635M | 12.7% blended | $80.5M |

The blended royalty cost rate of approximately 12.7% on 2026 guidance midpoint compares with a 17.0% combined tier 1 rate at the start of the launch trajectory. As ORLADEYO continues to grow into the $625 million to $645 million guidance band and beyond, the blended royalty cost rate continues to compress toward the long-term asymptote of 9.5% (the RPI tier 1 rate, with OMERS post-cap and tier 3 at zero on the marginal incremental dollar). The structural picture is that ORLADEYO's per-dollar royalty cost has been materially declining for two years and continues to decline.

The Astria Acquisition: Adding Navenibart Into the Portfolio

On October 14, 2025, BioCryst announced the acquisition of Astria Therapeutics for an implied value of $13.00 per Astria share, structured as $8.55 in cash plus 0.59 BioCryst common shares per Astria share, representing approximately $920 million in equity value and approximately $700 million in enterprise value (net of Astria's cash at closing). The transaction closed on January 23, 2026 and was accounted for as an asset acquisition, with BioCryst recognising a $697.8 million non-cash special charge for acquired in-process R&D in Q1 2026.

The asset BioCryst acquired is Astria's lead clinical program, navenibart (formerly STAR-0215), an investigational long-acting monoclonal antibody inhibitor of plasma kallikrein with YTE-modified Fc domain extension designed to enable subcutaneous administration every three months (Q3M) or every six months (Q6M) for HAE prophylaxis. Astria had originated the program internally, advanced it through ALPHA-STAR (Phase 1b/2) and ALPHA-SOLAR (long-term open-label extension), and initiated the Phase 3 ALPHA-ORBIT pivotal trial in February 2025.

Navenibart's positioning is the long-acting end of the HAE prophylaxis spectrum: against Takeda's Takhzyro (lanadelumab, every 2 weeks), CSL's Andembry (garadacimab, every 4 weeks), and Ionis's Dawnzera (donidalorsen, every 4 to 8 weeks; FDA approved August 2025), navenibart's two to four annual injections is the most infrequent dosing schedule of any monoclonal antibody approach in the category.

Financing the cash portion: the Blackstone facility

To fund the cash portion of the Astria consideration ($8.55 per share across approximately 50 million Astria shares), BioCryst entered into a $550 million senior secured credit facility with funds managed by Blackstone on October 14, 2025. The facility consists of three components: a committed initial term loan of $350 million; a committed delayed draw term loan of up to $50 million; and an uncommitted delayed draw term loan of up to $150 million. At closing on January 23, 2026, BioCryst drew approximately $396.6 million net of expenses, financing the cash portion of the acquisition through a combination of the Blackstone draw and cash on hand.

As reflected in the Q1 2026 balance sheet, BioCryst now carries a $395.2 million secured term loan against a royalty financing obligation of $447.5 million and total cash, cash equivalents, restricted cash and investments of $260.8 million as of March 31, 2026 ($330.8 million pro forma for the May 4 Neopharmed Gentili upfront payment).

The Blackstone facility's structural significance is that it replaces (and substantially increases) the term debt position that BioCryst had only recently retired via the European ORLADEYO sale.

The interest expense profile is meaningfully higher than the Pharmakon facility was: BioCryst recorded $19.8 million in Q1 2026 interest expense, against $23.5 million in Q1 2025 (Pharmakon-period). The Blackstone-managed facility was specifically structured around BioCryst's commercial-stage cash flow profile and the strategic integration of navenibart into the HAE franchise.

Astria's pre-close Kaken transaction

Critically for the navenibart royalty genealogy, Astria entered into the Kaken Pharmaceutical license for Japan on August 6, 2025, before the BioCryst acquisition was announced, with terms of $16 million upfront, up to $16 million in commercialisation and sales milestones, partial Phase 3 cost reimbursement, and tiered royalties from the mid-teens to 30%.

The Royalty Term in the Kaken agreement runs until the latest of expiration of the last-to-expire patent right, expiration of the last-to-expire regulatory exclusivity, or 10 years following first commercial sale in Japan. Kaken also took on responsibility for ALPHA-ORBIT Phase 3 trial support in Japan and Japanese regulatory submissions.

The Kaken deal accomplished two specific objectives for Astria pre-acquisition: it monetised the Japanese territorial rights at a sensible upfront, and it established the precedent that has now been reproduced by BioCryst in Europe. The 30% top-tier royalty band was set first by Astria/Kaken; reproduced eight months later by BioCryst/Neopharmed Gentili. By the time BioCryst closed the Astria acquisition in January 2026, the Japanese license obligation transferred with the asset and is now an ex-US royalty stream in the BioCryst ledger.

The May 4 Neopharmed Gentili European Navenibart License

The May 4, 2026 transaction grants an Irish affiliate of Neopharmed Gentili exclusive rights to commercialize navenibart for HAE prophylaxis in Europe.

The deal terms are: $70 million upfront, up to $275 million in regulatory and sales milestones, and tiered royalties on European net sales ranging from 18% to 30%. BioCryst retains all US commercial rights and full pipeline optionality for navenibart, including the ability to advance the molecule into adjacent indications.

Why 18% to 30% sits at the top of 2026 European HAE licensing

Several structural features of the deal underwrite the unusually high royalty band relative to historical European HAE licensing comparables.

Pre-2025 comparators sat materially lower. European rare disease licensing in HAE prior to 2025 typically priced top-tier royalties between 8% and 15%, reflecting smaller territorial markets, lower per-patient pricing in European single-payer systems relative to US gross-to-net economics, and a shallower distribution of comparable transactions.

The 18% to 30% band therefore sits at an immediate two-times-plus premium to the prior modal range, even before considering the absolute upfront and milestone components.

BioCryst retains all US commercial economics on navenibart. The US is by orders of magnitude the more economically valuable navenibart territory at peak. By forgoing direct EU launch economics in exchange for partnered royalty participation, BioCryst is compensated for what it is structurally giving up.

The 18% to 30% band, applied against partnered net sales, recovers a meaningful proportion of the risk-adjusted EU economic value that direct commercialization would have produced, while transferring operational responsibility for the European launch to a partner with relevant local infrastructure.

Neopharmed Gentili already operates the European HAE commercial infrastructure originally built by BioCryst for ORLADEYO. The October 2025 sale included the transfer of the European commercial organisation. Neopharmed Gentili therefore inherits a fully operational HAE-focused sales and medical affairs infrastructure across the EU5 and key CEE markets, and the incremental commercial cost of layering navenibart over that infrastructure is materially lower than building it de novo.

From Neopharmed Gentili's perspective, the marginal economics of navenibart are unusually favourable, which is what justifies the higher partner-side royalty obligation it has accepted.

HAE is a concentrated, high-price-per-patient rare disease. The European HAE prophylactic patient population is small (the global HAE prevalence is approximately one in 50,000 people, with prophylactic eligibility of roughly three-quarters of diagnosed patients per Ionis disease background materials), but per-patient pricing on existing prophylactic biologics is high in absolute terms.

A 30% top-tier royalty against single-product net sales in a rare disease category with this pricing profile is digestible at the partner's gross margin level in a way it would not be in a larger, lower-priced indication.

Two independent licensors at 30% is a market reference point. As discussed above, the Astria/Kaken Japan license and the BioCryst/Neopharmed Gentili Europe license now both top out at 30% on partnered net sales. Two independent transactions at the same top-tier rate, on the same asset, in two non-overlapping territories, is the canonical pattern by which a market reference point gets established.

The 30% top-tier royalty is now the navenibart partnered-territory ceiling, and any prospective future ex-US partner (whether for a region not yet covered or for a future indication expansion) will negotiate against that anchor.

Cost recovery dynamics on the Astria acquisition

The $70 million Neopharmed Gentili upfront is approximately 10% of the original Astria cash consideration ($396.6 million net drawn from the Blackstone facility) recovered in eight months, and 18% if measured against the cash component of the deal.

Combined with the $250 million Neopharmed Gentili upfront from October 2025, BioCryst has now realised $320 million of non-dilutive Neopharmed-Gentili-derived European cash inflows in eight months. This is before any Kaken-derived Japanese cash or the future milestone and royalty streams from either partner.

On a pro forma basis, including the May 4 Neopharmed Gentili payment, BioCryst's Q1 2026 cash position was $330.8 million, against $395.2 million of secured term loan obligations and $447.5 million of royalty financing obligations on the balance sheet.

The capital structure is meaningfully levered, but commercial-stage ORLADEYO cash generation provides material debt service capacity, and the navenibart European license has improved the near-term liquidity position by approximately 27% relative to the standalone Q1 cash balance.

Navenibart royalty genealogy

| Territory | Date | Counterparty | Upfront | Milestones | Royalty (top tier) | Notes |

|---|---|---|---|---|---|---|

| Japan | 6 Aug 2025 | Kaken Pharmaceutical | $16M | up to $16M | mid-teens to 30% | Astria pre-close, transferred to BioCryst in Jan 2026; partial Phase 3 cost reimbursement |

| Europe | 4 May 2026 (W19) | Neopharmed Gentili (Irish affiliate) | $70M | up to $275M | 18% to 30% | Builds on Oct 2025 EU ORLADEYO sale to same partner |

| United States | n/a | BioCryst (retained) | n/a | n/a | n/a (direct revenue) | Filing target end 2027 |

| Combined ex-US partnered | $86M | up to $291M | 30% ceiling on both |

The implied global navenibart partnered economics, before any future licenses, sit at $86 million upfront combined plus up to $291 million in milestone payments, against retained US direct revenue. The 30% top tier is now a market reference point.

A note on inverse royalty symmetry

There is a structural inversion in the royalty positions BioCryst occupies across its two HAE assets that is worth highlighting explicitly. On ORLADEYO, BioCryst is the licensor: the company sold downstream royalties to RPI and OMERS in 2020 and 2021 to fund the launch, and now pays royalties to those counterparties at combined rates of 17.0% / 10.5% / 0% across the three tiers.

On navenibart, post-acquisition, BioCryst is the licensee in Japan and Europe: the company collects royalties from Kaken and Neopharmed Gentili at top-tier rates of 30% on partnered ex-US net sales.

The asymmetry between the rates BioCryst pays on ORLADEYO (8.75% to 9.5% on tier 1 to RPI alone, plus 7.5% to OMERS) and the rates BioCryst collects on navenibart (18% to 30% from Neopharmed Gentili in Europe, mid-teens to 30% from Kaken in Japan) is meaningful. It reflects the difference between the 2020 to 2021 royalty financing market, in which a launch-stage commercial sponsor was paying 8% to 10% to monetise its first-product cash flow, and the 2025 to 2026 partnered licensing market, in which a Phase 3 asset commands 30% on partnered net sales.

The repricing reflects both general rare disease licensing market repricing over the five-year window and product-specific factors (the long-acting dosing differentiation of navenibart against the historical HAE prophylactic field).

For BioCryst specifically, the practical implication is that the ex-US navenibart partnered economics are structurally superior, on a per-dollar-of-net-sales basis, to the US ORLADEYO economics under the prior royalty stack.

A simple thought experiment: at $100 million of European navenibart net sales (a plausible ex-US peak revenue scenario), the 30% top-tier royalty would generate $30 million per year of pass-through revenue to BioCryst at zero incremental commercial cost. That same $100 million of net sales, if it were US ORLADEYO revenue under the 2021 royalty stack, would have cost BioCryst between $9.5 million (tier 3 at 0%) and $17.0 million (tier 1) in royalty obligations going the other direction. The post-2026 BioCryst cash flow profile is structurally improving on both sides of the royalty ledger simultaneously.

Pipeline and Clinical Programs

BioCryst's clinical pipeline is now concentrated on three programs across two therapeutic areas, following the Q1 2026 discontinuation of avoralstat (a plasma kallikrein inhibitor for diabetic macular edema) and a deliberate refocus on rare diseases.

Navenibart (lead pipeline asset, post-Astria)

Navenibart is the long-acting plasma kallikrein-targeting monoclonal antibody for HAE prophylaxis. The clinical foundation is the ALPHA-STAR Phase 1b/2 trial, which produced rapid onset of attack reduction and durable efficacy through 17 months of follow-up.

The ALPHA-SOLAR open-label extension reported a 95% mean monthly attack rate reduction in the Q3M dosing arm and 86% in the Q6M arm at June 2025 EAACI presentation, with 92% mean / 97% median overall reduction. Interim ALPHA-SOLAR data presented at AAAAI 2026 reaffirmed the durability of the Q3M and Q6M efficacy profiles, with median attack rate reductions exceeding 95% in both arms.

The pivotal Phase 3 program comprises:

- ALPHA-ORBIT (NCT06842823): a multicentre, randomised, double-blind, placebo-controlled trial in approximately 100 to 145 adolescents and adults with HAE-C1INH Type 1 or Type 2, evaluating navenibart Q3M and Q6M against placebo. BioCryst confirmed in its Q1 2026 update that enrollment is on track to be completed by the end of June 2026.

- ORBIT-EXPANSE: long-term open-label extension trial, initiated October 2025 by Astria pre-acquisition.

ALPHA-ORBIT topline is expected in early 2027, with US BLA submission targeted by end of 2027. Kaken is responsible for Japanese regulatory submissions. Neopharmed Gentili will lead European regulatory and commercial activities post-approval.

ORLADEYO (commercial)

ORLADEYO continues to grow through label expansion, real-world evidence generation, and competitive positioning against the broader HAE prophylaxis category. BioCryst presented nine HAE-related abstracts at AAAAI 2026 (six on ORLADEYO, three on navenibart), including pediatric APeX-P interim data through 48 weeks in children aged 2 to <12 years. The pediatric expansion to ages 2 to <12 was a meaningful 2025 label development that materially expanded the addressable patient population.

BCX17725 (Phase 1, Netherton syndrome)

BCX17725 is a recombinant human LEKTI-derived KLK5 inhibitor (the company's first protein therapeutic to advance to clinical development) designed to treat Netherton syndrome, a rare lifelong genetic disorder caused by SPINK5 mutations resulting in unregulated KLK5 activity, ichthyosis, immune dysregulation, and severe pruritus.

The Phase 1 trial began enrolling in October 2024 and is currently in its Part 4 dosing cohort (up to 12 patients, three months of dosing, with proof-of-concept data expected by end of 2026 per Q1 2026 update). Netherton syndrome has no approved disease-modifying therapy and is a representative ultra-rare orphan opportunity in the BioCryst pipeline.

RAPIVAB (commercial, non-core)

RAPIVAB (peramivir injection, intravenous influenza neuraminidase inhibitor) is a non-core commercial product included in the BioCryst guidance ($10 million to $15 million annual revenue at the midpoint of company guidance). It is not material to the equity story but contributes to total revenue.

The HAE Prophylaxis Competitive Landscape, May 2026

The HAE prophylaxis market in 2026 is structurally crowded relative to the size of the underlying patient population (approximately 7,000 diagnosed US patients, of whom approximately three-quarters are eligible for prophylaxis per Ionis disease background data). The competitive dynamic is shaped not by absolute population size but by the persistence of high per-patient pricing across a category that has produced multiple billion-dollar franchises despite a small denominator.

Approved HAE prophylactic therapies (as of May 2026):

| Product | Sponsor | Mechanism | Dosing | Approval Year |

|---|---|---|---|---|

| Cinryze (C1-INH IV) | Takeda | C1 esterase inhibitor | Twice weekly IV | 2008 |

| Haegarda (C1-INH SC) | CSL Behring | C1 esterase inhibitor | Twice weekly SC | 2017 |

| Takhzyro (lanadelumab) | Takeda | Plasma kallikrein mAb | Every 2 weeks SC | 2018 |

| ORLADEYO (berotralstat) | BioCryst / Neopharmed Gentili (EU) | Plasma kallikrein small molecule | Once daily oral | 2020 |

| Andembry (garadacimab) | CSL Behring | Factor XIIa mAb | Monthly SC | 2025 |

| Dawnzera (donidalorsen) | Ionis (US) / Otsuka (ex-US) | RNA-targeted (prekallikrein) | Q4W or Q8W SC | 2025 |

Key late-stage pipeline candidates:

- Navenibart (BioCryst, ex-Astria; Phase 3 ALPHA-ORBIT, US filing target end-2027; Q3M / Q6M SC) is the longest-acting prophylactic in clinical development.

- Deucrictibant (Pharvaris; Phase 3 ongoing; oral B2 receptor antagonist) is a non-mAb oral approach with development in both prophylaxis and on-demand acute treatment indications, orphan designation in EU and US granted.

- NTLA-2002 (Intellia Therapeutics; Phase 3 HAELO ongoing, dosed first patient January 2025) is a CRISPR-Cas9 in vivo gene editing therapy targeting plasma kallikrein, structured as a one-time IV infusion. NTLA-2002 represents the structural ceiling of long-acting prophylaxis: a single-dose intervention.

- Sebetralstat (KalVista; on-demand acute treatment, Japanese sNDA submitted January 2025) is positioned in the on-demand category rather than prophylaxis but indirectly affects the prophylaxis market by altering the unmet need calculus.

The competitive dynamic for navenibart specifically is that it slots into the most-infrequent-dosing position in the injectable prophylaxis category. Against Takhzyro's blockbuster Q2W dosing, Andembry's monthly dosing, and Dawnzera's Q4W or Q8W RNA-targeted dosing, navenibart's Q3M and Q6M positioning is the most differentiated dosing schedule of any monoclonal antibody approach in the category.

The clinical question is whether the ALPHA-ORBIT readout in 2027 demonstrates attack rate reduction sufficiently durable at the Q6M interval to support both the Q3M and Q6M labels. The W19 ALPHA-SOLAR interim data presented at AAAAI 2026, with median attack rate reductions exceeding 95% in both Q3M and Q6M arms, is supportive but not pivotal.

The competitive ceiling in HAE prophylaxis is now NTLA-2002. If Intellia produces a positive HAELO Phase 3 readout and successfully commercialises a one-time gene-editing prophylaxis, the entire chronic dosing category (Takhzyro, Andembry, Dawnzera, ORLADEYO, navenibart) will face a structural value-capture redefinition. The HAELO completion target is September 2027, which is effectively contemporaneous with navenibart's expected US filing window. Both events are material catalysts for category structure.

Capital Position and Cash Flow Profile

BioCryst's March 31, 2026 balance sheet shows the cumulative effect of the past 18 months of structural transactions:

| Item | $M (Mar 31, 2026) |

|---|---|

| Cash, cash equivalents and investments | 258.97 |

| Restricted cash | 1.79 |

| Receivables | 109.27 |

| Total assets | 465.05 |

| Secured term loan (Blackstone) | (395.20) |

| Royalty financing obligation | (447.50) |

| Accumulated deficit | (2,227.99) |

| Stockholders' deficit | (553.84) |

On a pro forma basis including the $70 million Neopharmed Gentili upfront after quarter-end, total cash, cash equivalents, restricted cash and investments was $330.8 million as of March 31, 2026. The stockholders' deficit reflects the cumulative non-cash IPR&D charge ($697.8 million in Q1 2026 alone for navenibart) and historical accumulated operating losses.

The structural simplification of the BioCryst capital stack is meaningful. Compared to the November 2021 high water mark ($350 million combined RPI + OMERS + the Pharmakon term loan), the company has now: (i) retired the Pharmakon term loan in full via the European ORLADEYO sale; (ii) replaced it with the Blackstone facility, on different terms and against a different underlying collateral and cash flow base; (iii) divested the European ORLADEYO business but preserved the global royalty tier credit; (iv) added navenibart as a second commercial-stage asset (subject to ALPHA-ORBIT readout); (v) established the Kaken Japan license as one component and the Neopharmed Gentili Europe license as the second component of the navenibart partnered royalty book.

For the pre-tax US ORLADEYO cash flow specifically, the structural picture is now meaningfully cleaner than at any point since the November 2021 RPI + OMERS combined $350 million financing. Global ORLADEYO net sales above $550 million attract zero RPI and zero OMERS royalties (subject to the OMERS cumulative cap not yet being fully reached). The 2026 guidance range of $625 million to $645 million implies $75 million to $95 million of incremental net sales falling into the zero-royalty tier.

In a post-2027 navenibart-approval scenario, the same zero-royalty mechanic continues to apply only to ORLADEYO; navenibart in the US will accrue to BioCryst as direct revenue without RPI or OMERS exposure (the navenibart asset was acquired via the Astria transaction post-RPI / OMERS structuring), and ex-US through the partnered royalty streams from Kaken (Japan) and Neopharmed Gentili (Europe).

Read-Through to the 2026 Royalty Dealmaking Environment

BioCryst's recent transaction sequence offers several specific data points relevant to royalty and structured credit underwriters working in the 2026 calendar year.

The 30% top-tier band is now the navenibart partnered-territory ceiling. Two independent licensors (Astria pre-acquisition with Kaken; BioCryst with Neopharmed Gentili) have negotiated identical 30% top-tier royalty rates on the same asset across two non-overlapping territories. The persistence across two independent transactions establishes 30% as a market reference point rather than a one-off outcome.

Any future ex-US navenibart license (whether for an additional region, an additional indication, or a structural restructuring of an existing license) will negotiate against that anchor. The 30% top tier on navenibart is also the second-highest disclosed top-tier band of 2026 dealmaking, after the 14% to 29% band on the Protagonist Therapeutics opt-out from the Takeda rusfertide US collaboration in W18.

European HAE rare disease licensing has repriced upward. Pre-2025 European HAE licensing typically priced top-tier royalties between 8% and 15%. The 18% to 30% band on navenibart Europe represents a material recalibration of comparables, driven by a combination of higher per-patient pricing tolerance in the prophylaxis category, the structural advantage of selling to a partner (Neopharmed Gentili) that already operates the European HAE infrastructure originally built by the licensor, and the broader market repricing of rare disease licensing economics observed across multiple categories in 2025 to 2026.

Any prospective European HAE license negotiated in the next 24 months will reference this band.

The structural inversion of royalty positions across two HAE assets at the same sponsor is unusual. BioCryst paying 8.75% to 9.5% on ORLADEYO US direct sales (to RPI), 7.5% on the same first-tier sales (to OMERS), and collecting 18% to 30% on navenibart European partnered sales, is the textbook example of how the rare disease licensing market has repriced over the past five years.

From a royalty acquirer perspective, the implication is that the marginal royalty acquired on a 2025 to 2026 vintage Phase 3 rare disease asset is being priced at 2x or more the rate that would have applied to a 2020 to 2021 commercial-launch synthetic royalty. The repricing is durable, not transient, and reflects underlying changes in both the supply of rare disease assets seeking partnered capital and the demand from specialty buyers willing to underwrite Phase 3 risk.

Structured credit can now substitute for synthetic royalty in commercial-stage rare disease. The Blackstone $550 million senior secured credit facility is structurally a different instrument from the RPI / OMERS synthetic royalty stack BioCryst built between 2020 and 2021. Blackstone's facility is term debt secured against BioCryst's commercial-stage US ORLADEYO franchise and acquired navenibart asset; RPI / OMERS were synthetic royalties that monetised future ORLADEYO sales without principal repayment.

The fact that BioCryst was able to access $550 million of structured term debt at terms commercially competitive with where it had previously accessed synthetic royalty is a mature-market signal: the structured credit market is now deep enough in commercial-stage rare disease to be a substitute for the synthetic royalty market when the sponsor has cash flow visibility against which to underwrite term debt.

Asset divestiture with global royalty tier preservation is a workable template. The October 2025 European ORLADEYO sale to Neopharmed Gentili is a worked example of a structurally complex transaction in which a sponsor divests a regional commercial business while preserving the global royalty tier credit and the cumulative cap mechanic for upstream royalty obligations.

Both BioCryst's RPI and OMERS royalties continue to apply against global ORLADEYO net sales (BioCryst direct + Neopharmed Gentili European), with the European partner paying its proportionate share at the aggregate global rate and BioCryst paying its proportionate share. The mechanic is increasingly relevant for any commercial-stage sponsor considering a regional divestiture against an existing synthetic royalty obligation, and is worth a separate detailed analysis.

Astria as a model M&A target structure. Astria's pre-acquisition Kaken license established a $16 million upfront, Japanese commercial partner, and a partial Phase 3 cost reimbursement structure that materially improved Astria's standalone cash runway into 2028. From an acquirer perspective, the Kaken license also pre-established the Japanese partnered economics that BioCryst inherited at acquisition close, removing one degree of uncertainty in the post-close ex-US partnership architecture.

The Astria template (originate the asset, take it through Phase 1b/2 and into Phase 3, license one ex-US territory pre-acquisition, get acquired with the partnership intact) is increasingly common for rare disease assets at the late preclinical to mid-clinical stage and is a worked example for sponsors and acquirers alike.

Red Team vs Blue Team Analysis

Risk Analysis (Red Team)

Single-product commercial concentration with US revenue dependency. Approximately 90% of BioCryst's commercial revenue post-European divestiture comes from a single product (ORLADEYO) in a single country (the United States). The HAE prophylaxis category is now structurally more competitive than it has been since ORLADEYO's 2020 launch, with three new entrants approved since 2024 (Dawnzera, Andembry, plus expanded Takhzyro pediatric labels) and additional pipeline competition from deucrictibant and NTLA-2002.

Patient and prescriber switching dynamics across the category will be the primary determinant of whether ORLADEYO continues its trajectory of 30%-plus growth or normalises into a slower-growth maturity profile.

Navenibart Phase 3 readout is the binary catalyst. ALPHA-ORBIT topline data in early 2027 is the binary clinical event that determines the entire economic case for the Astria acquisition. A positive readout supports a 2027 BLA submission, a subsequent navenibart launch into the long-acting end of the prophylactic spectrum, and the realisation of the partnered Kaken and Neopharmed Gentili royalty streams.

A negative or ambiguous readout would substantially impair the $700 million enterprise value of the Astria transaction, with limited optionality to recover the cost basis through subsequent indication expansion.

Blackstone facility leverage is meaningful. The $395.2 million secured term loan is the largest single liability item on the BioCryst balance sheet, against $260.8 million of cash and investments at quarter end ($330.8 million pro forma for the May 4 Neopharmed Gentili payment). The interest expense burden is approximately $19.8 million per quarter (Q1 2026 reported) against US ORLADEYO net revenue of approximately $145 million.

Debt service is comfortable at current revenue levels but reduces flexibility for additional pipeline investment, particularly if ORLADEYO growth normalises faster than guidance implies. The facility's covenants, while not publicly disclosed in detail, may further constrain operational flexibility.

Royalty stack preservation against incremental sales above $550 million is positive but the OMERS cap is not yet reached. Although both RPI and OMERS royalty rates fall to zero on global ORLADEYO net sales above $550 million, the OMERS cumulative cap of 1.425x of $150 million ($213.75 million total) has not yet been fully reached. As long as the cap remains unsatisfied, OMERS continues to receive royalties on the first $550 million tier.

The structural implication is that the BioCryst royalty cost base will not fully decline to zero until the OMERS cumulative payment reaches the cap. In the interim, ORLADEYO marginal economics improve incrementally with each additional dollar of net sales above $550 million, but not in a single discrete jump.

NTLA-2002 represents a category structural threat. Intellia's CRISPR-based HAELO Phase 3 trial, with completion targeted September 2027, is structurally contemporaneous with the navenibart US filing window.

If NTLA-2002 demonstrates durable single-dose efficacy with acceptable safety, the entire chronic dosing category in HAE prophylaxis faces a structural value-capture redefinition. Both ORLADEYO and navenibart would face commercial pressure from a one-time intervention, although the regulatory and reimbursement complexity of in vivo gene editing would likely produce a multi-year commercial uptake curve.

European pass-through royalty mechanics introduce counterparty risk. BioCryst's continued exposure to European ORLADEYO net sales runs through Neopharmed Gentili's commercial execution, with BioCryst no longer directly controlling the EU sales force, market access function, or pricing strategy.

While Neopharmed Gentili inherited the BioCryst-built infrastructure, the long-term commercial outcome depends on the partner's continued strategic prioritisation of ORLADEYO, the integration of navenibart on top of it, and the absence of strategic disruption (M&A, restructuring, or strategic refocus) at Neopharmed Gentili itself.

Astria asset acquisition accounting reduces near-term visibility. The $697.8 million IPR&D special charge in Q1 2026 produces a stockholders' deficit of $553.8 million that will not unwind without future earnings generation. From an external observer perspective, GAAP financial visibility into ongoing core operations is substantially obscured by acquisition-related items, and the non-GAAP reconciliation framework requires careful adjustment to extract underlying franchise economics.

Opportunities and Mitigants (Blue Team)

ORLADEYO is in zero-royalty territory on incremental global net sales above $550 million. Beginning in 2025, every incremental dollar of global ORLADEYO net sales above $550 million accrued at zero royalty cost to BioCryst from the RPI structure and zero from the OMERS structure (subject to the OMERS cap mechanism).

On 2026 guidance of $625 million to $645 million, $75 million to $95 million of net sales fall into the zero-royalty tier, materially improving incremental gross margin economics relative to the 2021 to 2024 royalty-encumbered base case.

The blended royalty cost rate has compressed from approximately 17.0% on the original $0 to $350M tier-1 dollars to approximately 12.7% blended on 2026 guidance, with continued compression as net sales grow.

The European divestiture cleaned up a substantial liability. The October 2025 sale of European ORLADEYO retired the $249 million Pharmakon term loan, eliminated approximately $70 million of future interest payments, and produced approximately $50 million of annual operating expense savings. The structural simplification preceded and enabled the Astria transaction, and the resulting cash flow profile is materially cleaner than the 2024 base case.

Navenibart positioning is the longest-acting injectable HAE prophylactic in development. Q3M and Q6M dosing represents two to four annual injections, the most infrequent SC schedule of any monoclonal antibody approach in the HAE category. ALPHA-SOLAR open-label data through the AAAAI 2026 readout supports both the Q3M and Q6M dosing schedules with median attack rate reductions exceeding 95%.

If ALPHA-ORBIT confirms that profile in a randomised, placebo-controlled design, navenibart becomes the structural long-acting end of the injectable prophylaxis spectrum, occupying a differentiated position relative to Takhzyro, Andembry, and Dawnzera.

Combined HAE franchise covers two delivery profiles. ORLADEYO (oral, daily) and navenibart (injectable, two to four times annually) are structurally complementary delivery profiles within HAE prophylaxis.

A patient considering a switch from a Q2W or Q4W injectable for a more convenient or tolerable option can choose either an oral once-daily regimen (ORLADEYO) or an extremely infrequent injectable regimen (navenibart).

BioCryst's commercial infrastructure post-launch will be able to position both products without internal channel conflict, since the patient-experience positioning is differentiated.

Partnered ex-US royalty streams are the structural inverse of the upstream ORLADEYO royalty stack. Where BioCryst sold downstream royalties on ORLADEYO to RPI and OMERS to fund the launch (8.75% to 9.5% combined RPI + 7.5% OMERS on tier 1), BioCryst is now collecting upstream royalty receipts from Kaken (Japan) and Neopharmed Gentili (Europe) for navenibart at top-tier rates of 30%.

The 18% to 30% European tier is materially above the 8.75% to 9.5% tier that RPI received on ORLADEYO direct sales, and the underlying economics are structurally favourable: a higher per-product royalty rate on ex-US partnered net sales than the per-product royalty cost on US direct sales.

Pediatric ORLADEYO label expansion sustains growth momentum. The 2024 pediatric expansion to ages 2 to <12 added a meaningful incremental patient population without additional R&D investment, and the AAAAI 2026 APeX-P interim data through 48 weeks supports continued real-world evidence generation in this expanded population. The pediatric expansion is one of the principal drivers of the 2025 to 2026 growth profile.

BCX17725 represents pipeline optionality. The Phase 1 program in Netherton syndrome is a low-cost protein therapeutic position in an ultra-rare orphan indication with no approved disease-modifying therapy.

Proof-of-concept data from Part 4 by end of 2026 would support either internal advancement or external partnering, with potential PRV and Orphan Drug optionality on a successful BLA pathway.

Capital structure is now strategically simpler than at any point since 2021. BioCryst has structurally simplified its commercial cash flow profile by retiring the Pharmakon term loan, cleaning up the OMERS cap mechanism through 2025 net sales performance, and pre-establishing partnered royalty streams on navenibart in two non-US territories.

The Blackstone facility, while a meaningful new liability, is structured against a more diversified franchise (ORLADEYO + acquired navenibart) than the 2021 RPI / OMERS structures were.

| Risk Category | Key Concern |

|---|---|

| Single-product concentration | ~90% of revenue from US ORLADEYO; new HAE entrants (Dawnzera, Andembry) competing |

| ALPHA-ORBIT binary | Phase 3 navenibart readout in early 2027 is the cornerstone of the Astria acquisition case |

| Blackstone leverage | $395M secured term loan; ~$19.8M / quarter interest expense; covenants not publicly disclosed |

| OMERS cap not yet reached | Royalty cost continues until cumulative payments reach 1.425x of $150M = $213.75M |

| NTLA-2002 category threat | CRISPR one-time prophylaxis Phase 3 readout contemporaneous with navenibart filing |

| EU pass-through counterparty | BioCryst no longer controls EU sales force; reliant on Neopharmed Gentili execution |

| Stockholders' deficit from IPR&D | $697.8M Q1 2026 charge produces accounting noise; non-GAAP reconciliation required |

| Opportunity | Observation |

|---|---|

| Zero-royalty tier on >$550M | $75M-$95M of 2026 net sales accrue at zero royalty cost; blended rate 12.7% |

| Capital structure simplification | Pharmakon retired; ~$70M future interest saved; $50M annual opex savings |

| Navenibart Q3M / Q6M positioning | Most infrequent SC mAb prophylactic in development |

| Combined HAE franchise | ORLADEYO oral + navenibart Q6M covers full delivery preference range |

| Inverse royalty structure | 18-30% on EU partnered vs 8.75-9.5% upstream on US direct |

| Pediatric label expansion | 2-<12 years population now addressable; APeX-P real-world evidence expanding |

| BCX17725 pipeline optionality | Netherton syndrome proof-of-concept end-2026; PRV / Orphan Drug pathway available |

| Cleaner capital structure | Most strategically simple BioCryst balance sheet since 2021 |

Scenario Analysis

Base case. ORLADEYO delivers 2026 global net revenue at the midpoint of guidance ($625M to $645M, with US direct sales of approximately $580M to $590M and Neopharmed Gentili European net sales producing the remainder). ALPHA-ORBIT enrolment completes by end of June 2026 as guided, with topline readout in early 2027 and US BLA submission by end of 2027. Kaken progresses its Japanese regulatory path on parallel timing with ALPHA-ORBIT topline.

The Neopharmed Gentili European license commences post-EMA approval (likely 2028 to 2029). BCX17725 produces proof-of-concept data in Netherton syndrome by end of 2026, supporting either internal Phase 2 advancement or external partnering.

The Blackstone facility is serviced from ORLADEYO US operating cash flow without material covenant pressure. BioCryst exits 2026 with cash, cash equivalents and investments of approximately $400M to $500M and a meaningfully simpler operational footprint.

Better-than-expected. ALPHA-ORBIT topline in early 2027 produces attack rate reduction at the Q6M interval consistent with the AAAAI 2026 ALPHA-SOLAR interim, supporting both Q3M and Q6M label discussions with FDA, and a navenibart US BLA filing on or ahead of the end-2027 target. ORLADEYO 2026 revenue exceeds the upper end of the guidance range driven by continued pediatric uptake and stable competitive positioning against Dawnzera and Andembry.

NTLA-2002 HAELO produces ambiguous data or experiences development delays, removing the one-time gene-editing structural threat for an additional 18 to 24 months. BCX17725 delivers compelling proof-of-concept in Netherton syndrome, supporting an external partnership at a meaningful upfront.

Combined non-dilutive capital from ex-US navenibart milestones, BCX17725 partnering economics, and accelerating ORLADEYO US cash flow positions BioCryst for an opportunistic share repurchase program or additional accretive M&A on a clean balance sheet.

Worse-than-expected. ALPHA-ORBIT Phase 3 readout in 2027 disappoints, either on Q6M durability (forcing a Q3M-only label) or on safety signals not previously visible in ALPHA-STAR or ALPHA-SOLAR.

The $697.8M IPR&D charge from Q1 2026 produces a sustained accounting overhang without offsetting revenue, and the structural value of the Kaken and Neopharmed Gentili partnered royalty streams diminishes. ORLADEYO 2026 revenue underperforms guidance on accelerating Dawnzera switching dynamics. NTLA-2002 HAELO delivers a positive Phase 3 readout with one-time-injection durability, repricing the entire chronic-dosing HAE prophylaxis category.

BioCryst faces compressed gross margins on incremental sales below the $550M global threshold and limited operational flexibility under Blackstone facility covenants. BCX17725 fails to deliver proof-of-concept in Netherton syndrome and the pipeline narrows to ORLADEYO and the impaired navenibart program.

Conclusion

BioCryst Pharmaceuticals is the textbook example of a single-product commercial biotech that used the synthetic royalty market to fund its launch, then progressively unwound and reconstituted the resulting capital stack as the product matured into a franchise capable of supporting the next round of strategic optionality. The 2020 to 2021 RPI and OMERS transactions financed the ORLADEYO launch and the BCX9930 Factor D inhibitor program (which the company later discontinued).

The October 2025 European ORLADEYO sale retired the Pharmakon term loan and produced $50 million of annual operating expense savings. The January 2026 Astria acquisition added navenibart to the portfolio, financed by a $396.6 million Blackstone facility draw and approximately 37.3 million BioCryst shares.

The May 4, 2026 Neopharmed Gentili European license recovers approximately 18% of the original Astria cash consideration in eight months, completes the navenibart European royalty genealogy alongside the inherited Kaken Japan license, and establishes 30% as the navenibart partnered-territory royalty ceiling.

For readers tracking 2026 royalty dealmaking specifically, the navenibart European license is the second consecutive disclosed transaction at a 30% top-tier royalty (after the Astria/Kaken Japan license signed eight months prior) and the second-highest top-tier band of 2026 dealmaking after the Protagonist/Takeda rusfertide opt-out.

The 18% to 30% band materially repriced European HAE rare disease licensing relative to the pre-2025 modal range of 8% to 15%, and is now a market reference point for any subsequent European HAE license.

The structural mechanic by which Neopharmed Gentili's prior acquisition of the European ORLADEYO commercial infrastructure justified the higher royalty band is also a worked example of how regional commercial infrastructure synergies can drive partnered economics into ranges that would not be available on standalone ex-novo licenses.

Whether navenibart delivers a positive ALPHA-ORBIT readout in early 2027 is the binary clinical question that determines the realised value of the Astria acquisition, and by extension determines the structural cash flow profile of BioCryst over the 2027 to 2030 window. The probability-weighted outcome embedded in the current capital structure, with $395 million of secured term debt, $447 million of royalty financing obligations, and a deferred-revenue royalty stack on the upstream cost side, is meaningfully levered to that outcome.

Investors and underwriters considering BioCryst's capital stack in any structured-credit, royalty acquisition, or strategic transaction context have to underwrite both the mature ORLADEYO franchise (which is structurally simpler than it has ever been) and the Phase 3 navenibart asset (which is binary on its 2027 readout).

For BioCryst itself, the structural picture is that the company is now approaching a meaningfully cleaner revenue-and-royalty profile than at any point since the November 2021 financing. The OMERS cap will be reached at some point in the next four to five years on current trajectory; the Blackstone facility is structured against a more diversified franchise than any prior debt position; and the partnered ex-US navenibart royalty streams represent a structural inverse of the upstream royalty stack that built the company's launch.

Whether the next chapter is the realisation of the navenibart commercial opportunity at scale, an opportunistic M&A target acquisition by a larger rare disease consolidator, or a continued independent execution of a two-product HAE franchise plus expanding orphan pipeline (BCX17725 and any future indication expansion) is a function that the next 18 to 24 months of clinical and commercial data will determine.

The financing infrastructure to carry BioCryst through to that determination is now in place. The next phase is execution.

All information in this article was accurate as of May 2026 and is derived from publicly available sources including company press releases, SEC filings, investor relations materials, and financial news reporting.

Specific terms of the Blackstone $550M senior secured credit facility (rate, covenants, prepayment terms), the Royalty Pharma sublicense revenue tiers, the Astria/Kaken license royalty schedule, the OMERS Regime A / Regime B 2023 sales threshold, and the Neopharmed Gentili royalty tier breakpoints are not fully publicly disclosed. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.