Revolving Credit Facilities in Pharmaceutical Financing

Understanding the instrument that sits behind every major royalty fund's capital structure and every commercial-stage biotech's liquidity toolkit — how revolvers work, why they matter, and how they interact with royalty financing transactions.

The Instrument in Context

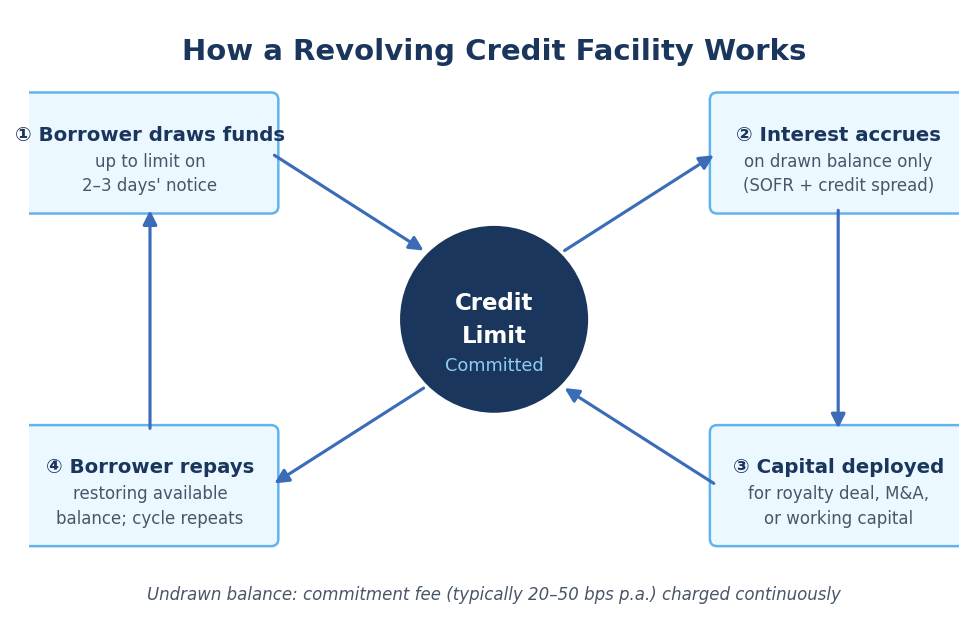

A revolving credit facility — universally abbreviated to "revolver" or "RCF" in deal documentation — is one of the most structurally flexible instruments in corporate finance. Unlike a term loan, which delivers a single lump sum and is repaid on a fixed schedule, a revolver provides a committed credit limit that a borrower can draw, repay, and redraw an unlimited number of times over the facility's life.

Interest accrues only on the drawn balance. The undrawn portion sits available, instantly accessible on short notice — typically two to three business days for standard draws, sometimes same-day for swingline sublimits.

In the broader corporate market, revolvers are used primarily for working capital: smoothing cash flow troughs, funding seasonal inventory, bridging acquisition closings. In the pharmaceutical industry, they perform an analogous function — but the cash flow profile of a drug company makes their role distinctly different from that of a retailer or industrial manufacturer.

Royalty receipts arrive quarterly, milestone payments arrive unpredictably, and the capital requirements of clinical programs are lumpy and often front-loaded. The revolver is the instrument that bridges these timing gaps without forcing a company into a full-scale term financing event every time it needs cash.

What makes pharmaceutical revolvers particularly interesting is that they appear on both sides of the royalty financing market: they are used by biotech and pharma companies as operational liquidity tools, and by royalty investment funds as leverage instruments to deploy capital faster and at greater scale than equity alone would permit. Understanding both uses is essential to understanding the full architecture of pharmaceutical royalty financing as it stands in early 2026.

The Mechanics: How a Revolver Works

The core mechanism is straightforward. A lender — typically a commercial bank, a syndicate of banks, or in life sciences increasingly an alternative credit fund — commits to make available up to a maximum amount for a defined period, usually three to five years. The borrower pays a commitment fee on the undrawn portion (typically 20 to 50 basis points annually) and an interest rate on any drawn amounts, calculated as a floating benchmark rate plus a credit spread.

In the United States, the floating benchmark is Term SOFR (the Secured Overnight Financing Rate, which replaced LIBOR). In Europe, EURIBOR or SONIA serves the same function. The credit spread — the margin above the benchmark — reflects the borrower's risk profile and typically varies based on the borrower's public debt rating or financial leverage.

The key economic features that distinguish a revolver from other debt instruments:

Interest on drawn amounts only. If a company has a $500 million revolver and draws $100 million, it pays interest only on $100 million. The remaining $400 million is available without cost other than the commitment fee.

Commitment fee on undrawn balance. The lender charges a fee — typically 20 to 50 basis points per annum — on the undrawn portion, as compensation for holding the capital in reserve. For a $1.8 billion facility, the annual commitment fee alone could be $3.6 to $9 million even if never drawn.

Draw-repay-redraw freely. Unlike a term loan, which cannot be redrawn once repaid, the revolver resets to its full committed amount upon repayment. A company can draw $200 million in January, repay it in March, and draw $300 million again in July — all under the same facility agreement without reapplying.

Defined maturity. Most revolvers have a maturity of three to five years, at which point any outstanding balance must be repaid or the facility renegotiated. Many include one or two one-year extension options, exercisable at the borrower's request with lender consent.

Financial maintenance covenants. Unlike high-yield bonds or many royalty financing instruments, revolvers typically carry financial maintenance covenants — tested quarterly — that require the borrower to maintain certain leverage ratios, interest coverage ratios, or minimum liquidity thresholds. Breach of a maintenance covenant does not automatically constitute a default, but it gives the lenders the right to accelerate repayment or demand remediation.

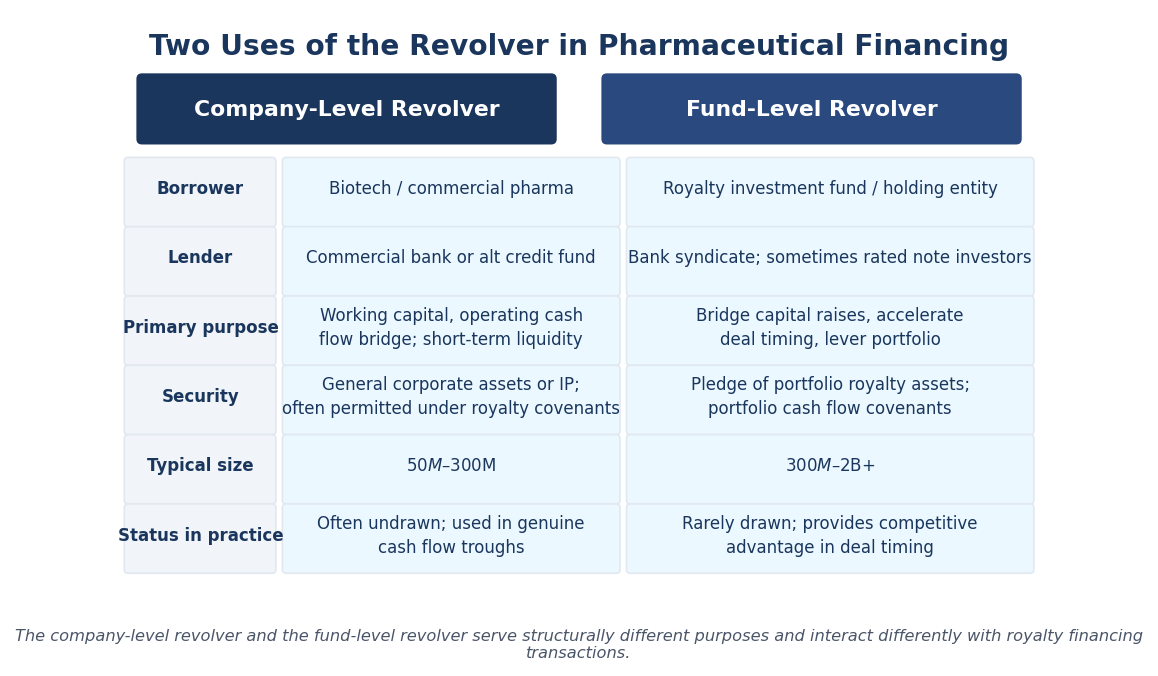

Two Distinct Uses in Pharmaceutical Financing

The pharmaceutical industry uses revolvers in two structurally different ways. The first is the traditional corporate revolver, used by a biotech or pharmaceutical company for operational liquidity. The second is the fund-level revolver, used by royalty investment funds to lever their portfolios between equity capital raises and to accelerate deal timing. Each has different lenders, different covenants, and different risk profiles.

Use Case 1: Biotech and Pharma Company Revolvers

For operating pharmaceutical companies, the revolver serves as a liquidity backstop. A commercial-stage biotech with a single approved product — generating steady but irregular quarterly revenues against a large cost base — will periodically face short-term cash shortfalls that are not indicative of structural weakness but simply reflect the timing mismatch between when revenues arrive and when expenses must be paid.

The revolver fills that gap without forcing a dilutive equity raise or a new debt financing event.

In practice, most biotech companies prefer to maintain the revolver as an undrawn, committed backstop. Drawing it signals to the market that operating cash flows are insufficient for self-funding — a signal most management teams prefer to avoid unless genuinely necessary. When drawn, it is typically repaid quickly as the underlying cash flow timing issue resolves.

Verona Pharma (2025): Following the successful launch of Ohtuvayre (ensifentrine) — the first inhaled COPD maintenance therapy to combine bronchodilator and non-steroidal anti-inflammatory activity in a single molecule — Verona Pharma refinanced its strategic financing in March 2025, repaying its existing revenue interest purchase and sale agreement (RIPSA) and increasing the primary term loan facility to $450 million on improved terms with Oaktree Capital Management and OMERS Life Sciences.

The amended documentation included a specific provision permitting Verona to access up to $75 million through a separate working capital revolving credit facility with a third-party lender. The RCF was not part of the Oaktree/OMERS facility — it was an additional liquidity layer, explicitly permitted as a carve-out under the primary facility's negative covenant package. Verona was subsequently acquired by Merck & Co. in October 2025, but the structural approach — royalty/term debt from specialty lender, working capital revolver from bank — illustrates the layered approach increasingly used in life sciences.

Apellis Pharmaceuticals (2024): Apellis, the developer of Syfovre (pegcetacoplan) for geographic atrophy, entered into a non-dilutive senior secured credit facility of up to $475 million with Sixth Street in May 2024, with $375 million funded at close and an option to draw an additional $100 million prior to September 2025. Crucially, the Sixth Street agreement also permitted Apellis to access $100 million through a separate third-party working capital revolving facility.

Apellis used the majority of the net proceeds to buy out an existing SFJ Pharmaceuticals development liability for approximately $326 million — eliminating $366 million in future payment obligations — while preserving separate revolving capacity for day-to-day liquidity management.

BridgeBio Pharma (2021): BridgeBio secured a credit facility of up to $750 million with a bank syndicate in November 2021 — a facility that included revolving components and was structured to fund more than 30 genetic disease and cancer pipeline programs. The facility, combined with BridgeBio's existing cash, provided access to over $1.2 billion.

BridgeBio subsequently repaid its previous term loan in February 2025 using proceeds from $563 million in new convertible notes, and in June 2025 separately completed a $300 million royalty interest purchase agreement with HealthCare Royalty (HCRx) and Blue Owl Capital for European royalties on Beyonttra/Attruby (acoramidis) for ATTR-cardiomyopathy. BridgeBio's evolution — from debt-funded pipeline company, through commercial launch, to royalty monetisation — illustrates the typical progression of the pharmaceutical financing toolkit.

Use Case 2: Royalty Fund Revolvers

The second and less widely understood use of revolvers in pharmaceutical financing is at the fund level. Royalty investment funds — Royalty Pharma, HealthCare Royalty Partners, and increasingly multi-strategy alternative asset managers — use revolving credit facilities as part of their own capital structures to bridge equity capital raises, accelerate deal timing, and lever their portfolios to enhance returns.

Royalty Pharma (Nasdaq: RPRX): Per its Q1 2025 10-Q filing with the SEC, Royalty Pharma's subsidiary RP Holdings maintains an unsecured revolving credit facility with borrowing capacity of $1.8 billion, with $1.69 billion of commitments maturing in December 2028 and the remaining $110 million maturing October 2027. The facility was established in September 2021 and has been amended five times, with Amendment No. 3 in December 2023 increasing the commitment from approximately $1.5 billion to $1.8 billion and extending maturities.

As of March 31, 2025 — and throughout full years 2024 and 2025 — the facility was entirely undrawn. Royalty Pharma's guidance documents for both years explicitly state that financial projections assume "no additional debt financing, including no drawdown on the revolving credit facility." The facility's interest rate, when drawn, floats based on the borrower's public debt rating: Term SOFR or the base rate plus an applicable margin that varies with Royalty Pharma's credit rating. The undrawn commitment fee similarly varies with the rating.

The one documented instance of the facility being drawn occurred in October 2023, when Royalty Pharma drew $350 million to fund a royalty acquisition. The company repaid the full amount before the end of Q4 2023 — within roughly six to eight weeks. This is the canonical use case for the fund-level revolver: see an opportunity, act immediately with bridge financing, close the deal, then refinance at leisure.

Without the committed $1.8 billion backstop, Royalty Pharma would have had to either time its royalty acquisitions to available cash — missing time-sensitive deal windows — or maintain a much larger cash balance permanently, which would drag on returns.

The covenant structure for Royalty Pharma's RCF reflects the fund's unique economics. The credit agreement defines Adjusted EBITDA as Portfolio Receipts minus operating and professional costs, and Portfolio Cash Flow as Adjusted EBITDA minus net interest paid. These non-GAAP definitions, disclosed in full in Royalty Pharma's quarterly filings, are the contractual basis for the material covenants.

Compliance is therefore tied directly to portfolio performance — meaning a significant drug underperformance event (such as the accelerated US generic entry of Promacta beginning in May 2025, which weighed on royalty receipts) could theoretically tighten covenant headroom even without an actual breach.

HealthCare Royalty Partners (HCRx): In October 2023, HCRx announced the closing of a $680 million credit facility for HCRx Holdings LP, its permanent capital vehicle. The facility comprised a $380 million term loan and a $300 million revolving credit facility, with the revolving portion disclosed as undrawn at closing. With total liquidity exceeding $1 billion, HCRx used this capital structure to expand its deal activity across its target mid-market range ($50 to $300 million per transaction), competing more effectively against the larger balance sheets of Royalty Pharma and Blackstone Life Sciences.

HCRx's strategy differentiates on scientific diligence and mid-market flexibility rather than transaction size — the revolver gives it the optionality to close quickly when a deal requires it. KKR subsequently acquired a majority stake in HCRx in mid-2025 at a valuation of approximately $3 billion, signalling growing institutional conviction in the royalty asset class and providing HCRx with further access to lower-cost capital.

RCF vs. Royalty Monetisation: The Structural Choice

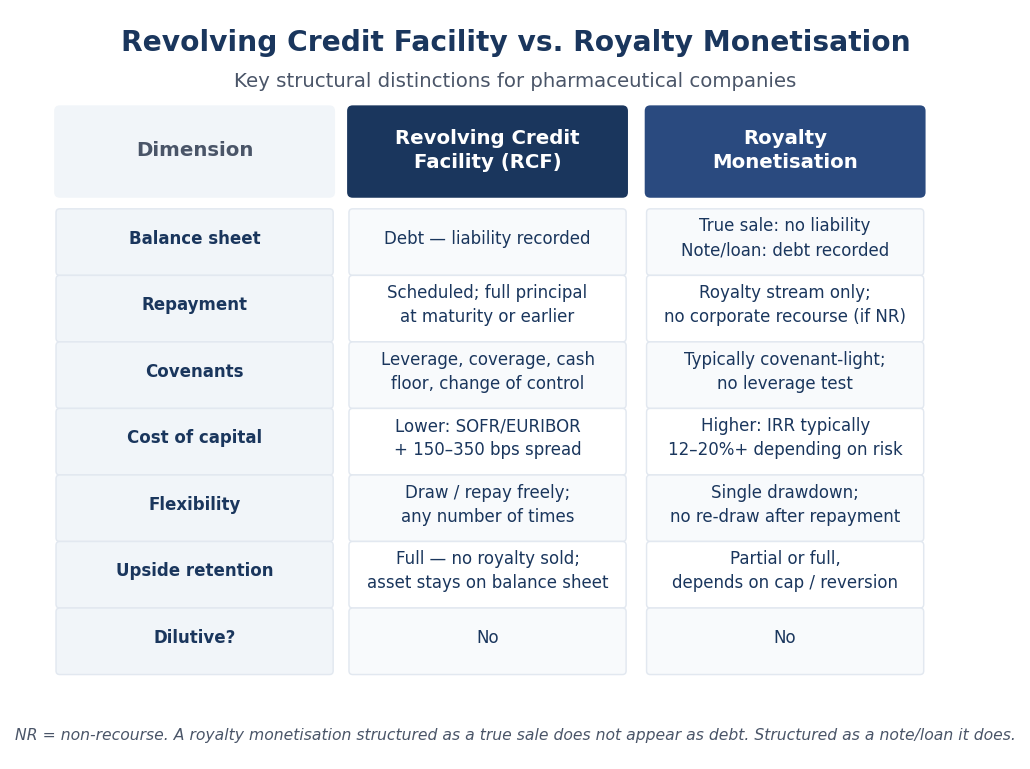

When a biotech company considers how to raise non-dilutive capital, the revolver and the royalty monetisation represent fundamentally different instruments suited to different strategic circumstances. The choice is not binary — most sophisticated companies eventually use both — but understanding the structural distinction is essential to CFO decision-making.

The revolver is cheaper but more constrained. Drawn at SOFR plus 150 to 350 basis points — roughly 6 to 9% all-in in the 2024–2026 rate environment — the revolver is significantly cheaper than royalty financing, which effectively prices at an IRR of 12 to 20% or higher depending on asset risk. But the revolver requires a lender willing to extend credit, which in turn requires bankable assets, a credible repayment path, and covenant compliance. A pre-commercial biotech with no product revenues and no tangible collateral will not secure a bank revolver on acceptable terms, regardless of how good its pipeline is.

The royalty monetisation is covenant-light but more expensive. When structured as a true sale of a royalty stream, the royalty monetisation does not appear as debt on the borrower's balance sheet, imposes no leverage covenants, and provides no-recourse capital (meaning the lender cannot pursue the company's other assets if the royalty stream underperforms). The cost of this structural flexibility is the higher effective return demanded by the royalty investor — and the permanent (or semi-permanent) transfer of a portion of the royalty upside.

The revolver preserves upside; the royalty monetisation monetises it. A company that draws its revolver and repays it has sold nothing — its royalty stream remains intact, and when the drug performs well, all of that performance accrues to equity.

A company that sells a royalty stream has traded future cash flows for current capital. If the drug subsequently becomes a blockbuster, the royalty investor participates in that success, not the company. This optionality preservation is the most important reason why well-capitalised companies with banking relationships will almost always prefer the revolver for short-term needs.

Covenant interaction when both exist. The most technically complex scenario is a company that has an existing revolver and subsequently enters into a royalty monetisation — or vice versa. Standard negative covenants in pharmaceutical revolvers restrict additional indebtedness, liens on assets, disposals of material assets, and changes of control. A royalty monetisation structured as a true sale does not technically constitute additional indebtedness (the company is selling an asset, not borrowing money) and therefore may not trigger the debt restriction covenant.

However, if the royalty purchaser takes a security interest over IP or product contracts as part of a royalty-backed loan, it may constitute a lien on assets, requiring either a carve-out in the original revolver documentation or explicit lender consent. Covington & Burling's 2025 overview of debt and royalty financing structures for life sciences businesses specifically addresses this interaction, noting that the Shoot the Moon bankruptcy case has clarified the security requirements for certain royalty financing structures and that careful documentation is required when layering instruments.

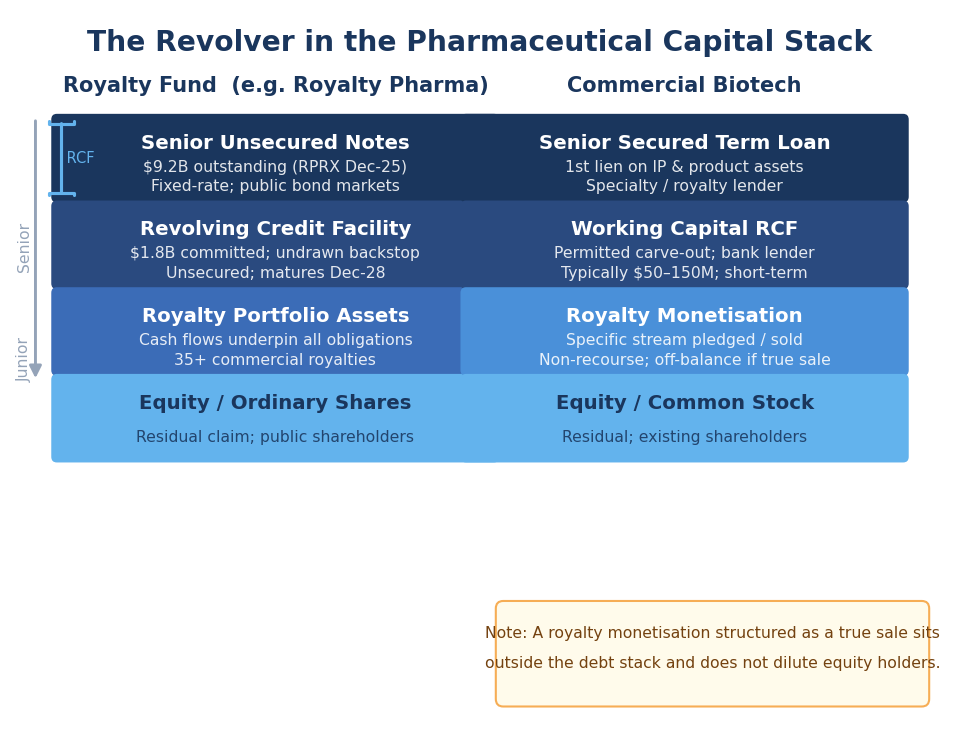

The Revolver in the Capital Stack

Where the revolver sits in the capital stack — and what that means for all other creditors and equity holders — depends on whether it is a company-level or fund-level facility and whether it is secured or unsecured.

For Royalty Pharma, the $1.8 billion revolver is pari passu with the senior unsecured notes: both are unsecured general obligations of RP Holdings, the operating subsidiary. As of December 2025, Royalty Pharma carried total debt of approximately $9.2 billion in senior unsecured notes — the revolver sits alongside those notes at the same priority level, undifferentiated in terms of payment priority.

The entire debt capital structure is underpinned by the royalty portfolio's cash generation: approximately $3.3 billion in Portfolio Receipts in 2025. The covenants in the credit agreement are calibrated to this portfolio cash flow — not to EBITDA in the traditional corporate finance sense.

For a commercial-stage biotech with a term loan from a specialty lender and a separate working capital revolver from a bank, the interplay is more nuanced. The term lender typically has a first-lien security interest over IP, product contracts, and other product-related assets. The revolving credit bank may have a second-lien position, a pari passu position over different asset classes, or an unsecured claim.

A royalty monetisation structured as a true sale sits entirely outside this framework — the royalty fund that purchased the stream holds a property right in the royalty, not a debt claim against the company, and the transaction does not subordinate any existing creditor or dilute existing equity holders.

The practical consequence of this structure is that a royalty monetisation and a revolver can coexist without either instrument threatening the other's position, provided the covenant documentation is appropriately drafted.

The Verona Pharma example demonstrates this: Oaktree and OMERS held the primary secured term loan position, Verona was permitted to raise a separate $75 million working capital revolver from a third-party bank, and none of these instruments interacted destructively with the others because the documentation was structured to accommodate all three.

Key Terms and Covenants

Pharmaceutical revolvers carry a set of standard economic and structural terms that differ in important ways from general corporate revolvers in other sectors. The following table summarises the key parameters across a typical life sciences revolver, drawing on publicly filed credit agreements and market convention as of March 2026.

| Term | Typical Range (Life Sciences) | What It Measures |

|---|---|---|

| Commitment fee (undrawn) | 20–50 bps per annum | Cost of maintaining undrawn availability |

| Drawn interest rate | SOFR/EURIBOR + 150–350 bps | All-in cost on drawn amounts; often varies with credit rating |

| Leverage covenant | Net debt / Adjusted EBITDA ≤ 4.0–6.0x | Limits total indebtedness relative to earnings |

| Interest coverage covenant | EBITDA / Interest expense ≥ 2.0–3.5x | Ensures cash earnings capacity to service debt |

| Portfolio cash flow covenant (fund-level) | Portfolio Receipts − opex ≥ defined threshold | Fund-specific metric tracking royalty income vs. running costs |

| Minimum liquidity / cash floor | $50M–$150M depending on facility size | Ensures borrower retains a minimum operating cash buffer |

| Maturity | 3–5 years; often with 1–2 one-year extension options | Duration of committed availability |

| Change of control | Typically triggers mandatory repayment | Protects lender against deterioration in credit quality on M&A |

| Permitted indebtedness | Carve-outs for working capital revolver, purchase money debt, etc. | Defines what additional debt is allowed alongside facility |

| Negative pledge | Restricts liens except for permitted exceptions | Prevents junior liens being placed on security package |

One feature worth emphasising is the portfolio cash flow covenant specific to royalty fund revolvers. For Royalty Pharma, the credit agreement defines Portfolio Cash Flow as Adjusted EBITDA (Portfolio Receipts minus operating costs) minus net interest paid. This covenant is tested quarterly.

It means the lenders' protection is directly tied to the royalty portfolio's performance — if key royalties decline (through patent expiry, generic competition, or biosimilar entry), the coverage ratios may tighten even if Royalty Pharma remains technically profitable. This is structurally different from a traditional corporate leverage covenant, where EBITDA can be maintained through cost reduction even as revenues fall. A royalty fund's only lever is the incoming cash from royalties — it cannot cut its way to covenant compliance if the underlying drugs underperform.

Selected Transactions and Examples

The following transactions illustrate how revolvers appear in the pharmaceutical and royalty financing landscape across different contexts and scales, accurate as of March 2026.

| Entity | RCF Size | Year | Context | Key Features |

|---|---|---|---|---|

| Royalty Pharma (RPRX) | $1.8 billion | 2021 (amended Dec 2023) | Fund-level liquidity for royalty acquisitions | Unsecured; undrawn as of Q1 2025; drawn once in Oct 2023 ($350M, repaid Q4 2023); matures Dec 2028 |

| HealthCare Royalty Partners | $300 million | Oct 2023 | Part of $680M facility for HCRx Holdings permanent capital vehicle | Paired with $380M term loan; undrawn at closing; KKR acquired majority stake in HCRx mid-2025 |

| Apellis Pharmaceuticals | $100 million | May 2024 | Permitted third-party working capital facility alongside $475M Sixth Street term loan | Explicit covenant carve-out; supports Syfovre commercial launch operations |

| Verona Pharma | Up to $75 million | Mar 2025 | Working capital RCF permitted alongside $450M Oaktree/OMERS term loan | Carve-out in primary facility documentation; Verona acquired by Merck & Co. Oct 2025 |

| BridgeBio Pharma | $750M facility (revolving component) | Nov 2021 | Credit facility funding 30+ pipeline programs including pre-commercial acoramidis | Provided runway to 2024; Attruby approved Nov 2024; BridgeBio subsequently did $300M HCRx/Blue Owl royalty deal June 2025 |

Accounting and Tax Treatment

The accounting treatment of a revolving credit facility is straightforward: it is debt, recorded as a liability on the balance sheet. Drawn amounts appear as current or non-current debt depending on the maturity profile; undrawn commitments are disclosed in notes to the financial statements but do not appear as balance sheet liabilities. Commitment fees paid on the undrawn portion are expensed as incurred and flow through the income statement as interest expense.

For a commercial company, this creates no particular accounting complexity unless a royalty monetisation is layered alongside. When the royalty financing is structured as a true sale — the dominant structure in the market for commercial royalties — the company derecognises the royalty asset from its balance sheet and the transaction does not appear as a liability.

If instead the royalty financing is structured as a secured note (as in the Zymeworks–Royalty Pharma non-recourse royalty-backed note announced in March 2026), the note appears as debt, and the company must disclose both the revolver and the royalty-backed note as separate liabilities with different seniority and security profiles.

The RSM analysis of royalty monetisation tax treatment highlights a critical distinction: tax characterisation is determined by substance, not form. A revolver is unambiguously debt for tax purposes — interest is deductible as a borrowing cost, subject to applicable thin capitalisation rules. A royalty monetisation structured as a true sale is treated as a sale: no interest deduction, but the seller may recognise a gain on disposal of the royalty asset.

If the royalty deal is re-characterised by a tax authority as a loan despite its sale-form documentation, the seller would lose the sale treatment and potentially face adverse consequences. This is a real risk in aggressive royalty monetisation structures and is one reason why careful documentation and legal opinions on true sale characterisation are standard in market-standard transactions.

When Does the Revolver Make Sense?

Not every pharmaceutical company needs a revolver, and not every royalty fund structures one. The instrument makes sense when specific conditions are met.

For an operating company, the revolver is justified when product revenues are predictable enough to service debt but irregular enough that short-term cash needs occasionally exceed available cash. The prototypical revolver borrower is a commercial-stage biotech with one or two approved products generating steady quarterly net sales, ongoing R&D spending that is front-loaded in certain quarters, and milestone payments arriving irregularly.

The revolver is not available — and banks will not provide it on acceptable terms — when the company has no bankable assets, no product revenues, and no path to self-sustaining cash flows. In that case, royalty monetisation or equity is the appropriate instrument.

For a royalty fund, the revolver is justified when deal volume and size create timing mismatches between equity capital deployment and available cash. A fund deploying $2 to $5 billion per year in royalty transactions will periodically identify opportunities where acting within 24 to 48 hours is competitively necessary.

The revolver bridges the gap. The annual commitment fee — at 20 to 40 basis points on a $1.8 billion facility, roughly $3.6 to $7.2 million per year — is negligible relative to the return impact of capturing a high-quality royalty at the right price versus missing it.

When not to rely on the revolver: The revolver is a bridge, not a foundation. It is not designed for, and should never be used for, long-term capital needs. A company that is perpetually drawing its revolver and rolling the balance forward is effectively using a short-term instrument as permanent capital — an inherently unstable financing structure that will likely require renegotiation at an unfavourable time. If a revolver is regularly drawn and not quickly repaid, it is a signal that the underlying business needs a term financing solution, not more revolving capacity.

Market Context: The Growing Sophistication of Pharma Capital Structures

The revolving credit facility has always existed in pharmaceutical financing, but its role has become considerably more sophisticated as the royalty financing market has matured into a mainstream institutional asset class. In the early years of royalty monetisation, the revolver was a niche instrument used by a handful of specialty finance vehicles and the occasional large pharmaceutical company with strong banking relationships.

By early 2026, the market looks very different. Gibson Dunn's 2026 Life Sciences Royalty Finance Outlook documented aggregate royalty financing transaction value reaching approximately $6.5 billion in 2025, up from $5.7 billion in 2024 and from less than $200 million per year in the early 2000s. The investor base has deepened substantially: KKR's mid-2025 acquisition of a majority stake in HealthCare Royalty Partners at a $3 billion valuation reflected growing institutional conviction, and Blackstone Life Sciences, Blue Owl, Sagard, OMERS, Oaktree, and a dozen other firms are now active across transaction sizes from $30 million to $2 billion.

As more capital has entered the royalty financing space, the sophistication of capital structures around royalty transactions has increased correspondingly. Royalty funds now maintain formal credit ratings, issue public investment-grade bonds, and maintain committed revolvers as a standard feature of their liquidity management — not as exceptional instruments.

Commercial biotech companies increasingly negotiate covenant packages that explicitly accommodate royalty monetisations alongside traditional term debt. And law firms specialising in the intersection of debt and royalty finance — Gibson Dunn, Covington & Burling, WilmerHale, Sidley Austin — have developed deep institutional knowledge of how these instruments interact.

For a biotech CFO building a multi-year financing plan, the practical implication is that the revolver and the royalty monetisation are not alternatives to each other — they occupy different layers of the capital stack and serve different types of capital need.

A company that understands both instruments, and structures its documentation to permit both to coexist without covenant conflicts, will have significantly more financial flexibility than one that treats them as mutually exclusive choices.

The revolver is unglamorous. It does not generate deal announcements. It is, in the typical year, entirely undrawn. But its existence — as a committed, standing offer of liquidity available on two days' notice — is precisely what makes it valuable in the unpredictable, lumpy world of pharmaceutical financing. Optionality is worth paying for, and the commitment fee is a reasonable price.

All information in this article was accurate as of the publication date and is derived from publicly available sources including company press releases, SEC filings, regulatory announcements, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.