Latin America's Pharmaceutical Royalty Market: The Overlooked Frontier

The conversation about emerging markets in pharmaceutical royalties runs a predictable circuit. China dominates the headlines, Korea is gaining ground, Japan is attracting renewed institutional attention following the analysis in our recent piece on the Japanese market, and Europe — from Basel to Berlin — has been reliably generating mid-market transactions for the better part of a decade. Latin America barely registers in that conversation.

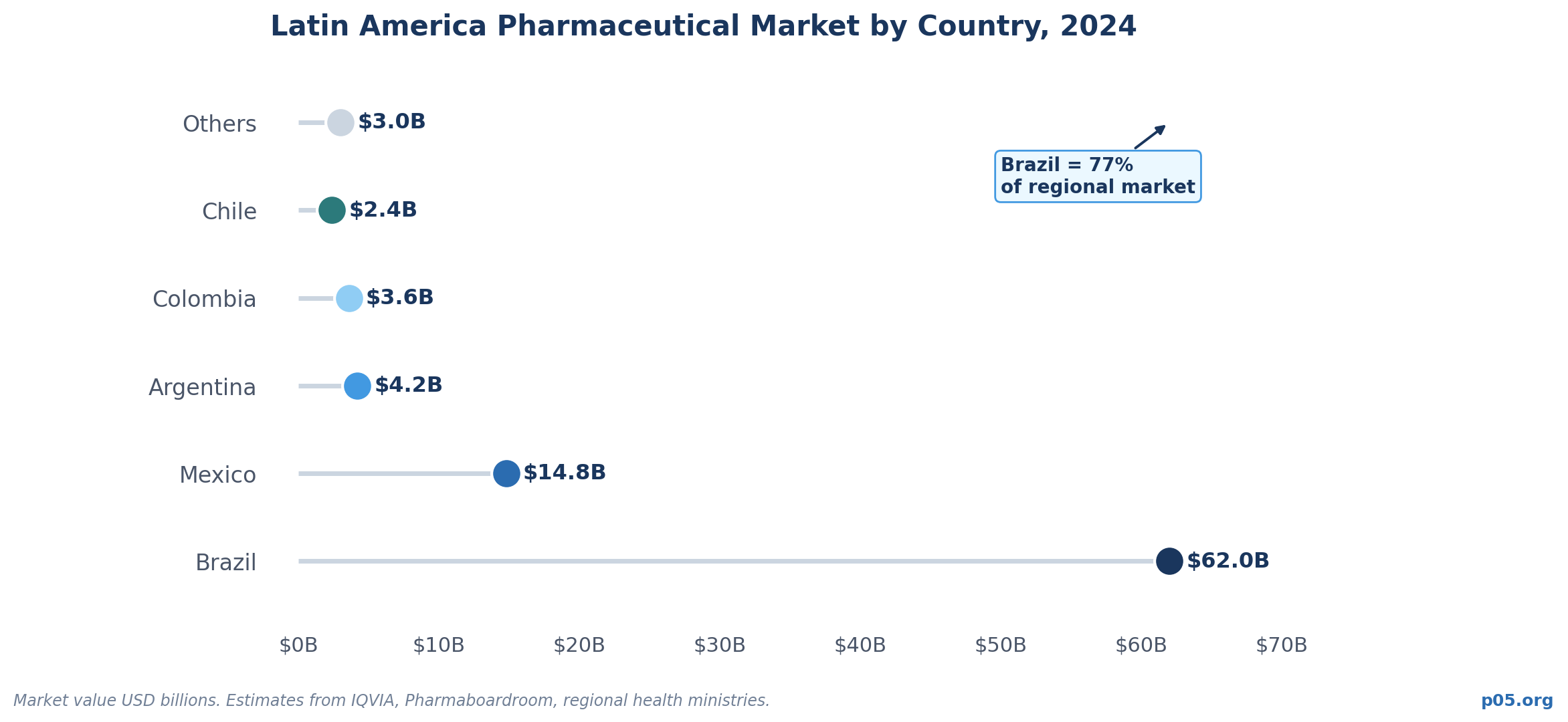

That absence is worth examining. The region has a pharmaceutical market that reached $80+ billion in aggregate value in 2024, with Brazil alone accounting for $62 billion of that figure.

It has a manufacturing base that supplies biosimilars to multiple continents, a clinical trials infrastructure that has attracted every major multinational, a scientific tradition — in Argentina, Brazil, and Cuba particularly — that goes back decades, and now has two OECD member states in Colombia and Chile that are actively reshaping their pricing frameworks. It also has almost no track record of pharmaceutical royalty financing transactions of the kind that Western royalty investors deploy capital into.

The question is whether that absence reflects a genuine structural barrier, or something simpler: that Western royalty capital has not yet made the investment in relationships, regulatory understanding, and deal architecture required to access a market it has largely ignored.

There is a case that it reflects the latter. The implications for investors willing to do that work are significant.

Understanding the Latin American Pharmaceutical Landscape

Before assessing the royalty opportunity, it is worth being precise about what Latin America's pharmaceutical sector actually is — because the common perception, that the region is primarily a market for multinational products rather than a source of innovation, needs significant qualification.

Brazil is by far the largest domestic market, representing roughly 79% of total regional biological product sales, followed by Mexico with 17%. Together they anchor an ecosystem that is urbanizing rapidly, aging structurally, and generating demand for innovative therapies that public health systems are increasingly unable to meet from domestic production alone. Brazil's $62 billion pharmaceutical market in 2024 makes it the largest in Latin America by a wide margin and one of the ten largest globally — comparable in scale to the Spanish or Canadian markets.

But the market is also fragmented and structurally complex in ways that create friction for royalty investors specifically. More than 60% of pharmaceutical products in Latin America are subject to direct price controls, with Brazil, Argentina, and Mexico enforcing mandatory price caps on essential medicines. Generic medicines accounted for over 60% of total pharmaceutical prescriptions across the region in 2023. The biosimilars market — the fastest-growing segment, projected to expand at a CAGR of 11.4% through 2033 — is built primarily around copying and localizing products developed elsewhere, not originating them.

This is the structural reality that explains the royalty financing gap. The typical royalty transaction in the biopharma context requires a company that has originated genuinely novel IP, typically through a proprietary clinical development program, and holds a royalty-eligible asset with revenue-generating potential in major markets. Latin American companies have largely been on the receiving end of those transactions, not the originating end. They are the counterparties that European and Chinese companies license to, not the originators who license from.

That framing is accurate as a general description. But it misses the exceptions — and the exceptions matter as both precedent and signal about where the market is heading.

The Pricing Architecture: Why Latin American Revenues Are Hard to Model

The price control environment in Latin America is more complex than a simple summary makes it sound, and it matters directly for royalty investors because royalty payments are calculated on net sales. Compressed or unpredictable net sales trajectories degrade the expected value of any royalty stream.

Brazil's pricing system operates through CMED, the Drugs Market Regulation Chamber, which administers a ceiling price methodology for all drugs sold commercially. Brazil also channels cost-effectiveness evidence through CONITEC, the National Committee for Health Technology Incorporation, for innovative new drugs seeking reimbursement via the public health system.

The 2021 Supreme Court ruling striking down Article 40 of the Industrial Property Law — which had provided automatic patent term extensions — had retroactive effects triggering a patent cliff for hundreds of molecules between 2021 and 2025. As of 2026, the secondary effect is playing out: patents that would have benefited from Article 40 are expiring at their standard 20-year mark, pulling forward generic entry on drugs filed in the mid-2000s.

Brazil's patent litigation environment has become notably more contentious as a result. Originators stripped of automatic extensions have pivoted to patent term adjustment (PTA) litigation, arguing that administrative delays at INPI constitute TRIPS violations warranting judicial remedy.

Brazil's antitrust authority CADE has simultaneously opened investigations into "sham litigation," classifying the filing of excessive divisional applications as an abuse of dominant position. INPI's Ordinance 04/2025, formalized in May 2025, explicitly bans voluntary divisional applications during the appeal phase unless they directly respond to an examiner-raised unity of invention objection.

Advocacy organization ABIA filed pre-grant oppositions against pembrolizumab applications in 2025, and successfully blocked patent extensions on islatravir and the BPaL tuberculosis regimen in 2024.

For a royalty investor, this environment has a specific implication: a royalty stream tied to Brazilian drug revenues carries patent life risk that is materially harder to model than the equivalent stream in the US or Europe. Generic entry can be accelerated by INPI decisions, advocacy interventions, or CADE antitrust actions — all independent of clinical performance or commercial trajectory. The discount rate applied to Brazilian domestic royalties must incorporate this legal uncertainty as a structural feature, not an idiosyncratic risk.

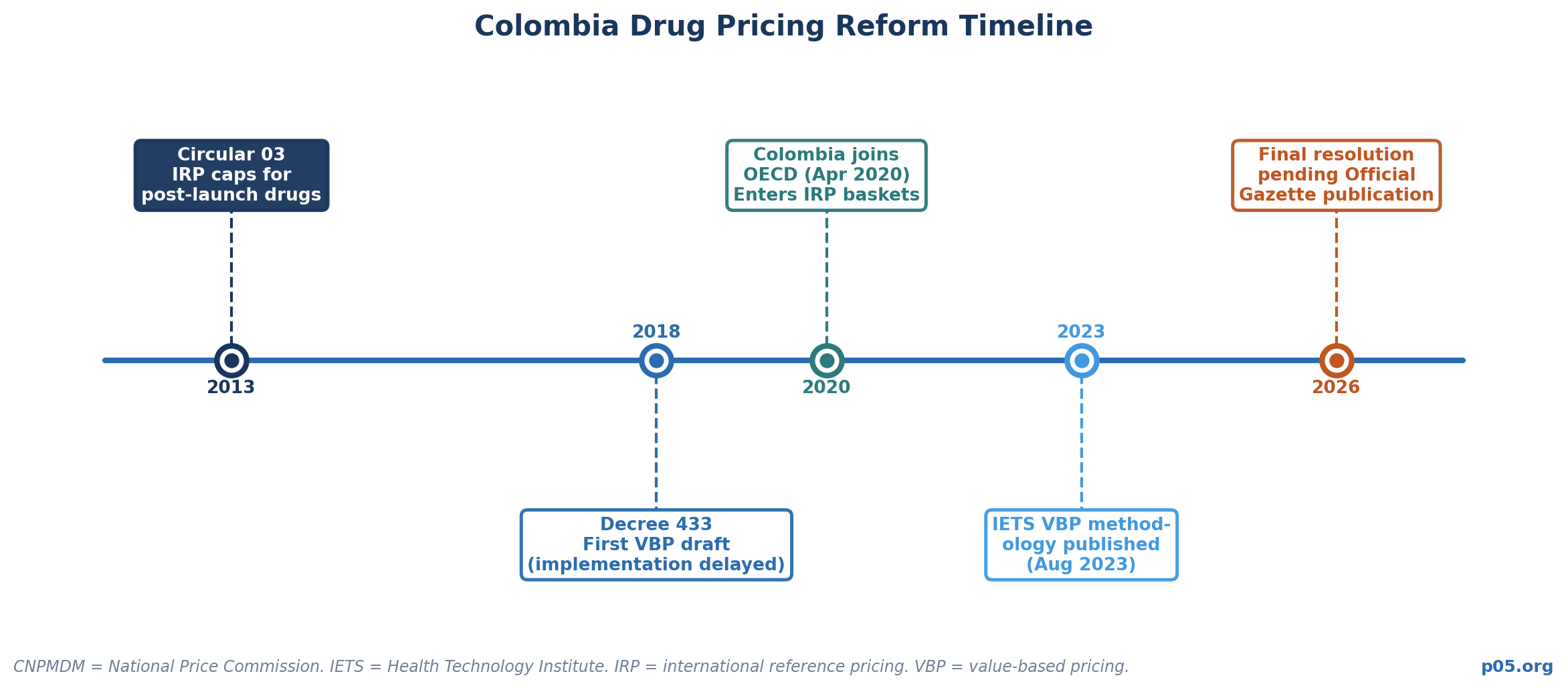

Colombia: The OECD Effect and the Value-Based Pricing Reform. Colombia joined the OECD in April 2020, making it the first Latin American country other than Chile to achieve membership. That status has direct consequences for pharmaceutical pricing: Colombia now appears in the reference baskets used by multiple other countries' international reference pricing (IRP) mechanisms.

What Colombia pays for a drug influences what other countries in the region will pay for the same drug — a dynamic that makes Colombian pricing decisions matter well beyond their domestic market implications.

Within Colombia, the National Price Commission (CNPMDM) has operated an IRP mechanism since its May 2013 Circular 03, using a reference basket drawn from 16 countries selected based on geographic proximity, price regulation policy, OECD membership, macroeconomic stability, and data availability. The more consequential development is Colombia's value-based pricing reform, whose methodological framework was published by IETS in August 2023.

Modeled closely on Germany's AMNOG process, with IETS working directly with Germany's IQWiG institute to develop its methodology, the reform requires new patented drugs to be evaluated by IETS before launch, with a therapeutic value classification driving the maximum allowable price. The IRP basket used in the new VBP model notably swaps Germany for the lower-priced Italy and Greece, compressing the reference price used to calculate Colombia's ceiling.

As of April 2026, the final resolution implementing VBP has not yet been published in the Colombian Official Gazette — it takes effect one year after that publication — meaning the system is not yet fully operational. But it represents the clearest direction of travel in the region toward European-style HTA-gated pricing.

Mexico: USMCA Pressure and the Enforcement Gap. Mexico's pharmaceutical IP framework is the most sophisticated in Latin America on paper, with patent linkage introduced in 2003 and IP law modernized in 2020 under USMCA obligations. But implementation gaps persist.

The US Trade Representative placed Mexico on its Priority Watch List in April 2025 due to persistent deficiencies in pharmaceutical IP enforcement — specifically around patent term adjustments, regulatory data protection implementing regulations, and the patent linkage system's failure to include pre-commercialization notifications and systematic coverage of second-use patents.

As of the 2026 USMCA sunset review, Mexico's missed implementation deadlines are a live flashpoint.

The IP Problem: Why Royalty Origination Has Been Structurally Difficult

The single most important structural barrier to pharmaceutical royalty financing origination in Latin America is the intellectual property environment. Royalty investors — whether buying traditional royalty streams or constructing synthetic royalties against future revenues — are buying claims against cash flows secured by IP.

If the IP is weak, inconsistently enforced, or subject to political override, the underlying security for the investment degrades.

The mechanisms that enable royalty security elsewhere — reliable patent terms, data exclusivity for innovative drugs, patent linkage systems that block generic entry during litigation — are partially implemented or inconsistently enforced across most Latin American jurisdictions.

Argentina operates without a formal patent linkage system. Its approach to data exclusivity is less stringent than most comparator markets. Decree 1741/2025 is specifically designed to promote local biosimilar manufacturing — a public health and industrial policy goal that is explicitly in tension with IP protection for originators.

Brazil's Article 40 ruling and the subsequent PTA litigation wave create a patent landscape where exclusivity periods are actively contested in court. Mexico's linkage system lacks pre-commercialization notifications and faces USMCA scrutiny.

For a royalty investor building a model on Latin American pharmaceutical revenues, this environment has direct consequences. The discount rate applied to a stream backed by domestic Latin American patents needs to reflect not only commercial risk but legal risk — the possibility that generic entry occurs earlier than expected because patent protection fails when tested in litigation, advocacy challenges, or antitrust proceedings.

This is a modelling problem, not an insurmountable one. But it requires analytical investment that most Western royalty shops have not made.

The Exceptions: Where Latin American Royalty Flows Have Actually Existed

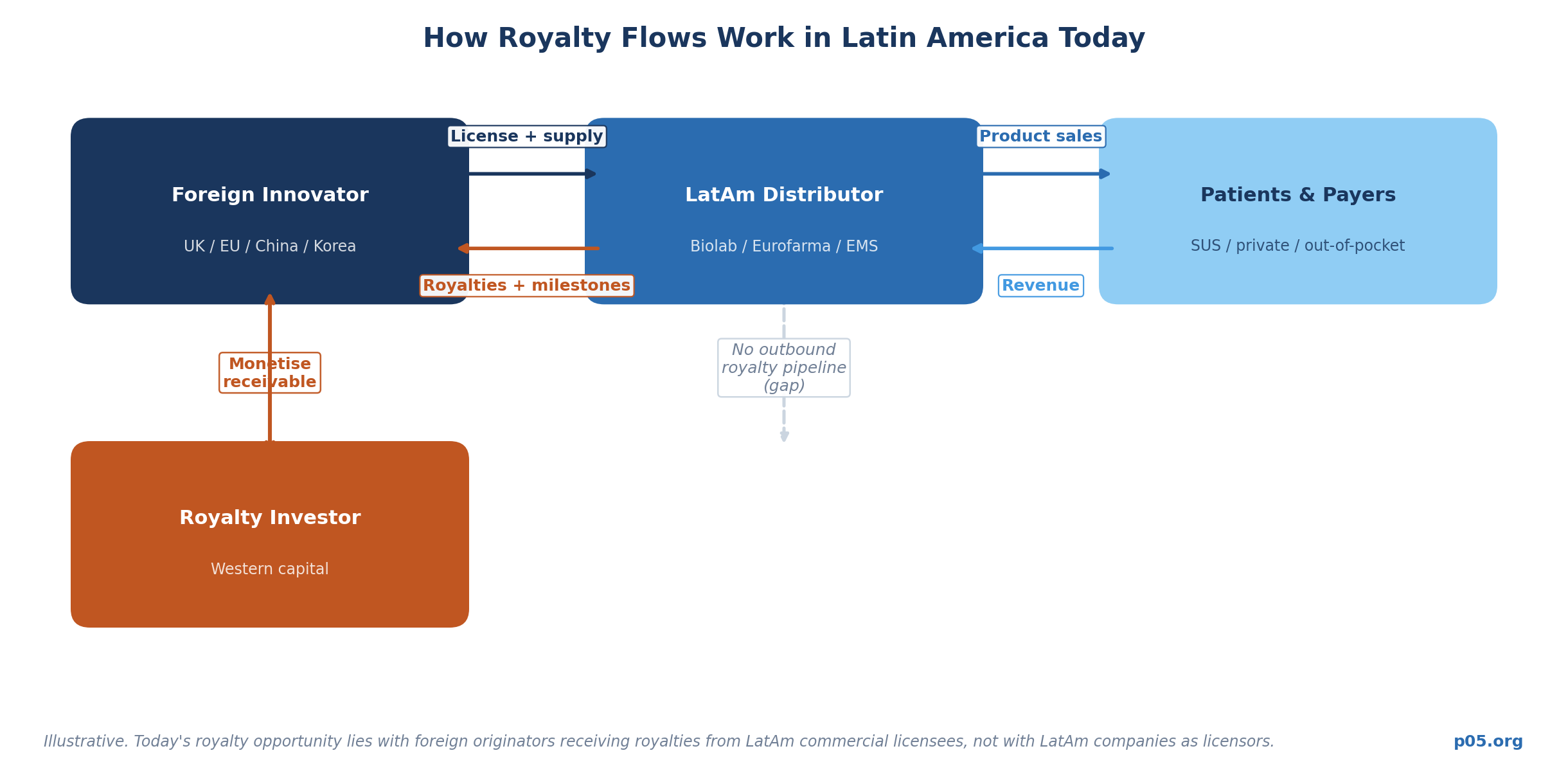

The near-total absence of Latin American companies in Western royalty market databases does not mean the region has generated no royalty-eligible IP. It means the structures and counterparties have been different from those that Western royalty investors typically engage with.

Cuba: Innovation Without Access to Capital Markets. Cuba is the most paradoxical case in the region. Since the early 1980s, the Cuban government made a strategic decision to invest heavily in biotechnology, building the Western Havana Scientific Pole — 38 integrated research and production centers — into a genuine scientific cluster that has produced first-in-class innovations by any standard.

The achievements are real. Cuba developed the world's first meningitis B vaccine, the world's first synthetic vaccine (Quimi-Hib against Haemophilus influenzae type B, WIPO Gold Medal winner in 2005), and CIMAvax-EGF, a therapeutic lung cancer vaccine approved in Cuba in 2008 and the only Cuban biopharmaceutical product to have received FDA Investigational New Drug status for North American development, through a joint venture with Roswell Park Cancer Institute.

By 2017, the Center of Molecular Immunology had 1,100 employees, 4 manufacturing facilities, 25 pipeline products, and 750 patents abroad.

Cuba's pharmaceutical exports generate an estimated $100-200 million annually — a fraction of what the underlying scientific productivity would suggest is possible. Not a single Cuban pharmaceutical product has yet achieved approval in North America, Europe, or Japan, which together account for roughly 80% of global pharmaceutical sales.

The Finlay Institute's meningitis B vaccine attracted SmithKline Beecham (now GSK), which entered into a marketing agreement while the Finlay Institute retained the patent and control over R&D and production — a structure that, in a different political environment, is a textbook royalty origination scenario. What exists instead are licensing relationships with entities in China, Malaysia, and various countries in South America and Africa, with Cuba receiving revenues channeled back into the Scientific Pole through a state-controlled closed economic cycle.

US sanctions, state ownership structures, and the absence of Western-standard legal infrastructure for royalty contracts make direct investment impractical today. But the scientific productivity underlying royalty markets exists in the region. It has simply been channeled into structures that Western royalty capital cannot access.

Argentina's mAbxience and the Biomanufacturing Precedent. mAbxience, the Argentinian biopharmaceutical company and subsidiary of the Chemo Group, produces monoclonal antibody biosimilars at its facilities near Buenos Aires.

In 2020, mAbxience entered into an agreement with AstraZeneca and the Serum Institute of India to manufacture the active substance for the Oxford-AstraZeneca COVID-19 vaccine for Latin America — a technology transfer and licensed manufacturing arrangement at a scale that placed Argentine biomanufacturing capabilities on the global stage. mAbxience earns contract manufacturing fees rather than royalties on downstream commercial sales. Its products are biosimilars of established molecules, not novel entities carrying proprietary royalty streams.

But the precedent matters: Argentine biomanufacturing companies can execute complex, high-quality biologics programs under international partner oversight, and can serve as counterparties in sophisticated cross-border transactions structured under Western frameworks.

Brazil's PDP Architecture: A Royalty-Adjacent Structure Built by the State. Brazil's Productive Development Partnerships (PDPs) represent an entirely state-designed mechanism that shares structural DNA with royalty financing — but inverts it. The Ministry of Health commits to purchasing a specified share of its biosimilar requirements from domestic producers — companies like BioNovis (a joint venture of União Química, Hypermarcas, EMS, and Aché), Orygen (Eurofarma and Biolab), Libbs, and Cristália — who partner with international companies to receive technology transfer.

Pfizer served as Orygen's international partner for adalimumab and infliximab programs; the Ministry of Health's guaranteed purchase volume provides the economic backstop.

As of 2026, Brazilian companies like BioNovis and Libbs are producing monoclonal antibodies at scale for domestic use. The PDP framework has successfully built industrial capability — BIOLAB established an R&D centre in Ontario, Canada; EMS, Brazil's largest pharmaceutical company, owns a biotech firm in the United States and acquired Serbia's Galenika pharmaceutical laboratory, which now manufactures peptides for its liraglutide injector; Eurofarma operates seven manufacturing facilities across Latin America.

These are not royalty-generating transactions, but they represent the expansion of Brazilian pharmaceutical companies' global operational footprints in ways that will eventually bring them into contact with licensing and royalty deal frameworks that Western investors understand.

The George Medicines / Biolab Deal: A Live Example of the Royalty Flow Direction. In October 2025, George Medicines — a UK-based late-stage cardiometabolic company — announced an exclusive licensing and supply agreement with Biolab Farmacêutica for its GMRx2 single-pill triple combination antihypertensive in Brazil. Under the terms, George Medicines receives an upfront licensing fee, regulatory and commercial milestone payments, and a future recurring revenue stream through a stepped royalty rate on Brazilian sales.

This followed George Medicines' January 2025 agreement with Bausch Health for Canada, Mexico, Colombia and Central America, and its July 2025 agreement with Azurity Pharmaceuticals for the US — three sequential out-licensing deals in which a UK innovator builds royalty receivables by licensing to regional commercial partners.

This transaction is representative of how Latin America's large pharma companies actually interact with the global royalty economy: as licensees taking on commercialization rights and paying royalties to foreign originators, not as originators generating royalty receivables. Biolab is the royalty payer in this structure. George Medicines is the royalty recipient. The irony is pointed: the originator is British, not Brazilian.

Eurofarma as Licensee: The In-Licensing Mirror. In 2022, Eurofarma entered into a license and collaboration agreement with Henlius, the Shanghai-based biopharmaceutical company, covering development, manufacturing, and commercialization of three biosimilars — rituximab, trastuzumab, and bevacizumab — across 16 Latin American countries. Henlius received up to $50.5 million including a $4.5 million upfront payment, and Eurofarma acquired commercial rights across key markets. Henlius receives royalties on Eurofarma's Latin American sales.

This deal pattern — a Chinese or European innovator out-licensing to a Latin American commercial partner in exchange for milestones and royalties — is the dominant structure of innovative product flow into the region. It generates royalty receivables for the foreign innovator, not for the Latin American company.

The Structural Question: Why Latin America Has Not Developed an Outbound Royalty Market

The comparison with China is the most instructive one for understanding why Latin America occupies such a different position in the global royalty landscape.

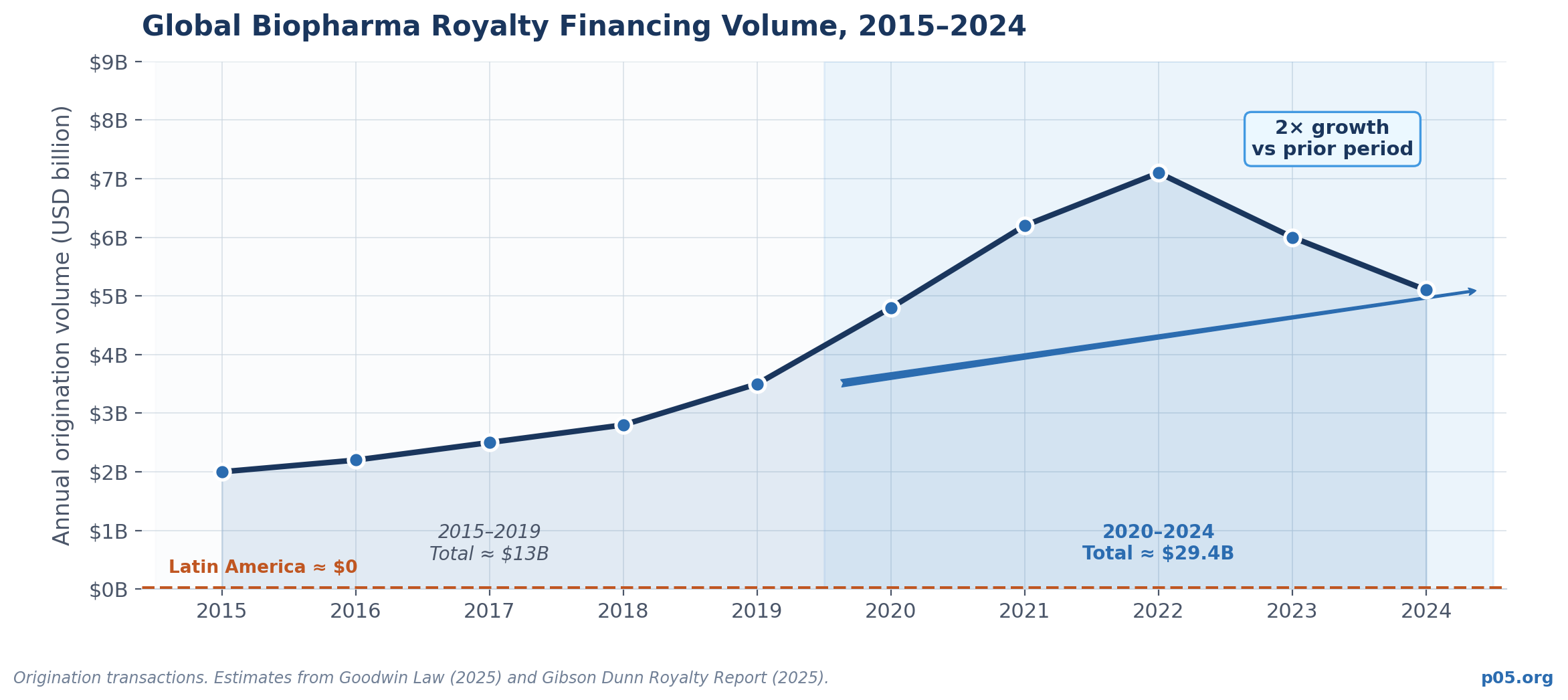

Chinese firms out-licensed 94 projects to overseas companies in 2024 alone, accounting for more than 30% of assets in-licensed by big pharma globally that year. The defining trend of 2024 in global biopharma dealmaking was the increase in in-licensing from China — a reversal of the historical direction of flow in which innovation moved into China, not out of it.

This out-licensing boom was driven by a specific combination of factors: massive domestic capital availability in the 2016-2021 period, government-led R&D prioritization, rapid regulatory modernization at the NMPA, and a generation of returnee scientists who trained in Western research institutions and built companies with globally competitive pipelines.

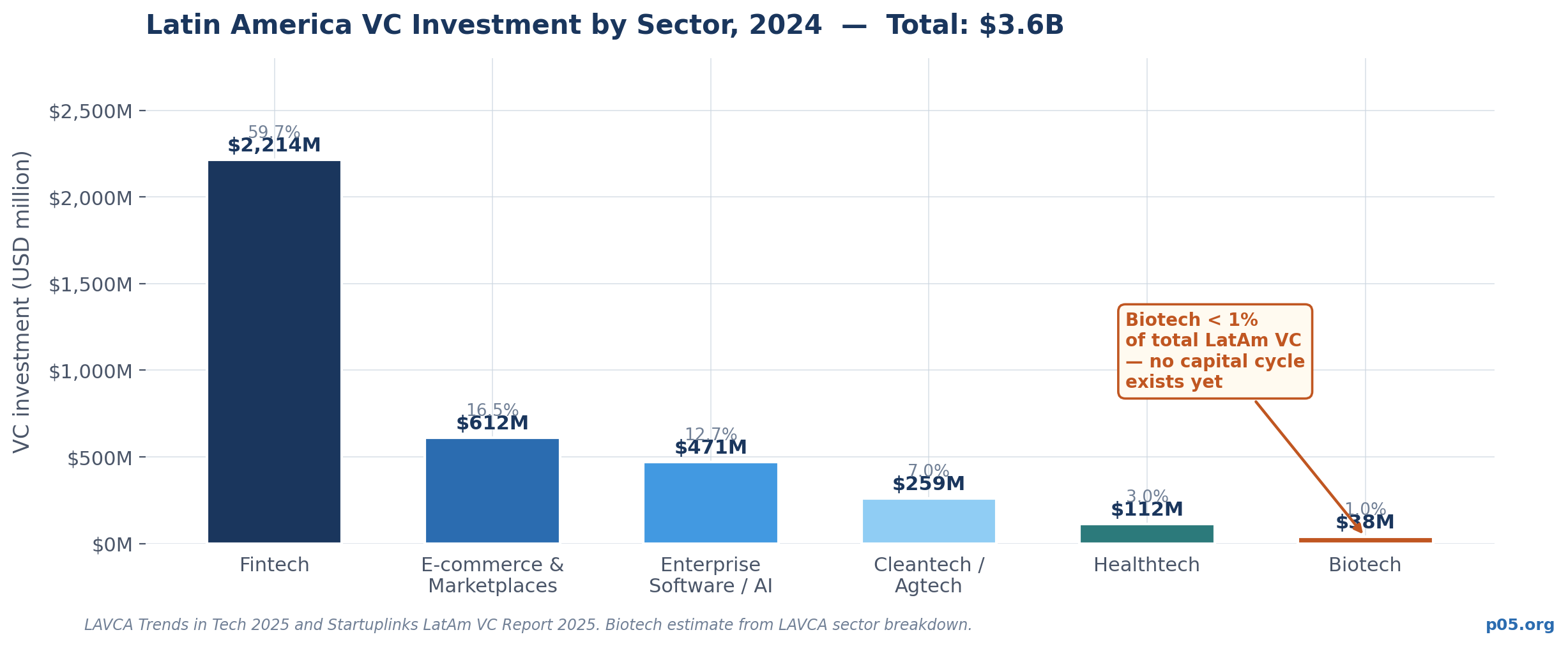

None of those conditions have replicated in Latin America. Total VC investment across all sectors in the region reached $4.1 billion in 2025 — a recovery, but still representing the entire VC ecosystem, not biotech alone. Fintech accounts for more than half of all early-stage capital. Biotech attracts less than 1% of regional VC dollars.

There is no Latin American equivalent of the NASDAQ biotech cycle that funded hundreds of novel drug development programs and built the capital base that Chinese and Korean biotechs subsequently drew from.

The scientific talent pool is present but has not been organized into capitalized platform companies that generate royalty-eligible IP. Brazil's FIOCRUZ — which joined CEPI's network of vaccine manufacturers in July 2024 — combines research, manufacturing, and public health functions at scale.

But it operates as a public institution with a mandate focused on public health access and domestic production, not on generating royalty streams for private capital. Brazil's innovation support infrastructure — Law 14.874/2024 governing clinical research, the GECEIS program, the BNDES CEIS Line, and the Deep Tech FINEP Protocol — is beginning to create stronger institutional foundations, but critical density remains absent.

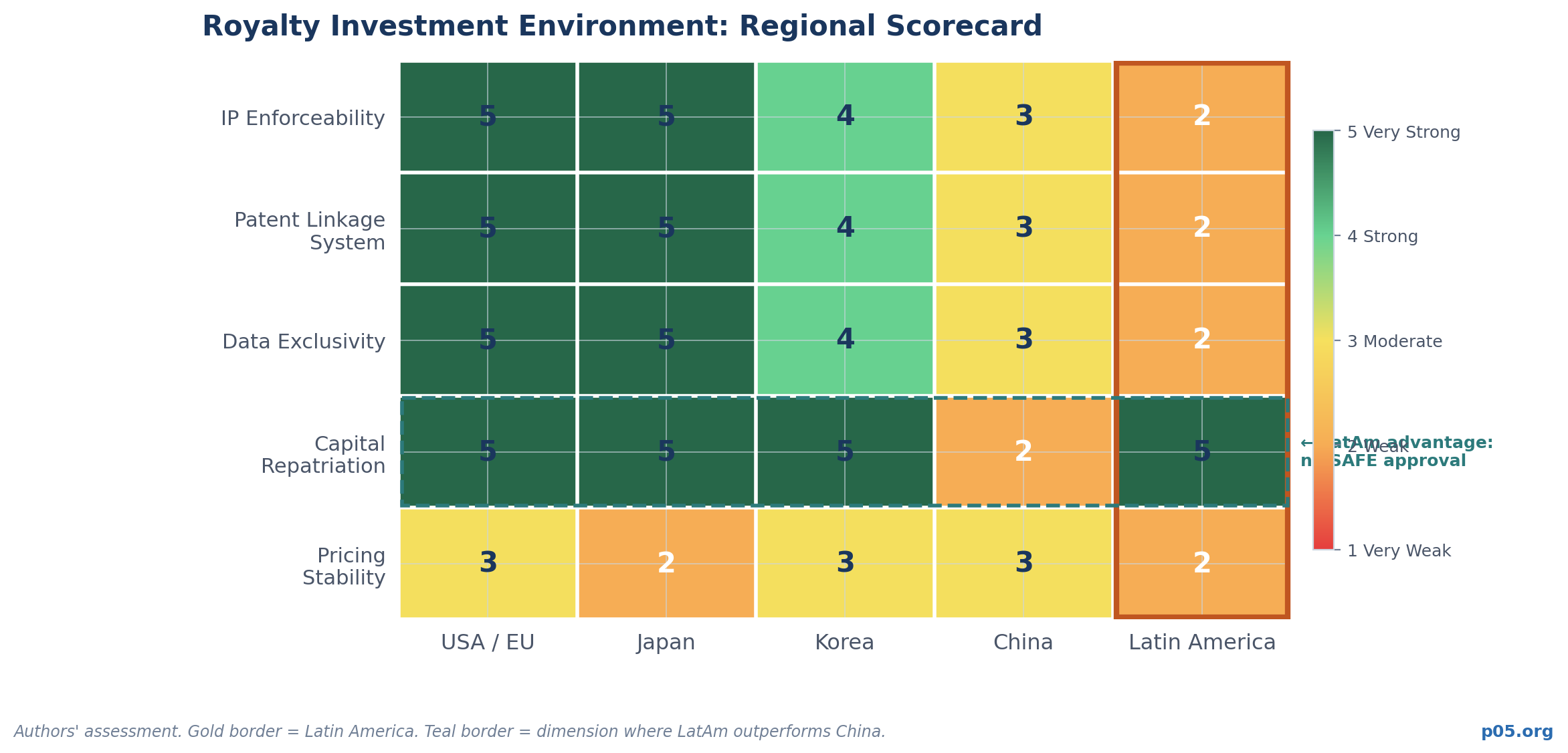

The Comparative Framework: Latin America vs. Other Emerging Markets

The scorecard above is unflattering for Latin America on most dimensions. But the capital repatriation row is genuinely important: unlike China, investing in Latin American royalty structures does not require navigating SAFE approvals or VIE architecture.

Standard Western deal documentation under New York or English law works. The legal framework for enforcing a royalty purchase agreement against a Brazilian or Mexican company is substantially cleaner than the equivalent enforcement question in a China-facing transaction.

That advantage is real. It is not sufficient to offset the weaknesses on IP enforceability, patent linkage, data exclusivity, and pricing stability. But in a future where those weaknesses are progressively addressed through regulatory reform, the combination — legal clarity without capital repatriation friction — becomes a meaningful structural positive.

What Is Actually Happening Right Now: April 2026

Several developments are beginning to shift, at the margins, the conditions that have suppressed Latin American pharmaceutical royalty activity.

The PTA Litigation Wave and Its Investment Implications. Brazil is experiencing a wave of patent term adjustment litigation by originators seeking judicial remedy for INPI administrative delays. This creates a new category of uncertain IP situation: drugs whose patent status is contested in Brazilian courts, with outcomes that will determine whether the originator retains exclusivity or faces immediate generic entry.

For royalty investors considering any transaction touching Brazilian drug revenues, the PTA litigation status of the underlying drug's Brazilian patents is now a first-order diligence item rather than a footnote.

Colombia's VBP Implementation Gap. The Colombian VBP reform published in August 2023 has not yet been formally implemented as of April 2026 — the final resolution has not appeared in the Colombian Official Gazette. This creates a transitional period where the pricing landscape for new patented drugs is in motion. Colombia, as an OECD member, now appears in IRP baskets used by other countries.

A compression of Colombian drug prices following VBP implementation could have ripple effects on royalties computed across multiple Latin American markets that reference Colombian prices.

Mexico's 2026 USMCA Sunset Review. The USMCA sunset review underway in 2026 is scrutinizing Mexico's missed pharmaceutical IP implementation deadlines. This increases the probability of one of two outcomes: either Mexico is pressured into implementing stronger pharmaceutical IP protections (positive for royalty security), or renegotiation pressure introduces new uncertainty into Mexico's IP framework (negative for near-term modelling confidence). The direction is not yet determinable as of April 2026.

Brazilian Companies Going Global. EMS acquired Serbia's Galenika pharmaceutical laboratory, which now manufactures peptides for its liraglutide injector. BIOLAB has an R&D centre in Canada. Eurofarma operates across seven Latin American countries. Companies with international manufacturing and R&D operations eventually develop the licensing and IP management capabilities that generate royalty-eligible assets. This trajectory is early-stage but real.

The George Medicines Template. The October 2025 George Medicines-Biolab licensing agreement, while not itself a royalty monetization in the investment sense, provides a documented data point on how royalty-generating in-licensing structures work in Brazil in 2025-2026: stepped royalty rates on net sales, upfront licensing fees, milestone payments tied to regulatory and commercial triggers, supply agreement from originator to licensee.

This is the documentation template that a royalty investor acquiring such a receivable would be analyzing. The existence of recent, documented transactions of this type in the Brazilian market is a prerequisite for building any origination pipeline.

Where the Opportunity Actually Exists: A Framework

Given the structural constraints outlined above, the Latin American pharmaceutical royalty opportunity is not where most Western investors would instinctively look. It exists in three distinct categories, ordered by proximity to current investability.

Category One: Royalty Receivables Held by Foreign Innovators Licensing Into Latin America. This is the most immediately actionable category. Foreign companies — British, Swiss, Chinese, Korean — are routinely licensing their products into Latin American markets in exchange for stepped royalties on net sales. Those receivables are held by companies whose financials are disclosed in their home jurisdictions, whose IP is validated in major regulatory markets, and whose royalty streams are governed by contracts under Western law. The George Medicines example illustrates the structure precisely.

A royalty investor acquiring a portion of such a receivable buys rights to a percentage of Latin American drug sales, backed by IP validated by the FDA or EMA, governed by a contract under English or New York law, with a Latin American commercial counterparty whose operations are auditable.

Category Two: Latin American Companies Holding International Royalty Receivables from Their Own Global Operations. As Brazilian and Argentine companies expand internationally — acquiring manufacturing assets in Europe, building R&D in North America — they will increasingly hold royalty receivables from international licensing arrangements. The time horizon for this category to produce actionable deal flow is five to ten years, not twelve to eighteen months.

Category Three: Academic Institution IP with Novel Drug Potential. The scientific institutions — FIOCRUZ, CONICET in Argentina, the University of São Paulo — have generated genuinely novel pharmaceutical IP embedded in institutional structures without private development capital. Brazil's Law 14.874/2024, the GECEIS program, and the BNDES CEIS Line are beginning to create the institutional foundations for technology transfer. This category requires the longest time horizon and the deepest relationship investment, but it mirrors the path that made Royalty Pharma possible in the first place.

Conclusion: An Overlooked Market, For Real Reasons

Latin America is not overlooked because royalty investors have missed an obvious opportunity. It is overlooked because the structural conditions that make a pharmaceutical royalty market function — reliable IP, novel drug origination, outbound licensing pipelines, royalty-eligible cash flows — are largely absent, and where they exist in nascent form, they are embedded in institutional structures that Western royalty capital has not built the relationships to access.

That is an honest assessment. It does not mean the market is permanently inaccessible. It means the timelines are longer, the relationship investment is higher, the analytical complexity is greater, and the patience required exceeds what most royalty fund structures accommodate.

The comparison to Japan remains useful. Japan's royalty opportunity rests primarily on a stock of existing ex-Japan royalty receivables — flows on US and European revenues generated by decades of outbound licensing by Ono, Shionogi, Otsuka, and Eisai. Latin America has not yet run that cycle.

The analogue would require a generation of Latin American drug originators to license their novel IP to Western partners, generate royalty receivables, and then have royalty investors offer to monetize those receivables. That generation does not yet exist at scale.

But the scientific capability that would underpin it — in Buenos Aires, in São Paulo, in Havana's Scientific Pole — is real. The question is whether the capital ecosystem and institutional infrastructure that convert scientific capability into royalty-bearing commercial assets can be built, and on what timeline.

For investors with the appetite to ask that question seriously, Latin America may be the most interesting long-duration opportunity in the global pharmaceutical royalty market. For those without that appetite, it will remain what it has always been: a footnote in the deal survey data, present in no transaction databases, absent from every deal roundup.

That absence is, in itself, the most important thing it tells you.

All information in this article was accurate as of the research date (April 2026) and is derived from publicly available sources including company press releases, regulatory publications, academic studies, legal analyses, and financial reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. I am not a lawyer or financial adviser.

Member discussion