Explainer: Why a Licensing Royalty and a Financing Royalty Are Not the Same Thing

Both are quoted as a percentage of net sales. That shared unit is the entire source of the confusion, and untangling it is the point of this explainer.

If you read pharmaceutical deal announcements for a living, you have seen the same word do two completely different jobs. A licensing partnership is announced with "tiered royalties on net sales."

A royalty monetization is announced with a company selling "a royalty" for an upfront sum. The natural inference, that a licensee and a royalty buyer are doing variations on one thing, paying cash now for a slice of sales later, is wrong in the way that matters most.

This explainer sets out the distinction cleanly, then tests it against named transactions from late 2025 and 2026. The short version: a license transfers the right to run the drug, and the royalty is the recurring price of that right; a royalty financing transfers only a claim on cash, and keeps the financier off the operating path entirely. Everything below is an elaboration of that one sentence.

Start With the Question That Actually Separates Them

Do not start with how the payment is calculated. Both instruments calculate it the same way, as a percentage of net sales, which is exactly why the calculation tells you nothing. Start instead with two questions:

- What did the counterparty receive in exchange for the cash?

- Who controls the drug's path from molecule to market after the deal closes?

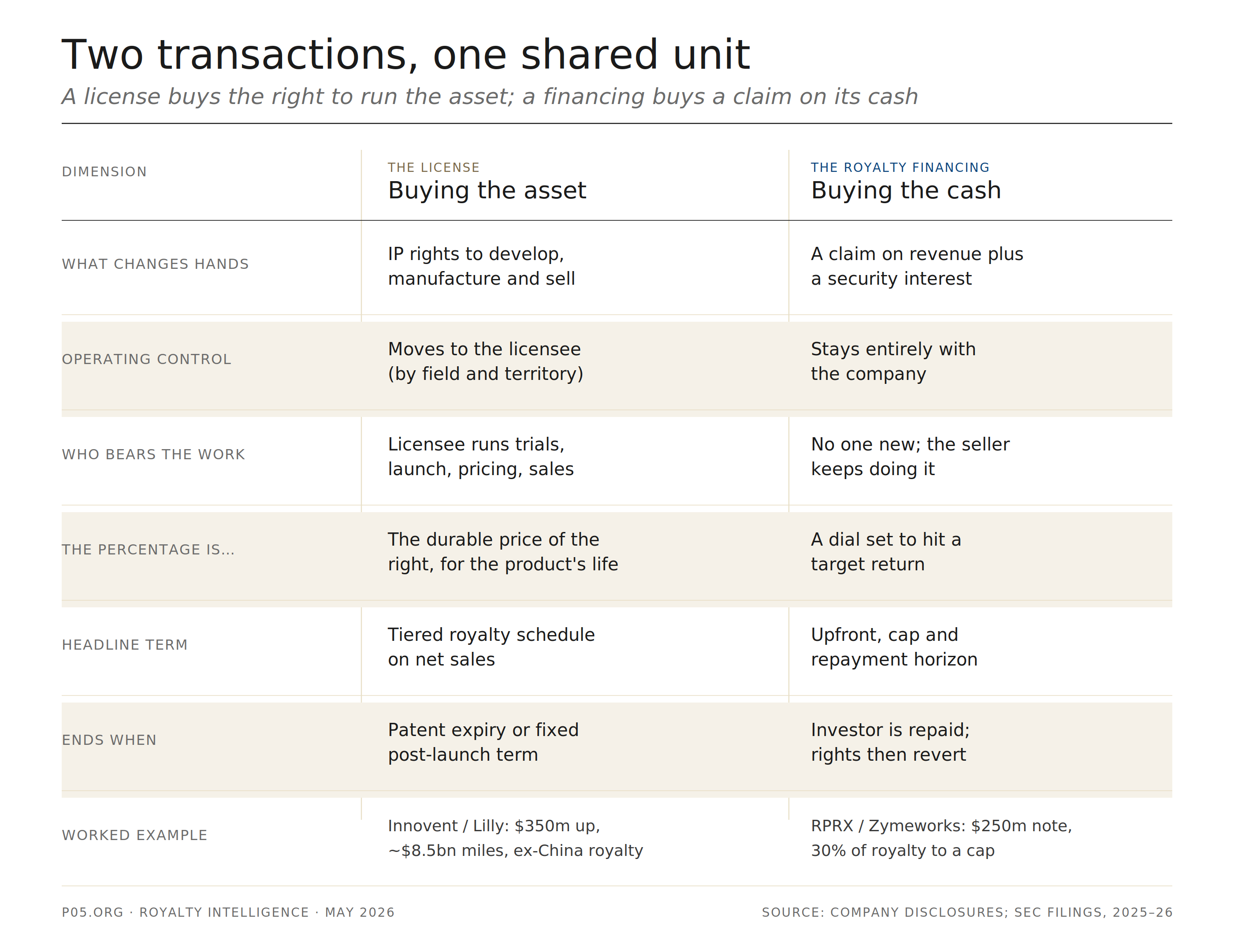

In a license, the counterparty receives the right and the obligation to move the asset down that path: to run the trials, file with regulators, manufacture, price, promote and book the sales. Control moves to them.

In a royalty financing, the counterparty receives a contractual claim on a stream of money and, usually, a security interest as backstop. It receives no operating rights, and in the well-structured cases it is contractually barred from touching the path at all. Control stays exactly where it was.

Hold those two questions in mind and the instruments never blur again.

The License: You Are Buying the Asset, the Royalty Is the Price

A pharmaceutical license is a transfer of intellectual property rights. The licensee gains the right to develop, manufacture or commercialize the asset in a defined field and territory, and pays the licensor across three canonical components: an upfront at signing, milestones triggered by development, regulatory and commercial events, and an ongoing royalty as a percentage of net sales.

The royalty here is a price for access. It is the recurring compensation the licensee pays for the continued right to exploit the IP, and for a successful product it typically carries the majority of the deal's expected net present value, because it is the only uncapped component and runs, tiered and escalating, for the commercial life of the drug.

What the licensee buys is not a cash flow. It is the right to generate one through its own capital and effort. The structure of recent deals shows the division of labour explicitly.

In the Innovent and Eli Lilly collaboration announced in February 2026, Innovent leads development through Phase 2 proof-of-concept in China and keeps Greater China rights, while Lilly takes an exclusive license to develop and commercialize everywhere outside Greater China, for 350 million dollars upfront, up to roughly 8.5 billion in milestones, and tiered royalties on ex-China net sales.

The royalty is the price Lilly pays Innovent, for the life of each product, for the right to be the company that sells it.

Three recent licenses, read straight from the announcements:

| Deal (announced) | Upfront | Milestones | Royalty term | What the counterparty acquired |

|---|---|---|---|---|

| Innovent / Lilly (Feb 2026) | $350M | up to ~$8.5B | Tiered on net sales ex-Greater China | Exclusive ex-China development and commercialization rights |

| Manifold Bio / Roche (Feb 2026) | $55M | up to ~$2B | Tiered, with a co-fund-for-enhanced-royalty option | License to Manifold's BBB-shuttle targets; Manifold keeps a co-fund right |

| Kaigene / Celltrion (Feb 2026) | $8M | up to $736M | Tiered on net sales | Exclusive license, autoimmune therapeutics |

Note the Manifold row in particular. The licensor retains a right to co-fund one program in exchange for enhanced royalties. That is the defining lever of a licensing royalty and one a financing royalty can never offer: a larger share of upside earned by taking on more of the operating risk.

The royalty rises because the licensor does more of the work, not because it lends more money.

The Financing: You Are Buying the Cash, Not the Asset

A royalty financing is a capital raise. No IP changes hands, no commercialization rights transfer, and the counterparty acquires no role in how the drug is developed or sold. The market has split into two instruments, and a specialist should never conflate them.

Traditional royalty monetization is the sale of a pre-existing royalty receivable. A party that already earns a royalty, usually from a prior out-license, sells that stream for a lump sum.

Royalty Pharma's December 2025 purchase of PTC Therapeutics' remaining royalty on Roche's Evrysdi, for 240 million dollars upfront plus up to 60 million in sales-based milestones, is the clean case: PTC was the passive licensor on a Roche-commercialized drug and sold that passive entitlement. Roche's license and Roche's operating control are untouched.

Synthetic royalty financing creates a new royalty where none existed, layered on a company's own product sales. Sagard describes the revenue interest financing structure as a blend of structured credit and royalty mechanics that lets the marketer keep full operational control of its clinical and commercial plans.

The retention of control is the structural heart of the matter: Covington's synthetic royalty guidance draws the contrast directly, noting that, unlike out-licensing, a synthetic royalty lets the seller keep control over the IP and commercialization. The financier holds a claim and a lien; it does not hold a vote.

Four recent financings, by the terms that actually govern them:

| Deal (announced) | Type | Capital | What governs the return | Operating control |

|---|---|---|---|---|

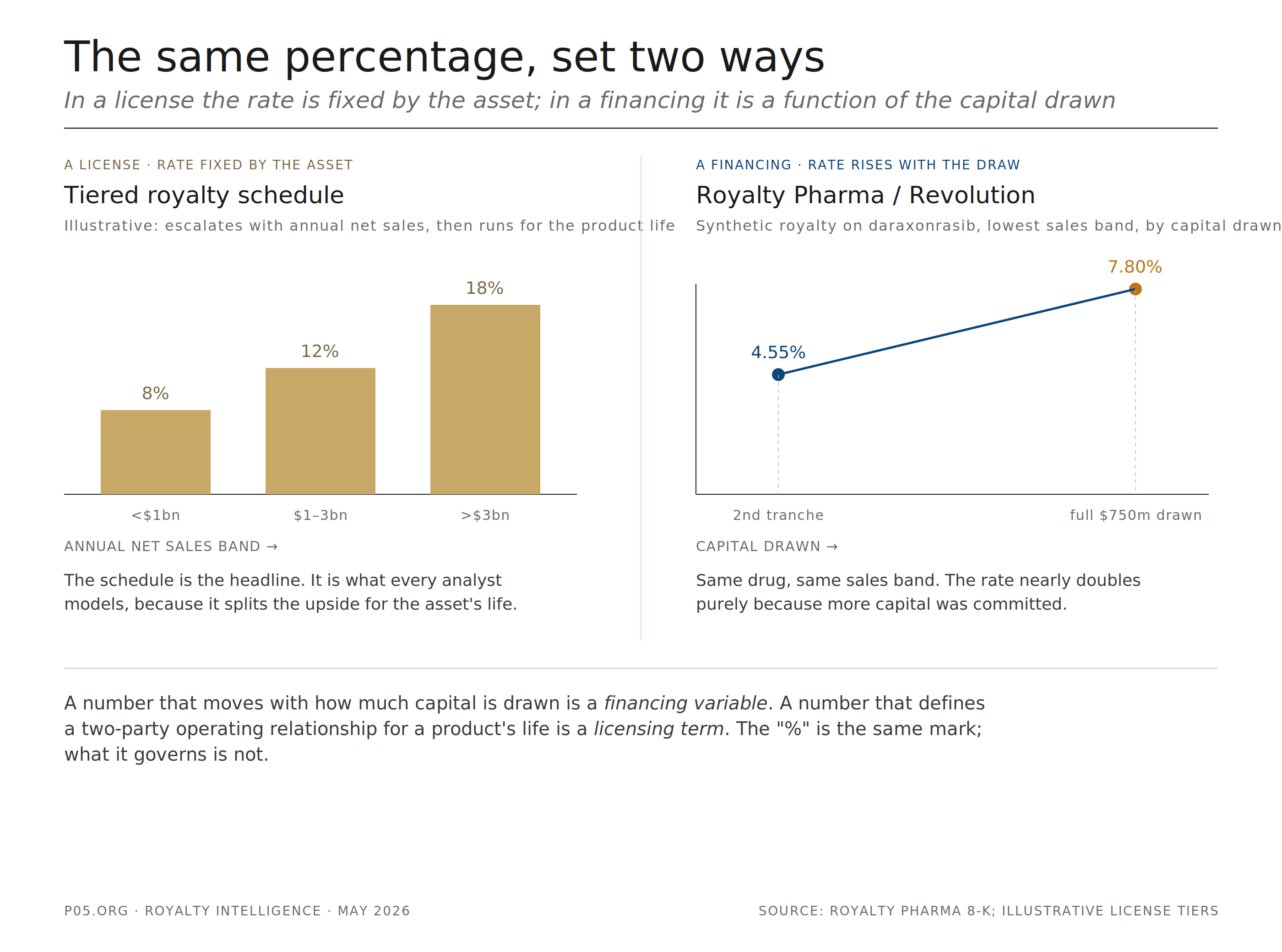

| RPRX / Revolution Medicines (Jun 2025) | Synthetic + secured loan | up to $1.25B synthetic, up to $750M loan | Tiered rate stepping up with the draw: 4.55/2.50/1.00% → 7.80/4.55/2.40% across sales bands | Retained by Revolution |

| RPRX / Zymeworks (Mar 2026) | Non-recourse royalty-backed note | $250M | 30% of Zymeworks' Ziihera royalty until repaid, to a pre-specified cap | Retained by Zymeworks; Jazz/BeOne commercialize |

| RPRX / PTC (Evrysdi) (Dec 2025) | Traditional monetization | $240M + up to $60M | Outright purchase of a pre-existing receivable | Untouched; Roche commercializes |

| RPRX / BeOne (Imdelltra) (Aug 2025) | Royalty interest acquisition | $885M upfront | Purchase of a royalty interest from BeOne | Untouched; Amgen commercializes |

The headline in every financing is the capital and its recovery profile: the upfront, the cap, the repayment limit, the draw-linked step-up. The percentage, where disclosed at all, is downstream of those.

The Tell: Why the Rate Headlines a License but Hides in a Financing

The cleanest external signal is what gets disclosed, and it follows from what the rate governs.

In a license, the royalty rate is the answer to the question every analyst is modelling: for the commercial life of this product, how is the upside split between discoverer and seller. A large upfront paired with tiered royalties starting above the mid-teens signals a contested auction and a validated data package. The rate is information about the asset, so it is reported, and reported as a tiered schedule because the schedule is the durable term.

In a financing, the rate is endogenous to the return target, so it is disclosed loosely or not at all.

The Zymeworks note is described in terms of 250 million dollars of capital, repayment from 30% of an existing royalty, a pre-specified repayment limit, and reversion of full rights once Royalty Pharma is repaid; the effective rate on Ziihera sales is given only as "approximately low to mid-single digit upward tiering," a derived figure, because the deal is defined by the capital and the cap.

The Revolution Medicines structure proves the point from the opposite direction. The synthetic royalty rate on daraxonrasib is not a property of the drug; it rises with the amount of capital drawn.

At the second tranche it is 4.55% on the lowest sales band; if Revolution draws the full optional 750 million, that same band's rate climbs to 7.80%. Same drug, same sales, nearly double the rate, purely because more money was committed. A number that moves with draw size is a financing variable. A number that defines a two-party operating relationship for a product's life is a licensing term.

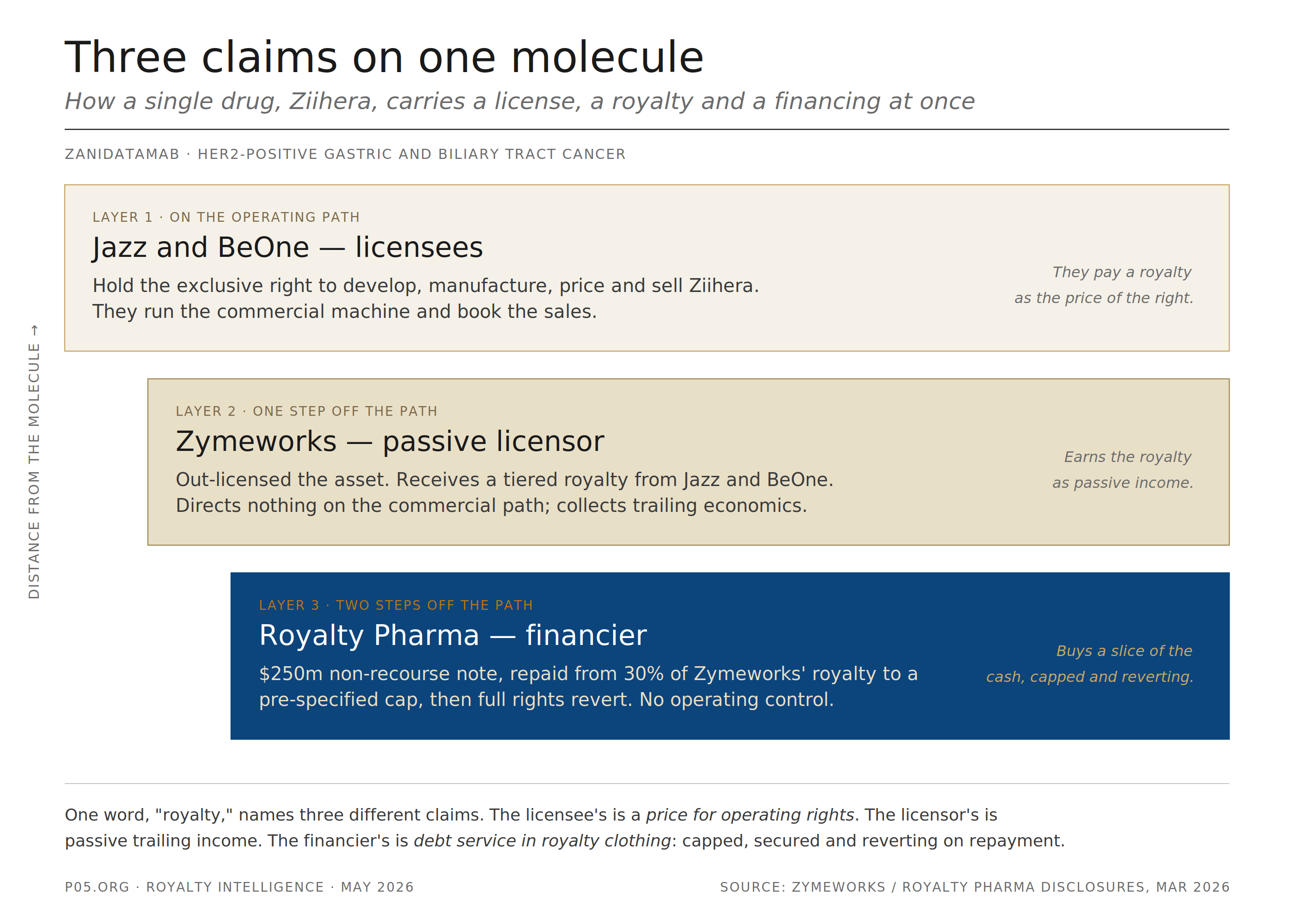

The Stacked Case: Three Royalties on One Molecule

The strongest proof that the two transactions are orthogonal is that they can sit on the same drug at the same time. Ziihera (zanidatamab) carries all three layers at once, and each is documented publicly.

Layer one is the license. Zymeworks out-licensed zanidatamab; Jazz Pharmaceuticals and BeOne Medicines commercialize it and owe Zymeworks a tiered royalty. The operating path belongs to Jazz and BeOne. Zymeworks is the passive licensor, and its royalty is the price the marketers pay for the right to sell the drug.

Layer two is the financing. In March 2026 Zymeworks raised 250 million dollars from Royalty Pharma via a non-recourse royalty-backed note, repaid from 30% of the Ziihera royalty Zymeworks receives, to a pre-specified limit, after which full rights revert to Zymeworks. Royalty Pharma touches nothing on the operating path; it does not develop, sell, or direct anyone. Zymeworks put the proceeds into share repurchases and runway beyond 2028, uses unrelated to the molecule.

Layer three is the accounting frame on the buyer's side. In its own Q1 2026 disclosure, Royalty Pharma records the transaction as having "acquired a royalty interest in Ziihera from Zymeworks for 250 million dollars," the buyer's label for the same instrument Zymeworks books as a non-recourse note.

So on one drug: Jazz and BeOne are on the operating path as licensees; Zymeworks sits one step off it as passive licensor; Royalty Pharma sits a further step off as financier of Zymeworks' passive position. Three parties, three different relationships to the molecule, one word, "royalty," attached to percentages that mean three different things. The licensee's royalty is a price for operating rights. The licensor's is passive trailing income. The financier's is debt service in royalty clothing, capped and reverting.

A Three-Step Reading Test

To classify any deal reliably, run three checks.

1. What did the counterparty receive? The right to develop, manufacture, price or sell makes it a license, and the royalty is the recurring price of that right. A claim on cash plus a security interest makes it a financing, and the royalty is a return calibration. Jazz and BeOne received the right to sell Ziihera; Royalty Pharma received 30% of a cash stream to a cap.

2. Where does operating control sit after close? A license moves control of the asset to the counterparty, in whole or by field and territory. A financing leaves control entirely with the company. The retention of operational control is the structural signature of the synthetic and note structures. A counterparty that cannot direct development or commercialization is a financier, not a partner, whatever the instrument is called.

3. Read the disclosed terms for their grammar. A prominent tiered royalty against net sales, paired with upfront and milestones, stated as a schedule that runs for the product's life, is licensing grammar. An upfront paired with a cap or repayment limit, a defined recovery horizon, a draw-linked or stepped rate, reversion on repayment, and a backup lien is financing grammar, and the percentage, if given, is derived rather than primary.

The Innovent tiered ex-China schedule is the former; the Revolution Medicines draw-linked step-up and the Zymeworks "low to mid-single digit" are the latter.

The percentage sign is the same mark in both cases. What it governs, who is responsible for turning the molecule into sales after the cash changes hands, could not be more different. The deals that confuse the market are precisely the ones where the number travels alone, detached from that question.

All information in this article was accurate as of the publication date and is derived from publicly available sources including SEC filings, company press releases, law firm publications, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.