Data Room Standards for Royalty Transactions: What Buyers Diligence First, and the Red Flags That Kill Deals

A royalty stream is only as good as the documents that prove it. The data room is where a buyer decides whether the cashflow it is being shown is real, durable, transferable, and unencumbered.

Get the room right and a deal closes in weeks. Get it wrong and the buyer either walks or reprices, because a disorganized room reads as a disorganized asset. The documents are the asset; everything else is narrative.

This piece sets out what a best-practice royalty data room contains, at the document level, the order in which buyers actually open the folders, the representations a buyer expects the seller to stand behind, and the findings that end a process before it starts.

What the room is buying

A royalty buyer is not buying a company. It is buying a contractual right to a slice of someone else's product sales, for a defined period, subject to a patent estate it does not control and a payer it cannot direct.

That narrows diligence to five questions, and the whole room exists to answer them:

- Is the cashflow real? Payment history, audit results, net-sales reporting.

- Will it last? Patent expiry, generic or biosimilar entry, the commercial trajectory.

- Can it be transferred? Anti-assignment and consent terms in the underlying licence.

- Is the title clean? Lien searches, the assignment chain, prior monetizations.

- What can break it? Termination rights, set-off, litigation, covenant breaches.

Royalty funds concentrate on commercial-stage products precisely because these questions are answerable from documents rather than forecasts. Funds focus on commercial-stage assets, with earlier-stage exposure taken through development funding or only where strong clinical data has de-risked the asset.

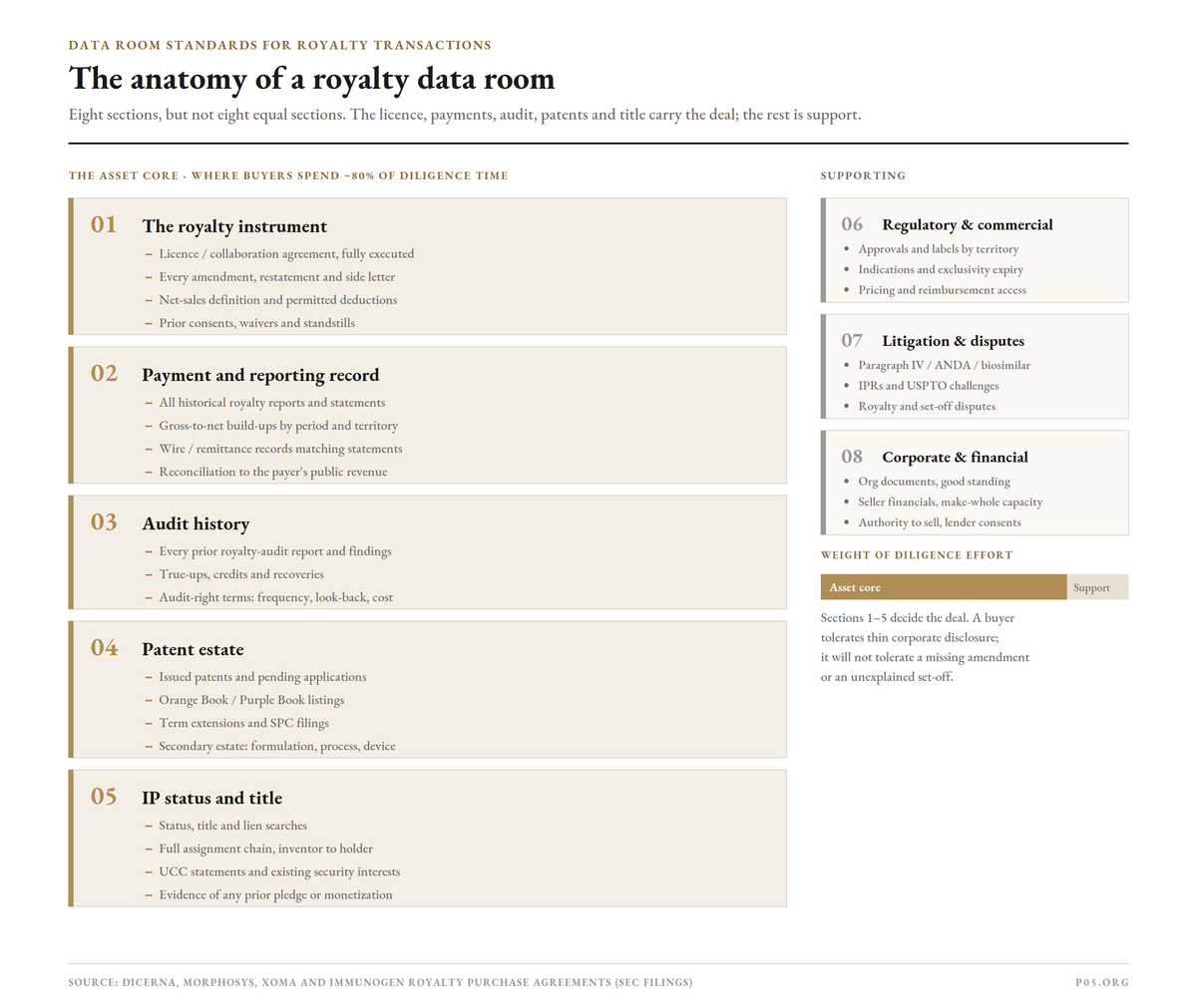

What a best-practice room contains

A royalty room is organized around the asset, not the company. The corporate and financial baseline still has to be there, but the centre of gravity is the licence, the patents, and the payment record. The detail below is the document-level contents a sophisticated buyer expects to find, not the folder headings.

1. The royalty instrument

The contract is the asset. The room must hold the complete chain, not just the base document:

- The license or collaboration agreement, fully executed.

- Every amendment, restatement, and side letter, in chronological order.

- Any prior consent, waiver, or standstill granted under the agreement.

- The full defined-terms set, especially the net-sales definition.

The single most consequential document in the room is the net-sales definition, because it sets what the royalty is actually calculated on. A buyer reads it for the permitted deductions: chargebacks, rebates, returns, cash and quantity discounts, and pricing adjustments, and for any contractual cap on total deductions. A missing amendment here is fatal, because the payer's real obligation often lives in an amendment, exactly the situation in Royalty Pharma's litigation with Boehringer, where a 2015 amendment rewrote the payment trigger.

2. The payment and reporting record

This is where the buyer tests whether the cashflow exists as described:

- Every historical royalty report and royalty statement from the payer.

- Net-sales build-ups showing gross-to-net, by period and ideally by territory.

- Wire confirmations or remittance records matching the statements.

- Reconciliations of reported sales to the payer's public revenue disclosure.

A best-practice room delivers what the agreements call the "Related Documents": all royalty reports and all material communications and notices between the seller and the payer, and with any governmental entity, relating to the product or the royalty.

3. Audit history

Underreporting and underpayment are common, and not always fraud; ambiguous contract language produces honest errors:

- Every prior royalty-audit report, with findings and methodology.

- Records of any true-up payment, credit, or recovery.

- The status of audit rights: how often, how far back, who bears the cost.

A clean audit history reassures. A history of true-ups, a live dispute, or no audit ever conducted is a flag. The relevant reps in modern agreements confirm whether any audit has been initiated and whether any set-off or reduction is outstanding.

4. The patent estate

The patents set the buyer's return horizon:

- Every issued patent and pending application covering the product.

- Orange Book listings for small molecules; Purple Book entries for biologics.

- Patent term extension and supplementary protection certificate filings.

- The secondary estate: formulation, process, polymorph, and device patents.

The headline composition-of-matter expiry is rarely the operative date. The secondary estate sets the true market window, as the 100-plus-patent Humira thicket showed.

5. IP status and title

A stream with broken title cannot be delivered clean:

- Status, title, and lien searches for every relevant patent.

- The full assignment chain from inventor to current holder.

- UCC financing statements and any existing security interests.

- Evidence of any prior monetization or pledge of the same stream.

Buyers run status, title, and lien searches precisely to catch a prior pledge or a break in the chain.

6. Regulatory and commercial

The product has to be on the market and protected:

- Marketing approvals and approval letters by territory.

- Current labels, approved indications, and any label expansions.

- Regulatory exclusivity periods and their expiry.

- Pricing, reimbursement, and any payer-access constraints in key markets.

7. Litigation and disputes

The buyer needs to know what is actively contested:

- Paragraph IV certifications and ANDA or biosimilar filings.

- Inter partes reviews and other USPTO challenges.

- Infringement suits, both offensive and defensive.

- Any dispute over the royalty itself, including set-off claims.

8. Corporate and financial

The supporting layer, secondary but still required:

- Organizational documents and good-standing certificates.

- The seller's own financials, sufficient to assess solvency and make-whole capacity.

- The seller's authority to sell, including board and, where relevant, lender consents.

The defining feature of a royalty room, versus a generic M&A room, is that sections 1 through 5 carry almost all the weight. A buyer can live with thin corporate disclosure. It cannot live with a missing licence amendment or an unexplained set-off.

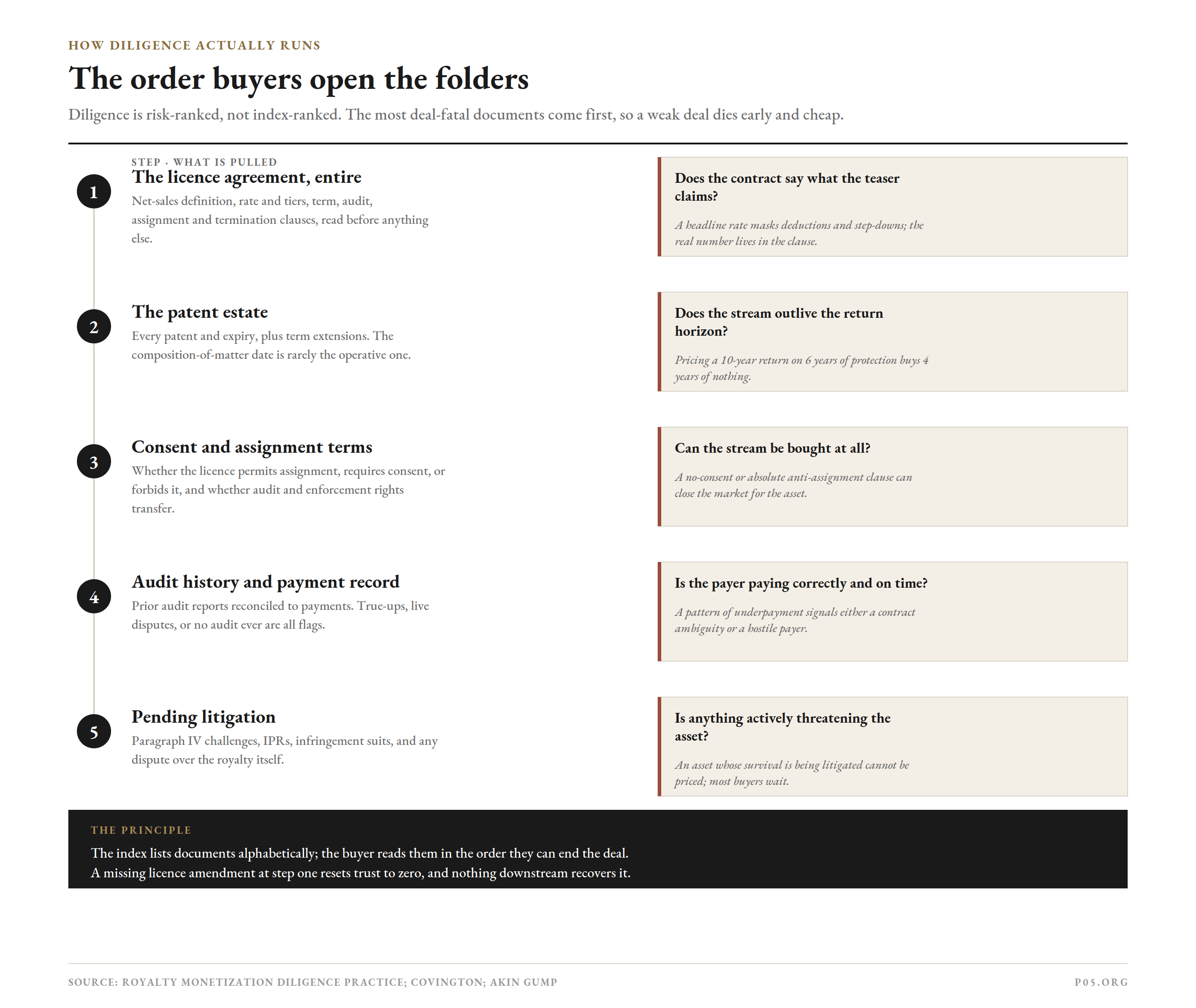

The order buyers actually open the folders

Diligence is sequential, and the sequence is risk-ranked. A buyer kills a weak deal as cheaply and as early as possible, which means the most deal-fatal documents are opened first. The real order is not the index order.

| Order | What is pulled first | The kill question |

|---|---|---|

| 1 | The license agreement, in full, with every amendment | Does the contract say what the teaser claims |

| 2 | The patent estate and expiry dates | Does the stream outlive the buyer's return horizon |

| 3 | Anti-assignment and consent terms | Can the stream be bought at all without the licensee |

| 4 | Audit history and payment record | Is the payer paying correctly and on time |

| 5 | Pending litigation and Paragraph IV status | Is anything actively threatening the patent or payment |

The license agreement, first and entire. Everything flows from the contract. The buyer reads the net-sales definition, the rate and tiers, the term, the audit clause, and the assignment and termination provisions before anything else. A teaser quotes a headline rate; the contract reveals the deductions, the step-downs, and the carve-outs that determine the real number.

The patent estate, second. The buyer sets its return horizon by the patents, mapping every patent and the original expiry plus any term extension, then the realistic window before generic or biosimilar entry.

Consent and assignment, third. A stream that cannot be transferred is not for sale. The buyer checks whether the licence permits assignment, requires consent, or prohibits it, and whether the assigned rights include the audit, enforcement, and consent rights it needs, not just the bare right to receive cash.

Audit history and payment record, fourth. Now the buyer tests whether the cashflow is real, reading prior audit reports and reconciling reported sales to payments. Underreporting is not uncommon and is not always fraud.

Litigation, fifth. Finally the buyer checks what is actively threatening the asset. Pending patent challenges make a royalty transaction very hard to complete, because an asset whose survival is being litigated cannot be priced.

The representations the documents must support

A buyer does not just read the room; it asks the seller to stand behind it. The representations in a royalty purchase agreement are the contractual mirror of the data room, and the disclosure schedules are where every exception must be listed. An undisclosed exception that surfaces later is a breach.

Five representations matter most, and each maps to a folder the buyer has already read.

| Representation | What the seller affirms | The document that proves it |

|---|---|---|

| No set-off | The royalty is not subject to any set-off or reduction, and no event exists that would permit one | Royalty reports, payer correspondence |

| No undisclosed audit | No audit is pending and no findings are outstanding | Audit history |

| No infringement notice | No notice of infringement has passed between seller and payer | Litigation file, payer correspondence |

| Clean title | The seller owns the stream free of liens, and its legal name and UCC position are as stated | Lien searches, assignment chain |

| Complete documents | All royalty reports and material communications have been delivered | The Related Documents set |

The set-off representation is the one buyers probe hardest. Modern agreements pair it with a make-whole: if the payer effects a set-off that is not a permitted reduction, the seller must true up the buyer so the buyer receives the full amount it was owed. That mechanic only works if the seller is solvent, which is why the corporate financials in section 8 still matter.

Where the buyer wants maximum comfort, it asks for a direct acknowledgement from the payer, an estoppel or consent letter confirming the amount owed, the absence of set-off, and the direction of future payments. That letter is the bridge between the seller's representations and the payer's actual conduct.

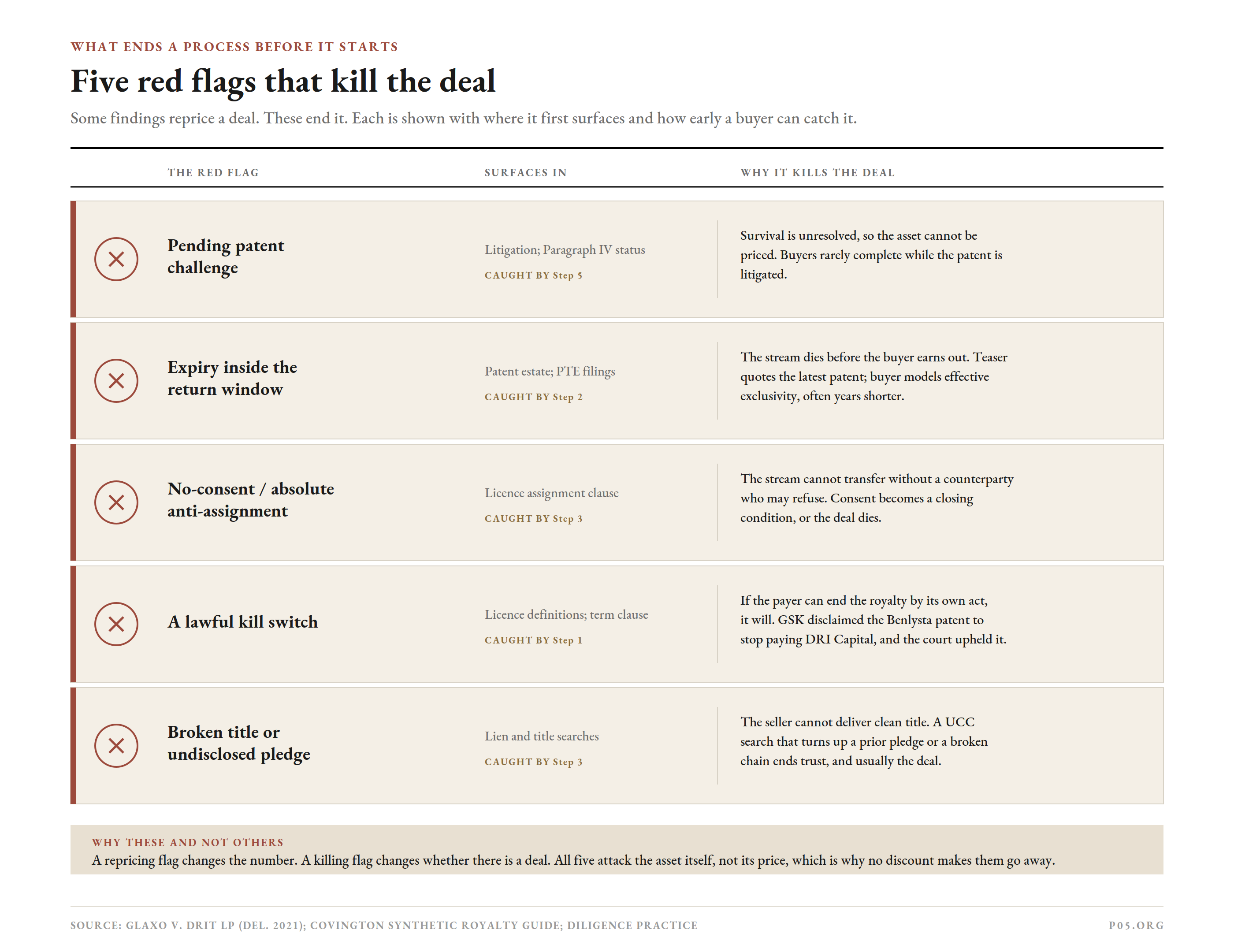

The red flags that kill deals

Some findings reprice a deal. Others end it. The deal-killers cluster in five places, and an experienced buyer can spot most of them in the first week.

| Red flag | Where it surfaces | Why it kills the deal |

|---|---|---|

| Pending patent challenge | Litigation, Paragraph IV status | The asset's survival is unresolved; it cannot be priced |

| Patent expiry inside the return window | Patent estate, PTE filings | The stream dies before the buyer earns its return |

| No-consent or absolute anti-assignment | License assignment clause | The stream cannot be transferred without a counterparty who may refuse |

| Disclaimer or termination kill switch | License definitions, term clause | The payer can lawfully end the royalty, as GSK did to DRI Capital |

| Broken title or undisclosed pledge | Lien and title searches | The seller cannot deliver clean, unencumbered title |

Three deserve detail.

The patent that expires too soon. A buyer pricing a ten-year return on a stream protected for six years is buying four years of nothing. This is the most common quiet killer, because the teaser quotes the latest secondary-patent expiry while the buyer models the effective market exclusivity, which averages 11 to 12 years post-approval for a small molecule, not the nominal patent life. The gap between the two is where deals die.

The disclaimer kill switch. If the royalty term ends when a "Valid Claim" disappears, and the contract lets the payer's own voluntary disclaimer count as the end of validity, the payer holds a lawful off switch. GSK disclaimed the Benlysta patent in 2015 to stop paying DRI Capital, and the Delaware Supreme Court held the disclaimer was a permitted contractual right. A buyer who finds this structure and no carve-out against voluntary disclaimer should expect to lose the stream the same way.

Broken title or a prior pledge. Post-Mallinckrodt, most synthetic royalty and development financings now require security over the IP, which makes clean, unencumbered title non-negotiable. A UCC search that turns up an undisclosed lien ends trust, and usually the deal.

What sellers should do before opening the room

The seller controls the single biggest variable in execution speed: room readiness. A buyer reads a clean room as a clean asset.

Five preparation steps separate a fast close from a stalled one:

- Assemble the complete licence chain. Base agreement plus every amendment, side letter, and consent, in one place. A missing amendment found mid-diligence resets buyer trust to zero.

- Clean the patent file. Confirm patents are properly assigned and not subject to challenge, and run your own lien search before the buyer runs theirs.

- Commission a pre-sale royalty audit. A recent clean audit, run by a recognized firm, pre-empts the buyer's biggest question about whether the cashflow is real.

- Map the consent path. Know whether the payer's consent is needed and how it will be obtained, so it can be presented as a manageable closing condition, not an open risk.

- Disclose the kill switches yourself. Surface disclaimer rights, termination triggers, set-off exposure, and change-of-control provisions up front. A buyer who finds them itself assumes there is more hidden.

The economics of preparation are simple. Every gap the buyer finds becomes either a price reduction or a reason to walk. Every gap the seller closes in advance is value retained.

The verdict

A royalty data room is a proof, not a pitch. It exists to convince a buyer that the cashflow is real, durable, transferable, and unencumbered, and it does so with documents, in that order of importance.

The room is organized around the asset. The licence, the patents, and the payment record carry the weight; corporate disclosure is secondary. Buyers open the folders in risk order, the contract and the patent expiry first, because that is where deals die fastest and cheapest. And the seller is asked to stand behind the room through representations, every exception to which must be disclosed in the schedules.

The deal-killers are consistent: a pending patent challenge, an expiry inside the return window, an untransferable stream, a lawful kill switch the seller drafted in, or a broken title. Most are visible in the first week to a buyer who knows where to look.

For sellers the conclusion follows directly. The value of a royalty stream is set partly by the asset and partly by how cleanly it is documented. The work of assembling the licence chain, cleaning the patent file, commissioning the audit, and surfacing the kill switches is not administrative. It is the difference between the price on the teaser and the price at close.

This article reflects publicly available information as of June 2026. It does not constitute investment, legal, or tax advice. The standards and mechanics described are derived from SEC filings, royalty purchase agreements, reported judicial decisions, and published legal and transactional analysis. Sellers, buyers, and counsel preparing or diligencing a specific royalty transaction should rely on the underlying contracts, the governing law of the relevant jurisdiction, and qualified counsel. The author is not a lawyer or financial adviser.