Insolvency Liens in Pharma Royalty Transactions: The Risk That Reshapes Deal Structure

When Clearside Biomedical filed for Chapter 11 protection in November 2025, equity holders quickly zeroed in on a detail buried in the company's pre-petition filings: a September 2025 amendment to its royalty agreement with HealthCare Royalty Partners had allegedly waived a contingent $12.5 million payment, nearly five times the $2.7 million stalking horse bid for the company's entire asset base. The company had no funded debt.

The royalty subsidiary structure, designed to protect HealthCare Royalty's interest through insolvency, was functioning exactly as intended. But the interaction between that structure and the remaining estate created precisely the kind of complex allocation dispute that defines insolvency risk in pharmaceutical royalty transactions.

This is not an edge case. The biotechnology sector has experienced an unprecedented wave of insolvencies: 14 Chapter 11 filings in 2023, 13 in 2024, and the pace has continued into 2025 and 2026. More than $32.7 billion in royalty-linked transactions closed between 2020 and 2025, creating a growing pool of royalty interests that must survive counterparty distress. The structural protections built into these transactions, the liens, the true sale opinions, the bankruptcy-remote vehicles, are no longer theoretical. They are being tested in courtrooms.

This article examines how insolvency liens operate in pharmaceutical royalty transactions, the legal architecture that protects or fails to protect royalty holders, the cross-border complications that arise when counterparties span multiple jurisdictions, and the case law from 2022 to 2026 that is actively reshaping deal structure.

What Are Insolvency Liens in Pharma Royalty Transactions?

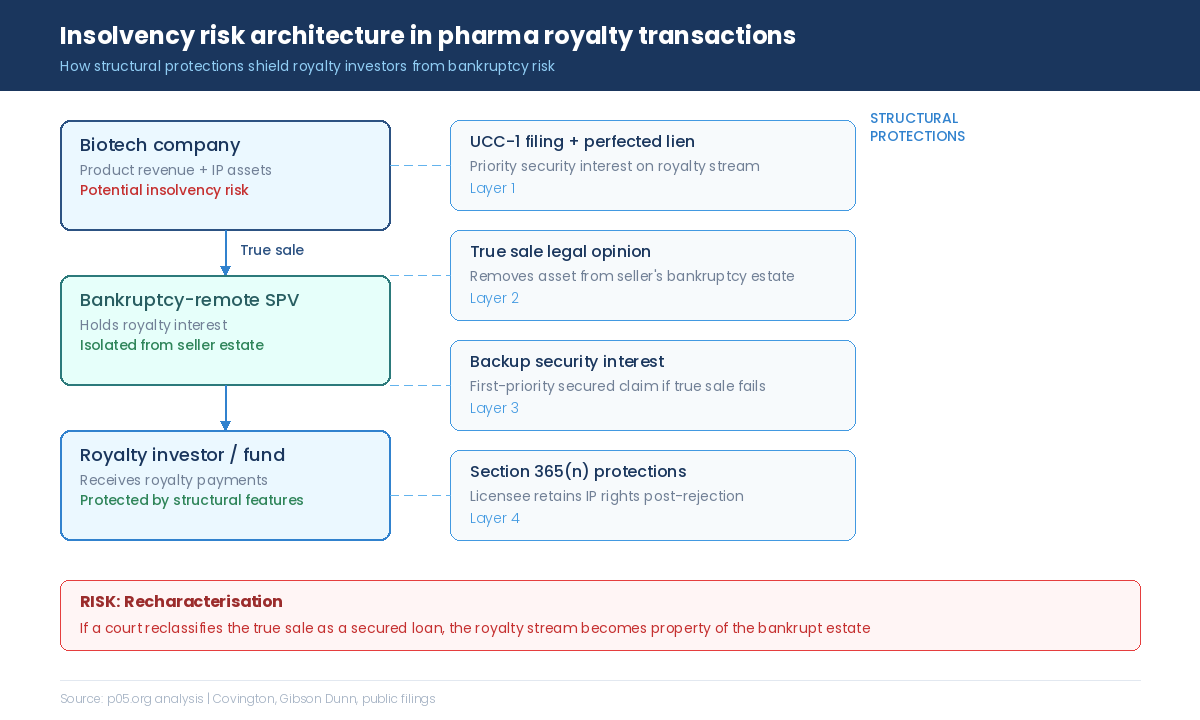

The term "insolvency lien" in this context refers to the security interests, claims, and structural protections that determine what happens to a royalty stream when the underlying obligor enters bankruptcy or insolvency proceedings. It is not a single legal concept but an umbrella covering several interlocking mechanisms: UCC-perfected security interests, true sale characterisation, backup liens, SPV structures, and the interplay between these protections and applicable bankruptcy or insolvency law.

The fundamental question is straightforward: does the royalty holder own an asset that sits outside the bankrupt estate, or does it hold a claim against an estate that may not have enough assets to satisfy everyone?

The answer depends entirely on how the transaction was structured at inception. A well-structured royalty transaction places the royalty interest beyond the reach of the seller's creditors. A poorly structured one leaves the royalty holder competing with every other creditor for whatever value remains after bankruptcy costs, secured lenders, and priority claims have been satisfied.

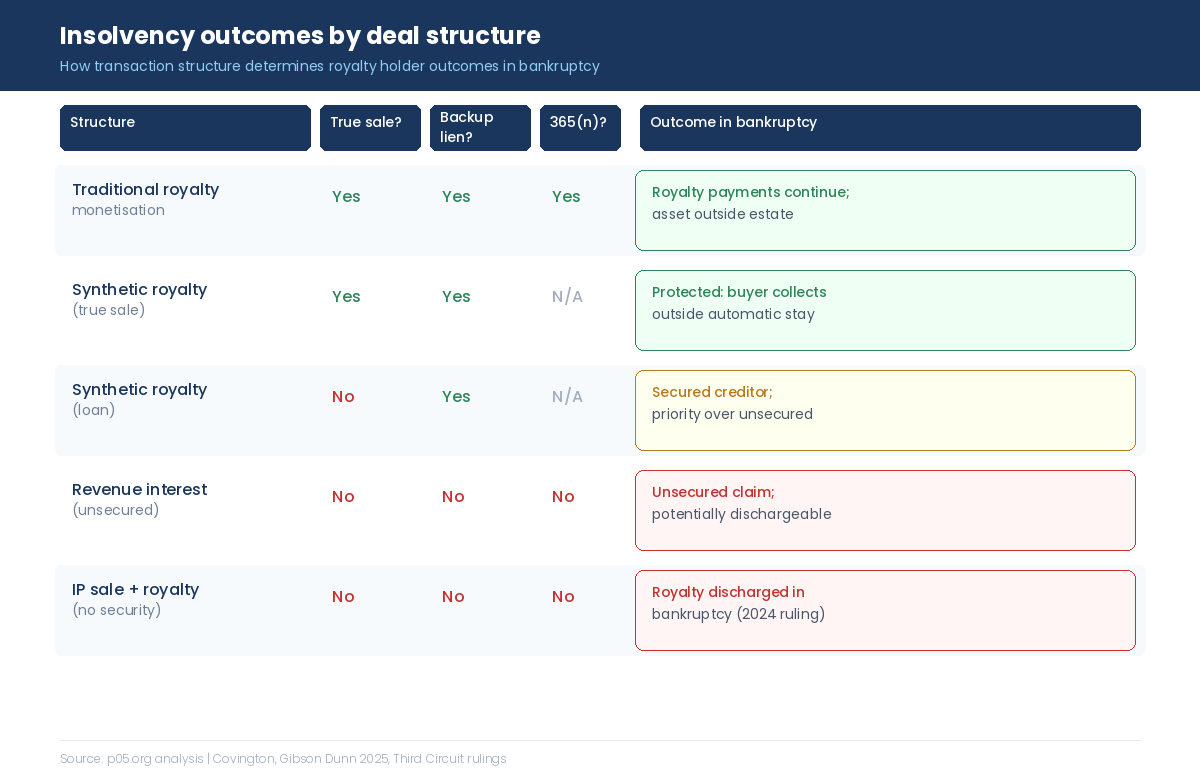

The Third Circuit's April 2024 ruling in In re Mallinckrodt PLC demonstrated the catastrophic end of that spectrum: Sanofi lost a perpetual royalty on a drug generating nearly $1 billion in annual sales because the transaction was structured as an outright IP sale with no retained security interest, no licence, and no structural protection.

The Mallinckrodt outcome is now well understood. What is less appreciated is how the four layers of structural protection interact, how they differ across jurisdictions, and how recent cases have exposed gaps that the standard deal playbook does not always address.

The True Sale Question: The Central Structural Risk

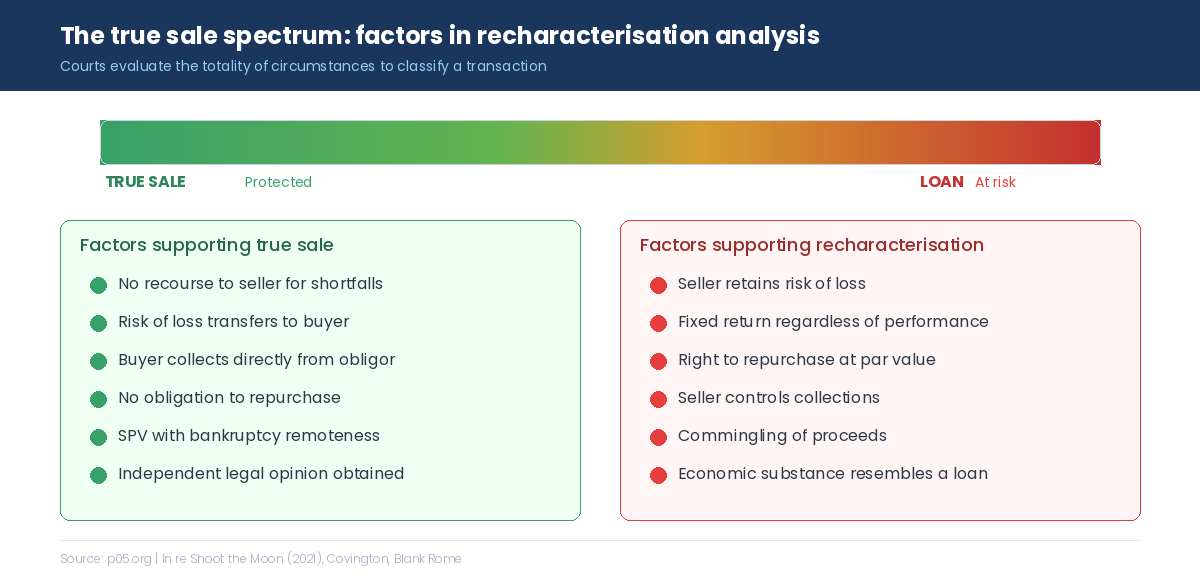

The most consequential legal question in any royalty monetisation is whether the transaction will be respected as a "true sale" in bankruptcy or recharacterised as a secured loan.

In a true sale, the royalty interest has been irrevocably transferred from the seller to the buyer. If the seller files for bankruptcy, the royalty stream is not property of the bankrupt estate. The buyer continues to collect payments uninterrupted, unaffected by the automatic stay.

In a recharacterised transaction, the court determines that the economic substance of the deal was a loan. The "sold" royalty interest becomes collateral, which means it is property of the estate. The buyer's interest is reduced to a secured claim if the security interest was properly perfected, or an unsecured claim if it was not.

Whether a transaction qualifies as a true sale requires what courts describe as a "fact-intensive analysis of the totality of the circumstances."

The inquiry focuses on how the parties allocated risk. As the bankruptcy court held in In re Shoot the Moon (2021), simply labelling a transaction as a true sale is not sufficient. The court focused on whether the risk of loss genuinely transferred to the buyer, whether the seller retained a repurchase obligation, and whether the economic substance of the arrangement resembled a loan.

Gibson Dunn's 2026 Royalty Finance Market Update, analysing 133 life sciences royalty transactions from 2020 through 2025 totalling $32.7 billion, confirms that the market has decisively shifted toward true sale structures.

In 2020 and 2021, roughly half of synthetic royalty transactions were documented as true sales. By 2024 and 2025, that figure reached 71% of deals and 91% of value. The shift was catalysed by Royalty Pharma's transaction approach and has been broadly adopted across the buyer market.

For synthetic financings structured as true sales, Gibson Dunn found that a product-level lien is expected for all but the largest and most credit-worthy counterparties. Where a synthetic financing is structured as a loan, a lien on key assets, if not all assets, is standard. Non-incurrence covenants, which prevent the seller from layering additional secured debt on product-related assets, are present in 96% of synthetic royalty financings.

The Backup Security Interest and Section 365(n)

Even in true sale structures, most royalty purchasers obtain a backup security interest: a belt-and-suspenders mechanism that converts the buyer from an unsecured creditor to a first-priority secured creditor if the true sale characterisation fails in court.

The backup security interest is typically perfected under Article 9 of the Uniform Commercial Code by filing a UCC-1 financing statement. It should cover not just the royalty payment stream but the underlying intellectual property, regulatory approvals, and product rights. UCC filings expire after five years and must be renewed through a UCC-3 continuation; a lapsed filing renders the security interest unperfected and vulnerable to avoidance by a bankruptcy trustee.

For transactions structured around IP licences, Section 365(n) of the Bankruptcy Code provides a separate layer of protection. When a debtor rejects an executory contract containing an IP licence, the non-debtor licensee can elect to retain its rights and continue using the licensed intellectual property. In exchange, the licensee must continue making all royalty payments due under the contract.

The critical limitation, exposed by the Mallinckrodt ruling, is that Section 365(n) applies only when the underlying transaction is structured as a licence. An outright sale of IP with a retained royalty creates a non-executory contract, and the royalty obligation becomes a dischargeable unsecured claim.

Case Studies: How Insolvency Risk Has Played Out

PhaseBio v. SFJ Pharmaceuticals (2022-2023): The Recharacterisation Battle

PhaseBio's bankruptcy presented a direct test of what happens when a debtor attempts to recharacterise a drug development financing agreement. In 2020, SFJ Pharmaceuticals agreed to fund up to $120 million to advance PhaseBio's Phase III trial for bentracimab. In exchange, SFJ would receive milestone and royalty payments, with a potential five-times return on its investment, plus ownership of the trial data package. Critically, SFJ obtained a perfected first-priority security interest in substantially all of PhaseBio's assets.

When PhaseBio filed for bankruptcy in October 2022, it sought to recharacterise the SFJ agreement as an equity investment, which would have stripped SFJ of its secured creditor status. PhaseBio argued that the pure risk-capital nature of the investment, the five-times return structure, and the fact that SFJ would receive nothing if the product was never approved all supported equity treatment. PhaseBio also described the drug development financing structure as "never-before-tested" in bankruptcy proceedings.

SFJ countered that the agreement was an arm's-length transaction giving SFJ specific contractual rights secured by a perfected lien. The case settled through mediation in December 2022. SFJ received the bentracimab programme and related assets in satisfaction of its $120 million secured claim, plus paid $32.9 million to PhaseBio's estate. A residual royalty of 2.5% on worldwide net sales exceeding $300 million was retained for PhaseBio creditors, but only after SFJ recovers its return thresholds.

The PhaseBio case illustrates two principles. First, the recharacterisation risk is real: debtors will attempt it when the stakes are high enough. Second, a properly perfected security interest, obtained at inception and clearly documented, provides the structural backbone that survives the challenge.

Clearside Biomedical and HealthCare Royalty (2025-2026): SPV Structures Under Stress

Clearside Biomedical's November 2025 Chapter 11 filing presented an unusual dynamic: a bankruptcy with no funded debt. The company had entered into a royalty purchase agreement with HealthCare Royalty Partners in August 2022, selling certain rights to receive royalty and milestone payments related to XIPERE and its SCS Microinjector technology for $32.5 million.

The transaction structure was carefully layered. Clearside created a dedicated royalty subsidiary (Clearside Royalty LLC), transferred the relevant royalty rights to that subsidiary, and the subsidiary sold them to HealthCare Royalty. Clearside also pledged the equity in the royalty subsidiary to secure its obligations. The royalty had a revenue cap of $106.5 million.

The complexity emerged in September 2025, weeks before the bankruptcy filing, when Clearside amended the royalty agreement. An Ad Hoc Group of Equity Holders subsequently alleged that the amendment waived a contingent $12.5 million payment from HealthCare Royalty, nearly five times the stalking horse bid. The equity holders argued that because Clearside had no funded debt, all sale proceeds after administrative expenses should benefit shareholders, and the $2.7 million stalking horse bid severely undervalued assets worth $10.3 to $20.3 million.

The case illustrates that SPV structures, while effective at isolating royalty interests, create their own set of complications. The equity in the royalty subsidiary was itself an asset of the estate, and the right to revenue after the royalty cap was reached represented future value that the estate could claim. Pre-petition amendments to royalty agreements, particularly those occurring in the "zone of insolvency," become flashpoints for fraudulent transfer and fiduciary duty claims.

Acorda Therapeutics (2024): Secured Creditors and Royalty-Bearing Asset Sales

When Acorda Therapeutics filed for Chapter 11 in April 2024, it carried $171 million in convertible senior secured notes and marketed three commercial products: Inbrija for Parkinson's disease, and Ampyra and Fampyra for multiple sclerosis. The company's assets were sold to Merz Pharmaceuticals for $185 million in a Section 363 sale.

The distribution of proceeds revealed the insolvency hierarchy in practice. Secured creditors recovered approximately 64% on their $171 million in claims. General unsecured creditors received approximately 7% on $11.4 million in claims. The approximately $139 million distributed to secured creditors included repayment of the $20 million DIP facility provided by certain noteholders.

For royalty holders, Acorda illustrates the practical consequence of creditor priority. Fampyra's royalty obligations to Biogen, under which Acorda had licensed dalfampridine, were treated as executory contracts subject to assumption or rejection in the 363 sale process. Merz, as the buyer, acquired the products "free and clear of liens and interests." Any royalty holder without structural protections, without a perfected security interest, without true sale documentation, is at the mercy of whatever recovery rate the unsecured creditor class receives. In Acorda's case, that was seven cents on the dollar.

Gamida Cell (2024): Cross-Border IP Liens Between Israel and the US

Gamida Cell's May 2024 prepackaged bankruptcy added a cross-border dimension that is increasingly relevant for European and Israeli biotech companies. The company, incorporated in Israel with US operations through its subsidiary, had taken a $25 million secured loan from Highbridge Capital under a loan and lien agreement that created liens over substantially all assets of both the Israeli parent and the US subsidiary, including all intellectual property.

The restructuring converted Highbridge's $75 million in unsecured bonds into 100% of the company's equity, while the $25 million secured loan, backed by liens on IP and other assets, was treated as a priority claim. The case required coordination between US bankruptcy proceedings and Israeli corporate law, including Highbridge's guarantee claims against the Israeli parent.

For royalty investors with European or Israeli biotech counterparties, Gamida Cell demonstrates that the lien structure must be valid and enforceable under both the debtor's home jurisdiction and the jurisdiction where the IP is registered or the bankruptcy is filed. A UCC-1 filing that perfects a security interest under New York law does not automatically protect the same interest in Israeli or Swiss insolvency proceedings.

Cross-Border Insolvency: Where the Standard Playbook Breaks Down

The structural protections that work under the US Bankruptcy Code, true sale opinions, UCC security interests, Section 365(n), do not automatically translate to other jurisdictions. For the growing number of royalty transactions involving European counterparties, this creates layers of complexity that are often under-appreciated at the deal structuring stage.

The Swiss Problem

Switzerland is home to a significant concentration of pharmaceutical and biotech companies, and Swiss law treats security interests fundamentally differently from the UCC framework.

Under the Swiss Debt Enforcement and Bankruptcy Act (SchKG), the two most commonly used security interests are pledges (Pfandrechte) and transfers or assignments for security purposes (Sicherungsubereignung und -abtretung). Swiss law does not recognise the concept of a floating charge or a blanket lien. This means that the broad, all-assets security interest routinely obtained in US royalty transactions has no direct equivalent under Swiss law.

For intellectual property specifically, the valid creation of a pledge requires a written pledge agreement. Registration in the relevant registers for patents, trademarks, and designs is not required for valid creation but is required for perfection vis-a-vis third parties. Failing to register means the security interest is not enforceable in an insolvency context, a parallel to the UCC filing requirement but with a different registration system and different procedural mechanics.

The insolvency treatment of pledged assets diverges sharply from the US model. Upon the opening of Swiss bankruptcy proceedings, secured creditors benefitting from a pledge must hand in the collateral to the bankruptcy administration.

They retain priority over the enforcement proceeds but cannot enforce privately, as they typically can in a US Chapter 11 proceeding. This means that a royalty investor with a Swiss pledge on pharmaceutical IP will have its collateral administered by the Swiss bankruptcy office and sold at auction or by mutual agreement, rather than being able to exercise remedies directly.

However, Swiss law provides one structural advantage that does not exist under the US Bankruptcy Code: assets transferred for security purposes (Sicherungsübereignung) rather than pledged do not form part of the bankruptcy estate. They can be subject to private enforcement during ongoing bankruptcy proceedings.

This means that a royalty transaction structured as a security transfer of the relevant IP, rather than a pledge, preserves the buyer's ability to enforce outside the collective insolvency proceeding.

This distinction, between a pledge and a security transfer, has no equivalent in US law and is frequently missed by deal teams accustomed to US-style UCC filings. A US royalty investor acquiring an interest in a product developed by a Swiss biotech must structure the security package under Swiss law principles, not simply replicate the US approach.

Furthermore, Switzerland is not an EU member state. The EU's insolvency regulation and its COMI (Centre of Main Interests) framework do not apply to Swiss debtors. Swiss authorities will not recognise or give effect to foreign main insolvency proceedings opened against a Swiss corporate debtor outside Switzerland.

Foreign insolvency proceedings can be recognised, but only under the restrictive conditions of the Swiss Private International Law Act (Articles 166-175), which requires that Swiss-located assets be used first to satisfy Swiss-located creditors before any remaining balance is remitted to the foreign bankruptcy estate.

For a royalty investor holding an interest in a product developed by a Swiss company with US commercial operations, this creates a genuine structural problem: which jurisdiction's insolvency regime will govern the royalty interest?

If the Swiss company enters Swiss bankruptcy proceedings, Swiss law determines the treatment of the IP and the security interest. If the US subsidiary files for Chapter 11, US law applies to US-located assets but may not reach Swiss-registered patents or Swiss-domiciled royalty payment obligations.

The EU Harmonisation Effort

The European Commission has been working toward harmonisation of insolvency rules across EU member states, driven by the recognition that divergent regimes are a significant obstacle to cross-border investment. In November 2025, the Council and European Parliament reached a provisional agreement on a directive harmonising certain aspects of insolvency law.

The agreement establishes EU-wide rules on avoidance actions (challenging pre-insolvency transactions that reduced creditor value), introduces pre-pack liquidation procedures across all member states, and improves insolvency practitioners' access to beneficial ownership registers.

The pre-pack provision is particularly relevant for royalty transactions: it allows the sale of a debtor's business to be prepared and negotiated before formal insolvency proceedings open, with executory contracts transferring automatically to the buyer without counterparty consent.

For royalty investors, the directive creates both opportunity and risk. Pre-pack procedures may allow royalty-burdened assets to be sold quickly and with greater value preservation. But the automatic transfer of executory contracts could mean that a royalty obligation is assigned to a buyer that the original royalty holder did not evaluate as a credit risk, without the royalty holder's consent.

The English Law Dimension

English law restructuring plans and schemes of arrangement have become increasingly popular vehicles for pharmaceutical company restructurings, in part because they can compromise the claims of dissenting creditor classes in ways that US Chapter 11 cannot. A key feature is the ability to restructure debts governed by English law even when the debtor is incorporated elsewhere, provided the English court has jurisdiction.

For a royalty agreement governed by English law with a debtor incorporated in the Netherlands or Ireland, an English court may assert jurisdiction over the royalty obligation and include it in a restructuring plan. The Gibbs rule, which holds that a debt governed by English law cannot be discharged by foreign insolvency proceedings, creates a potential conflict: a US Chapter 11 discharge or a continental European insolvency proceeding may not, under English law principles, release the debtor from an English-law-governed royalty obligation.

This has direct implications for deal structuring. A royalty agreement governed by English law provides the royalty holder with the protection of the Gibbs rule, but it also means the royalty could be compromised through an English restructuring plan. A royalty agreement governed by New York law avoids the English restructuring risk but loses the Gibbs protection. The choice of governing law in a cross-border royalty transaction is therefore not a boilerplate decision but a substantive allocation of insolvency risk.

The UNCITRAL Model Law Gap

Approximately 50 countries have adopted some version of the UNCITRAL Model Law on Cross-Border Insolvency, including the US (through Chapter 15) and the UK. Notable absentees include most continental European jurisdictions (which rely instead on the EU insolvency regulation) and Switzerland. The Model Law provides a framework for recognising foreign insolvency proceedings and coordinating cross-border cases, but it does not harmonise substantive insolvency rules.

For pharmaceutical royalty transactions, the Model Law gap means that a Chapter 15 proceeding in the US can recognise a foreign insolvency and impose the automatic stay on US-located assets, but it cannot change the substantive treatment of the royalty under the foreign jurisdiction's insolvency law. If a Dutch biotech enters Dutch insolvency proceedings and the royalty is governed by New York law, the Chapter 15 court can protect the Dutch estate's US assets but cannot apply Section 365(n) protections that are specific to US bankruptcy law.

The Biotech Insolvency Wave: Scale and Systemic Exposure

The structural concerns examined above are not academic. The biotechnology sector's insolvency rate has been running at historically elevated levels for three consecutive years.

In 2023, 28 biotech companies closed or went bust, the highest count since at least 2010. In 2024, 13 companies filed for Chapter 11 protection, with another 16 formally announcing closures in 2025. The drivers are structural: the pandemic-era funding boom created a cohort of public biotech companies that took on more debt financing than had previously been typical. When credit tightened, companies that had not yet achieved profitability found themselves unable to refinance.

The royalty financing market has grown alongside this distress. Gibson Dunn's data shows annual deal volume growing from $5.2 billion in 2020 to $7.1 billion in 2025, with transaction counts stabilising at 25 to 27 deals per year. Among capped synthetic royalties, the median cap is 2.0x, with a range from 1.55x to 4.0x. Tiered rate structures, where the royalty rate declines as product sales scale, are now common.

As more biotechs use royalty financing to extend their cash runways, the pool of royalty-burdened companies that could enter insolvency grows correspondingly. Every structural shortcoming that existed on paper is being exposed in practice. The interaction between the rising stock of outstanding royalty obligations and the elevated rate of biotech insolvencies means that the structural protections described in this article are no longer safeguards for remote contingencies. They are the load-bearing architecture of the asset class.

What to Watch

Three developments will shape the insolvency risk landscape for pharma royalties through 2027 and beyond.

First, the EU insolvency harmonisation directive, agreed in November 2025, will require member state implementation over the coming years. The directive's provisions on avoidance actions, pre-pack procedures, and automatic contract transfers will change how royalty obligations are treated in European restructurings. Royalty investors with exposure to EU-domiciled counterparties should be modelling the impact of these provisions on their existing portfolios.

Second, the continued growth of the royalty market itself creates systemic exposure. With over $32 billion in transactions from 2020 through 2025, the total stock of outstanding royalty obligations is substantial.

A significant downturn in biotech equity markets or a wave of clinical failures could trigger multiple simultaneous insolvencies involving royalty-burdened companies. Whether the structural protections that have been built into recent transactions will perform as intended under stress conditions remains an open question.

Third, the convergence of US and European deal activity is creating a growing number of transactions where the royalty interest spans multiple jurisdictions. A Swiss-incorporated biotech with US-registered patents, EU-approved products, and a royalty obligation governed by New York law presents insolvency risk across at least three legal regimes. The deal teams that structure these transactions must grapple with questions that have no settled answers: which jurisdiction's avoidance rules apply to a pre-insolvency royalty amendment?

Can a Swiss bankruptcy office enforce against US-registered patent rights? Does a Section 365(n) election by a US licensee protect against a concurrent Swiss composition proceeding?

The time to address these questions is at the negotiating table. The answers, as PhaseBio, Clearside, Acorda, and Gamida Cell have demonstrated, will be determined by how the transaction was structured years or decades before the insolvency occurs.

All information in this report was accurate as of the research date and is derived from publicly available sources including company press releases, SEC filings, court decisions, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.