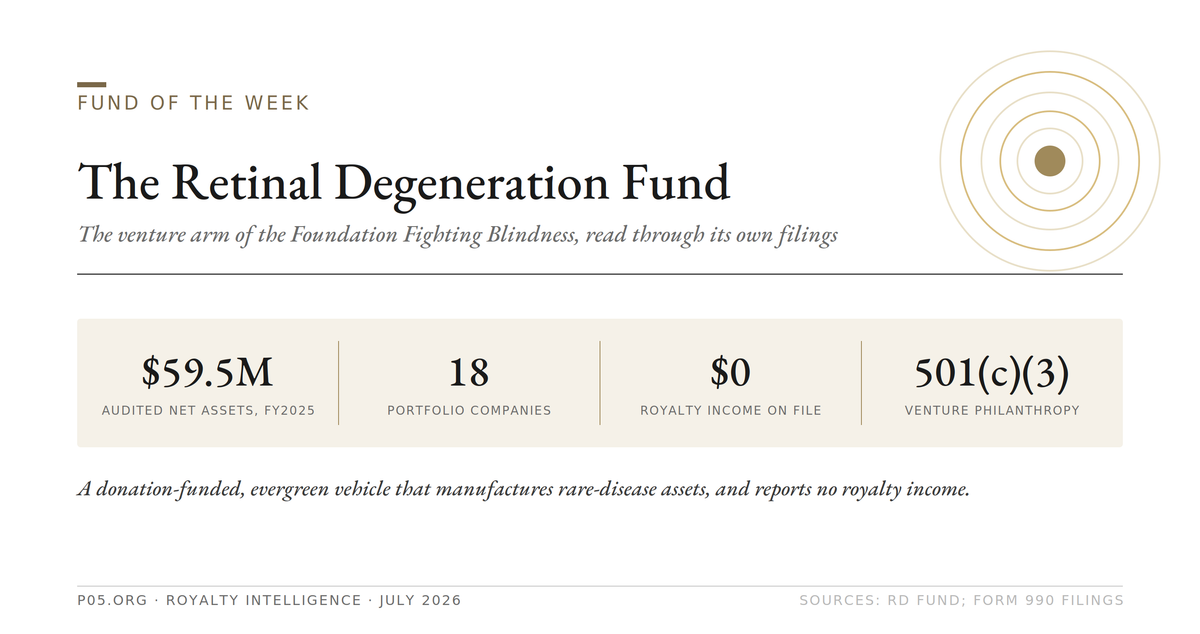

Fund of the week: Retinal Degeneration Fund

Venture philanthropy: the RD Fund is donor-backed and evergreen, with $59.5M net assets, 18 companies and $0 royalty income on file. Its value is upstream, originating the rare-disease assets whose royalties later land on other desks.

The Retinal Degeneration Fund (RD Fund) is the venture arm of the Foundation Fighting Blindness. It is a 501(c)(3) not-for-profit subsidiary of the Foundation, registered in Maryland under EIN 45-0524687, and it files its own Form 990 separate from the parent.

It was launched in 2018 out of the Foundation's former Clinical Research Institute, seeded with roughly 70 million dollars, and given a defined remit: make mission-related investments in companies developing therapies for inherited retinal diseases (IRDs) and dry age-related macular degeneration, then return the proceeds to the Foundation to fund research. The Foundation describes the vehicle as having a dual mandate: accelerate the approval of retinal therapies, and generate an alternative revenue source for the charity.

That structure differs from a private fund in a way that matters for how its economics read. The RD Fund does not raise from limited partners and does not distribute carried interest. It raises from donors and recycles realized proceeds back into a charitable balance sheet. Its published financial statements are consolidated into the Foundation's, and its stand-alone financials are visible in its annual 990 filings, which is a level of disclosure a private manager does not provide.

For a royalty or structured-credit reader, three things are worth separating at the outset, because the fund's own materials sometimes blur them: what the fund is permitted to do, what it has actually done, and what its portfolio companies do downstream. All three are covered below, with the reported figures attached.

Investment thesis and mandate

The fund's stated thesis is companies ranging from near pre-IND through clinically staged programs in IRD conditions and dry AMD. It describes itself as geographically agnostic and modality-agnostic within that disease area, covering gene therapy, biologics, small molecules, neuroprotection, optogenetics, and cell therapy, and both gene-specific and gene-agnostic approaches.

The differentiator the fund emphasises is access to the parent's infrastructure: the Foundation's My Retina Tracker genetic registry, its natural history studies, and its clinical and scientific consortium. A repeat co-investor, Bain Capital Life Sciences, has publicly attributed value to the fund's knowledge of retinal disease prevalence and regulatory pathways. That claim is the fund's central non-financial selling point and should be read as such.

The fund deploys through two vehicles. The Core Fund writes initial checks of 1 to 5 million dollars from seed to Series B, with 10 to 15 million dollars in follow-on reserves, released in tranches tied to clinical milestones. The Discovery Fund makes seed investments typically starting around 250 thousand dollars. The stated preference is ground-floor equity, but the mandate explicitly permits convertible notes, equity, fixed-multiple return-of-capital structures, and royalties.

How capital enters and returns

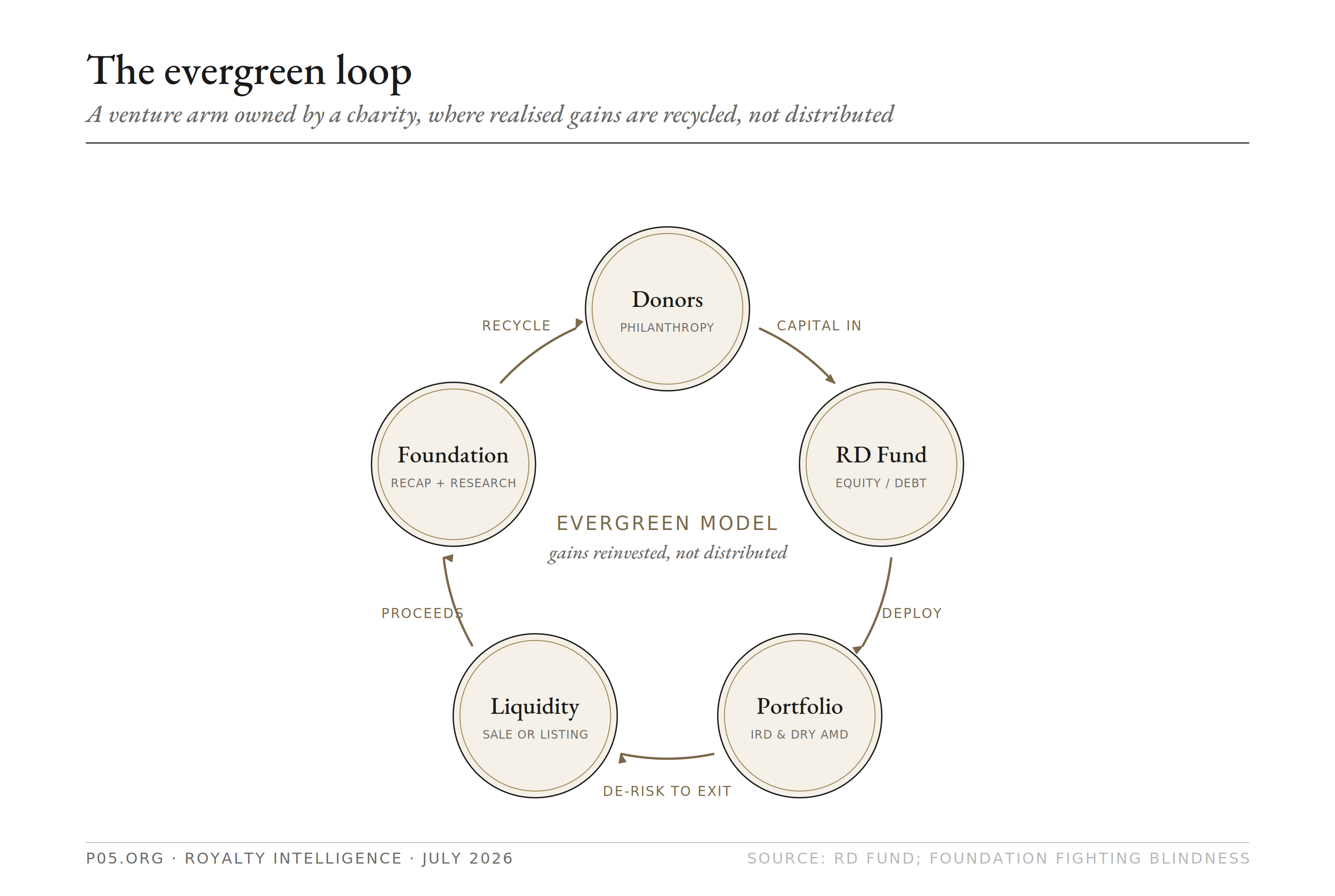

The mechanism is a closed loop. Donor capital enters the fund as a contribution. The fund deploys it as equity, or occasionally as a convertible, royalty, or fixed-multiple structure, into a portfolio company. When a company is acquired or reaches a liquidity event, the realized proceeds are recognised on the fund's books and are directed back to the Foundation to support research and to recapitalise the fund for the next cycle. The fund describes this as an evergreen model in which realized gains are reinvested rather than distributed.

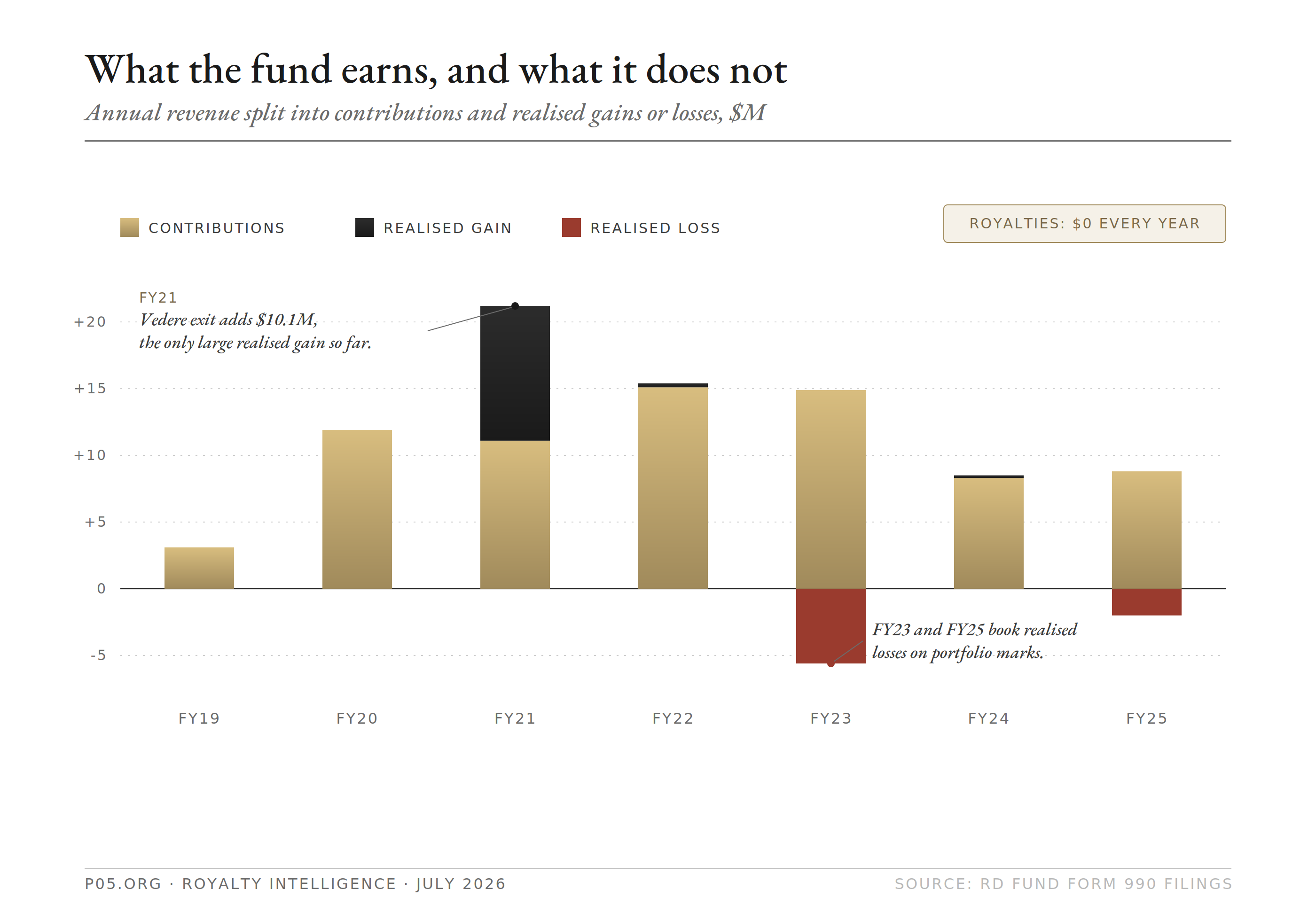

The practical consequence, visible in the financials below, is that the fund's revenue is dominated by contributions rather than investment returns, and its realized gains appear as a lumpy, episodic line item rather than a recurring yield.

The evergreen loop. Proceeds from liquidity events return to the Foundation, which recapitalises the fund and funds research. Source: RD Fund; Foundation Fighting Blindness.

Financial profile and assets

Because the RD Fund files a stand-alone Form 990, its balance sheet and income statement are a matter of public record. The table below is drawn from those filings, for fiscal years ending 30 June. Figures are rounded.

| FY (ending June) | Total revenue | Of which contributions | Net gain/(loss) on sale of assets | Royalty income | Net assets, year end |

|---|---|---|---|---|---|

| 2019 | 3.1M | 3.1M | 0 | 0 | 3.6M |

| 2020 | 11.9M | 11.9M | 0 | 0 | 10.3M |

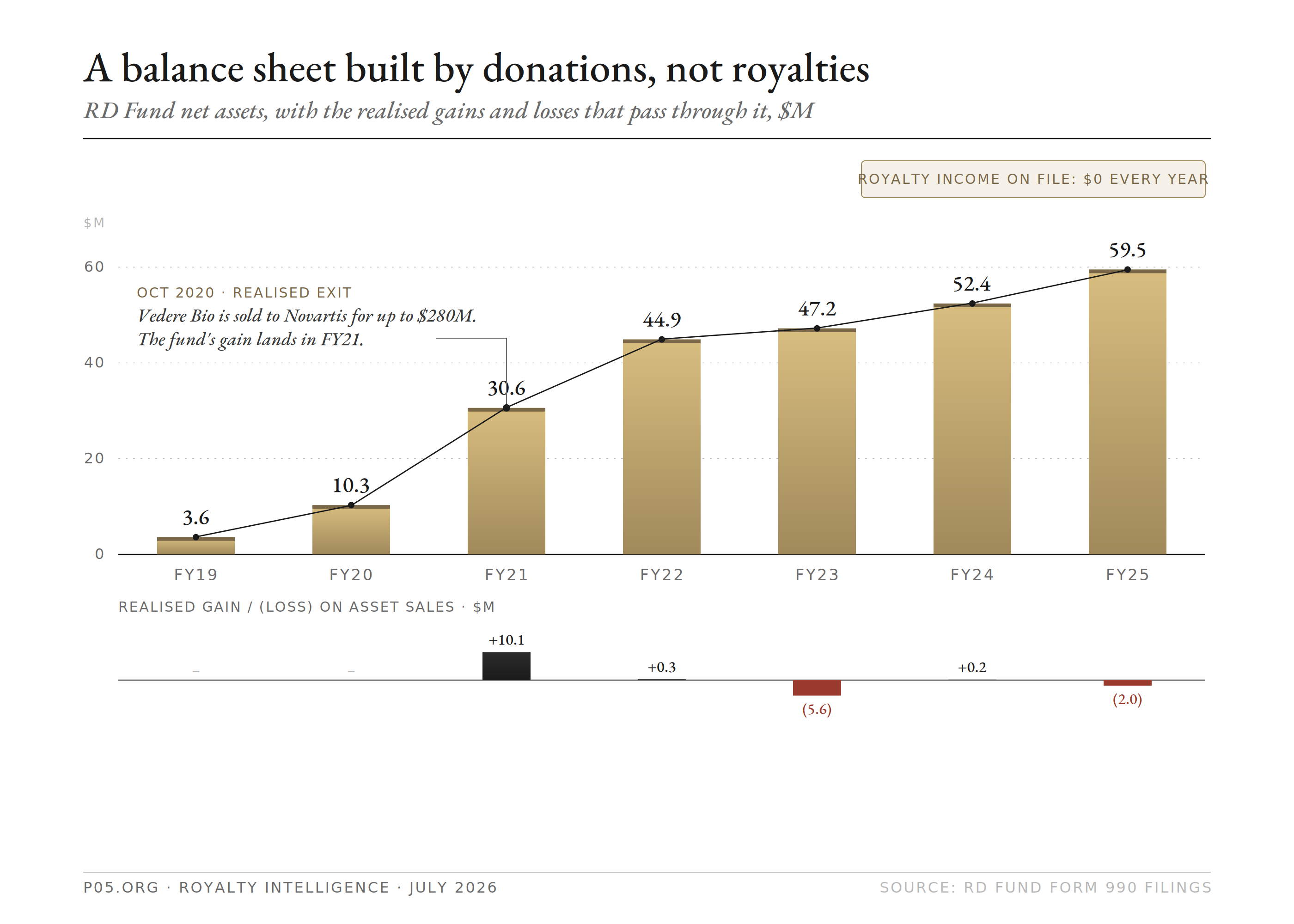

| 2021 | 21.2M | 11.1M | +10.1M | 0 | 30.6M |

| 2022 | 15.4M | 15.1M | +0.3M | 0 | 44.9M |

| 2023 | 9.3M | 14.9M | (5.6M) | 0 | 47.2M |

| 2024 | 8.8M | 8.3M | +0.2M | 0 | 52.4M |

| 2025 | 7.0M | 8.8M | (2.0M) | 0 | 59.5M |

Source: RD Fund Form 990 filings, ProPublica Nonprofit Explorer.

RD Fund net assets have grown roughly sixteenfold since 2019, funded mainly by contributions. Royalty income was zero in every year on file. Source: RD Fund Form 990 filings.

Contributions carry the fund. In every year on record, contributions are the overwhelming majority of revenue. Investment income is small, ranging from zero to roughly 284 thousand dollars a year.

Realized gains are episodic. The gain on sale of assets is the line that captures exits. It was positive by roughly 10.1 million dollars in FY2021, the fiscal year that spans the October 2020 Novartis acquisition of Vedere Bio, and it was negative in FY2023 and FY2025, consistent with write-downs or realized losses on other positions. The fund does not publish an internal rate of return, and its returns cannot be reconstructed as a smooth series from these filings.

Royalty income has been zero. Every 990 on record reports zero on the royalties line. This is the single most important fact for a royalty reader and is developed in the dedicated section below.

Net assets have grown steadily. Net assets rose from roughly 3.6 million dollars at FY2019 to roughly 59.5 million dollars at FY2025, funded primarily by contributions and, in FY2021, by an exit gain.

Contributions carry the fund; realised gains are episodic and were negative in FY2023 and FY2025. The FY2021 gain coincides with the Vedere Bio exit. Source: RD Fund Form 990 filings.

Reconciling the size figures

Three different numbers circulate for the fund's size, and they measure different things.

The fund's own website states roughly 122 million dollars under management. Its April 2026 Investing in Cures Summit materials state roughly 95 million dollars committed across 18 portfolio companies. Its audited balance sheet, per the FY2025 Form 990, shows net assets of roughly 59.5 million dollars.

These are not contradictory. The 122 million dollar figure is best read as cumulative or committed capital across RD Fund 1 and the ongoing RD Fund 2 campaign, including pledged commitments not yet on the balance sheet. The 95 million dollar figure is capital committed to companies.

The 59.5 million dollar figure is book-value net assets at a point in time, carried at cost or written-down value rather than at the marked-up fair value a private company might command in its latest round. A reader should use whichever measure matches the question and should not treat the 122 million dollar figure as a balance-sheet number.

The same fund measured three ways. Only the 59.5 million dollar net-assets figure is an audited balance-sheet number. Sources: RD Fund; Form 990.

Donors and the LP-equivalent base

The RD Fund has no limited partners in the conventional sense. Its capital is philanthropic, and the people who would be LPs in a private fund are, here, donors to a charity whose return is measured in mission progress and recycled capital rather than in distributions.

Unlike a private fund, that base is partly public, because charities name their anchors. The two named anchor donors are Gordon Gund, the Foundation's blind co-founder, and Paul Manning, whose family completed a Gund Challenge pledge of nearly 12 million dollars directed to the fund. Both are cited by the fund as the catalytic capital behind its venture model, including the creation of Opus Genetics. Both also appear in the fund's earlier 990 filings as directors.

The RD Fund 2 campaign, opened in 2021, targets at least 75 million dollars in new philanthropic capital and had passed 40 million dollars in committed capital when last disclosed. RD Fund 2 is structured to lead new investments and to make follow-on investments in RD Fund 1 companies.

The donor engine is still active and structured. In June 2026, the fund and Foundation announced a 1 million dollar commitment from A Race Against Blindness, a family-run nonprofit founded in 2023, of which 775 thousand dollars was directed to the RD Fund and 225 thousand dollars to a Foundation research award.

The 775 thousand dollars to the fund is matched dollar for dollar through the Gordon and Llura Gund Foundation Challenge, a standing donor match on new and increased gifts, taking the combined impact to roughly 1.55 million dollars. The transaction is a useful illustration of how capital actually enters the fund: named affected-family philanthropy, amplified by an anchor match, rather than institutional commitments.

The practical characterisation is that the fund's capital base is a concentrated set of disease-affected, high-net-worth philanthropists rather than the institutional mix of pensions, endowments, and funds of funds that backs a private fund of comparable deployment. That gives it patience a return-seeking fund does not have, and a scaling ceiling a return-seeking fund does not face.

Governance and compensation

The fund is overseen by an independent board that has been chaired at the investor level by Warren Thaler, with Adrienne Graves, PhD, serving as chairman of the RD Fund board in recent filings, and Karen Petrou named as vice chair in the FY2025 filing. Directors include scientific and clinical figures such as Jean Bennett, Mark Blumenkranz, Jacque Duncan, Jose-Alain Sahel, and Tony Adamis. The Foundation's CEO, Jason Menzo, sits ex officio.

Day-to-day management is led by Rusty Kelley, PhD, MBA, managing director and principal officer, who helped launch the fund in 2018. The 990 filings disclose his compensation: it rose from roughly 210 thousand dollars in FY2020 to roughly 447 thousand dollars in base compensation plus 86 thousand dollars in other compensation in FY2025. Total executive compensation reported by the fund was roughly 640 thousand dollars in FY2025 against total expenses of roughly 2.4 million dollars. Several directors with scientific roles receive modest compensation from the related Foundation entity, which is disclosed on the same filings.

These are disclosed facts rather than judgements. For a reader comparing cost structures, the point is that the fund runs a small, salaried team inside a charity, and its compensation is public in a way a private manager's is not.

Royalties, instruments, and the economics of return

This is the section that matters most for this readership, and it requires separating three distinct things.

1. The fund's own royalty income is zero to date

Despite royalties being named in its mandate, the RD Fund has reported zero royalty income on every Form 990 it has filed, from FY2012 through FY2025. There is no evidence in the public record that the fund currently holds a producing royalty interest that generates ongoing cash. Royalties are a permitted instrument, not a realised revenue stream.

2. Royalties and fixed-multiple structures are in the toolkit, behind an equity preference

The fund's stated instrument set is convertible notes, equity, fixed-multiple return-of-capital, and royalties, with an explicit preference for ground-floor equity. The rationale the fund gives is that ultrarare IRD programs often cannot support a clean priced equity round, so a structured position, such as a capped multiple on invested capital or a synthetic royalty on a future product, can be a better fit. This is the contingent-claim territory this publication covers, but in the RD Fund's case it is a stated capability rather than a demonstrated book. The fund does not disclose the terms of any specific royalty or fixed-multiple position, and none is visible in its filings.

What its 2026 deployments actually show is a spread of conventional structures rather than royalties. In January 2026 it participated in Beacon Therapeutics' 75 million dollar Series C as an equity co-investor. In the same month it committed up to 2 million dollars of non-dilutive funding to Opus Genetics to advance the OPGx-MERTK program toward IND-enabling studies, a milestone-linked grant-style instrument to an already-public company rather than a royalty. And in mid-2026 it joined a 26 million dollar seed syndicate for Amber Bio. Across these, the pattern is equity and non-dilutive milestone funding, with the royalty and fixed-multiple options remaining on the shelf.

3. Realised returns to date have come through equity exits

The two liquidity events on record are both equity outcomes, not royalty monetisations.

Vedere Bio. The RD Fund co-invested alongside Atlas Venture and Mission BioCapital in Vedere Bio, an optogenetics company. In October 2020, Novartis acquired Vedere for 150 million dollars upfront and up to 280 million dollars including milestones, roughly a year after the Series A. The Foundation has described the fund's original position as 3 million dollars. The fund's FY2021 Form 990 reports a gain on sale of assets of roughly 10.1 million dollars, in the fiscal year that captured this transaction.

Opus Genetics. The RD Fund conceived and seed-funded Opus Genetics in 2021 as its first internal spinout. In October 2024 Opus went public through an all-stock reverse merger into Ocuphire Pharma, a transaction valued at roughly 26 million dollars, in which former Opus holders received approximately 42 percent of the combined company. The company now trades on Nasdaq as IRD. This converted an illiquid venture position into a marketable equity holding rather than a cash exit.

As the fund's only public position, Opus is also the one holding whose financing is fully visible in 2026, and its capital stack is instructive. Through late 2025 and early 2026 the company raised a 23 million dollar equity round led by Perceptive Advisors and Balyasny (November 2025), then in April 2026 secured a senior secured note facility of up to 155 million dollars from Oberland Capital, a healthcare structured-credit lender, drawing an initial 35 million dollar tranche plus 5 million dollars of equity.

That left roughly 90 million dollars of cash at 31 March 2026 and a runway the company projects into 2029. The detail worth noting for this readership is that the fund's flagship de-risked asset is now partly financed through exactly the kind of structured, revenue-linked debt that sits adjacent to the royalty market, provided by a specialist lender rather than by the RD Fund itself. On the clinical side, Opus reported FDA acceptance of OPGx-LCA5 into the Rare Disease Evidence Principles program in May 2026, with pivotal Phase 3 dosing expected in the fourth quarter of 2026 and OPGx-BEST1 cohort data due around mid-2026.

4. The royalty-bearing economics sit at the portfolio-company level

The clearest royalty structure connected to the fund is one the fund does not directly own. In November 2024, portfolio company Atsena Therapeutics signed an exclusive license with Nippon Shinyaku for ATSN-101, its LCA1 gene therapy. Under the terms, Nippon Shinyaku holds exclusive commercial rights in the US and Japan through its NS Pharma subsidiary, Atsena retains the rest of world, and Atsena receives an upfront payment, development and sales milestones, downstream royalties on net sales, and reimbursement for development including a planned global pivotal trial. The upfront was not disclosed.

The structural point for a royalty reader is precise: those royalties accrue to Atsena, the operating company. The RD Fund's exposure to them is indirect, mediated by its equity stake in Atsena, not a direct claim on the royalty stream. This is the same layering the EcoR1 profile described from the equity side. The RD Fund manufactures and de-risks the asset; the royalty-bearing license is struck by the company; the fund participates only through its shares.

5. Priority review vouchers are a parallel, non-royalty lever

Several RD Fund programs carry FDA Rare Pediatric Disease designations, including Atsena's ATSN-101, which makes them potentially eligible for a Rare Pediatric Disease Priority Review Voucher on approval. The Atsena-Nippon Shinyaku agreement includes an explicit PRV provision, and Opus cites potential vouchers as part of its own value story. Kelley has publicly described PRVs as a financing lever for rare-indication developers.

The timing is now favourable, which was not the case a year ago. The Rare Pediatric Disease PRV program had lapsed on 20 December 2024, but it was reauthorised on 3 February 2026 through the Consolidated Appropriations Act, 2026, with the FDA able to award vouchers through 30 September 2029. A voucher is a transferable, saleable asset rather than a royalty; 63 have been awarded since 2012, and one recently changed hands for roughly 150 million dollars. For the RD Fund, a PRV is another way portfolio-company value can be crystallised, again captured through equity rather than through a direct claim, and the reauthorisation restores that option for its pediatric-designated programs.

Per-deal economics on record

Where the fund or its companies have disclosed check sizes, the figures are modest and consistent with the stated 1 to 5 million dollar Core Fund range. The Foundation reported investing roughly 7.9 million dollars (7 million euro) in the RdCVF program at SparingVision and roughly 7.5 million dollars in Nacuity's NPI-001. Its Vedere position was described as 3 million dollars. These are gross commitments to programs or companies, not net returns.

Portfolio of investments, as of July 2026

The fund reports roughly 95 million dollars committed across 18 companies since 2018, having co-invested with more than 50 firms, a figure that predates several 2026 additions. The table below reflects the disclosed portfolio from the fund's companies page and recent financing announcements, with round sizes shown where the round, not the RD Fund's specific check, has been disclosed.

| Company | Focus | Disclosed round / status | Royalty or licensing relevance |

|---|---|---|---|

| Opus Genetics (Nasdaq: IRD) | AAV gene therapy for IRDs (LCA5, BEST1, MERTK, RDH12, RHO) | Public since Oct 2024; up to 2M USD RD Fund non-dilutive grant to MERTK program, Jan 2026; ~90M USD cash after Oberland facility; Phase 3 LCA5 dosing expected Q4 2026 | LCA5 in FDA RDEP program; PRV-eligible programs |

| Atsena Therapeutics | AAV gene therapy (LCA1, X-linked retinoschisis) | LCA1 advancing to Phase 3; RMAT, Orphan Drug, Rare Pediatric Disease designations | Nippon Shinyaku US/Japan license: upfront, milestones, sales royalties, dev reimbursement, PRV provision |

| Beacon Therapeutics | Gene therapy for XLRP (laru-zova) and dry AMD | Series C over 75M USD, Jan 2026, led by Goldman Sachs; RD Fund participated | Pre-commercial; pivotal VISTA readout expected H2 2026 |

| Perceive Bio | Gene therapy for dry AMD / GA | 78M USD Series B, 2023, led by J&J Innovation | Partnered later-stage economics not yet disclosed |

| Perceive Pharma | Small-molecule neuroprotection (glaucoma) | 15M USD Series A, Feb 2025 | Early stage |

| SparingVision | Gene-agnostic cone preservation (SPVN06) | ~7.9M USD FFB program investment; Intellia collaboration; Bain and Wellington round | Intellia CRISPR collaboration |

| Nacuity | Antioxidant therapy (NPI-001, oral NACA) for RP | ~7.5M USD FFB program investment | Gene-agnostic; early stage |

| Amber Bio | Multi-kilobase RNA editing | Participated in 26M USD seed, 2026, with Playground Global and a16z Bio + Health | Platform; early stage |

| Agnos Therapeutics | Cell-based retinal renewal | New 2026 portfolio addition | Early stage |

| NVasc | Revascularisation for dry AMD / GA | Early-stage, Oct 2023 | Founded by VEGF pioneer Napoleone Ferrara |

| SalioGen | Gene coding / Saliogase editing | Preclinical platform | Platform |

| ProQR | RNA editing for IRDs | Legacy CRI-era position | Platform |

Realised, public, or inactive positions include Vedere Bio (acquired by Novartis, 2020), Opus Genetics (public since 2024), and earlier programs such as Nayan and Stargazer, which the fund lists in the past tense.

The nearest disclosed clinical catalyst is Beacon's pivotal VISTA readout for laru-zova in XLRP, which the company expects in the second half of 2026, followed by Opus's Phase 3 LCA5 dosing in the fourth quarter and Atsena's LCA1 Phase 3 progression.

Blue team and red team

Blue team: the case for

An information advantage tied to the parent. Access to a disease-specific genetic registry, natural history data, and a clinical consortium is a resource a generalist cannot easily replicate, in a field where the investment case turns on prevalence, penetrance, and regulatory path.

A demonstrated ability to de-risk to an exit. The fund has produced one trade sale to a large pharma and one public listing, co-invests alongside institutional names including Goldman Sachs and Bain, and its companies have raised additional outside capital. Its FY2021 filing shows the Vedere gain reaching its books.

Patient, disclosed, mission-aligned capital. Because proceeds revert to a charity rather than to fee-sensitive LPs, the fund can hold through the volatility of ultrarare development, and its stand-alone financials are public.

Instrument flexibility. The mandate permits royalties, fixed-multiple structures, and convertibles alongside equity, which in principle lets the fund finance companies that cannot support a clean priced round.

Red team: the case against

The instrument flexibility is unproven. Royalty income is zero across every filing, and the fund discloses no specific royalty or fixed-multiple position. The capability is stated, not demonstrated.

A small, single-disease, illiquid book. Roughly 95 million dollars committed across 18 companies in one therapeutic area concentrates clinical risk, and most positions are early and illiquid. Realised gains are episodic, and the fund publishes no IRR.

The leverage headline is gross, not net. The fund's roughly 10x multiplier measures outside capital attracted to portfolio companies, not net cash returned to the Foundation. The 990 gain-on-sale line, which is the closest public proxy for realised return, is far smaller and was negative in two of the last three years.

Donor dependence and a ceiling. The capital base is philanthropic, competes with the parent's other fundraising, and cannot scale like an institutional fund. RD Fund 2 is still filling.

Size figures require care. The 122 million dollar under-management figure, the 95 million dollar committed figure, and the 59.5 million dollar net-asset figure measure different things, and only the last is an audited balance-sheet number.

Implications for the pharmaceutical royalty and biotech capital markets

For commercial capital markets, the RD Fund is relevant less as a competitor than as a source and a signal, with the caveats above attached.

As a source of assets. The fund originates and de-risks the rare-disease gene therapies that later carry orphan economics, priority review vouchers, and partnered, royalty-bearing licenses. Atsena's Nippon Shinyaku deal is a concrete example of a portfolio asset generating the milestone and royalty flows that structured-finance desks underwrite, even though the fund itself holds none of those royalties directly.

As a signal of asset quality. In a disease area where prevalence and regulatory nuance dominate, RD Fund participation, backed by the parent's registry data, can serve as a partial screen for asset quality. It is a soft signal, not a substitute for diligence.

As a model of contingent structures inside venture. The evergreen, mission-return design is a working, publicly documented example of a philanthropic balance sheet using equity and, in principle, contingent instruments to finance early-stage rare-disease development without a secondary market. For purpose-driven LPs and for anyone building rare-disease or vaccine-adjacent structures, it is a case study, with the honest footnote that its own royalty line has so far stayed at zero.

Financial history and recent developments

| Date | Event |

|---|---|

| 2018 | RD Fund launched from the Foundation's Clinical Research Institute with roughly 70 million dollars |

| Oct 2020 | Vedere Bio acquired by Novartis, up to 280 million dollars including milestones |

| FY2021 | Fund's 990 reports roughly 10.1 million dollars gain on sale of assets |

| 2021 | RD Fund 2 fundraising opens, target at least 75 million dollars; Opus Genetics conceived internally |

| Nov 2024 | Atsena signs Nippon Shinyaku license for ATSN-101, with sales royalties and a PRV provision |

| Oct 2024 | Opus Genetics goes public via reverse merger into Ocuphire, Nasdaq: IRD, the fund's first public company |

| Feb 2025 | Perceive Pharma closes 15 million dollar Series A |

| Jun 2025 | Fund's FY2025 net assets reach roughly 59.5 million dollars |

| Jan 2026 | Beacon Therapeutics closes Series C over 75 million dollars, led by Goldman Sachs, with RD Fund participation |

| Jan 2026 | RD Fund commits up to 2 million dollars non-dilutive to Opus Genetics for OPGx-MERTK |

| Feb 2026 | Rare Pediatric Disease PRV program reauthorised through September 2029 |

| Apr 2026 | Investing in Cures Summit: roughly 95 million dollars committed across 18 companies; Agnos added |

| Apr 2026 | Opus Genetics secures Oberland Capital senior secured note facility of up to 155 million dollars |

| May 2026 | Opus Genetics OPGx-LCA5 accepted into FDA Rare Disease Evidence Principles program |

| Jun 2026 | A Race Against Blindness commits 1 million dollars, with 775 thousand dollars to the fund matched by the Gund Challenge |

| 2026 | RD Fund participates in Amber Bio 26 million dollar seed round |

| H2 2026 (expected) | Beacon VISTA readout for laru-zova; Opus Phase 3 LCA5 dosing; Opus BEST1 cohort data |

Conclusion

The RD Fund is a venture-philanthropy vehicle that is easier to read as a balance sheet than most private funds, because it files one. Donor capital enters, the fund invests it in inherited retinal disease and dry AMD companies, and realised proceeds return to a research charity and recapitalise the fund.

On the specific question this publication cares about, the record is clear and worth stating plainly. Royalties are in the fund's mandate, but its reported royalty income has been zero in every year on file. Its realised returns to date have come from two equity events, one trade sale and one reverse merger, recorded in a lumpy gain-on-sale line rather than a recurring yield. The royalty-bearing structures connected to the fund, such as Atsena's Nippon Shinyaku license, sit at the portfolio-company level and reach the fund only through its equity.

The reason the fund is worth a royalty professional's attention is upstream. It is one of the more concentrated and better-informed originators of rare retinal disease assets in the market, and those assets are the ones whose licenses, milestones, royalties, and vouchers later appear on other parties' term sheets. The near-term signal to watch is the next Beacon readout and the next portfolio-company license, both of which will say more about where retinal-disease royalty flows are forming than any figure on the fund's own return line.

All information in this article was accurate as of the publication date and is derived from publicly available sources including the RD Fund's IRS Form 990 filings, the fund's own disclosures, Foundation Fighting Blindness announcements, company press releases and SEC filings, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.