Royalty Financing and the Share Price

Why non-dilutive capital sometimes cuts against the stock

Royalty monetisation is sold as the friendliest capital a biotech can raise.

Most of the time, the market agrees.

The interesting question is the exception: the deals where a non-dilutive, roughly value-neutral transaction takes a fifth of the equity off in a single session.

The answer is not in the cash. It is in what the cash reveals.

The short version

- Royalty financing usually helps or is neutral for the stock. It is non-dilutive and often clears an overhang.

- It hurts the stock in one specific situation: when it deletes a takeover premium the market had already paid for.

- The cash is a wash either way. The signal is what moves the price.

- Two deals show the damage (Cytokinetics 2024, Apogee 2026). Three show the opposite (Theravance, BridgeBio, PTC).

The deal that started this

On 27 May 2026, Apogee Therapeutics released Phase 2 atopic dermatitis data for zumilokibart that analysts called competitive.

In the same breath, it announced up to $1.3 billion of financing from Blackstone Life Sciences.

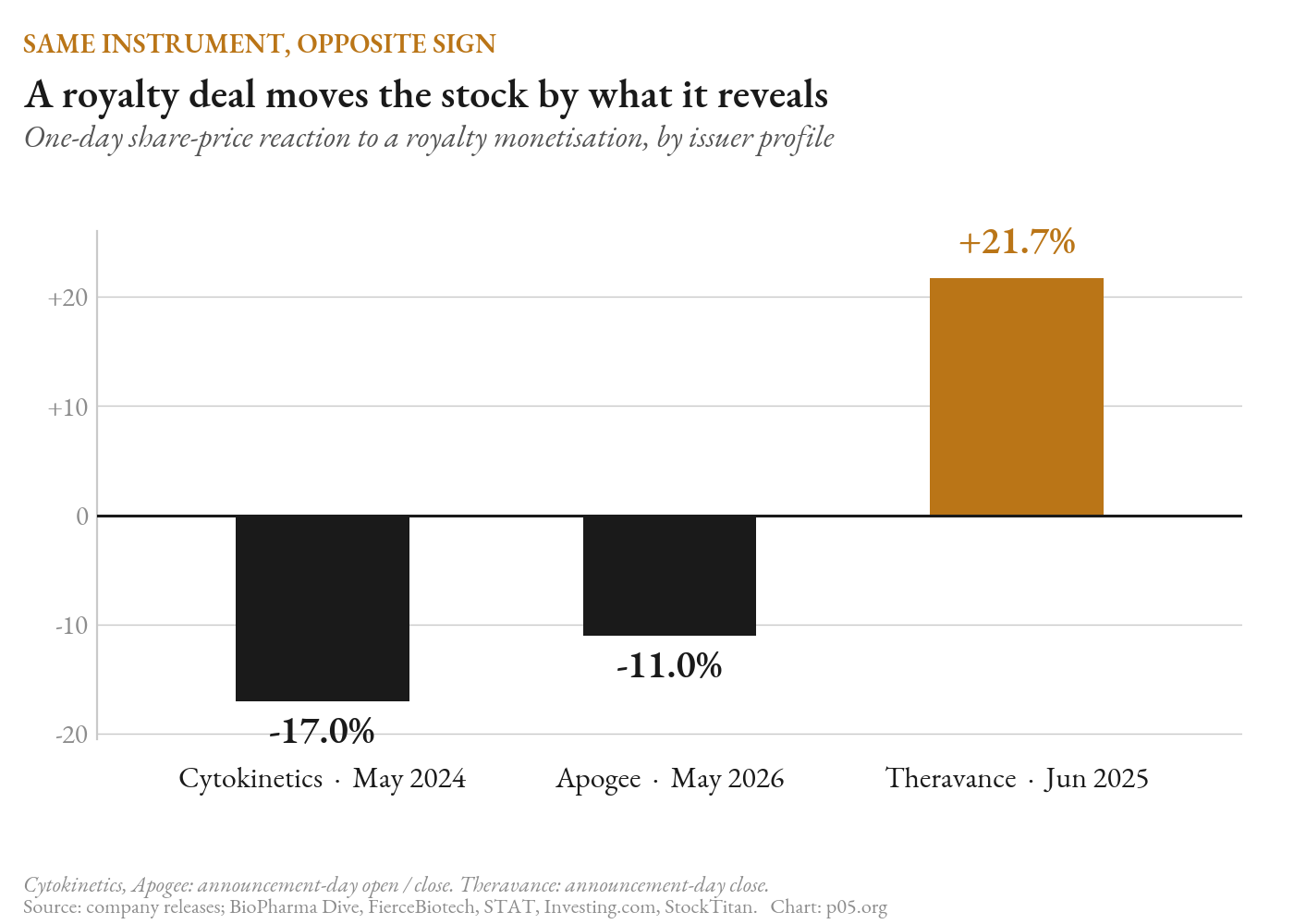

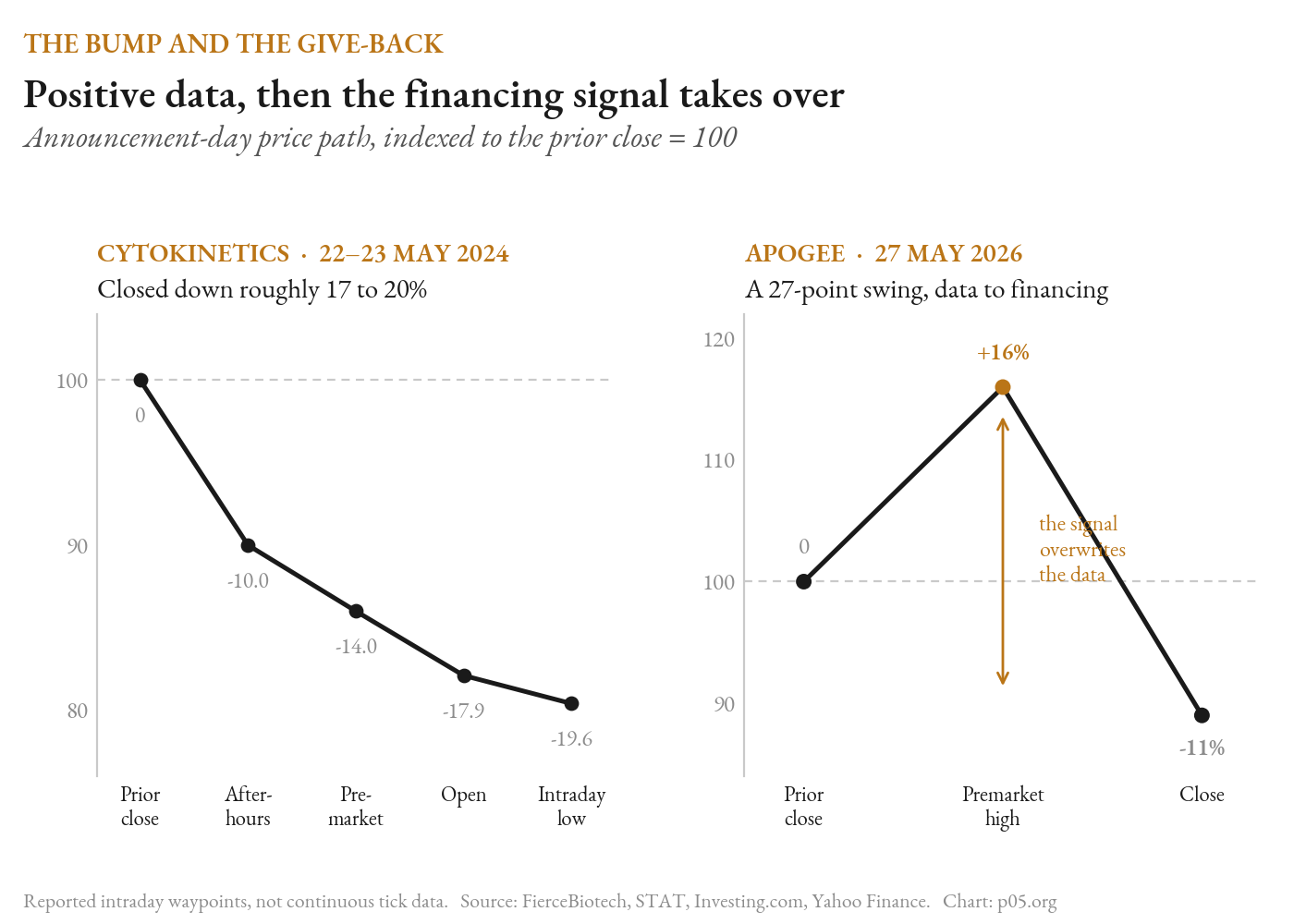

The stock did something revealing. It jumped about 16% premarket on the data, then reversed to close down roughly 11%.

Truist told clients the give-back was the financing, not the readout. A 15-year royalty on the lead asset signalled to a market that had priced Apogee as a takeover target that no deal was coming.

That sequence, good news erased by the financing attached to it, is the puzzle.

To understand it, start from the opposite fact: royalty financing is usually good for the stock.

The base case: they move together

For most issuers most of the time, a royalty deal and the share price are positively correlated. The reasons are structural.

- No dilution. Cash without issuing shares.

- Light covenants. No maintenance leverage ratios, unlike term debt.

- Asset-linked. Returns track product sales, so the instrument is less exposed to the macro swings that whipsaw biotech equity.

Goodwin's 2025 review frames it as non-dilutive capital that preserves equity as valuations soften.

WilmerHale puts the reaction plainly: shareholders see efficient, non-dilutive capital and generally react positively, while warning the effect on any single stock still has to be checked case by case.

The benchmark that makes royalty look good is the alternative.

A follow-on equity raise reliably knocks the stock. When Editas, Inovio, Dyne and CytomX priced offerings on the same night in early 2021, all four fell 10% to 16% the next morning. New shares dilute the old ones.

Royalty financing is built to avoid that hit.

BridgeBio is the clearest recent example. In mid-2025 it sold 60% of the royalties on the first $500 million of European acoramidis sales to HealthCare Royalty and Blue Owl for $300 million, capped at 1.45 times, keeping 40% above the cap.

Raymond James called it resolving an "overhang" tied to cash burn and dilution risk. The desks reiterated Buy.

Here the royalty did not cut against the stock. It removed the thing that was weighing on it.

So the default is benign to positive. The conflict is the special case, and it has identifiable causes.

Where the conflict comes from

When a royalty announcement does hurt the stock, the damage runs through one or more of four channels.

None is about the cash, which is close to a wash. All are about information, because the choice of instrument tells the market something new.

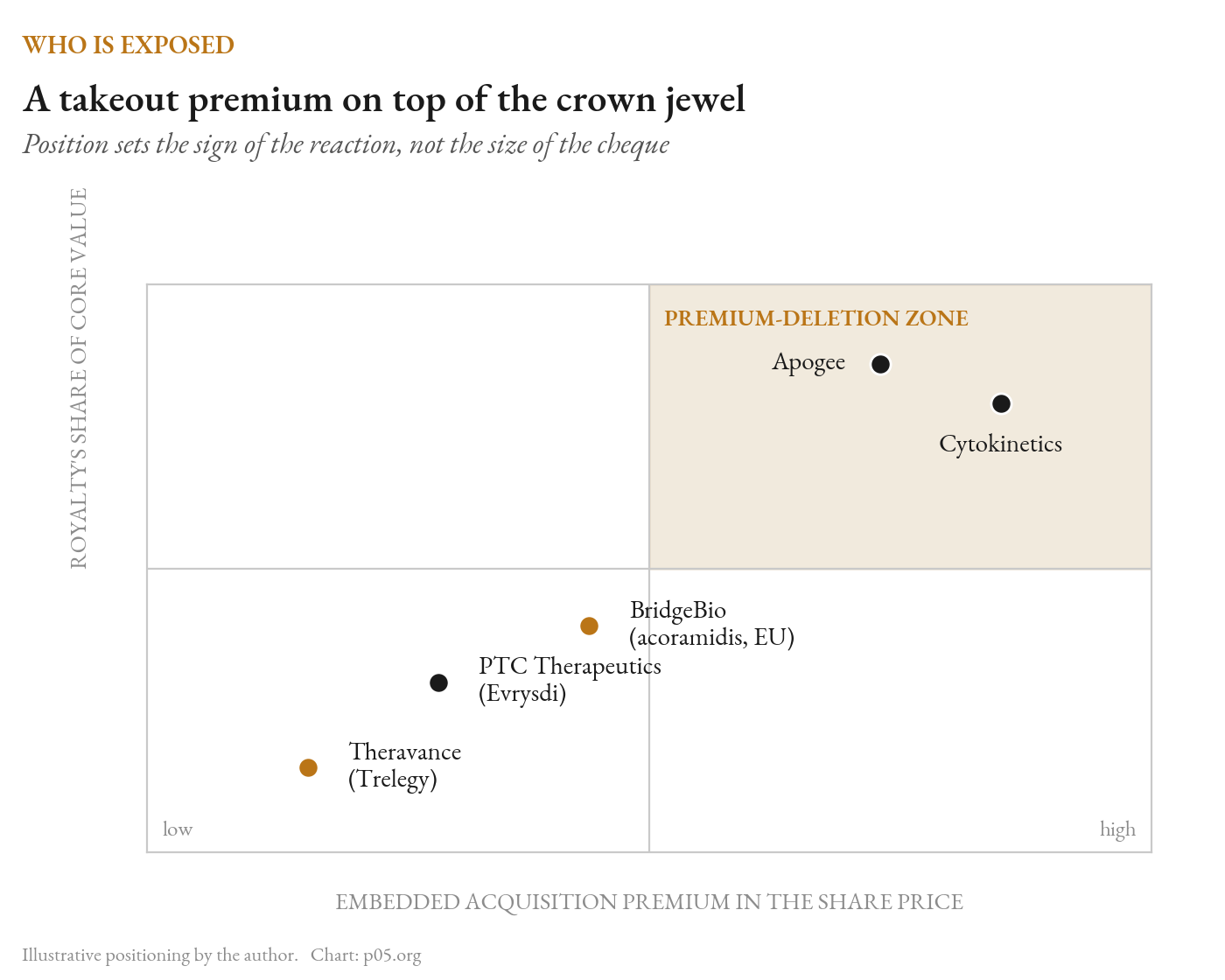

1. The signalling channel. The big one. A board that locks up its crown-jewel asset for 15 years is saying it does not expect to be acquired soon. Where the price holds a takeover premium, that signal deletes it. The drop is roughly the size of the premium, not the size of the cheque.

2. The cost-of-capital channel. Royalty capital is not cheap. Implied costs on development-stage synthetic royalties sit in the low-to-mid teens. Advisers are candid that it is less dilutive than equity but carries a higher implied cost, especially early-stage. Choosing it can read as validating a high discount rate on your own product.

3. The upside-cap channel. Selling future sales caps participation in the blockbuster case. As ZS notes, the optionality comes at the expense of margin on the product. For a single-asset story priced on the right tail, thinning that tail is a real cost.

4. The pairing channel. A royalty struck alongside an equity raise, or with cash-runway guidance withdrawn, compounds the signal. The raise reintroduces the dilution the royalty was meant to avoid.

Royalty cash is informationally neutral. It is wrapped around an information-rich choice.

The sign of the reaction is set by which prior expectation the deal overwrites.

Overwrite a takeover premium and the stock falls hard. Overwrite a dilution overhang and it rises. Same instrument, both times.

The evidence

Line up structurally similar deals and watch the sign flip with the issuer's situation, not the terms.

| Company (date) | The deal | Reaction | What it overwrote |

|---|---|---|---|

| Cytokinetics (May 2024) | Aficamten royalty re-tier to Royalty Pharma, up to $575m, plus ~$500m equity | -17% to -20% | An active takeover premium |

| Apogee (May 2026) | $800m Blackstone synthetic on zumilokibart, plus up to $500m debt | +16%, then -11% | A premium, on top of $1.3bn cash |

| Theravance (Jun 2025) | $225m to GSK for a non-operating Trelegy royalty | +21.7% | Nothing. Returning capital |

| BridgeBio (Jun 2025) | $300m for 60% of EU acoramidis royalty, 1.45x cap | Positive | A cash-burn / dilution overhang |

| PTC (Oct 2023) | $1.0bn to Royalty Pharma for more of the Evrysdi royalty | Muted | Nothing. Balance-sheet funding |

The two that broke

Cytokinetics, May 2024

The cleanest case on record. Every part of the mechanism is visible.

The deal: a re-tier of the aficamten royalty owed to Royalty Pharma, moving to 4.5% on sales up to $5 billion and 1% above, from a prior 4.5% to $1 billion and 3.5% above. Cash of $250 million at closing, up to $575 million in total.

Alongside it: roughly $500 million of equity (including a $50 million Royalty Pharma purchase), plus $100 million to revive omecamtiv mecarbil, a programme many investors had written off.

The setup is what made the reaction violent. The stock had traded above $100 after the positive SEQUOIA-HCM readout and carried a heavy premium, because Novartis had been reported circling in 2023, with J&J and AstraZeneca also named, before Novartis walked in January 2024.

The move, against a $59.23 prior close:

- After hours: down about 10%

- Open: $48.62, down 17.9%

- Intraday low: near -19.6%

The sell side said it out loud. Raymond James judged the deal reduced the takeout probability, in line with management's own "go it alone" commentary. A Mizuho poll found 21 of 29 investors now putting acquisition odds at one-in-five or lower.

Three of the four channels fired at once: the premium deletion, the dilution from the raise, and the capital-discipline complaint about omecamtiv.

A later retrospective summed it up: parting with the royalty cost about a fifth of the value and signalled the company was no longer for sale.

Apogee, May 2026

The same pattern, cleaner structure, different financier.

The Blackstone synthetic pays low-to-mid single digit royalties for 15 years, reverse-tiered to zero above $8 billion of annual sales. Capital comes in tranches ($100m at signing, $100m on Phase 3 enrolment, $200m on positive data, up to $400m more on approval), with a change-of-control buyback if Apogee is acquired.

Two choices sharpened the signal:

- Apogee said the deal made it self-sustainable through commercialisation without future equity, and withdrew its cash-runway guidance. That is the exact vocabulary that deflates a takeover premium.

- It had already raised about $345m and $350m of equity in late 2025 and March 2026. So the question was not whether it needed cash, but why this much, structured this way, on top of $1.3 billion already banked.

The premarket pop on the data and the 11% close are the two halves of one answer.

The three that did not

They share no structure with each other, except the one thing that matters: no takeover premium for the royalty to delete.

Theravance is the mirror image of Cytokinetics. On 2 June 2025 it sold its remaining outer-year Trelegy royalty to GSK for $225 million, and the stock rose 21.7%.

Trelegy is a GSK-marketed product, not Theravance's crown jewel. The royalty was a financial asset. The company was sub-scale, carried no premium, and recycled the cash into capital return. Same instrument, opposite prior, opposite sign.

BridgeBio, as above, used a capped, partial royalty to clear a dilution overhang on a company with a freshly approved product and a deep pipeline. The analysts treated it as housekeeping.

PTC sits in the same camp. Its 2023 Evrysdi monetisation ($1.0 billion upfront, up to $1.5 billion) was a multi-asset company funding the balance sheet against a partnered, approved, non-lead royalty. No crown jewel encumbered, no premium to lose, muted reaction.

The same logic explains the quiet runway deals that pass without drama: REGENXBIO's $250m HCRx bond, BeOne's $885m Imdelltra royalty, the smaller Eagle and Nuvation structures, and BioCryst's layered financings on ORLADEYO.

BioCryst is the tell on dilution: in 2021 it scrapped a $200 million equity offering after the announcement knocked the stock 14%, then leaned on royalty and structured debt instead.

For these companies, royalty capital is the thing that protects the share price from the raise they would otherwise have to do.

And the financiers know it. The whole pitch of the synthetic structure is that it lets a company retain operational control and stay independent. A Deloitte survey found about 90% of leaders expecting to use royalties, with executives dismissing the idea that the deals limit acquisitions.

That feature is accretive for a company expected to stay independent. It is destructive for one the market expects to be bought.

Who is exposed

The risk is the position, not the instrument. The danger profile is narrow and recognisable:

- A single-asset or near-single-asset company

- Pre-commercial or at launch

- Trading with a visible acquisition premium

- Taking a large royalty on that one asset

- On the same morning as good clinical data

- Paired with a withdrawn runway or a concurrent raise

Move any one variable and the deal becomes ordinary. Stack them and the financing becomes the story.

What it means

For issuers. A lead-asset royalty is a strategy disclosure before it is a financing.

If the plan is genuine independence, the premium that evaporates was never going to be paid, so own the message. If a sale is still wanted, taking the capital is close to self-defeating.

Where independence is the plan, the levers that reduce the damage are practical: separate the data print from the financing, do not withdraw runway guidance in the same release, size to the visible need, and lead with the change-of-control buyback.

For financiers. The "retain control" narrative is both the product and the source of announcement risk.

Structures that visibly preserve a sale (change-of-control buybacks, milestone tranching, reverse tiers, explicit caps) let a public issuer present the deal as confidence rather than capitulation. That closes more transactions, on better terms.

For investors. The drop is a re-pricing of takeover probability, not a verdict on the asset.

Re-estimate the acquisition odds explicitly, as the Mizuho poll did for Cytokinetics, then re-value with and without the premium. If the thesis is intact, the post-drop price may be the standalone value with the speculative premium stripped out.

The verdict

Royalty financing and public-market value move together far more often than not. The instrument does what it says: cash without dilution, and often the clearing of an overhang.

The conflict is real but conditional. It shows up when the deal overwrites an expectation the market had already paid for.

The most expensive expectation to overwrite is a takeover.

Reflects publicly available information as of June 2026, from company releases, SEC filings, analyst commentary reported in the trade press, and published industry surveys. Share-price figures are intraday, open, or close as reported by the cited sources. For informational purposes only; not investment, legal, or financial advice. The author is not a lawyer or financial adviser.