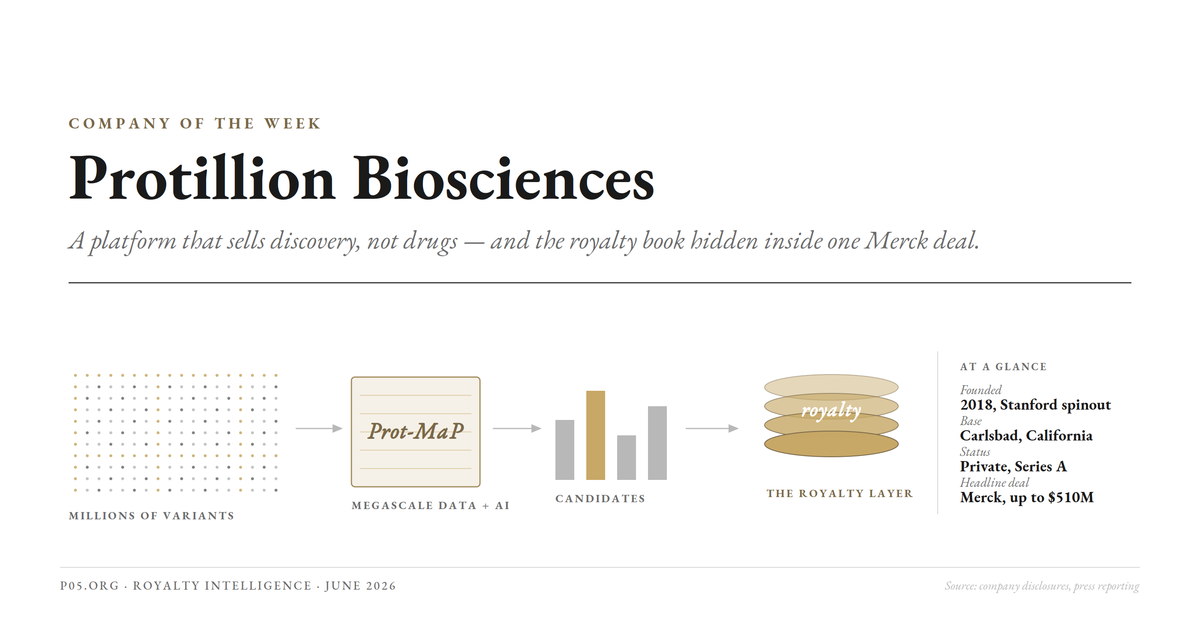

Company of the week: Protillion Biosciences

Protillion Biosciences is a Stanford spinout in Carlsbad that sells a protein-discovery engine rather than a drug. It stayed quiet and lightly funded for years, then in June 2026 signed a multi-target collaboration with Merck worth up to $510 million in milestones.

Protillion Biosciences, Inc. (private) spent its first six years as a deep-technology project: a high-throughput way to measure how millions of engineered proteins bind, built to feed protein-design AI. It raised an $18 million Series A in 2022 and then said very little. On 16 June 2026 it surfaced with a discovery collaboration and license agreement with Merck carrying an undisclosed upfront and up to $510 million in research, development, and commercial milestones.

For a royalty-intelligence reader the interesting question is not the biophysics but the shape of the cash flow. A platform company like Protillion does not own the drugs that its technology helps discover. It holds contingent claims on them: upfront fees, milestone payments, and, by convention, royalties on any product a partner eventually sells.

That is a genuine royalty stack, but it is a peculiar one. It is diversified across programs the company neither owns nor controls, and its terms sit below every disclosure threshold that would normally make them legible.

This piece does three things: it explains, plainly, what a platform royalty is and why a discovery-tools company ends up holding one; it traces Protillion's specific path from a quiet Stanford spinout to a Merck counterparty; and it follows the money, showing exactly what the royalty layer consists of, where it sits, and why almost none of it appears in any public filing.

At a glance

| Item | Detail |

|---|---|

| Company | Protillion Biosciences, Inc. (private), Carlsbad, California |

| Founded | 2018, incorporated to commercialise 2019; Stanford University spinout |

| Core technology | Prot-MaP, a megascale protein-data generation platform for protein-design AI |

| Underlying IP | Stanford-owned foundational patents (US 10,011,830 family), licensed to Protillion |

| Business model | Platform licensing and discovery collaborations, not proprietary drug sales |

| Disclosed funding | ~$18M Series A (Dec 2022, ARCH Venture Partners and Illumina Ventures); earlier ~$2M grant |

| Headline deal | Merck, signed 16 Jun 2026: undisclosed upfront, up to $510M milestones |

| Royalty position | Originator: contingent milestones and royalties on partner programs |

| Surviving question | The royalty rate, upfront, and program count are all undisclosed |

A quiet platform with a loud pedigree

Protillion was founded out of the Stanford laboratory of William Greenleaf, a genetics professor known for high-throughput tools for studying biological systems. The technology was developed by Curtis Layton, who took a PhD in computational biology at Duke and then worked as a postdoctoral fellow in Greenleaf's lab before organising the company to commercialise it. Layton is chief executive and a co-founder.

The third co-founder is David Walt, the single-molecule-detection pioneer who is a scientific founder of both Illumina and Quanterix. That lineage matters, and not only for credibility: Protillion's instrument runs on Illumina sequencing hardware, and Illumina's venture arm is an investor. It matters in one other way too.

The technique was patented by Stanford: the foundational family, headed by US 10,011,830 and naming Greenleaf and Layton, is owned by the university, not the company. A spinout that commercialises university-owned IP does so under a licence, and that Stanford licence sits underneath everything Protillion later earns. The point is developed below.

The funding history is deliberately lean. After an early grant of roughly $2 million, the company raised an $18 million Series A in December 2022 co-led by ARCH Venture Partners and Illumina Ventures. No priced round has been disclosed since. In the interim the company moved its headquarters from Burlingame to a larger facility in Carlsbad, and in March 2026 it hired Bob Hollingsworth as chief scientific officer, a veteran with prior scientific leadership at Pfizer, GSK, and AstraZeneca's MedImmune, most recently chief scientific officer at Shoreline Therapeutics. The Merck deal followed three months later.

A company that raised $18 million and then signed a top-twenty pharma is, in effect, using partnership cash flow rather than venture equity to fund itself.

What Prot-MaP actually does

The platform is called Prot-MaP, marketed as "megascale data plus AI." The mechanic, as the company describes it, is to generate tens of millions of clusters of immobilised proteins directly on an Illumina DNA-sequencing flow cell, using tethered in situ transcription and translation, and then to measure their binding quantitatively.

The claim is that it can characterise on the order of a million antibody variants in a two-day automated run, producing binding data at amino-acid resolution.

The point of all that throughput is not the data itself but what the data trains. Protillion positions Prot-MaP as a "lab-in-the-loop" engine that produces just-in-time training sets for protein-design AI, the idea being that bespoke, large, freshly generated experimental data avoids the overfitting that plagues models trained on sparse or stale datasets.

The marketed outputs are biologics with hard-to-engineer profiles: pH-dependent "sweeping" antibodies, multi-target specificity, tuned affinity with preserved manufacturability. In plain terms, Protillion sells the wet-lab data layer that makes a partner's protein-design AI useful.

| Program element | What Protillion provides | What it does not provide |

|---|---|---|

| Data generation | Megascale binding measurements on sequencing flow cells | Clinical development |

| Design support | Just-in-time training sets for protein-design AI | Ownership of the resulting molecule |

| Output | Optimised candidate biologics with defined profiles | Manufacturing, trials, or commercialisation |

What a platform royalty actually is

Because this is the entire point for a royalty desk, it is worth stating the mechanic precisely before getting to the Merck specifics.

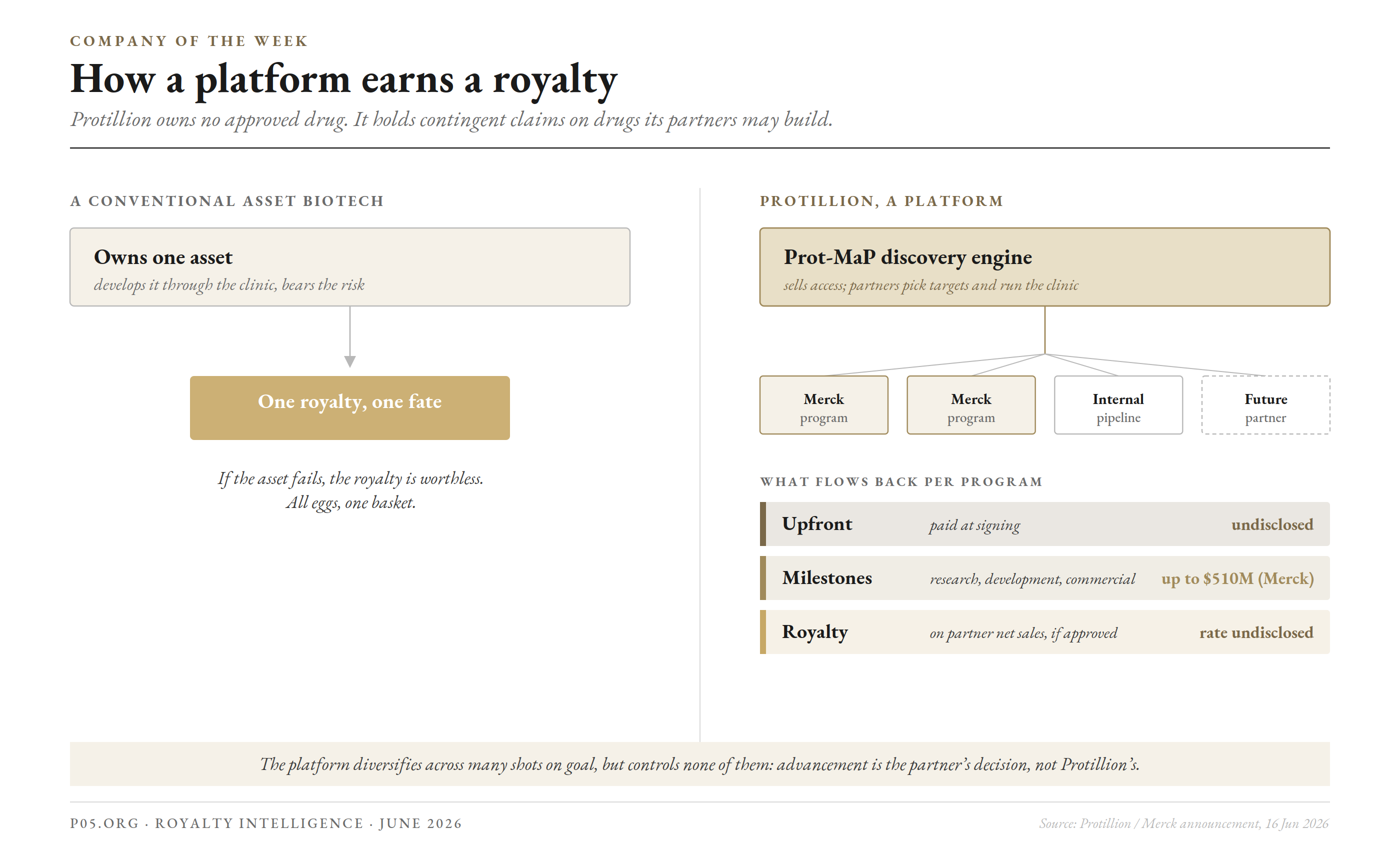

A conventional biotech owns an asset, develops it through the clinic, and bears the risk. If the drug is approved and sold, the owner collects all the economics, and a royalty financier can buy a slice of that single, identifiable stream. The royalty and the asset share one fate.

A platform company owns neither the asset nor the clinical risk. It licenses a capability, and the partner picks the targets, runs the trials, and commercialises the product. In exchange the platform receives a layered, contingent claim: an upfront fee at signing, success-based milestones as programs advance, and, customarily, a royalty on net sales of anything that reaches the market.

The platform's royalty book is therefore a portfolio of small claims on many assets it does not control, rather than one claim on an asset it does.

The structural difference. A conventional biotech holds one royalty on one asset it owns. A platform holds contingent claims across many programs it neither owns nor advances. Source: Protillion and Merck announcement, 16 June 2026.

The trade-off is symmetric. The platform diversifies across many shots on goal, which lowers single-asset risk, but it surrenders control: whether any program advances, and therefore whether any milestone or royalty ever triggers, is the partner's decision.

A royalty on a partnered platform program is a claim on someone else's prioritisation. That is the structural feature that defines the asset class, and it is what makes these streams hard to value and harder still to underwrite.

The Merck deal, decomposed

The 16 June 2026 agreement is a multi-target discovery collaboration and license. Merck, known as MSD outside the United States and Canada, gains access to Prot-MaP to support biologics discovery across multiple undisclosed targets.

Protillion receives an undisclosed upfront payment and is eligible for up to $510 million in research, development, and commercial milestones across multiple therapies. Merck's side was framed by Juan Alvarez, vice president of discovery biologics at Merck Research Laboratories.

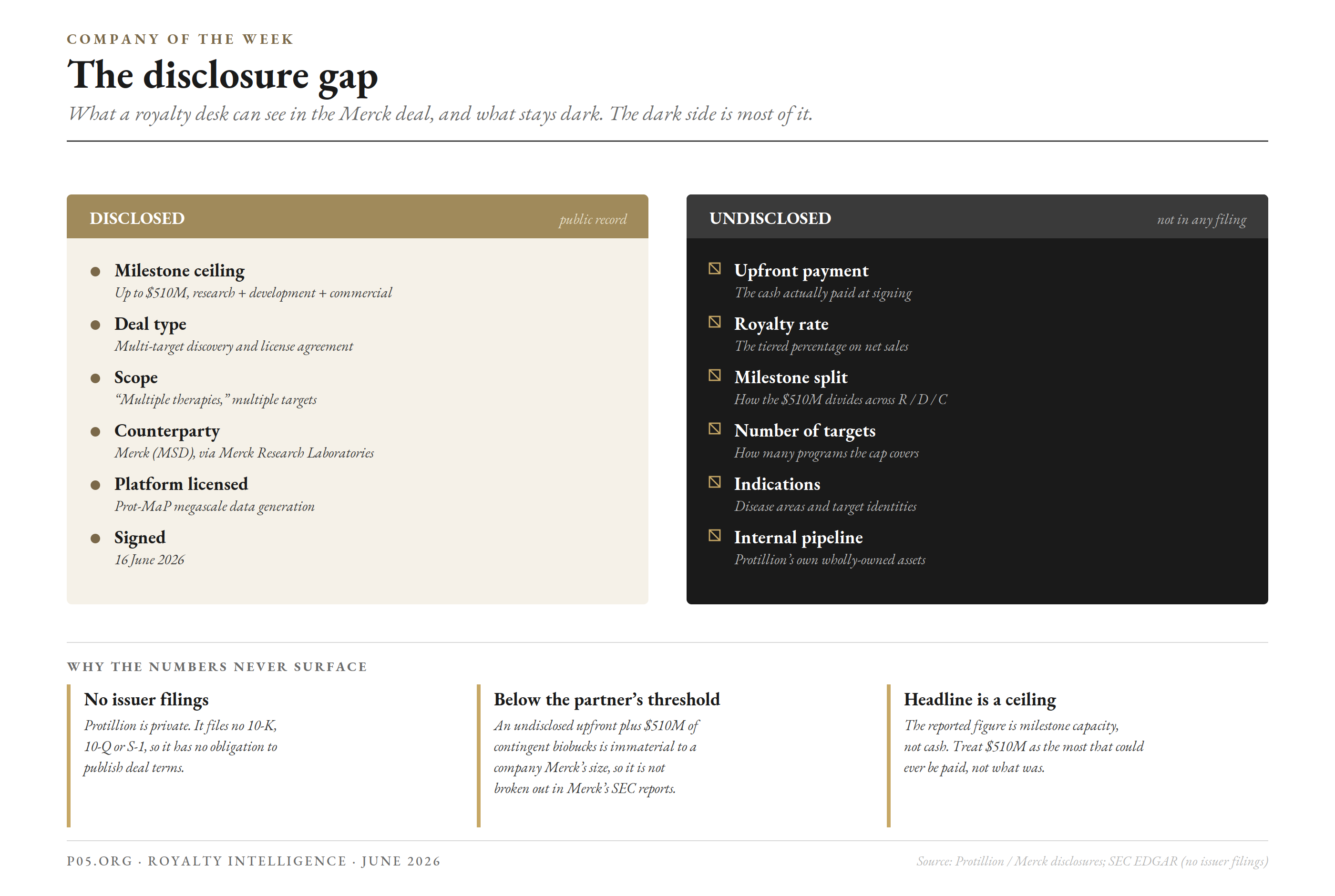

What is disclosed, and what is not, is itself the story. Note in particular what the press release does and does not say:

| Component | Disclosed terms | Comment |

|---|---|---|

| Upfront | Exists; amount undisclosed | For comparable platform deals this is typically single-to-double-digit millions |

| Milestones | Up to $510M, research + development + commercial | A ceiling across all programs, not cash paid |

| Royalty | Not mentioned | License agreements of this type customarily carry net-sales royalties, but neither the rate nor its existence is confirmed publicly |

| Targets / indications | "Multiple," undisclosed | Number of programs the $510M covers is unknown |

| Term and exclusivity | Undisclosed | Not in the public record |

The omission of royalties from the announcement is worth dwelling on. In the same week, Jazz Pharmaceuticals and AbCellera disclosed a comparable platform collaboration that explicitly named "mid-single to low double-digit net-sales royalties" alongside its milestones. Protillion's release names milestones only.

That does not mean there is no royalty; a discovery-and-license agreement almost always carries one. It means the royalty, the single most important number for a royalty desk, was not disclosed.

The other framing point is that $510 million is a ceiling, not a cheque. It is the maximum that could be paid if every target nominated, every program advanced, and every product reached peak sales. Treated as contingent milestone capacity rather than committed cash, the headline shrinks considerably.

The royalty stack: real, diversified, and almost entirely dark

Here is the part that matters, and it is the opposite of last week's Rallybio problem. Rallybio's surviving company owed royalties upstream; the interesting cash flows were the ones leaving. Protillion's cash flows point inward. It is an originator. The difficulty is not direction but visibility.

What a royalty desk can see in the Merck deal against what stays dark. The disclosed column is a milestone ceiling and a deal type. The undisclosed column is every number that would let anyone value the stream. Source: Protillion and Merck disclosures; SEC EDGAR, which holds no issuer filings for Protillion.

The royalty layer, as best it can be assembled from the public record, looks like this:

| Stream | Source | Status | Visibility |

|---|---|---|---|

| Merck milestones | Discovery and license agreement | Contingent on program advancement | Ceiling disclosed ($510M), schedule and split dark |

| Merck royalties | Net sales of any commercialised product | Contingent on approval and sales | Existence implied, rate undisclosed |

| Merck upfront | Paid at signing | Booked | Exists, amount undisclosed |

| Other partner deals | Not disclosed | Unknown | Dark |

| Internal pipeline | Wholly-owned programs | Pre-clinical, opaque | Dark |

| Stanford deduction | University licence on foundational IP | Senior claim on sublicence income | Dark, terms not public |

So the entire inbound stack is: one disclosed milestone ceiling, an implied but unquantified royalty, an undisclosed upfront, an unknown number of other partner arrangements, and a private internal pipeline. Every figure that would let an analyst risk-adjust the stream is missing. This is not unusual for a private platform company; it is the defining condition of the segment.

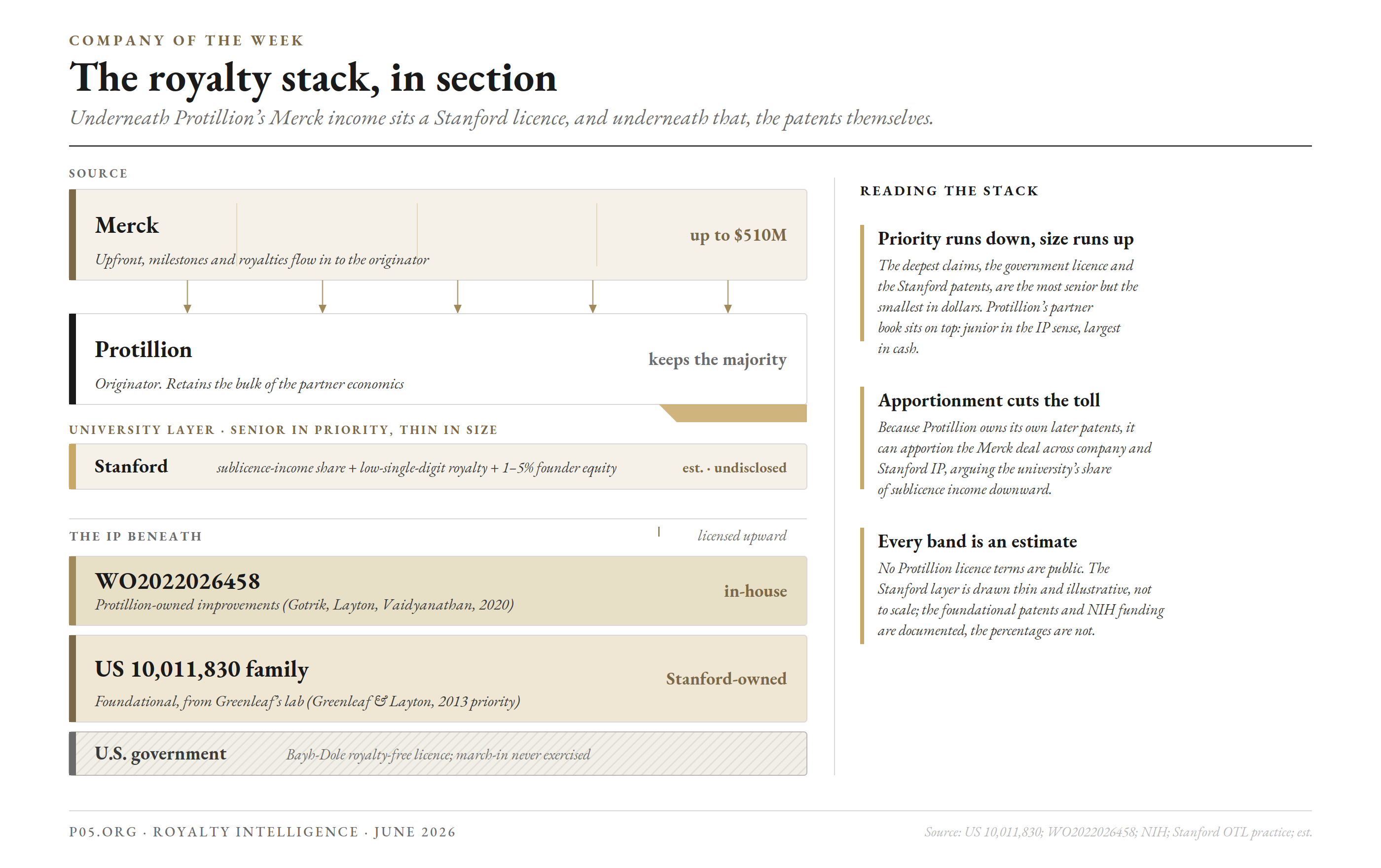

The layer underneath: Stanford's royalty stack

The platform's outbound book is not the bottom of the stack. Prot-MaP descends from a method invented in Greenleaf's Stanford lab and published in Molecular Cell in 2019, where the authors stated plainly that Stanford had filed a patent and that Layton and Greenleaf were named as inventors. That family, headed by US 10,011,830, is owne

d by the Board of Trustees of the Leland Stanford Junior University. Because Stanford licenses its patents rather than assigning them, a Stanford royalty layer sits underneath every dollar Protillion collects from Merck.

The stack runs deeper than the partner book. Above the waterline is Protillion's contingent Merck income. Beneath it sit a thin Stanford royalty layer and a two-tier patent substrate, with a dormant federal licence at the base.

Bands are illustrative, not to scale; the percentages are not public. Source: US 10,011,830; WO2022026458; NIH grant records; Stanford OTL practice.

The IP comes in two tiers, and the second one matters commercially. The foundational layer (US 10,011,830 and its continuations, naming Greenleaf and Layton) belongs to Stanford and is licensed up to Protillion. On top of it sits Protillion's own later family (WO2022026458, naming Gotrik, Layton, and Vaidyanathan, with a 2020 priority), developed in-house and partly with NIH small-business money.

Owning that second tier lets Protillion apportion a partner deal across company and university IP, which is the standard lever for arguing a university's share of sublicence income downward.

What Stanford's cut actually is has never been disclosed, but the architecture is well established. Stanford's Office of Technology Licensing does not assign patents; it licenses them, typically taking founder's equity (commonly one to five per cent, with rights to buy up to ten), a low-single-digit running royalty on net sales, and a share of sublicensing income, alongside an issue fee and annual minimums.

The cleanest read on the running terms comes from a current Stanford licence disclosed by Quanterix, which pays Stanford a low-single-digit royalty on net sales plus a portion of sublicensing income. The nearest structural precedent is closer still: ATAC-seq, another Greenleaf-lab invention, was licensed by Stanford to Epinomics, later acquired by 10x Genomics, under an exclusive equity agreement of exactly this shape.

| Stanford layer component | Typical form | Status for Protillion |

|---|---|---|

| Founder equity | ~1 to 5% of stock; OTL purchase rights up to 10% | Likely held; size undisclosed |

| Running royalty | Low single-digit on net sales | Customary; rate undisclosed |

| Sublicence income share | Portion of partner upfronts and milestones | Would apply to Merck payments; share undisclosed |

| Upfront and maintenance | Issue fee plus annual minimums, creditable against royalties | Customary; amounts undisclosed |

| Exclusivity | Exclusive licence to the foundational patents | Likely, given platform investment; not confirmed |

There is also a Bayh-Dole wrinkle. The Stanford research was federally funded (NIH grant R01-GM111990 is acknowledged in the 2019 paper), and Protillion itself later took roughly $1.96 million in NIH SBIR funding (under GM137655). Federal funding carries reach-through obligations: the government retains a royalty-free licence for its own use, plus march-in rights and a US-manufacturing preference.

Two details are worth flagging. The foundational Stanford patents carry no government-interest statement on their face despite the funded research, a discrepancy rather than a release. And march-in has never once been exercised in the four decades of the Act, so the practical threat to the Merck stream is close to zero. The federal claim is real, senior, and almost always dormant.

So the full stack runs deeper than the disclosure-gap picture alone suggested. Above the waterline is Protillion's contingent partner book. Below it sit a thin Stanford royalty layer, a two-tier patent substrate, and a dormant federal licence. None of the percentages are public, but the order is not in doubt: priority runs downward, dollars run upward, and the university layer is senior in right and small in size.

Where Protillion sits in the deal landscape

The Merck agreement is one entry in a wave of AI-and-data platform collaborations signed across 2026, and the comparable terms help calibrate what $510 million in milestones actually signals. The pattern across these deals is consistent: modest near-term cash, very large contingent ceilings, and royalties that are sometimes named and sometimes hidden.

| Platform | Partner | Upfront | Milestone ceiling | Royalty disclosed |

|---|---|---|---|---|

| Protillion | Merck (Jun 2026) | Undisclosed | Up to $510M | No |

| AbCellera | Jazz (Jun 2026) | $56M + $28M | Up to $792M per program | Yes, mid-single to low double-digit |

| Infinimmune | Merck (2026) | Undisclosed | ~$838M | No |

| Iambic | Takeda (Feb 2026) | Undisclosed | Up to $1.7B | Yes, royalties noted |

| Nabla Bio | Takeda (2025) | Double-digit millions | $1B+ | Not specified |

| Absci | AstraZeneca (2023) | Undisclosed | Up to $247M | Not specified |

| BigHat | AbbVie (2023) | $30M | Up to $325M | Not specified |

Sources: company announcements as compiled in industry coverage of AI-platform dealmaking.

Two observations follow. First, Protillion's $510 million ceiling is mid-pack and entirely credible for a data-generation platform with a single named partner; it is not an outlier in either direction. Second, the disclosure practice is inconsistent across the field, which is precisely why a royalty desk cannot rely on press releases. The economics that matter are negotiated privately and reported selectively.

It is also worth noting how Protillion differs from the better-funded names in the category. Companies such as Xaira and Generate Biomedicines raised hundreds of millions to a billion dollars and, in several cases, retain equity or co-development stakes in the programs their platforms produce.

Protillion took the leaner route: little disclosed venture capital, a data-generation tool licensed to a large partner, and a claim on the partner's downstream success. That makes its royalty position purer in form, a true originator's book, and thinner in disclosed substance.

The SEC reality as of June 2026

A reader expecting to verify the Merck economics in a filing will be disappointed, and the reason is structural rather than evasive.

Protillion is a private company. As of June 2026 it has no registration statement, no annual report, and no periodic reports on EDGAR, which is consistent with a venture-backed private issuer. There is no 10-K to read, no S-1 risk-factor section enumerating the partner agreement, and no MD&A breaking out collaboration revenue. Private financings of this kind are customarily noticed to the SEC on Form D, which discloses an offering's size but nothing about commercial contracts or royalty terms.

The other side of the deal does file with the SEC, but that does not help either. Merck reports tens of billions of dollars in annual revenue. An undisclosed upfront plus up to $510 million of contingent biobucks spread across multiple programs is immaterial to a company of that scale, so it is not individually broken out in Merck's 10-K or 10-Q.

Public companies disclose collaboration agreements when they are material or when a specific accounting or risk-factor trigger applies; a small discovery deal with a private platform clears neither bar.

The result is a clean illustration of the private-royalty-data problem. The deal is real, the milestone ceiling is public, and yet the upfront, the royalty rate, the milestone schedule, the number of targets, and the indications are all outside the disclosure system entirely. Public asset-level royalty data is comparatively easy to obtain. This is the part that is not, and it is exactly the gap that a private-royalty intelligence practice exists to fill.

Red team vs blue team

Risk analysis (red team)

The headline number is a contingent ceiling. Up to $510 million is the maximum payable if multiple programs advance through development and commercialisation. With an undisclosed upfront and no disclosed royalty, the risk-adjusted present value could be a small fraction of the headline, and nothing about the schedule is public.

Control sits with the partner. Protillion does not decide whether any Merck program advances. Milestone and royalty triggers depend entirely on Merck's internal prioritisation across a pipeline that dwarfs this collaboration. A platform royalty is a claim on someone else's roadmap.

No AI-designed biologic has yet reached the market. As of 2026 the category remains unproven at the finish line. Prot-MaP improves discovery-stage data, but the distance from a better binder to an approved, royalty-bearing product is long and littered with attrition that no platform removes.

Single disclosed partner, concentrated exposure. The public royalty book rests on one named relationship. If the Merck programs stall, the disclosed stack is thin, and any other partnerships are invisible and therefore unverifiable.

The economics are undisclosed by design. For an external underwriter, the most important terms cannot be confirmed. The deal is, from a diligence standpoint, a black box with a published upper bound.

A university layer sits underneath. The Stanford licence behind Prot-MaP takes a share of sublicence income and a running royalty before Protillion's economics are clean. The cut is almost certainly modest, but it is senior in right, it is undisclosed, and it reduces the net value of every partner dollar.

Opportunities and mitigants (blue team)

The model is non-dilutive and self-funding. A company that raised roughly $18 million and signed a top-twenty pharma is converting partnership cash flow into runway rather than selling equity. The Merck upfront and near-term research payments fund the platform without a new round.

The royalty book is genuinely diversified. Unlike a single-asset biotech, Protillion's claims spread across multiple Merck targets and, presumably, other undisclosed arrangements. One program failing does not extinguish the stream.

The pedigree de-risks the technology. A founding team spanning Greenleaf's lab and David Walt, hardware built on Illumina sequencing, ARCH and Illumina Ventures backing, and a seasoned CSO in Bob Hollingsworth all point to a credible platform rather than a slideware one.

Platform economics compound. Each partner program generates data and validation that can improve the engine and attract the next deal. The asset is the system, not any single output, and its value can grow with use rather than decay with one clinical readout.

A large partner is a strong validating counterparty. Merck choosing Prot-MaP across multiple targets is a meaningful third-party endorsement of the data layer, and it positions Protillion to sign further collaborations on better terms.

Protillion controls its own improvement IP. Because the company owns later patents stacked on top of the Stanford foundation, it can apportion partner deals across company and university IP and argue the Stanford share of sublicence income downward, limiting the toll the academic layer takes on each Merck dollar.

| Risk | Concern |

|---|---|

| Contingent ceiling | $510M is a maximum, not committed cash; upfront and royalty undisclosed |

| No control | Advancement and triggers are Merck's decision, not Protillion's |

| Unproven category | No AI-designed biologic has reached market as of 2026 |

| Concentration | One disclosed partner; other deals, if any, are invisible |

| Opaque terms | Key economics cannot be verified by an external party |

| University layer | Stanford licence skims sublicence income and a royalty, senior and undisclosed |

| Opportunity | Observation |

|---|---|

| Self-funding | Partnership cash flow substitutes for dilutive equity |

| Diversification | Claims spread across multiple programs and likely partners |

| Pedigree | Greenleaf, Walt, Illumina hardware, ARCH backing, experienced CSO |

| Compounding | Platform value grows with data and use, not a single readout |

| Validation | A top-twenty pharma endorsing the data layer aids future deals |

| Apportionment | Owning later IP lets Protillion argue Stanford's share down |

Conclusion

Protillion is a case study in the platform royalty: a real, diversified, originator's stream that is almost entirely illegible from the outside. The company does not own the drugs its technology helps discover, so its economics are a layered claim on partners' success, an upfront fee, success milestones, and a customary but undisclosed royalty.

The Merck agreement gives that book a credible anchor and a public ceiling of $510 million, while leaving every number that would let anyone value it in the dark. And the stack runs deeper than the partner book alone: underneath it sit a thin Stanford royalty layer and the patents themselves, senior in right and undisclosed in size.

For a royalty desk the lesson is the mirror image of last week's. Rallybio showed what happens to a royalty interest when the company that created it does not survive, and how the surviving entity becomes a net payer. Protillion shows the opposite structure, a company built to originate royalties rather than pay them, and a different obstacle: not direction but disclosure.

The stream exists and may well compound, but the upfront, the rate, the schedule, and the program count sit below every reporting threshold, in a private issuer with no filings and a partner too large to itemise the deal.

The near-term tests are concrete. Whether Merck nominates targets and advances programs, which would begin to convert the $510 million ceiling into actual milestone cash, will be the first signal. Whether Protillion discloses or signs additional partnerships will show whether the royalty book is one relationship or a portfolio.

And whether the broader category produces its first approved, royalty-bearing AI-designed biologic will determine whether platform royalties of this kind are an asset class or an aspiration. Until then, Protillion is best understood not as a drug company but as a royalty originator whose book is real, diversified, and, for now, mostly dark.

All information in this article was accurate as of the research date and is derived from publicly available sources including company press releases, financial news reporting, and SEC resources. Specific terms of the Merck collaboration, including the upfront payment, any royalty rate, the milestone schedule, and the number of programs, are not disclosed in the public record and are described here only as far as public sources allow. The Stanford licence terms, including any equity stake, running royalty, and sublicence-income share, are likewise not public and are described only by reference to Stanford's standard licensing practice and comparable agreements; the patent and grant references are from public records, the percentages are estimates. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.