Co-Promotion Rights in Pharmaceutical Royalty Deals: How They Work, How They Reshape the Stack

Co-promotion rights are the most consistently underestimated provision in pharmaceutical license agreements. They sit innocuously in the term sheet as a one-line option held by the licensor, often free, often "subject to mutually agreed terms." When exercised, they restructure the entire economic profile of the contract: the US royalty stream is extinguished or reduced, a profit-and-loss share takes its place, the licensor commits to fund a share of US commercial spend, and the asset becomes structurally harder to monetize through any of the standard royalty financing channels. Few buy-side models capture this transition correctly.

This piece works through the mechanics of co-promotion rights as they appear in modern pharmaceutical license agreements, the resulting impact on the royalty stack, the recent deals that illustrate the variation in structure, and the legal architecture that royalty financiers and licensors should pay attention to when negotiating or evaluating these positions.

What a co-promotion right actually is

A co-promotion right is a contractual entitlement of one party (typically the originator of an asset, increasingly a clinical-stage biotech) to participate in the marketing, detailing, or commercial promotion of a product within a specified territory, alongside the party that holds the marketing rights. The simplest version is a co-detail arrangement in which the licensor's sales force delivers a fixed percentage of sales calls in the US in exchange for a per-detail fee or a performance bonus, with the underlying royalty contract intact.

The most economically significant version is a full co-promotion or co-commercialization arrangement in which the US royalty stream is replaced by a 50/50 profit-and-loss share, the licensor funds 50% of US commercial spend, and the licensee continues to book all sales.

Industry terminology is inconsistent. The same contract may use "co-promotion," "co-commercialization," "co-detail," and "promotion participation" interchangeably.

The Wikipedia summary of co-promotion describes the arrangement as one in which "partners can choose either profit sharing without royalty payments or higher royalties on sales," which captures the binary that is at the heart of the structure: the licensor either takes a higher royalty and stays passive, or accepts a lower royalty (often zero in the co-promo territory) and takes operational economics. The choice has substantial consequences for valuation, financeability, and risk.

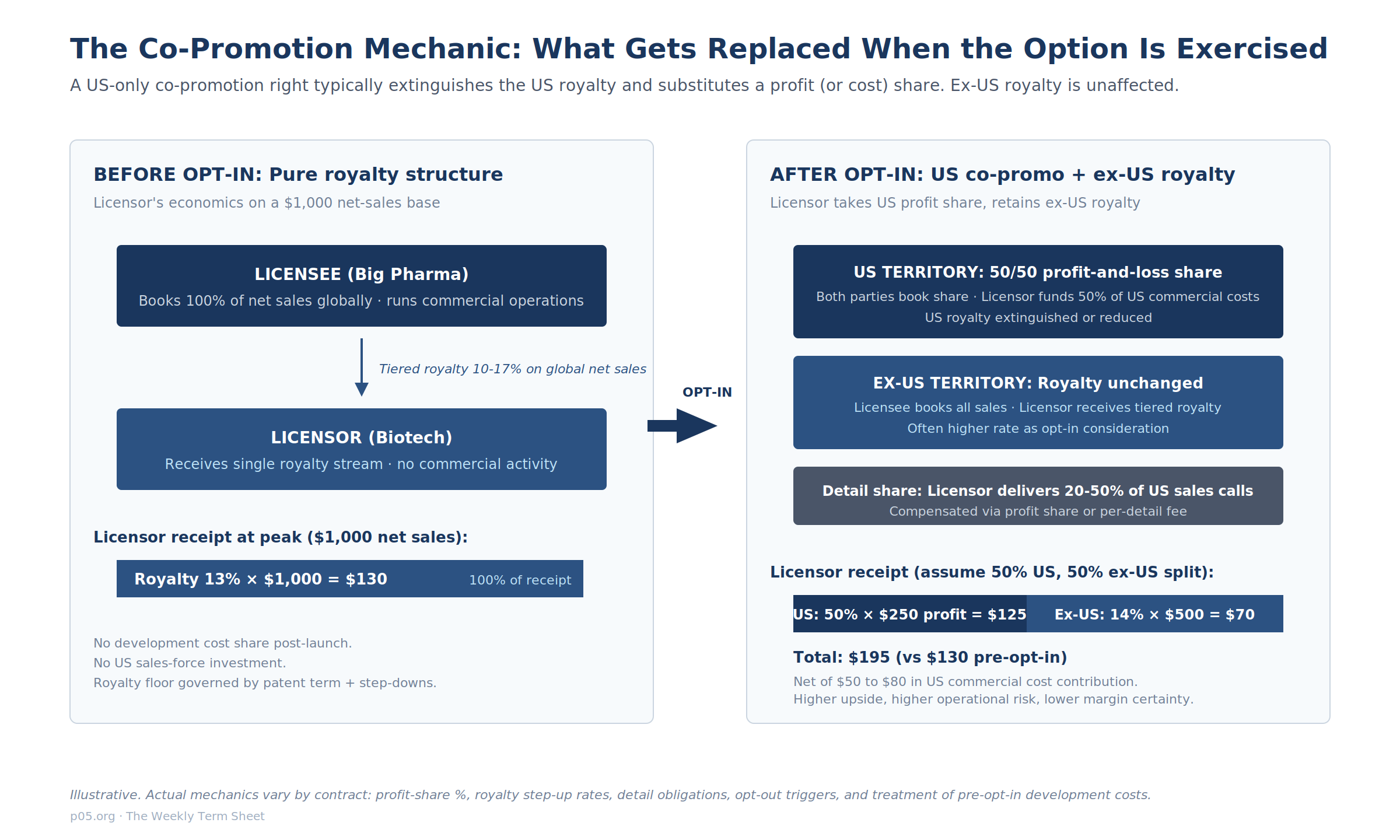

A clean illustration of the binary mechanic comes from the 2005 Memory Pharmaceuticals-Roche PDE4 amendment, filed with the SEC: "If Roche exercises its option, the Registrant will have co-promotion rights in the United States, subject to its fulfillment of certain conditions, including contributing a percentage of Phase III actual global development costs. In such case, Roche shall be relieved of its obligation to pay royalties to the Registrant for sales in the United States for such Option Compound during the co-promotion term."

The structure is now standard. What has changed in 2024 to 2026 is the centrality of co-promotion options to mid-cap biotech licensing strategy and the resulting impact on the population of contracts available for royalty financing.

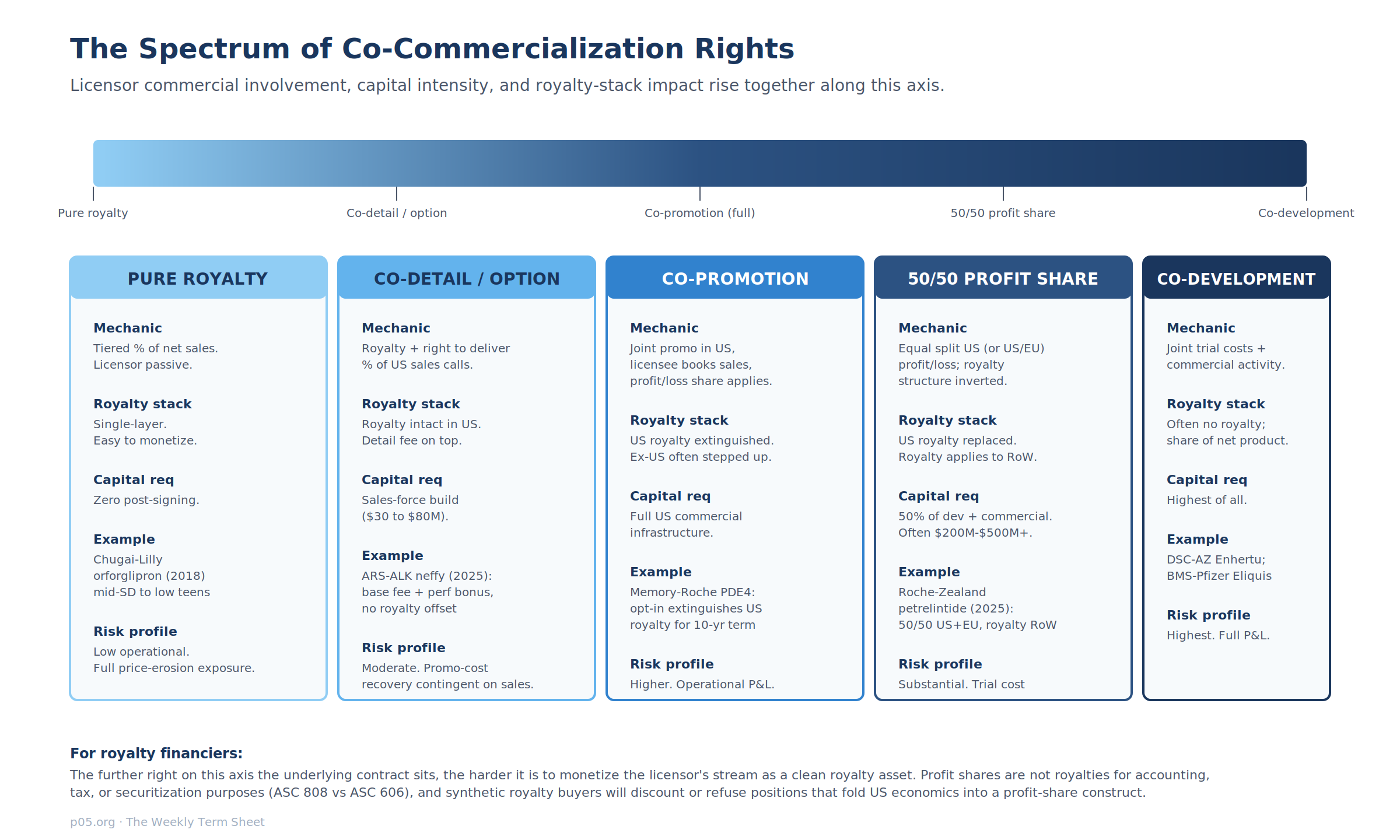

The five-position spectrum of co-commercialization

Pharma alliances exist on a continuum from pure royalty (licensor passive) to full co-development (licensor a 50% operational partner in everything). Co-promotion sits in the middle of this spectrum and the precise position determines whether the contract behaves more like an investment instrument or more like an operating joint venture.

The spectrum collapses into five identifiable structures.

Pure royalty. A discoverer licenses the asset to a commercializer in exchange for a tiered royalty on net sales. The licensor takes no operational role. Examples: Chugai's 2018 orforglipron license to Lilly (mid-single-digit to low-teens royalty, no co-promo right); the Summit-Akeso 2022 ivonescimab agreement (low double-digit royalty to Akeso on Summit territories, no co-promo right). The contract is monetizable as a clean royalty asset and behaves like a traditional financial instrument.

Co-detail / option. The licensor retains the underlying royalty and adds the right to contribute a fraction of US sales-call volume, compensated through a performance bonus or per-detail fee. The royalty is intact. The capital outlay is moderate, in the order of $30M to $80M for a small US sales force.

The ARS Pharma-ALK April 2025 neffy co-promotion agreement sits here: ARS books all US sales, ALK details to up to 9,000 specified pediatricians, and ALK earns a base fee plus a bonus equal to 30% of net sales generated above a market-share threshold. Importantly, the ARS-ALK agreement explicitly states that "the Company granted ALK a non-exclusive, royalty-free license to use the neffy trademarks." The royalty layer is entirely absent from the bilateral economics.

Full co-promotion. The US royalty is extinguished and replaced by a US profit-and-loss share, typically 50/50 but sometimes weighted (20/80, 30/70). The licensor funds its share of commercial costs and a share of any continued development. Ex-US royalty often steps up as compensation.

This is the Memory-Roche PDE4 structure and the Geron-Janssen 2014 imetelstat structure, where opt-in to a 20/80 cost share was paired with an option to deliver 20% of US selling effort in lieu of a 20% promotion-cost contribution.

50/50 profit share. The contract is functionally a joint venture in the licensor's home and partner territories, with a residual royalty stream applying only to rest-of-world. The Roche-Zealand petrelintide collaboration is the cleanest 2025 example: 50/50 profit and loss share in the US and EU, royalty (low double-digit to high-teens) in rest-of-world.

The Takeda-Protagonist rusfertide deal is a US-only variant: 50/50 US profit share, 10% to 17% tiered royalty ex-US, with an embedded opt-out swap that converts the position to a 14% to 29% global royalty if Protagonist withdraws from the profit share.

Co-development. No royalty layer at all. Both parties share trial costs, both share commercial costs, profits are split. The Daiichi Sankyo-AstraZeneca Enhertu collaboration is the best-known modern example. The BMS-Pfizer Eliquis alliance, often described as royalty-driven in its plumbing, is structurally a profit-share with one partner booking sales and royalty-like flows used as the cash mechanism, but it is not a royalty contract in the legal sense.

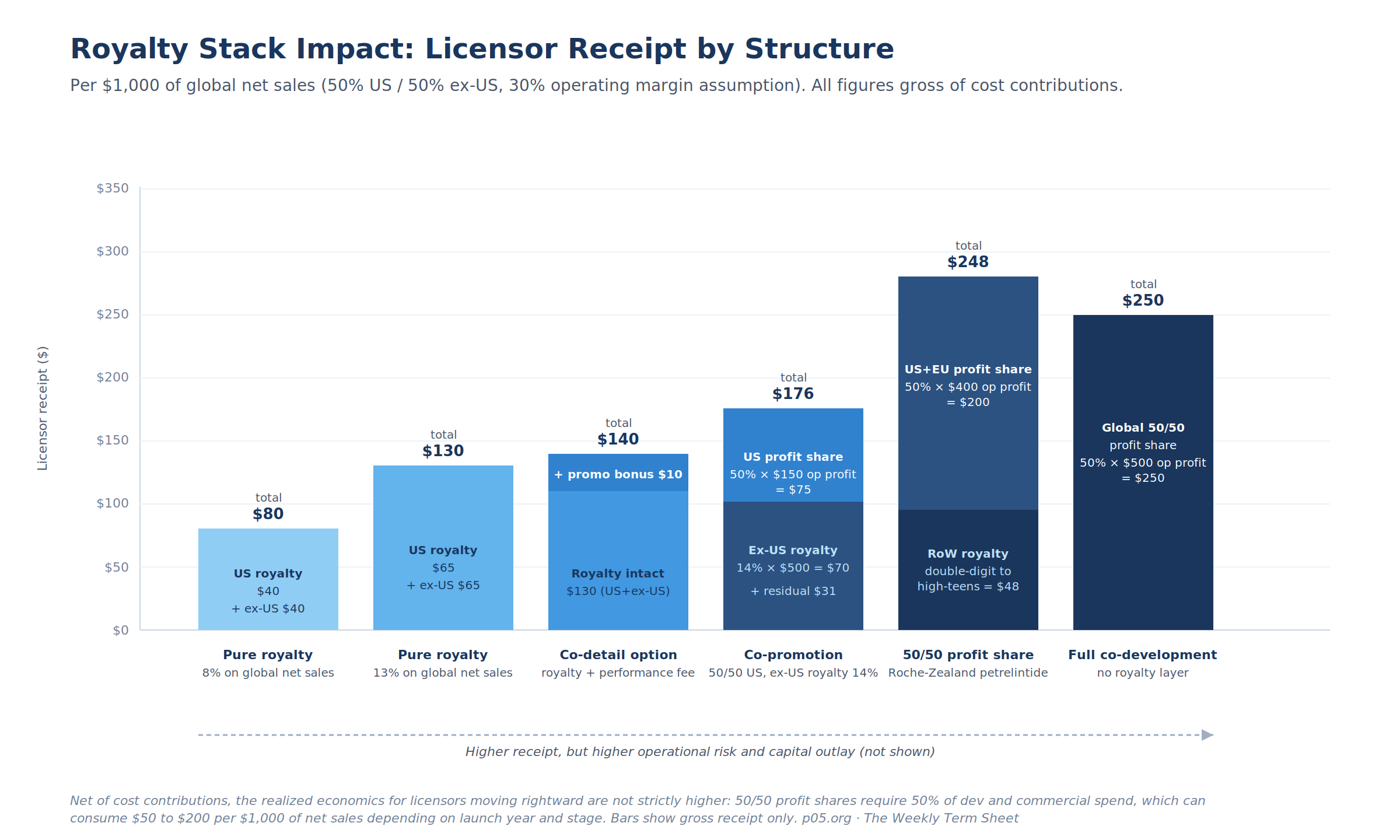

Royalty stack impact: where the cash actually goes

The economic distinction between these positions becomes vivid when traced through a representative net-sales base. Assume $1,000 of global net sales split 50/50 between US and ex-US, a 30% operating margin, and standard tiered rates. Licensor receipt varies by structure as follows.

The mechanical conclusion is that gross receipt rises as the licensor moves rightward along the spectrum, but the receipt comprises increasingly heterogeneous economic components. A pure royalty stream is a clean cash flow over the patent term. A 50/50 profit share is a stream of net operating income subject to currency translation, accounting consolidation, joint steering committee decisions, and the licensor's own commercial cost performance.

The two are not interchangeable for any of the analytical or financing purposes that royalty fund analysts care about.

Three specific second-order effects on the stack are worth noting.

Royalty step-ups as opt-in consideration. Where a co-promotion right exists but is not exercised, ex-US royalty rates frequently include a step-up triggered by non-exercise. The Geron-Janssen 2014 contract provides a useful template: opting into the 20% US profit share triggered "higher tiered royalty rates and higher future milestone payments" globally; not opting in left the rate structure at the lower base level.

In the Takeda-Protagonist rusfertide structure, opting out of the 50/50 US profit share converts the contract to a global royalty in the 14% to 29% range, materially higher than the 10% to 17% ex-US rate that applies under the profit share. The opt-in/opt-out mechanic is therefore embedded in the royalty rate itself, not separately priced.

Stacking and combination products. When a co-promotion product is later sold in combination with another asset (a fixed-dose combination, a co-formulation, or a regimen with a separately reimbursed product), the allocation of net sales for royalty calculation purposes becomes contractually fraught. License agreements signed before 2020 often used pro-rata allocation; agreements signed in 2024 to 2026 increasingly specify explicit allocation rules.

This matters more for co-promotion contracts because the allocation rule applies to whatever residual royalty layer remains (typically ex-US) while the US economics flow through the profit share at the combination-product level.

Patent expiry and royalty step-down. Co-promotion rights often have term provisions that survive patent expiry. The Kura-Kyowa Kirin ziftomenib co-promotion agreement, for example, runs until "the latest of expiration of all valid claims of the Company's patent rights licensed to Kyowa Kirin in the United States, expiration of the last-to-expire regulatory exclusivity in the United States or ten years after first commercial sale in the United States" (SEC 8-K, June 2025).

A pure royalty contract typically steps down post-patent. A co-promotion contract anchored to the latest of three end-dates can extend the licensor's economics meaningfully past nominal patent expiry.

Recent deal evidence: 2024 to 2026

The 2024 to 2026 deal cohort shows that co-commercialization structures are now the modal outcome for substantial mid-stage and late-stage licensing transactions. Six representative deals capture the variation.

The Roche-Zealand petrelintide deal of March 2025 is the largest co-development structure in the obesity class. Roche paid $1.65 billion upfront with up to $3.6 billion in milestones for a 50/50 profit-and-loss share in the US and EU, plus a tiered royalty (described as "double digit to high teens") in rest-of-world. Zealand contributes to ongoing development costs proportionally.

The deal was signed before the November 2025 Most-Favored-Nation pricing reset for GLP-1 brands and the IRA Maximum Fair Price publication, but it was structured with explicit awareness that pricing in the US obesity class was likely to compress; the 50/50 economics insulate Zealand from the rate-on-net-sales compression that pure royalty holders face. There is no clean royalty stream on US/EU petrelintide for any future financing buyer.

The Takeda-Protagonist rusfertide deal of January 2024 embeds the most flexible recent opt-in/opt-out mechanic. Protagonist takes a 50/50 US profit share with an option to lead the VERIFY Phase 3 program, plus 10% to 17% tiered royalty ex-US. If Protagonist exercises an "Opt-out Right" at any future point, the contract converts to a 14% to 29% global royalty. This bidirectional convertibility is unusual; it allows Protagonist to exit the operational track if commercial scale is unattractive, and it gives the Takeda side a higher royalty as compensation for absorbing the full operating burden.

From a royalty financing perspective, the Protagonist position is the most monetizable of the recent profit-share contracts because the convertibility option creates a path to a clean royalty asset.

The ARS Pharma-ALK neffy agreement of April 2025 is the textbook co-detail structure with a wrinkle: the trademark license is royalty-free, the underlying intercompany economics include a base fee plus a bonus equal to 30% of net sales above an initial market-share threshold (rising to 50% in years three and four), and on early termination by ARS for convenience the post-termination payment converts to a "specified mid-to-low double-digit percentage of the portion of neffy net sales generated from the ALK-targeted prescribers."

The post-termination payment functions as a tail royalty on a defined sub-segment of US sales. The structure illustrates that "co-promotion" can be a lighter-touch arrangement that does not eliminate royalty mechanics, particularly when the licensor has already commercialized the asset and is using the partner only for incremental detailing reach.

The Kura-Kyowa Kirin ziftomenib co-promotion agreement of June 2025 builds on the underlying November 2024 collaboration agreement. The collaboration provides for 50/50 US profit share and ex-US royalties to Kura. The June 2025 amendment formalizes the US co-promotion mechanic: Kyowa Kirin US delivers up to a specified percentage of US details, the parties share US commercial costs equally, and the agreement runs until the latest of patent, regulatory exclusivity, or ten-years-from-first-commercial-sale. The structure is two-stage: an initial collaboration with embedded co-promotion option, and a separate co-promotion document filed at or near launch.

This pattern is increasingly common because it allows the financial economics to be fixed at signing while the operational mechanics are negotiated closer to commercial readiness.

The Pfizer-Metsera transaction of September 2025, which closed in November 2025, is an outright acquisition rather than a license, but the Contingent Value Right structure functions as a royalty-equivalent. Pfizer paid $47.50 per share in cash plus a non-transferable CVR worth up to $22.50 per share contingent on three regulatory milestones (Phase 3 start, monthly monotherapy approval, combination approval).

There is no co-promotion option because there is no licensor anymore; the equivalent economics are bundled into the CVR. The Phase 2b VESPER-3 readout in February 2026 at 10.5% maximum weight loss has already raised the execution risk profile of the CVR. CVRs are royalty surrogates with capped upside, regulatory rather than commercial triggers, and (critically) non-transferability. They are not financeable through any of the standard royalty channels.

The Summit-Akeso ivonescimab agreement is the counter-example. Akeso licensed Summit the rights to develop and commercialize ivonescimab in North America, Europe, Japan, and (after the 2024 expansion) Latin America, the Middle East, and Africa, retaining the rights to China and Asia ex-Japan as a separate territory. Akeso receives a low double-digit royalty on Summit-territory net sales. There is no co-promotion right.

The asset is structurally a clean royalty stream on a global blockbuster-candidate, and Akeso's position is one of the most monetizable mid-cap royalty assets currently in the market for that reason.

The legal architecture: what to look for in the contract

The detail of the co-promotion provisions varies by deal but the same set of clauses recurs. For royalty financiers, licensors evaluating new opportunities, and counsel structuring deals, these are the provisions that determine the shape of the asset.

Trigger for opt-in. Most modern agreements grant the licensor a discretionary right to opt in at a specified clinical or commercial milestone. Common triggers include IND filing, Phase 1 completion, Phase 2 completion, NDA filing, and commercial launch. A 2020 Ropes & Gray survey reported that the most common opt-in points concentrated around IND filing, Phase 1 completion, and regulatory or marketing approval.

The earlier the trigger, the larger the licensor's eventual capital commitment if exercised; the later the trigger, the lower the value of the option because more of the development risk has resolved.

Cost reimbursement on opt-in. A pivotal question is whether the licensor reimburses the licensee for development costs incurred before opt-in. Practice varies. The same Ropes & Gray survey concluded that "in most cases, past development costs were not reimbursed." Where reimbursement is required, it is typically computed as a defined percentage (often 50%) of a specified cost category, plus a premium that compensates the licensee for risk-bearing.

The premium can be substantial; the Memory-Roche template included payment of "actual global development costs for Phase II for such Option Compound, plus a premium" plus milestone uplift on Phase 3 events.

Geographic scope. The vast majority of co-commercialization rights are limited to the US. The Ropes & Gray 2020 study found that out of the surveyed agreements, only "a handful" extended co-commercialization rights to a second territory. The Roche-Zealand petrelintide structure extending to both US and EU is therefore an outlier and reflects Zealand's commercial maturity and capital position rather than a market-wide trend. For analytical purposes, a co-promotion right should be assumed to be US-only unless the contract specifies otherwise.

Duration. Co-promotion terms are typically anchored to the longer of patent, regulatory exclusivity, or a fixed period from first commercial sale (commonly ten years). The Memory-Roche template specified "a period of ten years from the first commercialization."

The Kura-Kyowa Kirin agreement uses the latest of three triggers. Royalty contracts typically step down after the fixed period; co-promotion contracts typically continue at their full economic terms but may include a step-down once the milestone is reached.

Detail share and minimum performance. Co-promotion contracts specify the licensor's share of US sales calls (commonly 20% to 50%), minimum representative qualifications, and minimum detailing requirements. Failure to meet detailing thresholds typically allows the licensee to terminate the co-promotion arrangement and return the parties to a royalty mechanic.

The Kura-Kyowa Kirin agreement requires Kyowa Kirin US to "meet minimum detailing requirements using sales representatives that meet specific qualifications."

Booking of sales and revenue recognition. In nearly all co-promotion contracts, one party books all sales and the other receives its economics through an intercompany transfer (royalty, profit share, or detail fee). This single-booker convention has substantial accounting consequences, discussed below.

Audit and information rights. Royalty contracts grant the licensor audit rights over royalty calculations. Co-promotion contracts grant broader information rights covering commercial spend, detailing volume, and rebate computation. The expansion of audit rights is one of the practical reasons co-promotion contracts are harder to monetize: a financing buyer inherits a more complex set of audit and information obligations.

Change of control. Co-promotion rights are usually expressed as personal to the licensor and are subject to consent or termination on change of control. Royalty rights are typically transferable. The non-transferability of co-promotion rights is the single most important factor in their treatment for financing purposes: a co-promotion option, even when exercised, may not survive the assignment of the underlying contract to a financing vehicle.

Accounting and financing consequences

The ASC 808 / ASC 606 distinction is central to understanding why co-promotion contracts behave differently from royalty contracts in financial statements and in financing transactions.

A pure royalty contract is generally treated as a license of intellectual property under ASC 606, with revenue recognized as the underlying licensee sells the product. The licensor's cash flow is a unilateral payment from the licensee, the contract is bilateral, and the asset is a financial right that can be sold or pledged.

A co-promotion contract, by contrast, typically falls within ASC 808 (Collaborative Arrangements) because each party is an active participant in a joint operating activity and both are exposed to the risks and rewards of commercial success. This has three concrete consequences.

First, the income statement presentation differs. Profit-share receipts are typically recorded as collaboration revenue or as a reduction of operating expenses, not as royalty revenue. The line-item label matters because royalty financiers (and the public market that values royalty pure-plays) discount collaboration revenue more heavily than royalty revenue.

Second, the legal treatment of a synthetic royalty sale on a profit-share contract is more complex. Under Article 9 of the New York UCC, a synthetic royalty sale is treated as a transfer of an account, defined as a right to payment for property sold.

A profit share is a right to payment of the net result of an operating activity, not a right to payment for property; the characterization is less clean. Synthetic royalty transactions on profit-share contracts have been done but typically require additional structural complexity (waterfalls, top-stream allocations, intercreditor arrangements with the underlying licensee).

Third, the underwriting changes. Royalty financiers underwriting a co-promotion contract must underwrite the operational performance of the licensor (its ability to deliver the contracted detailing, fund its share of commercial spend, and avoid covenant breach in any senior debt that may be secured by the same asset), in addition to the underlying drug's commercial performance.

The two risks compound. Royalty financiers will typically discount profit-share streams or refuse them entirely, and synthetic royalty deals on assets governed by profit-share contracts are priced wider than equivalent deals on pure-royalty assets.

A representative example of a synthetic royalty transaction structured around a clean royalty asset is the November 2024 Syndax-Royalty Pharma agreement on Niktimvo, in which Royalty Pharma paid $350 million for a 13.8% royalty on US net sales of Niktimvo, with payments capped at a 2.35x multiple of capital invested.

The structure works because the underlying Syndax-Incyte arrangement on Niktimvo is bilateral and royalty-like in the commercially relevant respect; a 50/50 profit share would require materially different documentation and pricing.

The June 2025 Royalty Pharma-Revolution Medicines $2 billion arrangement on daraxonrasib is similarly structured around a synthetic royalty on net sales rather than a profit share. The deals that have closed in the synthetic royalty market over the last 18 months are, with very few exceptions, on assets with no co-promotion encumbrance.

What this means for new deals

Three implications for the negotiation of pharmaceutical license agreements in 2026 and beyond.

For licensors with future financing needs. Co-promotion options are valuable to retain at signing because they preserve optionality on the licensor's commercial strategy, but they should be structured with explicit financeability in mind. The Takeda-Protagonist convertibility mechanic (opt-out converts to a global royalty) is the cleanest template; it preserves the option value of co-promotion while ensuring that the asset retains a clean royalty form if the licensor chooses operational withdrawal.

Licensors that take co-promotion options without convertibility provisions should expect that any future synthetic royalty financing will be priced at a discount or will exclude the US economics entirely.

For royalty financiers. Disaggregate the contract structure before underwriting any biotech licensor's royalty potential. A "tiered royalty 10% to 20%" headline can mean anything from a clean global royalty to a residual rest-of-world royalty layered on a US profit share. The economic value of these positions differs by an order of magnitude when the asset reaches commercial scale.

The diligence question is not "what is the royalty rate" but "what is the royalty rate net of the licensor's co-promotion exercise probability." For Phase 3 assets, that probability is increasingly above 50%.

For licensees structuring new agreements. The 2024 to 2026 cohort makes clear that mid-cap and late-stage biotechs will increasingly demand co-promotion options as a condition of licensing. The negotiating choice is not whether to grant the option but how to structure the trigger, the cost reimbursement, the geographic scope, and the conversion mechanic.

Granting a co-promotion option without a convertibility provision creates the highest expected total cost (because the licensor is more likely to exercise) and the lowest residual licensee flexibility. Granting an option with a convertibility provision allows the licensee to retain pure-royalty economics in the scenarios where the licensor's commercial readiness disappoints.

For combination-product situations. The increasing prevalence of fixed-dose combinations (and, in obesity, of incretin-amylin and incretin-ACSL5 combinations) means that allocation-of-net-sales rules in co-promotion contracts will become commercially important within two to three years.

Contracts that do not specify allocation rules will be subject to negotiation under pressure when the combination launches, and the negotiation typically favors the party that controls commercial pricing.

The verdict

Co-promotion rights are a legitimate value-creation mechanism for capable mid-cap licensors, but they impose a structural cost on the royalty stack that few buy-side models price correctly. Each step rightward on the spectrum from pure royalty to co-development raises the licensor's gross expected receipt, raises its capital and operational obligations, raises the accounting and audit complexity, and lowers the contract's financeability through standard royalty channels.

The 2024 to 2026 deal cohort shows that the modal mid- and late-stage license now sits in the co-promotion-to-50/50 range; the population of clean royalty assets available for financing is shrinking relative to the population of profit-share or co-development assets.

For royalty financiers, the practical response is to disaggregate by contract structure, discount profit-share streams appropriately, and concentrate diligence on the convertibility provisions that determine whether a co-promotion-encumbered asset can be unwound back to a clean royalty form. For licensors, the practical response is to embed convertibility from signing rather than fight for it later. For licensees, the practical response is to recognize that co-promotion options are now table-stakes and to negotiate the structural terms accordingly.

The next two to three years of synthetic royalty issuance will reveal which contract templates clear the buy side and which are priced as second-class assets. The dispersion will be wider than in any prior pharmaceutical financing cycle.

This article reflects publicly available information as of April 2026. It does not constitute investment, legal, or tax advice. Mechanics and structural details described are derived from SEC filings, company press releases, and published agreements. Royalty holders, licensors, and counsel evaluating specific positions should rely on the underlying contracts and counsel.