Company of the week: Vera Therapeutics

Vera Therapeutics spent six years turning a drug that had failed in lupus, MS, and arthritis into an approved kidney medicine. On 7 July 2026 the FDA cleared atacicept, and in the same moment flipped a dormant royalty owed to Merck KGaA into a live, cash-paying obligation. Vera is now a royalty payer with its first monetisable revenue stream, entering the single most crowded market in nephrology.

Vera Therapeutics is a single-asset company that just crossed the line most single-asset companies never reach.

For most of its life it looked like a clinical-stage biotech studied for its data, not its balance sheet. A royalty desk had little reason to open the file, because there was no product, no revenue, and therefore nothing to price.

That changed two days before this was written.

On 7 July 2026 the FDA granted accelerated approval to atacicept, branded Trutakna, for adults with immunoglobulin A nephropathy (IgAN). It is the first drug in the United States that blocks both BAFF and APRIL, the two cytokines that keep the disease's autoantibody machinery running.

What makes Vera worth a full read is not the approval itself. It is what the approval switched on.

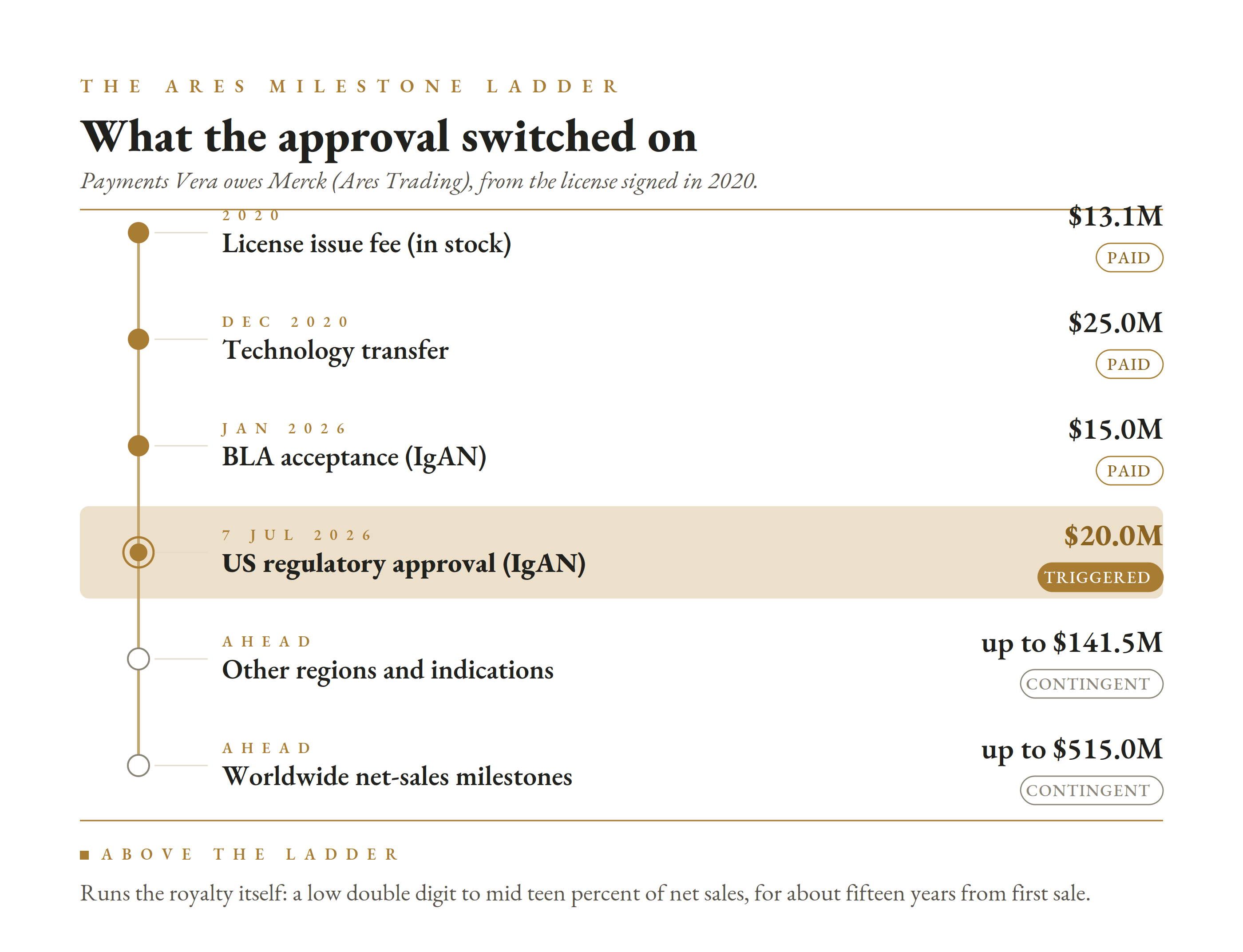

The drug is not Vera's invention. Atacicept was created elsewhere, changed hands twice, and reached Vera in 2020 through an out-licence from Merck KGaA. That licence carries a milestone ladder and a running royalty that had been sitting dormant, waiting for a first commercial sale that until this week had never come.

Approval turns that structure on. Vera now owes Merck a $20 million approval milestone, a tiered royalty on every vial it sells, and up to hundreds of millions more if atacicept scales.

At the same time, approval hands Vera something it never had before: a product revenue stream on its own books, unencumbered by any prior monetisation, that it could one day sell.

Last week's Pacira piece looked at a product owner that spent two years managing royalties it owed. Vera is a younger specimen of the same type, caught at the exact moment its first royalty obligation goes live.

At a glance

| Item | Detail |

|---|---|

| Company | Vera Therapeutics, Inc. (Nasdaq: VERA), Brisbane, California |

| Leadership | Marshall Fordyce, M.D., founder and chief executive; Sean Grant, chief financial officer; Matt Skelton, chief commercial officer |

| Lead product | Atacicept (Trutakna), dual BAFF/APRIL inhibitor, once-weekly subcutaneous autoinjector |

| Newest event | FDA accelerated approval in IgAN, 7 July 2026; US launch planned mid-2026 |

| List price | $425,000 per year, a premium to Otsuka's Voyxact at $390,000 |

| Approval basis | ORIGIN 3 interim: 42% placebo-adjusted proteinuria (UPCR) reduction at week 36 (p < 0.0001) |

| Confirmatory data | ORIGIN 3 eGFR pulled forward to Q3 2026; supplemental BLA for full approval targeted Q4 2026 |

| Pipeline | VT-109 (next-gen BAFF/APRIL, preclinical, Stanford licence); MAU868 (BK virus antibody) |

| Q1 2026 financials | Net loss $121.0M; operating cash burn $106.5M; R&D $86.0M |

| Balance sheet | Cash and securities $596.8M; ~$75M drawn on a $500M Oxford Finance term facility; accumulated deficit $881.9M (31 Mar 2026) |

| Market value | ~$3B, roughly 71.8M shares; stock rose ~8% to $43.47 on approval day, 52-week range $19 to $56 |

| Defining royalty item | The Ares (Merck KGaA) licence: tiered low-double-digit to mid-teen royalty on atacicept net sales, plus a milestone ladder up to roughly $675M |

The drug, and the owners who came before

Atacicept is a recombinant fusion protein.

It carries the soluble TACI receptor, which binds two tumour necrosis factor family cytokines, BAFF and APRIL. Both drive the survival of B cells and the production of the autoantibodies that damage the kidney in IgAN. Block both, and you cut the disease off further upstream than any drug before it.

That mechanism is the whole thesis. It is also the reason atacicept has such a long history.

The science began not in a company but in a hospital. The foundational TACI patents were invented at St. Jude Children's Research Hospital in the late 1990s and licensed to ZymoGenetics at the end of 1998. ZymoGenetics built the molecule. Merck KGaA acquired worldwide rights in 2008 and spent years testing it across autoimmune disease. In lupus the results were mixed. In multiple sclerosis and rheumatoid arthritis the drug underperformed or failed outright, and for a time atacicept looked like a shelved asset.

So the chain of ownership runs four deep before Vera: a children's research hospital, then ZymoGenetics, then Merck, then Vera. That lineage matters later, because a royalty tends to leave a trail behind it at every handover.

The revival came from a narrow, well-chosen signal. In a small Merck-run Phase 2a study in IgAN, atacicept produced a dose-dependent drop in the antibodies that seed the disease, and an improvement in proteinuria.

Merck did not pursue it. Vera did.

The lesson a royalty desk takes from this is not about biology. It is that the drug reached Vera already carrying two decades of other people's spending, and the price of that history is written into the licence Vera signed. The upside is Vera's. A defined slice of it always flows back to the originator.

The royalty it now owes: the Ares ladder

The single most important cash-flow feature at Vera is the licence it took from Merck KGaA in October 2020, signed through Merck's Swiss subsidiary Ares Trading S.A.

Under it, Vera holds an exclusive worldwide licence to atacicept and assumes all development and commercialisation. In return, Merck holds a layered claim on the drug's future.

The consideration was unusual in one respect. Merck took equity, not only cash.

The licence fee was paid in preferred stock valued at $13.1 million, which converted into about 1.9 million Vera common shares. Merck's original stake was described in 2020 as roughly 10 percent of Vera. Dilution alone has ground it down since: the position was last disclosed at about 7 percent in early 2023, and against a share count now past 70 million those same shares would sit below the 5 percent reporting line, which is likely why Merck no longer appears among Vera's named large holders. The originator did not just sell the drug. It bought into the buyer.

On top of the equity sits a milestone ladder and a running royalty. The milestones, itemised in Vera's filings, run as follows.

| Ares milestone | Amount | Status |

|---|---|---|

| Licence issue fee (in stock) | $13.1M | Paid 2020 |

| Technology transfer | $25.0M | Paid Dec 2020 |

| BLA acceptance (IgAN) | $15.0M | Paid Jan 2026 |

| US regulatory approval (IgAN) | $20.0M | Triggered 7 Jul 2026 |

| Other regions and indications | up to $141.5M | Contingent |

| Worldwide net-sales milestones | up to $515.0M | Contingent, first at $250M sales |

The sales-milestone leg is the one to watch. It begins with a $15 million payment when worldwide net sales first reach $250 million, and a further $50 million at $500 million, stepping up from there to an aggregate cap of $515 million.

Above the milestones runs the royalty itself.

Vera owes Ares a tiered royalty of low-double-digit to mid-teen percentages on annual net sales of atacicept, on a product-by-product and country-by-country basis. The obligation runs until the latest of three dates in each country: fifteen years after first commercial sale there, the expiry of the last covering patent, or the end of regulatory and data exclusivity.

Read as a royalty desk reads it, this is a clean, textbook stream.

It is single-asset, patent-and-exclusivity-anchored, tiered so the percentage rises with volume, and long-dated at a fifteen-year floor from first sale. Until 7 July it was contingent on an approval that had not happened. Now it is a live obligation that begins collecting on the first Trutakna vial shipped at the mid-2026 launch.

That is the pivot at the heart of this company. Approval did not only unlock revenue for Vera. It converted Merck's dormant paper into a cash-paying, mid-teen-ceiling royalty on a drug entering a market Vera itself sizes at $20 billion.

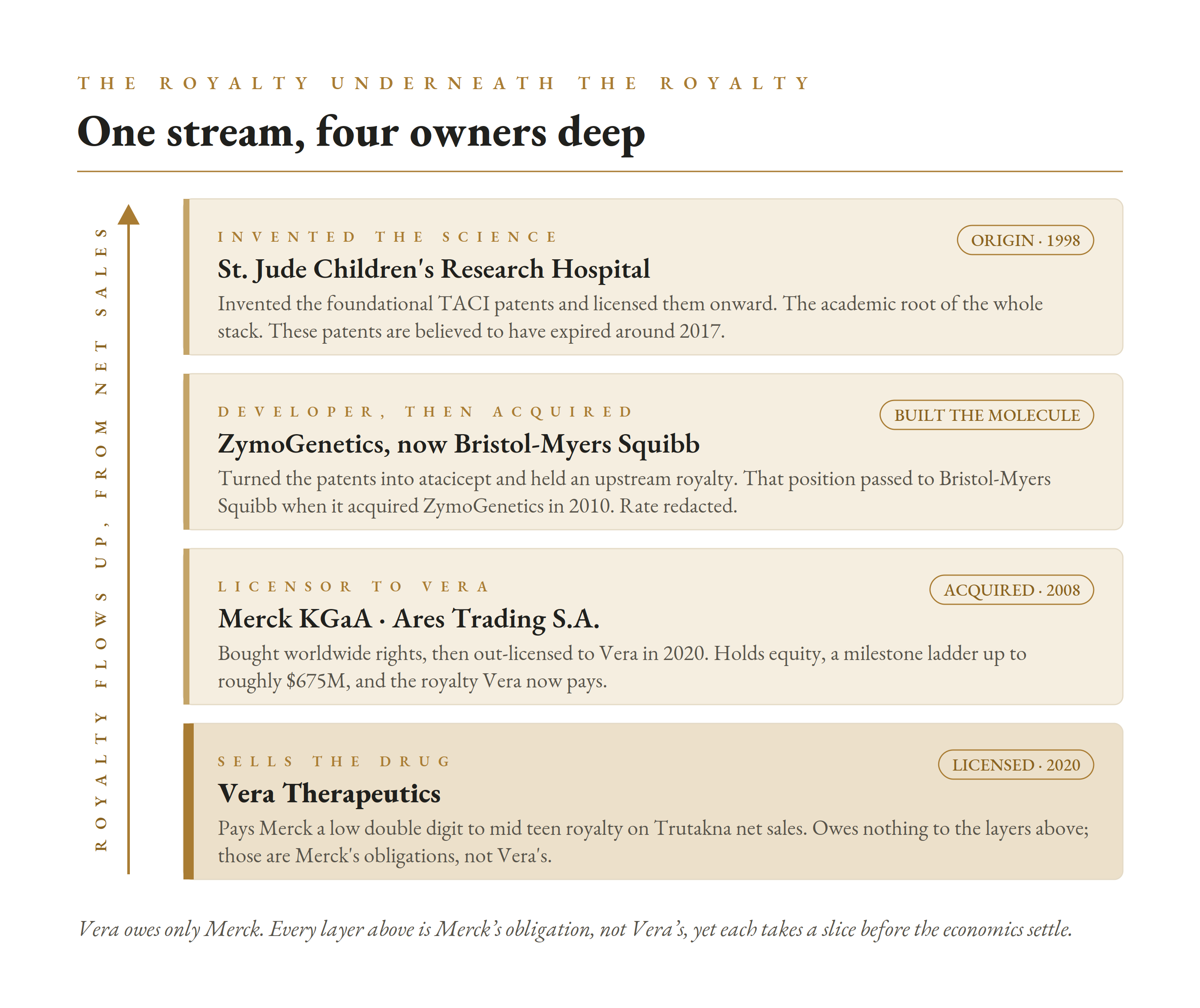

The royalty underneath the royalty

Here is the part a royalty desk will not find in Vera's filings, because it is not Vera's to disclose.

The mid-teen royalty Vera owes Merck is not the bottom of the stack. It is the top of it.

When Merck acquired atacicept, it also took on an obligation to pay royalties upstream, to ZymoGenetics, the company that originally built the molecule. That obligation did not disappear when ZymoGenetics was bought. Bristol-Myers Squibb acquired ZymoGenetics in 2010, and the royalty-receivable position on atacicept would have passed to BMS with it. So a slice of every atacicept sale traces, through Merck, to a large-cap pharma that has nothing to do with the drug's development.

And ZymoGenetics was not the origin either. The foundational TACI patents were invented at St. Jude Children's Research Hospital and licensed to ZymoGenetics at the end of 1998. The academic institution sat at the very bottom of the stack as the original royalty recipient.

Two cautions matter here. The exact percentages at these upper layers are redacted in the underlying filings, so the stack is visible in structure but not in size.

And the foundational St. Jude patents likely expired around 2017, which under a standard patent-life royalty term would have ended that particular academic royalty well before atacicept ever reached the market. BMS's continuing position is inferred from the 2010 acquisition rather than confirmed in a current filing.

The key point for Vera is what does not change. Vera's own filings disclose no royalty obligation to any party other than Ares and Merck. These upstream layers reduce what Merck keeps from Vera's payments. They do not add a cent to what Vera pays.

Read as royalty archaeology, though, it is a clean illustration of how these instruments accrete. The stream Trutakna now throws off runs Vera to Merck to Bristol-Myers Squibb, and began, decades ago, as a licence out of a children's research hospital.

The royalty ledger, in one view

For a company this young, the royalty picture is unusually one-directional.

Almost everything points outward, to Merck.

Vera pays the Ares royalty and milestone ladder. It has out-licensed nothing, so it collects no inbound royalty of its own. It retains all global rights to atacicept, to the next-generation follow-on VT-109, and to the BK-virus antibody MAU868.

The two pipeline assets carry their own in-licence royalties out, to Stanford on VT-109 and to Novartis and Amplyx on MAU868, but both are dormant while those programmes sit preclinical or non-commercial. For now, the Ares royalty on atacicept is the only outbound stream that matters.

That retention is a deliberate posture. Every ex-US territory Vera keeps rather than partners is a royalty it does not receive today, in exchange for control it hopes to convert into direct sales or a richer partnership later.

There is also a latent claim that does not appear on any filing.

Atacicept's US revenue stream is, as of this week, entirely unencumbered by any royalty monetisation. Vera has funded itself with equity and a modest term loan, not by selling a synthetic royalty against future Trutakna sales. That option now exists for the first time, and it is exactly the kind of non-dilutive launch capital a company burning $106 million a quarter tends to consider.

So the ledger is simple to state. One real royalty flows out to the originator. No royalty flows in. And one monetisable stream sits on the books, valuable precisely because nobody has yet borrowed against it.

The data that won the approval

Trutakna's clearance rests on the Phase 3 ORIGIN 3 trial.

The study enrolled 431 adults with biopsy-confirmed IgAN, randomised one to one to atacicept 150 mg self-administered weekly by subcutaneous injection, or placebo.

At a prespecified 36-week interim analysis in the first 203 dosed patients, atacicept cut proteinuria, measured by the urine protein-to-creatinine ratio, by 46 percent from baseline. Against placebo, the reduction was 42 percent, and statistically significant at p below 0.0001.

The trial's lead investigators called it the largest placebo-adjusted proteinuria reduction shown by any Phase 3 IgAN trial at week 36 to date. Supporting endpoints pointed the same way: a 68 percent reduction in Gd-IgA1, the galactose-deficient antibody that seeds the disease, and an 81 percent reduction in hematuria, though these were not adjusted for multiplicity.

These are not thinly reported numbers. The ORIGIN 3 primary results were presented in a late-breaking plenary at ASN Kidney Week in November 2025 and published in the New England Journal of Medicine, which is about as much external validation as a proteinuria dataset can carry before the eGFR question is settled.

The safety profile is the other half of the pitch.

Across the programme, infections occurred in 32 percent of atacicept patients versus 28 percent on placebo, and injection-site reactions in 30 percent versus 5 percent. Serious adverse events were actually rarer on the drug than on placebo, and there were no deaths in the registrational analysis.

Because atacicept suppresses part of the immune system, the label warns physicians to screen for active infection and to avoid live vaccines around dosing, but it carries no boxed warning and no risk-management programme, and the only contraindication is serious hypersensitivity. For a chronic immunology drug, that is about as clean a label as approval allows, and it is the point management returns to most.

One structural caveat sits underneath the whole approval.

This is an accelerated approval, granted on proteinuria as a surrogate. Proteinuria predicts kidney decline, but it is not the outcome that matters to patients, which is preserved kidney function measured by eGFR.

The date that decides whether the approval holds

Full approval requires confirmatory eGFR data showing atacicept actually slows the loss of kidney function.

The reassuring signal is already on the record. In the earlier ORIGIN Phase 2b study, atacicept patients saw an annualised eGFR decline of about 0.6 mL/min per 1.73 m² over 96 weeks, close to the decline seen in healthy adults simply ageing, alongside a 52 percent reduction in proteinuria from baseline.

The confirmatory read is now close. After a June 2026 alignment with the FDA, Vera pulled its ORIGIN 3 eGFR analysis forward to Q3 2026, from a previous 2027 timeline. It plans to file a supplemental BLA for full approval in Q4 2026, with the two-year eGFR analysis following in Q1 2027.

The company's stated rationale for accelerating was partly ethical. Chief executive Marshall Fordyce argued it was hard to justify holding patients on placebo for a full two years when the treatment separation looked meaningful well before then.

For a royalty desk, the eGFR readout is the single most important dated event in the file.

A strong result converts a surrogate-based accelerated approval into a durable, full approval and hardens every downstream cash flow, including Merck's royalty. A weak or ambiguous result would put the accelerated approval itself in question and reprice the entire structure. The confirmatory data land in a quarter, not years, which is unusually fast and unusually consequential.

The market it is walking into

Six years ago, IgAN had no approved disease-modifying therapy. Trutakna arrives as the sixth approved drug, into a field that filled in almost overnight.

The drugs already there attack the disease from different angles.

| Drug | Company | Mechanism | Note |

|---|---|---|---|

| Tarpeyo | Calliditas | Targeted-release budesonide | First IgAN approval, 2021 |

| Filspari | Travere | Dual endothelin / angiotensin blocker | Non-immunological arm |

| Fabhalta | Novartis | Complement (factor B) inhibitor | Expanded IgAN nod |

| Vanrafia | Novartis | Endothelin A receptor blocker | Atrasentan |

| Voyxact | Otsuka | APRIL-only inhibitor | Approved late 2025 |

| Trutakna | Vera | Dual BAFF / APRIL inhibitor | Approved Jul 2026 |

Vera's differentiation claim is mechanistic. Atacicept is the first to block both BAFF and APRIL, one step further upstream than Otsuka's APRIL-only Voyxact.

It priced that claim confidently. Vera set Trutakna's list price at $425,000 a year, a deliberate premium to Voyxact's $390,000, arguing that hitting two targets is worth more than hitting one. Jefferies' analyst framed the premium as justified by the most robust dataset in the class so far, while William Blair countered that Voyxact keeps real first-to-market advantages.

For a royalty desk the number matters directly: the mid-teen royalty Vera owes Merck is a share of net sales, and net sales are price times volume, so the launch price sets the base the whole royalty is measured against.

Vera also won a subtly better label. Where Voyxact was approved for patients at high risk of progression, Trutakna was cleared for patients at risk of progression, a broader population that analysts at Guggenheim read as a genuine access advantage.

That mechanistic edge is real, but it is narrowing, and it is under attack on two fronts.

The first is competitive eGFR data. On 1 July 2026, days before Vera's approval, Otsuka reported that Voyxact showed statistically significant kidney-function stabilisation over two years in its Phase 3 VISIONARY trial, with what it called evidence of improvement. Novartis's Fabhalta has its own two-year eGFR slope on record. The confirmatory bar Vera still has to clear is one competitors are already clearing.

The second is a direct mechanistic rival. Vertex's povetacicept, acquired through its 2024 purchase of Alpine Immune Sciences, is also a dual BAFF/APRIL inhibitor. It posted a 49.8 percent placebo-adjusted proteinuria reduction at week 36 in Phase 3, and faces an FDA decision by 30 November 2026. If cleared, Vera's first-and-only-dual-inhibitor window closes inside five months of opening.

Dosing is where the rivalry gets pointed.

Atacicept is dosed weekly. Both Voyxact and povetacicept are dosed once every four weeks. In a chronic disease treated for years, a weekly injection is a real adherence and convenience disadvantage against a monthly one, whatever the mechanism.

Vera's answer to that is VT-109.

The pipeline behind the pipeline

VT-109 is a next-generation BAFF/APRIL fusion protein Vera licensed from Stanford University in 2025 for an undisclosed sum.

It is preclinical, so it is years from any approval. Its point is dosing. Management has said early data suggest dosing on the order of quarterly or less frequently, which would flip Vera's weekly disadvantage into a durability advantage if it ever reaches the clinic and holds up.

The strategy is coherent. Atacicept establishes the dual-inhibition category and the commercial footprint. VT-109, if it works, defends that category against the every-four-week competitors on the one axis atacicept loses on today.

Vera's second pipeline asset, MAU868, is a monoclonal antibody aimed at BK virus, a serious problem in kidney transplant recipients. It keeps Vera inside nephrology, but it is not the story.

Fordyce has been explicit that Vera intends to stay narrow: lead in IgAN first, then expand atacicept into adjacent autoantibody-driven kidney diseases such as membranous nephropathy and focal segmental glomerulosclerosis through the ongoing PIONEER basket trial, rather than chase every autoimmune indication the class could reach.

That discipline is a bet. It concentrates the company on kidney disease and on a single molecule's success, at exactly the moment the competition is broadening.

How it funds itself: equity and a term loan, not a royalty sale

Vera does not yet earn revenue, so for now it funds itself the way a pre-commercial biotech does.

At 31 March 2026 it held $596.8 million in cash, cash equivalents, and marketable securities. That is a large cushion, but it is being spent quickly, and the pace is accelerating. Vera burned $241 million from operations across full-year 2025, then $106.5 million in the first quarter of 2026 alone, more than double the year-earlier quarter, as it staffed and stocked for a commercial launch. The first-quarter net loss was $121.0 million.

The capital structure is mostly equity, with debt held in reserve. The accumulated deficit stood at $881.9 million and the share count near 71.8 million. The debt is a term loan facility of up to $500 million with Oxford Finance, an existing lender, signed in June 2025 to refinance a smaller prior Oxford loan.

Only the first $75 million tranche was drawn at quarter-end. The other $450 million is staged, largely discretionary capacity, with tranches that unlock on events such as accelerated approval and commercial milestones.

The July 7 approval opened one of those approval-linked tranches. The drawn loan runs at one-month SOFR plus 4.95 percent, roughly 9.3 percent at the time of funding, matures around 2030, carries a 5 percent exit fee, and is secured by the company's assets other than its intellectual property. Vera also issued Oxford warrants over about 141,000 shares. The refinancing lowered the borrowing cost by 320 basis points and pushed principal payments out past 2026, which is the point: several hundred million of pre-negotiated, cheaper debt sits behind the cash pile without touching the atacicept IP.

What is notably absent is any royalty monetisation.

Vera has not pre-sold a synthetic royalty against atacicept, taken a revenue-interest advance, or borrowed against the drug's future sales. Every dollar raised has been equity or a conventional loan. The company has diluted rather than mortgaged the asset.

That is a defensible choice for a company that until this week had no product to monetise. It also leaves the most interesting non-dilutive lever fully intact.

| Capital item | Detail |

|---|---|

| Cash and securities | $596.8M (31 Mar 2026) |

| Debt facility | Up to $500M with Oxford Finance (June 2025); ~$75M drawn at SOFR + 4.95% |

| FY2025 operating burn | $241.1M |

| Q1 2026 operating burn | $106.5M |

| Q1 2026 net loss | $121.0M |

| Accumulated deficit | $881.9M |

| Shares outstanding | ~71.8M |

| Royalty monetisation | None to date; Trutakna stream unencumbered |

With approval in hand, a US launch beginning, and a $20 billion market opportunity in front of it, Vera for the first time owns a revenue stream a royalty buyer would underwrite.

Whether it ever sells a piece of that stream, to fund the launch or the pipeline without further dilution, is now a live strategic question rather than a hypothetical. It is the question that moves Vera from a name a royalty desk watches to one it could actually transact with.

Red team vs blue team

Risk analysis (red team)

One drug, one mechanism, one disease. Vera is atacicept, and atacicept is IgAN. There is no second commercial product and no near-term diversification. Every risk below lands on the same asset.

The approval is accelerated, not full. Clearance rests on a proteinuria surrogate. Full approval depends on the ORIGIN 3 eGFR confirmatory data due in Q3 2026. A disappointing readout would not just delay full approval, it would cast doubt on the accelerated approval already granted.

The market is already crowded. Trutakna is the sixth approved IgAN drug. Competitors including Otsuka's Voyxact and Novartis's Fabhalta already have two-year eGFR data on record, the bar Vera still has to clear.

A direct dual-inhibitor rival is weeks behind. Vertex's povetacicept, also a BAFF/APRIL drug with comparable Phase 3 proteinuria data, faces an FDA decision by 30 November 2026. Vera's first-in-class window may close within months.

Weekly dosing is a real disadvantage. Atacicept is injected weekly; Voyxact and povetacicept are monthly. In a lifelong disease, dosing convenience shapes adherence, formulary position, and share. The fix, VT-109, is preclinical.

The burn is steep and accelerating. Operating burn ran $241 million in 2025 and $106.5 million in Q1 2026 alone, more than double a year earlier. The cash pile and the undrawn Oxford facility cover it, but launch execution is unproven and the sales ramp behind a $425,000 price is a forecast, not a fact.

Every success feeds an outbound royalty. The better atacicept sells, the more Vera pays Merck: a mid-teen-ceiling royalty plus up to $515 million in sales milestones. Upside is shared with the originator by contract.

Opportunities and mitigants (blue team)

Approval is done, and the label is broad. Trutakna was cleared for patients at risk of progression, a wider population than Voyxact's high-risk label, giving Vera a genuine access edge plus first-mover status as the only dual BAFF/APRIL inhibitor on the US market.

The confirmatory data are close and pre-supported. The eGFR readout was pulled forward to Q3 2026, and the earlier Phase 2b eGFR signal, a near-normal 0.6 mL/min annual decline, is exactly what full approval needs. The FDA agreed to the earlier analysis on the strength of that effect size.

Placebo-like safety in a chronic disease. A safety profile close to placebo is a durable advantage in a condition treated for years, and is the differentiation management leans on hardest against both the complement and endothelin classes.

A large, expanding opportunity. Vera frames US IgAN at roughly 160,000 patients and a $20 billion market at current class pricing, with atacicept's mechanism extendable into membranous nephropathy and FSGS through the PIONEER trial.

A deep, flexible balance sheet into launch. Nearly $600 million in cash sits alongside an undrawn balance on a $500 million Oxford Finance facility, and none of it mortgages the drug. The atacicept revenue stream stays completely unencumbered and available as future non-dilutive capital.

A dosing answer in the pipeline. VT-109, the next-generation follow-on, targets quarterly-or-less dosing. If it advances, it neutralises the one axis on which atacicept loses to its monthly-dosed rivals, and extends the franchise a decade.

Summary

| Risk | Concern |

|---|---|

| Concentration | Single drug, single mechanism, single disease |

| Surrogate approval | Accelerated approval hinges on Q3 2026 eGFR confirmation |

| Crowded market | Sixth IgAN entrant; rivals already hold two-year eGFR data |

| Direct rival | Vertex povetacicept decision due 30 Nov 2026 |

| Dosing | Weekly injection versus monthly competitors |

| Outbound royalty | Sales success feeds Merck's mid-teen royalty and milestones |

| Opportunity | Observation |

|---|---|

| Broad label | Cleared for at-risk patients, wider than Voyxact's high-risk label |

| Premium pricing | $425K list versus Voyxact $390K, backed by the strongest dataset in class |

| Confirmatory runway | eGFR data pulled to Q3 2026, Phase 2b signal supportive |

| Safety | Near-placebo profile in a chronically treated disease |

| Market size | ~160,000 US patients, ~$20B market, expansion indications |

| Balance sheet | ~$600M cash plus undrawn $500M Oxford facility, stream unencumbered |

| Next-gen dosing | VT-109 targets quarterly dosing, defends the franchise |

Conclusion

Vera is a royalty story caught at its origin.

For six years it was a clinical company with nothing to price. On 7 July 2026 the FDA changed that in a single decision, and the change cut two ways at once.

It gave Vera a product, a $425,000 price, a launch, and a claim on a market it sizes at $20 billion. And it gave Merck KGaA a live royalty, a $20 million approval milestone, and a path to hundreds of millions more, all measured against that same net-sales base by the terms of a licence signed in 2020.

The financing tells you where the company is in its life. This is not yet a cash-generative franchise managing what it owes, as Pacira is. It is a pre-revenue company that has funded itself with equity and a small loan, and has just been handed its first monetisable asset without having borrowed a cent against it.

The tests over the next two quarters are unusually concrete.

Whether the ORIGIN 3 eGFR data in Q3 2026 confirm the accelerated approval will decide if this franchise is durable or provisional. Whether Vertex's povetacicept is approved by 30 November 2026 will decide how long Vera's dual-inhibitor window stays open. And whether Vera launches into share, against monthly-dosed rivals, will decide if the $20 billion market description ever becomes revenue.

Until those resolve, Vera is best read as a royalty payer on day two.

It owes the originator a rising share of a drug it did not invent, it collects nothing inbound because it has out-licensed nothing, and it holds one clean, unsold revenue stream that, for the first time, someone on the other side of a royalty desk would want to buy.

All information in this article was accurate as of the research date and is derived from publicly available sources including company press releases, SEC filings, FDA announcements, and financial news reporting. The FDA accelerated approval of atacicept (Trutakna) was announced on 7 July 2026; the US commercial launch had not yet occurred as of the research date, and the $425,000 figure is a list price that does not reflect net price after rebates and discounts. Milestone and royalty terms are described as disclosed in Vera Therapeutics' filings; certain terms are subject to conditions and may be reduced under the agreement. The upstream royalty layers described here (Merck to ZymoGenetics, now Bristol-Myers Squibb, and the original St. Jude Children's Research Hospital licence) are drawn from the historical filings of those parties; the exact percentages are redacted, Bristol-Myers Squibb's current position is inferred from its 2010 acquisition of ZymoGenetics, and the foundational patents at the academic layer are understood to have expired around 2017. These upstream obligations belong to Merck, not to Vera. Financial figures reflect the most recent reported period, the quarter ended 31 March 2026, and may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.