Biotech SPACs and the Royalty Question: Where Blank-Check Capital Meets Drug-Royalty Financing in 2026

Two markets are running hot at the same time and rarely touch. The SPAC market has revived, with 138 vehicles raising about 25.8 billion dollars in 2025 on Renaissance Capital data, nearly triple the 8.7 billion of 2024, and biotech sponsors are back in the funnel. The pharmaceutical-royalty market is at a record, with Royalty Pharma, Ligand, and a widening field of buyers deploying multiples of what they did five years ago.

The natural question, given both, is whether the blank check has any role in royalty financing: as a way to take a royalty aggregator public, to assemble a royalty book, or to monetise a stream.

The empirical answer as of mid-2026 is that the two have stayed apart, and the separation is structural rather than accidental. No SPAC has de-SPAC'd into a pure royalty-aggregation business. The royalty-adjacent blank checks that did exist either abandoned the attempt or liquidated.

The royalty platforms available to public investors reached the market by other routes, and the reasons trace less to fashion than to a specific feature of the Investment Company Act of 1940.

The SPAC Revival, and Where Biotech Sits in It

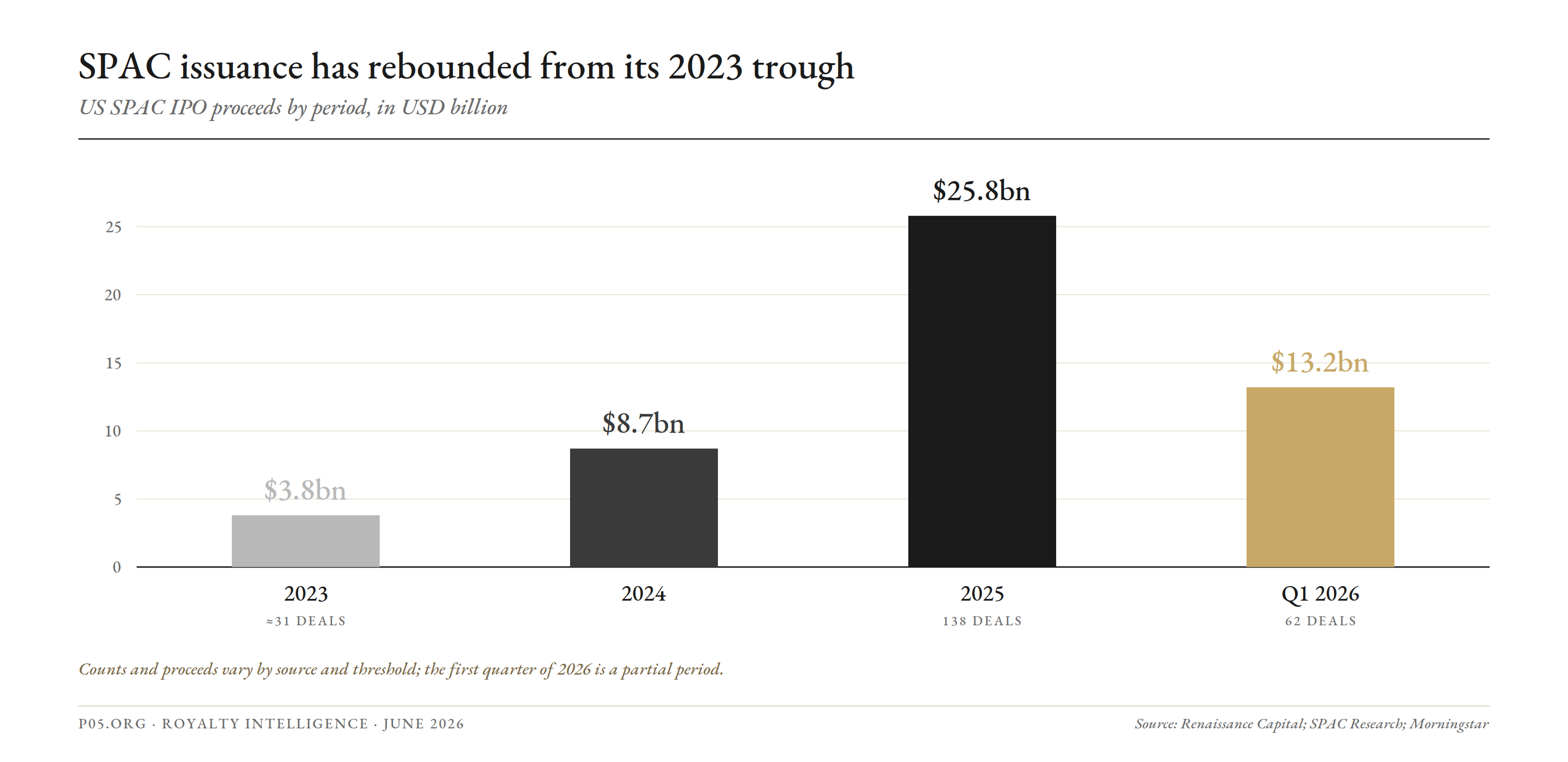

The revival is well documented. After the 2023 trough, new issuance more than doubled from 2024 to 2025, and serial sponsors with prior wins, rather than first-time promoters, have driven the rebound. Estimates vary by source and threshold: Renaissance Capital and FTI put 2025 at roughly 138 SPACs and 25.8 billion dollars, around 40 percent of US IPO count, while SPAC Research figures cited by Morningstar recorded 62 SPACs and 13.2 billion dollars in the first quarter of 2026 alone. The direction is not in dispute even where the counts differ.

Figure 1. US SPAC IPO proceeds by period, 2023 to the first quarter of 2026. Counts and proceeds vary by source and threshold; the first quarter of 2026 is a partial period. Source: Renaissance Capital; SPAC Research; Morningstar.

Biotech sits inside that revival without leading it, and the vehicles are conventional operating-company merger shells. Cormorant Asset Management priced Helix Acquisition Corp III at 150 million dollars in January 2026, trading on Nasdaq under HLXC with a healthcare mandate; its prior vehicles merged with MoonLake Immunotherapeutics and BridgeBio Oncology.

RA Capital followed with Research Alliance III, a 75 million dollar vehicle aimed at a China-based target; its first SPAC merged with Point Biopharma, later bought by Eli Lilly for 1.4 billion dollars, while its second never found a target and liquidated.

Perceptive Advisors took the same conventional route in the other direction, agreeing in December 2025 to merge its Perceptive Capital Solutions vehicle with the cancer-detection company Freenome, backed by roughly 90 million dollars in trust and a circa 240 million dollar PIPE.

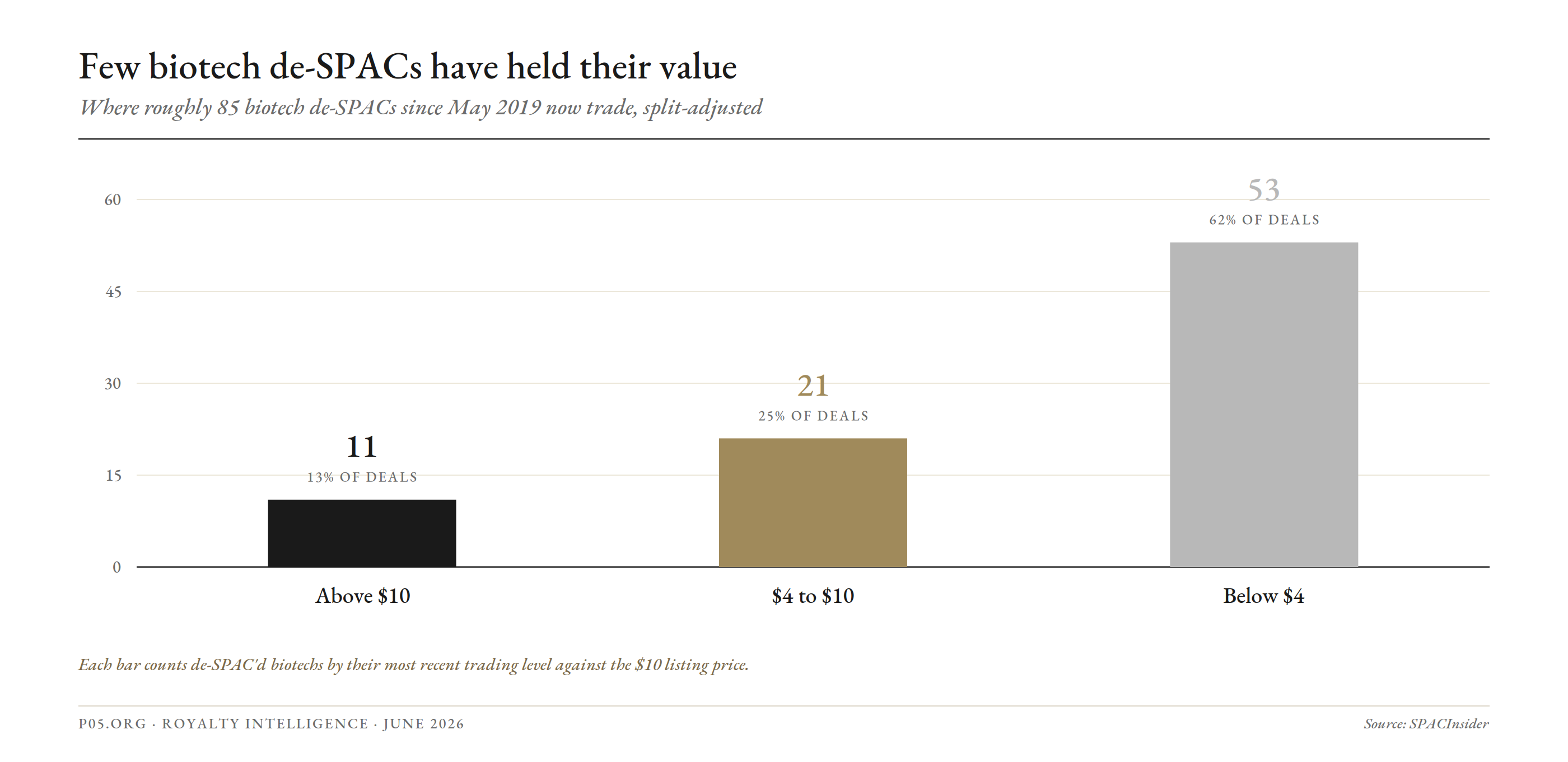

The aggregate de-SPAC record in biotech is the relevant backdrop. On SPACInsider's count, of roughly 85 biotech de-SPACs dating to May 2019, only about eleven traded above their 10 dollar deal price once adjusted for splits, and only about 21 others were last seen above 4 dollars. The durable exceptions tend to be operating platforms rather than artefacts of the structure.

Roivant, which came public through the Montes Archimedes vehicle in 2021, is the most cited, and it functions as an acquire-and-advance holding company that recycles post-listing cash into its own subsidiaries, one of which, Immunovant, had itself de-SPAC'd in 2019. In each case the SPAC functioned as the listing mechanism for an operating company.

Figure 2. Where roughly 85 biotech de-SPACs completed since May 2019 now trade against their 10 dollar listing price, split-adjusted. Source: SPACInsider.

How the SPAC Structure Fits a Royalty Portfolio, and How It Does Not

There is a coherent case for the pairing and a coherent case against, and both are worth stating plainly before the legal constraint narrows them.

The case for is that royalty aggregation is capital-intensive and rewards permanent public capital, and a SPAC offers a pre-funded trust and a faster, price-negotiated path to a listing than a traditional IPO in a still-selective biotech window. A credible specialist sponsor could in principle de-SPAC a royalty company and then raise follow-on equity and debt to deploy.

In a market that says it now prefers targets with real cash flows over pre-revenue stories, a portfolio of contracted royalty streams is, on its face, the kind of fundamentals-first target the disciplined 2025 to 2026 SPAC is meant to favour.

The case against is mechanical. A SPAC consummates a single initial business combination; the trust, the deadline, the sponsor promote, and the warrant overhang are all built around one transaction that converts the shell into one operating company.

Serial acquisition of many royalty positions over time is the royalty business model, and a SPAC can only pursue it after the de-SPAC, as the resulting public company, which means the blank check is the listing of the platform rather than the platform itself.

The trust mechanics point the same way. Proceeds sit at roughly 10 dollars a share in government securities or money-market instruments against shareholder redemption rights exercisable at the combination, and with aggregate redemption rates frequently above 95 percent, a sponsor cannot count on the trust to fund royalty purchases and typically raises a PIPE instead.

The promote and warrants then dilute a vehicle that yield- and NAV-focused investors will price tightly.

Operating royalty aggregators such as Royalty Pharma and Ligand have instead built permanent balance sheets that issue equity and debt repeatedly, the capability serial deployment requires. A further constraint is legal rather than financial.

The Investment Company Act Constraint

Any vehicle whose assets are predominantly royalties has to answer a question unrelated to the science or the discount to net cash, which is whether it is an investment company under the Investment Company Act of 1940.

The answer matters because registered investment company status brings a regime an operating acquirer cannot comfortably inhabit: leverage limits, affiliate-transaction prohibitions, governance and custody rules, and constraints on running an active acquisition business.

The exposure comes from the definition. Under Section 3(a)(1), an issuer is an investment company if it holds itself out as primarily engaged in investing in securities, or if more than 40 percent of its total assets, excluding government securities and cash, consist of investment securities.

A vehicle holding cash pending deployment into royalty interests can approach the second limb, and one whose acquired royalties are characterised as securities can cross it.

A detail in the statute matters specifically here. Section 3(c)(9) carves out persons substantially all of whose business consists of owning or holding oil, gas, or other mineral royalties or leases and fractional interests in them. There is no parallel paragraph for pharmaceutical, drug, or intellectual-property royalties.

A mineral-royalty holder has a dedicated exemption written for it; a drug-royalty holder does not, and has to reach safety through another route, typically Section 3(c)(5)(A), which covers entities primarily engaged in acquiring obligations representing the sales price of merchandise or services, or by arguing that royalty interests are not securities at all.

Figure 3. The Section 3(a)(1) threshold and the divergent treatment of mineral versus pharmaceutical royalties. Source: Investment Company Act of 1940; SEC no-action correspondence, 2010.

The path the largest buyer used is on the public record. When Royalty Pharma set out its position to the SEC staff, it did not invoke a pharmaceutical-royalty exemption, because none exists. In a 2010 no-action letter under Section 3(c)(5)(A), its counsel argued that royalty interests are contractual rights rather than securities, conveying no equity, voting, or dividend rights and not perceived as securities in the marketplace, and that the company does not hold itself out as investing in securities.

The staff granted relief on the 3(c)(5)(A) basis and expressly did not rule on whether royalties are securities or whether the company is an investment company under Section 3(a)(1). The posture is a drafting and conduct discipline sustained over the life of the entity, not a one-time determination.

A SPAC sits awkwardly against that backdrop because, until it combines, it is largely a pool of cash and government securities.

How long it can hold that posture before resembling an investment company became a live question in 2021, when a series of lawsuits, advanced with former SEC Commissioner Robert Jackson and Yale's John Morley, alleged that several large SPACs were unregistered investment companies, and more than sixty law firms responded that a SPAC following a stated plan to combine with an operating company within a defined period is not.

No court reached the merits; the lead case was dismissed with prejudice after the SPAC wound down.

The Rule 3a-2 transient-investment-company safe harbor gives an issuer up to one year to be primarily engaged in a non-investment business, provided it has a bona fide intent to get there as soon as reasonably possible. When the Commission finalised its SPAC rules in 2024, it declined to adopt the proposed bright-line duration safe harbor and left the question to facts and circumstances, noting that a SPAC could be an investment company at any stage depending on its assets, activities, and how it holds itself out.

Covington's guidance to life-science companies read the release as a reminder that any issuer holding large securities or cash balances relative to operating assets can trip the definition.

A blank check is already within the one-year window by virtue of sitting on cash, and a target that is itself a pool of royalty interests would have to clear the 3(a)(1) analysis at the moment of combination, with no established operating history to lean on and with redemption-depleted capital and a promote to absorb. A sequence that establishes the operating-company facts first and treats the listing as a later, separate step inverts the usual blank-check order.

The royalty platforms that reached public markets did so as operating companies or as trusts, and their disclosure reads as aggregators rather than as portfolios.

The Royalty-Adjacent SPACs That Did Not Hold

No pharmaceutical-royalty SPAC has reached the public market, and the royalty-adjacent vehicles that came closest did not hold. Pershing Square Tontine Holdings, a roughly 4 billion dollar vehicle, agreed in June 2021 to buy about 10 percent of Universal Music Group, a music-rights and royalty business, from Vivendi. The structure was a stock purchase rather than a conventional de-SPAC merger, the SEC objected, and the deal was abandoned within weeks; the SPAC later wound down and returned trust cash to holders.

The Music Acquisition Corporation, billed as the first music-specific SPAC, raised 230 million dollars on the NYSE in February 2021 to pursue music rights and never found a target, filing to liquidate in late 2022.

The listed pools that did hold royalties chose a different wrapper, and their experience is instructive for any public royalty vehicle. Hipgnosis Songs Fund and the Round Hill Music Royalty Fund both listed in London as closed-end investment companies rather than SPACs, and both ultimately traded at steep discounts to net asset value and were taken private, Hipgnosis by Blackstone and Round Hill by Concord in a roughly 469 million dollar deal approved in 2023 at a price well above the prevailing quote.

The discount-to-NAV problem that pushed both off the public market is the same risk that would attach to any listed royalty pool, whether it arrived by SPAC or otherwise.

What the Capital Used Instead

The royalty-financing thesis is robustly investable in public markets; the routes simply bypass the blank check. Royalty Pharma, the largest buyer of biopharmaceutical royalties, came public through a conventional IPO in June 2020 and has since monetised and recycled positions at scale, selling the MorphoSys development-funding bonds for 511 million dollars among other transactions.

Ligand presents itself as a biopharma royalty aggregator and in April 2026 agreed to acquire XOMA Royalty for about 739 million dollars in cash plus a litigation-linked contingent value right, a deal that would take its portfolio past 200 assets and is expected to close in the third quarter of 2026.

HealthCare Royalty Partners, which has committed more than 7 billion dollars since 2006 and manages roughly 3 billion, moved under majority KKR ownership in a transaction completed in July 2025.

The closest thing to a listed, liquid pharmaceutical-royalty pool is DRI Healthcare Trust, quoted in Toronto, which has deployed more than 3 billion dollars across seventy-five-plus royalties and held 28 streams on 22 products at the end of the first quarter of 2026 against an intangible royalty book near 753 million dollars.

Its recent history is a case study in the governance pressures the structure invites: the trust internalised its external manager in a transaction completed on 1 July 2025, after the board sought its former chief executive's resignation amid disclosed expense irregularities, and it runs a continuing buyback precisely because the units have often traded below the value of the underlying assets.

| Vehicle | Route to public or institutional market | Structure |

|---|---|---|

| Royalty Pharma | IPO, June 2020 | Operating company, 3(c)(5)(A) posture |

| Ligand | Long-listed operating company | Operating aggregator, acquiring XOMA in 2026 |

| XOMA Royalty | Long-listed operating company | Operating aggregator, pending sale to Ligand |

| HealthCare Royalty Partners | Private, majority sold to KKR in 2025 | Private fund platform |

| DRI Healthcare Trust | Listed on the TSX | Income trust, manager internalised in 2025 |

| Hipgnosis, Round Hill (music) | Listed closed-end funds, later taken private | Investment companies, discount-to-NAV exits |

The Distressed-Biotech Supply, and the Roll-Ups Harvesting It

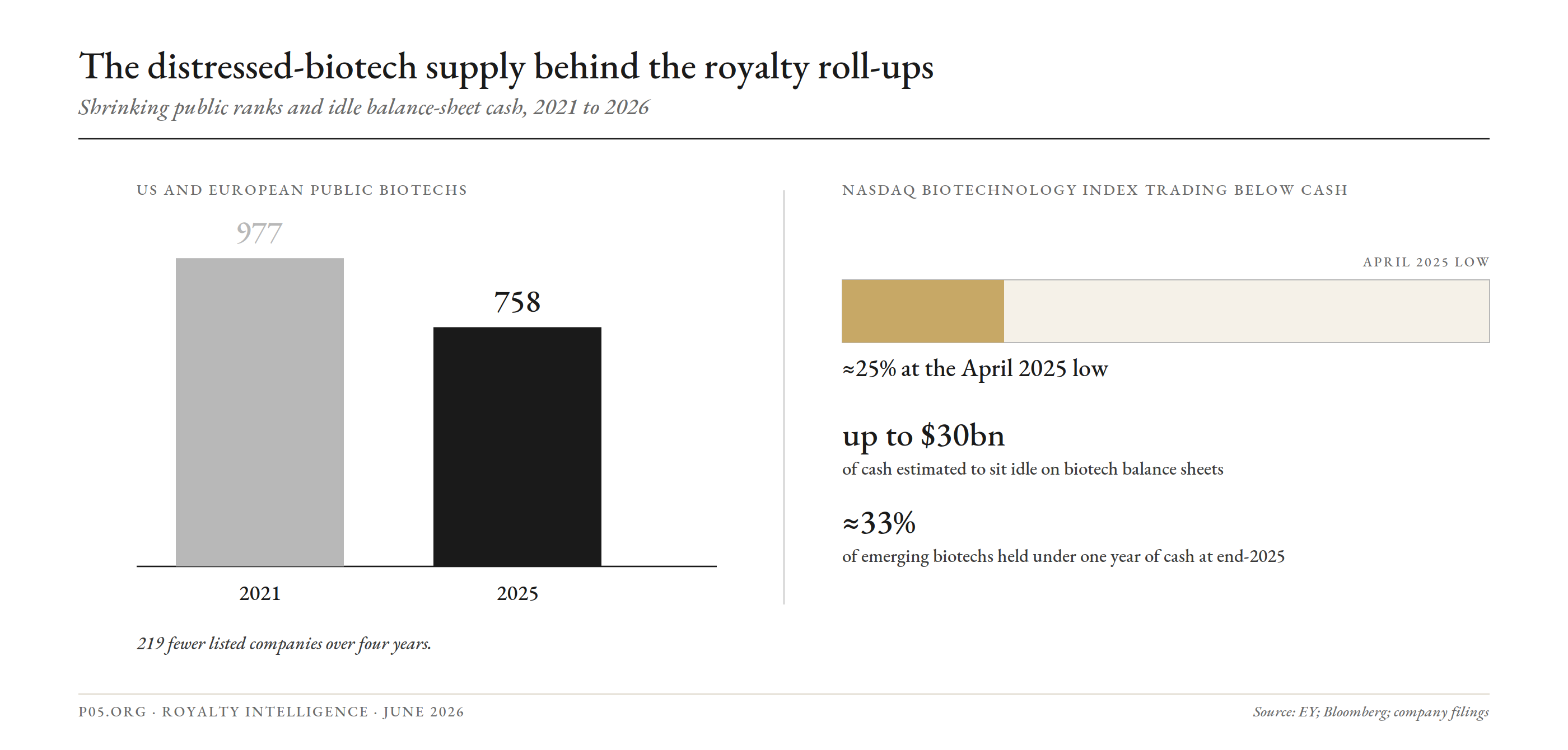

The raw material for royalty and whole-company roll-ups is abundant rather than scarce. At the April 2025 low, roughly a quarter of the Nasdaq Biotechnology Index traded below the cash on its balance sheet, and one fund estimated as much as 30 billion dollars of idle capital sitting on biotech balance sheets.

EY's year-end work found the population of US and European public biotechs falling from 977 in 2021 to 758 in 2025, with a third holding under a year of cash. Activist pressure has made liquidation a respectable board outcome rather than a last resort.

Figure 4. Shrinking public ranks and idle balance-sheet cash, 2021 to 2026.

A cluster of acquirers has turned that distress into a repeatable trade that harvests cash and residual royalty or milestone rights. Tang Capital's Concentra Biosciences ran an active 2025 buying spree across names including Cargo Therapeutics, Elevation Oncology, Kronos Bio, and Allakos, typically at a small premium to a depressed price with a contingent value right capturing most of any later upside.

XOMA Royalty pursued the same logic across Kinnate, Turnstone, Mural Oncology, HilleVax, LAVA Therapeutics, and Generation Bio, in each case keeping the milestone and royalty economics while passing legacy pipeline value back to selling shareholders through CVRs.

Newer entrants such as Alis Biosciences offer the same service with varying splits. The CVR is the connective tissue across the wave: it is how residual royalty and milestone value is monetised without the acquirer paying for optionality it does not want.

Royalty-Backed Notes as a Parallel Channel

Operating biotechs that own a stream rather than seek to buy one have increasingly raised non-dilutive capital through synthetic royalties and royalty-backed notes, usually ring-fenced in a special-purpose entity on a non-recourse basis.

Royalty Pharma's run through 2025 and into 2026 illustrates the breadth: a synthetic royalty and senior secured loan package with Revolution Medicines, an Imdelltra royalty from BeOne, the final Evrysdi royalty from PTC, a Teva arrangement, and a 250 million dollar non-recourse note with Zymeworks repaid from 30 percent of the worldwide tiered royalties on Ziihera, with collection capped at a stated multiple.

These instruments are a financing technique rather than a listed-vehicle phenomenon, but they bear on the SPAC question in two ways.

They give an operating company with a single good royalty a way to raise cash without diluting equity or surrendering the asset, which removes much of the reason such a company would seek a blank-check listing. And their accounting is settled in a way a listed royalty pool's is not: a non-recourse royalty-backed note is debt in form and substance, recorded as a liability and unwound through imputed interest, so the leverage screens read it as borrowing.

Where a Blank Check Could Still Fit

The narrow place the structure could plausibly serve is the inverse of the assembling role: not as the engine that buys royalties, but as the listing event for a royalty company that is already built and already behaves as an operating business. A private aggregator that has spent years establishing the conduct and holding-out that keep it outside Section 3(a)(1) could, in principle, treat a de-SPAC as a faster, price-negotiated alternative to a traditional IPO in a selective window, in the way the structure served Roivant as a door to a platform that already existed.

The sequence is what matters: the operating-company facts have to predate the shell, so the combined entity clears the analysis at listing rather than starting a one-year clock to become something it is not.

A second, quieter use is liquidity rather than financing, giving a private royalty platform's backers an exit without an outright sale.

Both uses run into the same hazard that pushed the listed music trusts and, at times, DRI Healthcare off or below par: the market's tendency to price a visible pool of financial interests at a discount to the value of those interests, rather than at an operating multiple. Whether a vehicle escapes that discount turns less on how it lists than on whether investors read it as an aggregator with a business or as a portfolio with a manager.

In sum, the SPAC revival and the royalty boom are both real and largely non-overlapping, and the gap reflects securities law more than sentiment. The blank check has reopened as a listing route.

Royalty financing is being done through operating aggregators, a listed income trust, private platforms now backed by larger sponsors, whole-company roll-ups that harvest residual royalty rights, and non-recourse notes against single streams. A SPAC could in principle attach to this activity at the listing stage; to date none has.

All information in this article was accurate as of the research date and is derived from publicly available sources including SEC filings, company press releases, rating agency and law firm commentary, regulatory guidance, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, accounting, tax, or financial advice. The author is not a lawyer, accountant, tax adviser, or financial adviser.