Fund of the week: M Ventures

What is M Ventures?

M Ventures is the strategic corporate venture capital arm of Merck KGaA, Darmstadt, Germany, the German science and technology group with operations spanning pharmaceuticals, life science tools and bioprocessing, and electronics materials. Founded in 2009 with an initial focus on healthcare drug development, M Ventures has progressively expanded its mandate, doubled in scale through successive parent-company commitments, and now operates as one of the largest and most active corporate venture capital units in European life sciences and deep technology.

M Ventures has cumulatively invested in more than 100 companies since inception, currently holds a portfolio of 114 companies as of December 2025, and operates with what its parent calls an "evergreen" structure: capital is allocated by the parent rather than raised from external limited partners, and proceeds from exits recycle back into further investments. The fund operates with a deliberately dual mandate: financial returns alongside strategic alignment with the long-term R&D and commercial priorities of Merck KGaA, Darmstadt, Germany.

This dual focus distinguishes M Ventures from purely financial life sciences VCs and from many corporate venture units that prioritise strategic returns over financial discipline.

For pharmaceutical royalty investors, biotech VCs, and licensing executives, M Ventures matters for three reasons. First, it is one of the most consistent corporate co-investors in European Series A and Series B biotech rounds, often setting valuations and round structures alongside specialist VCs.

Second, it operates as a reliable spin-off creator from Merck KGaA's own Healthcare R&D pipeline, with Calypso Biotech (acquired by Novartis in 2024 for up to $425 million) being the most prominent recent example. Third, its portfolio is concentrated in areas where royalty and licensing transactions are increasingly active: DDR oncology, RNA-modifying enzymes, spatial biology, AI-enabled drug discovery, and next-generation antibody platforms.

This piece focuses on M Ventures specifically: its mandate, capital structure, parent-company relationship, portfolio composition, leadership team, exit history, and relevance to the commercial life sciences capital markets.

Overview and Investment Focus

M Ventures invests across two primary verticals (Biotechnology and Technology) covering four sectoral focus areas: Healthcare drug development, Life Science tools, Electronics, and Frontier Technology & Sustainability. The fund is headquartered in Amsterdam, with offices in Germany, the United States, and Israel, and operates an Israel Bioincubator that supports company creation from Israeli academic research.

Investment Thesis: M Ventures' thesis rests on three propositions. First, that the most consequential biotech and deep-tech innovations originate from academic and entrepreneurial settings rather than from inside large corporate R&D, and that a corporate-backed venture fund with privileged information about the parent's long-term strategy is uniquely positioned to identify and back those innovations early.

Second, that strict separation between the venture fund and the parent's commercial business units (the "Chinese Wall" or information firewall) is essential to maintaining both fiduciary discipline toward portfolio companies and the credibility required to syndicate with leading specialist VCs. Third, that the convergence between biotech and technology, particularly through AI-enabled discovery, single-cell and spatial biology, and synthetic biology, requires a venture investor that operates fluidly across both spaces rather than treating them as separate programs.

The fund describes its mandate as financing "innovative technologies and products with the potential to significantly impact" the core business areas of Merck KGaA, Darmstadt, Germany, while maintaining the option to invest in adjacent or earlier-stage technologies that could open new commercial opportunities for the group over a five-to-ten-year horizon.

The investment style is hands-on: M Ventures regularly takes board seats, leads or co-leads rounds at Series A and Series B, and participates actively in company-building, recruitment, and follow-on financings.

Background and Formation

M Ventures (originally Merck Ventures) was founded in 2009 as the corporate venture capital arm of Merck KGaA, Darmstadt, Germany. The initial mandate was healthcare-focused: investing in early-stage biotech companies whose science aligned with the parent's pharmaceutical R&D priorities.

The fund operated for its first seven years entirely within healthcare, building an early portfolio that included ObsEva (NASDAQ IPO), EpiTherapeutics (sold to Gilead), and Prexton Therapeutics (acquired by Lundbeck for close to $1.1 billion in 2018), establishing an early track record that made the case for the fund's continuation and expansion.

In 2016, the mandate was broadened to include Life Science tools and selected technology areas, reflecting Merck KGaA's repositioning of itself as a science and technology group rather than a pure pharmaceuticals company.

This expansion brought in technology partners and broadened the investment scope into electronics, semiconductor materials, and frontier technology areas including synthetic biology, alternative proteins, and advanced computing. The 2016 expansion also coincided with the parent's strategic emphasis on the convergence of biotech and technology, particularly in AI-enabled discovery and lab automation.

The parent company has incrementally increased M Ventures' capital allocation three times since inception. The initial commitment was approximately €100 million, expanded to €300 million by the mid-2010s, and in December 2021 the parent committed an additional €600 million (approximately $677 million at the time) to be deployed over the following five years. This third increase brought cumulative parent-company allocations to approximately €900 million, making M Ventures one of the larger corporate venture capital arms in European life sciences.

Parent-company rationale, as articulated by Belén Garijo (Chair and CEO of Merck KGaA, Darmstadt, Germany), framed the increase as recognition of M Ventures' track record as a leading partner to the biotech and tech venture ecosystems globally.

Strategic Differentiators

Evergreen structure with strategic alignment. M Ventures does not raise external limited partner capital or operate on a fixed fund cycle. The parent allocates capital, and exits recycle back into further investment. This structure removes the time pressure inherent in conventional ten-year fund vintages and allows M Ventures to hold positions through extended development cycles without forced exits.

Combined with the strategic-plus-financial dual mandate, this means M Ventures can underwrite very long-duration biotech bets that conventional VCs would struggle to justify within their fund life.

Operational alignment with a research-intensive corporate parent. Merck KGaA, Darmstadt, Germany operates one of the largest pharmaceutical and life sciences R&D programs in continental Europe, alongside its electronics business. M Ventures has visibility into the parent's long-term R&D and commercial strategy through structured information channels (formally separated from individual portfolio companies by a "Chinese Wall" or information firewall) that allow the fund to anticipate where strategic value can be created without compromising portfolio company independence.

Portfolio companies including Artios Pharma have entered into multi-asset partnerships with the parent, illustrating the channel.

Spin-off creation as a parallel business line. Beyond external investments, M Ventures actively creates and finances spin-offs from Merck KGaA's own R&D pipeline. Calypso Biotech, an anti-IL-15 monoclonal antibody company spun out of Merck KGaA's healthcare business, was acquired by Novartis in 2024 for up to $425 million. This spin-off pathway is operationally distinct from external investing and provides Merck KGaA with a structured way to monetise non-core internal assets while retaining strategic optionality through M Ventures' equity position.

Israel Bioincubator and academic spin-off platform. M Ventures operates an Israel-focused company creation programme, the Israel Bioincubator, with the explicit aim of advancing innovative academic research toward independent companies with global ambition.

This programme provides proprietary deal flow into Israeli biotech that is structurally hard for external funds to replicate without local presence and local academic relationships.

Cross-pollination between biotech and technology teams. Since the 2016 expansion, M Ventures has progressively integrated its biotech and technology teams. AI-enabled drug discovery, lab automation, single-cell analysis, and protein design sit at the intersection of both verticals, and the fund's structure allows for joint deal evaluation that pure-biotech or pure-tech funds cannot easily achieve. The parent's recent partnership with Imec on preclinical model technology, alongside portfolio company Genopore's collaboration with Imec on protein identification, illustrates this convergence operationally.

Parent Company and Capital Structure

M Ventures is structurally distinct from a private VC fund. It does not raise capital from external limited partners, does not operate a closed-end fund vintage, and does not return distributions to LPs at the end of a defined fund life. Instead, capital is allocated by Merck KGaA, Darmstadt, Germany, the parent group, in periodic commitments. Exits and dividends recycle into further investment, supporting the fund's evergreen mandate.

Capital allocation history:

| Date | Allocation Event | Cumulative Approx. | Notes |

|---|---|---|---|

| 2009 | Founding allocation | ~€100M | Healthcare focus only |

| ~2014 | Second increase | ~€200M | Within healthcare mandate |

| 2016 | Mandate expansion | ~€300M | Added Life Science tools, Electronics, Frontier Tech |

| December 2021 | Third increase: +€600M | ~€900M | 5-year deployment plan; broader cheque sizes |

| 2026 | Active deployment | >€900M | Record deal year in 2024; capital actively being put to work |

Merck KGaA, Darmstadt, Germany itself is a publicly listed German company (FWB: MRK; not affiliated with the separate US-based Merck & Co., Inc.), with three operating sectors (Healthcare, Life Science, and Electronics) generating roughly €21 billion in annual revenue. The group is majority-controlled by the Merck family, providing a long-horizon shareholder structure that complements M Ventures' evergreen mandate. The parent's October 2025 Capital Markets Day confirmed the strategic focus on Process Solutions, the new Rare Diseases portfolio, and Semiconductor Solutions as the engines of future growth, all areas with direct M Ventures alignment.

The Chinese Wall structure between M Ventures and Merck KGaA's commercial business units is operationally important. It allows the fund to invest in companies whose technologies might compete with or complement parent-company priorities without information contamination in either direction.

In practice, this means M Ventures portfolio companies can negotiate independently with Merck KGaA, Darmstadt, Germany business units, and the parent's BD and licensing teams treat M Ventures portfolio companies as third-party negotiating partners. Several portfolio companies (notably Artios Pharma) have entered into significant licensing partnerships with the parent on this basis.

For context, M Ventures is one of several corporate venture units in European life sciences. Comparable peers include Novartis Venture Fund, Bayer Leaps, Boehringer Ingelheim Venture Fund, Sanofi Ventures, and the separately operated MRL Ventures Fund of Merck & Co., Inc. (Rahway, NJ). M Ventures distinguishes itself within this peer group by the breadth of its mandate (biotech plus deep technology) and by the evergreen capital structure.

Royalty and Strategic Income Positions

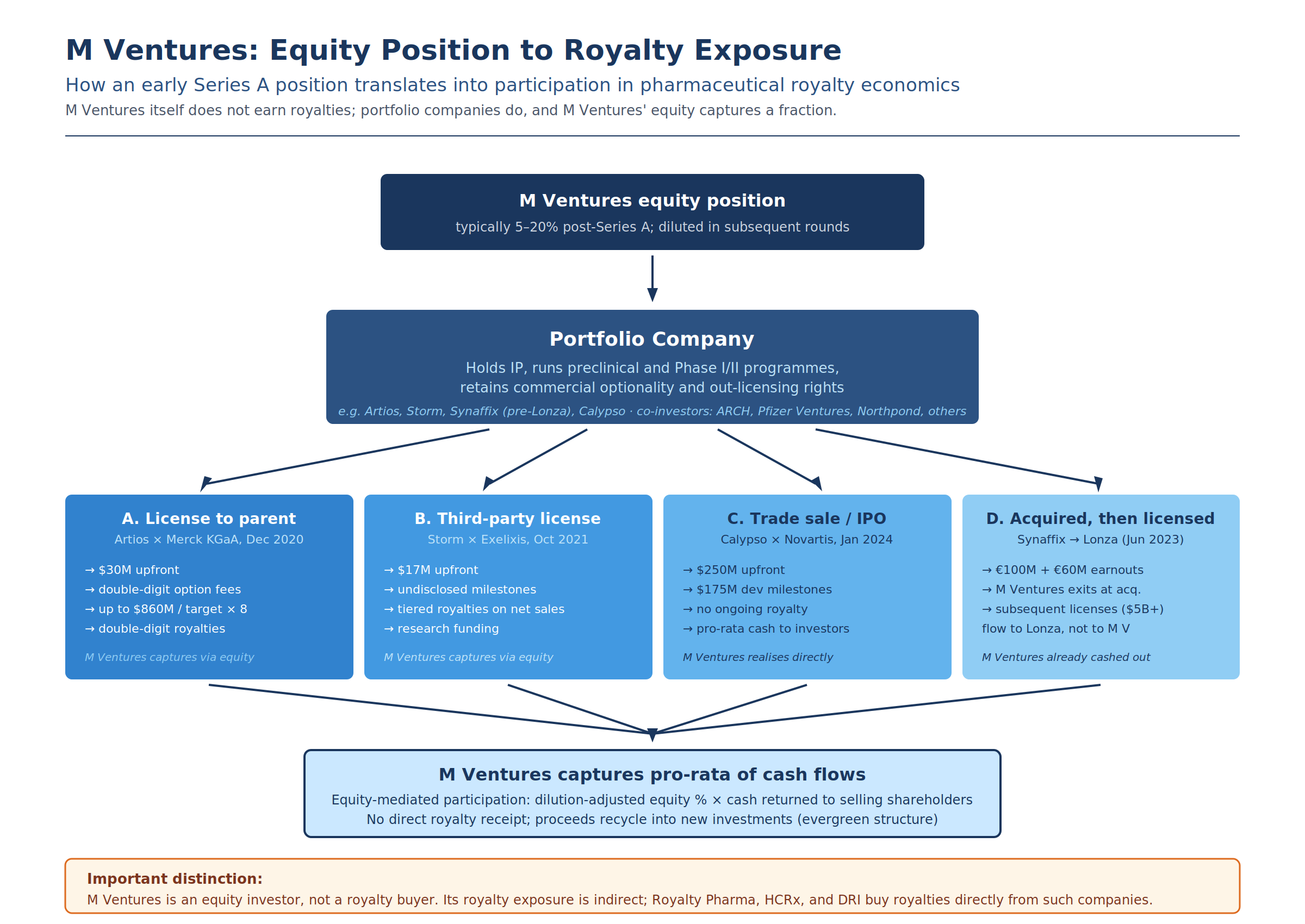

M Ventures invests primarily through equity. It does not maintain a pharmaceutical royalty portfolio, does not issue royalty-backed debt, and does not earn ongoing royalty income on the products its portfolio companies develop. This is a structural difference from royalty-focused funds like Royalty Pharma, HealthCare Royalty Partners, or DRI Healthcare Trust, which buy royalty interests directly. M Ventures' royalty exposure is indirect, mediated entirely by equity ownership of portfolio companies whose own licensing agreements include royalty terms.

That equity-mediated exposure is nonetheless substantial, because several portfolio companies have entered into licensing agreements with substantial milestone and royalty structures attached. Understanding how these agreements work, and how much of the headline value typically converts to realised cash, is essential to assessing the fund's underlying economics.

The Artios × Merck KGaA agreement: anatomy of a strategic royalty stack

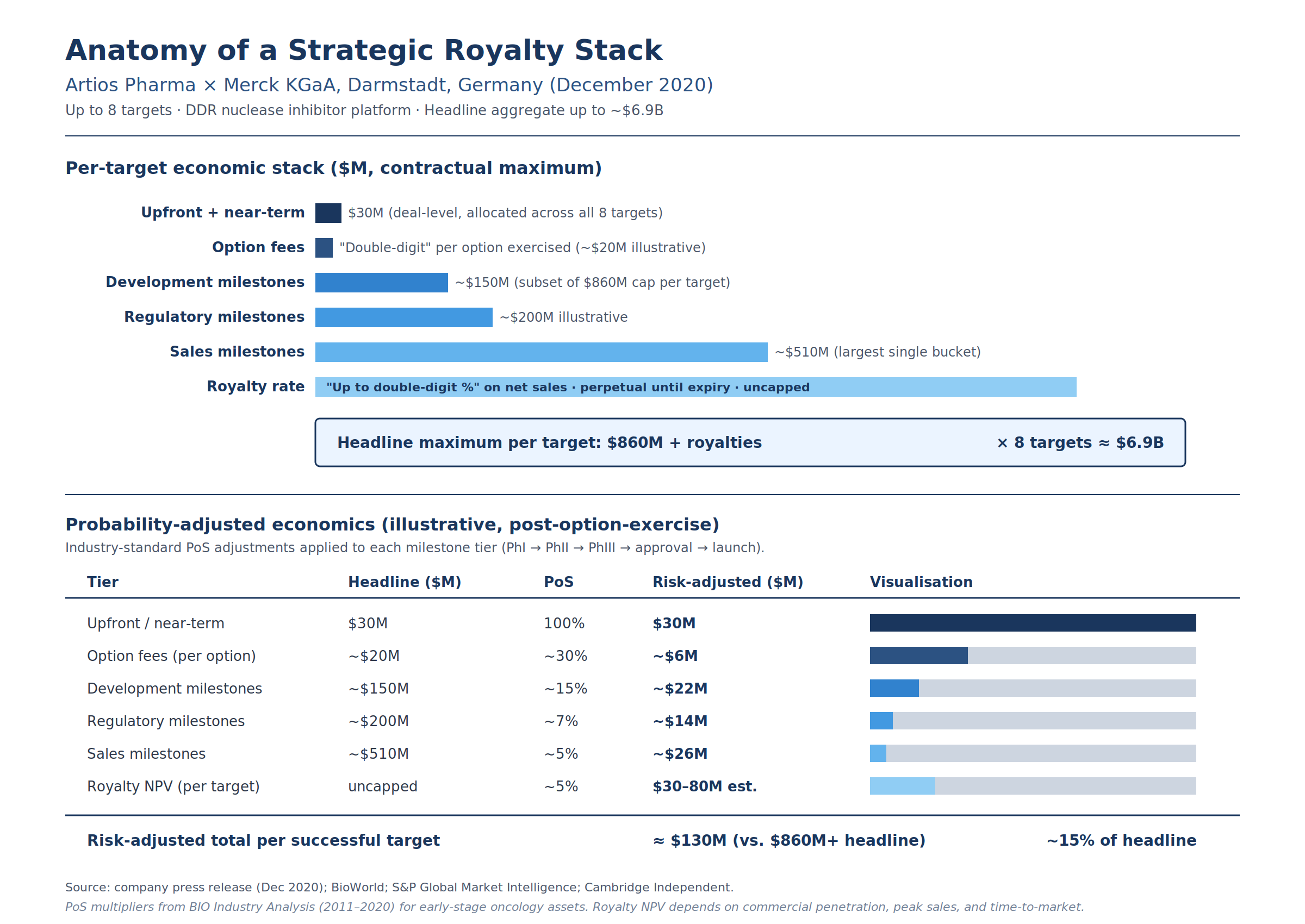

The most prominent royalty-bearing agreement involving an M Ventures portfolio company is the December 2020 strategic collaboration between Artios Pharma and Merck KGaA, Darmstadt, Germany. The deal is structured as a research collaboration with option-based licensing rights for up to eight DDR (DNA damage response) nuclease targets, and demonstrates the typical architecture of strategic-pharma royalty stacks.

Per public disclosures from Artios, BioWorld, and S&P Global, the deal terms are: $30 million in upfront and near-term payments at the deal level, double-digit option fees per target if Merck KGaA exercises its option to develop and commercialise, and up to $860 million per target in development, regulatory, and sales milestones across all eight targets, plus up to double-digit royalty rates on net sales of any product Merck KGaA commercialises. Aggregate headline value: approximately $6.9 billion if all eight options are exercised and all milestones achieved.

The royalty stack architecture has five distinct economic tiers, each with very different probabilities of payment. Upfront payments are realised on signing. Option fees are realised only if Merck KGaA exercises its option, which typically requires the partner to have generated convincing preclinical or early clinical proof-of-concept.

Development milestones are tied to clinical trial initiation and progression (Phase I start, Phase II start, Phase III start). Regulatory milestones are tied to approval events (FDA, EMA, other regions). Sales milestones are tied to cumulative net sales thresholds, typically $250 million, $500 million, $1 billion, $2 billion, and so on. Royalties are tiered percentages applied to net sales, typically stepping up at higher revenue thresholds.

Applying industry-standard probability of success (PoS) multipliers from BIO Industry Analysis to a single oncology asset (roughly 30% probability for option exercise after early clinical work, 15% for Phase III start, 7% for approval, and 5% for commercial success) produces a risk-adjusted value of approximately $130 million per target, or roughly 15% of the headline $860 million. For the full eight-target deal, the risk-adjusted aggregate is around $1 billion, against the $6.9 billion headline.

The royalty NPV component depends on commercial penetration, peak sales, and time to market, and contributes a meaningful share of risk-adjusted value precisely because royalties are perpetual rather than capped.

For M Ventures, the relevant economic question is what fraction of any realised value flows to its equity position in Artios. This depends on the dilution-adjusted equity stake (typically declining round by round as the company raises further capital), the timing of any liquidity event, and whether Artios remains independent or is acquired before licensed products reach market. The Artios Series D in November 2025, at $115 million with M Ventures continued participation, suggests the company is on a path to extended independence rather than near-term acquisition.

Other royalty-bearing licensing agreements in the M Ventures portfolio

Beyond the Artios deal, several other M Ventures portfolio companies have executed licensing agreements with royalty-bearing structures. The pattern is consistent: modest upfront payments, substantial milestone potential, and tiered royalty rates on net sales of any successfully commercialised product.

Storm Therapeutics × Exelixis (October 2021): $17 million upfront for licensing two RNA-modifying enzyme programs (including ADAR1) plus research funding, undisclosed development, regulatory, and commercialisation milestones, and tiered royalties on net sales of any compounds commercialised under the collaboration. Exelixis is solely responsible for global development, manufacturing, and commercialisation. Storm retains separate programs (notably its METTL3 inhibitor STC-15) outside the Exelixis collaboration.

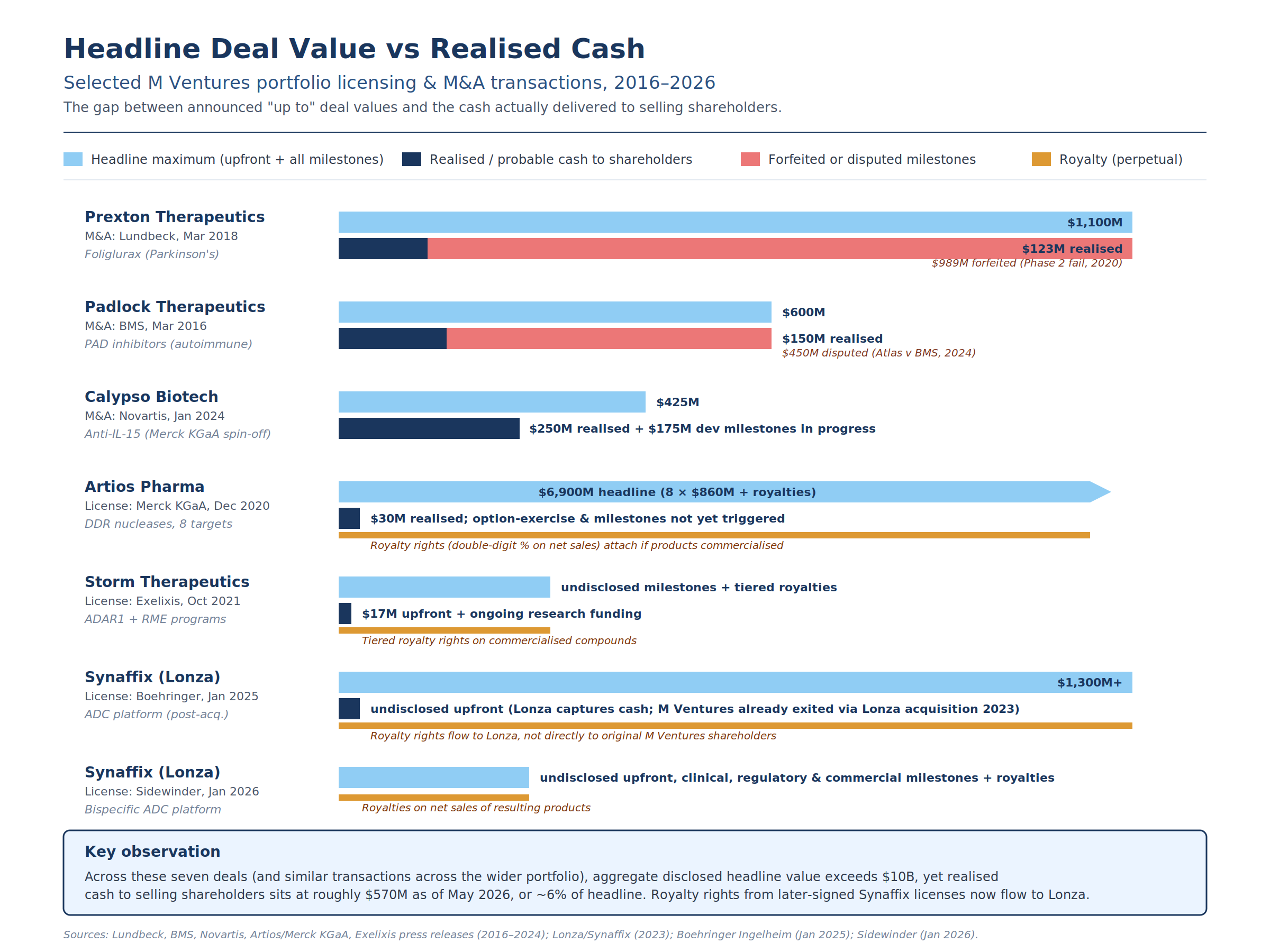

Calypso Biotech × Novartis (January 2024): not a licensing agreement but an outright acquisition. $250 million upfront to Calypso shareholders plus up to $175 million in development milestones for total deal value of up to $425 million. No ongoing royalty stream because Novartis acquired full rights to CALY-002, the lead anti-IL-15 monoclonal antibody. M Ventures, as the founding investor and largest shareholder of the Merck KGaA spin-off, captured a pro-rata share of the upfront cash and is exposed to the development milestones via the escrow / earnout structure typical of these transactions.

Padlock Therapeutics × Bristol Myers Squibb (March 2016): also an acquisition. $150 million upfront plus up to $450 million in contingent development and regulatory milestones for total deal value up to $600 million.

In December 2024, Atlas Venture and other Padlock shareholders sued BMS in Delaware Chancery Court, alleging that BMS used a "deceptive scheme involving manipulation of the patent process" to avoid making any of the milestone payments. The litigation illustrates a structural risk of milestone-heavy biotech deals: when development decisions are entirely controlled by the acquiring pharma, the seller's milestone economics depend on counterparty good faith and contractual specificity.

Prexton Therapeutics × Lundbeck (March 2018): another acquisition. €100 million upfront plus up to €805 million in development, regulatory, and sales milestones for total headline value up to €905 million ($1.1 billion). Foliglurax, the lead asset, failed its Phase 2 AMBLED trial in March 2020, and Lundbeck terminated development and wrote down the €100 million balance sheet value. The €805 million in milestones was extinguished. M Ventures, as a co-founder and major shareholder of Prexton, realised the €100 million upfront pro-rata share but received no portion of the headline milestone structure.

Synaffix and the Lonza ADC platform: a fourth pathway

The most instructive recent case from the M Ventures portfolio is Synaffix B.V., an Amsterdam-based ADC technology platform company that M Ventures backed in its 2014 Series A alongside Aravis, BioGeneration Ventures, and BOM Capital. Synaffix developed a clinical-stage site-specific antibody-drug conjugate platform (GlycoConnect, HydraSpace, toxSYN) that is now used by more than 13 pharmaceutical and biotech companies for ADC product development.

In June 2023, Lonza acquired Synaffix for €100 million in cash upfront plus up to €60 million in performance-based earnouts (€160 million headline). M Ventures, as a Series A investor since 2014 (with Investment Director Bauke Anninga representing the fund on the board until acquisition), realised its return at the acquisition.

What makes the Synaffix case particularly relevant for understanding pharmaceutical royalty economics is what happened after the M Ventures exit. Under Lonza's ownership, Synaffix has continued to sign large ADC technology licensing agreements with global pharma partners, each carrying its own royalty stack:

| Counterparty | Date | Headline value | Royalty terms |

|---|---|---|---|

| MacroGenics (original) | February 2022 | up to $586M | Royalties on commercial sales |

| Amgen, Hummingbird, Sotio (collective 2023) | 2023 | ~$5B aggregate | Royalties on commercial sales |

| MacroGenics (expansion) | March 2023 | up to $2.2B | Tiered low to high single-digit royalties |

| Sotio (separate) | October 2023 | up to $740M | Royalties on commercial sales |

| BigHat Biosciences | November 2024 | undisclosed | Royalties on net sales |

| Boehringer Ingelheim | January 2025 | up to $1.3B | Additional royalty payments |

| Sidewinder Therapeutics | January 2026 | undisclosed | Royalties on net sales of resulting products |

Aggregate headline value of Synaffix-platform licensing agreements signed during 2022–2026 exceeds $10 billion. None of those royalty rights flow back to M Ventures or to the original Synaffix investors. They flow to Lonza. The acquisition crystallised M Ventures' equity return at €160 million headline / €100 million certain, and severed any residual claim on downstream royalty economics.

This pattern is important to understand because it represents a fourth pathway distinct from the three more commonly discussed (license to parent, third-party license, trade sale or IPO of the portfolio company). When a portfolio company is acquired by a larger platform operator (Lonza, Charles River, Danaher, Thermo Fisher) that then proceeds to monetise the underlying technology through a series of licensing agreements, the royalty economics accrue to the acquirer, not to the original VC investors.

M Ventures realised its Synaffix return by exit, not by ongoing royalty participation, and the post-acquisition Synaffix licensing book illustrates how much value can be created by the acquirer in the years following.

Headline deal value vs realised cash: a critical distinction

The Prexton case is not unusual. Across milestone-heavy biotech transactions generally, the gap between announced "up to" deal values and actual cash received by selling shareholders is typically very large. Sales-tied milestones in particular convert at low rates because they require not only successful clinical development and regulatory approval but also commercial penetration sufficient to reach contractual sales thresholds.

For seven M Ventures-relevant transactions (Prexton, Padlock, Calypso, Artios licensing, Storm licensing, plus the post-Lonza Synaffix licensing book including the January 2025 Boehringer deal and January 2026 Sidewinder deal), aggregate disclosed headline value exceeds $10 billion. Realised cash to shareholders, including ongoing licensing income retained by Lonza rather than distributed to original Synaffix investors, totals approximately $570 million as of May 2026, or about 6% of headline.

The pattern is stark: upfront payments are essentially always realised; sales-tied milestones rarely are; clinical failures (Prexton) extinguish the entire back-loaded milestone structure regardless of the headline ratio; and royalty rights that arise after an acquisition flow to the acquirer, not to the original venture investors.

This is why royalty buyers in commercial markets (Royalty Pharma, HCRx, DRI, Sagard Healthcare Royalty Partners) typically prefer to buy royalty streams on already-approved products, where commercial uncertainty has been substantially resolved, rather than buying milestone payment streams on assets still in clinical development.

Equity investors like M Ventures, by contrast, accept the higher binary risk of clinical-stage assets in exchange for the upside of carried interest on successful exits, with the explicit understanding that royalty economics generally arrive too late to capture except through downstream M&A or licensing transactions that crystallise the equity value.

M Ventures' equity position to royalty exposure: the value chain

The mechanism by which M Ventures captures any value from its portfolio companies' royalty agreements is illustrated below. M Ventures itself does not earn royalties; portfolio companies do, and M Ventures' equity position captures a fraction of whatever cash the portfolio company ultimately receives from royalty-bearing transactions.

This equity-mediated structure has several implications. First, M Ventures is exposed to the same dilution mechanics as any other VC: its initial Series A position erodes with each subsequent financing round, even as the company's value grows. Second, it captures upside on royalty streams only via liquidity events (acquisition, IPO, secondary sale).

Third, in the case of an outright acquisition with milestone earnouts, M Ventures' equity-mediated participation in milestones is typically sequestered in escrow and released as milestones are achieved, with the same probability-of-payment dynamics described above. Fourth, where the acquirer is itself a platform operator that subsequently monetises the technology through downstream licensing (the Synaffix-Lonza pattern), the post-acquisition royalty book accrues to the acquirer, not to the original venture investors.

Realised exits to date

M Ventures' realised returns to date have come almost entirely through M&A and IPO exits rather than royalty income:

| Realisation Event | Year | Type | Outcome |

|---|---|---|---|

| EpiTherapeutics | 2015 | Acquisition (Gilead) | Trade sale |

| Padlock Therapeutics | 2016 | Acquisition (BMS) | $150M upfront; $450M milestones disputed |

| ObsEva | 2017 | NASDAQ IPO | Public listing |

| Prexton Therapeutics | 2018 | Acquisition (Lundbeck) | $123M upfront; $989M milestones forfeited (Phase 2 failed) |

| Progyny (NASDAQ: PGNY) | 2019 | NASDAQ IPO | Public, fertility benefits |

| Galecto Biotech | 2020 | NASDAQ IPO | $369M market cap at listing |

| Xilio Therapeutics | 2021 | NASDAQ IPO | $427M market cap at listing |

| Akili Interactive | 2022 | SPAC merger | Public via Social Capital Suvretta |

| Calypso Biotech | 2024 | Acquisition (Novartis) | $250M upfront + up to $175M milestones |

According to Tracxn data, M Ventures has cumulatively realised five IPOs and 17 acquisitions across its portfolio history. PitchBook records 38 exits across the same dataset. The discrepancy reflects the inclusion of partial liquidity events in PitchBook's count.

For commercial royalty investors, the practical implication is that M Ventures is an upstream actor whose portfolio occasionally generates assets that ultimately become royalty-eligible products through licensing deals or via acquisition by larger pharma companies. The fund itself is not a royalty counterparty, but its portfolio is a leading indicator of which therapeutic areas, modalities, and platforms may produce royalty-bearing assets in the medium term.

Portfolio of Investments

M Ventures held 114 portfolio companies as of December 2025, with nine new investments in the prior twelve months and 16 investments completed in calendar year 2025. The portfolio spans biotech (the largest single sector by company count), life science tools, electronics, and frontier technology. Geographic distribution is concentrated in the United States and the United Kingdom, with substantial European exposure (Switzerland, Netherlands, Germany, France) and selective positions in Israel.

The healthcare portfolio's most prominent active positions include Artios Pharma (DNA damage response oncology, $115 million Series D in November 2025), Storm Therapeutics (RNA-modifying enzyme inhibitors, METTL3 program in clinical development), Nucleome Therapeutics (precision genetic medicines via dark genome decoding, £37.5 million Series A in 2022), FoRx Therapeutics (synthetic lethality / DDR, $50 million Series A in December 2025 alongside Pfizer, Novartis Venture Fund, and EQT), and Nouscom (next-generation cancer immunotherapies / vaccines).

The life science tools portfolio includes Vizgen (spatial biology and multiomics, $48 million Series E in January 2026 alongside Northpond Ventures and ARCH Venture Partners), DNA Script (enzymatic DNA synthesis), Lightcast Discovery (single-cell functional analysis, $27 million round in 2025 alongside ARCH and Illumina Ventures), LabGenius Therapeutics (AI antibody discovery), Concerto Biosciences (microbial interaction discovery), Nucleai (spatial AI biomarkers, $14 million round led by M Ventures in 2025), and Abselion (analytical tools).

The electronics and frontier-tech portfolio includes Celestial AI (optical interconnects for AI compute, unicorn valuation following its 2024 round), Metalenz (metasurface optical sensing), MemryX (Edge AI processors), SeeQC (quantum computing), Mosa Meat (cultured beef, Maastricht University spin-off co-founded by Peter Verstrate and Mark Post), and Neurable (brain-computer interface).

The fund's spin-off creation track record is anchored by Calypso Biotech, spun out of Merck KGaA's healthcare business and acquired by Novartis in 2024 for up to $425 million. Other Merck KGaA spin-offs in the portfolio have followed a similar template of single-asset or platform-based companies built around technology unbundled from the parent's core R&D pipeline.

Leadership

| Person | Role | Background |

|---|---|---|

| Hakan Goker | Managing Director, Co-head; Head of Biotechnology Investments | 20+ years in biotech investing; with M Ventures since the mid-2010s; oversees Healthcare and Life Science investments |

| Javier Rodriguez | Co-head; Head of Technology Investments | Joined M Ventures 2016 as CFO; assumed Tech co-head role in mid-2025 covering Electronics and Frontier Tech & Sustainability |

| Christian Patze | Executive Director, Technology team | Promoted in 2025; semiconductor and tech investment expertise |

| Daniel Franke | Executive Director, Technology team | Promoted in 2025; semiconductor and tech investment expertise |

| Caroline Soulard | Chief Financial Officer | Took over CFO role from Rodriguez in mid-2025 |

| Björn Kuhl | Head of Business Operations | Operational and portfolio support |

| Roman Werth | Head of M&A, Strategy and Venturing, Merck KGaA, Darmstadt, Germany | Group-level oversight of M Ventures |

| Bauke Anninga | Investment Director, Healthcare | Sourced and led the Nucleome Therapeutics Series A; Global Corporate Venturing Rising Star 2023 |

Hakan Goker, Managing Director and Head of Biotechnology Investments, is the operational and intellectual leader of the fund's healthcare and life sciences activity. He has been with M Ventures for nearly a decade and was named to the Global Corporate Venturing Powerlist 2025 alongside former co-head Owen Lozman. Goker's deal track record includes the early seeding of Storm Therapeutics in 2015 and the Series A of Artios Pharma in 2016, both of which became foundation positions in the fund's RNA-and-DDR oncology thesis. He hosts a 2026 Beyond Biotech podcast discussing M Ventures' positioning and 2025 deal activity, including FoRx Therapeutics and Artios' FDA Fast Track designation.

Javier Rodriguez, Co-head and Head of Technology Investments, joined M Ventures in 2016 as CFO and assumed the Tech co-head position in mid-2025 following the departure of Owen Lozman, who had led the technology team since 2018 and went on to launch 55 North, a Copenhagen-based quantum technology fund. Rodriguez's appointment formalises the integration of finance and portfolio management discipline into the technology team's leadership at a moment when AI-driven semiconductor and photonics opportunities are accelerating.

Christian Patze and Daniel Franke were promoted to Executive Director positions within the Technology team in 2025, leading semiconductor and broader tech investment activity under Rodriguez. Caroline Soulard assumed the CFO role from Rodriguez in mid-2025. Roman Werth, Head of M&A, Strategy and Venturing at Merck KGaA, Darmstadt, Germany, provides group-level oversight of M Ventures and articulated the rationale for the 2025 leadership changes.

The team totals approximately 19 investment professionals as of late 2025 (Tracxn data), with 35 total employees including operations and finance roles, distributed across Amsterdam (headquarters), Germany, the United States, and Israel.

2025–2026 Investment Activity and Priorities

M Ventures completed 16 investments in calendar year 2025, reflecting a sustained high deployment pace following the 2021 capital expansion. The fund has also stated, through Goker's January 2026 podcast appearance, that 2026 is an inflection year for the post-2021 expansion vintage: "we're going to hit year eight for the new (post-expansion) funds, so now is when we're going to start being able to see some of those exits coming to fruition."

Recent biotech activity (2024–2026):

- FoRx Therapeutics ($50M Series A, December 2025), DDR / synthetic lethality, alongside Pfizer, Novartis Venture Fund, and EQT

- Nucleai ($14M round led by M Ventures, 2025), spatial AI biomarkers for ADCs, bispecifics, and immunotherapies

- Artios Pharma ($115M Series D, November 2025), continued support of the lead DDR position

- Vizgen ($48M Series E, January 2026), spatial biology platform, alongside ARCH Venture Partners and Northpond Ventures

- Lightcast Discovery ($27M round, 2025), single-cell functional analysis, alongside ARCH and Illumina Ventures

Recent technology activity (2024–2026):

- NovoLINC (December 2025), thermal management technology for AI chips, alongside Foothill Ventures and Hitachi Ventures

- MemryX continued support, fabless semiconductor for Edge AI

- Tignis continued support, AI/ML for semiconductor manufacturing process control

- Celestial AI support through nine-figure rounds, optical interconnects for AI compute (unicorn status)

Stated 2026 priorities, drawn from Goker's recent commentary, emphasise three areas: (1) AI-enabled drug discovery and lab solutions that compress development timelines, (2) RNA modulation and modification, particularly building on the Storm Therapeutics platform thesis, and (3) the convergence of biotech and electronics through AI-bio infrastructure.

Strengths and Competitive Advantages

Evergreen capital and patient horizons. Unlike conventional VCs operating on ten-year fund cycles, M Ventures can hold positions through extended biotech development timelines without forced exits. This is particularly valuable for platforms like Storm Therapeutics (RNA-modifying enzymes) or Artios Pharma (DNA damage response) where clinical readout cycles run multi-year and meaningful value creation often happens after a conventional fund vintage would have closed.

Strategic alignment with a research-intensive parent. Merck KGaA, Darmstadt, Germany operates one of the largest pharmaceutical and life sciences R&D programs in continental Europe, with deep expertise across oncology, immunology, neuroscience, fertility, and life science tooling. M Ventures' visibility into the parent's long-term R&D strategy gives it a structural advantage in identifying which scientific platforms are likely to attract strategic interest in five to ten years.

Spin-off creation track record. The Calypso Biotech outcome (acquired by Novartis for up to $425 million) is the clearest validation of the spin-off model. Spinning out non-core internal assets, equity-supporting them through M Ventures, and then exiting via trade sale or licensing is a repeatable model that few peer corporate venture units execute systematically.

Cross-pollination across biotech and technology. Few peer corporate venture units operate fluidly across both biotech and deep tech. The integration of these teams under a shared mandate gives M Ventures unusual reach into AI-enabled drug discovery, lab automation, single-cell biology, and protein design, all areas where the biotech-technology boundary is dissolving.

Strong syndication relationships. M Ventures regularly co-invests with leading specialist VCs including ARCH Venture Partners, Pfizer Ventures, Novartis Venture Fund, EQT Life Sciences, and Northpond Ventures. Co-investor data (Tracxn) shows 345+ co-investors across the portfolio, evidence of the fund's integration into the global life sciences syndicate ecosystem.

Geographic breadth with European depth. M Ventures' Amsterdam headquarters, Israel office, and active US activity allow it to source globally while maintaining particular strength in European biotech (UK, Switzerland, Netherlands, France, Germany), where many specialist competitors are thinner on the ground than in Boston or San Francisco.

Risks, Challenges, and Vulnerabilities

Single-funder concentration. The fund's capital base derives entirely from Merck KGaA, Darmstadt, Germany. Any material change in the parent's strategy, financial condition, or leadership priorities could affect M Ventures' deployment capacity, mandate, or institutional independence. The parent's October 2025 Capital Markets Day reaffirmed strategic focus on Process Solutions, Rare Diseases, and Semiconductor Solutions, but corporate strategy can shift, and M Ventures' continuity through such shifts is not guaranteed by structure alone.

Strategic-financial dual mandate tension. Operating with both strategic and financial objectives creates ongoing tension. Investments that look strategically attractive may not be the highest-return financial bets, and vice versa. The Chinese Wall structure mitigates this in principle, but in practice the fund's identity is bound up with the parent's commercial priorities, which can constrain investment latitude in areas where pure financial discipline would otherwise dictate.

Information firewall complexity. The Chinese Wall between M Ventures and Merck KGaA business units is essential to the fund's credibility with portfolio companies and co-investors, but it imposes operational complexity. Portfolio companies negotiating with parent-company business units must do so as third parties, and the fund's information advantage from parent visibility is bounded by what the firewall permits to flow. This is a feature, not a bug, but it does limit certain forms of value capture that might be available to a more integrated CVC structure.

Exit market dependency. The fund's realised returns to date have come primarily through M&A and IPOs. Both channels have experienced significant compression in the post-2022 biotech environment. While M Ventures has continued to see exits (Calypso, Akili Interactive), the broader market environment for biotech IPOs has been challenging, and the post-expansion vintage's ability to deliver financial returns within a reasonable horizon depends on continued recovery in trade sale and listing activity.

Talent retention and team continuity. The departure of Owen Lozman to launch 55 North, a quantum technology fund, in 2025 illustrates a common challenge for corporate venture units: senior partners with successful track records become attractive targets for independent fund formation. The internal promotion of Patze and Franke and the elevation of Rodriguez to co-head are partial mitigations, but corporate venture units often experience higher senior turnover than independent VCs once partners have built personal reputational capital.

Dependence on parent-company commercial demand for portfolio outcomes. Some of M Ventures' realised value is mediated by the parent's licensing and acquisition behaviour. If Merck KGaA, Darmstadt, Germany shifts strategic priorities away from a portfolio company's therapeutic area, the strategic value flows that justify the dual-mandate structure can erode, leaving M Ventures exposed to financial-only outcomes.

Increasing competition from independent specialist VCs. European and US specialist biotech VCs have raised substantial capital in the past five years, and the competition for the highest-quality Series A opportunities has intensified. M Ventures' value-add to entrepreneurs (parent-company strategic relationships, evergreen capital, hands-on company building) remains differentiated, but the marginal cost of accepting corporate VC capital relative to independent specialist VC capital has risen as more entrepreneurs prioritise capital provider neutrality.

Implications for the Pharmaceutical Royalty and Biotech Capital Markets

For commercial capital markets, M Ventures matters as both a deal-flow source and as an upstream signal of where Merck KGaA, Darmstadt, Germany may eventually direct licensing capital. Three patterns are worth tracking.

First, M Ventures portfolio companies regularly progress to commercial inflection points where royalty financing becomes relevant. Artios Pharma's DDR oncology pipeline, currently in Series D financing, is exactly the type of late-stage clinical asset that royalty buyers and structured credit lenders evaluate as candidates for synthetic royalty arrangements or licensing-backed debt. Royalty investors monitoring Series C and Series D announcements from M Ventures-backed companies will see early indicators of upcoming licensing activity.

Second, M Ventures' parent (Merck KGaA, Darmstadt, Germany) is itself a buyer in pharmaceutical licensing and royalty markets, with substantial historical activity in oncology, neurology, and fertility. The fund's portfolio thesis serves as a leading indicator of the parent's strategic priorities: areas where M Ventures is concentrating capital frequently align with areas where the parent's BD team is likely to pursue licensing activity within five to ten years. The Artios partnership, layered on top of the M Ventures equity position, illustrates the pattern.

Third, M Ventures' spin-off creation pathway is a relatively unusual model that life sciences finance professionals should understand. When an M Ventures portfolio company is a spin-off from Merck KGaA's own R&D pipeline (as Calypso Biotech was), the company's underlying IP, regulatory history, and strategic context are different from a typical academic-spin-out biotech. Royalty investors evaluating such companies should account for both the institutional pedigree and the structural relationships embedded in the spin-off agreement, which can affect everything from royalty stack composition to step-up provisions on subsequent licensing.

Finally, M Ventures' integration into the global syndicate ecosystem makes it a useful signal node. When M Ventures co-leads a round alongside Pfizer Ventures, Novartis Venture Fund, ARCH, or Northpond, the implied corporate-strategic interest in the underlying technology is meaningfully higher than from a pure-financial syndicate. Royalty and licensing teams who track corporate VC participation patterns can use M Ventures' presence as a partial proxy for which assets have multi-pharma strategic optionality.

Recent Developments (2024–2026)

| Date | Event |

|---|---|

| 2024 | Record deal year for M Ventures (busiest year ever, per Goker) |

| 2024 | Calypso Biotech acquired by Novartis for up to $425M |

| Mid-2025 | Owen Lozman departs to launch 55 North (Copenhagen quantum fund) |

| Mid-2025 | Javier Rodriguez appointed Co-head; takes over Tech team |

| Mid-2025 | Christian Patze and Daniel Franke promoted to Executive Director |

| Mid-2025 | Caroline Soulard becomes CFO |

| October 2025 | Merck KGaA Capital Markets Day 2025; strategic focus on Process Solutions, Rare Diseases, Semiconductor Solutions |

| November 2025 | Artios Pharma $115M Series D |

| December 2025 | FoRx Therapeutics $50M Series A (alongside Pfizer, Novartis Venture Fund, EQT) |

| January 2026 | Vizgen $48M Series E (alongside ARCH and Northpond) |

| January 2026 | Goker Beyond Biotech podcast appearance; "year eight" inflection commentary |

| 2026 | Active deployment of post-2021 expansion vintage; record-pace deal year continues |

As of May 2026, M Ventures is in active deployment mode. The post-2021 vintage is approaching its five-year deployment milestone, the 2024 deal record has been sustained into 2025, and the leadership transitions are complete. Goker's expectation, articulated in early 2026, is that the next two years should produce material exit activity from earlier portfolio investments now reaching commercial inflection.

Conclusion

M Ventures is one of the more clearly differentiated corporate venture capital units in European life sciences. Its evergreen structure, dual strategic-financial mandate, and integration with a research-intensive multi-sector parent (Merck KGaA, Darmstadt, Germany) give it a positioning that few peer corporate venture units match.

The breadth of its mandate (biotech and deep technology, healthcare and electronics, drug development and life science tools) is unusual within corporate venture capital, and the operational integration of biotech and technology teams positions it well for the AI-bio convergence that increasingly drives value creation in life sciences.

The open questions are primarily ones of execution and exit-market timing. Can the post-2021 expansion vintage deliver the financial returns that justify the fund's evergreen mandate within a reasonable horizon? Will the spin-off creation model continue to produce Calypso-scale outcomes as the parent's R&D priorities evolve? And can the team retain its senior talent in a market where successful corporate venture partners are increasingly attractive targets for independent fund formation?

For commercial life sciences capital markets, M Ventures is most relevant as an upstream signal node and as a deal-flow originator. It is not a competitor for royalty buyers, structured credit funds, or specialty pharma lenders, but its portfolio frequently produces companies that ultimately become royalty-eligible or licensing-eligible assets.

Royalty investors, biotech VCs, and licensing executives who pay close attention to M Ventures' new-investment patterns, syndicate composition, and parent-company partnership disclosures will see meaningful indicators of which therapeutic areas and platform technologies are likely to attract strategic capital over the medium term.

All information in this article was accurate as of May 2026 and is derived from publicly available sources including Merck KGaA, Darmstadt, Germany press releases, M Ventures official communications, Tracxn and PitchBook data, Global Corporate Venturing reporting, Fierce Biotech reporting, and company announcements. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.