Fund of the week: The Michael J. Fox Foundation

The Michael J. Fox Foundation for Parkinson's Research (MJFF) is the largest nonprofit funder of Parkinson's research in the world, and, unusually for this series, it files a full public tax return. It is donor-funded, evergreen, and structured as a grantmaker rather than an investor. Its Form 990 royalty line was zero every year from FY2011 through FY2023, then reported roughly $1.28M in FY2024, the first non-zero figure on file. This profile examines what that number is, what it is not, and why a royalty desk should care about MJFF chiefly as an originator of assets whose economics accrue elsewhere.

At a glance

- What it is: 501(c)(3) public charity, EIN 13-4141945, founded 2000, New York

- Scale: more than $3 billion funded into Parkinson's research to date (2026)

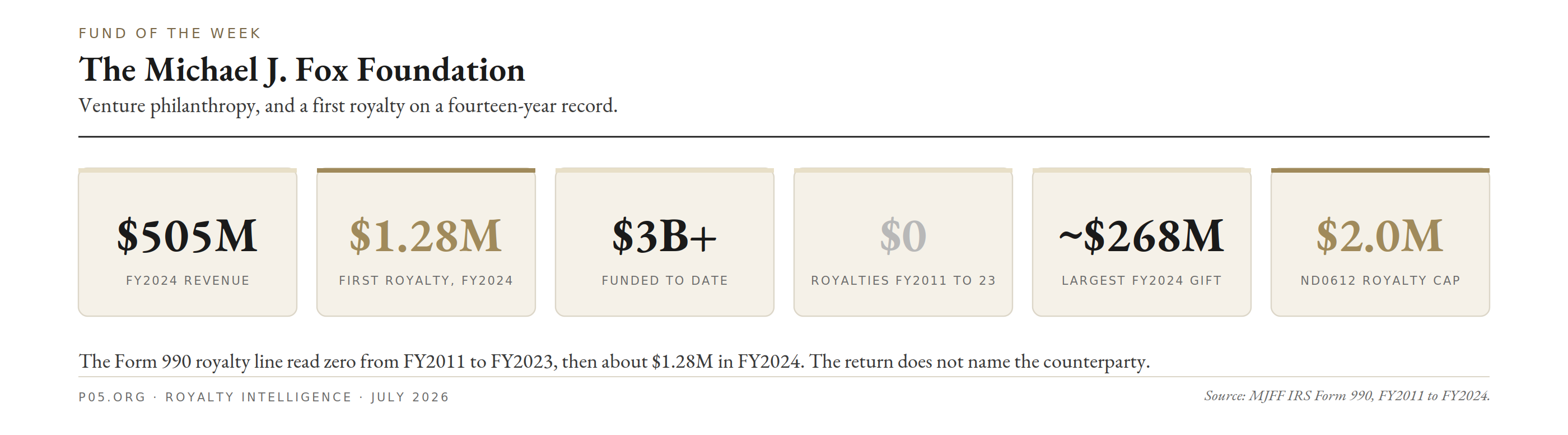

- FY2024 revenue: about $505M, of which about $490M contributions

- FY2024 grants paid: about $343M (about $240M domestic, about $103M foreign)

- Net assets (FY2024): about $196M

- Royalty income: $0 every year FY2011 to FY2023, then about $1.28M in FY2024

- Model: non-dilutive research grants, with optional case-by-case return-payment clauses

- Owned IP: minimal; no significant patent estate, no venture vehicle

- Disclosure: full Form 990 annually, audited on a consolidated basis

- Note: as of July 2026, the FY2025 Form 990 was not yet available

MJFF was founded in 2000 by the actor Michael J. Fox and Deborah W. Brooks. Because it files a full Form 990, its balance sheet, grant flows and executive pay are public, a level of disclosure a private manager does not provide.

Its economics resemble those of the Retinal Degeneration Fund profiled earlier in this series: a mission-return vehicle that runs on contributions rather than yield. What distinguishes MJFF for this readership is the return-payment mechanism inside its grants, a single new figure on the FY2024 return, and a documented royalty interest whose underlying product reached the market in 2026.

For a royalty or structured-credit reader, three things are worth separating at the outset: what MJFF is permitted to do, what it has actually done, and what its funded programs do downstream. Each is addressed below, with reported figures attached and inference flagged as inference.

Investment thesis and mandate

MJFF describes itself as a venture philanthropy. It provides non-dilutive funding to early-stage projects to build the data packages that help a program attract larger funders, collaborators, or an acquirer.

The stated rationale is that many scientifically sound Parkinson's projects cannot raise a clean private round on their own, so a de-risking grant fills the gap.

The mandate is broad within the disease area. It spans basic, translational and clinical research, and funds large pharmaceutical companies, small biotechs and academic laboratories. Its scientific priorities centre on alpha-synuclein, the genetic subtypes LRRK2 and GBA1, and objective biomarkers of onset and progression.

The differentiator MJFF emphasises is infrastructure and convening power: a global biomarker study, a biobank, a data platform, and a network that industry co-funds. That is the Foundation's own framing and is presented here as such.

How capital enters and returns

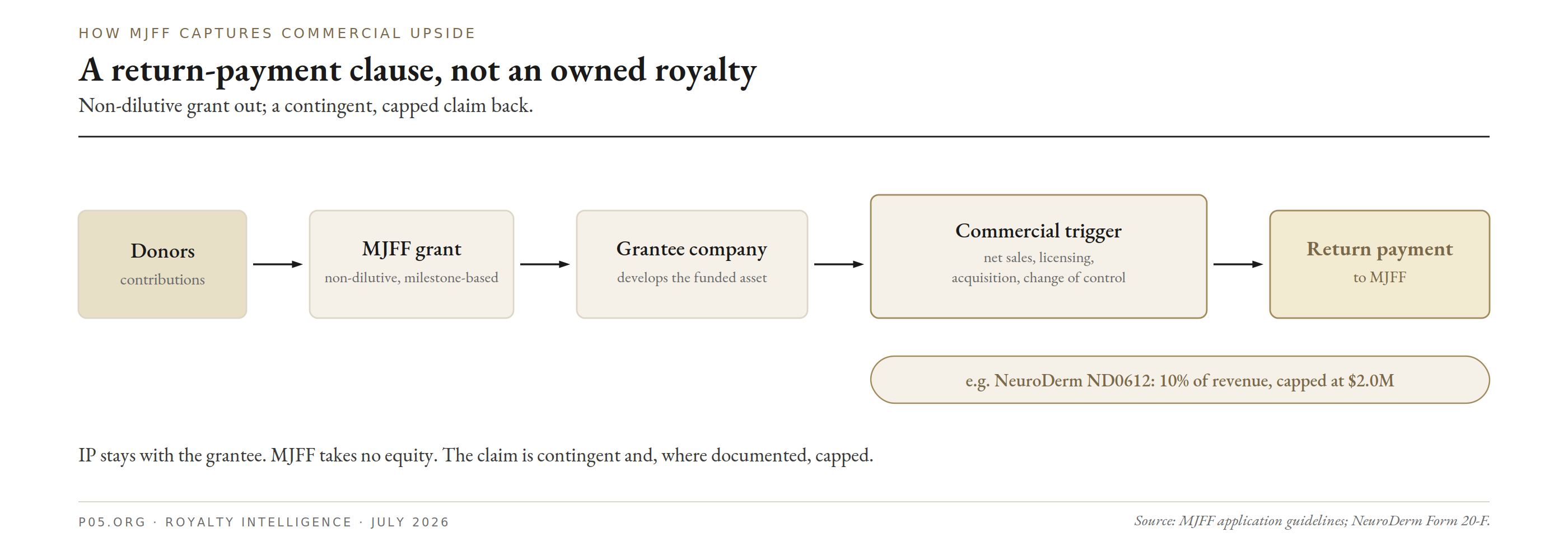

The mechanism is a loop that is mostly, but not entirely, charitable.

Donor capital enters as a contribution. MJFF deploys it as a research grant built around milestones and deliverables rather than equity. When a funded program succeeds, the primary return is a scientific or clinical result, and any commercial value usually accrues to the grantee.

The feature that places MJFF within scope for this publication is that its grants can carry a claim on the grantee's commercial upside. Per its published application guidelines, funding agreements may include return payment terms tied to downstream commercial milestones, such as net sales, licensing, acquisition, or change of control, negotiated case by case. Separately, MJFF states that discoveries made under its sponsorship belong to the researcher, who has first opportunity to commercialise them.

In this publication's terms, MJFF does not take equity and does not, by default, own IP, but it can hold a contingent, revenue-linked or milestone-linked claim on a funded product. That is a return-payment mechanism inside a charitable grant, applied selectively, not a standing royalty book.

The consequence, visible below, is that revenue is dominated by contributions, realised commercial returns have historically been near zero, and the first reported royalty income appears only in the most recent year on file.

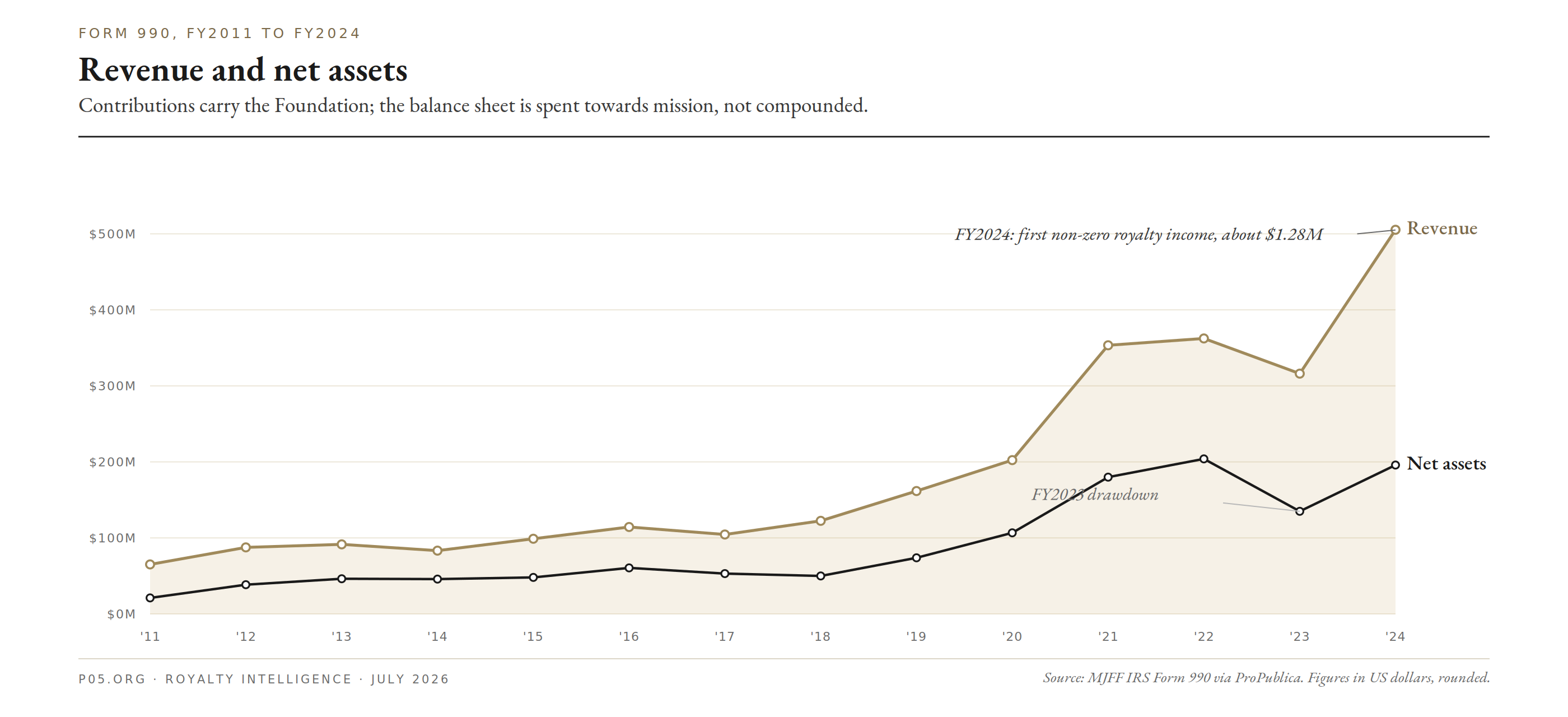

Financial profile and assets

Because MJFF files a full Form 990, its income statement and balance sheet are public. The table below covers the full digitised history, for fiscal years ending 31 December, via ProPublica Nonprofit Explorer. Figures in millions of dollars, rounded.

| FY (Dec) | Revenue | Contributions | Royalties | Net assets |

|---|---|---|---|---|

| 2011 | 65.2 | 65.0 | 0 | 21.1 |

| 2012 | 87.5 | 87.3 | 0 | 38.4 |

| 2013 | 91.5 | 90.7 | 0 | 46.2 |

| 2014 | 83.2 | 82.9 | 0 | 45.9 |

| 2015 | 98.9 | 97.2 | 0 | 48.1 |

| 2016 | 114.4 | 113.9 | 0 | 60.6 |

| 2017 | 104.5 | 103.2 | 0 | 53.0 |

| 2018 | 122.4 | 121.4 | 0 | 50.0 |

| 2019 | 161.7 | 157.7 | 0 | 73.9 |

| 2020 | 202.3 | 199.0 | 0 | 106.7 |

| 2021 | 353.4 | 350.7 | 0 | 180.0 |

| 2022 | 362.4 | 358.3 | 0 | 204.0 |

| 2023 | 316.1 | 303.5 | 0 | 135.0 |

| 2024 | 505.3 | 490.2 | 1.3 | 195.9 |

Source: MJFF Form 990 filings via ProPublica Nonprofit Explorer.

[Figure opportunity, house style: a two-line time series, revenue and net assets 2011 to 2024, with a marker on FY2024 flagging the first non-zero royalties line.]

Contributions carry the Foundation

In every year on record, contributions are roughly 96 to 99 percent of revenue. Investment income is small in absolute terms, though it has grown with net assets, reaching about $12.9 million in FY2024.

The revenue line is lumpy

Revenue roughly tripled between the mid-2010s and the 2020s, but not smoothly. FY2024 stands at about $505 million, and the FY2024 filing's Schedule B shows a single anonymised gift of roughly $268 million in donated securities, the largest of the year. A single gift can therefore move a full year's total.

FY2023 was a drawdown year

In FY2023, MJFF spent ahead of what it raised, running about $386 million of expenses against $316 million of revenue, and net assets fell from about $204 million to about $135 million before recovering to about $196 million in FY2024. This reflects an evergreen balance sheet spent toward mission rather than compounded.

Royalty income was zero for thirteen years, then positive

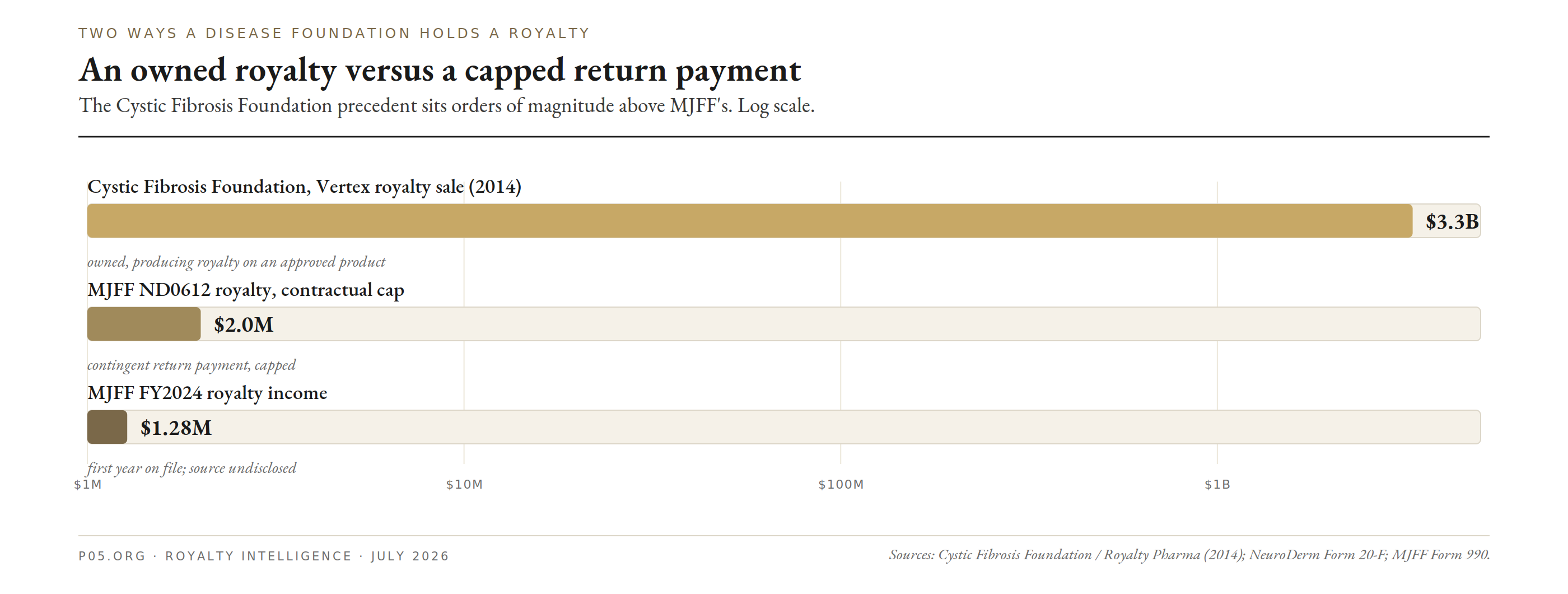

Every Form 990 from FY2011 through FY2023 reports zero on the royalties line. The FY2024 filing reports about $1.276 million, booked as passive income excluded from unrelated-business tax, which is consistent with a licensing-type royalty rather than an operating activity. The return does not name the counterparty. The source is examined in the IP and royalties section below.

The balance sheet is mostly promises and commitments

Net assets of about $196 million are not held as a large liquid endowment. On the FY2024 balance sheet, the largest asset is roughly $170 million of pledges and grants receivable, and the largest liability is roughly $205 million of grants payable, commitments made but not yet disbursed. Net assets should be read as book equity at a point in time, not as available cash.

Spending reaches the mission efficiently

Of about $452 million in FY2024 expenses, grants were about $343 million and total program spending about $404 million, close to 89 percent of expenses on program, with roughly 7 percent on fundraising and 4 percent on management and general. Grants split roughly $240 million domestic and $103 million foreign.

Reconciling the size figures

Several numbers circulate, and they measure different things.

- Cumulative: MJFF states it has funded more than $3 billion of Parkinson's research to date, and in early 2026 was described as having put more than $2 billion directly to scientists. Cumulative figures can include co-funded and leveraged programs.

- Annual flow: the Form 990 shows revenue of roughly $200 million to $505 million across recent years, almost all contributions.

- Balance sheet: net assets of about $196 million at FY2024 is the only audited point-in-time figure.

The $3 billion cumulative figure should not be read as a balance-sheet number.

Donors and the LP-equivalent base

MJFF has no limited partners. The people who would be LPs are donors to a charity whose return is measured in mission progress. That base is partly public, because charities name their anchors and the 990 discloses gift sizes.

Concentration is a feature of the base. The FY2024 Schedule B lists one gift of roughly $268 million in donated securities, with the next-largest disclosed gifts at roughly $39 million, $15 million and $13 million.

The named anchors are substantial. MJFF's flagship study is backed by the Sergey Brin Family Foundation and by Aligning Science Across Parkinson's (ASAP), the Brin-funded open-science initiative, with a lead gift from the Edmond J. Safra Philanthropic Foundation, and further named support from families including the Ballmers. The study is also funded by a consortium of more than 40 biotech and pharmaceutical firms and by tens of thousands of individual donors.

The board includes capital-markets and media figures, among them Blue Owl Capital's Douglas Ostrover and Marc Lipschultz, AIG chief executive Peter Zaffino, Greenlight Capital's David Einhorn, Karen Finerman, and public figures including Ryan Reynolds, George Stephanopoulos and Tracy Pollan. This is noted as an indicator of fundraising reach rather than as governance commentary.

The base is therefore a mix of technology-fortune philanthropy, disease-affected families, an industry consortium and mass giving, anchored by a small number of very large gifts. That gives MJFF patience a return-seeking fund lacks, and a fundraising ceiling tied to donor appetite.

Governance and compensation

MJFF is led by co-founder and CEO Deborah W. Brooks, with Michael J. Fox as founder. Per the FY2024 Form 990, Fox draws no compensation.

Reported FY2024 pay: Brooks about $1.47 million; Todd Sherer, the former CEO now Chief Mission Officer, about $1.21 million; Chief Program Officer Sohini Chowdhury about $0.98 million. The science function is led by two Chief Science Officers, Mark Frasier and Brian Fiske. The board lists Andrew J. O'Brien as chairman.

Total executive compensation was about $4.7 million against total expenses of about $452 million, a fraction of a percent of the money moved. MJFF is audited on a consolidated basis and undergoes a federal single audit, consistent with its receipt of some federal awards. These are disclosed facts rather than judgements.

IP, royalties, and the economics of return

This is the section most relevant to this readership. It separates several distinct points, and it distinguishes confirmed facts from inference.

1. Royalty income was zero for over a decade, then positive in FY2024

Every Form 990 from FY2011 through FY2023 reports zero royalty income. FY2024 reports about $1.276 million, recorded as passive income excluded from unrelated-business tax. The return does not disclose the source. As of July 2026, the FY2025 Form 990 was not yet available, so whether the line recurred cannot yet be confirmed from filings.

2. The return-payment mechanism is real and documented in grantee filings

MJFF grants can include return payments tied to net sales, licensing, acquisition or change of control. Grantee SEC filings confirm the mechanics and provide occasional hard terms:

- NeuroDerm: on a 2013 grant of about $1.0 million, NeuroDerm's Form 20-F states an obligation to pay MJFF a 10 percent royalty on ND0612 revenue, capped at a maximum of $2.0 million, after which no further obligation exists.

- MapLight Therapeutics: its filings state possible future payments to MJFF capped at two times the grant awards received, contingent on certain net product sales. MapLight's MJFF grants total $25.7 million across four agreements (2020 to 2022).

- Sangamo/Ceregene: a 2010 grant required royalty payments based on annual net sales of the CERE-120 program, which was later discontinued.

- By contrast, an earlier Omeros grant carried no royalty obligation to MJFF, showing the terms are negotiated case by case.

MJFF does not, by default, own the resulting IP. The contingent claim, where it exists, is a negotiated recapture clause, not a securitisable royalty interest that MJFF holds and could sell.

3. A targeted SEC search did not surface an FY2024 payment to MJFF

A full-text search of grantee SEC filings found no company disclosing an FY2024 royalty or milestone payment to MJFF. In particular, MapLight's FY2025 Form 10-K shows MJFF grant funds flowing to the company (about $1.0 million recognised in 2024 and $3.2 million in 2025), that is, MJFF spending rather than receiving; its return-payment obligation has not triggered because the company is pre-commercial. NeuroDerm's ND0612 was not approved anywhere during FY2024. Other royalty-bearing grantees are pre-commercial or discontinued.

The absence of a disclosed payment in public filings makes a US-sales royalty from a public grantee unlikely as the FY2024 source, and points instead toward either a private grantee milestone or a licensing royalty on a research tool, diagnostic, dataset or biobank that would not appear in a product company's filings.

4. Candidate sources for the FY2024 royalty, ranked by evidence

Attribution is inference; the return does not name a counterparty.

- Candidate A, a return payment triggered by a 2023 to 2024 commercial milestone from an undisclosed or private grantee. This is the most consistent with the documented mechanism and with a first-time figure near the size of a capped return payment. The product is not identified.

- Candidate B, NeuroDerm ND0612. MJFF holds a documented capped royalty, but ND0612 had no marketing approval in FY2024 (US Complete Response Letter in 2024), so a sales-based trigger in FY2024 is unlikely.

- Candidate C, the Amprion alpha-synuclein assay. Developed with MJFF and PPMI support, but no public document establishes that MJFF holds a license or royalty right in Amprion's test, which Amprion says it owns. Speculative.

5. MJFF holds essentially no owned patent estate

MJFF does not appear as an assignee on any significant patent portfolio. Its IP position is effectively two things: research tools, antibodies and animal models it sponsors and distributes at cost through partners, where the depositing investigator retains rights; and PPMI datasets and biosamples, shared broadly. The alpha-synuclein seed amplification assay IP is held by Amprion, not MJFF.

6. The originated asset that matters most is a biomarker

MJFF's central originated asset is its longitudinal study, the Parkinson's Progression Markers Initiative, launched in 2010 and renamed in May 2026 the Parkinson's Precision Medicine Initiative.

Its samples underpinned the 2023 validation of the alpha-synuclein seed amplification assay, the first tool to detect Parkinson's pathology in living people, and the 2024 publication of a biological staging system. In September 2024 the FDA issued a letter of support for the biomarker in trials. The assay is delivered commercially by Amprion. Whether MJFF participates in that commercial layer is not established in public filings; the asset was originated upstream of any royalty its use may generate.

7. A documented forward catalyst: ND0612 reached the market in 2026

The clearest royalty interest MJFF holds is the capped 10 percent royalty on ND0612. That product, developed by NeuroDerm and now branded Onerji, received European Commission marketing authorisation on 27 April 2026. Its US application was resubmitted in 2025 with a regulatory decision due in late 2025.

Because MJFF's ND0612 royalty triggers on revenue after marketing approval, European sales from 2026 create a datable path for MJFF to collect against the $2.0 million cap in FY2026 and beyond. Two caveats apply: this post-dates FY2024, so it does not explain the FY2024 figure; and NeuroDerm is wholly owned by Mitsubishi Tanabe Pharma, a private Japanese parent, so any resulting royalty to MJFF is unlikely to appear in US public filings.

8. No royalty monetisation, and no venture vehicle

No transaction resembling a royalty sale, revenue-interest financing, or structured deal with a dedicated royalty investor was found. MJFF has no for-profit subsidiary, LLC, or venture fund. Its only consolidated affiliate is MJFF Canada, a registered Canadian charity whose operations were not significant in 2024 and 2023.

How MJFF compares to royalty-holding disease foundations

The venture-philanthropy field contains several structures for capturing commercial returns. MJFF sits at the lighter-touch end.

- The Cystic Fibrosis Foundation is the reference case for monetisation. In November 2014, Royalty Pharma acquired the CF Foundation's royalties on Vertex's cystic fibrosis therapies for $3.3 billion, and the Foundation later monetised a residual interest for up to roughly $650 million. That model requires an owned, producing royalty on an approved product.

- Breakthrough T1D, formerly JDRF, runs the T1D Fund, an equity-investing venture-philanthropy subsidiary that recycles realised gains into new investments rather than distributing them.

- MJFF uses neither structure. It relies on non-dilutive grants with contingent return-payment clauses, which, until FY2024, produced no realised royalty income. The FY2024 figure is a first data point rather than evidence of a durable stream, and the size gap with the CF Foundation precedent is several orders of magnitude.

Portfolio of enabled assets and programs, as of July 2026

MJFF holds a portfolio of funded and originated programs, not investments in the private-fund sense. The table reflects the most royalty-relevant.

| Program or asset | What it is | Royalty or licensing relevance |

|---|---|---|

| PPMI, now Parkinson's Precision Medicine Initiative | Biomarker study and biobank since 2010 | Generated the data behind the aSyn-SAA biomarker and the NSD staging system; 40+ firms co-fund and use it |

| aSyn-SAA biomarker | First assay to detect PD pathology in living people (2023) | Delivered commercially via Amprion; FDA letter of support 2024; MJFF's rights, if any, undocumented |

| ND0612 (Onerji) | Subcutaneous levodopa/carbidopa infusion (NeuroDerm/Mitsubishi Tanabe) | MJFF holds a 10% royalty capped at $2.0M; EU approval April 2026 is a forward catalyst |

| Inbrija (Civitas to Acorda) | Inhaled levodopa for "off" episodes | Civitas acquired about $525M (2014); approved 2018; no confirmed royalty to MJFF |

| Kynmobi (Cynapsus to Sunovion) | Sublingual apomorphine film | Cynapsus acquired about $624M (2016); approved 2020; discontinued 2023 |

| MapLight programs | Circuit-based PD and neuropsychiatric therapeutics | Return payment capped at 2x grants on net sales; pre-commercial |

| ASAP Collaborative Research Network | Global open-science network on PD biology | $261M in new grants April 2026; open-access terms; no fees to MJFF |

Blue team and red team

Blue team: the case for

An origination role with few peers. A disease-specific biobank, a validated biomarker and a global cohort study are resources a generalist cannot easily replicate. Industry co-funds the infrastructure MJFF built.

A record of de-risking to an outcome. MJFF grants sit behind approved therapies and large acquisitions, a biomarker with FDA backing, and genetic-subtype programs now in industry hands.

Patient, disclosed capital. Because proceeds serve a charity rather than fee-sensitive LPs, MJFF can spend through long neurodegeneration timelines, and its financials are public.

A first realised royalty and a documented forward catalyst. The FY2024 royalty line turned positive, and the ND0612 EU approval gives the capped ND0612 royalty a concrete path to pay.

Red team: the case against

The commercial return is small and, so far, a single year. About $1.28 million against about $452 million of annual spend is immaterial financially, and the source is undisclosed.

Value accrues mostly to others. By design, MJFF originates assets whose acquisition value and product royalties land on company balance sheets, not its own.

Donor concentration and spend-down. FY2024's record year leaned on one roughly $268 million gift, and the model is built to be spent rather than compounded.

Size figures require care. The cumulative, annual and balance-sheet numbers measure different things, and only net assets are audited point-in-time.

Implications for the pharmaceutical royalty and biotech capital markets

For commercial capital markets, MJFF is relevant mainly as a source and a signal.

As a source of assets. MJFF originates and de-risks the Parkinson's programs, targets and tools that later carry orphan and precision-medicine economics, partnered licences, and milestone and royalty flows. The historical exits and the current LRRK2, GBA1 and ND0612 programs are the pipeline whose downstream economics appear on other parties' term sheets.

As the origin of a category-defining biomarker. The alpha-synuclein assay and the associated staging system are changing trial design and diagnosis across Parkinson's and related conditions, which reshapes which assets get funded and where royalty-bearing approvals form.

As a lighter-touch model of contingent structures inside philanthropy. MJFF's return-payment clauses are a documented, publicly filed example of a charitable balance sheet reaching for commercial upside without equity or an owned royalty book. The honest footnote is that its royalty line only turned positive in 2024, modestly, and that the one clearly documented royalty interest, on ND0612, is capped at $2.0 million.

Recent filings and developments, as of July 2026

- FY2025 Form 990: not yet available as of July 2026. MJFF's fiscal year ends 31 December and it files on extension, so whether the royalty line recurred in FY2025 cannot yet be confirmed.

- MapLight FY2025 Form 10-K (filed 2026): confirms MJFF grant funds flowing to the grantee, not a royalty to MJFF; the return-payment obligation remains untriggered.

- ND0612 (Onerji): European Commission marketing authorisation granted 27 April 2026; US decision due in late 2025. Relevant to MJFF's capped ND0612 royalty going forward, not to FY2024.

- ASAP Collaborative Research Network: $261 million expansion announced with MJFF in April 2026, on open-access terms.

Financial history and recent developments

| Date | Event |

|---|---|

| 2000 | MJFF founded by Michael J. Fox and Deborah W. Brooks |

| 2010 | PPMI, the biomarker cohort study, launched |

| 2013 | NeuroDerm grant carries a 10% royalty on ND0612, capped at $2.0M |

| 2014 | Civitas acquired by Acorda (about $525M); Inbrija later approved 2018 |

| 2016 | Cynapsus acquired by Sunovion (about $624M); Kynmobi later approved 2020 |

| Apr 2023 | aSyn-SAA biomarker validated using PPMI samples (Lancet Neurology) |

| Jan 2024 | Biological staging system published (Lancet Neurology) |

| Sep 2024 | FDA letter of support for the aSyn-SAA biomarker in trials |

| FY2024 | First reported royalty income (about $1.28M); revenue about $505M on a single about $268M securities gift; net assets about $196M |

| Feb 2026 | Reported as the largest funder of PD research, over $2 billion directly to scientists |

| Apr 2026 | ND0612 (Onerji) receives EU marketing authorisation; ASAP and MJFF announce a $261M network expansion |

| May 2026 | PPMI renamed the Parkinson's Precision Medicine Initiative; cumulative funding cited above $3 billion |

| Jul 2026 | FY2025 Form 990 not yet available |

Conclusion

MJFF is a venture-philanthropy vehicle that is easier to read than most private funds because it files a full public return. Donors give, MJFF funds Parkinson's research across academia and industry, and realised value returns mainly as scientific progress.

On the question this publication tracks, the position is now more textured than a flat zero, but it should not be overstated. Return payments and milestone recapture are in the grant toolkit, applied case by case. Realised returns to date came through grantee acquisitions and approvals rather than cash to MJFF. The Form 990 royalty line turned positive for the first time in FY2024, at about $1.28 million, from a source the return does not disclose and that a targeted SEC search did not surface. The one clearly documented royalty interest, on ND0612, is capped at $2.0 million and only became collectable once the product reached the market in 2026.

The reason to follow MJFF is upstream. It is among the most significant originators and de-riskers of Parkinson's assets and biomarkers, and those assets are the ones whose licences, milestones and royalties later appear on other parties' term sheets. The near-term signals to watch are the next FY2025 return, which will show whether the royalty line recurs, the commercial trajectory of the biomarker, and ND0612 sales against the capped royalty.

All information in this article was accurate as of the publication date and is derived from publicly available sources including the Michael J. Fox Foundation's IRS Form 990 filings, grantee SEC filings, the Foundation's own disclosures and announcements, regulatory and peer-reviewed publications, company and partner press releases, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.