The Weekly Term Sheet (2026-W23)

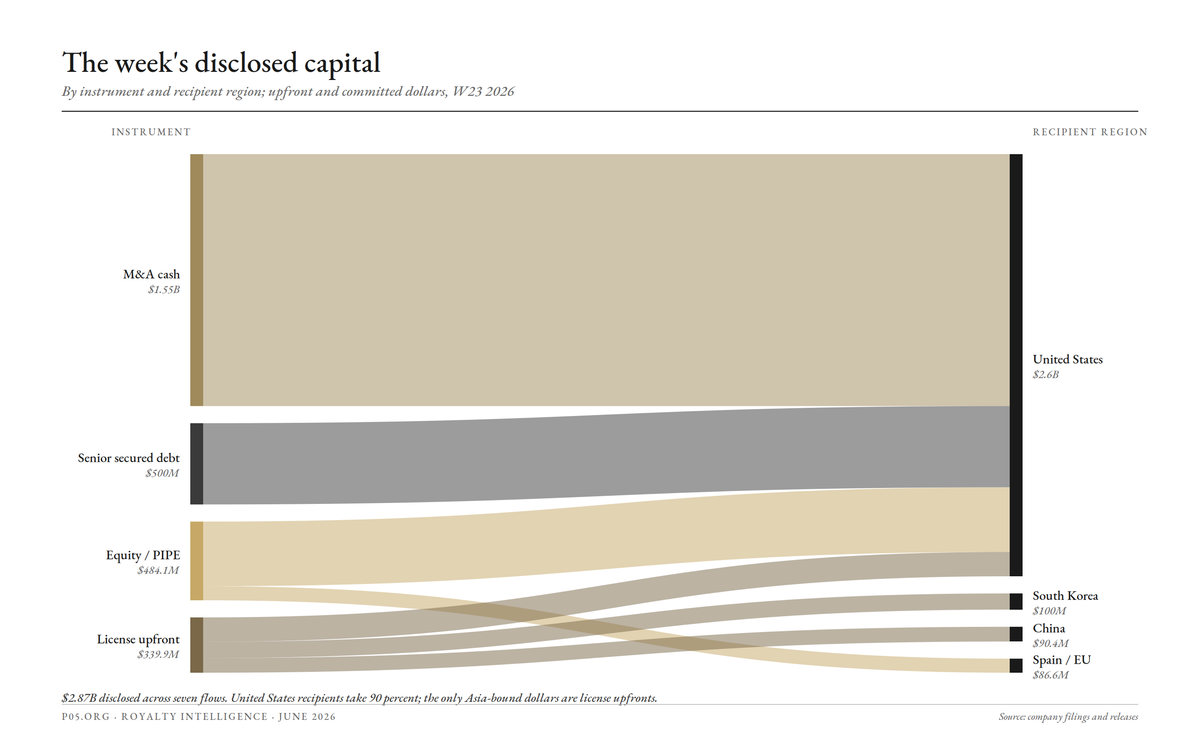

The week in numbers

Disclosed cash and committed capital first. The milestone-inclusive "up to" ceilings are noted second, not led with: where an upfront or a committed amount is disclosed, that is the number to anchor on.

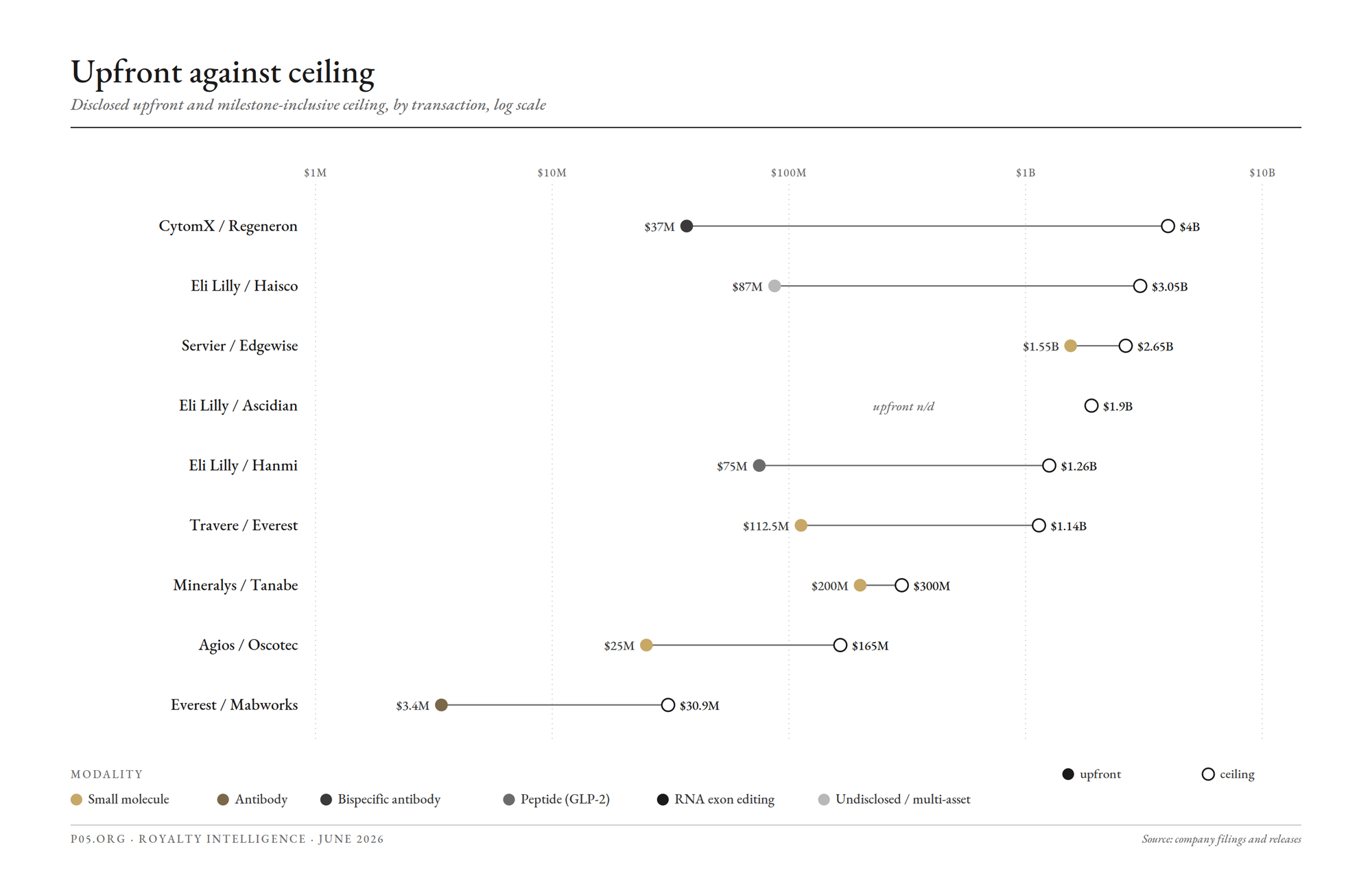

- $1.55B upfront cash: Servier to Edgewise for the muscular dystrophy business and sevasemten. Ceiling up to $2.65B with milestones; a divestiture, no retained royalty.

- $500M committed debt, plus $200M upfront cash: Mineralys financing package (June 3). A $500M Pharmakon senior secured term loan ($100M funded at closing) and a ~$150M equity raise fund a $200M upfront, up to $300M with milestones, repurchase of the Tanabe royalty on lorundrostat. The window's only royalty extinguishment, and a BioPharma Credit debt origination.

- Up to $1.9B ceiling, undisclosed upfront: Ascidian to Eli Lilly for RNA exon editing in monogenic kidney disease, plus tiered royalties to Ascidian. The window's third Lilly external-sourcing license and a US-origin royalty-bearing platform deal.

- $215M committed: Rallybio / Avenzo concurrent private placement, alongside the reverse merger that takes Avenzo public; pre-closing Rallybio holders receive contingent value rights on the legacy REV102 disposition.

- $112.5M upfront: Travere to Everest Medicines for ex-China rights to civorebrutinib (EVER001). Ceiling up to ~$1.14B (up to ~$1.03B milestones across up to five indications), plus high-single-digit to double-digit tiered royalties to Everest. A China-outbound, royalty-bearing license.

- $86.6M raised: Ona Therapeutics Series B (June 4), the cut's largest venture round, to advance the first-in-class ADCs ONA-255 (breast) and ONA-389 (colorectal); academic (Barcelona consortium) and Biocytogen antibody-platform license layers sit beneath the lead asset.

- $75M upfront: Lilly to Hanmi for worldwide ex-Korea rights to sonefpeglutide. Ceiling up to ~$1.26B with milestones, plus post-launch royalties to Hanmi.

- Up to $87M upfront and near-term: Lilly to Haisco across up to five discovery-stage programs. Ceiling up to ~$3.05B with milestones, plus single-digit tiered royalties to Haisco. Upfront and near-term under 3% of the ceiling.

- $37M target-nomination payment: CytomX from Regeneron for two new targets in their expanded conditional-bispecific oncology collaboration. Ceiling up to ~$4B with milestones, plus tiered global net-sales royalties to CytomX; a US-origin platform-royalty origination.

- $32.5M raised: Oak Hill Bio Series A for the Angelman-syndrome ASO rugonersen, which carries an upstream Roche milestone-and-royalty layer.

- Up to RMB 209M (~$30.9M) disclosed, plus profit share: Everest Medicines to Mabworks for Asia-Pacific (ex mainland China) rights to Bejescin, an approved third-generation anti-CD20 antibody. RMB 23M (~$3.4M) upfront, up to RMB 186M (~$27.5M) in sales milestones, plus an undisclosed gross-profit share to Mabworks. Everest as licensee, the inverse of its civorebrutinib out-license the same week.

- $25M upfront: Agios to Oscotec for exclusive global rights to cevidoplenib, a next-generation oral SYK inhibitor, in immune thrombocytopenia and additional indications. Up to $140M in development and regulatory milestones across up to three indications, plus commercial milestones and high-single-digit to mid-teen tiered royalties to Oscotec; Oscotec retains a South Korea reacquisition option after Phase 3. A Korea-outbound, royalty-bearing license.

- Undisclosed terms, royalties to Lonza: Lonza to Stipple Bio for target-specific access to its Synaffix-derived ADC platform, including lead candidate STP-100. Upfront, clinical, regulatory, and commercial milestones plus royalties on net sales to Lonza. A Swiss CDMO-origin platform-royalty line.

- ~JPY 575M (~$3.7M) reported, plus an AMED grant: Periotherapia, for the anti-periostin antibody PT0101; an Osaka University academic-license layer sits beneath it.

- Upfronts undisclosed: Circio / GenAssist (AAV research collaboration, no royalty or milestone structure) and TheraPPI (pre-seed, academic-license layer); neither carries a disclosed figure.

- No new capital: the daraxonrasib (Royalty Pharma), ivonescimab (Akeso), sac-TMT (Kelun), frontMIND tafasitamab (Xencor, OMERS-held portion), ZYNLONTA LOTIS-5 (HealthCare Royalty), and Innovent IBI343 (Innovent's ex-China royalty under the Takeda license) readouts re-rate existing royalty paper without new money; the J&J PROTEUS apalutamide plenary touches only a UC Regents academic layer, with no aggregator royalty on Erleada (the Royalty Pharma UCLA royalty is on Xtandi, not Erleada). Regulatory items (Xocova, giredestrant) and the EMERALD-3, SERENA-6, and InnoCare orelabrutinib SLE readouts are logged as backdrop.

M&A and major licensing:

- Servier / Edgewise muscular dystrophy business acquisition (Mon June 1): $1.55B upfront cash, up to $2.65B with milestones; outright divestiture of sevasemten and the muscular dystrophy business, no retained royalty; closing targeted Q3 2026 subject to HSR clearance (see M&A and Restructuring)

- Mineralys / Tanabe lorundrostat royalty repurchase plus Pharmakon term loan (Wed June 3): $200M upfront, up to $300M with milestones, to extinguish the Tanabe royalty on lorundrostat and acquire the IP; funded by a $500M Pharmakon senior secured term loan ($100M first tranche) and a ~$150M equity raise. A royalty extinguishment, not an aggregator purchase (see M&A and Restructuring)

- Eli Lilly / Haisco research and licensing collaboration (announced Fri May 29; PR Newswire Mon June 1): up to ~$3.05B (up to $87M upfront and near-term plus up to $2,967M milestones plus single-digit tiered royalties), up to five Haisco-discovered programs, Greater China retained by Haisco (see BD Origination and Licensing)

- Eli Lilly / Hanmi sonefpeglutide license (Mon June 1): up to ~$1.26B ($75M upfront plus up to $1.185B milestones plus post-launch royalties), worldwide ex-Korea rights to the LAPSGLP-2 analog (see BD Origination and Licensing)

- Travere / Everest Medicines civorebrutinib (EVER001) license (entered Mon June 1; announced Tue June 2): up to ~$1.14B ($112.5M upfront plus up to ~$1.03B milestones across up to five indications plus high-single-digit to double-digit tiered royalties to Everest), ex-China rights to the oral covalent-reversible BTK inhibitor; subject to HSR clearance (see BD Origination and Licensing)

- Eli Lilly / Ascidian RNA exon-editing collaboration (Wed June 3): up to ~$1.9B (undisclosed upfront plus development and commercial milestones plus tiered royalties to Ascidian), exclusive target-specific rights to Ascidian's RNA exon-editing platform in monogenic kidney disease; third Lilly Asia-and-US external-sourcing license of the window (see BD Origination and Licensing)

- CytomX / Regeneron expanded conditional-bispecific collaboration (Wed June 3): $37M target-nomination payment for two new targets, up to ~$4B with milestones, plus tiered global net-sales royalties to CytomX; Regeneron funds development and commercialisation; a US-origin platform-royalty origination (see BD Origination and Licensing)

- Agios / Oscotec cevidoplenib license (Mon June 1): $25M upfront plus up to $140M development and regulatory milestones across up to three indications plus commercial milestones plus high-single-digit to mid-teen tiered royalties to Oscotec, exclusive global rights to the next-generation oral SYK inhibitor, with a South Korea reacquisition option to Oscotec after Phase 3; a Korea-outbound royalty-bearing in-license (see BD Origination and Licensing)

- Rallybio / Avenzo reverse merger plus $215M private placement (Sun May 31): Avenzo goes public into the Rallybio shell (renamed Avenzo, ticker AVZO); CVRs on the legacy REV102 disposition; a corporate combination, not a royalty origination (see M&A and Restructuring)

Royalty-bearing license-outs and academic layers (upfront + milestones + tiered royalties):

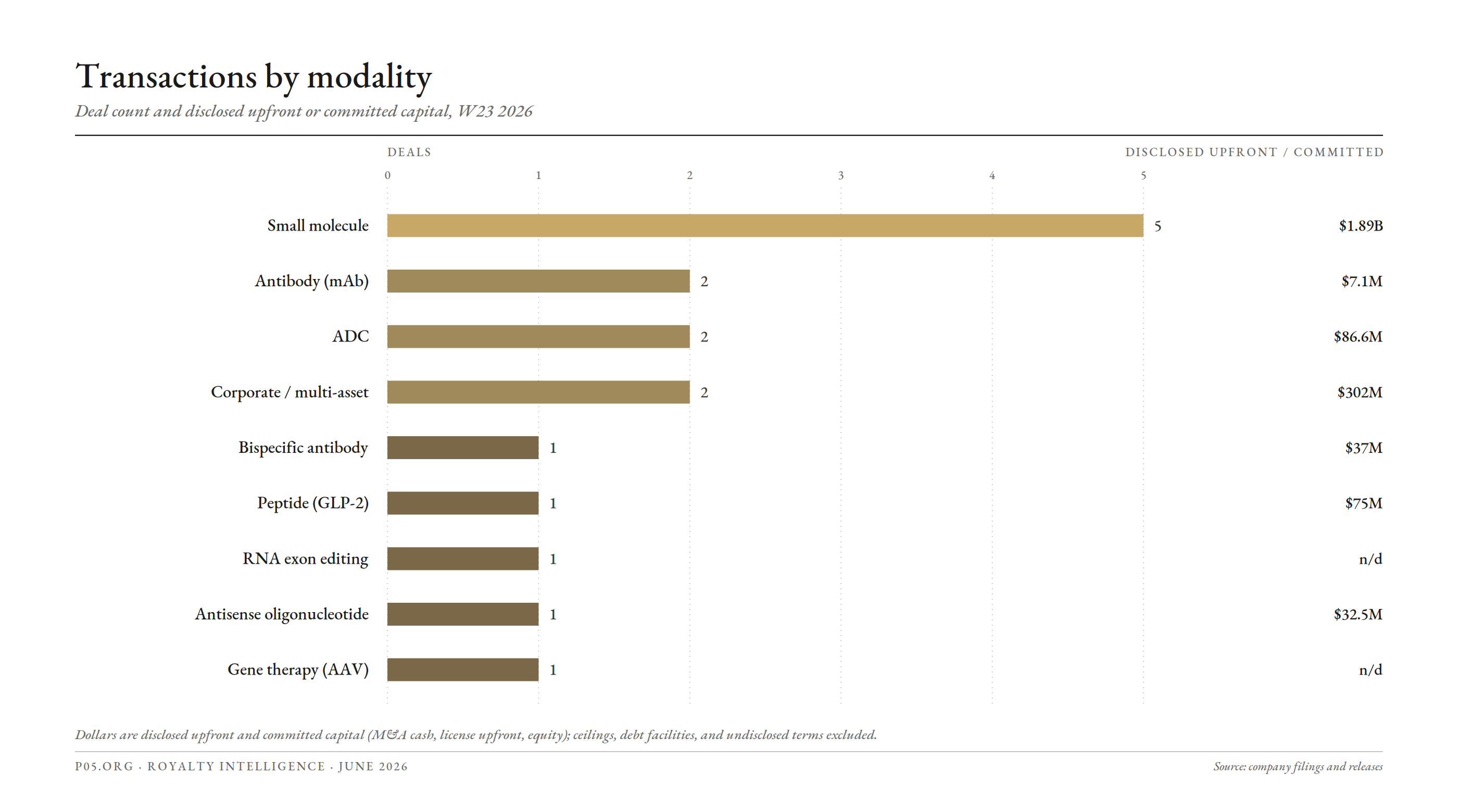

- Eight royalty-bearing license-outs in the cut. The three Eli Lilly licenses (Hanmi, Haisco, Ascidian) each carry tiered royalties to the originator: Hanmi (Korea) and Haisco (China) are Asia-outbound, Ascidian (Boston) is a US-origin platform license (Eli Lilly / Ascidian, Wed June 3: undisclosed upfront, up to ~$1.9B with milestones, plus tiered royalties on worldwide sales to Ascidian). Travere / Everest civorebrutinib (Tue June 2) is China-outbound: $112.5M upfront, up to ~$1.14B with milestones, plus high-single-digit to double-digit royalties to China-origin Everest. CytomX / Regeneron (Wed June 3) is a US-origin platform expansion: $37M nomination payment, up to ~$4B with milestones, plus tiered global net-sales royalties to CytomX (see BD Origination and Licensing). Three June 4 additions and one June 1 addition complete the set: Lonza / Stipple Bio is a Swiss CDMO-origin ADC platform license (undisclosed terms, milestones plus net-sales royalties to Lonza), Everest / Mabworks Bejescin is an Asia-Pacific in-license of an approved anti-CD20 antibody (up to RMB 209M, ~$30.9M, plus an undisclosed gross-profit share to Mabworks), and Agios / Oscotec cevidoplenib (Mon June 1) is a Korea-outbound in-license of an oral SYK inhibitor ($25M upfront, up to $140M development and regulatory milestones plus commercial milestones, plus high-single-digit to mid-teen royalties to Oscotec)

- Oak Hill Bio Series A (Mon June 1): $32.5M to advance rugonersen to Phase 3 in Angelman syndrome; an upstream Roche milestone-and-royalty layer re-activates as the asset advances (see Financings)

- Shionogi Xocova (ensitrelvir) FDA approval (Mon June 1): COVID-19 post-exposure prophylaxis approval, carrying a Hokkaido University academic-origin layer; no tradable third-party commercial royalty (see Regulatory Events)

Financings and research collaborations (undisclosed or no royalty structure):

- Circio / GenAssist AAV gene-therapy research collaboration (Mon June 1): circVec circular-RNA cassette plus liver-de-targeting AAV capsids for genetic muscle disease and in vivo CAR-T; no disclosed terms or royalty mechanics (see BD Origination and Licensing)

- TheraPPI pre-seed close (Mon June 1): a Lyon / Geneva CRCL spin-out advancing a first-in-class ERK/MyD88 inhibitor; pre-clinical, no disclosed figure, academic-license layer (see Financings)

- Periotherapia JPY 575M financing plus AMED grant (Tue June 2): an Osaka University spin-out funding the anti-periostin antibody PT0101 in Phase I/IIa; academic-license layer, no royalty structure disclosed (see Financings)

Royalty re-ratings (no new capital):

- Revolution Medicines daraxonrasib RASolute 302 plenary and NEJM (Sun May 31): OS 13.2 vs 6.7 months (HR 0.40, p<0.0001) in previously treated metastatic pancreatic cancer; de-risks the Royalty Pharma up-to-$1.25B synthetic royalty (see Clinical Readouts)

- Summit / Akeso ivonescimab HARMONi-6 plenary (Sun May 31): OS HR 0.66 (27.9 vs 23.7 months) in first-line squamous NSCLC; re-rates the Akeso ex-China royalty under Summit's up-to-$5B license (see Clinical Readouts)

- Merck / Kelun-Biotech sac-TMT OptiTROP-Lung05 (Fri May 29): PFS HR 0.35 (p<0.0001) in first-line PD-L1-positive NSCLC; re-rates the Kelun royalty under its Merck ex-China license (see Clinical Readouts)

- Incyte frontMIND tafasitamab readout (Sat May 30): 25% reduction in progression or death risk in first-line DLBCL; re-rates the Xencor royalty and its OMERS-held capped portion (see Clinical Readouts)

- ADC Therapeutics ZYNLONTA LOTIS-5 confirmatory readout (Wed June 3): primary PFS met (HR 0.73, p=0.008) in 2L+ r/r DLBCL, supporting label expansion; re-rates the HealthCare Royalty 7% synthetic royalty on ZYNLONTA, whose rate steps toward 10% on 2026 and 2027 performance tests (see Clinical Readouts)

- Johnson & Johnson PROTEUS apalutamide plenary (Sun May 31): 20% reduction in metastasis or death risk in high-risk localized prostate cancer; touches only a UC Regents academic layer, with no aggregator royalty on Erleada (the Royalty Pharma UCLA royalty is on Xtandi) (see Clinical Readouts)

- Innovent IBI343 (arcotatug tavatecan) Phase 3 plus China NDA acceptance (Thu June 4): met its primary endpoint at the first interim analysis in previously treated CLDN18.2-positive advanced gastric or gastroesophageal-junction cancer, with the China NMPA accepting the NDA under priority review (the first CLDN18.2 ADC into regulatory review); re-rates Innovent's ex-China milestone-and-royalty receivable under the December 2025 Takeda license (up to ~$11.4B total) (see Clinical Readouts)

Other in-window prints:

- NewLimit $435M Series C (Tue June 2): cellular-reprogramming / longevity; no royalty layer

- Alnylam / Inceptive Nucleics AI collaboration (Wed June 3): up to $2B, $30M upfront in cash and equity plus milestones; AI tech-enablement, no disclosed running royalty

- Verastem VS-7375 FDA Fast Track designation, NSCLC (Wed June 3): Phase 2 KRAS G12D inhibitor licensed from GenFleet (China); a GenFleet ex-China royalty layer sits beneath it

- Annexin Pharmaceuticals SEK 20M rights issue (Wed–Thu June 3–4): Swedish micro-cap recapitalisation; no royalty layer

- Eli Lilly / Camurus FluidCrystal option exercise (Mon June 1): Lilly exercised its June 2025 option to add amylin receptor agonists; $5M trigger payment to Camurus; consolidated frame up to ~$870M milestones ($290M development and regulatory plus $580M sales-based) plus tiered mid-single-digit royalties to Camurus; option exercise inside an existing agreement

- Pfizer / Chai Discovery AI license (Thu June 4): Pfizer deploys Chai's Chai-3 model and a custom Pfizer-data model; software and tech-enablement license, no therapeutic asset or disclosed running royalty

- Biogen salanersen (BIIB115) FDA Breakthrough Therapy Designation, spinal muscular atrophy (Thu June 4): SMN2 antisense oligonucleotide from the Ionis / Biogen collaboration; an Ionis milestone-and-royalty layer sits beneath it

- Quoin QRX003 Japan orphan designation (Netherton syndrome) (Thu June 4): no royalty layer

- Attralus AT-02 FDA orphan designation (AL amyloidosis) (Thu June 4): no royalty layer

- InnoCare orelabrutinib Phase IIb SLE topline (Fri June 5, EULAR 2026): primary endpoint (SRI-4 at week 48) met; orelabrutinib is out-licensed to Zenas BioPharma (October 2025) for multiple sclerosis worldwide and non-oncology fields outside Greater China and Southeast Asia, with royalties to InnoCare, so the readout re-rates that InnoCare royalty stream; Royalty Pharma's separate up-to-$300M Zenas funding (September 2025) is on obexelimab

- AstraZeneca EMERALD-3 liver-cancer readout (Mon June 1, LBA4000): AstraZeneca-owned; no external royalty

- AstraZeneca SERENA-6 camizestrant final PFS2 and ctDNA data (Tue June 2, LBA1007): AstraZeneca-owned

- Bristol Myers Squibb mezigdomide (ASCO): more than doubled progression-free survival in relapsed or refractory multiple myeloma; BMS-owned

How the week reads

M&A and restructuring, by value: Servier / Edgewise.

$1.55B upfront, up to $2.65B with milestones; a divestiture of sevasemten and the muscular dystrophy business with no retained royalty. The Rallybio / Avenzo reverse merger is the window's second corporate combination, carrying a CVR on the legacy REV102 disposition.

Structured finance: Mineralys / Tanabe royalty repurchase.

The cut's only royalty event, and its most directly relevant to a royalty-finance lens. Mineralys pays $200M upfront (up to $300M with milestones) to extinguish the Tanabe royalty on lorundrostat and take the IP, converting an in-licensed, royalty-bearing asset into a royalty-free, wholly owned one. It is funded by a $500M Pharmakon (BioPharma Credit) senior secured term loan and a ~$150M equity raise, a non-dilutive-plus-dilutive package assembled around an NDA-stage asset.

Licensing, by ceiling: Lilly / Haisco, Lilly / Ascidian, Lilly / Hanmi, Travere / Everest, CytomX / Regeneron, plus Agios / Oscotec. Six royalty-bearing licenses. Among the three Lilly deals, Haisco is the larger ceiling (up to ~$3.05B across five discovery programs), Ascidian (up to ~$1.9B) is a US-origin RNA exon-editing platform license in monogenic kidney disease, and Hanmi is the larger upfront ($75M, up to ~$1.26B, post-launch royalties).

Travere / Everest (up to ~$1.14B, $112.5M upfront, high-single-digit to double-digit royalties) is a China-outbound out-license of the BTK inhibitor civorebrutinib for rare kidney disease. CytomX / Regeneron ($37M, up to ~$4B, tiered global royalties) is a US-origin platform expansion in conditional bispecifics, the cut's second platform-royalty origination alongside Ascidian. Agios / Oscotec ($25M upfront, up to $140M development and regulatory milestones plus commercial milestones, high-single-digit to mid-teen royalties) is a Korea-outbound in-license of the oral SYK inhibitor cevidoplenib. Haisco (China), Hanmi (Korea), Everest (China), and Oscotec (Korea) extend the 2026 Asia-outbound corridor; Ascidian and CytomX are US-origin platform deals.

Financings: one PIPE, four early rounds, plus the Mineralys package.

The Rallybio / Avenzo $215M private placement is the largest venture-style raise; the Mineralys $500M Pharmakon term loan plus ~$150M equity is the largest capital event but is covered under the royalty repurchase. Ona Therapeutics ($86.6M, academic plus Biocytogen layers) is the largest pure venture round of the cut. Oak Hill Bio ($32.5M, upstream Roche layer), TheraPPI, and Periotherapia (academic layers) are earlier-stage rounds carrying originator or academic royalty layers beneath them rather than new royalty originations.

Royalty paper: re-rated and one stream retired, none redeployed by an aggregator. No new aggregator capital printed. ASCO data (daraxonrasib / Royalty Pharma, ivonescimab / Akeso, sac-TMT / Kelun, frontMIND / Xencor and OMERS) plus the ZYNLONTA LOTIS-5 confirmatory readout (HealthCare Royalty's 7% synthetic royalty, with 2026 and 2027 rate-step performance tests), the Innovent IBI343 Phase 3 readout plus China NDA acceptance (Innovent's ex-China royalty receivable from Takeda), and the regulatory clears touch existing positions without new money; Mineralys retires a private royalty rather than trading it. PROTEUS touches only a UC Regents academic layer; the Royalty Pharma UCLA royalty is on enzalutamide (Xtandi), not apalutamide (Erleada).

M&A and Restructuring

Two royalty-relevant events anchor this section. The Servier acquisition of Edgewise Therapeutics' muscular dystrophy business and sevasemten, up to $2.65B, is a full divestiture, not a royalty-bearing license, so Edgewise retains no royalty. The Mineralys / Tanabe transaction is the cut's only royalty event: a repurchase that extinguishes the royalty on lorundrostat, funded by a Pharmakon senior secured term loan and an equity raise. It is logged here, rather than under Financings, because the royalty mechanics are the lead and the debt and equity are the funding for it.

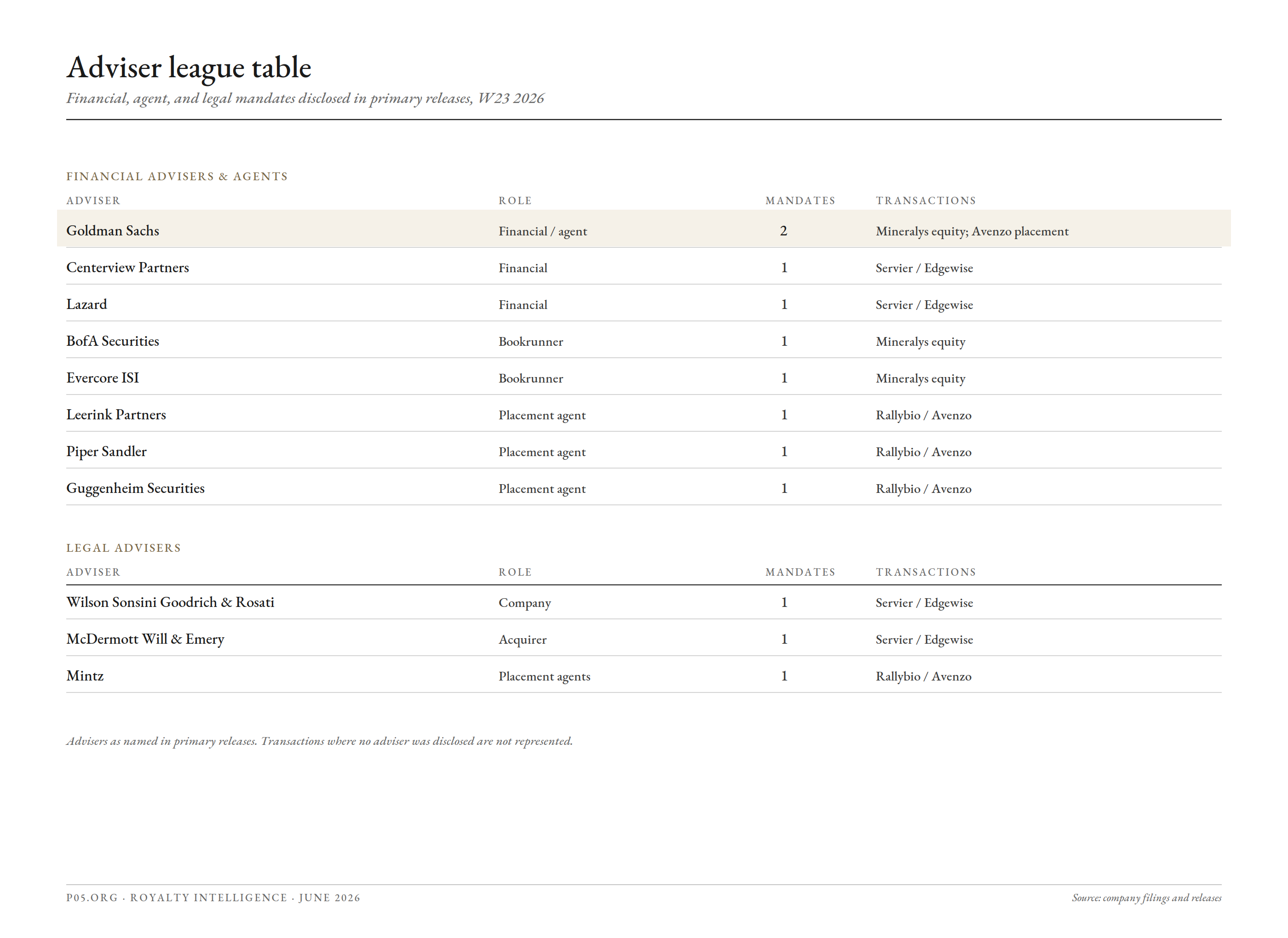

A third corporate combination, the Rallybio / Avenzo reverse merger plus $215M private placement (May 31), is a going-public transaction rather than a royalty event; it carries a CVR on Rallybio's legacy REV102 disposition. The concurrent placement was agented by Leerink Partners, Goldman Sachs & Co. LLC, Piper Sandler, and Guggenheim Securities, expected to close concurrently with the merger (Mintz, advising the placement agents).

Servier / Edgewise Therapeutics: Muscular Dystrophy Business and Sevasemten, Up to $2.65B (Mon June 1)

Servier (the foundation-governed French pharmaceutical group) agreed to acquire the muscular dystrophy business of Edgewise Therapeutics (Nasdaq: EWTX), including sevasemten, for $1.55B upfront cash plus up to $1.1B in milestones, up to $2.65B total (Edgewise release; Servier release).

Servier takes all sevasemten rights, IP, regulatory filings, clinical data, and the supporting team. Edgewise becomes a cardiovascular-focused company (EDG-7500, EDG-15400, EDG-003), funded into EDG-7500 development; closing is targeted for Q3 2026, subject to HSR clearance.

| Term | Detail |

|---|---|

| Acquirer | Servier (Suresnes, France; foundation-governed; FY2024/25 revenue €6.9B; medicines in 130-plus countries) |

| Seller | Edgewise Therapeutics, Inc. (Nasdaq: EWTX; Boulder, CO) |

| Acquired | Muscular dystrophy business plus sevasemten (oral first-in-class fast skeletal myosin inhibitor): all IP, know-how, key agreements, regulatory filings, clinical data, and supporting team |

| Indications | Becker muscular dystrophy (pivotal GRAND CANYON cohort, 175 participants, fully enrolled, powered greater than 98%, topline Q4 2026) and Duchenne muscular dystrophy (Phase 2) |

| Becker prevalence | Approximately 12,000 individuals across US, EU-5, and Japan; no approved therapy today |

| Economics | $1.55B upfront cash plus up to $1.1B regulatory and commercial milestones (aggregate up to $2.65B) |

| Structure | Outright asset-and-business acquisition; Edgewise retains no royalty |

| Edgewise retained pipeline | EDG-7500 (HCM, Phase 2 CIRRUS-HCM, Part D 12-week data Q2 2026, Phase 3 initiation targeted Q4 2026), EDG-15400 (HFpEF, advancing to Phase 2), EDG-003 (undisclosed) |

| Advisors | Centerview Partners (Edgewise financial), Wilson Sonsini Goodrich & Rosati (Edgewise legal); Lazard (Servier financial), McDermott Will & Emery (Servier legal) |

| Closing | Targeted Q3 2026, subject to HSR clearance and customary conditions |

| Date | Mon June 1, 2026 |

- Royalty structure. None retained. The deal is a divestiture: Servier takes all rights and IP, and Edgewise exits the franchise for an upfront-plus-milestone package with no retained royalty or co-promotion economics.

- Why it clears. Largest disclosed print of the cut. A Nasdaq biotech with a Phase 3-staged neuromuscular asset chose an outright sale over a royalty-bearing license or royalty monetisation, taking certainty of capital to fund EDG-7500 rather than a retained royalty.

- Strategic context. Sevasemten gives Servier an immediate platform in Becker and Duchenne muscular dystrophy, aligned with its stated 2030 ambition in neurology and rare neuromuscular disease (Servier release). Becker has no approved treatment, and sevasemten, if approved, would be the first therapy indicated for it (Edgewise release).

Mineralys Therapeutics: Repurchase of the Tanabe Royalty on Lorundrostat, $200M Upfront, Funded by a $500M Pharmakon Term Loan and a ~$150M Equity Raise (Wed June 3)

Mineralys Therapeutics (Nasdaq: MLYS; Radnor, PA) agreed to repurchase all future royalty payments owed to Tanabe Pharma Corporation on lorundrostat, extinguishing the royalty under its in-license in exchange for $200M upfront plus up to $100M in new commercial milestones, and funded the package with a $500M senior secured term loan from funds managed by Pharmakon Advisors and a concurrent ~$150M equity offering (Mineralys repurchase and financing release; equity pricing release).

The royalty repurchase is effected through a fourth amendment to the Tanabe license, converting Mineralys' rights to lorundrostat into an exclusive, worldwide, royalty-free, perpetual license and removing remaining diligence obligations; a follow-on termination agreement is planned to assign Tanabe's remaining intellectual property to Mineralys, while preserving Tanabe's right of first negotiation for Japan (TradingView summary). After the repurchase, Mineralys' aggregate go-forward milestone obligation to Tanabe is up to $265M: up to $100M in new commercial milestones plus up to $165M in existing commercial milestones (the latter including up to $10M tied to a second indication). Lorundrostat is an oral aldosterone synthase inhibitor for hypertension and related comorbidities (CKD, OSA); its US NDA was accepted on May 6, 2026.

| Term | Detail |

|---|---|

| Company | Mineralys Therapeutics, Inc. (Nasdaq: MLYS; Radnor, PA; founded by Catalys Pacific; CEO Jon Congleton) |

| Counterparty | Tanabe Pharma Corporation (originator / licensor of lorundrostat) |

| Asset | Lorundrostat: oral, highly selective aldosterone synthase inhibitor; US NDA accepted May 6, 2026 |

| Royalty repurchase | $200M upfront plus up to $100M in new commercial milestones to extinguish all future Tanabe royalties on lorundrostat; up to $300M total consideration for the repurchase |

| Mechanism | Fourth amendment converting the license to exclusive, worldwide, royalty-free, perpetual; planned termination agreement to assign Tanabe IP to Mineralys; Tanabe retains a right of first negotiation for Japan |

| Residual Tanabe economics | Aggregate go-forward milestones up to $265M (up to $100M new plus up to $165M existing, incl. up to $10M for a second indication); no further royalty |

| Senior secured term loan | Up to $500M from funds managed by Pharmakon Advisors, LP (BioPharma Credit); four tranches; first tranche $100M funded at closing; later drawdowns subject to customary conditions |

| Loan terms | Five-year term, matures June 2031; interest at SOFR (3.25% floor) plus 5.50% per annum |

| Equity | ~$150M underwritten offering; 5,660,378 shares at $26.50; gross ~$150.0M; book-running managers BofA Securities, Goldman Sachs & Co. LLC, and Evercore ISI; expected to close on or about June 4, 2026; net proceeds part-fund the $200M Tanabe upfront |

| Lender / pedigree | Pharmakon is the investment manager of the BioPharma Credit funds; funds managed by Pharmakon have committed up to $12B across 76 investments since 2009 |

| Date | Wed June 3, 2026 |

- Royalty mechanics (the repurchase). This is a royalty extinguishment, not a sale: the developer pays to retire a stream it was obligated to pay, the inverse of a monetisation. The structural move is the fourth amendment converting an in-licensed, royalty-bearing asset into a royalty-free, perpetual, wholly owned one, with the IP assignment to follow. Mineralys converts a variable, sales-linked obligation (an undisclosed running royalty to Tanabe) into a fixed, milestone-capped one (up to $300M for the repurchase; up to $265M residual milestones), trading away royalty cash flow that would have scaled with a successful launch in exchange for retaining that upside itself. The CEO framed it as eliminating all future royalty payments and capturing incremental value from future lorundrostat sales.

- Debt mechanics (Pharmakon facility). The $500M senior secured term loan is a classic BioPharma Credit structure: tranched (only the $100M first tranche funds at closing, with the remaining $400M available against conditions), five-year bullet maturity (June 2031), and floating at SOFR plus 5.50% with a 3.25% SOFR floor. It is non-dilutive but senior secured, so it ranks ahead of equity and sits on the asset Mineralys has just cleaned of a third-party royalty, a sequencing that makes lorundrostat a cleaner collateral package for the lender.

- Equity. The ~$150M raise (5,660,378 shares at $26.50, book-run by BofA Securities, Goldman Sachs & Co. LLC, and Evercore ISI) is explicitly earmarked to part-fund the $200M Tanabe upfront, so the cash-out to Tanabe is met from equity plus the first loan tranche rather than balance-sheet cash alone (equity pricing release). The stock fell roughly 7% on the day, to about $28.85, against a ~$2.38B market capitalisation.

- Why it clears. The window's only royalty event and its most relevant to a royalty-finance lens: a worked example of royalty extinguishment, IP consolidation, and a BioPharma Credit-style tranched term loan executed as a single package around an NDA-stage asset. Pharmakon is a direct comparator in the non-dilutive financing market, and the sequencing (retire the royalty, then secure the loan on the now royalty-free asset, then part-fund the buy-out with equity) is a template worth flagging.

- Read for an originator. For an aggregator, this is a stream removed from the tradable universe rather than created: lorundrostat will not carry a third-party royalty into launch. The countervailing read is the demand signal, a developer willing to pay up to $300M to own its economics outright ahead of approval, which is the same conviction that supports a synthetic-royalty origination on the other side of the trade.

BD Origination and Licensing

Nine BD items in the cut: three Eli Lilly royalty-bearing licenses, the Hanmi sonefpeglutide license (up to ~$1.26B), the Haisco collaboration (up to ~$3.05B), and the Ascidian RNA exon-editing collaboration (up to ~$1.9B); the Travere / Everest civorebrutinib license (up to ~$1.14B); the CytomX / Regeneron expanded conditional-bispecific collaboration ($37M plus up to ~$4B); the Lonza / Stipple Bio ADC platform license (undisclosed, milestones plus net-sales royalties to Lonza); the Everest / Mabworks Bejescin Asia-Pacific in-license (up to RMB 209M, ~$30.9M, plus gross-profit share); the Agios / Oscotec cevidoplenib license ($25M upfront, up to $140M development and regulatory milestones plus commercial milestones plus high-single-digit to mid-teen royalties to Oscotec); plus the Circio / GenAssist AAV research collaboration (undisclosed, no royalty).

Eight of the nine carry royalty or royalty-equivalent economics to the originator: Hanmi on a single Phase 2 asset, Haisco across up to five discovery-stage programs, Ascidian on platform-derived products in monogenic kidney disease, Everest on civorebrutinib in ex-China rare-kidney markets, CytomX on Probody-derived bispecifics commercialised by Regeneron, Oscotec on cevidoplenib in immune thrombocytopenia, and Lonza on Stipple's ADCs built with its Synaffix-derived conjugation technologies; Mabworks takes a gross-profit share rather than a net-sales royalty on Everest's Asia-Pacific sales of Bejescin. By origin, Hanmi (Korea), Haisco (China), Everest (China, on civorebrutinib), and Oscotec (Korea, on cevidoplenib) are Asia-outbound, with the Everest / Mabworks Bejescin license an intra-Asia in-license; Ascidian (Boston) and CytomX (South San Francisco) are US-origin platform license-outs, and Lonza (Basel) is a Swiss CDMO-origin platform license-out. The three Lilly deals also mark three Lilly external-sourcing transactions inside the same window.

Eli Lilly / Hanmi Pharmaceutical: Worldwide (ex-Korea) Sonefpeglutide License, Up to ~$1.26B (Mon June 1)

Hanmi (KRX: 128940; Seoul) granted Eli Lilly (NYSE: LLY) exclusive worldwide rights, excluding Korea, to sonefpeglutide (LAPSGLP-2 analog, HM15912), a long-acting GLP-2 receptor agonist built on Hanmi's LAPSCOVERY platform (Hanmi / Lilly release).

Hanmi receives $75M upfront plus up to $1.185B in milestones (up to ~$1.26B total) and post-launch royalties (pharmaphorum). Hanmi continues its global Phase 2 in short bowel syndrome (NCT04775706); Lilly plans additional studies.

| Term | Detail |

|---|---|

| Licensor / originator | Hanmi Pharm. Co., Ltd. (KRX: 128940; Seoul, South Korea) |

| Licensee | Eli Lilly and Company (NYSE: LLY) |

| Asset | Sonefpeglutide (LAPSGLP-2 analog, HM15912): long-acting GLP-2 receptor agonist; GLP-2 linked via a linker to an antibody constant region (LAPSCOVERY platform) |

| Lead indication / stage | Short bowel syndrome; global Phase 2 (NCT04775706); GI indications beyond SBS not specified |

| Geography | Worldwide excluding Korea (Hanmi retains Korea) |

| Economics | $75M upfront plus up to $1.185B milestones (total up to ~$1.26B) plus post-launch royalties to Hanmi |

| Structure | Hanmi continues the ongoing SBS Phase 2; Lilly leads further development across multiple indications |

| Platform context | LAPSCOVERY long-acting platform; one LAPSCOVERY biologic has prior FDA approval; five further LAPSCOVERY programs in global trials |

| Prior relationship | Second Lilly / Hanmi alliance, after a 2015 BTK-inhibitor deal (~$690M, abandoned in Phase 2) |

| Date | Mon June 1, 2026 |

- Royalty structure. The in-scope hook is the tiered post-launch royalty payable to Hanmi on worldwide ex-Korea net sales, stacked on a $75M upfront and an up-to-$1.185B milestone ladder (Hanmi / Lilly release). The royalty rate was not disclosed.

- Why it clears. A clean royalty-bearing out-license of an Asia-origin asset to global pharma, and the largest royalty-bearing print of the cut. It also extends Lilly's 2026 external sourcing: this lands eight days after Lilly's three simultaneous vaccine acquisitions (Curevo, LimmaTech, Vaccine Company; up to ~$3.83B combined, W22), funded by its GLP-1 franchise cash flows.

- Origination chain. Sonefpeglutide is Hanmi-discovered on the proprietary LAPSCOVERY platform, so the upfront, milestones, and royalty all accrue to a Korean originator that retains its home market. This is a tradable Korea-origin royalty line in the making, and a forward monetisation candidate for Hanmi once the stream matures.

Eli Lilly / Haisco Pharmaceutical: Five-Program Research and Licensing Collaboration, Up to ~$3.05B (announced Fri May 29; PR Newswire Mon June 1)

Haisco (SZSE: 002653; Chengdu, China) entered a licensing and research collaboration with Eli Lilly (NYSE: LLY) across multiple therapeutic areas. Haisco leads discovery of up to five target programs; Lilly leads IND-enabling work, clinical development, and commercialisation (Haisco / Lilly release).

Haisco is eligible for up to $87M upfront and near-term, up to $2,967M in milestones, plus single-digit tiered royalties (up to ~$3.05B total) (Fierce Biotech). Lilly takes worldwide rights to certain programs and ex-Greater-China rights to others; Haisco retains the Haisco Territory. Targets and modalities undisclosed.

| Term | Detail |

|---|---|

| Licensor / originator | Haisco Pharmaceutical Group Co., Ltd. (SZSE: 002653; Chengdu, China; CEO Dr. Pangke Yan) |

| Licensee | Eli Lilly and Company (NYSE: LLY) |

| Assets | Up to five Haisco-discovered target programs; targets and modalities undisclosed |

| Indication | Multiple therapeutic areas (undisclosed) |

| Stage | Discovery (Haisco leads discovery; Lilly leads IND-enabling, clinical development, commercialisation) |

| Geography | Lilly worldwide on certain programs; Lilly ex-Haisco-Territory (ex mainland China, Hong Kong, Macau, Taiwan) on others, Haisco retains the Haisco Territory |

| Economics | Up to $87M upfront and near-term plus up to $2,967M milestones (total up to ~$3.05B) plus single-digit tiered royalties to Haisco |

| Date | Announced Fri May 29, 2026 (Haisco SZSE disclosure); PR Newswire dateline Mon June 1, 2026 |

- Royalty structure. The in-scope hook is the single-digit tiered royalty payable to Haisco on Lilly net sales, stacked on a low (up to $87M) upfront and a milestone-heavy (up to $2,967M) ladder, the classic risk-shifted China-outbound structure where the originator earns most of its value contingently (Haisco / Lilly release).

- Why it clears. A royalty-bearing China-outbound discovery-stage licensing collaboration to global pharma, and the second-largest disclosed print of the cut. It is the second Lilly Asia-outbound license of the window, struck hours after the Hanmi deal, extending the 2026 China-outbound corridor that ran through the W22 Pfizer / Innovent collaboration.

- Caveat. Discovery-stage and undisclosed-target, so the royalty is remote and contingent; the upfront and near-term payments are under 3% of the ~$3.05B total, a back-end-weighted option rather than a near-term royalty origination.

Eli Lilly / Ascidian Therapeutics: RNA Exon-Editing Collaboration for Monogenic Kidney Disease, Up to ~$1.9B (Wed June 3)

Ascidian Therapeutics (Boston, MA; privately held; founded within Flagship Pioneering) granted Eli Lilly (NYSE: LLY) exclusive, target-specific rights to its RNA exon-editing platform for undisclosed monogenic kidney disease targets, with an option to expand to additional targets (Ascidian / Lilly release; BioSpace).

Ascidian is eligible for up to $1.9B total, comprising an undisclosed upfront, development and commercial milestones, and tiered royalties on worldwide net sales (Precision Medicine Online). Ascidian leads discovery and selected preclinical work; Lilly leads later preclinical, clinical, manufacturing, and commercialisation. Ascidian retains the right to pursue other kidney targets alone or with other partners. The platform rewrites RNA at the exon level using endogenous splicing, correcting mutations without altering the genome, a modality positioned between transient RNA therapeutics and permanent DNA editing (Fierce Biotech).

| Term | Detail |

|---|---|

| Licensor / originator | Ascidian Therapeutics (Boston, MA; Flagship-founded; RNA exon-editing platform) |

| Licensee | Eli Lilly and Company (NYSE: LLY) |

| Asset / platform | RNA exon editing: kilobase-scale replacement of whole exons via endogenous splicing, without genomic modification |

| Indication | Undisclosed monogenic (inherited) kidney disease targets; option to expand |

| Geography | Global; Lilly holds exclusive, target-specific rights to specified kidney targets |

| Economics | Up to ~$1.9B (undisclosed upfront plus development and commercial milestones) plus tiered royalties on worldwide net sales to Ascidian |

| Division of labour | Ascidian leads discovery and selected preclinical; Lilly leads later preclinical, clinical, manufacturing, commercialisation; Ascidian retains other kidney targets |

| Prior precedent | Ascidian / Roche (2024) in neurology: $42M upfront, up to $1.8B milestones |

| Date | Wed June 3, 2026 |

- Royalty structure. The in-scope hook is the tiered royalty payable to Ascidian on Lilly worldwide net sales of any products arising from the collaboration, stacked on an undisclosed upfront and a milestone ladder inside the ~$1.9B ceiling. The royalty rate was not disclosed. This is a US-origin, platform-derived royalty line in the making, accruing to a Flagship company that retains independent kidney programs.

- Why it clears. A royalty-bearing platform license-out to global pharma and the window's third Lilly external-sourcing deal, after the Hanmi and Haisco licenses (June 1). It extends Lilly's run of genetic-medicine pacts and gives Ascidian a second major-pharma partner, with Roche in neurology (2024) and now Lilly in renal disease, across two distinct therapeutic areas on the same platform.

- Caveat. Discovery- and platform-stage with undisclosed targets, so the royalty is remote and contingent and the upfront is undisclosed; a back-end-weighted option rather than a near-term royalty origination, comparable in maturity to the Haisco collaboration rather than the launch-stage names elsewhere in the cut.

Travere Therapeutics / Everest Medicines: Civorebrutinib (EVER001) Ex-China License, Up to ~$1.14B (entered Mon June 1; announced Tue June 2)

Everest Medicines (HKEX: 1952.HK; Shanghai; originator and licensor) granted Travere Therapeutics (Nasdaq: TVTX; San Diego) an exclusive license to develop and commercialise civorebrutinib (EVER001), an oral, covalent-reversible BTK inhibitor, in all markets outside China and certain countries in East and Southeast Asia (Travere release; Everest release).

Everest receives $112.5M upfront plus up to ~$1.03B in development, regulatory, and commercial milestones across up to five indications (up to ~$1.14B total), and high-single-digit to double-digit tiered royalties on Travere net sales in the licensed territories (Fierce Biotech). The lead indications are primary membranous nephropathy (PMN), immune-mediated FSGS, and minimal change disease. A Phase 1/2 PMN study showed reductions in anti-PLA2R autoantibodies and proteinuria with high rates of immunologic and clinical remission through 52 weeks. The agreement is subject to HSR clearance.

| Term | Detail |

|---|---|

| Licensor / originator | Everest Medicines (HKEX: 1952.HK; Shanghai; Chairman Yifang Wu) |

| Licensee | Travere Therapeutics, Inc. (Nasdaq: TVTX; San Diego) |

| Asset | Civorebrutinib (EVER001): oral, covalent-reversible Bruton's tyrosine kinase (BTK) inhibitor |

| Indications | Primary membranous nephropathy (lead, Phase 1/2 proof of concept), immune-mediated FSGS, minimal change disease; pipeline-in-a-product across rare immune-mediated kidney disease |

| Geography | Travere takes all markets outside China and certain East and Southeast Asian countries; Everest retains China and the named Asian markets |

| Economics | $112.5M upfront plus up to ~$1.03B milestones across up to five indications (total up to ~$1.14B), plus high-single-digit to double-digit tiered royalties on Travere net sales to Everest |

| Condition | Effectiveness subject to expiration or termination of the HSR waiting period |

| Date | Agreement entered Mon June 1, 2026; announced Tue June 2, 2026 (Travere investor call 8:30 a.m. ET) |

- Royalty structure. The in-scope hook is the tiered royalty payable to Everest on Travere's ex-China net sales, stacked on a $112.5M upfront and an up-to-~$1.03B milestone ladder. The high-single-digit to double-digit band, disclosed by tier, is wider and more concrete than the single-digit Haisco rate or the undisclosed Hanmi and Ascidian rates, reflecting a clinical-stage asset with human proof of concept rather than a discovery- or platform-stage option. This is a China-origin royalty line accruing to Everest on a partner's developed-market sales, a future monetisation candidate for Everest once the stream matures.

- Royalty-stack cross-reference. Travere's marketed lead asset, Filspari (sparsentan), already carries a fixed 9% royalty to Ligand Pharmaceuticals on worldwide net sales (Ligand release, April 2026). Civorebrutinib stacks a second, originator royalty (to Everest) onto the same rare-kidney portfolio, so Travere is building a franchise in which each pillar carries a separate third-party royalty layer: Ligand on Filspari, Everest on civorebrutinib.

- Why it clears. A royalty-bearing, clinical-stage out-license with disclosed economics and a disclosed royalty band, and the window's clearest China-outbound print after the Lilly / Haisco discovery collaboration. It extends the 2026 Asia-outbound corridor (Innovent, Haisco, Hanmi, now Everest) into a China-origin asset with human data, where the royalty is nearer-term and better-defined than the discovery-stage Asia deals elsewhere in the cut.

CytomX Therapeutics / Regeneron: Expanded Conditional-Bispecific Oncology Collaboration, $37M plus Up to ~$4B (Wed June 3)

CytomX Therapeutics (Nasdaq: CTMX; South San Francisco; originator and platform licensor) expanded its 2022 collaboration and licensing agreement with Regeneron (Nasdaq: REGN) to develop conditionally-activated bispecific cancer therapies combining CytomX's Probody masking platform with Regeneron's Veloci-Bi bispecific platform (CytomX release).

CytomX receives a $37M target-nomination payment for two additional selected targets, and Regeneron holds an option to select up to six further targets. Total potential target-nomination, preclinical, clinical, regulatory, and commercial milestones across the expanded scope reach up to ~$4B, and CytomX is eligible for tiered global net-sales royalties on covered products. Regeneron funds preclinical and clinical development and commercialisation. The 2022 original carried $30M upfront, up to $800M in milestones, plus up to $1.2B tied to expansion (Fierce Biotech).

| Term | Detail |

|---|---|

| Licensor / originator | CytomX Therapeutics (Nasdaq: CTMX; South San Francisco); Probody conditionally-activated masking platform |

| Licensee | Regeneron (Nasdaq: REGN); Veloci-Bi bispecific antibody platform; funds preclinical, clinical, and commercial activities |

| Asset / platform | Conditionally-activated (protease-cleavable, tumor-localised) bispecific antibodies for oncology |

| Economics | $37M target-nomination payment for two new targets; option on up to six more; total nomination plus development, regulatory, and commercial milestones up to ~$4B; tiered global net-sales royalties to CytomX |

| Structure | Expansion of the 2022 CytomX / Regeneron collaboration and licensing agreement (originally $30M upfront, up to $800M milestones, plus up to $1.2B expansion-linked) |

| Date | Wed June 3, 2026 |

- Royalty structure. The in-scope hook is the tiered global net-sales royalty payable to CytomX on Regeneron commercial products arising from the collaboration, stacked on the $37M nomination payment and the up-to-~$4B milestone ladder. The royalty rate band was not disclosed. This is a US-origin, platform-derived royalty line accruing to CytomX, comparable in type to the Ascidian platform royalty but at an earlier collaboration stage and against a larger, multi-target milestone ceiling.

- Why it clears. A royalty-bearing platform license expansion to large-cap pharma, with a disclosed cash payment ($37M), a defined milestone ceiling (~$4B), and explicit tiered royalties to the originator. It sits alongside the window's other royalty-bearing license-outs and is the cut's second platform-royalty origination (with Ascidian) where a US biotech licenses a discovery engine rather than a single asset.

- Caveat. Discovery- and platform-stage with target selection still open (two nominated, up to six optioned), so the royalty is remote and contingent and the rate is undisclosed; a back-end option rather than a near-term royalty origination.

Lonza / Stipple Bio: Multi-Target ADC Platform License, Undisclosed (Thu June 4)

Lonza (SIX: LONN; Basel) granted Stipple Bio (Cambridge, MA; privately held) target-specific access to its site-specific antibody-drug-conjugate platform across multiple oncology programs, including Stipple's lead candidate STP-100; financial terms were not fully disclosed (Lonza / Stipple release; Contract Pharma).

The deal pairs Stipple's Pointillist epitope-discovery platform, which identifies tumour-specific cell-surface epitopes to widen the therapeutic index, with Lonza's GlycoConnect conjugation, HydraSpace polar-spacer, and toxSYN linker-payload technologies (the Synaffix-derived stack Lonza acquired in 2023). Lonza is eligible for upfront, clinical, regulatory, and commercial milestone payments plus royalties on net sales of resulting products, and manufactures the components tied to its proprietary technologies; Stipple leads research, development, manufacturing, and commercialisation. STP-100 is expected to enter the clinic in 2027; Stipple emerged from stealth on an oversubscribed $100M Series A co-led by RA Capital and a16z Bio+ (BioSpace; allsci).

| Term | Detail |

|---|---|

| Licensor / originator | Lonza (SIX: LONN; Basel, Switzerland): site-specific ADC platform (Synaffix-derived) |

| Licensee | Stipple Bio, Inc. (Cambridge, MA; privately held; Pointillist epitope-discovery platform) |

| Scope | Target-specific access to GlycoConnect, HydraSpace, and toxSYN technologies across multiple ADC programs, including STP-100 |

| Economics | Undisclosed; Lonza eligible for upfront, clinical, regulatory, and commercial milestones plus royalties on net sales of resulting products |

| Division of labour | Lonza manufactures proprietary-technology components; Stipple leads research, development, manufacturing, and commercialisation |

| Stage | Preclinical; STP-100 clinic-bound 2027 |

| Date | Thu June 4, 2026 |

- Royalty structure. The in-scope hook is the royalty on net sales payable to Lonza on any Stipple product built with the licensed conjugation technologies, stacked on an undisclosed milestone ladder. This is a Swiss-origin, platform-derived royalty line accruing to a CDMO rather than a therapeutics originator: Lonza converting its Synaffix conjugation IP into a milestone-and-royalty book, the same structure as the Synaffix / Sidewinder bispecific-ADC license in January 2026.

- Why it clears. A royalty-bearing platform license-out, the cut's third platform-royalty origination alongside Ascidian and CytomX, and the first where the originator is a contract manufacturer. Comparable in type to enabling-technology royalty franchises such as Halozyme and Ligand, where the licensor monetises a delivery or manufacturing technology across many partners' assets rather than a single molecule.

- Caveat. Preclinical and terms undisclosed, so the royalty is remote and unquantified; a platform-stage option rather than a near-term stream, with STP-100's 2027 clinic entry the first value inflection.

Everest Medicines / Mabworks: Bejescin (MIL62) Asia-Pacific In-License, Up to RMB 209M (~$30.9M) Plus Profit Share (Thu June 4)

Everest Medicines (HKEX: 1952; Shanghai) in-licensed exclusive Asia-Pacific clinical-development and commercialisation rights to Bejescin (MIL62, obinutuzumab beta), a third-generation anti-CD20 monoclonal antibody, from Mabworks (Beijing), covering Southeast Asia, India, South Korea, Australia, New Zealand, Hong Kong, Macao, and Taiwan; mainland China is retained by Mabworks (Everest release; allsci).

Everest pays RMB 23M (~$3.4M) upfront and up to RMB 186M (~$27.5M) in sales milestones (RMB 209M, ~$30.9M, total disclosed), plus an undisclosed share of gross profit in the territory to Mabworks. Bejescin is a glycoengineered, near-fully afucosylated Type II anti-CD20 antibody that received China NMPA approval in February 2026 for NMOSD, the first CD20 antibody approved globally for that indication; its primary membranous nephropathy NDA is under NMPA Priority Review (NMPA Breakthrough Therapy Designation, October 2025), and Phase III trials are running in SLE and follicular lymphoma.

| Term | Detail |

|---|---|

| Licensee | Everest Medicines (HKEX: 1952; Shanghai) |

| Licensor / originator | Mabworks (Beijing): originator of MIL62 |

| Asset | Bejescin (MIL62, obinutuzumab beta): third-generation, afucosylated Type II anti-CD20 monoclonal antibody |

| Territory | Asia-Pacific ex mainland China (Southeast Asia, India, South Korea, Australia, New Zealand, Hong Kong, Macao, Taiwan) |

| Economics | RMB 23M (~$3.4M) upfront plus up to RMB 186M (~$27.5M) sales milestones (up to RMB 209M, ~$30.9M); plus undisclosed gross-profit share to Mabworks |

| Status | China-approved (NMOSD, Feb 2026); PMN NDA under NMPA Priority Review; Phase III in SLE and follicular lymphoma |

| Date | Thu June 4, 2026 |

- Royalty structure. The in-scope hook is the gross-profit share payable to Mabworks on Everest's Asia-Pacific sales, a profit interest rather than a net-sales royalty, stacked on a small (RMB 23M) upfront and an up-to-RMB 186M sales-milestone ladder. The profit-share rate was not disclosed. This is a China-origin, royalty-equivalent line accruing to Mabworks on a partner's regional commercialisation of an already-approved asset, so the stream is nearer-term and less contingent than the discovery- and platform-stage royalties elsewhere in the cut.

- Direction note. Everest's second appearance in the window, and on the opposite side of the table. In the civorebrutinib license Everest is the licensor, out-licensing ex-China rights to Travere; here Everest is the licensee, in-licensing Asia-Pacific rights from a China originator. A single regional player both monetising an in-house asset abroad and importing a domestic asset into its commercial network within the same week, a textbook two-way intra-Asia flow.

- Why it clears. A royalty-equivalent, commercial-stage in-license of an approved China-origin asset, with disclosed cash terms and a defined sales-milestone ladder. It adds a gross-profit-share structure distinct from the net-sales royalties elsewhere in the cut and extends the 2026 intra-Asia licensing corridor into a regional commercialisation deal rather than a global out-license.

Agios Pharmaceuticals / Oscotec: Cevidoplenib Global License, $25M Upfront Plus Up to $140M in Milestones (Mon June 1)

Agios Pharmaceuticals (Nasdaq: AGIO; Cambridge, MA) entered an exclusive global license agreement with Oscotec (KOSDAQ; South Korea) to develop and commercialise cevidoplenib, a next-generation oral SYK (spleen tyrosine kinase) inhibitor, in immune thrombocytopenia and additional indications (Agios release; GlobeNewswire).

Oscotec receives $25M upfront plus up to $140M in development and regulatory milestones across up to three US and EU indications, additional commercial milestones, and high-single-digit to mid-teen tiered royalties on net sales; Oscotec retains an option to reacquire South Korea rights after Phase 3 (Stock Titan). Cevidoplenib holds FDA orphan drug designation in immune thrombocytopenia (March 2024) and is backed by Phase 2 data.

| Term | Detail |

|---|---|

| Licensee | Agios Pharmaceuticals (Nasdaq: AGIO; Cambridge, MA) |

| Licensor / originator | Oscotec (KOSDAQ; South Korea): originator of cevidoplenib |

| Asset | Cevidoplenib: next-generation oral SYK (spleen tyrosine kinase) inhibitor |

| Lead indication / stage | Immune thrombocytopenia; Phase 2 (FDA orphan drug designation, March 2024); option to expand to additional indications |

| Geography | Exclusive global rights to Agios; Oscotec retains a South Korea reacquisition option after Phase 3 |

| Economics | $25M upfront plus up to $140M development and regulatory milestones across up to three US and EU indications, plus commercial milestones, plus high-single-digit to mid-teen tiered royalties to Oscotec |

| Date | Mon June 1, 2026 |

- Royalty structure. The in-scope hook is the high-single-digit to mid-teen tiered royalty payable to Oscotec on Agios's worldwide net sales, stacked on a $25M upfront and an up-to-$140M development and regulatory milestone ladder plus undisclosed commercial milestones. A Korea-origin royalty line accruing to Oscotec on a clinical-stage asset, with the South Korea reacquisition option preserving a domestic-market carve-out.

- Why it clears. A royalty-bearing, clinical-stage in-license of a Korea-origin asset by US pharma, with a disclosed upfront, a defined milestone ladder, and a disclosed royalty band. It is the fourth Asia-outbound print of the cut, alongside Hanmi (Korea), Haisco (China), and Everest (China, on civorebrutinib).

- Caveat. Phase 2 stage in immune thrombocytopenia, so the royalty is contingent on registrational success; the disclosed milestone ceiling is modest relative to the larger licensing prints of the week.

Circio / GenAssist: AAV Gene-Therapy Research Collaboration for Muscle Disease and In Vivo Cell Therapy (Mon June 1)

Circio Holding ASA (OSE: CRNA; Oslo) and GenAssist Ltd (Suzhou, China) entered a research collaboration to develop circVec-enhanced AAV vectors for in vivo cell therapy and targeted, low-dose systemic gene therapy (Circio release; Contract Pharma).

The collaboration combines Circio's circVec circular-RNA expression cassette, which the company reports can boost AAV gene expression up to 50-fold in vivo, with GenAssist's second-generation tissue-specific, liver-de-targeting AAV capsids and promoters (Circio release). The focus areas are genetic muscle disease, where conventional high-dose AAV carries severe toxicity, and joint in vivo CAR-T candidates for oncology and autoimmune indications using GenAssist's T-cell-targeting AAVs (TipRanks). Constructs that perform will be nominated for preclinical development.

| Term | Detail |

|---|---|

| Party | Circio Holding ASA (OSE: CRNA; Oslo, Norway): circVec circular-RNA expression platform |

| Party | GenAssist Ltd (Suzhou, China): tissue-specific, liver-de-targeting AAV capsids and promoters |

| Scope | Develop and test circVec-enhanced, tissue-targeted AAV vectors; low-dose systemic gene therapy and in vivo CAR-T |

| Indications | Genetic muscle disease; oncology and autoimmune (in vivo CAR-T) |

| Economics | Undisclosed; no royalty or milestone structure disclosed |

| Date | Mon June 1, 2026 |

- Structure. A pre-clinical research collaboration with no disclosed financial terms and no royalty mechanics. It is part of Circio's stated strategy of testing circVec across tissues and AAV variants with multiple external partners, and a forward partnering or origination watch item rather than a tradable structure today.

Financings

Four financings in the cut: the Oak Hill Bio $32.5M Series A, the Ona Therapeutics $86.6M Series B, the TheraPPI pre-seed close, and the Periotherapia JPY 575M raise plus AMED grant (June 2).

All four carry academic or originator license layers beneath them; none is a royalty origination today.

The cut's largest capital event, the Mineralys $500M Pharmakon senior secured term loan and ~$150M equity raise (June 3), is covered under M&A and Restructuring because it funds the Tanabe royalty repurchase and the royalty mechanics lead.

Oak Hill Bio: $32.5M Series A to Advance Rugonersen (OHB-724) to Phase 3 in Angelman Syndrome (Mon June 1)

Cambridge, MA-based Oak Hill Bio closed a $32.5M Series A co-led by Balyasny Asset Management, venBio, and Janus Henderson Investors, with participation from KCap Biotechnology Fund, to advance rugonersen (OHB-724) into a pivotal Phase 3 in Angelman syndrome (Oak Hill Bio release). Doug Fambrough, Rich Gaster, and Sandeep Kulkarni joined the board.

Rugonersen is an antisense oligonucleotide that suppresses the UBE3A-ATS transcript to restore UBE3A expression from the paternal allele, the genetic deficit in Angelman syndrome (roughly 30,000 diagnosed across the US and EU-5, no approved treatment). The Phase 1 TANGELO study (61 patients) was published in Nature Medicine and showed a dose-dependent reduction in EEG delta power (TANGELO publication).

| Term | Detail |

|---|---|

| Company | Oak Hill Bio (Cambridge, MA; clinical-stage rare-disease therapeutics) |

| Round | $32.5M Series A |

| Investors | Balyasny Asset Management, venBio, Janus Henderson Investors (co-leads); KCap Biotechnology Fund |

| Lead asset | Rugonersen (OHB-724): UBE3A-ATS antisense oligonucleotide; Phase 3-bound (mid-2026 initiation) |

| Indication | Angelman syndrome (approximately 30,000 diagnosed US plus EU-5; roughly 500K globally; no approved treatment) |

| Origination | In-licensed from Roche on a global exclusive basis; upstream Roche milestone-and-royalty layer applies |

| Other pipeline | OHB-607 (recombinant IGF-1/IGFBP-3; collaboration with Chiesi) |

| Board additions | Doug Fambrough, Rich Gaster, Sandeep Kulkarni |

| Date | Mon June 1, 2026 |

- Royalty layer (Roche license). Rugonersen was in-licensed from Roche on an exclusive global basis; the milestone and royalty terms are undisclosed (TANGELO publication). A fresh $32.5M raise that funds the asset into Phase 3 brings that dormant out-licensor royalty layer back toward relevance: a venture-funded developer carrying a Roche royalty obligation that re-prices upward as the program advances.

- Why it clears. A clean rare-disease ASO financing with a defined upstream royalty layer, in an indication with no approved therapy and a clear Phase 1-to-Phase 3 progression. Re-evaluate the Roche royalty layer at Phase 3 readout.

Ona Therapeutics: $86.6M Series B to Advance First-in-Class ADCs ONA-255 and ONA-389 into the Clinic (Thu June 4)

Barcelona-based Ona Therapeutics closed an oversubscribed $86.6M Series B co-led by new investors Columbus Venture Partners and Mérieux Equity Partners (through its Mérieux Innovation 2 / MI2 fund), with COFIDES and Korys plus existing investors, to advance its first-in-class antibody-drug conjugates (Ona release; Mérieux Partners). Proceeds fund the lead program ONA-255 (a first-in-class ADC, initially HR-positive, HER2-negative third-line breast cancer) toward clinical proof of concept, and progress ONA-389 (a second ADC in colorectal cancer) toward first-in-human studies. Ona retains full worldwide commercial rights to all its assets.

| Term | Detail |

|---|---|

| Company | Ona Therapeutics (Barcelona, Spain; first-in-class ADCs for treatment-resistant cancer) |

| Round | $86.6M Series B (oversubscribed) |

| Investors | Columbus Venture Partners, Mérieux Equity Partners (co-leads; Mérieux through its Mérieux Innovation 2 / MI2 fund); COFIDES, Korys; existing investors (incl. Alta Life Sciences) |

| Lead asset | ONA-255: first-in-class ADC; HR-positive, HER2-negative metastatic breast cancer (3L); toward clinical proof of concept |

| Second asset | ONA-389: ADC in colorectal cancer; toward first-in-human |

| Origination layers | ONA-255 target/biology exclusively licensed from a Barcelona academic consortium (Hospital Clínic / FCRB-IDIBAPS, IRB Barcelona, UB, ICREA); antibody platform under a 2023 Biocytogen evaluation, option, and license agreement |

| Rights | Ona retains full worldwide commercial rights to all assets |

| Date | Thu June 4, 2026 |

- Royalty layers (academic plus platform). Two upstream license layers sit beneath ONA-255: an exclusive academic license from the Barcelona research consortium that identified and validated the target, and a 2023 Biocytogen antibody evaluation, option, and license agreement underpinning the antibody. Both carry undisclosed milestone and royalty obligations that re-price upward as ONA-255 advances toward the clinic, the same dormant-layer dynamic as Oak Hill Bio's Roche license, here doubled across an academic originator and a China-based antibody platform.

- Why it clears. The largest financing in the cut and a clinical-transition round for a European ADC developer, carrying defined academic and originator license layers beneath the lead asset. No new royalty is originated by the round itself; the relevance is the upstream layers that advance with the program. Re-evaluate at ONA-255 first-in-human.

TheraPPI: Pre-Seed Close for a First-in-Class ERK/MyD88 Protein-Protein-Interaction Oncology Program (Mon June 1)

TheraPPI (TheraPPI Bioscience SAS, Lyon, France; and TheraPPI Bioscience SA, Geneva, Switzerland) closed a pre-seed financing to advance its lead program targeting the ERK/MyD88 protein-protein interaction in the Ras-MAPK pathway, aimed at overcoming cancer drug resistance in patients with advanced cancers (TheraPPI release).

The company is a spin-out of the Centre de Recherche en Cancérologie de Lyon (CRCL). Its scientific basis is the disruption of the ERK-MyD88 interaction (the EI-52 benzimidazole class), which induces an integrated stress response and immunogenic cancer-cell death while preserving ERK kinase activity, and has shown anti-tumour efficacy in patient-derived models (Nature Communications; CRCL).

| Term | Detail |

|---|---|

| Company | TheraPPI (TheraPPI Bioscience SAS, Lyon; SA, Geneva); CRCL spin-out |

| Round | Pre-seed (amount not disclosed) |

| Asset | First-in-class small-molecule inhibitor of the ERK/MyD88 protein-protein interaction (Ras-MAPK pathway; EI-52 class) |

| Indication | Advanced cancers; cancer drug resistance |

| Stage | Pre-clinical |

| Royalty structure | None disclosed; carries an academic-license layer (CRCL / host institutions) |

| Date | Mon June 1, 2026 |

- A platform and pre-clinical-stage European origination candidate, with an academic-license layer from the CRCL / Lyon host institutions sitting beneath it. Nothing tradable today; re-evaluate at seed or IND. Logged for the EU oncology origination pipeline.

Periotherapia: JPY 575M Financing Plus AMED Grant for Anti-Periostin Antibody PT0101 (Tue June 2)

Periotherapia Co., Ltd. (Osaka, Japan; an Osaka University spin-out) raised a reported JPY 575M and received an AMED grant to fund clinical development of PT0101, an anti-periostin antibody that selectively targets tumour-specific periostin splice variants implicated in chemotherapy resistance, in a Phase I/IIa first-in-human trial in HER2-negative recurrent or metastatic breast cancer and advanced solid tumours (PT0101-CT1, NCT-listed, Annals of Oncology abstract).

| Term | Detail |

|---|---|

| Company | Periotherapia Co., Ltd. (Osaka, Japan; Osaka University spin-out) |

| Round | Reported JPY 575M plus AMED grant (labelled series D in the deal feed) |

| Asset | PT0101: anti-periostin antibody targeting tumour-specific periostin splice variants (ASV21 / exon-17 class) |

| Indication | HER2-negative recurrent or metastatic breast cancer; advanced solid tumours |

| Stage | Phase I/IIa (PT0101-CT1) |

| Royalty structure | None disclosed; academic-license layer (Osaka University IP) |

| Date | Tue June 2, 2026 |

- A small Japan-origin clinical-stage financing with an academic-license layer (Osaka University periostin IP) sitting beneath it. The figure (~JPY 575M, roughly $3.7M) is modest and partly grant-supported, so the "series D" label in the deal feed is best read as the company's terminology rather than a venture round of that scale. Nothing tradable today; logged for the Japan oncology origination pipeline and as an EDINET / Japanese-disclosure watch item.

Clinical Readouts

Eight clinical readouts in the cut. Seven re-rate or touch royalty paper (daraxonrasib, ivonescimab, sac-TMT, PROTEUS, frontMIND, the June 3 ZYNLONTA LOTIS-5 confirmatory readout, and the June 4 Innovent IBI343 Phase 3 readout plus China NDA acceptance); the eighth, the Oculis OCS-01 DIAMOND Phase 3 failure, carries no royalty. Five of the seven are ASCO 2026 events; the ZYNLONTA readout prints June 3 and the IBI343 readout June 4.

Revolution Medicines daraxonrasib RASolute 302 ASCO Plenary and NEJM Publication, Previously Treated Metastatic Pancreatic Cancer (Sun May 31)

Revolution Medicines (Nasdaq: RVMD) presented the pivotal Phase 3 RASolute 302 results for daraxonrasib (RMC-6236, an oral multi-selective RAS(ON) inhibitor) at the ASCO 2026 plenary session (Abstract LBA5), with simultaneous publication in the New England Journal of Medicine (Revolution Medicines release; NEJM). In previously treated metastatic pancreatic ductal adenocarcinoma, daraxonrasib delivered median overall survival of 13.2 versus 6.7 months for chemotherapy in the intent-to-treat population, a hazard ratio of 0.40 (p<0.0001), with all primary and key secondary endpoints met and significantly delayed deterioration in cancer-related pain and quality of life (Revolution Medicines topline; NEJM). Data cutoff was February 10, 2026, median follow-up 8.5 months; Revolution Medicines intends to file a US NDA under a Commissioner's National Priority Voucher.

| Term | Detail |

|---|---|

| Sponsor | Revolution Medicines (Nasdaq: RVMD) |

| Asset | Daraxonrasib (RMC-6236): oral multi-selective RAS(ON) inhibitor |

| Indication | Previously treated metastatic pancreatic ductal adenocarcinoma (with or without identified RAS mutation) |

| Data | RASolute 302 (NCT06625320); ITT median OS 13.2 vs 6.7 months, HR 0.40 (p<0.0001); PFS also significant; ASCO Abstract LBA5; NEJM May 31, 2026 (DOI 10.1056/NEJMoa2605555) |

| Royalty holder | Royalty Pharma (Nasdaq: RPRX): synthetic royalty on daraxonrasib (and zoldonrasib in overlapping indications) |

| Date | Sun May 31, 2026 (ASCO plenary and NEJM) |

- Royalty-stack cross-reference. In June 2025 Royalty Pharma and Revolution Medicines signed funding agreements for up to $2B: an up-to-$1.25B synthetic royalty on daraxonrasib (and zoldonrasib in overlapping indications) plus an up-to-$750M senior loan (RPRX / RevMed agreement).

- Tiers. Reported base tiers are roughly 4.55% on the first $2B of net sales, 2.50% on $2B to $4B, and 1.00% on $4B to $8B, with step-ups to as high as ~7.80% if the remaining funding is drawn. Royalty Pharma reportedly funded a second $250M tranche in early May 2026, taking funded capital to ~$500M.

- Read. The plenary-grade OS data and the planned NDA materially de-risk this stream.

- Why it clears. A direct, plenary-grade re-rating of a large, recently deployed synthetic royalty held by the sector's largest aggregator, in an indication (metastatic PDAC) where a doubling of overall survival is genuinely category-defining. Flagged as a carry-forward in prior cuts; the detailed data now print.

Summit Therapeutics / Akeso ivonescimab HARMONi-6 ASCO Plenary, First-Line Squamous NSCLC (Sun May 31)

Summit Therapeutics (Nasdaq: SMMT) and Akeso (HKEX: 9926) reported HARMONi-6 Phase 3 overall-survival data for ivonescimab (a PD-1 by VEGF bispecific antibody) plus chemotherapy versus tislelizumab plus chemotherapy in first-line advanced squamous NSCLC, at the ASCO 2026 plenary session (Abstract LBA4), with simultaneous publication in The Lancet (Summit / Akeso release). Ivonescimab cut the risk of death by 34% (HR 0.66, 95% CI 0.50 to 0.87, p=0.0017), with median OS of 27.9 versus 23.7 months and 24-month OS of 64.7% versus 48.6%, across 532 patients (data cutoff February 27, 2026). The release noted it as the first China-originated investigational oncology drug selected for the ASCO plenary in the meeting's history.

| Term | Detail |

|---|---|

| Licensee / royalty payer | Summit Therapeutics (Nasdaq: SMMT): US, Canada, Europe, Japan rights |

| Originator / royalty holder | Akeso (HKEX: 9926): retains China and rest of world; receives royalties on Summit-territory sales |

| Asset | Ivonescimab: PD-1 by VEGF bispecific antibody |

| Indication | First-line advanced squamous NSCLC (irrespective of PD-L1; comparator tislelizumab plus chemotherapy) |

| Data | HARMONi-6; OS HR 0.66 (95% CI 0.50 to 0.87, p=0.0017); median OS 27.9 vs 23.7 months; 24-month OS 64.7% vs 48.6%; n=532; ASCO Abstract LBA4; published in The Lancet |

| License terms | Summit in-licensed from Akeso (Dec 2022): $500M upfront, up to $4.5B milestones (up to $5B total), low-double-digit royalties to Akeso (Summit / Akeso license) |

| Date | Sun May 31, 2026 |

- Royalty-stack cross-reference. Akeso holds a low-double-digit royalty on Summit-territory ivonescimab sales under the December 2022 up-to-$5B license, alongside its retained China and rest-of-world economics. A positive OS plenary in first-line squamous NSCLC supports the Summit-territory commercial case behind that royalty. SMMT rose ~13% overnight, then reversed ~10% lower on June 1 on HARMONi-3 read-through concerns.

- Window note. HARMONi-6 enrolled squamous NSCLC irrespective of PD-L1 status and used tislelizumab (not pembrolizumab) as the comparator; the PD-L1-selected pembrolizumab comparison belongs to the earlier HARMONi-2 study.

Merck / Kelun-Biotech sac-TMT OptiTROP-Lung05 Readout, First-Line PD-L1-Positive NSCLC (Fri May 29)

Kelun-Biotech (HKEX: 6990) reported OptiTROP-Lung05 Phase 3 data for sac-TMT (sacituzumab tirumotecan, a TROP2 antibody-drug conjugate) plus pembrolizumab in first-line PD-L1-positive NSCLC (ASCO Abstract #8506), showing a progression-free survival HR of 0.35 (95% CI 0.26 to 0.47, p<0.0001), median PFS not reached versus 5.7 months, and 12-month PFS of 62.4% versus 29.0%, with an early favourable overall-survival trend; published in The Lancet on May 29, 2026 (OncLive).

| Term | Detail |

|---|---|

| Sponsor / originator | Kelun-Biotech (HKEX: 6990); sac-TMT is a Kelun-developed TROP2 ADC |

| Licensee / royalty payer | Merck (NYSE: MRK): ex-China license for sac-TMT, with milestones and royalties to Kelun |

| Asset | Sac-TMT (sacituzumab tirumotecan): TROP2 antibody-drug conjugate, plus pembrolizumab |

| Indication | First-line PD-L1-positive NSCLC |

| Data | OptiTROP-Lung05 (Abstract #8506); PFS HR 0.35 (95% CI 0.26 to 0.47, p<0.0001); mPFS NR vs 5.7 months; 12-month PFS 62.4% vs 29.0%; OS immature, trend favourable; published in The Lancet May 29, 2026 |

| Date | Fri May 29, 2026 |

- Royalty-stack cross-reference. Sac-TMT is Kelun-developed and licensed to Merck ex-China, with milestone and royalty economics accruing to Kelun on Merck-territory sales. W22 flagged this readout as an ASCO carry-forward; the detailed PFS data now print and re-rate the Kelun royalty line.

Johnson & Johnson PROTEUS Apalutamide (Erleada) ASCO Plenary and NEJM Publication, High-Risk Localized Prostate Cancer (Sun May 31)

Johnson & Johnson (NYSE: JNJ) presented the final analysis of the Phase 3 PROTEUS study of perioperative (neoadjuvant and adjuvant) apalutamide (Erleada) plus androgen deprivation therapy (ADT) versus placebo plus ADT around radical prostatectomy in high-risk localized or locally advanced prostate cancer, at the ASCO 2026 plenary session (Abstract LBA1), with simultaneous publication in the New England Journal of Medicine (J&J release; Taplin et al., NEJM, doi:10.1056/NEJMoa2603878). The trial met both primary endpoints: patients on apalutamide plus ADT were roughly nine times more likely to have little to no residual cancer at surgery (pathologic complete response or minimal residual disease 8.9% versus 1.0%), with a 20% reduction in the risk of metastasis or death; 2,109 patients across 184 sites in 18 countries.

| Term | Detail |

|---|---|

| Sponsor | Johnson & Johnson (NYSE: JNJ) |

| Asset | Apalutamide (Erleada, ARN-509): oral androgen receptor inhibitor |

| Indication | Perioperative (neoadjuvant and adjuvant) treatment of high-risk localized or locally advanced prostate cancer |

| Data | PROTEUS Phase 3; pCR/MRD 8.9% vs 1.0%; 20% reduction in risk of metastasis or death; n=2,109; ASCO Abstract LBA1; NEJM May 31, 2026 |

| Royalty structure | No aggregator sales royalty; only a UC Regents / UCLA academic-license layer applies |

| Date | Sun May 31, 2026 (ASCO plenary and NEJM) |

- Royalty cross-reference (important caveat). Apalutamide originated at Aragon Pharmaceuticals (acquired by J&J in 2013) and traces to UCLA chemistry, so the only third-party economic interest is the UC Regents / UCLA academic-license royalty. There is no disclosed aggregator sales royalty on Erleada. Royalty Pharma's up-to-$1.14B March 2016 purchase of UCLA's royalty (UCLA's share ~$520M) was on enzalutamide (Xtandi), not apalutamide (Erleada): distinct AR inhibitors that share a UCLA lineage but not a royalty instrument.

- Why it is logged. A plenary-grade, paradigm-shifting readout for a major marketed oncology asset, but with no tradable third-party royalty re-rating. Logged as a pipeline-value and competitive-landscape data point, and as a reminder that the UCLA AR-inhibitor royalty paper held by Royalty Pharma sits on Xtandi, not Erleada.

Incyte frontMIND Tafasitamab (Monjuvi / Minjuvi) Readout, First-Line DLBCL (Sat May 30)

Incyte (Nasdaq: INCY) reported pivotal Phase 3 frontMIND data for tafasitamab (Monjuvi / Minjuvi) plus lenalidomide added to R-CHOP (Tafa-Len-R-CHOP) versus R-CHOP alone in previously untreated high-risk diffuse large B-cell lymphoma (DLBCL) or high-grade B-cell lymphoma (HGBL), at ASCO 2026 (Abstract LBA7000), with simultaneous publication in The Lancet on May 30, 2026 (Incyte release; Lenz et al., Lancet, doi:10.1016/S0140-6736(26)00866-4). The triplet reduced the risk of disease progression or death by 25% versus R-CHOP (n=899, high-intermediate to high-risk), and Incyte plans global regulatory submissions in first-line DLBCL.

| Term | Detail |

|---|---|

| Sponsor / licensee | Incyte (Nasdaq: INCY); worldwide rights to tafasitamab licensed from Xencor |

| Originator / royalty holder | Xencor (Nasdaq: XNCR): XmAb Fc-engineered CD19 antibody; receives tiered royalties on global net sales |

| Asset | Tafasitamab (Monjuvi / Minjuvi): humanized Fc-modified CD19 monoclonal antibody, plus lenalidomide and R-CHOP |

| Indication | First-line previously untreated high-risk DLBCL / HGBL |

| Data | frontMIND Phase 3; 25% reduction in risk of progression or death vs R-CHOP; n=899; ASCO Abstract LBA7000; The Lancet May 30, 2026 |

| Date | Sat May 30, 2026 |

- Royalty-stack cross-reference. Tafasitamab is Xencor-discovered and licensed worldwide to Incyte (via the former MorphoSys franchise), with Xencor earning tiered royalties on global net sales. A capped portion of Xencor's Monjuvi / Minjuvi royalty was sold to OMERS in November 2023 (the Monjuvi component of a $215M Xencor royalty-monetisation package, structured to run until OMERS recovers roughly 1.3 times its purchase price). A positive first-line DLBCL readout materially expands the addressable base for that royalty line, so OMERS, not an aggregator like Royalty Pharma, is the royalty-relevant holder re-rated here.

ADC Therapeutics LOTIS-5 Phase 3 Confirmatory Readout, ZYNLONTA plus Rituximab in Relapsed or Refractory DLBCL (Wed June 3)

ADC Therapeutics (NYSE: ADCT; Lausanne) reported topline Phase 3 LOTIS-5 confirmatory data for ZYNLONTA (loncastuximab tesirine-lpyl), a CD19-directed antibody-drug conjugate, in combination with rituximab versus standard immunochemotherapy R-GemOx in relapsed or refractory diffuse large B-cell lymphoma (r/r DLBCL) after one or more prior lines (ADCT release; 8-K, SEC). The trial met its primary endpoint of progression-free survival with statistical significance (HR 0.73, p=0.008, median PFS 6.1 versus 4.7 months) and showed no detrimental effect on overall survival (HR 0.96), with a higher complete-response rate and longer duration of complete response. Overall treatment-emergent adverse-event rates were similar between arms, though serious, Grade 5, and withdrawal events were more frequent with ZYNLONTA plus rituximab, particularly in patients aged 75 and older. ZYNLONTA holds FDA accelerated approval (2021) in third-line-plus DLBCL; LOTIS-5 is the confirmatory trial. ADCT plans a pre-sBLA FDA meeting in August and an sBLA filing in Q4 2026.

| Term | Detail |

|---|---|

| Sponsor | ADC Therapeutics SA (NYSE: ADCT; Lausanne) |

| Asset | ZYNLONTA (loncastuximab tesirine-lpyl): CD19-directed antibody-drug conjugate with a pyrrolobenzodiazepine payload, plus rituximab |

| Indication | Relapsed or refractory DLBCL after one or more prior lines (2L+); confirmatory for the 2021 accelerated approval in 3L+ |

| Data | LOTIS-5 (NCT04384484); PFS HR 0.73 (p=0.008), mPFS 6.1 vs 4.7 months; OS HR 0.96 (no detriment); higher CR rate and DoCR; serious/Grade 5/withdrawal events higher with Lonca-R, especially age 75+ |

| Royalty holder | HealthCare Royalty (HCRx): synthetic royalty on worldwide ZYNLONTA net sales and licensing revenue |

| Regulatory path | Pre-sBLA FDA meeting targeted August 2026; sBLA filing targeted Q4 2026 |

| Date | Wed June 3, 2026 |