Medical Device Royalty Financing: Deal Mechanics, Structural Precedent, and Royalty-Readiness Thresholds

Pure medical device royalty monetization remains a small segment of the life sciences non-dilutive capital market. Of Gibson Dunn's reported $6.5 billion in aggregate 2025 royalty financing, the device share is statistically rounding error — and Q1 2026 continued the pattern. Three transactions closed in January 2026 that should be read as the working template for commercial-stage medtech non-dilutive capital: AVITA Medical's Perceptive-led refinancing, CVRx's Innovatus term loan amendment, and the Perimeter Solutions / MMT senior-secured-notes-financed acquisition. None is a synthetic royalty.

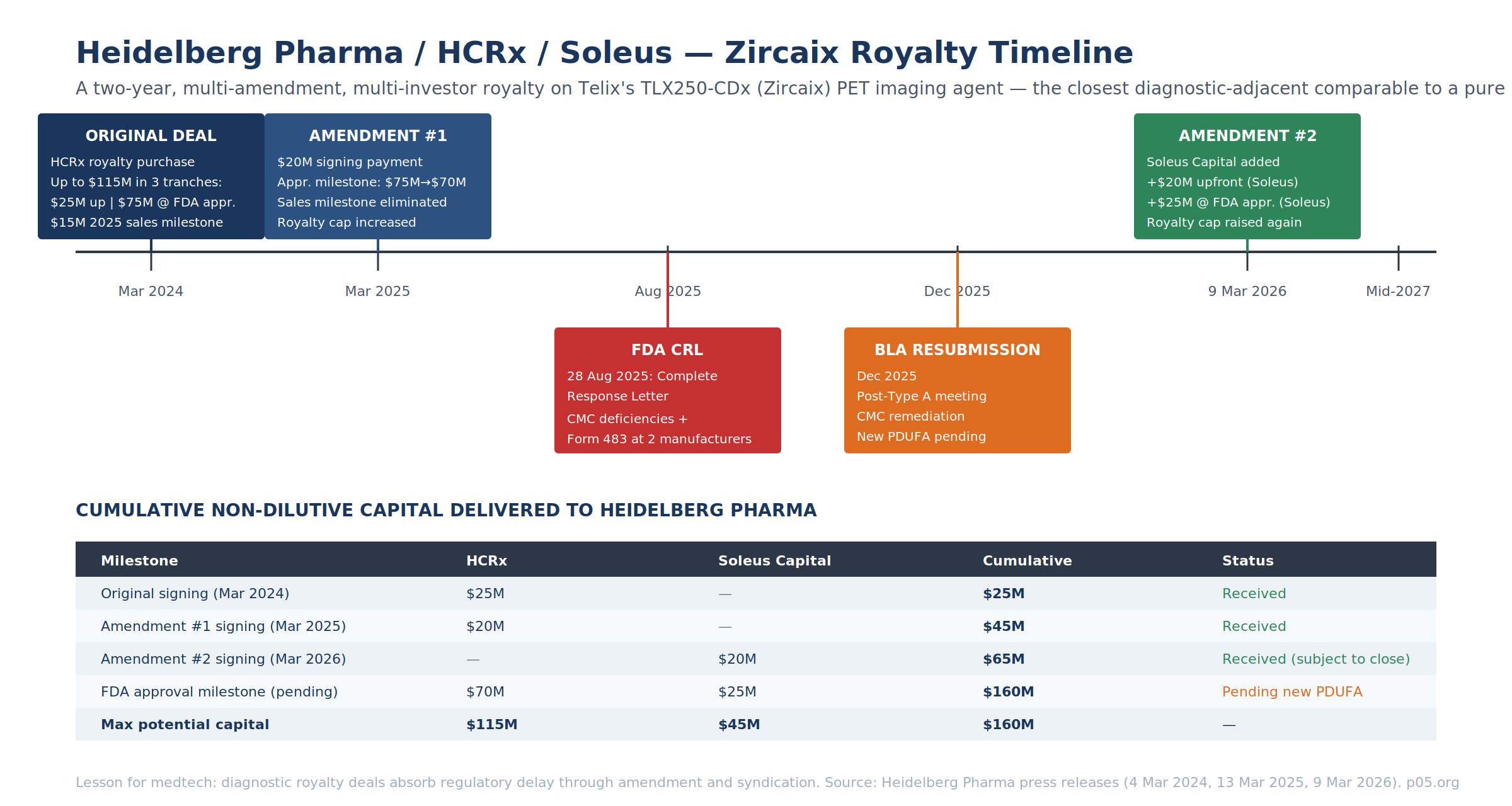

The single Q1 2026 royalty-space transaction adjacent to medtech was the March amendment to the Heidelberg Pharma / HCRx agreement on Zircaix (TLX250-CDx), bringing Soleus Capital in as a second royalty investor.

This piece covers the Q1 2026 deal mechanics at SEC-filing granularity, then constructs the contractual template a pure medical device royalty would need to look like based on mid-market biopharma precedent, and closes with threshold-level royalty-readiness criteria for medtech startups and scaleups. It is a follow-up to Indication-Specific Royalties in Pharma and Medtech, Revolving Credit Facilities in Pharmaceutical Financing, Patent Life and Loss of Exclusivity: Modeling the Royalty Cliff, and When Does the Money Stop? Modelling Royalty Stream Expiry.

Q1 2026 Deal Anatomy: SEC Filing Detail

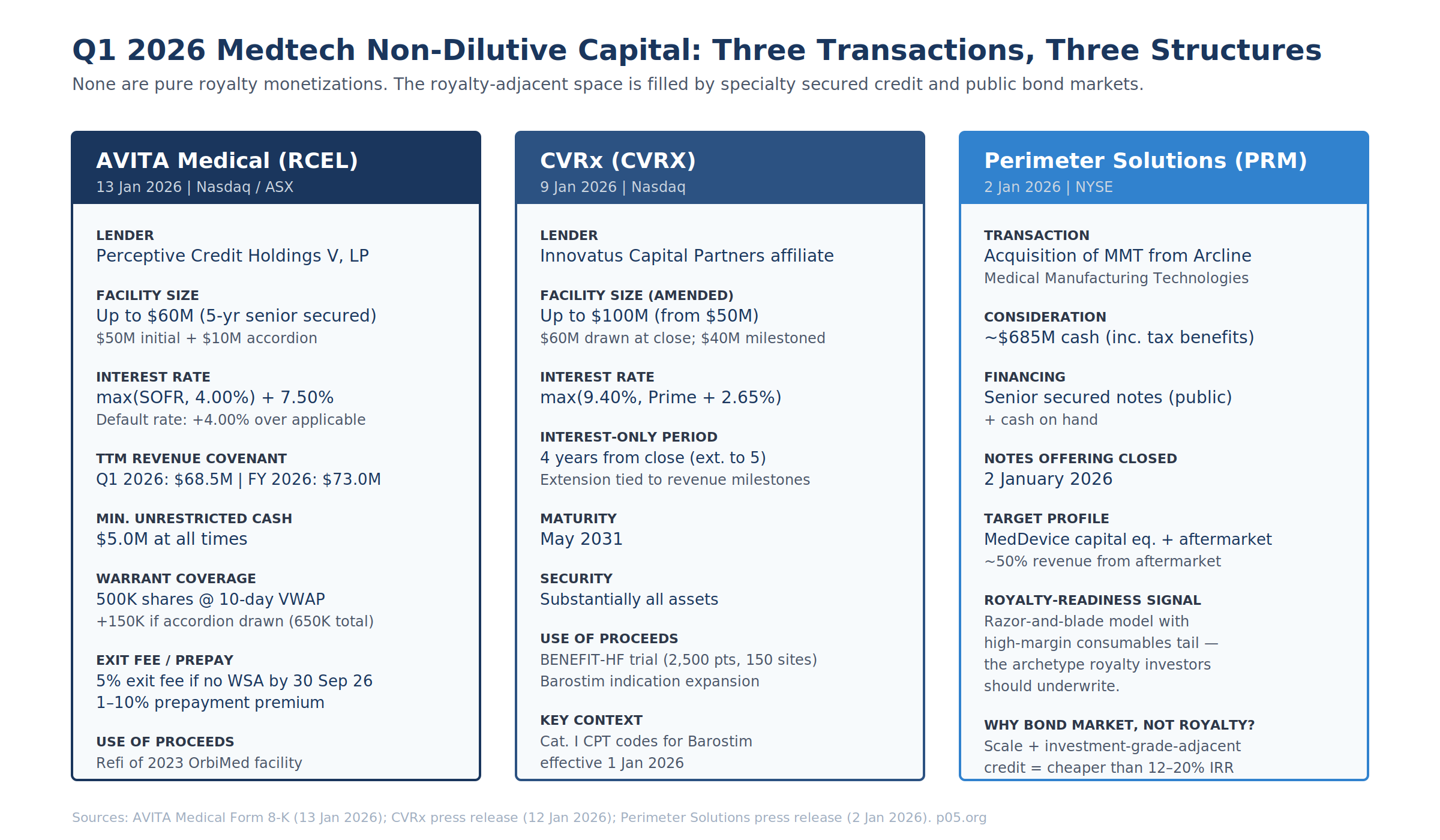

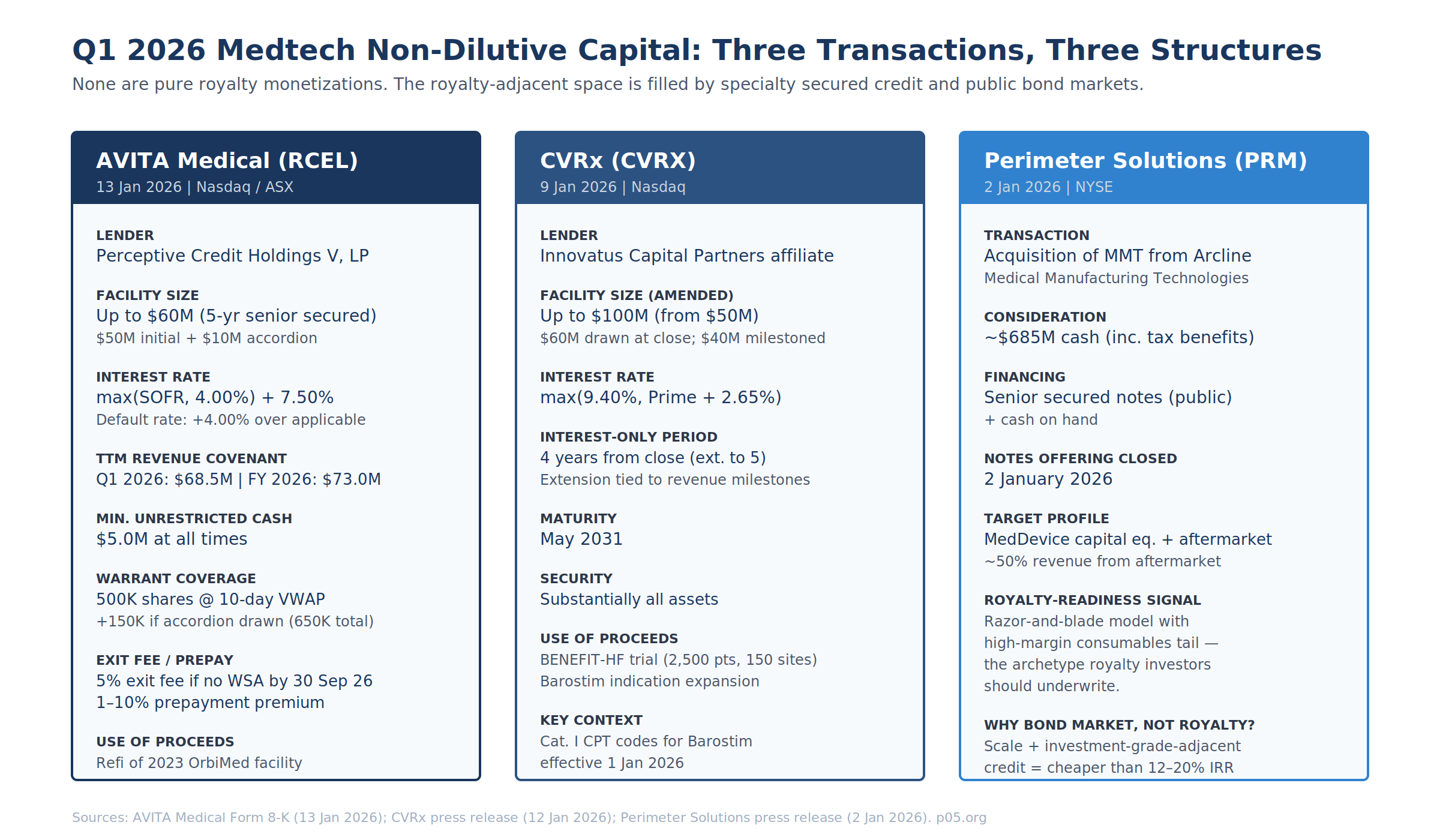

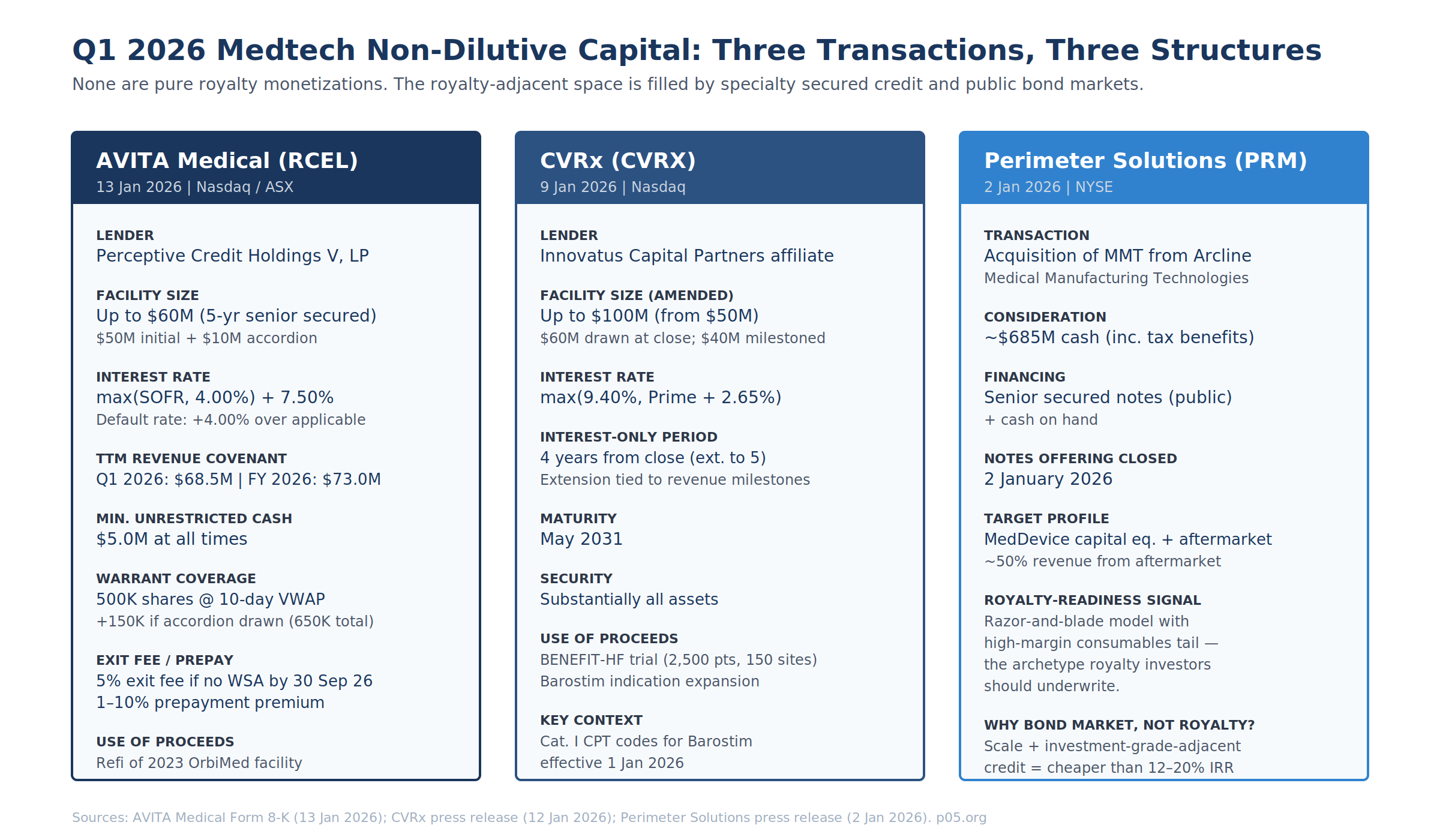

AVITA Medical / Perceptive Credit Holdings V — Form 8-K, 13 January 2026

The AVITA 8-K discloses a Credit Agreement and Guaranty and a Security Agreement with Perceptive Credit Holdings V, LP, governing a five-year senior secured credit facility of up to $60M. Initial commitment $50M drawn at close; additional $10M accordion exercisable by 31 March 2027 subject to a net revenue test.

| Economic Term | Value / Mechanic |

|---|---|

| Interest rate | max(SOFR, 4.00%) + 7.50% per annum, cash-pay |

| Default rate | Applicable rate + 4.00% |

| Exit fee (conditional) | 5% of aggregate principal borrowed if Warrant Shareholder Approval (WSA) not obtained by 30 Sep 2026 |

| Prepayment premium | 1% to 10% of amount prepaid (voluntary or mandatory, incl. on acceleration) |

| Financial maintenance covenant | Specified minimum TTM net revenue per fiscal quarter: $68.5M (Q1 26), $73.0M (FY 26) |

| Minimum liquidity | $5.0M unrestricted cash held by Obligors at all times |

| Security | Substantially all assets of Company and Avita Medical Americas, LLC (Guarantor) |

| Event of default (extra) | Failure to obtain WSA by 30 Nov 2026 is itself an EoD |

The warrant is the instrument that converts AVITA from a pure debt transaction into a revenue-interest-adjacent structure. Perceptive receives a 10-year warrant for 500,000 shares of common stock (an additional 150,000 vesting if the accordion is drawn, bringing the total to 650,000). The exercise price is the lower of (i) the 10-day VWAP ending the business day immediately prior to closing, and (ii) the 10-day VWAP ending the business day immediately prior to warrant issuance. Customary weighted-average anti-dilution. Registration rights require the Company to file a resale registration statement within 30 days of warrant issuance.

Two details worth flagging for practitioners:

- The WSA condition is an Australian Securities Exchange Listing Rules requirement (AVITA dual-listed on ASX as AVH). The 30 Sep 2026 / 30 Nov 2026 bifurcation creates an engineered governance-pressure mechanism — miss the first date, pay a 5% exit fee on the entire drawn balance; miss the second, trigger an EoD.

- The SOFR floor of 4.00% is a meaningful pricing feature in the current rate environment. At the disclosed Term SOFR of ~4.32% (Jan 2026), the floor is near-binding. If SOFR drifts below 4.00% during the 5-year term, Perceptive captures the spread.

The refinancing terminated the October 2023 OrbiMed facility. OrbiMed and AVITA had executed a Fifth Amendment and Waiver on 30 September 2025 adjusting principal-payment triggers after revenue underperformance relative to the original covenants. Per the August 2025 8-K on the OrbiMed Fifth Amendment, TTM covenants had been stepped down to $73M (Q3 25), $77M (Q4 25), $90M (Q1 26), $103M (Q2 26), then $115M thereafter. The Perceptive refinancing re-set Q1 26 from $90M to $68.5M — a 24% reduction on the covenant threshold, reflecting both the lender change and the revised 2026 revenue guidance of $80–85M against 2025 actuals of $71.6M.

CVRx / Innovatus Capital Partners — Amendment, 9 January 2026

CVRx's 12 January 2026 press release discloses an amendment to its term loan agreement with an Innovatus Capital Partners affiliate:

| Term | Pre-Amendment | Post-Amendment |

|---|---|---|

| Aggregate commitment | Up to $50M | Up to $100M (conditional on milestones) |

| Drawn | $50M | $60M at closing |

| Interest rate | Prior rate | max(9.40%, Prime + 2.65%) |

| Interest-only period | Prior IO period | 4 years from close, extendable to 5 on revenue milestone achievement |

| Maturity | Prior maturity | May 2031 |

| Security | Substantially all assets | Substantially all assets (unchanged) |

The Innovatus facility is explicitly scaled to fund BENEFIT-HF — CVRx's 2,500-patient randomized controlled trial across ~150 sites in the U.S. and Germany, evaluating Barostim in an expanded heart-failure population. FDA granted IDE in November 2025; enrollment expected Q2 2026. CMS Category B IDE coverage has been approved. New Category I CPT codes for Barostim therapy took effect 1 January 2026.

Absent a pharma-style synthetic royalty market for pure devices, this transaction is doing two jobs that a synthetic royalty would normally do in biopharma:

- Capital for an expansion trial with asymmetric upside — the "successful BENEFIT-HF triples Barostim's addressable population" thesis.

- Milestone tranche structuring — the facility's conditional $40M upsize is effectively a milestone payment, functionally similar to the approval-milestone tranching in the Heidelberg Pharma / HCRx Zircaix deal.

The deal is priced as secured debt, not royalty. At the Jan 2026 Wall Street Journal Prime Rate of ~7.50%, Prime + 2.65% = 10.15% — above the 9.40% floor, meaning the floor was not binding at signing. Compared with AVITA's max(SOFR, 4.00%) + 7.50% ≈ 11.82%, CVRx is pricing ~170bps tighter, consistent with its larger commercial-stage revenue base, longer product history (FDA-approved 2019), and reimbursement-cleared status.

Perimeter Solutions / MMT — Senior Secured Notes, 2 January 2026

Perimeter Solutions (NYSE: PRM) closed its acquisition of Medical Manufacturing Technologies (MMT) from Arcline Investment Management on 2 January 2026 for approximately $685M cash (inclusive of tax benefits). The acquisition was funded via cash on hand and proceeds from a senior secured notes offering that closed 2 January 2026, per the PrivSource transaction record.

This is not a royalty transaction. It is included here because MMT's revenue architecture — engineered machinery for minimally invasive medical device manufacturing plus ~50% of revenue from proprietary aftermarket consumables — is the archetype of a device-adjacent business that royalty investors should want to underwrite. The fact that PRM chose senior secured notes over any royalty structure is a revealed-preference datapoint: at investment-grade-adjacent credit quality with that revenue mix, the public bond coupon beats the 12–20% IRR a royalty fund would demand. Royalty capital for medtech competes not with equity but with the bond market.

The Heidelberg Pharma / HCRx / Soleus Q1 2026 Amendment

The 9 March 2026 Heidelberg Pharma press release announced a second amendment to the March 2024 royalty purchase agreement with HCRx on Telix Pharmaceuticals' TLX250-CDx (Zircaix, 89Zr-DFO-girentuximab) — a PET imaging agent for clear cell renal cell carcinoma. The amendment brings Soleus Capital Management in as a second royalty investor via its Soleus Capital Credit Opportunities Fund I.

| Amendment Term | Value |

|---|---|

| Soleus upfront (signing) | $20M, subject to customary closing conditions |

| Soleus FDA-approval milestone | $25M upon FDA approval of TLX250-CDx |

| HCRx payment structure | Unchanged (already amended in March 2025) |

| Cumulative royalty cap | Increased; exact figure not disclosed |

| Post-cap tail | High single-digit royalty percentage to investors |

| Financing visibility | Secured through mid-2027 |

This is the only 2025–2026 diagnostic-adjacent royalty deal that provides a full public view of how amendment mechanics operate when regulatory timing slips. The lesson for device practitioners is contractual:

- Cap expansion buys amendment flexibility. Each of the 2025 and 2026 amendments increased the cumulative royalty cap — giving investors more back-end upside in exchange for accepting milestone restructuring in the front-end. This is a usable template for any device deal that hits a delay.

- Multi-investor syndication is a mid-deal option. The March 2026 Soleus entry does not displace HCRx — the two royalty payment structures sit in parallel in the same agreement. For medtech companies with a $100M+ capital need, the template is HCRx-anchor + mid-market co-investor rather than forcing a single investor to bear the whole check.

- Royalty tail structure preserves sponsor optionality. Post-cap, payments revert to Heidelberg Pharma subject to a high-single-digit tail — this is Brulotte-compliant (the structure is not patent-royalty-linked; see Patent Life and Loss of Exclusivity) and preserves meaningful long-tail upside to the sponsor once the investor IRR is satisfied.

On the underlying asset: Telix received an FDA Complete Response Letter on 28 August 2025 citing Chemistry, Manufacturing, and Controls deficiencies and Form 483 notices issued to two third-party manufacturing partners. BLA resubmission was filed in December 2025 following a Type A meeting. The Soleus participation is priced against a product with no PDUFA date currently set — which is why the $25M Soleus approval milestone carries such a meaningful risk premium over the $20M signing payment.

Anatomy of a Pure Medical Device Synthetic Royalty

A pure device royalty deal would need to engineer four structural elements that a pharma royalty inherits from the underlying product economics.

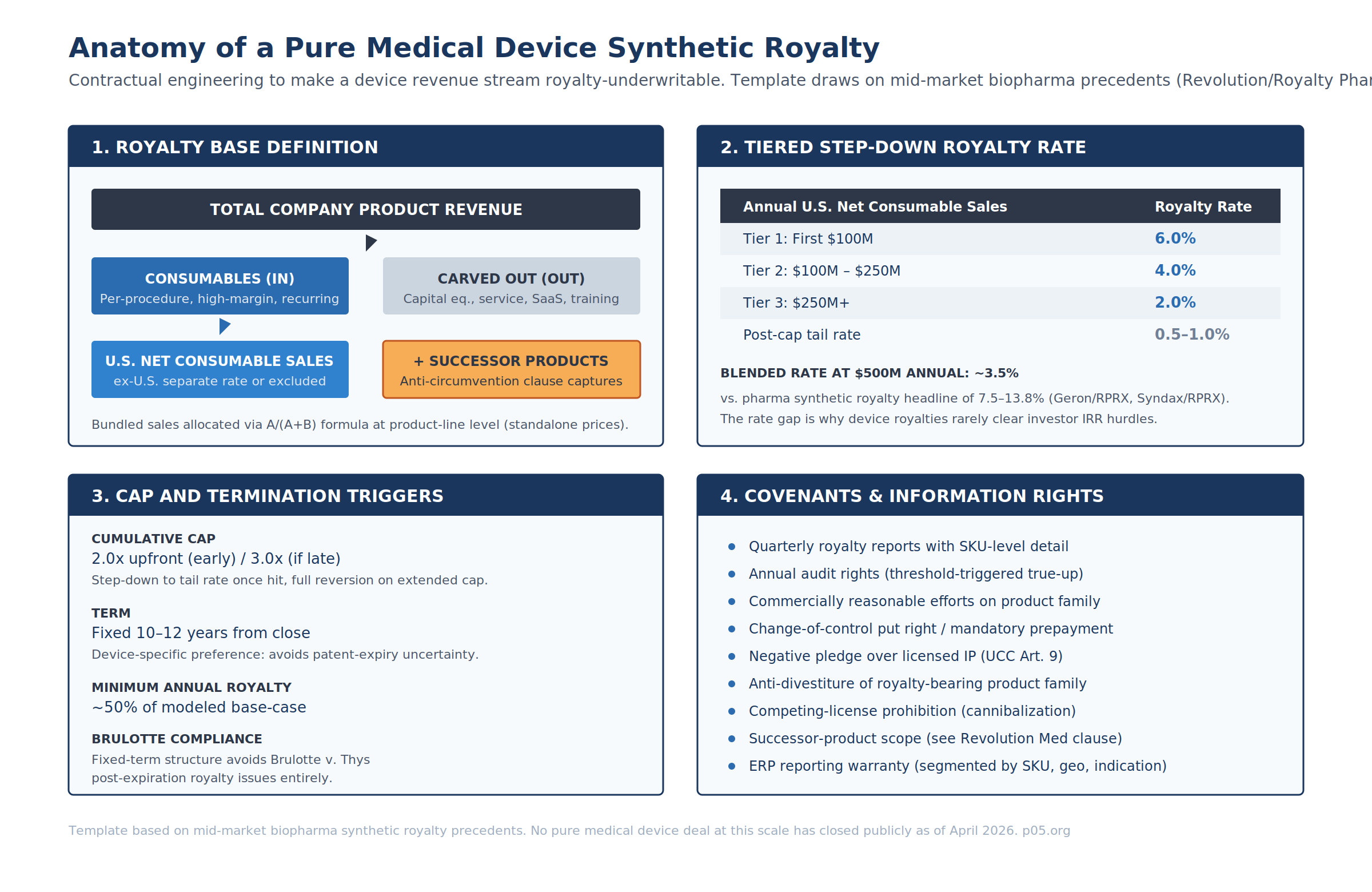

Royalty Base Definition

Pharma royalties use "net sales" of a defined product as the base, with standard deductions. Device royalties require substantially more granularity because revenue composition is mixed.

| Revenue Category | Royalty Base Treatment | Drafting Rationale |

|---|---|---|

| Capital equipment / console | Excluded | Lumpy, hospital capital-budget-dependent, often break-even |

| Proprietary single-use consumables | Included (primary base) | Per-procedure, high-margin, recurring |

| Service / maintenance contracts | Excluded or ring-fenced | Recurring but margin structure differs |

| Software / SaaS | Excluded or separate revenue-share | Does not map to unit-based royalty accounting |

| Training / clinical support | Excluded | Not product revenue |

| Bundle sales | Allocated via A/(A+B) standalone-price formula | Standard combination-product mechanic |

| Ex-territory sales | Separate rate or excluded | FX and reimbursement noise |

| Successor products (same indication) | Included via anti-circumvention | See Revolution / Royalty Pharma zoldonrasib precedent |

The bundle allocation formula — identical to the combination-product mechanic from the indication-specific piece — applies at the product-line level rather than the indication level:

NetSales_RoyaltyBearing = NetSales_Combo × ( P_A / (P_A + P_B) )

Where P_A is the standalone price of the royalty-bearing consumable and P_B is the standalone price of the non-royalty-bearing bundled item. Where no standalone price exists (e.g., software never sold separately), the contract must provide an alternative allocation — either cost-of-goods-based or an agreed relative value with a dispute-resolution mechanism (typically independent expert determination).

Rate Tiering

Device royalty rates sit meaningfully below biopharma synthetic royalty headlines:

| Synthetic Royalty Precedent (Biopharma) | Headline Rate | Tiering |

|---|---|---|

| Syndax / Royalty Pharma (Niktimvo, 2023) | 13.8% U.S. net sales | Flat |

| Geron / Royalty Pharma (Rytelo, 2024) | 7.75% / 3% / 1% U.S. net sales | Tiered @ $500M / $1B |

| Revolution / Royalty Pharma (daraxonrasib, 2025) | Tiered | Step-down at $2B / $4B |

| Hypothetical pure device royalty | 6% / 4% / 2% U.S. net consumable sales | Tiered @ $100M / $250M |

A template tiering — 6.0% on the first $100M, 4.0% from $100M–$250M, 2.0% above $250M — produces a blended rate of ~3.5% at $500M annual sales. That is consistent with the Micronomics study average of 4.35% for medical device license agreements (1986–2006) and with the Stanzione 2026 healthcare-equipment benchmark of 5–7%.

The underlying math problem is well-known: a flat synthetic royalty at biopharma-market rates of 7.5–13.8% damages device unit economics on a 50–75% gross margin base. A synthetic royalty at medtech-license-market rates of 4–6% does not clear a royalty fund's 12–20% IRR hurdle against device-specific underwriting risks. Tiered step-downs close part of the gap; the rest must come from tight cap structuring and structural protections.

Cap, Term, and Tail

| Structural Element | Device-Specific Template |

|---|---|

| Cumulative cap | 2.0x upfront (if hit within ~7 years) / 3.0x (extended cap) |

| Post-cap tail | 0.5–1.0% on continuing sales |

| Term | Fixed 10–12 years from close — avoids patent-expiry ambiguity |

| Minimum annual royalty | ~50% of modeled base-case royalty payment |

| Milestone tranching | FDA label expansion, CPT code establishment, MAC coverage thresholds |

The fixed-term structure is the principal drafting answer to the medtech patent-life problem discussed in Patent Life and Loss of Exclusivity and When Does the Money Stop?. A biopharma royalty anchored to patent expiry inherits a well-defined cliff. A device royalty anchored to patent expiry inherits design-around risk, 510(k) predicate risk, and competitive-iteration risk all at once. Fixing the term at 10–12 years prices all of those into the headline rate rather than the termination trigger. This also eliminates Brulotte v. Thys issues — a fixed-term contract not nominally tied to patent practice does not implicate the doctrine.

Anti-Circumvention and Successor Product Capture

Medical devices iterate. A royalty drafted against "Catheter X v2.0" needs to capture "Catheter X Next Gen" in the royalty base, or the sponsor can effectively walk away from the royalty obligation by introducing a re-SKU'd successor.

The template clause structure (borrowing from Revolution Medicines / Royalty Pharma on zoldonrasib, covered in the indication-specific royalties piece):

- Definition of Successor Product — any product with (i) the same intended use, (ii) substantially similar mechanism of action, and (iii) substantially similar target anatomy as the original royalty-bearing product.

- Automatic capture — Successor Product net sales are included in the royalty base absent express carve-out.

- Carve-out mechanism — sponsor may apply in writing with supporting data; investor has defined consent framework (not unreasonably withheld).

- Dispute mechanism — independent expert determination (LCIA, AAA, or named clinical/regulatory expert) if parties cannot agree on successor-product scope.

Accounting: True Sale vs. Debt

| Structure | Balance Sheet | Tax | Bankruptcy Remoteness |

|---|---|---|---|

| True sale (UCC Art. 9 + non-recourse) | Derecognized | Gain on sale | Bankruptcy-remote (structured) |

| Revenue interest financing / secured note | Liability recorded | Interest deductible | Secured claim |

For medtech, true-sale treatment is harder than for biopharma because the royalty base is narrower and the underlying cash-flow life is shorter — audit challenges to the economic substance of the "sale" are more likely to succeed. Most medtech royalty deals, if and when they close at scale, will be structured as revenue interest financings or royalty-backed notes. The accounting simplicity outweighs the off-balance-sheet optics. This was the path taken in the Intarcia 2015 transactions and in multiple subsequent revenue interest financing agreements (RIFAs) since. Under ASC 470 / ASC 606 the classification turns on substance rather than form; device deals are more likely to fail the "true sale" substance test than pharma deals.

Covenants and Information Rights

Even in true-sale form, the investor will require a covenant and information-rights package that is functionally equivalent to a secured debt covenant set:

- Quarterly royalty reports at SKU / geography / indication granularity

- Annual audit rights, with threshold-triggered true-up (typically 5% underpayment)

- Commercially Reasonable Efforts obligation on the royalty-bearing product family

- Anti-divestiture lock-up or mandatory prepayment-on-divestiture

- Negative pledge over licensed IP

- Change-of-control put right at defined multiple

- Competing-license prohibition with defined scope (same indication, same mechanism)

- ERP segment-reporting warranty with remediation process if reporting breaks down

Rate and Deal-Size Benchmarks

Medical Device Royalty Rate Benchmarks

| Source | Sample / Period | Statistic |

|---|---|---|

| Micronomics medical device license study | 1986–2006 | Average 4.35% of net sales |

| RoyaltyRange medtech benchmarking | 2024 | Median varies by sub-segment; 3–6% core |

| Royalty Rates for Medical Devices & Diagnostics 2022 | Cumulative database | Range 0.5%–44%; modal rate 5% |

| Stanzione IP Law 2026 | 2026 estimate | Healthcare equipment 5–7% |

Stage-Gated Rate Table (Medtech Specific)

| Stage | Rate Range | Precedent Notes |

|---|---|---|

| Preclinical / bench | 1–3% | Rare for medtech; most assignments not licensed on royalty |

| First-in-human / early clinical | 2–4% | University-originated device licenses cluster here |

| 510(k) cleared, pre-commercial | 3–5% | Most common pre-launch medtech license band |

| De Novo / PMA approved | 4–7% | Reduced 510(k) predicate risk justifies premium |

| Commercial, reimbursement-established | 5–8% | Consistent with Stanzione healthcare equipment band |

| Breakthrough / orphan-equivalent position | 8–15% | Rare; dominant IP + no practical substitute required |

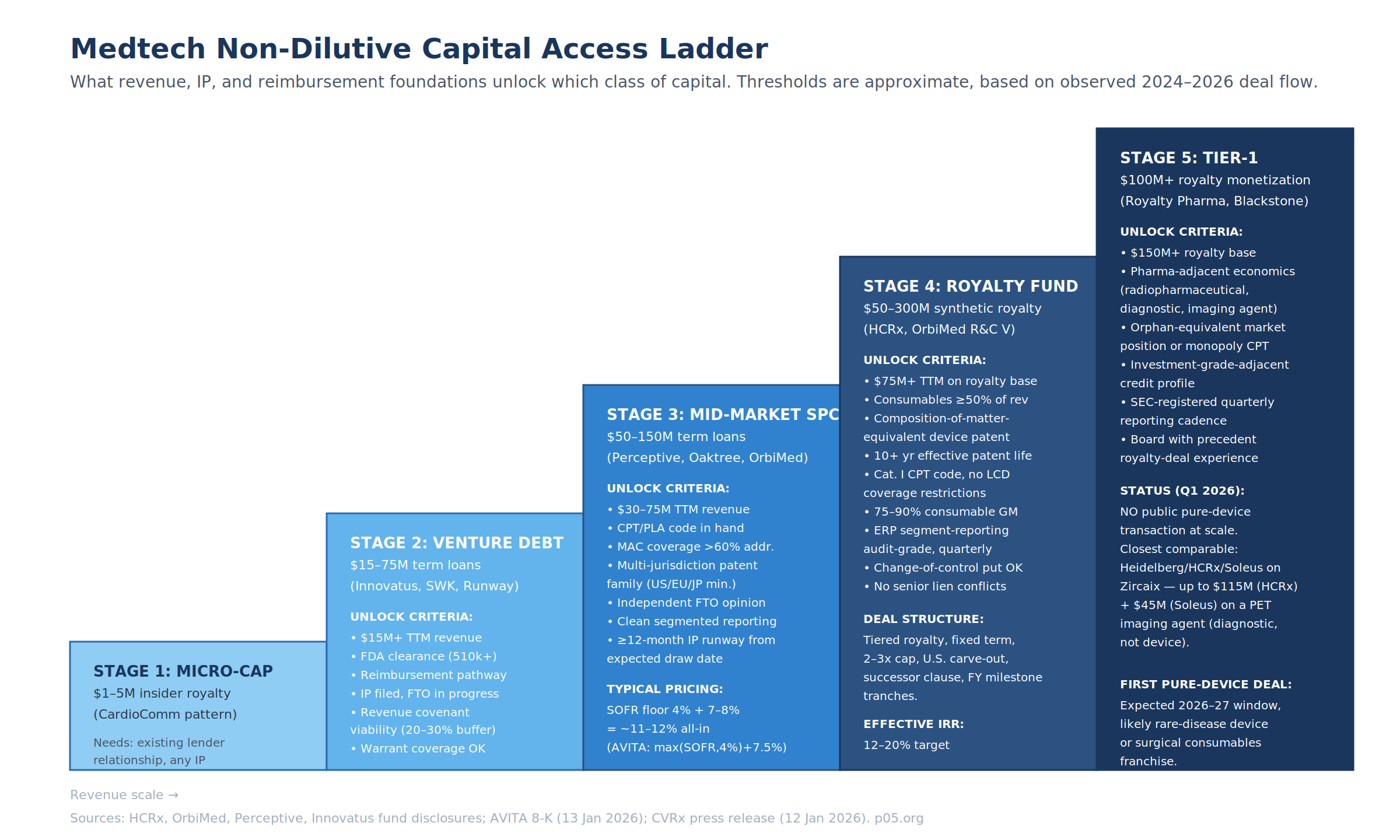

Investor-Type / Deal-Size Matrix

| Investor Class | Typical Check | Instrument | Pricing Anchor |

|---|---|---|---|

| Insider / micro-cap royalty | $1–5M | Royalty-based financing | Informal; CardioComm pattern |

| Specialty credit (Innovatus, SWK, Runway) | $15–75M | Term loan + warrants | ~Prime + 2.65%–4.00% or SOFR + 7.00%–8.00% |

| Mid-market specialty credit (Perceptive, Oaktree, OrbiMed) | $50–150M | Senior secured term loan | max(SOFR, 4.00%) + 7.00%–7.50% |

| Royalty fund with device mandate (HCRx, OrbiMed R&C V) | $50–300M | Synthetic royalty / royalty-backed note | 12–20% implied IRR |

| Tier-1 royalty (Royalty Pharma, Blackstone LS) | $100M+ | Pure synthetic royalty | 10–18% implied IRR, but no device precedent at scale |

The AVITA and CVRx Q1 2026 deals fall into the mid-market specialty credit band. No Q1 2026 medtech transaction hit the royalty-fund band — the closest public comparable is Heidelberg Pharma / HCRx / Soleus on Zircaix, which is diagnostic-adjacent rather than pure medtech.

Royalty-Readiness Ladder

The ladder above maps observable 2024–2026 deal thresholds to five capital tiers. The gating criteria are a working synthesis of fund disclosures (HCRx, OrbiMed, Perceptive, Innovatus), AVITA and CVRx 8-K covenant structures, and comparable biopharma royalty deal terms.

Tier 2 (Venture Debt) — $15–75M

Minimum substantive requirements:

| Dimension | Threshold |

|---|---|

| TTM revenue (target base) | $15M+ |

| FDA status | 510(k) cleared at minimum |

| Reimbursement | Defined pathway; initial payer coverage |

| IP | Filed; FTO assessment in process |

| Financial reporting | GAAP-compliant, quarterly |

| Covenant buffer | Company can support ~20–30% headroom on revenue covenant |

| Warrant coverage | Sponsor willing to issue 1–3% of common stock on a 10-year warrant |

Tier 3 (Mid-Market Specialty Credit) — $50–150M

Adds to Tier 2:

| Dimension | Threshold |

|---|---|

| TTM revenue | $30–75M |

| CPT / PLA code | Secured (Category I or PLA in place) |

| MAC coverage | ≥60% of addressable patient population |

| Patent family | Filed U.S., EPO (EU5 validated), Japan minimum |

| FTO | Independent third-party opinion on file |

| Segmented reporting | Product, geography, indication — quarterly, audit-grade |

| Remaining IP runway | ≥12 months beyond expected draw date |

| All-in price | ~11–12% (AVITA at max(SOFR, 4%) + 7.50% = 11.82%) |

Tier 4 (Royalty Fund Device Mandate) — $50–300M

Adds to Tier 3:

| Dimension | Threshold |

|---|---|

| TTM revenue on royalty base | $75M+ |

| Consumables share of revenue | ≥50% of target royalty base |

| IP profile | Composition-of-matter-equivalent claim(s); multi-jurisdiction family |

| Effective patent life | 10+ years from expected deal close |

| Reimbursement | Category I CPT code; no restrictive LCD; no prior-authorization surprises |

| Gross margin on royalty base | 75–90% (consumable or diagnostic-like) |

| Change-of-control provisions | Put right or mandatory prepayment acceptable |

| Senior lien interaction | No unresolvable conflicts with existing senior credit |

Tier 5 (Tier-1 Royalty Fund) — $100M+

Adds to Tier 4:

| Dimension | Threshold |

|---|---|

| Royalty base scale | $150M+ TTM |

| Economic profile | Pharma-adjacent (radiopharmaceutical, diagnostic, imaging, rare-disease device) |

| Market position | Orphan-equivalent or effectively-monopoly CPT code |

| Credit profile | Investment-grade-adjacent on the underlying product cash flows |

| Reporting cadence | SEC-registered quarterly, or equivalent IFRS disclosure |

| Board experience | At least one member with prior royalty-deal execution |

No public pure-device transaction has cleared Tier 5 as of April 2026. The closest comparable remains Heidelberg Pharma / HCRx / Soleus on Zircaix at up to $160M cumulative potential capital on a PET imaging agent.

The Overlooked Tripwire: Negative Pledge Conflicts

The single most common structural problem preventing a later royalty monetization is a negative-pledge clause in an earlier venture debt or term loan facility. Both the AVITA 8-K and the standard Perceptive and Innovatus credit agreement templates include covenants that "limit or restrict the ability of the Company and its subsidiaries to … create liens and encumbrances [and] incur additional indebtedness." A true-sale synthetic royalty should not technically constitute indebtedness — but in practice it routinely does constitute a lien or encumbrance on IP, product contracts, or revenue, which puts it squarely inside the negative-pledge clause unless a carve-out was negotiated in the original facility.

Practitioner implication: the covenant package in a Series B or C venture debt facility determines the optionality a commercial-stage company will have five years later when it wants to monetize a royalty. This is the same problem covered in the RCF article in the biopharma context. For medtech it is more consequential because the royalty window is narrower.

Structural Outlook

Three forces will move the medtech royalty market in 2026–2027:

| Force | Mechanism | Expected Impact |

|---|---|---|

| KKR integration of HCRx | Lowered cost of capital via Global Atlantic insurance float | HCRx able to price deals previously below its IRR hurdle |

| OrbiMed Fund V deployment | $1.86B closed Aug 2025 with explicit device mandate | Pressure to source device transactions alongside biopharma credit book |

| Inflation Reduction Act precedent | Pharma negotiation timelines push more biopharma toward synthetic royalties | Spillover sophistication into device-adjacent deals |

The first Tier-5 pure-device royalty transaction is likely to land in either (a) a consumables-heavy surgical or procedural platform where the consumable revenue segment isolates cleanly, (b) a rare-disease device franchise with orphan-designated reimbursement and a Category I CPT code, or (c) a drug-device combination product where the drug component anchors a pharma-style royalty with the device riding along.

For medtech CFOs with a 24–36 month non-dilutive capital horizon, the priority order is (1) engineer the consumables revenue architecture now, (2) build the IP and FTO file, (3) lock down CPT coding and MAC coverage, (4) negotiate negative-pledge carve-outs in any current debt facility that permit a future royalty monetization, and (5) open exploratory conversations with HCRx and OrbiMed 12 months before the capital is needed. The AVITA and CVRx Q1 2026 transactions are the working template for what the bridge looks like in the meantime.

All information in this article was accurate as of the publication date and is derived from publicly available sources including SEC filings, company press releases, regulatory announcements, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.