Company of the week: Pacira BioSciences

Pacira BioSciences owns its non-opioid drugs rather than licensing a platform, so its royalty life runs backwards: it litigated one royalty out of existence, wrote a negative royalty against EXPAREL's own volumes to 2039, and in June 2026 sold iovera° to Zimmer Biomet for up to $140 million.

Pacira BioSciences owns its drugs rather than licensing a platform. It generates cash, and buys back its own stock.

It is the kind of company a royalty desk usually studies from the outside, as the payer on the other side of someone else's claim.

What makes it worth a full read is that, over the last two years, Pacira has actively rearranged those claims. It litigated one royalty out of existence. It carries a milestone obligation that is almost certainly never going to pay. It has written a quasi-royalty against its own flagship that runs to 2039.

And, five days before this was written, it sold one of its three products for cash plus a contingent tail.

The flagship is EXPAREL, a long-acting local anaesthetic that supplies roughly four fifths of revenue.

Around it sit a second commercial drug, a clinical pipeline the company is trying to turn into a second act, a reimbursement law Pacira spent years lobbying into existence, a swarm of generic challengers, and an activist investor that forced a June 2026 proxy vote.

Pacira (Nasdaq: PCRX) won the vote, settled with the lead generic, and has just begun shedding non-core assets. None of those threads is fully resolved.

Last week's Protillion piece looked at a private platform that originates royalties it cannot see clearly.

Pacira is the opposite specimen: a public product owner whose numbers are almost entirely lit by SEC filings, and whose royalty life is written in obligations and earnouts rather than income.

At a glance

| Item | Detail |

|---|---|

| Company | Pacira BioSciences, Inc. (Nasdaq: PCRX), Brisbane, California |

| Leadership | Frank D. Lee, chief executive (since January 2024); Shawn Cross, chief financial officer |

| Products | EXPAREL; ZILRETTA; iovera° (divestiture to Zimmer Biomet pending) |

| Core technology | DepoFoam multivesicular liposome, the delivery system under EXPAREL |

| Pipeline | PCRX-201 (gene therapy for knee OA, Phase 2); PCRX-2002 ropivacaine; AMT-143 |

| 2025 revenue | $726.4M, up ~4% on 2024's $701.0M; record gross margins; 2.5M+ patients treated |

| Q1 2026 revenue | $177.4M; EXPAREL $143.3M, ZILRETTA $26.8M (+15%), iovera° $6.2M, veterinary $1.2M |

| 2026 guidance | EXPAREL $600 to $620M; total revenue $745 to $770M; non-GAAP gross margin 77 to 79% |

| Balance sheet | Cash ~$144.3M; total debt ~$367.7M, incl. $281.7M of 2.125% convertible notes due 2029 |

| Market value | ~$0.9B, roughly 39.4M shares, stock in the low $20s through mid-2026 |

| Newest deal | iovera° sold to Zimmer Biomet, 30 Jun 2026, up to $140M ($70M upfront + up to $70M milestones) |

| Defining royalty item | The Fresenius settlement: a rising, capped share of EXPAREL volumes ceded from 2030 to 2039 |

The franchise, and the law it wrote

EXPAREL is old-drug, new-delivery.

The active ingredient, bupivacaine, is a generic local anaesthetic that has been in use for decades. The value sits in DepoFoam, a multivesicular liposome that packages the drug and releases it slowly at a surgical site, so a single injection controls pain for days instead of hours.

EXPAREL launched in the United States in April 2012 and has been the centre of the company ever since. It has been used in more than 14 million patients, at a list price around $444 a vial.

The other products were bought, not invented.

ZILRETTA, an extended-release steroid injection for osteoarthritis knee pain, came through the 2021 acquisition of Flexion Therapeutics. That deal also carried debt and a contingent-value-right obligation the company still reports.

iovera°, a handheld device that freezes a targeted nerve to blunt pain without any drug, came through the 2019 purchase of MyoScience. As of 30 June 2026, it is on its way back out the door (see below).

In July 2025 Pacira added a co-promotion agreement with Johnson & Johnson MedTech, pushing ZILRETTA into sports medicine, pain management, rheumatology, and other specialties beyond orthopaedics.

A self-made reimbursement tailwind

The most underappreciated part of the EXPAREL story is that Pacira built its own demand.

The company led a lobbying coalition from 2017 for what became the NOPAIN Act (Non-Opioids Prevent Addiction in the Nation), passed inside the Consolidated Appropriations Act of 2023.

From 1 January 2025, the law requires Medicare to pay separately for qualifying non-opioid drugs and devices in hospital outpatient and ambulatory surgery settings. The rate is average sales price plus six per cent, instead of the cost being buried in a bundled procedure payment.

Both of Pacira's flagship products made the qualifying list: EXPAREL under a new permanent J-code, J0666, and iovera° under a device code worth up to an extra $255.85 per use.

A single-product company that persuades Congress to reimburse its product line separately has done something more durable than a good quarter. With iovera° leaving, EXPAREL is the qualifying product Pacira keeps.

The pipeline, and one date

EXPAREL's exclusivity begins to erode in 2030, so the company's clinical bets are timed against that clock.

The lead candidate is PCRX-201 (enekinragene inzadenovec), a locally delivered gene therapy for knee osteoarthritis. It runs on a high-capacity adenovirus platform Pacira took fully in-house by acquiring the rest of GQ Bio in February 2025.

It holds an RMAT designation and is in the Phase 2 ASCEND study: a two-part, randomised, double-blind, active-controlled trial of roughly 135 patients aged 45 to 80 with knee OA. Topline Part A results are expected around the end of 2026.

A second candidate, PCRX-2002, is a long-acting reformulation of ropivacaine. And in late 2025 the company in-licensed AMT-143 from AmacaThera.

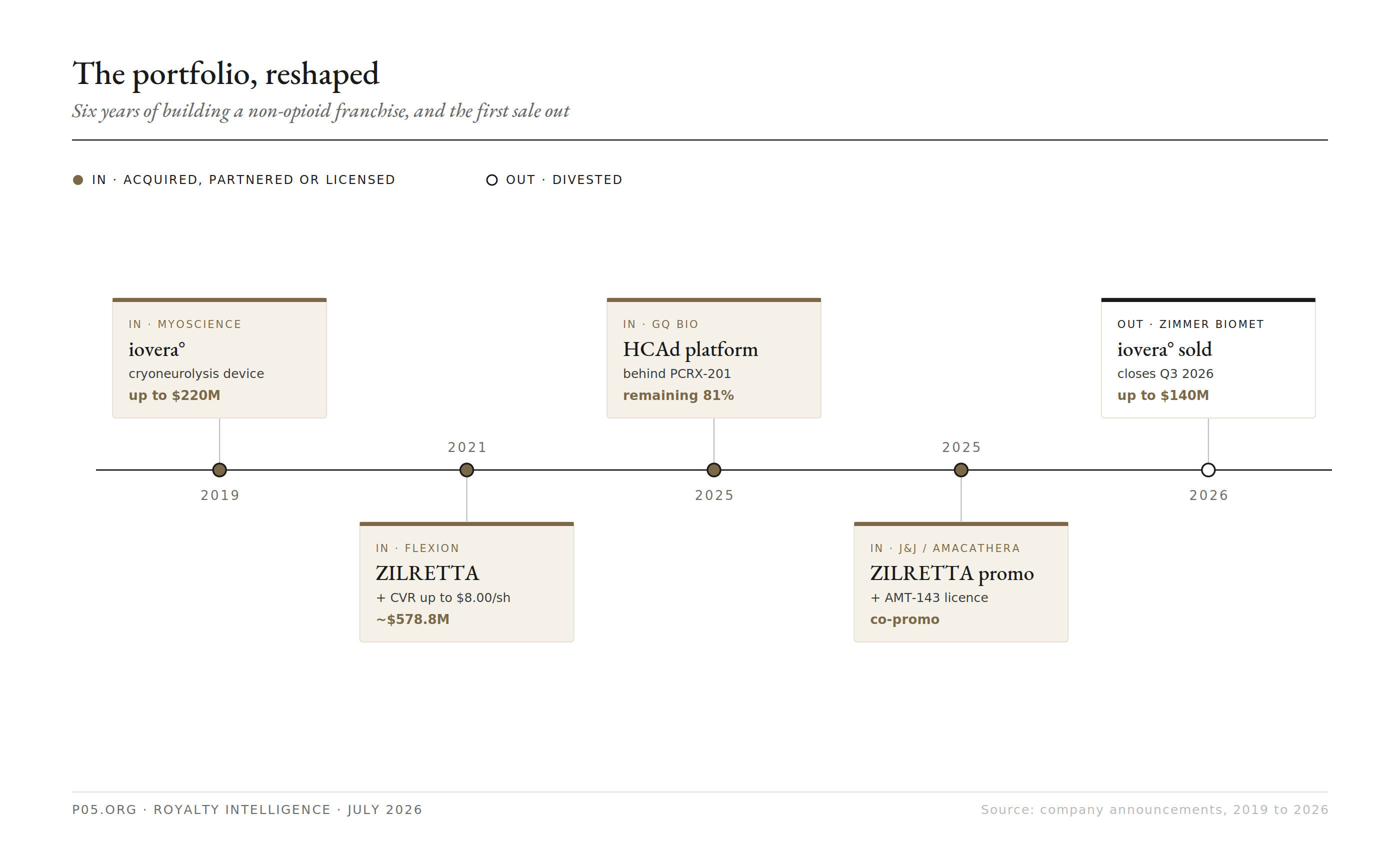

Deals and acquisitions: a portfolio being reshaped

Pacira has spent the last several years assembling a non-opioid portfolio by acquisition, and has now started pruning it.

The pattern is worth laying out, because the buy-side and the newest sale both run on the same contingent-payment plumbing a royalty desk reads for a living.

Six years of portfolio building by acquisition, and the first divestiture out. Tan nodes mark assets and rights coming in; the outlined node is iovera° going to Zimmer Biomet in 2026. Source: company announcements.

| Date | Counterparty | Direction | Structure |

|---|---|---|---|

| Apr 2019 | MyoScience | Acquired | Up to $220M for iovera° ($120M upfront + up to $100M milestones); Pacira renames to BioSciences |

| Nov 2021 | Flexion Therapeutics | Acquired | ~$578.8M total; $8.50/share cash + CVR up to $8.00/share; brought ZILRETTA and assumed debt |

| Feb 2025 | GQ Bio Therapeutics | Acquired | Bought remaining 81%; brought the HCAd gene-therapy platform behind PCRX-201 |

| Jul 2025 | J&J MedTech | Partnered | ZILRETTA co-promotion into new physician specialties |

| Late 2025 | AmacaThera | In-licensed | Exclusive licence to AMT-143, adding to the pipeline |

| Jun 2026 | Zimmer Biomet | Divested | iovera° sold for up to $140M ($70M upfront + up to $70M milestones through 2031) + spasticity earnout |

The iovera° divestiture, announced 30 June 2026, is the cleanest signal of where the company is heading.

Pacira is selling its only device, the same iovera° it bought via MyoScience in 2019 for up to $220 million, to orthopaedics giant Zimmer Biomet for up to $140 million.

The terms: $70 million upfront and up to $70 million more in revenue-based milestones through 31 December 2031. The two companies will also collaborate on iovera°'s spasticity programme, with Pacira eligible for further payments if a registrational study and approval land.

iovera° had grown to $24.2 million of sales in 2025, so the sale is small in revenue terms, roughly 14% of Pacira's market value in deal size. RBC Capital advised Pacira.

Read structurally, the trade is instructive.

Pacira converts a wholly-owned but small device business into upfront cash plus two contingent claims it now holds looking outward: an earnout on iovera°'s future sales under Zimmer, and a milestone on the spasticity programme.

The company said the upfront proceeds will pay down its senior secured revolving credit facility, which ties the divestiture straight back to the balance-sheet discipline discussed further down.

It also simplifies Pacira into a two-drug commercial company plus pipeline. And it moves one of the two NOPAIN-qualifying products off the books, leaving EXPAREL as the reimbursement beneficiary that matters.

The five sections that follow trace Pacira's royalty-shaped claims one by one. Taken together, they look like this:

Three obligations point outward, two small claims point in, and the franchise-defining exposures all run away from the company. Source: Pacira SEC filings and D. Nev. court records.

The royalty it stopped paying: RDF

DepoFoam did not start at Pacira.

In early 1994 the company's predecessor licensed foundational technology from the Research Development Foundation (RDF), a Nevada-based patent-holding foundation, in return for a running royalty.

For years that royalty fell only on DepoCyt, an older cytotoxic product, because EXPAREL did not yet exist. Once EXPAREL launched and scaled, a low-single-digit royalty on its net sales became a real and growing line item, flowing to a foundation that had no other hand in the product.

A 2004 amendment tied the royalty to specific patents, and made it payable only while those patents were unexpired.

The relevant patents lapsed on 24 December 2021. Pacira took the position that the obligation lapsed with them, sued RDF for declaratory judgment in the District of Nevada (case 2:21-cv-02241, before Judge Cristina D. Silva), and kept paying under protest while the case ran.

When the patent argument weakened, RDF switched theories, asserting a right to royalties based on trade secrets embedded in Pacira's manufacturing process rather than the expired patents.

That pivot did not hold.

In April 2025 the court ruled for Pacira, declaring the royalty obligation over and allowing the company to stop paying immediately.

It then ordered RDF to return $23.1 million of royalties paid under protest plus $5.2 million of interest, a $28.3 million payment received in July 2025.

A monetisation turns a future royalty into cash by selling it. Pacira did the reverse: it used litigation to delete a royalty it owed and recover what it had already paid, permanently lifting EXPAREL's contribution margin without shipping a single extra vial.

It is also a useful caution for anyone modelling royalties as bond-like. This one lived and died on patent-expiry language, and the payer found the exit.

The royalty it owes but probably won't pay: the Flexion CVR

Part of the price for Flexion in 2021 was not cash but a contingent value right.

Flexion holders received $8.50 per share up front plus one non-tradeable CVR worth up to $8.00 per share, payable only on defined milestones. All must be met by 31 December 2030:

| CVR trigger | Payment |

|---|---|

| ZILRETTA calendar-year net sales ≥ $250M | $1.00/share |

| ZILRETTA calendar-year net sales ≥ $375M | $2.00/share |

| ZILRETTA calendar-year net sales ≥ $500M | $3.00/share |

| FDA approval of FX201 (now PCRX-201) | $1.00/share |

| FDA approval of FX301 | $1.00/share |

Set those thresholds against reality.

ZILRETTA ran about $107 million annualised in early 2026, and Pacira's full-year 2026 guidance across the entire portfolio tops out at $770 million.

The first sales trigger sits at $250 million for ZILRETTA alone, more than double its current run rate, with less than five years left on the clock. PCRX-201 is in Phase 2 and will not be FDA-approved by 2030 on any normal timeline, and FX301 has effectively fallen away.

The CVR is a genuine obligation, carried as contingent consideration and remeasured each quarter. But it is deep out of the money on every leg.

For a royalty analyst it is the cleanest kind of claim to price: milestone-shaped, product-linked, and, on the current trajectory, worth close to nothing.

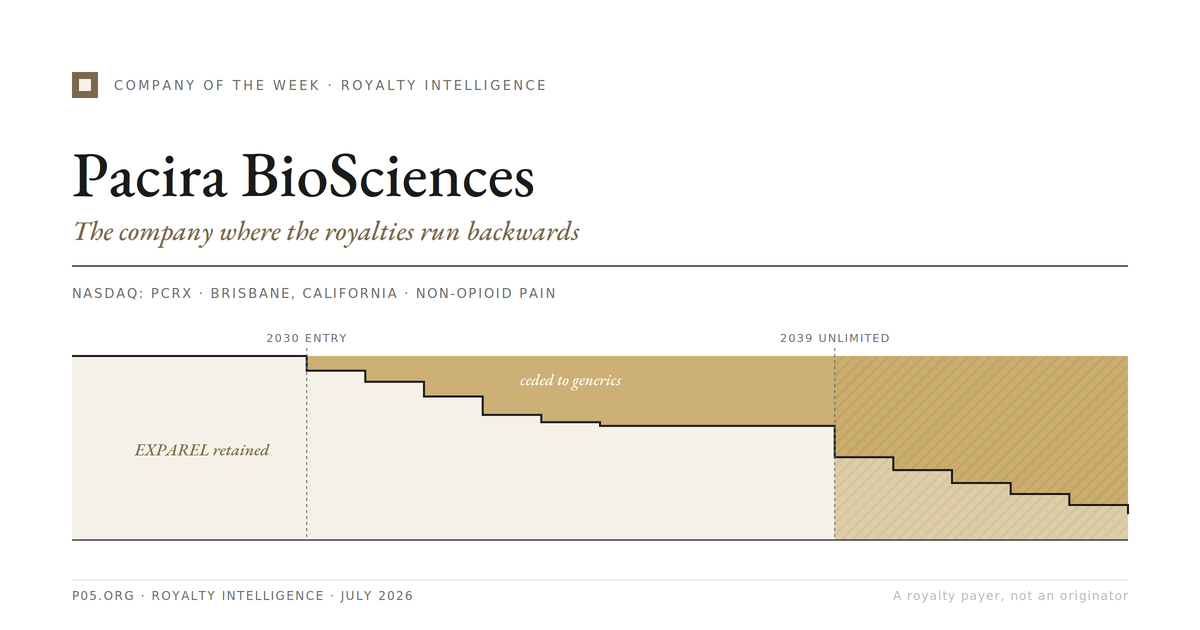

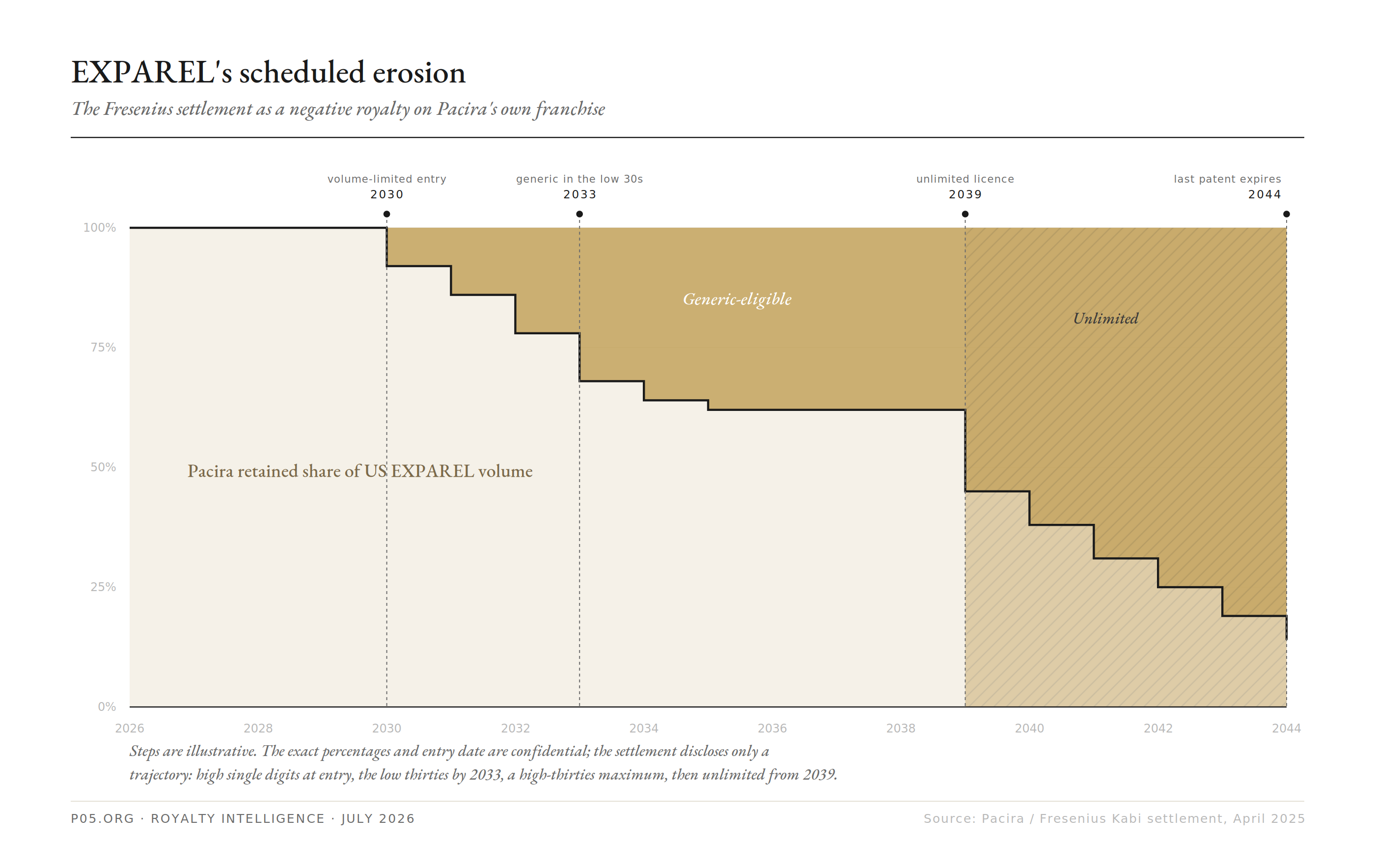

The royalty it wrote against its own franchise: the Fresenius ladder

The single most important cash-flow feature at Pacira is the EXPAREL patent settlement. It does not carry the word royalty anywhere in it.

Pacira defended EXPAREL against generic filers for years, and lost a key round in August 2024, when the District of New Jersey found the '495 patent invalid in the eVenus case.

Rather than gamble on an at-risk launch during appeal, the company settled in April 2025 with Fresenius Kabi, Jiangsu Hengrui, and eVenus. The terms trade a cliff for a slope.

Fresenius gets a licence to sell volume-limited quantities of generic EXPAREL in the United States, starting on a confidential date in early 2030.

The permitted volume begins in the high single digits as a share of total US market volume, and steps up every twelve months. It reaches the low thirties by 2033 and a maximum in the high thirties, before an unlimited licence opens in 2039. The last of Pacira's Orange Book patents does not expire until 2 July 2044.

Strip out the legal packaging and the settlement is a pre-agreed, escalating surrender of EXPAREL's own volumes: a negative royalty on the franchise that switches on in 2030 and ratchets through the mid-2030s.

What Pacira bought with it is the absence of a sudden collapse, plus roughly five more years of full exclusivity to convert EXPAREL cash into a diversified portfolio.

The sell side largely read it that way. Management has since expanded the patent estate to 21 Orange Book listings across two families, with the contested '495 patent reissued on reexamination with strengthened claims.

The line is settled with one challenger and open with others. In November 2025 Pacira sued two later filers, The WhiteOak Group and Qilu Pharmaceutical, triggering a thirty-month regulatory stay that runs into 2028. Those cases were still live in mid-2026.

EXPAREL's retained share of its own US volume. Full exclusivity holds to 2030, then a capped, rising generic share erodes it, with an unlimited licence opening in 2039. Steps are illustrative; the exact percentages are confidential. Source: Pacira / Fresenius Kabi settlement.

| EXPAREL exclusivity element | Detail |

|---|---|

| Full exclusivity through | Early 2030 (confidential date) |

| Volume-limited generic entry | Fresenius, starting in the high-single-digit % of US volumes |

| Escalation | Rises each 12 months to the low thirties by 2033, high thirties maximum thereafter |

| Unlimited generic licence | 2039 |

| Last Orange Book patent | Expires 2 July 2044 |

| Patent estate | 21 Orange Book patents, two families, exclusivity claimed into the mid-2040s |

| Still in litigation | WhiteOak and Qilu, ANDA suits filed Nov 2025, 30-month stay, pending mid-2026 |

The small claims it collects

Pacira's inbound royalty-style claims are minor, and after the Zimmer deal there are two of them.

The older one is veterinary. A version of the EXPAREL formulation sold outside the United States for animal pain is licensed to a partner (originally Aratana Therapeutics, since absorbed by Elanco).

That partner pays Pacira a tiered double-digit royalty on ex-US net sales under an agreement running to July 2033, worth about $1.2 million a quarter.

The newer one arrives with the iovera° sale: the up-to-$70 million revenue-based earnout on iovera° under Zimmer through 2031, plus the spasticity milestone.

Neither moves the needle against EXPAREL. But together they are a reminder that Pacira's only genuinely inbound streams are contingent tails on products it has either out-licensed or sold outright.

How it funds itself: debt and buybacks, not dilution

Pacira does not raise money to survive.

It is profitable on an adjusted basis, generated $726.4 million of revenue in 2025, and threw off enough cash to buy back stock through the year. Its financing choices are about structure and returns, not runway.

The debt is cheap and conventional.

The largest piece is $281.7 million of 2.125% convertible senior notes due 2029. An older 0.750% convertible issue matured in August 2025 and was repaid with $202.5 million of cash rather than refinanced.

Separately, in July 2025 Pacira retired its term loan A and replaced it with a new $300 million, five-year revolving credit facility. A partial draw on that revolver makes up most of the balance beyond the converts.

Total debt sat near $367.7 million against roughly $144.3 million of cash at the end of the first quarter of 2026. The $70 million iovera° upfront is earmarked to pay the revolver down further.

With the stock in the low $20s through the first half of 2026, well under the conversion economics of the 2029 notes, the converts behave as low-coupon debt rather than looming equity.

And the company has been shrinking its share count, not expanding it. Under a $300 million buyback authorisation it repurchased 2.24 million shares for $50.4 million in the first quarter of 2026 alone, leaving around $100 million of capacity and about 39.4 million shares outstanding.

Non-dilutive here is not clever structuring to avoid issuing equity. It is retiring equity and debt out of operating cash and asset sales, from a company whose flagship faces a scheduled decline it would rather buy shares against than hoard cash for.

| Capital item | Detail |

|---|---|

| 2029 convertible notes | $281.7M principal, 2.125% coupon, due May 2029 |

| Revolving credit facility | New $300M five-year revolver, July 2025; iovera° proceeds to pay down |

| 2025 convertible notes | 0.750%, matured Aug 2025, repaid with $202.5M cash |

| Cash | ~$144.3M (Q1 2026) |

| Total debt | ~$367.7M (Q1 2026) |

| Buyback | $300M authorisation; $50.4M used in Q1 2026; ~$100M remaining |

| Shares outstanding | ~39.4 million |

One number stays dark in an otherwise fully reported company.

The exact volume percentages and start date in the Fresenius settlement, the figures that most directly price EXPAREL's decline, are confidential by agreement. They are disclosed only as a range and a trajectory.

Even a company that files 10-Ks, 10-Qs, proxies, and 8-Ks keeps the one input that most determines terminal value out of the public text. It is the same private-data gap that defines the royalty segment, surfacing inside an issuer that otherwise hides nothing.

The settlement, then the proxy fight

The Fresenius deal did more than reshape cash flows. It became the central exhibit in an activist campaign.

DOMA Perpetual Capital Management, holding about 7.5%, ran a proxy contest into the June 2026 annual meeting.

Its argument: the board had mishandled the litigation, the settlement ceded roughly 38% of future EXPAREL volumes, management pay was excessive, and Pacira should run a formal sale process rather than keep litigating and reinvesting. It nominated three directors and called for the chief executive's removal.

The dispute is really an argument about the same schedule seen through two discount rates.

Management and its analysts call the volume ladder a win: full exclusivity to 2030, a capped and gradual entry to 2039, and a runway to diversify.

DOMA calls the identical ladder value handed away: a concentrated single product surrendering a rising slice of its own market.

Whether that is prudent risk management or an expensive giveaway depends entirely on what you assume the pipeline is worth, and how hard you discount the 2030s.

At the 9 June 2026 meeting, all three of the company's nominees (Christopher Christie, Samit Hirawat, and Thomas Wiggans) were elected, and DOMA's slate was defeated. It was the second straight year the firm ran directors and lost.

The thesis did not win the vote, but it did not disappear. It remains a standing external claim that the market is under-pricing the 2030 erosion.

And the iovera° sale three weeks later can be read either as the beginning of the portfolio focus management promised, or as a first, small concession to the pressure for asset action.

Red team vs blue team

Risk analysis (red team)

One product, on a scheduled decline. After the iovera° sale, EXPAREL is an even larger share of a two-drug company. The Fresenius settlement has already put the start of its erosion on the calendar: volume-limited generics from early 2030, rising to a high-thirties maximum, unlimited from 2039.

The decisive number is confidential. The exact entry date and volume percentages are undisclosed, so any model of the 2030 to 2039 glide path rests on a range rather than a figure.

Litigation is not closed. Fresenius, Hengrui, and eVenus are settled, but WhiteOak and Qilu remain in active ANDA litigation into 2028. A further adverse patent ruling could compress the runway the settlement was meant to lock in.

The replacement is years out and unproven. PCRX-201 is a Phase 2 gene therapy with a topline readout only expected near the end of 2026; PCRX-2002 and AMT-143 are earlier still. None is close to filling an EXPAREL-sized hole, and all must deliver on roughly the timeline the erosion begins.

Selling a grower narrows the base. iovera° was a small but double-digit-growing product, and one of Pacira's two NOPAIN-qualifying assets. Shedding it sharpens focus but concentrates the company further on EXPAREL just as the clock starts.

The activist thesis is still live. DOMA lost the vote but not the argument, keeping a sale-or-mismanagement overhang on the shares and a credible external voice pushing for strategic alternatives.

Opportunities and mitigants (blue team)

The RDF win is permanent margin. Litigating away the upstream royalty removed a senior deduction from EXPAREL net sales and clawed back $28.3 million: durable margin expansion achieved without a single extra unit.

The settlement removed a cliff. Trading a sudden generic collapse for a capped, gradual entry from 2030 keeps most of EXPAREL's economics intact for roughly five more years, and turns an existential legal risk into a plannable erosion.

Reimbursement is a self-made tailwind. NOPAIN gives EXPAREL separate Medicare payment at ASP plus six per cent in outpatient settings from 2025, a structural demand support Pacira spent years engineering rather than a one-off.

The iovera° sale is clean capital and focus. Up to $140 million for a small device, with the upfront earmarked to cut debt and contingent upside retained through the earnout and spasticity milestone. It simplifies the company into a drug business while strengthening the balance sheet.

A deeper patent estate. Pacira now cites 21 Orange Book patents across two families with claimed exclusivity into the mid-2040s, and the '495 patent that failed once was reissued with strengthened claims on reexamination.

A real second-act option. ZILRETTA (up 15% year on year) plus the J&J MedTech co-promotion is diversifying the base. And PCRX-201 with the in-housed HCAd platform gives Pacira a differentiated, RMAT-designated shot at a large prevalent disease, on exactly the timeline the runway was bought to cover.

Summary

| Risk | Concern |

|---|---|

| Concentration | EXPAREL ~80% of revenue, scheduled erosion from 2030, more so post-iovera° |

| Confidential terms | Exact generic entry date and volume percentages undisclosed |

| Open litigation | WhiteOak and Qilu ANDA suits pending into 2028 |

| Pipeline timing | PCRX-201, PCRX-2002, AMT-143 all years from replacing EXPAREL cash |

| Activist overhang | DOMA lost the vote but keeps a sale thesis alive |

| Narrower base | Divesting a growing, NOPAIN-eligible device concentrates the company |

| Opportunity | Observation |

|---|---|

| Margin uplift | RDF royalty extinguished, $28.3M recovered, permanent benefit |

| No cliff | Settlement converts a collapse into a capped glide to 2039 |

| NOPAIN tailwind | Separate Medicare payment for EXPAREL from 2025 |

| Clean capital | iovera° sale cuts debt, keeps contingent upside; buybacks continue |

| Deeper IP | 21 Orange Book patents, two families, strengthened '495 |

| Second act | ZILRETTA growing double digits; PCRX-201 gene-therapy option |

Conclusion

Pacira is a royalty story told from the paying side.

It owns its drugs, so it holds almost nothing worth calling an inbound stream. Its royalty life is defined by what it owes, and what it does with those obligations.

It litigated away an upstream royalty it had carried for two decades, and recovered the cash. It still reports a milestone CVR to Flexion's former holders that, on current numbers, will lapse worthless at the end of 2030. It has priced a quasi-royalty into its own future, a scheduled surrender of EXPAREL volumes to a generic from 2030. And it has just sold iovera° to Zimmer Biomet for upfront cash plus an earnout, swapping an owned product for a contingent tail and a smaller debt load.

The financing points the same way.

This is not a company reaching for a royalty sale or an equity raise. It is a cash-generative franchise using cheap convertible debt, repaying maturities instead of rolling them, selling non-core assets to cut debt, and buying back its own shares, while a self-lobbied reimbursement law props up demand for its lead product.

The tests over the next two years are concrete.

Whether the WhiteOak and Qilu suits hold the 2030 line the Fresenius settlement drew will decide if that date is firm or soft.

Whether ZILRETTA and the J&J co-promotion keep diversifying a now-narrower base will show how single-threaded the company still is when erosion begins.

And whether PCRX-201's ASCEND readout lands will decide whether the runway the settlement bought was spent on a genuine second act or merely on a slower descent.

Until then, Pacira is best read not as a royalty originator, but as a royalty payer that has spent two years actively managing what it owes, and is now starting to sell what it no longer wants to keep.

All information in this article was accurate as of the research date and is derived from publicly available sources including company press releases, SEC filings, court records, and financial news reporting. The iovera° divestiture to Zimmer Biomet was announced on 30 June 2026 and had not yet closed as of the research date; its terms are described as disclosed by the parties. Certain terms, including the exact volume-limited percentages and generic entry date under the Fresenius Kabi settlement, are confidential and are described here only as far as public sources and disclosed ranges allow. Financial figures reflect the most recent reported periods available at the research date and may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.