Rights Reacquisition: Buyer Archetypes, Royalty Stack Mechanics, and the Asymmetric Pricing of Returned Pharmaceutical Assets

A pharmaceutical right, once licensed, comes home through a dozen distinct mechanisms operated by five distinct buyer archetypes. The same legal instrument (an Asset Purchase Agreement, a Termination Agreement, a contractual reversion clause) means very different things depending on whether a Phase-3-failed asset is being salvaged by its original developer, a Greater China territory is being consolidated by a global rightsholder, or a distressed listed biotech is being acquired by a hedge-fund-sponsored cash arbitrage vehicle.

Three deals from a single seven-day window in April 2026 make the asymmetry concrete. On April 16, MeiraGTx reacquired worldwide rights to bota-vec from Johnson & Johnson for $25 million upfront and a high-double-digit royalty back to J&J starting mid-2029. On April 20, Biogen reacquired Greater China rights to felzartamab from TJ Biopharma for $100 million upfront, up to $750 million in milestones, and a tiered royalty to TJ Bio. Eight months earlier, on June 25, 2025, Arbutus and Qilu mutually terminated their imdusiran agreement with no payments at all.

Three orders of magnitude in headline value. The reason is not deal-craft. It is the asset's clinical state, the licensee's strategic state, and the buyer's archetype.

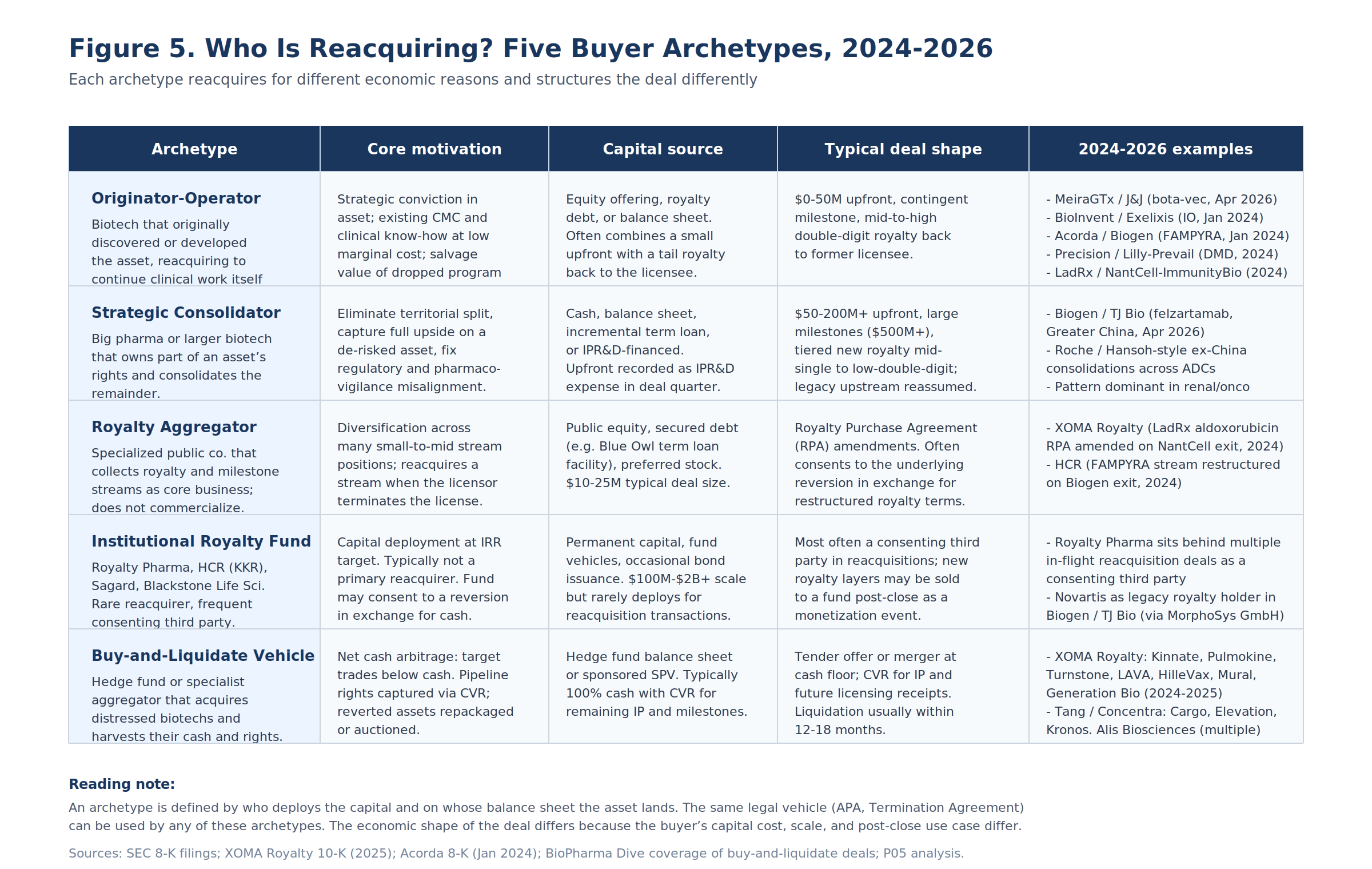

Section 1: Who Is Reacquiring?

Most analyses of reacquisition treat the buyer as monolithic. The 2024-2026 transaction set shows otherwise: there are five distinct buyer archetypes, each with a different capital cost, a different post-close use case for the asset, and a different deal shape.

Originator-Operators

The biotech that originally discovered or developed the asset reacquires it to continue clinical work itself. This is the most common 2024-2026 archetype. Capital comes from equity offerings, royalty-backed debt, or balance sheet cash. Deal economics are favorable to the originator because the licensee has typically already concluded the asset has limited internal value.

| Deal | Date | Original out-license | Reacquisition terms | Driver |

|---|---|---|---|---|

| MeiraGTx / J&J (bota-vec) | Apr 2026 | $415M (Dec 2023) | $25M up + 1 milestone + high-double-digit royalty | Phase 3 LUMEOS fail at J&J |

| Acorda / Biogen (FAMPYRA) | Jan 2024 | 2009 ex-US license | Termination, no payment; double-digit royalty back from Biogen runs out in transition | Generic erosion on a 15-year-old MS asset |

| Precision / Lilly-Prevail (DMD ARCUS) | Apr 2024 | Up to $2.05B headline (2023) | Termination "without cause" by Lilly; full data and material reversion | Lilly pipeline reprioritization post preclinical milestone |

| BioInvent / Exelixis (IO antibodies) | Jan 2024 | Discovery option from 2020 | Notice of termination; 90-day wind-down | Exelixis early-discovery deprioritization |

| LadRx / NantCell-ImmunityBio (aldoxorubicin) | Jun 2024 | 2017 license | Mutual termination; XOMA RPA amended in parallel | NantCell program shutdown |

What unites these deals is the asymmetry of post-deal economics. The originator pays close to zero upfront in cash, retains all upside, and pays back via a tail royalty contingent on commercial success. The licensee recovers a small fraction of its original outlay (J&J's $25M from MeiraGTx is roughly 19% of the $130M upfront J&J paid in December 2023, before milestones) and holds optionality on the relaunch via the tail royalty.

Strategic Consolidators

A pharma or larger biotech that already owns part of an asset's rights buys out the remainder. This is the most expensive archetype and the one with the most operationally complex post-close royalty stack, because consolidation almost always involves reassuming a pre-existing upstream royalty obligation on the newly consolidated territory.

The Biogen / TJ Bio felzartamab deal is the canonical 2026 example, structured around the headline $100M upfront, up to $750M in milestones, and a mid-single-to-low-double-digit royalty on Greater China net sales. Every component is materially larger than the originator-operator archetype, because the consolidator is paying for an actively advanced asset, not for a salvage opportunity. The 11.8% upfront-to-headline ratio is materially above the 2026 median of around 7% for licensing, but that is the wrong reference point: the relevant comparison is what Biogen would lose by perpetually conceding 25-35% of worldwide net sales to a separate Greater China rightsholder.

Roche's pattern of ex-China consolidation deals across ADCs in late 2025 (with Hansoh and others) is the same playbook. The question for an analyst tracking 2026-2027 announcements is which other late-stage Greater-China-split assets exist in big pharma's pipeline that could see this consolidation move next.

Royalty Aggregators (the XOMA Model)

A specialized public company that collects royalty and milestone streams as its core business. The aggregator does not commercialize. It does not take operational responsibility for an asset post-close. It builds a portfolio of small-to-mid-sized stream positions, often with $5-25M ticket sizes per asset, and absorbs the diversification benefit across many programs.

XOMA Royalty's strategy since its 2017 pivot is the cleanest example: as of year-end 2025, XOMA holds economic rights to over 120 commercial products and pre-commercial therapeutic candidates. The reacquisition exposure for XOMA is unusual: it sits as a third-party royalty holder when the underlying license terminates, and must amend its Royalty Purchase Agreement in parallel with the reacquisition transaction. The LadRx case is exemplary: when LadRx and NantCell mutually terminated the aldoxorubicin license in June 2024, XOMA consented to the termination, received an amended RPA giving it a low-single-digit royalty on aldoxorubicin and a mid-single-digit cut of any future out-license economics, and remained in the capital structure of the reacquired asset.

The aggregator's economic interest is to keep the asset alive. Where the originator wants to relaunch and the licensee wants to exit, the aggregator wants the rights to pass to whichever party can monetize them. XOMA's restructured RPA is designed exactly for this: low single-digit royalties on direct LadRx commercialization, mid-single-digit on any out-license LadRx pursues. XOMA wins more on a future out-license than on an internal LadRx commercialization, and the contract economics reflect that preference.

Institutional Royalty Funds

The big institutional funds (Royalty Pharma, HCR which is now KKR-controlled, Sagard, Blackstone Life Sciences) are rare primary reacquirers. Their underwriting standards and ticket sizes ($100M-$2B+) make them poorly fit for the typical reacquisition deal, which is concentrated at the small end of the size distribution.

But they appear frequently as consenting third parties in reacquisitions, because they hold synthetic royalty layers on assets whose underlying licenses are being unwound. The Acorda / Biogen FAMPYRA termination is an example: HCR holds a synthetic royalty position on FAMPYRA from a 2017 transaction, and Biogen's January 2024 termination notice meant the underlying revenue stream Biogen was paying through to Acorda would now flow to Acorda directly, requiring restructuring of the HCR position.

A second use case for institutional funds is buying the new royalty layer after the reacquisition closes. The TJ Bio royalty stream that Biogen now pays on Greater China felzartamab net sales is monetizable: TJ Bio could sell the royalty rights to a fund for an upfront cash payment. There is no evidence this has happened yet, but the structure is exactly the kind of post-close royalty financing that Royalty Pharma deploys at scale. Expect 2027-2028 to see secondary royalty market activity on the new layers created by 2026 reacquisitions.

Buy-and-Liquidate Vehicles

The newest archetype, and the most aggressive in 2024-2025. A hedge fund or sponsored SPV acquires a publicly listed biotech whose market capitalization trades below its net cash, harvests the cash, and disposes of the pipeline rights via license-back to a successor or via liquidation auction. The reacquisition step occurs because the target's pipeline includes assets that had been licensed out; on liquidation, those assets revert under the licensor's reversion clauses, and the buy-and-liquidate vehicle captures the proceeds.

XOMA Royalty has been the most active buy-and-liquidate operator: it acquired Kinnate, Pulmokine, Turnstone, LAVA, HilleVax, Mural Oncology, and Generation Bio across 2024-2025. The Tang Capital / Concentra Biosciences vehicle has been similarly active, acquiring Cargo Therapeutics, Elevation Oncology, and Kronos Bio. Alis Biosciences is a third active player. A William Blair analysis of the six buy-and-liquidate deals in Q2 2025 alone found $1.5 billion in combined net cash on the seller balance sheets.

The legal architecture of these deals is distinctive: a tender offer or merger at a cash floor (often slightly below the trading price, because the target's stock is trading on residual hope rather than fundamental cash value), combined with a Contingent Value Right (CVR) covering excess cash, future milestone receipts on out-licensed assets, and any monetization of reverted IP. The reacquisition mechanic operates inside the CVR: when an out-licensed program reverts to the wound-down target, the proceeds flow to the CVR holders (the former target shareholders), not to the buy-and-liquidate vehicle directly.

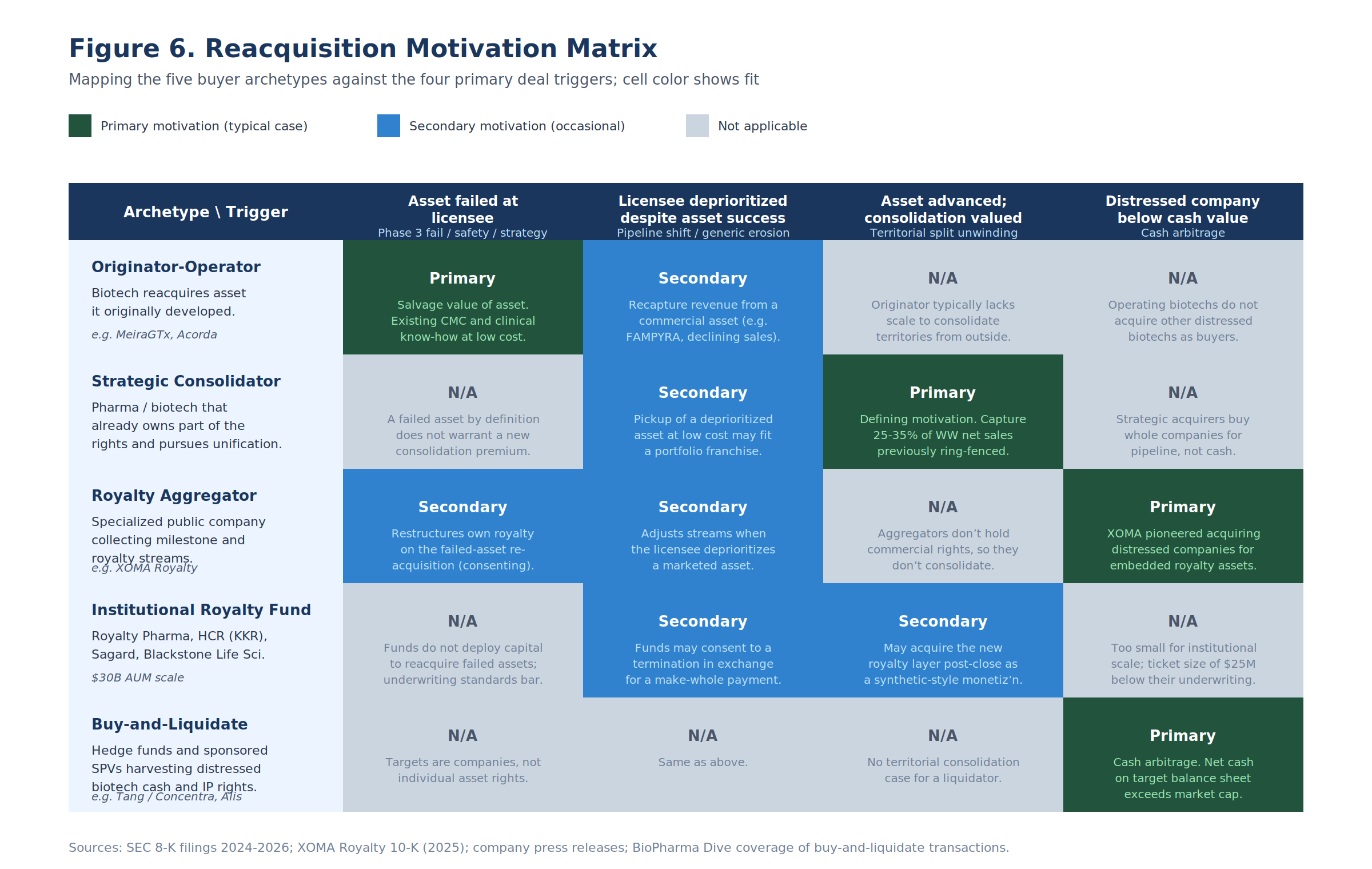

Section 2: The Motivation Matrix

The five archetypes do not all reacquire for the same reasons. Mapping archetypes against trigger types produces a 5x4 motivation matrix, with most cells empty.

The structure of the matrix carries information. Strategic consolidators do not reacquire failed assets, because failure does not warrant a consolidation premium. Originators do not buy distressed companies. Buy-and-liquidate vehicles do not pursue territorial unification. The cell-level fit is determined by the buyer's capital cost, scale, and post-close use case, not by the legal vehicle they happen to deploy.

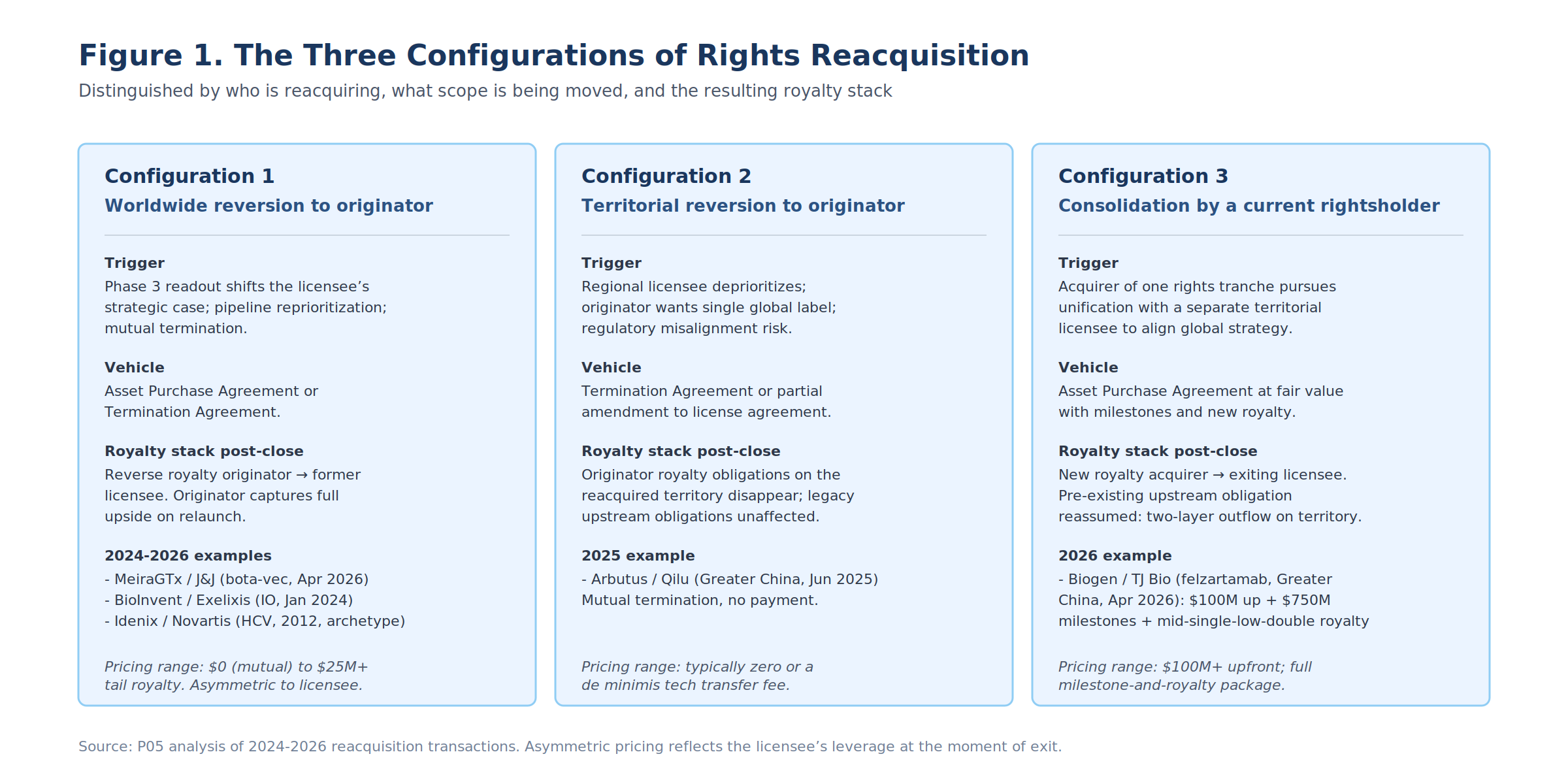

Section 3: The Three Deal Configurations

Within the five-archetype landscape, deals fall into three structural configurations distinguished by who is reacquiring and what scope is being moved.

| Configuration | Scope | Who reacquires | Vehicle | Pricing range | 2024-2026 examples |

|---|---|---|---|---|---|

| 1. Worldwide reversion to originator | Full global rights | Originator-Operator | APA or Termination Agt. | $0 (mutual) to ~$25M + tail royalty | MeiraGTx / J&J; Acorda / Biogen; BioInvent / Exelixis; Precision / Lilly-Prevail; LadRx / NantCell |

| 2. Territorial reversion to originator | Single regional territory | Originator-Operator | Termination Agt. or license amendment | Typically zero | Arbutus / Qilu (Greater China) |

| 3. Consolidation by current rightsholder | Single regional territory bought into existing global rights | Strategic Consolidator | Asset Purchase Agreement | $100M+ upfront; full milestone-and-royalty package | Biogen / TJ Bio (felzartamab Greater China) |

The pricing-by-configuration spread is the most consequential pattern in the 2024-2026 dataset. The same anti-CD38 mAb, in two transactions on opposite sides of a Greater China split, would have priced at $850M+ if Biogen consolidated from an actively advancing TJ Bio (which it did) versus close to zero if TJ Bio had simply walked away (which it did not).

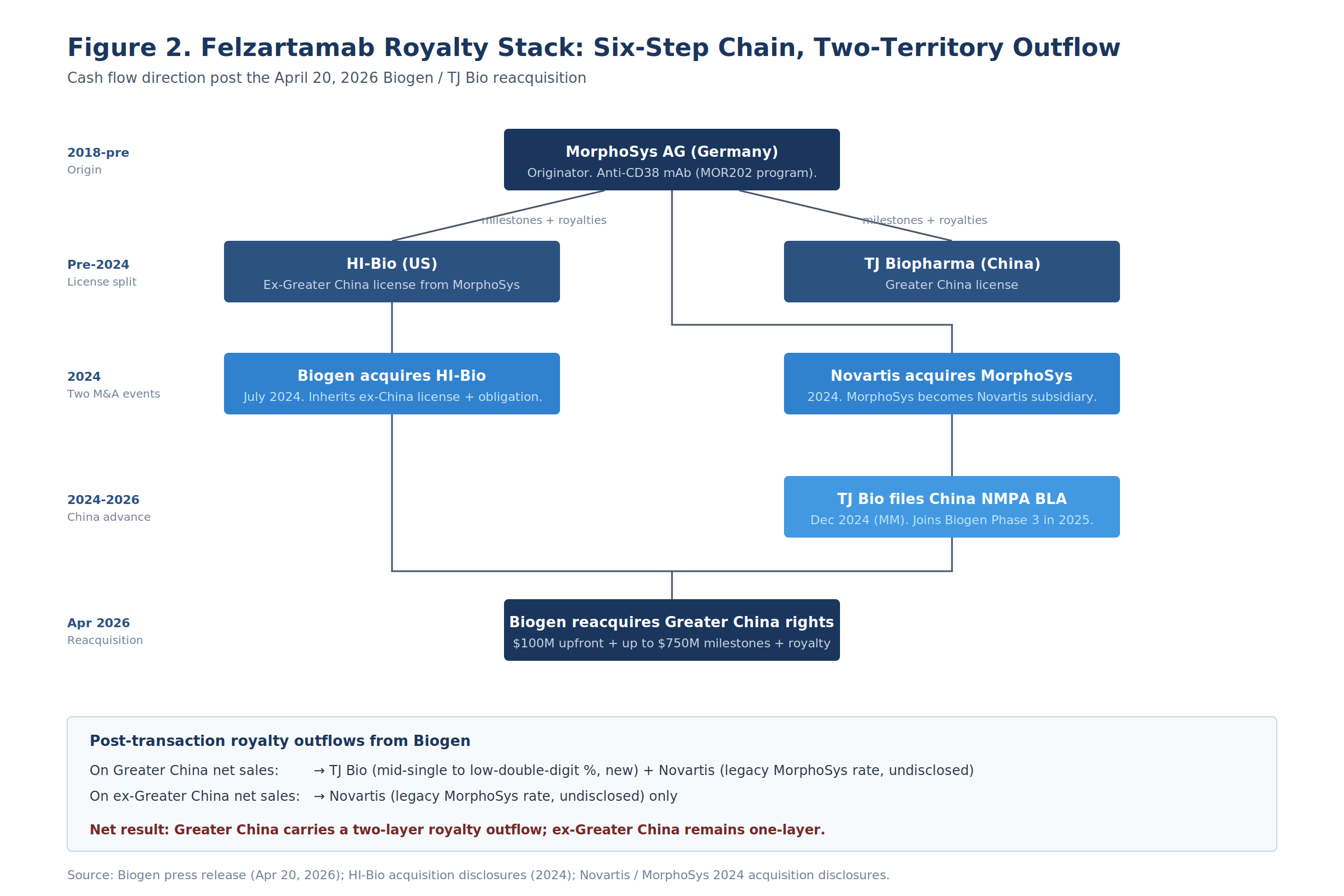

Section 4: The Felzartamab Anchor Case

Felzartamab is the densest reacquisition transaction visible in the public record this year, because the asset is in active Phase 3 with FDA Breakthrough Therapy Designation, the originator chain runs four entities deep, and the consolidation creates a documented two-layer royalty outflow on the reacquired territory.

The headline:

| Term | Detail |

|---|---|

| Acquirer | Biogen Inc. (NASDAQ: BIIB) |

| Seller (Greater China rights) | TJ Biopharma (private, Hangzhou) |

| Upfront | $100M |

| Milestones | Up to $750M (commercial / sales only) |

| Royalty to TJ Bio | Mid-single-digit to low-double-digit % on Greater China net sales |

| Total headline | Up to $850M plus tail royalty |

| Accounting | Upfront recorded as IPR&D expense in Q2 2026 |

| Asset stage | Phase 3 IgAN, PMN, AMR; FDA BTD for late AMR; China NMPA BLA filed Dec 2024 for MM |

| Manufacturing carve-out | TJ Bio retains Hangzhou GMP for the MM indication |

The transaction does three things at once: it reverses a territorial split that ring-fenced Greater China away from the rest of the world; it layers a new royalty stream from Biogen to TJ Bio on Greater China net sales; and it triggers a reassumption by Biogen of the legacy MorphoSys (now Novartis) milestone-and-royalty obligation that had previously routed through TJ Bio on the Greater China territory.

The full origin chain runs through six steps:

Each layer persists in modified form post-transaction. MorphoSys originally developed felzartamab as MOR202. MorphoSys then split commercial rights, licensing ex-Greater China to HI-Bio and Greater China through a separate path that ultimately landed at TJ Biopharma. Biogen acquired HI-Bio in July 2024 for $1.15 billion upfront and up to $650 million in development milestones, inheriting the HI-Bio license and its associated MorphoSys obligation.

Novartis acquired MorphoSys in 2024, converting the upstream royalty counterparty from a public German midcap to a wholly-owned Novartis subsidiary. TJ Bio advanced the Greater China program independently, filing a multiple myeloma BLA with the NMPA in December 2024 and joining the global Phase 3 trials in 2025.

The April 20 transaction unifies all of this back under Biogen. The post-transaction royalty outflow position is asymmetric across territories:

| Territory | Layer 1 (new) | Layer 2 (legacy) | Total layers |

|---|---|---|---|

| Greater China | TJ Bio: mid-single-to-low-double-digit % | Novartis (via MorphoSys GmbH): undisclosed legacy rate | Two |

| Ex-Greater China | (none new) | Novartis (via MorphoSys GmbH): undisclosed legacy rate | One |

For a felzartamab worldwide model, that asymmetry matters more than any single rate disclosure. A standard assumption assigns roughly 25-35% of total net sales to Greater China for IgAN and PMN given the prevalent disease populations in that region. A two-layer outflow of (illustratively) 10% to TJ Bio plus 8% legacy MorphoSys equates to an 18% gross-to-net haircut on the largest single regional revenue pool, against an 8% haircut everywhere else. The weighted-average global royalty drag therefore lands closer to 11-12%, versus 8% if the original split had persisted.

Section 5: Why the Pricing Spread Is So Wide

Five 2024-2026 reacquisitions illustrate the pricing range and what drives it.

The pricing determinants reduce to four variables:

| Variable | Direction | Magnitude |

|---|---|---|

| Asset clinical state at deal time | Higher = higher price | ~10x: Phase 3 + BTD vs failed |

| Licensee strategic state | "Walking away" = lower price | Up to 100x at the extreme |

| Buyer archetype | Strategic consolidator pays most; aggregator pays least | Up to 5x on upfront |

| Upstream royalty stack complexity | More layers = lower upfront available for licensee | Up to 30% discount in the upfront |

The MeiraGTx case illustrates the lower bound starkly. After J&J's Phase 3 LUMEOS trial in XLRP failed in 2024, J&J had no strategic case for retaining bota-vec. MeiraGTx, having retained manufacturing and clinical-development know-how, had a colorable case for restarting the program with a different regulatory thesis. Pricing reflects the asymmetry: $25 million upfront against a high-double-digit royalty back to J&J starting mid-2029.

The Arbutus / Qilu unwinding shows the floor: zero upfront, mutual termination, full reversion. By contrast, the Biogen / TJ Bio deal at $850M+ shows what the same kind of territorial reversion costs when the licensee is actively advancing the asset into Phase 3 and a regulatory filing.

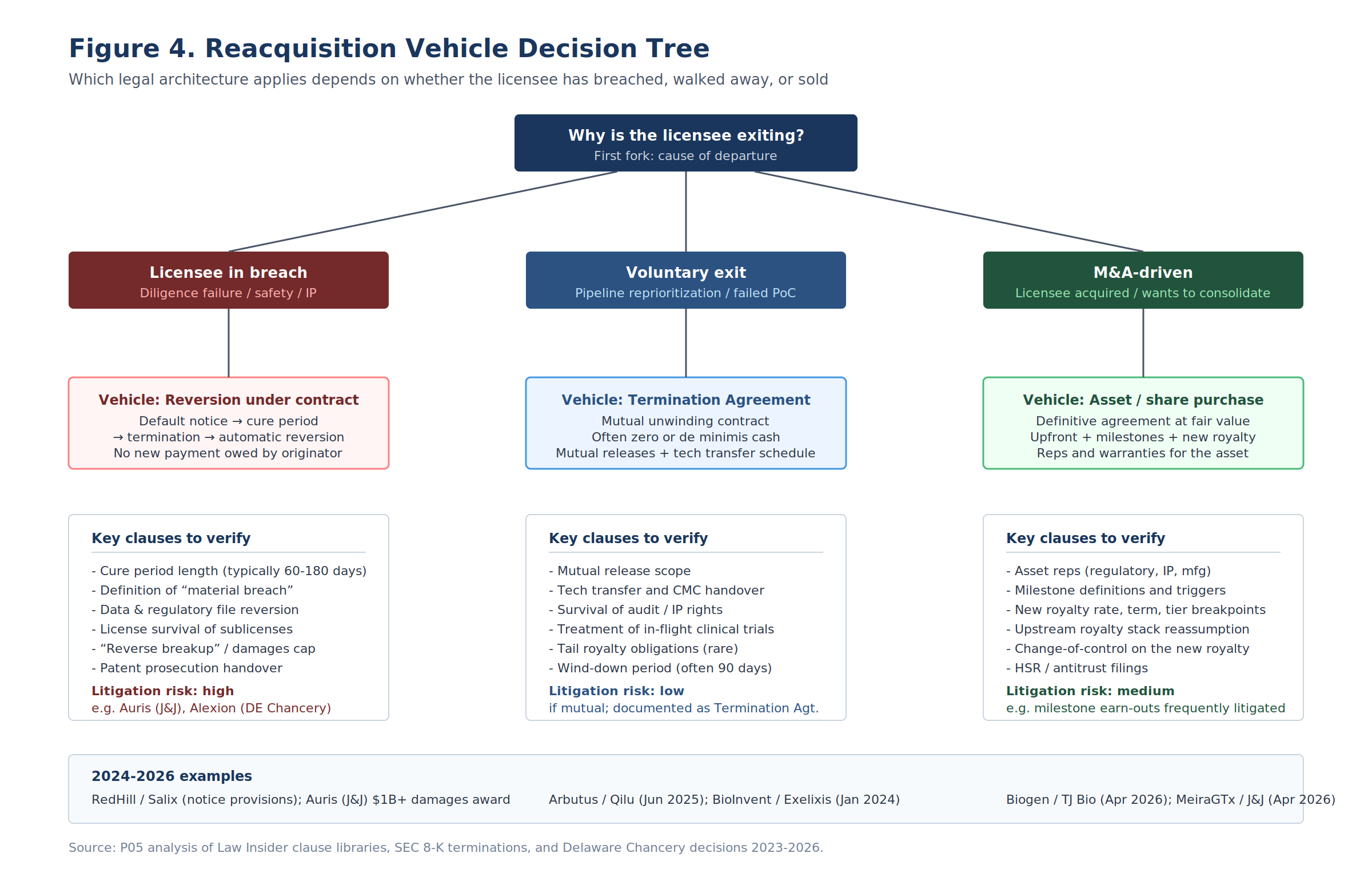

Section 6: The Vehicle Decision Tree

Contract architecture follows from the cause of departure.

A licensee leaves an agreement for one of three reasons. It is in breach. It has voluntarily decided to exit. Or it is consolidating or divesting in a portfolio context. Each cause maps to a different vehicle, a different cash profile, and a different litigation surface.

| Cause | Vehicle | Typical cure / wind-down | Cash to originator | Litigation risk |

|---|---|---|---|---|

| Breach (diligence, safety, IP) | Reversion clause + termination notice | 60-180 day cure period | Possibly damages or reverse breakup fee | High; CRE characterization is heavily litigated |

| Voluntary exit | Termination Agreement | 90-day wind-down typical | Zero or de minimis | Low |

| M&A-driven consolidation | Asset Purchase Agreement | HSR + closing conditions | Significant upfront + milestones + royalty | Medium; milestone earnouts frequently disputed |

Breach-Driven Reversion: The Reversion Clause

Reversion of license clauses are standard. The mechanic is uniform: a non-breaching party serves a default notice; the breaching party has a cure period (60-180 days, with some agreements running longer for development milestones); if the breach is not cured, the agreement terminates and licensed rights revert automatically.

The contestable elements are: what counts as "material breach," what data and regulatory documents revert, whether sublicenses survive, and whether the breaching licensee owes damages or a reverse breakup fee.

Diligence-failure terminations are the most-litigated subspecies because the standard is the Commercially Reasonable Efforts clause. The Processa / Ocuphire license is a representative drafting: efforts are pegged to what a "biopharmaceutical company of comparable size and resources would normally use to accomplish a similar objective under similar circumstances." Objective in principle; fact-intensive in practice.

Two recent decisions confirm the litigation surface:

| Case | Year | Holding | Implication |

|---|---|---|---|

| Shareholder Representatives LLC v. Alexion | 2024 (Del. Chancery) | Alexion failed to use commercially reasonable efforts to develop a licensed product | A licensor can recover damages on CRE failure; reversion is not the only remedy |

| Auris Health / J&J | 2024 | $1B+ damages award against J&J for failure to support development under earnout | Earnout failure adjacent to diligence failure; large damages possible |

A well-drafted reversion clause specifies the cure period, the deliverables on reversion (regulatory dossier, IND/BLA correspondence, raw clinical data, master cell banks, manufacturing process know-how), the timeline for delivery (60-120 days post-termination), the survival of audit rights (1-3 years), the treatment of in-flight clinical trials, and the fate of sublicenses.

Voluntary Exit: The Termination Agreement

When neither party is in breach but both want out, the vehicle is a Termination Agreement. The Arbutus / Qilu termination is exemplary: no payments associated with the termination, all rights reverted to Arbutus.

Drafting work concentrates in: defining what reverts, mutual releases scoped to the terminated agreement, survival of confidentiality and audit rights, the wind-down period (often 90 days during which the licensee continues operating for the licensor's benefit), and tail royalty obligations (rare but not unheard of).

M&A-Driven Consolidation: The Asset Purchase Agreement

When the cause is strategic consolidation, the vehicle is an APA (or MIPA/SPA). This is the heaviest documentation burden:

| Provision | Why it matters |

|---|---|

| Defined territory and conveyed rights | Prevents post-close ambiguity on the scope of what changed hands |

| Asset reps and warranties | Regulatory status, IP ownership, FTO, manufacturing compliance, product liability |

| Milestone definitions and triggers | Specific events with clear triggers reduce earnout litigation |

| New royalty rate, tier structure, term | The tail economic relationship between buyer and seller |

| Reassumption of upstream stack | What legacy obligations the acquirer is taking on |

| Change-of-control treatment of new royalty | Whether a future M&A on either side extinguishes or assumes the royalty |

| HSR and antitrust filings | Timing and reverse termination fees |

Section 7: Royalty Stack Engineering Around Reacquisition

The most consequential structural design choice in a reacquisition is how the new royalty layer interacts with the legacy upstream stack. Three patterns recur.

| Pattern | Mechanic | Effect on post-close royalty drag | Typical use case |

|---|---|---|---|

| Stacking | New royalty added on top of legacy royalty | Highest gross-to-net haircut | Default; preserves legacy counterparty relationship |

| Anti-stacking caps | New royalty reduced by % of legacy royalty paid on same revenue base | Capped haircut | Synthetic-royalty-heavy structures |

| Buyout of legacy layer | Acquirer pays upfront premium to extinguish legacy royalty | One layer post-close | Cleanest but most expensive at signing; requires legacy counterparty consent |

Biogen / TJ Bio is a stacking deal: TJ Bio royalty is added to the Novartis legacy obligation on Greater China sales. This produces the highest gross-to-net royalty drag of any of the three patterns but preserves the legacy Novartis (formerly MorphoSys) counterparty relationship intact. It also preserves the legacy counterparty's audit rights and contractual protections.

Anti-stacking is the structurally cleaner alternative but underused in reacquisition deals because it requires bilateral agreement with the legacy counterparty. The legacy holder loses something (potential overpayment if both layers stack at full rate) and must be compensated, typically through an undisclosed fee or rate adjustment.

Buyouts of the legacy layer are the cleanest post-close structure but the most expensive at signing. In the felzartamab case, Biogen would have needed Novartis's agreement to buy out the legacy MorphoSys royalty, and Novartis as a strategic-rationale royalty holder (not a financial royalty fund) typically prices these buyouts at a meaningful premium to NPV. There is no public indication any such buyout was attempted.

The choice among the three patterns has direct accounting consequences. Under ASC 470-10-25 and parallel IFRS guidance, a stacked structure produces two separate royalty obligations on the income statement, each as a reduction of revenue (or as a financing liability if recharacterized). An anti-stacked structure produces a single net obligation calculated as a function of both rates. A bought-out structure eliminates the legacy obligation entirely at the cost of a one-time IPR&D or intangible asset on the balance sheet.

Section 8: The Consenting-Third-Party Problem

Reacquisitions do not operate in a vacuum. Most assets at the moment of reacquisition have a non-trivial royalty stack already in place, and that stack contains parties whose consent is required to consummate the deal.

Three categories of consenting third party recur:

| Category | Example | Consent leverage | Typical resolution |

|---|---|---|---|

| Upstream license holder (originator pre-licensee) | Novartis (via MorphoSys) on felzartamab | High; can refuse to assign | Acquirer reassumes obligation in full |

| Synthetic royalty holder | HCR on FAMPYRA | Medium; can demand make-whole | RPA amendment with revised economics |

| Senior secured creditor | Blue Owl term loan facility for XOMA | Low to medium; lien on collateral | Intercreditor or release-and-repledge mechanics |

The consenting third party is the underdiscussed liability in every reacquisition. In the Acorda / Biogen FAMPYRA case, the underlying Biogen-to-Acorda royalty stream that HCR had purchased in 2017 changed character on Biogen's January 2024 termination notice: instead of receiving Biogen's royalty payments to Acorda, the FAMPYRA revenue would flow to Acorda directly post-2025. HCR's economic position depends entirely on whether Acorda's direct commercialization produces revenue at parity with, above, or below Biogen's commercialization. The HCR position was restructured to accommodate this transition; the terms are not fully public.

For an analyst reading a reacquisition press release, the consenting-third-party question is one of the most useful diligence dimensions. Assets that have been monetized through a synthetic royalty in the past 5-7 years are likely to carry a consenting-fund obligation. Assets that originated through a multi-step licensing chain (felzartamab is the extreme example) carry consenting-pharma obligations.

Section 9: Manufacturing Continuity Mechanics

For complex biologics and gene therapies, the manufacturing chain is the binding constraint on the post-reversion timeline. Three patterns:

| Pattern | Description | Typical timeline | Cost impact |

|---|---|---|---|

| Originator retained CMC | Originator never relinquished commercial manufacturing license | Immediate | None |

| Tech transfer back | Originator must rebuild manufacturing from licensee's process | 18-30 months for AAV; 12-18 for mAbs | Significant |

| Continued supply agreement | Originator buys supply from former licensee post-close | Ongoing | Margin transfer to former licensee |

MeiraGTx's bota-vec reacquisition was operationally feasible only because MeiraGTx had retained the commercial manufacturing license at its London facility and the QC release function in Shannon, Ireland. Without that retained CMC capability, the reacquisition would have required either tech transfer or a continued supply agreement with J&J, each with its own contractual frictions.

For Biogen / TJ Bio, the CMC question reads inverted: TJ Bio retained the Hangzhou GMP facility for the MM indication. The disclosure does not specify how Biogen will source Greater China supply for the IgAN/PMN/AMR indications. Either Biogen ships ex-China supply into Greater China (NMPA importation considerations), Biogen contracts with TJ Bio's Hangzhou facility on commercial supply terms (long-tail counterparty dependency), or Biogen builds or contracts a separate Greater China supply node. Each path has materially different cost and timing implications. The disclosure is silent. For an analyst, this is the single largest unmodeled operational variable.

Section 10: Change-of-Control Mechanics on the New Royalty

Every new royalty agreement created in a reacquisition includes change-of-control provisions, and the design determines whether the royalty becomes an asset, a liability, or an obstacle in any future M&A on either side.

Four standard configurations:

| Configuration | Acquirer-friendliness | Royalty-holder-friendliness | Effect on M&A optionality |

|---|---|---|---|

| Automatic assumption | High | Low | Royalty transfers with no consent right; minimal friction in future M&A |

| Consent right for royalty holder | Medium | High | Acquirer must obtain consent, often subject to credit-quality tests |

| Buy-out right for acquirer | High | Low | Acquirer can extinguish at 1.5x-4x of upfront less royalties paid |

| Put right for royalty holder | Low | High | Royalty holder can accelerate and demand make-whole; pulls toward loan characterization |

The Biogen / TJ Bio press release does not disclose the change-of-control treatment of the new TJ Bio royalty. For a $100M-upfront, $750M-milestone deal, this is the most material undisclosed term. If Biogen is acquired in 2027-2028, the TJ Bio royalty on Greater China felzartamab sales becomes a liability that any acquirer must price into its bid.

The MeiraGTx / J&J reacquisition embeds change-of-control terms that work in the opposite direction: J&J holds the tail royalty back from MeiraGTx, and any acquirer of MeiraGTx must assume the J&J royalty as a first-dollar obligation on bota-vec global net sales. For MeiraGTx, this is a structural anti-takeover provision similar in effect to the Cytokinetics / Royalty Pharma 2024 anti-M&A synthetic royalty, although in MeiraGTx's case the structural effect was incidental rather than designed.

Section 11: Disclosure Gaps in the Public Record

For each reacquisition, four dimensions are answerable from typical disclosure and four are not:

| Dimension | Answerable? | Why it matters |

|---|---|---|

| Headline value | Yes | Market signals |

| Configuration (1, 2, or 3) | Yes | Structural reading |

| New royalty range (rate band) | Usually yes | Modeling the new stream |

| Asset clinical state at deal time | Yes | Risk profile |

| Legacy upstream royalty rate | No | Largest single modeling unknown |

| Anti-stacking treatment | Rarely disclosed | Determines true gross-to-net drag |

| Change-of-control treatment of new royalty | Rarely disclosed | M&A optionality on either side |

| Manufacturing continuity terms | Rarely disclosed | Operational risk and supply margin |

The first four drive the headline read of the deal. The latter four drive the actual P&L and M&A profile post-close. Anyone modeling a reacquired asset who has not stress-tested the four undisclosed elements is modeling a distribution, not a point estimate.

Section 12: What This Tells Us About 2026 Royalty Markets

Reacquisition activity is bidirectional and accelerating. Three forward dynamics are visible.

The buy-and-liquidate vehicle is now an institutional category. XOMA Royalty went from a traditional biopharma developer to a $384M market cap royalty aggregator in five years and now competes with hedge funds for distressed listed biotechs. The economic logic is sound: with nearly 300 listed biotechs trading below their cash reserves, the universe of takeover candidates is structurally large. The reacquisition mechanic operates inside the CVR, and the secondary royalty market created by these deals is a new asset class for institutional fund deployment.

Strategic consolidation by current rightsholders will be the dominant new royalty layer creator in 2026-2028. The Biogen / TJ Bio template is the playbook: an originator chain creates a multi-territory split during the asset's clinical development phase, the asset advances, the rightsholder with global ambition pays a substantial upfront-plus-milestones-plus-royalty package to consolidate, and the new royalty layer becomes a future monetization candidate. The pattern is most likely in renal, oncology, and rare disease assets where multinational sponsors and Asia-Pacific licensees have advanced asset-by-asset programs in parallel.

Originator-operator reacquisitions will price near zero, with high-rate tail royalties. As big pharma pipeline reprioritization continues and Phase 3 failure rates in gene therapy and other complex modalities remain high, the supply of failed-or-deprioritized assets returning to originators will outpace the supply of cash with which originators can pay for them. The equilibrium is a near-zero upfront and a high-rate tail royalty. MeiraGTx / J&J at $25M upfront against a high-double-digit royalty is the template.

For royalty financing investors, the new royalty layers created in Configuration 3 transactions are the most attractive fresh underwriting opportunities. They are created on already-validated assets at terms that price commercial risk rather than early-stage uncertainty. Expect royalty funds to start sitting on the seller side of these reacquisitions in 2026-2027, monetizing the new royalty stream pre-close to free cash for the seller's wind-down or pipeline pivot.

The 2025-2030 reacquisition wave is structurally different from the 2010-2020 wave because the buyer landscape is different. There were originators reacquiring assets in 2012 (Idenix from Novartis on HCV, the textbook archetype). There were no royalty aggregators in the contemporary XOMA mold deploying capital at scale, no buy-and-liquidate vehicles harvesting cash-below-market biotechs, and no institutional royalty funds at $30B-AUM scale acting as consenting third parties on most of the deals. The buyer ecosystem matters at least as much as the deal terms.

Sources: Biogen / TJ Bio joint press release, April 20, 2026. MeiraGTx 8-K and asset purchase agreement, April 16, 2026. Arbutus 8-K and Qilu Termination Agreement, June 25, 2025. Acorda 8-K, January 11, 2024. LadRx 8-K and XOMA Royalty Purchase Agreement amendment, June 3, 2024. Precision BioSciences 8-K, April 11, 2024. XOMA Royalty 10-K (year ended December 31, 2025). Industry analyses from BioPharma Dive, FiercePharma, Gibson Dunn, Goodwin, Morgan Lewis, and DrugPatentWatch as cited inline. SEC filings as cited inline. This post is informational and does not constitute investment, legal, or tax advice.