Fund of the week: EcoR1 Capital

What is EcoR1 Capital?

EcoR1 Capital, LLC is a San Francisco based, biotechnology dedicated investment manager founded by Oleg Nodelman.

The management entity was organised in 2012 and began investing in 2013. It runs from 357 Tehama Street, in the South of Market district.

It is a registered investment adviser and the general partner of the EcoR1 Capital Funds. The SEC categorises it across an unusually wide set of strategies: long/short equity, event driven, venture capital, and credit.

EcoR1 sits in a very different place from the small founder led vehicle this series profiled last week. Where KCap is a sub 24 million dollar crossover fund built around two principals, EcoR1 is a multi billion dollar specialist with a deep bench, a flagship hedge fund, a qualified purchaser feeder, and a dedicated venture vehicle.

It is one of the better known names on the buy side of biotech. The kind of fund whose participation in a private round is treated by other investors as a quality signal.

For royalty investors, structured credit funds, and licensing executives, EcoR1 is interesting on two levels.

The first is what it owns: a concentrated book of clinical and commercial stage biotech equities, several of which sit at the centre of live pharmaceutical royalty structures.

The second is what it does not own, and why that matters. EcoR1 buys equity and accepts binary clinical risk in exchange for exit upside. It is not a royalty buyer. Yet its single largest position spent early 2026 executing one of the more instructive royalty financings of the year.

Overview and Investment Focus

EcoR1 is a manager sitting above a family of pooled vehicles.

The general partner and adviser is EcoR1 Capital, LLC. Beneath it sit the flagship long biased hedge fund, a parallel qualified purchaser fund for larger and more restricted investors, and the EcoR1 Venture Opportunity Fund, L.P., the dedicated private vehicle first raised toward the end of the last decade.

The adviser reports a small number of advisory clients. Those clients are the pooled vehicles themselves, not the underlying investors.

A single sector, two time horizons. EcoR1's mandate is narrow by sector and broad by stage. It invests almost exclusively in biotechnology and life sciences, but across the full life cycle of a drug developer: private rounds, crossover financings ahead of an IPO, the public float itself, and selective credit positions.

The firm describes its ethos as patient driven and scientifically literate. In practice that means board seats, large concentrated stakes, and a willingness to hold through the volatility that defines the sector.

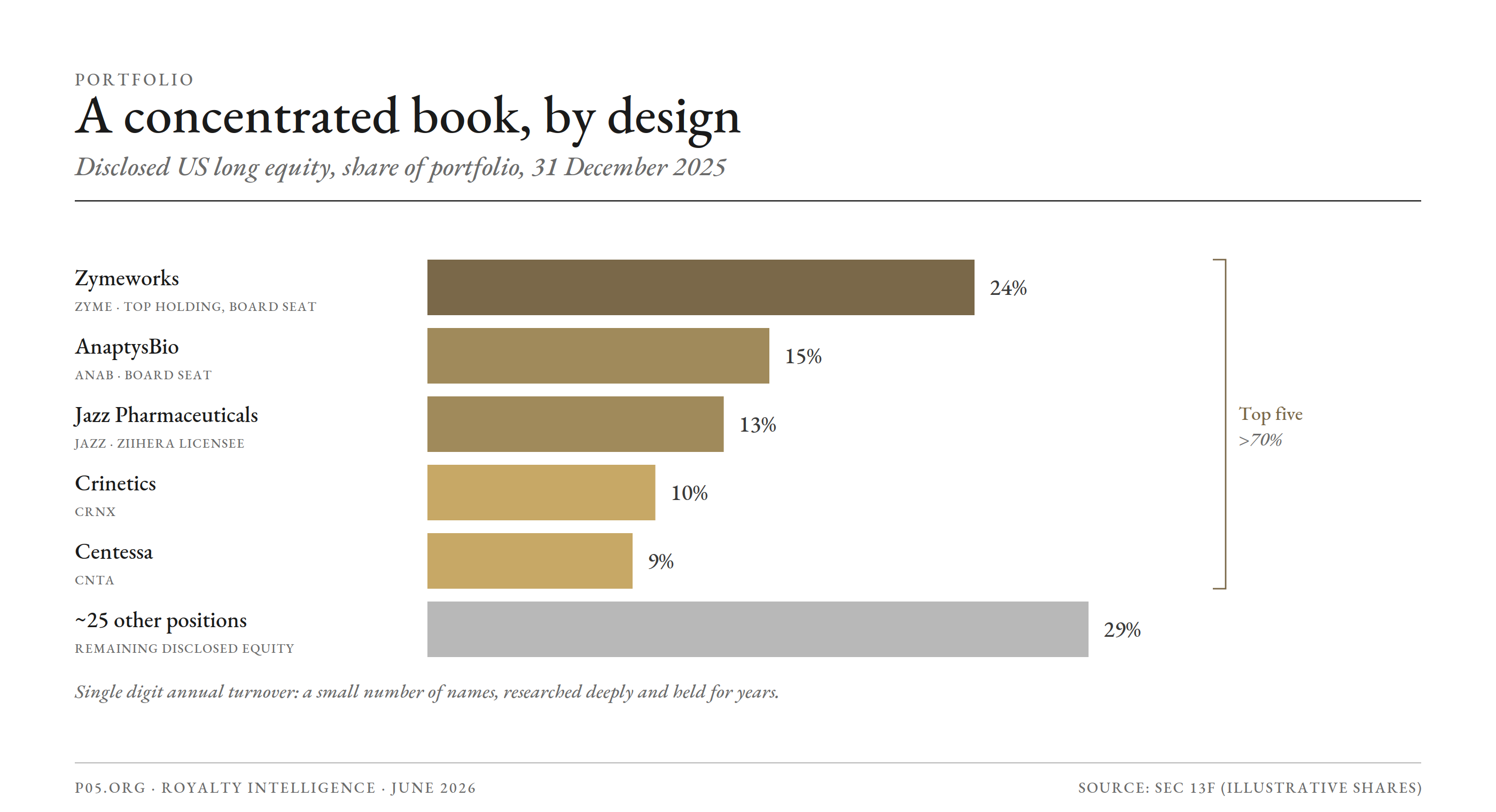

Concentration over diversification. Unlike a generalist platform that spreads capital across a hundred names, EcoR1 runs a deliberately concentrated book. Its most recent comprehensive snapshot showed roughly thirty disclosed long positions, with the top five accounting for more than seventy percent of the disclosed equity and turnover in the single digits.

This is a high conviction, low churn strategy. A small number of deeply researched bets held for years, not a trading book.

The crossover bridge. The structural point that matters for royalty and credit readers is that the same firm holds both private venture positions and the public equity of commercial stage companies.

It can back a company in a Series B, follow it through an IPO, take a board seat, and still own a meaningful stake when that company starts monetising its pipeline through licensing and royalty structures. EcoR1 sees the full arc, which is exactly the arc royalty markets eventually buy into.

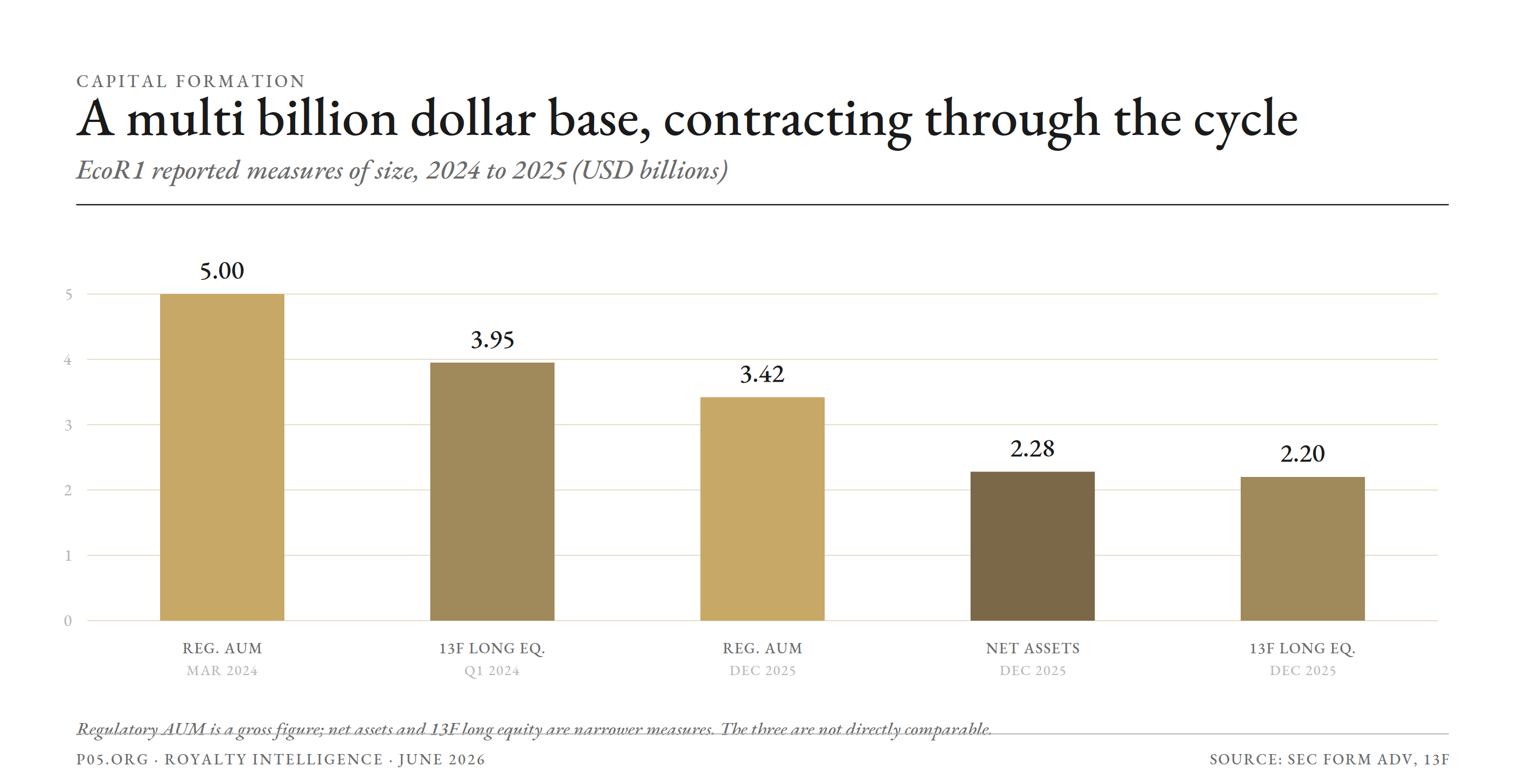

Capital Formation and Assets Under Management

EcoR1's asset base is itself a read on the biotech cycle.

The firm scaled into a multi billion dollar manager during the 2020 to 2021 bull market, then contracted through the long sector drawdown that followed.

The figures below come from the firm's Form ADV filings and quarterly 13F disclosures. They should be read with care, because regulatory assets, net assets, and 13F equity value are three different measures.

| Date / period | Measure | Figure | Notes |

|---|---|---|---|

| March 2024 (Form ADV) | Regulatory AUM | ~5.00 billion USD | Reported across a small number of pooled clients |

| Q1 2024 (Form 13F) | Disclosed US long equity | ~3.95 billion USD | Top ten concentration ~61% |

| 31 December 2025 (Form ADV) | Regulatory (gross) AUM | ~3.42 billion USD | Filed March 2026 |

| 31 December 2025 (Form ADV) | Net assets under management | ~2.28 billion USD | Discretionary, net basis |

| 31 December 2025 (Form 13F) | Disclosed US long equity | ~2.20 billion USD | ~30 positions, top five ~70% |

A few points follow.

Regulatory assets is a gross figure that can include leverage and uncalled commitments, which is why it sits above the roughly 2.28 billion dollars of net assets reported for the same date.

The 13F value captures only US listed long positions. It excludes cash, shorts, private holdings, and foreign listed names, so it understates the true size of the firm.

The direction of travel is the headline. On a regulatory basis the firm moved from around 5.0 billion dollars in early 2024 to around 3.4 billion dollars by the end of 2025.

Some of that is mark to market: a concentrated long biotech book falls hard when the sector falls hard, and this was one of the worst sustained drawdowns small and mid cap biotech has seen. Some of it may reflect redemptions or distributions. The filings do not separate the two, and this article does not speculate on the split.

What can be said is that EcoR1 remains a multi billion dollar manager, and that its asset base is sensitive to a sector that has been out of favour.

Management Company and Limited Partners

The adviser, EcoR1 Capital, LLC, is controlled by Oleg Nodelman, its manager, controlling owner, and portfolio manager.

The named officers on the most recent filing include Nodelman alongside the firm's chief financial officer and its chief operating officer and general counsel. These are signals of a built out back office, not a one person shop. The firm employs a full investment and operations team.

On the limited partners themselves, the public record is, as it almost always is for a private fund, effectively silent. No specific limited partner names are disclosed in any public filing.

What can be said is structural rather than nominal:

- The adviser's handful of reported clients are the pooled fund vehicles, not the underlying investors. The investor base sits one layer below that, inside each partnership, and is not publicly itemised.

- A specialist that scaled to several billion dollars in 2020 and 2021 will, in the ordinary course, have raised from an institutional base: endowments, foundations, public and corporate pensions, funds of funds, insurance balance sheets, and large family offices, alongside the general partner's own capital. That is the standard composition for a franchise of this size, and it differs sharply from the high net worth circle that backs a first time fund.

- Participation is restricted to accredited investors and qualified purchasers. The qualified purchaser feeder exists precisely to accommodate the larger and more restricted end of that base.

In short, the limited partner picture is best understood as an institutionally weighted base backing a marquee specialist manager.

Anyone seeking specific names will not find them in the public record, and this article does not speculate about individual investors. The honest position is that the composition can be inferred from the fund's size and category, while the roster cannot be confirmed.

The Founder

EcoR1 is, to a first approximation, Oleg Nodelman and the team he has built around him.

Oleg Nodelman (founder and portfolio manager). Nodelman has more than two decades in biotech investing.

Before founding EcoR1 he was a portfolio manager at BVF Partners, one of the original dedicated biotechnology hedge funds, where he learned the concentrated, research first style that EcoR1 now runs.

He holds a Bachelor of Science in Foreign Service from Georgetown University, with a concentration in science and technology. An unusual route into a field dominated by PhDs and MDs, and one that helps explain the firm's self description as bilingual, fluent in both the science and the strategy.

What distinguishes Nodelman from a purely financial allocator is how deeply he embeds in his companies. He currently sits on the boards of several public biotechs, including AnaptysBio (ANAB), Zymeworks (ZYME), and Lakefront Biotherapeutics, and on the board of Aktis Oncology (AKTS), a radiopharmaceutical company EcoR1 backed privately and supported through its public debut.

This is the behaviour of an operator investor. A manager who takes governance responsibility, not just a position.

A deep bench, not a solo act. The contrast with the typical emerging manager is the institutional depth behind the founder. EcoR1 runs a full team across research, trading, finance, operations, and legal.

Key person risk is still present, because Nodelman is the central decision maker and the holder of the board seats. But it is buffered by a far larger organisation. The firm is more institution than vehicle.

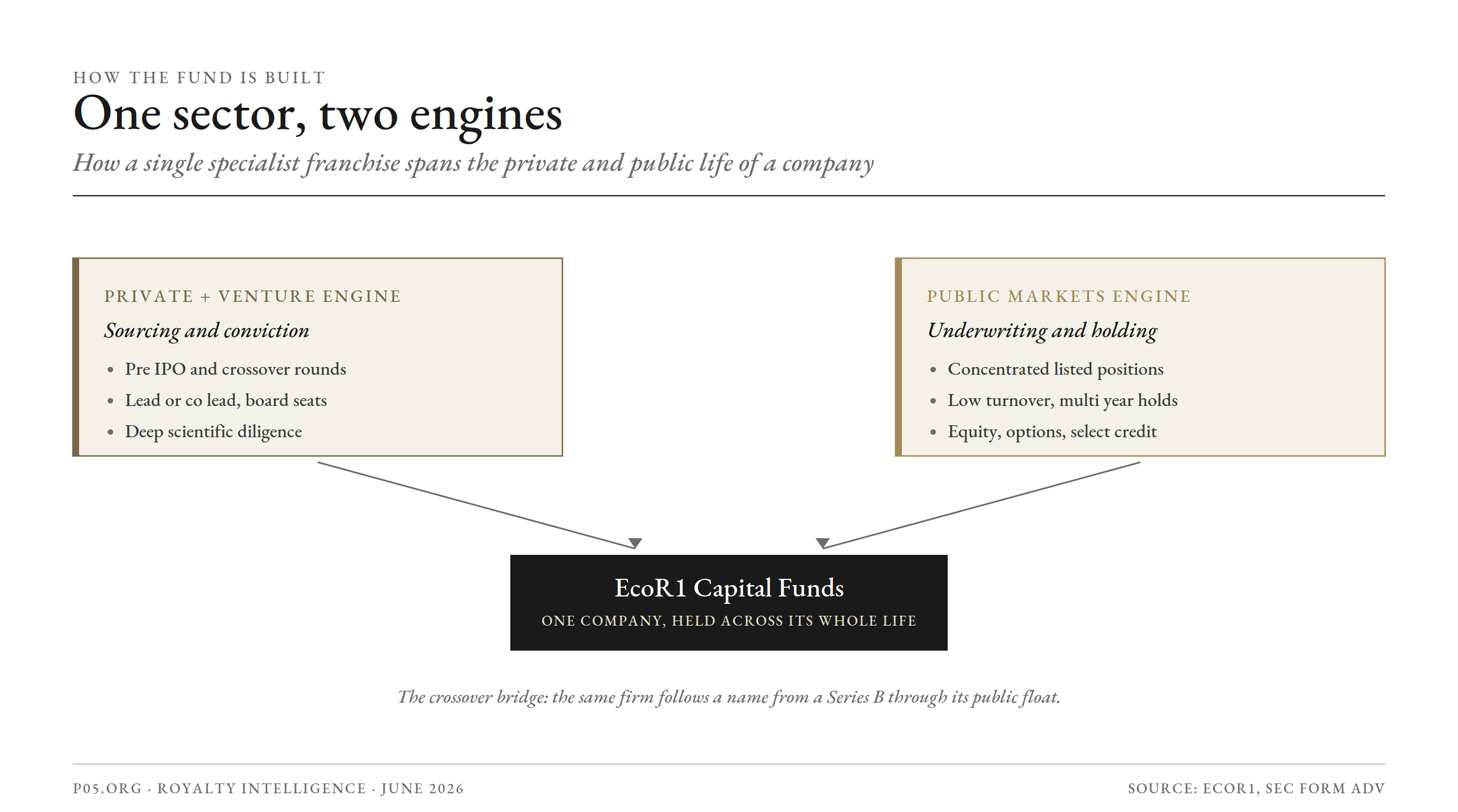

How the fund is built

What differentiates EcoR1 from both a conventional biotech hedge fund and a conventional life sciences venture fund is that it runs both engines under one roof, pointed at one sector.

A private and venture engine sources pre IPO companies, leads or co leads crossover rounds, and takes board seats in the companies the firm believes in most.

A public market engine underwrites and holds concentrated positions in listed biotech, including the same companies after they go public, expressed through equity, options, and selective credit.

Folded into a single specialist franchise, the result is a manager that can hold a company across its entire life as a public and private entity, compounding informational edge from one stage to the next.

The low turnover and high concentration are the visible fingerprints of that design. EcoR1 is built to know a small number of companies extraordinarily well and to stay with them.

Royalty and Strategic Income Positions

EcoR1 invests through equity and, at the margin, credit.

It does not own a pharmaceutical royalty portfolio, does not issue royalty backed debt, and does not earn ongoing royalty income on the products its portfolio companies develop. A royalty buyer such as Royalty Pharma, HealthCare Royalty, or Sagard Healthcare buys cash flows directly. EcoR1 buys equity.

What makes it worth a royalty reader's attention is not its balance sheet but its book. Several of its largest positions sit directly on top of live royalty structures, and during early 2026 its biggest holding executed a textbook royalty financing.

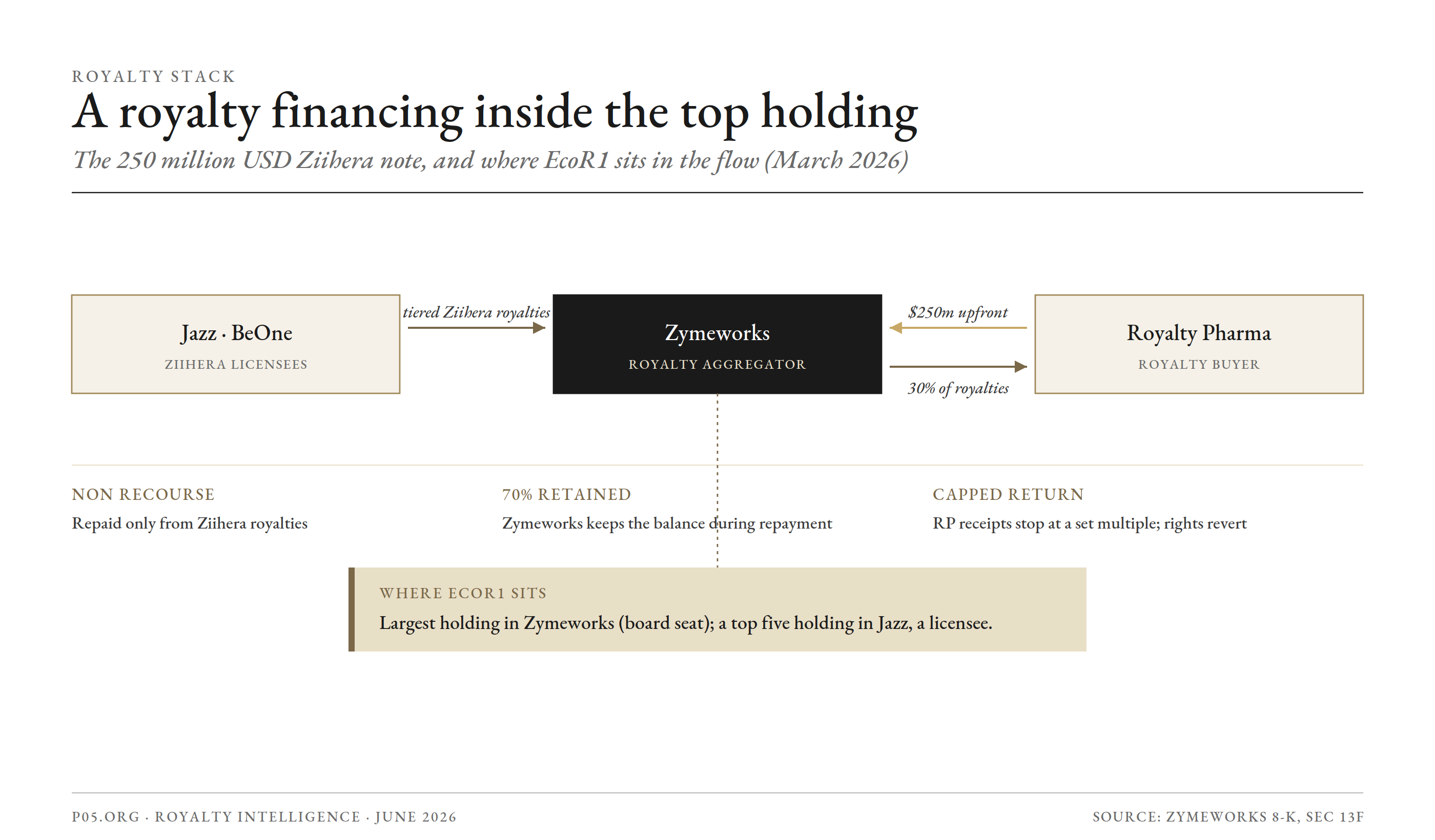

Zymeworks and Royalty Pharma: a royalty financing inside the top holding

EcoR1's largest disclosed equity position at the end of 2025 was Zymeworks, the company on whose board Nodelman sits.

Zymeworks is itself an instructive royalty story. It has repositioned around what it calls an asset and royalty aggregation strategy, building cash flows from licensed products including Ziihera (zanidatamab), partnered with Jazz Pharmaceuticals and BeOne Medicines.

In March 2026, Zymeworks and Royalty Pharma announced a 250 million dollar non recourse, royalty backed note. The structure is a clean teaching example.

Zymeworks receives 250 million dollars up front. Repayment comes from 30 percent of the worldwide tiered royalties it is owed on Ziihera. Zymeworks retains the other 70 percent during the repayment period, and full royalty rights revert to it once Royalty Pharma has been repaid.

Royalty Pharma's return is capped: its receipts stop once they reach a defined multiple of the note, a higher multiple applying the longer repayment runs. The capital is non dilutive, and Zymeworks used it to fund buybacks and extend runway.

For a royalty reader the relevance is layered. EcoR1's largest equity position is a company that is simultaneously a royalty recipient, a royalty seller, and a royalty aggregator.

And EcoR1's third largest position at year end was Jazz Pharmaceuticals, one of the licensees on the other side of those Ziihera royalties. Through its equity book, EcoR1 sits on multiple sides of a single royalty flow.

Commercial assets and embedded royalty economics

Beyond Zymeworks, the book skews toward commercial and near commercial companies whose value is driven by royalty bearing and milestone bearing licensing.

Crinetics, Centessa, and AnaptysBio each carry the standard architecture: partnered programmes with upfronts, development and regulatory milestones, sales milestones, and tiered royalties on net sales.

The headline value of these arrangements is almost always dominated by back loaded, low probability tiers, while the certain cash sits in the upfront and near term components. EcoR1's equity captures that value only at the company level, mediated by the share price, not as a direct claim on any royalty stream.

The credit option

The detail most often overlooked is that the SEC classifies EcoR1 as running credit strategies alongside its equity book.

A specialist biotech manager with credit capacity is structurally positioned to participate in exactly the instruments that increasingly blur the line between equity, debt, and royalty: convertible notes, synthetic royalty financings, development funding bonds, and revenue interest facilities.

The public record does not detail the size or content of EcoR1's credit activity, so this is a capability flag rather than a confirmed book. But it places the firm closer to the structured financing world than a pure long/short equity manager would be.

Portfolio of Investments

EcoR1's public equity book is disclosed quarterly through its 13F filings. Its venture positions surface mainly when a private company names its investors. The two together describe a single, sector concentrated strategy.

Public equity book (most recent comprehensive snapshot, 31 December 2025). The disclosed long portfolio held roughly thirty US listed positions worth about 2.2 billion dollars, with the top five names representing more than seventy percent of disclosed equity value and turnover in the single digits.

| Position | Ticker | Role in book | Royalty / licensing relevance |

|---|---|---|---|

| Zymeworks | ZYME | Largest holding; Nodelman on board | Royalty aggregator; 250M USD Royalty Pharma note (March 2026) |

| AnaptysBio | ANAB | Top five; Nodelman on board | Partnered immunology programmes |

| Jazz Pharmaceuticals | JAZZ | Top five | Commercial licensee; pays Ziihera royalties to Zymeworks |

| Crinetics | CRNX | Top five | Commercial stage endocrinology |

| Centessa | CNTA | Top five | Clinical pipeline; milestone bearing assets |

Venture and crossover positions (representative). EcoR1's private activity spans the modalities the firm knows best.

Representative names include Aktis Oncology (radiopharmaceuticals, where Nodelman is a director and EcoR1 added roughly 40 million dollars of stock around its January 2026 public debut), Janux Therapeutics, Relay Therapeutics, Artiva Biotherapeutics, and recent 2026 syndicates such as the 125 million dollar Diagonal Therapeutics Series B. Earlier exposure included Affinia, Codiak, and Clementia.

A note on disclosure: the venture roster is necessarily partial, visible only where companies have named EcoR1 or where the firm has filed as a beneficial owner. Readers should treat the confirmed positions as a floor, not a complete picture.

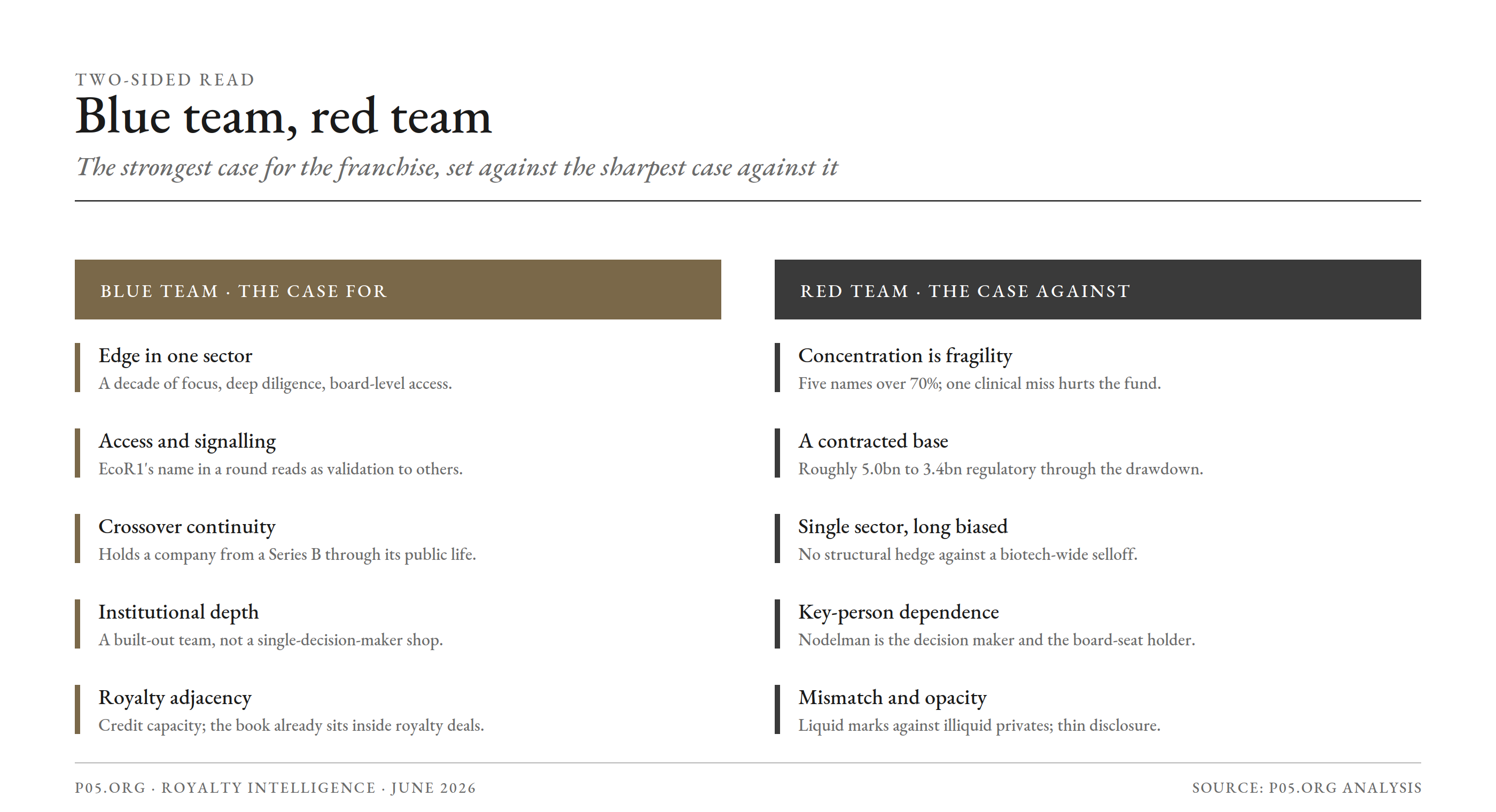

Blue Team and Red Team

The blue team builds the strongest defensible case for the franchise. The red team attacks it from the position of a sceptical allocator or a competitor. Both are true at once, which is what makes the fund worth watching rather than simply admiring.

Blue team: the case for

A genuine edge in one sector. EcoR1 does one thing, and it has done it for over a decade. Narrow mandate, deep scientific literacy, board level access, and a low turnover book mean it accumulates knowledge a generalist cannot replicate. In a sector where edge comes from clinical and regulatory nuance, that focus is the moat.

Operator credibility and deal access. Nodelman's board seats and reputation give EcoR1 access to the highest quality private syndicates. When the firm participates, other sophisticated investors read it as validation.

Crossover continuity. The ability to hold a company from a private round through its public life is a structural advantage. EcoR1 does not have to re underwrite a name it already knows when it goes public. That continuity lowers diligence cost and sharpens conviction.

Institutional depth. Unlike the emerging managers this series often profiles, EcoR1 has a built out team and back office. The franchise is more resilient to any single departure than a two person shop.

Royalty adjacency. With credit capacity and a book that already sits inside live royalty structures, EcoR1 is closer to the structured financing world than most equity managers. That adjacency is an option on the financing innovations reshaping how biotech monetises its pipelines.

Red team: the case against

Concentration cuts both ways. A book where five names are more than seventy percent of disclosed equity is a high variance bet. A single pivotal trial failure or label disappointment in a top position has an outsized effect on returns. The same focus the blue team calls a moat, the red team calls fragility.

The asset base has contracted. Regulatory assets fell from around 5.0 billion to around 3.4 billion through the drawdown. Mark to market explains much of it, but a shrinking base pressures fee revenue, can force selling at the wrong time, and tests limited partner patience.

Single sector, single direction. EcoR1 is long biased and confined to one of the most cyclical corners of public markets. It has no structural diversification away from a biotech wide drawdown.

Key person concentration. The deep bench buffers but does not eliminate the dependence on Nodelman. He is the central decision maker, the holder of the board seats, and the source of much of the firm's deal access.

Liquidity mismatch and opacity. A vehicle that holds illiquid private positions alongside a liquid public book carries an inherent mismatch: in a stressed market, the public side can be marked and redeemed against while the private side cannot be sold. And as a private manager, EcoR1 discloses little about strategy, terms, or performance.

Implications for the Pharmaceutical Royalty and Biotech Capital Markets

For commercial capital markets, EcoR1 matters as a signal, as a counterparty in waiting, and as a case study.

As a signal. When a manager with Nodelman's record takes a board seat and writes a large cheque, the implied scientific and commercial validation is meaningfully higher than that of a generalist syndicate. Royalty and structured credit teams can use EcoR1's involvement as a partial proxy for asset quality in oncology, radiopharmaceuticals, immunology, and endocrinology.

As a source of assets. EcoR1's portfolio companies are exactly the population that becomes royalty eligible over time. Its venture names are the clinical assets that royalty buyers evaluate for synthetic royalty and milestone backed structures. Its commercial holdings already carry partnered, royalty bearing economics. The Zymeworks note shows the endgame: an EcoR1 portfolio company selling a slice of its royalties to Royalty Pharma for non dilutive capital.

As a sign of convergence. A royalty desk underwriting a Ziihera backed note and an equity manager holding Zymeworks stock are looking at the same cash flows from opposite ends. With credit capacity of its own, EcoR1 is the kind of equity franchise that can, in principle, sit on either side. For royalty originators and arrangers, specialist crossover funds like EcoR1 are both the source of the assets and, increasingly, potential co investors in the structures built on them.

Recent Developments

| Date | Event |

|---|---|

| 2012 / 2013 | EcoR1 Capital management entity organised; Nodelman begins investing the strategy |

| 2019 | EcoR1 raises a dedicated Venture Opportunity Fund alongside the flagship hedge fund |

| March 2024 | Form ADV reports regulatory assets of approximately 5.0 billion USD |

| January 2026 | EcoR1 joins the 125 million USD Diagonal Therapeutics Series B; adds ~40 million USD of Aktis Oncology stock around its public debut |

| March 2026 | Form ADV (as of 31 December 2025) reports ~3.42 billion USD regulatory and ~2.28 billion USD net assets; top holding Zymeworks closes a 250 million USD royalty backed note with Royalty Pharma |

| May 2026 | EcoR1 active in new biotech financings, including Artiva Biotherapeutics |

Conclusion

EcoR1 Capital is a marquee specialist: a multi billion dollar, single sector, high conviction biotech manager built around one of the more respected portfolio managers on the buy side.

It is not a royalty buyer, and it is not a competitor to the royalty funds or specialty lenders. Its significance for royalty professionals is different, and arguably more useful. EcoR1 is an early, high quality indicator of where credible biotech assets are forming, and its book is a working map of where equity value and royalty value meet.

The blue team case is a genuine and durable edge in a sector that rewards focus, paired with access and institutional depth that few specialists match. The red team case is concentration, cyclicality, a contracted asset base, and the ordinary opacity of a private manager.

For royalty and licensing professionals, the practical reading is twofold. EcoR1 is a signal node for asset quality in biotech, and its largest position is, right now, a live demonstration of how a royalty financing gets done and why an equity holder welcomes it.

The open question is the ordinary one for a concentrated long biotech franchise in a difficult cycle: whether focus and conviction, the same qualities that built the firm, carry it through a sector that has tested everyone. That answer will come from the next few clinical readouts, not from any filing.

All information in this article was accurate as of the punlication date and is derived from publicly available sources including SEC Form ADV and Form D filings, quarterly 13F disclosures, beneficial ownership filings, company press releases and 8-K filings, third party data providers, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.