Debt for Deferral: When a Royalty Monetisation Is Taxed as a Loan, Not a Sale

A royalty monetisation is characterised separately by tax law, accounting, bankruptcy law, and its commercial terms. The four answers can differ on the same deal. Only the tax answer decides whether the upfront cash is income this year or deferred across the life of the stream.

This piece covers how the seller reaches the loan characterisation, how a contingent royalty is then taxed inside a debt wrapper, and how the cross-border position turns on the same choice. It is stated as of mid-2026, after the July 2025 tax legislation.

Two prior pieces on this site cover the buyer and fund side of royalty taxation: fund domicile and treaty withholding, and cross-border seller taxation across the UK, Germany, France, and Switzerland. This piece is about a different question: whether the monetisation is a sale or a loan for the seller's own income tax, and what follows from that.

Four answers to one question

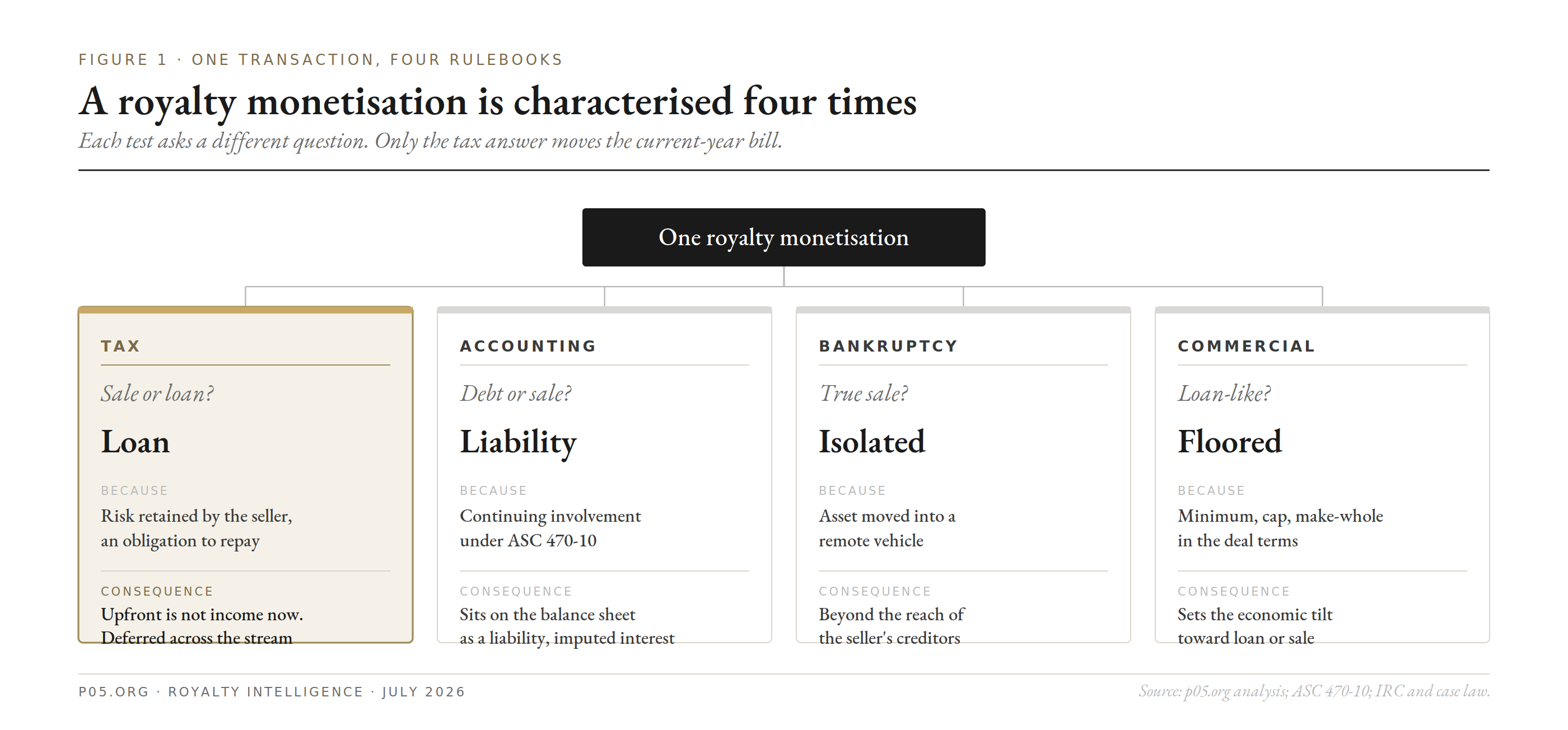

The same monetisation is characterised four times, under four tests, for four purposes.

- Tax. Sale or loan, decided by whether the risk of loss shifted to the financier or the seller retains an obligation to repay. This controls whether the upfront is income now.

- Accounting. Debt or sale, decided by continuing involvement under ASC 470-10. This controls whether the proceeds sit on the balance sheet as a liability. Covered in the balance-sheet piece.

- Bankruptcy. True sale or secured financing, decided by asset isolation into a remote vehicle. This controls whether the seller's creditors can reach the stream. Covered in the interest agent piece.

- Commercial. Sale-like or loan-like, set by the floor, the cap, and the make-whole. Covered in the minimum guarantee piece.

A deal can be a true sale for bankruptcy, a liability for accounting, and either a sale or a loan for tax. The tax answer is the one that determines the current-year tax bill, and it is decided on its own rules.

Figure 1. One transaction, four rulebooks. Each test asks a different question, and only the tax answer moves the current-year bill.

Sale and loan are taxed on different timelines

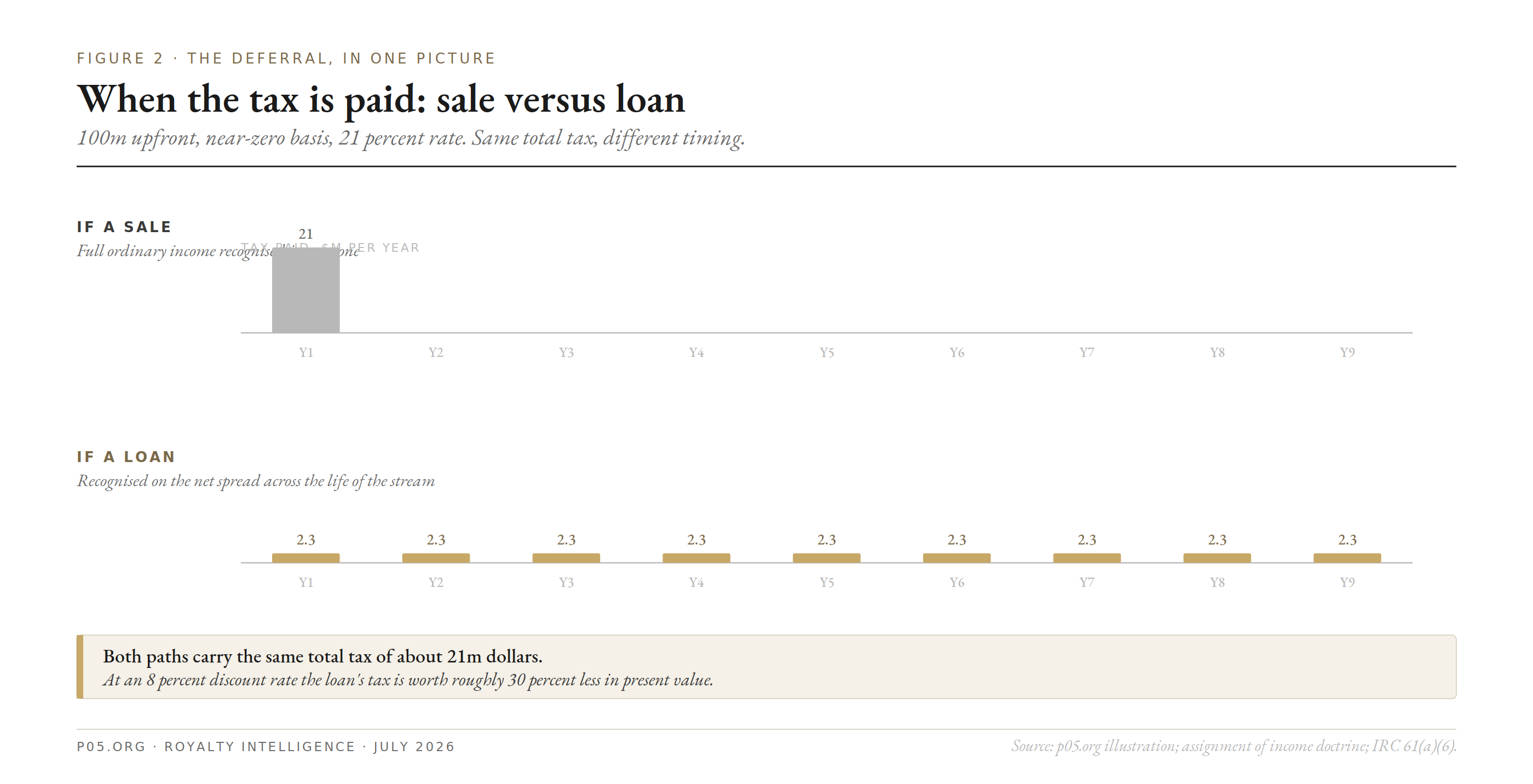

The sale case

If the monetisation is a sale for tax, the upfront payment is proceeds of a disposition. The seller recognises it in the year received, reduced only by tax basis. For a company that generated the royalty itself, basis is usually near zero. The future royalties are then the buyer's income.

The loan case

If the monetisation is a loan for tax, the upfront is loan proceeds, which are not income. The seller keeps recognising the royalty income as it arrives, pays that cash to the financier, and deducts interest on the deemed borrowing. Tax is paid over the life of the stream, on the net spread.

A sale of a royalty does not produce capital gain

The common assumption is that a sale is preferable because it produces capital gain at a lower rate. For a royalty that is generally not the outcome.

A royalty is ordinary income under Section 61(a)(6). Selling the right to future ordinary income for a lump sum does not change its character. Under the assignment of income doctrine, the proceeds remain ordinary income, because what was transferred was the right to receive ordinary income. The Supreme Court applied this in P.G. Lake, taxing the assignment of an oil payment right for cash as ordinary income. Self-created patents and similar intangibles are also excluded from the capital asset definition under Section 1221(a)(3).

Deal documents confirm the character directly. In the Lyell Immunopharma licence, the parties agree that for United States federal income tax purposes the payments are treated as royalties within Section 61(a)(6).

So for most pharmaceutical royalties the sale case delivers ordinary income, in full, in year one. The loan case delivers ordinary income spread across years. The difference is timing, not rate.

The size of the difference

A profitable royalty holder monetises a stream for 100 million dollars up front, near-zero basis, 21 percent corporate rate.

| Sale for tax | Loan for tax | |

|---|---|---|

| Upfront treated as | Income now | Loan proceeds, not income |

| Year-one tax on the upfront | About 21 million dollars | Nil |

| Future royalties | Buyer's income | Seller's income, offset by interest and OID |

| Timing of the seller's tax | Front-loaded into year one | Spread across the stream |

The benefit of the loan is the time value of the tax the sale would have accelerated, over the eight to nine years a typical stream runs off.

Figure 2. The deferral in one picture. A sale recognises the whole amount in year one; a loan spreads it across the life of the stream, for the same total tax and a lower present value.

When the seller prefers the sale

A development-stage company with large net operating losses may prefer a sale, to recognise the income in a year where expiring losses absorb it. Tax authorities have challenged this. In Hydrometals a taxpayer documented a sale of future receivables to accelerate income, and the court, finding repayment effectively guaranteed, recharacterised it as a loan. The tax preference depends on whether the seller has income to defer or losses to use.

The tax test is its own test

The tax sale-or-loan question is not the bankruptcy true-sale question, and the two can reach different results on the same deal.

The tax test is a substance-over-form inquiry. Under Frank Lyon, the paper does not control when the economics point elsewhere. Under Geftman, the question is whether there was an unconditional obligation to repay and an unconditional intention to enforce it. Where intent is not stated, it is inferred from where the risk sits.

- If the financier's return depends on whether the drug sells, the risk has shifted and it is a sale.

- If the seller has effectively guaranteed the return, the risk has not shifted and it is a loan.

The features that shift risk to the buyer, non-recourse and no floor and no make-whole, produce a clean true sale and forfeit the deferral. The features that keep risk with the seller, recourse and a floor and a make-whole, support the loan characterisation. Those loan-like features are the same terms that dominate the synthetic and development-stage end of the market, quantified in the structuring analysis. The minimum guarantee and the make-whole are, among other things, the levers that move the tax result onto the debt side.

How the treatment appears in filings

The characterisation is disclosed. Live filings sit at four points on the spectrum.

Documented as a loan

Progenics Pharmaceuticals monetised its RELISTOR royalty through a wholly owned subsidiary that entered a royalty-backed loan with a HealthCare Royalty Partners fund. The terms are those of debt: a stated principal of up to 100 million dollars, a 9.5 percent interest rate, a stated maturity, and repayment from the RELISTOR royalties. The lender's recourse is limited to those royalties, so the structure is non-recourse debt held in a bankruptcy-remote subsidiary, recorded with a debt discount amortised on the effective interest method.

Documented as a sale but taxed as debt

Phathom Pharmaceuticals, in its revenue interest financing, has the parties agree that for tax purposes the advances are treated as indebtedness and as contingent payment debt instruments under Treasury Regulation 1.1275-4(b), with the royalty payments applied pro rata across the separate debt instruments. The agreement is a financing that produces royalty-based payments, and the tax covenant fixes the debt characterisation and the regime that governs it.

Booked as a liability for accounting

A large group of sellers records the monetisation as a liability related to the sale of future royalties, accreted on the effective interest method:

- Minerva Neurosciences treats its Royalty Pharma monetisation as a debt financing because it retained continuing involvement and the buyer has recourse, at an effective rate near 10.7 percent, with the cash not repayable if the drug is discontinued.

- Clearside Biomedical cites ASC 470-10 for debt and ASC 835-30 for imputation of interest.

- Alnylam records its Leqvio monetisation as a debt financing.

- Xencor does the same for royalties sold to OMERS.

- AnaptysBio treats its Jemperli and Zejula royalty monetisations as debt.

The accounting liability is driven by continuing involvement, which is a different and lower bar than the tax risk-shift test. Many royalty sales that appear as debt on the balance sheet are sales for tax. The liability line reports the accounting answer, not the tax answer. The seller seeking deferral needs the tax result to be a loan on its own terms, through recourse and a floor and a make-whole, not merely a liability on the accounts.

Non-recourse notes through an SPV

BioCryst monetised its RAPIACTA royalties from Shionogi by transferring them under a purchase and sale agreement to a wholly owned subsidiary, JPR Royalty Sub LLC, which issued non-recourse notes with an interest reserve account and a currency hedge. This is the securitisation format: the notes are debt at the subsidiary, and the royalty is isolated in the vehicle.

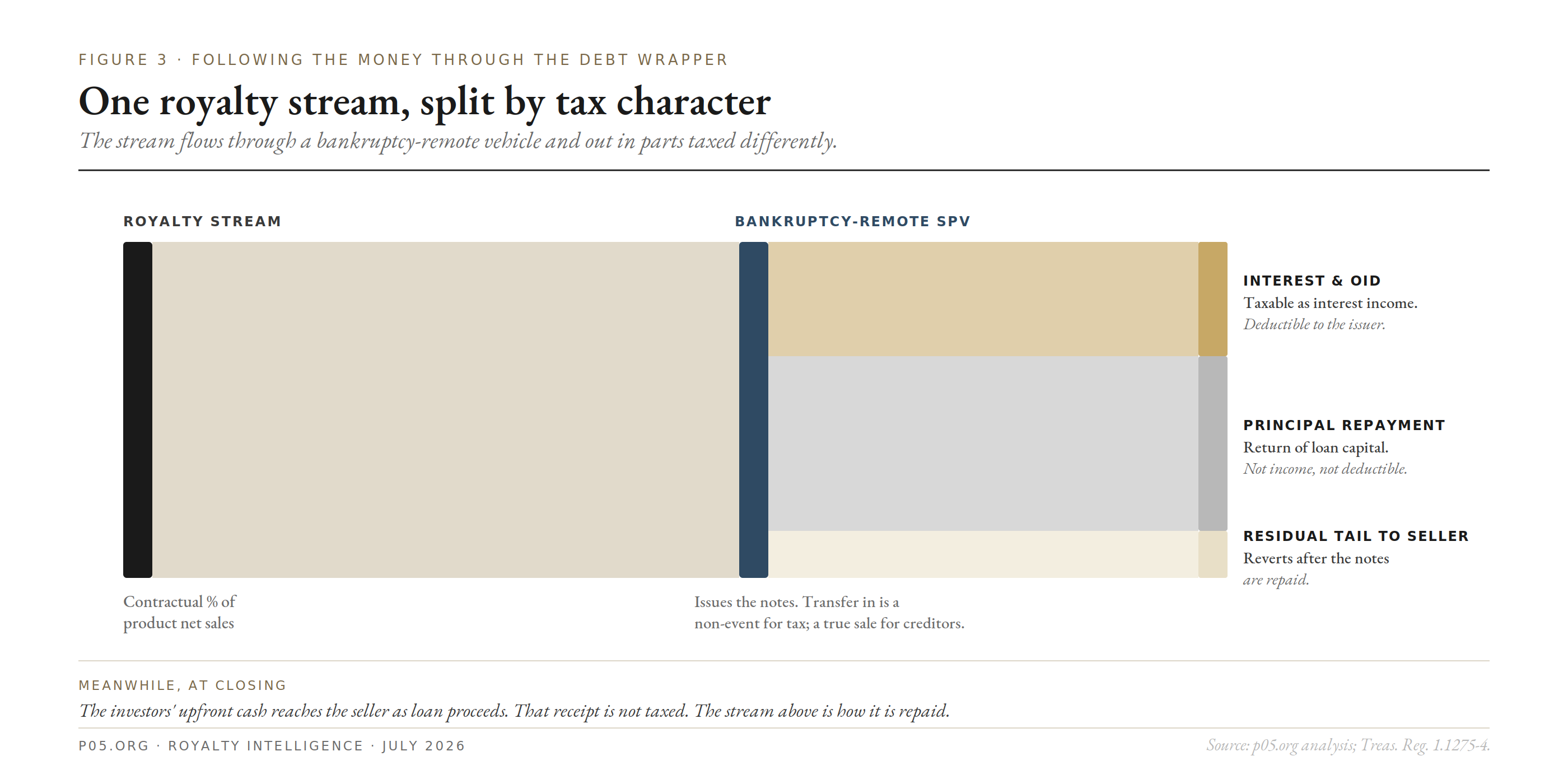

The special purpose vehicle separates the tests

The SPV is what lets a deal reach different answers on the different tests at once.

The seller transfers the royalty into a wholly owned vehicle, and the vehicle issues notes to the investors. Toward the seller's creditors, the transfer can be a true sale that isolates the asset. Toward the tax system, the vehicle is usually disregarded or consolidated, so the transfer is a non-event.

The only transaction tax law sees is the vehicle issuing debt for cash. Debt issued for cash is a borrowing, and the proceeds are not income. The bankruptcy isolation and the tax deferral both survive because two bodies of law are looking at two different steps.

The Progenics and BioCryst structures above are both built this way. The bond and note formats are catalogued in the royalty bonds piece.

Figure 3. Following the money through the debt wrapper. The stream passes through a bankruptcy-remote vehicle and out in parts taxed as interest, principal, and residual.

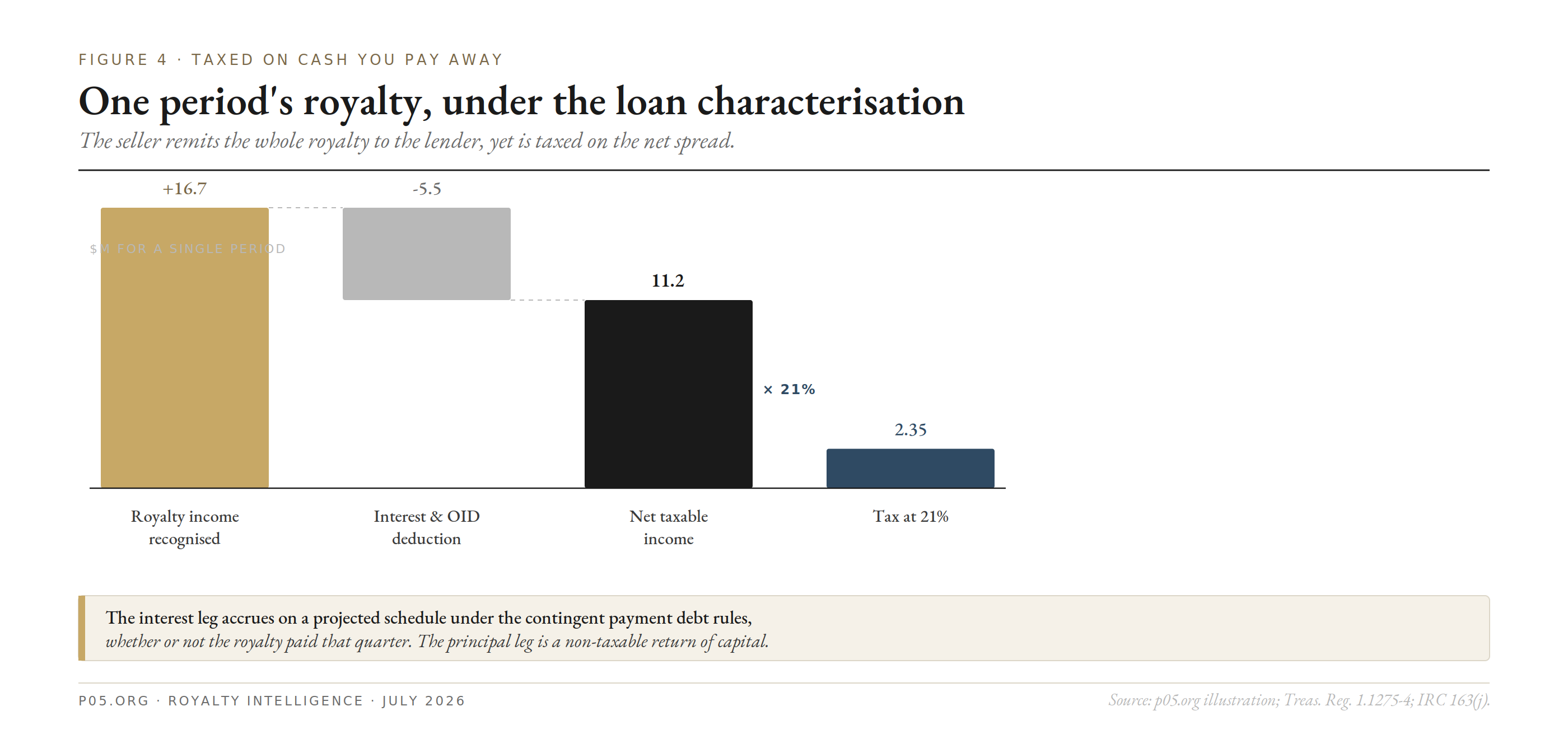

Contingent payment debt instrument rules

Once the instrument is debt, the payments are still contingent, because they track drug sales. Contingent payments on a debt instrument are governed by Treasury Regulation 1.1275-4. This is the regime the Phathom covenant selects, and it runs the noncontingent bond method, set out by the IRS in Revenue Ruling 2002-31.

The method has four steps.

- Comparable yield. The issuer sets the rate at which it could issue a fixed-rate instrument on similar terms, no lower than the applicable federal rate.

- Projected payment schedule. A full schedule of assumed payments, contingent ones included, is built to produce that yield.

- Accrual. Interest accrues on the projected schedule as original issue discount, regardless of cash paid in the period.

- Adjustment. When the actual royalty differs from the projection, a positive or negative adjustment trues up the difference.

The same mechanics appear in standard structured-note disclosure, where issuers accrue original issue discount under the noncontingent bond method using the comparable yield and the adjusted issue price.

Two consequences follow for a royalty deal:

- The deferral is smoothed, not open-ended. Both sides accrue on the projected schedule whether or not the royalty paid that quarter, so income and deductions follow a modelled yield rather than the actual stream.

- Character is interest. Gain on a sale, exchange, or retirement of the instrument is generally treated as interest income, not capital gain.

Figure 4. Taxed on cash paid away. Royalty income recognised, less the interest and OID deduction, equals the net taxable spread, taxed at 21 percent.

Interest deductibility under Section 163(j)

The seller's deferral depends on deducting the interest and OID that offset the royalty income it keeps recognising. Section 163(j) caps the business interest deduction at 30 percent of adjusted taxable income.

The One Big Beautiful Bill Act, signed 4 July 2025, made two relevant changes:

- It restored the EBITDA-based measure of adjusted taxable income permanently, for tax years beginning after the end of 2024, which raises the deductible-interest ceiling.

- For tax years beginning after the end of 2025, it removes certain foreign income items from the base and brings capitalised interest within the limitation.

The corporate rate remains 21 percent, and companies under roughly 31 million dollars of average gross receipts are exempt.

For a profitable holder this is usually not a constraint, because the royalty income lifts adjusted taxable income enough to absorb the matching interest. For a loss company it is: adjusted taxable income is low, the interest is disallowed and carried forward, and the deferral becomes phantom income with a deduction that may go unused. This is the same profile that makes a loss company prefer a sale.

Cross-border: the portfolio interest exemption

The treaty and fund-domicile side of cross-border royalty taxation is covered in the fund architecture and cross-border transaction pieces, including treaty withholding rates, the EU Interest and Royalties Directive, Pillar Two, and anti-hybrid rules. One point specific to the debt characterisation belongs here: the United States portfolio interest exemption, which is a statutory route separate from any treaty.

The baseline

United States source income paid to a foreign person is subject to a 30 percent withholding tax under Sections 871 and 881, collected at source. This applies to both royalties and interest, so the label alone does not reduce the rate.

The exemption, and its limit

The portfolio interest exemption in Sections 871(h) and 881(c) removes the withholding tax on interest paid to a foreign lender, without a treaty, if the debt is in registered form, the lender is not a bank lending in the ordinary course, and the lender is under the 10 percent voting-ownership threshold and outside the related-party rules.

The limit is decisive for a royalty. Portfolio interest does not include contingent interest, meaning interest determined by reference to the borrower's receipts, sales, income, or profits. A straight royalty pass-through is contingent interest, and is returned to the 30 percent net. The exemption reaches only the fixed, non-contingent part of the return.

The practical result: to use the exemption, the deal needs a fixed coupon or a minimum guarantee. That is the same floor that supported the debt characterisation for the seller, now also doing the withholding work. The contingent tail above the floor gets no relief from the portfolio rules and depends on a treaty instead.

Current-law notes

- A proposed Section 899, which would have raised withholding on investors from certain jurisdictions, was dropped from the final 2025 law.

- BEAT was set permanently at 10.5 percent, relevant to large groups with deductible cross-border payments.

Reading the four fingerprints

Each characterisation leaves a different trace in the documents.

| Regime | Where it appears | What to look for |

|---|---|---|

| Accounting | Financial statements | Liability related to sale of future royalties, effective interest, ASC 470-10 and 835-30 |

| Tax | Risk factors, tax covenant | Intent to treat as indebtedness, contingent payment debt instrument, 1.1275-4 |

| Bankruptcy | Closing set | Remote SPV, non-consolidation and true-sale opinions |

| Commercial | Deal terms | Floor, cap, make-whole, recourse |

All four can appear in one deal. The seller seeking deferral needs the tax fingerprint to read loan, and builds the recourse and floor to get there, accepting the drag those features put on the true-sale opinion.

Diligence checklist

Seller

- Is deferral useful, or do losses make a sale the better answer?

- Is enough risk retained, through recourse, a floor, or a make-whole, to support the loan characterisation?

- Will the interest and OID survive Section 163(j)? For a loss company they may not.

- Is the seller prepared to accrue royalty income for years on cash it pays away, on a projected schedule?

Financier

- Is the return interest or royalty income, and does the noncontingent bond method change the timing of what is booked?

- For a tax-exempt or foreign holder, does the characterisation create UBTI, or withholding the portfolio interest exemption will not cover because the return is contingent?

- Is the fixed leg genuinely non-contingent and in registered form, and is the holder inside the 10 percent voting threshold?

- Does the eventual exit get sale treatment, and is the after-tax return modelled rather than the multiple?

Cross-border

- Which part of the return is fixed and which is contingent, and therefore which part the 30 percent withholding reaches?

- Does a treaty do better than the portfolio interest exemption for the holder's residence?

- Does the instrument create a hybrid mismatch that anti-hybrid rules would attack?

The contract label does not determine the tax result. A royalty monetisation can be a sale on its face, a liability on the balance sheet, a true sale in bankruptcy, and a loan in its economics, and only the tax characterisation moves the current-year bill.

The seller seeking deferral is choosing the loan answer to the tax question, and paying for it with the recourse and floor that make the other answers harder to give. The pre-funded warrant is the equity-side version of the same pattern: one instrument, counted differently by different rulebooks.

All information in this article was accurate as of July 2026 and is derived from publicly available sources including SEC filings, the Internal Revenue Code and Treasury Regulations, IRS guidance, court opinions, accounting standards, law-firm practice notes, and financial news reporting. It reflects the tax law as amended by the One Big Beautiful Bill Act of July 2025. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, accounting, tax, or financial advice. The author is not a lawyer, accountant, tax adviser, or financial adviser.