Non-Recourse Royalty-Backed Notes in Pharmaceutical Financing

The Instrument in Context

The non-recourse royalty-backed note sits in a structural sweet spot that neither a full royalty sale nor traditional pharmaceutical debt can occupy. The issuer (a biotech or pharma company) issues a note—formally a debt instrument—but repayment is secured exclusively by a pledged portion of a royalty stream. The investor's sole recourse upon default is that stream. No claim against the issuer's other assets, no cross-default with corporate obligations, no general liens.

This distinguishes the royalty-backed note from the more familiar royalty purchase agreement (where the buyer takes permanent ownership of the stream) and from synthetic royalty financings (where the funder typically receives a percentage of product revenue with some form of corporate recourse or make-whole provision). The note structure explicitly preserves the issuer's ownership of the underlying royalty; the investor is a creditor with a ring-fenced collateral pool, not an owner of the income stream.

The concept is not new—HealthCare Royalty Partners has long described royalty-backed notes as a distinct category alongside full and partial royalty sales—but the structure has gained traction as the royalty financing market has matured. Gibson Dunn's 2026 Life Sciences Outlook noted that hybrid structures blending royalty economics with elements of term debt are increasingly prevalent, with aggregate royalty financing transaction value reaching approximately $6.5 billion in 2025, up from $5.7 billion the prior year.

Anatomy of the Zymeworks–Royalty Pharma Deal

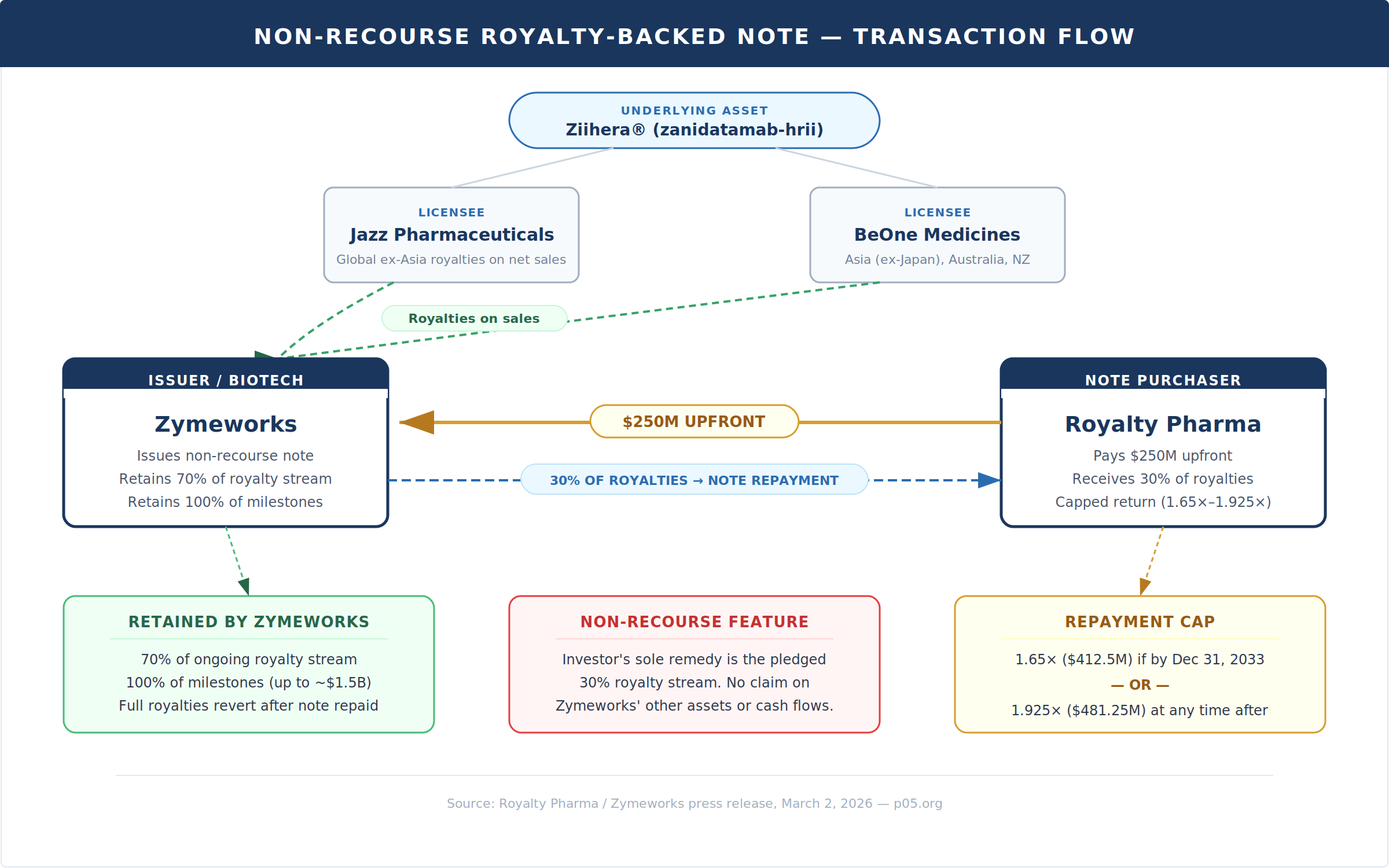

Today's announcement between Royalty Pharma (Nasdaq: RPRX) and Zymeworks (Nasdaq: ZYME) is a textbook illustration of the royalty-backed note. Zymeworks receives $250 million from Royalty Pharma through the issuance of a non-recourse note. Repayment is secured by 30% of the worldwide tiered royalties on Ziihera (zanidatamab-hrii) owed to Zymeworks under separate license agreements with Jazz Pharmaceuticals and BeOne Medicines.

The deal's key commercial terms are worth unpacking in detail.

Royalty allocation. Zymeworks retains 70% of the royalty stream during the repayment period. Under the Jazz collaboration, Zymeworks earns tiered royalties of 10% to high-teens on global annual net sales of Ziihera up to $2.0 billion and 20% above that threshold. Under BeOne, the tiers range from mid-single to mid-double digits on sales up to $1.0 billion and 19.5% above. Royalty Pharma's 30% slice of these streams equates to an approximately low-to-mid-single digit effective royalty on underlying net sales.

Repayment cap. Royalty Pharma's return is hard-capped at two levels: 1.65× the note amount ($412.5 million) if received by December 31, 2033, or 1.925× ($481.25 million) at any point thereafter. Once either threshold is hit, the note is fully discharged and 100% of royalties revert to Zymeworks.

Milestone carve-out. All earned regulatory and commercial milestones under the Jazz and BeOne agreements—potentially up to $1.5 billion—are retained entirely by Zymeworks. This is a critical structural feature: the investor participates only in the royalty stream, not in the binary upside of milestone payments.

Non-recourse. The note is non-recourse to Zymeworks. If Ziihera underperforms commercially and the royalty stream is insufficient to repay the note, Royalty Pharma absorbs the loss. There is no corporate guarantee, no balance-sheet claim.

The Zymeworks Context: Why This Deal, Why Now

The timing and structure of this transaction are inseparable from Zymeworks' broader corporate transformation. The deal was announced alongside Zymeworks' Q4 and full-year 2025 earnings, which reported total revenue of $106.0 million for 2025 (up 39% year-over-year), a net loss of $81.1 million (down 34% from 2024's $122.7 million loss), and $270.6 million in cash, cash equivalents, and marketable securities as of December 31, 2025.

The Underlying Asset: Ziihera

Ziihera (zanidatamab-hrii) is a bispecific HER2-directed antibody engineered by Zymeworks using its proprietary Azymetric platform. It binds two distinct extracellular domains on HER2 simultaneously, triggering receptor internalisation, complement-dependent cytotoxicity (CDC), antibody-dependent cellular cytotoxicity (ADCC), and antibody-dependent cellular phagocytosis (ADCP). The molecule was licensed to Jazz Pharmaceuticals (global ex-Asia) and BeOne Medicines (Asia ex-Japan, Australia, New Zealand) under separate collaboration agreements.

Ziihera currently holds U.S. FDA accelerated approval for previously treated, unresectable or metastatic HER2-positive (IHC 3+) biliary tract cancer (BTC). The drug also received regulatory approvals in the EU, China, and Canada for BTC during 2025. It carries Breakthrough Therapy designation from the FDA for HER2-amplified BTC and for locally advanced or metastatic GEA, along with Orphan Drug designations from both the FDA and EMA.

The more significant commercial catalyst is first-line GEA. In November 2025, Zymeworks announced positive Phase 3 results from HERIZON-GEA-01, which evaluated Ziihera in combination with chemotherapy (with or without the PD-1 inhibitor tislelizumab/Tevimbra) as first-line treatment for HER2+ GEA. At the first interim analysis, Ziihera plus chemotherapy showed a statistically significant improvement in progression-free survival versus trastuzumab plus chemotherapy, and a clinically meaningful effect with a strong trend toward statistical significance for overall survival, with median OS exceeding two years. An additional planned OS interim analysis is expected in mid-2026.

Jazz plans to submit a supplemental BLA in Q1 2026 with a potential U.S. GEA launch in the second half of 2026.

Financial Anatomy

With the deal's structure in hand, the financial picture becomes clearer:

Zymeworks' cash position post-deal. The $250 million note proceeds, combined with $270.6 million in existing cash/securities, gives Zymeworks approximately $520 million in available capital. Against projected aggregate adjusted gross operating expenses of approximately $300 million over 2026–2028 (front-loaded in 2026, declining in 2027–2028), this provides substantial runway.

Share repurchase programme. As of March 2, 2026, Zymeworks had utilised approximately $62.5 million of a $125 million buyback programme to repurchase 2,580,415 shares at an average price of $24.22. CEO Kenneth Galbraith described the stock as trading at a "compelling discount to our estimate of intrinsic value." The note proceeds are explicitly intended to continue funding buybacks—a signal that management views the implied cost of the note as lower than the return on retiring undervalued shares.

Milestone payments retained. The segregation of milestones from the note's collateral pool is critical. Zymeworks' near-term milestone stack includes:

| Milestone | Amount |

|---|---|

| U.S. GEA regulatory approval | $250.0M |

| EU GEA regulatory approval | $100.0M |

| Japan GEA regulatory approval | $75.0M |

| China GEA regulatory approval | $15.0M |

| Third-indication regulatory milestones | $89.0M |

| Commercial milestones (aggregate) | $977.5M |

| Total remaining potential | ~$1.5B |

None of these flow to Royalty Pharma under the note. This is a significant structural concession by the investor—in many royalty financing transactions, milestone payments are either partially or fully included in the collateral pool.

Analyst consensus on Ziihera. Third-party projections suggest peak risk-adjusted sales of approximately $1.5 billion for Ziihera globally. At that level, Zymeworks' total royalty stream (combining Jazz and BeOne tiers) would be substantial, and 30% of that stream directed to Royalty Pharma would likely hit the 1.65× repayment cap well within the 2033 deadline—delivering a healthy return to the investor and triggering full reversion to Zymeworks.

Implied economics for Royalty Pharma. The 30% share of Zymeworks' royalties equates to an effective royalty on Ziihera net sales of approximately low-to-mid single digits. At the 1.65× cap ($412.5 million), Royalty Pharma's gross return on the $250 million outlay is $162.5 million over the repayment period. The actual IRR depends on the pace of royalty accrual—faster sales growth means a compressed payback period and higher IRR. If repayment stretches beyond 2033, the cap rises to 1.925× ($481.25 million), increasing Royalty Pharma's total return but reducing its annualised IRR due to the longer duration.

Advisors

TD Cowen served as financial advisor to Zymeworks. Gibson Dunn acted as legal advisor to Zymeworks. Covington & Burling, Choate, and Maiwald acted as legal advisors to Royalty Pharma. The presence of Gibson Dunn and Covington—both market leaders in royalty financing—signals the institutional sophistication of this deal. Gibson Dunn has historically advised on many of the largest synthetic royalty and structured financing transactions in the sector, and Covington has represented several of the leading royalty fund investors.

Why "Note" and Not "Sale"?

The choice to structure this as a note rather than a purchase agreement is not merely semantic. It has implications across accounting, tax, bankruptcy treatment, and the issuer's strategic flexibility.

In a royalty purchase (true sale), the seller permanently transfers ownership of the royalty interest. The transaction typically sits outside the seller's bankruptcy estate under UCC Article 9 analysis, which is valuable—but the seller permanently forfeits any participation in the upside. As RSM has documented, the tax characterization question (sale vs. loan) turns on substance-over-form analysis, and a transfer that fails to convey all substantial rights may be re-characterized regardless of the label.

The note structure, by contrast, explicitly preserves the issuer's economic ownership. Zymeworks retains 70% of the stream during repayment and 100% afterward. This framework allows the issuer to treat the transaction as debt for accounting purposes, which has several advantages: no immediate recognition of a gain on sale, no derecognition of the underlying asset, and cleaner financial reporting for a company that wants to present the royalty stream as part of its long-term value proposition.

From the investor's perspective, the non-recourse note offers something a true sale does not: a defined ceiling on returns. Royalty Pharma's cap at 1.65–1.925× creates a known maximum-return profile, which simplifies underwriting. In a pure royalty purchase, the investor bears the risk of overpaying (if sales disappoint) and captures the upside (if sales explode). With a capped note, the investor accepts a bounded return in exchange for contractual certainty.

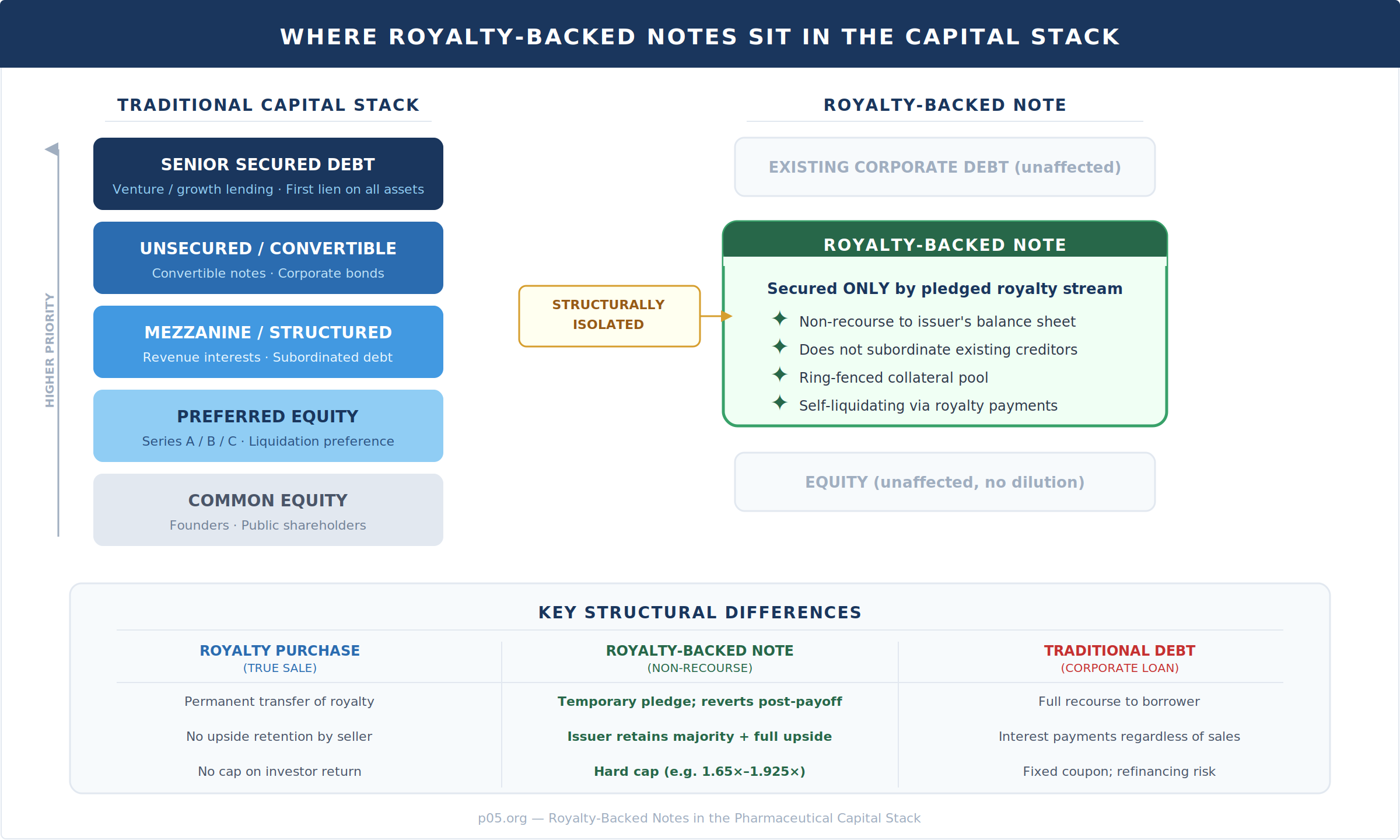

Position in the Capital Stack

The structural isolation of a non-recourse royalty-backed note is its defining feature in the capital stack. Unlike traditional debt—which sits as a claim against the entire enterprise—the note exists in a parallel track, secured only by the ring-fenced royalty stream.

This has significant implications for existing stakeholders. A non-recourse royalty-backed note does not subordinate existing creditors, does not trigger cross-default provisions in the issuer's other debt instruments, and does not dilute equity holders. For Zymeworks specifically, the $250 million in proceeds strengthens its balance sheet without adding corporate-level leverage.

Contrast this with how other royalty financing structures interact with the capital stack. Covington & Burling's 2025 overview of debt and royalty financing structures for life sciences businesses documented the spectrum: venture lending involves first-lien security on substantially all corporate assets and extensive financial covenants; synthetic royalties often require security over IP and product-related assets following recent U.S. court decisions (most notably the Shoot the Moon bankruptcy case); and royalty monetizations, while often unsecured, involve permanent transfer of the payment stream.

The royalty-backed note occupies a distinct position because it is formally debt (a note), but its non-recourse and ring-fenced nature means it behaves more like a partial sale from the perspective of every other claim in the capital structure.

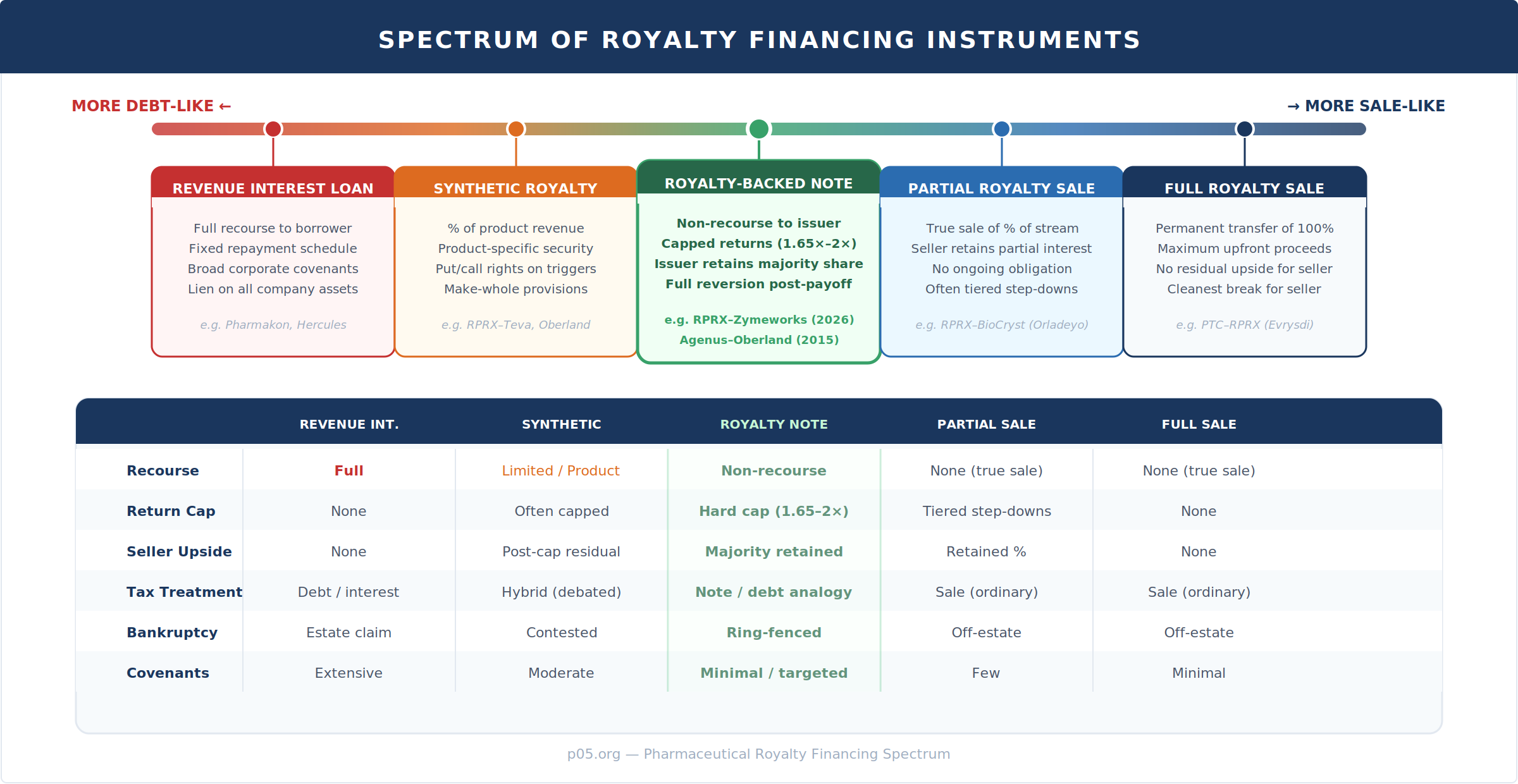

The Financing Spectrum

The five instruments above represent the current landscape of pharma royalty financing. Each offers a different combination of recourse, return profile, and issuer flexibility. Notably, the royalty-backed note occupies the centre of this spectrum—more protective for the issuer than a synthetic royalty or revenue interest loan, but less capital-efficient than a full sale (since the issuer receives less upfront than it would by permanently selling the stream).

The choice of instrument depends on the issuer's strategic calculus. Zymeworks explicitly cited three intended uses for the proceeds: share repurchases (the company's stock was trading at what management considered a discount to intrinsic value), potential strategic acquisitions, and extending cash runway beyond 2028. A full royalty sale would have maximised upfront proceeds but permanently destroyed optionality. The note structure lets Zymeworks retain long-term exposure to Ziihera's commercial success while accessing the capital it needs now.

The Non-Recourse Mechanic Under Stress

The non-recourse feature is the most important and most misunderstood element of these transactions. In practice, it means the investor is underwriting the drug, not the company.

If Ziihera fails to gain traction in first-line metastatic gastroesophageal adenocarcinoma (the indication under review based on HERIZON-GEA-01 data), the royalty stream could be insufficient to repay the note. In that scenario, Royalty Pharma's only remedy is to continue collecting its 30% share of whatever royalties materialise until the cap is reached—or until the underlying patents and exclusivity periods expire, at which point the stream goes to zero. There is no acceleration clause against Zymeworks' corporate cash, no conversion to equity, no right to compel Zymeworks to make whole the shortfall.

This is fundamentally different from, for example, the Agenus–Oberland Capital note purchase agreement (2015), where Oberland received 100% of the QS-21 royalties on GSK's shingles and malaria vaccines with a make-whole provision: if cumulative royalties fell short of the principal amount by a specified date, Agenus owed the difference. That deal was described as "generally limited recourse" but included explicit downside protection for the investor. The Zymeworks structure appears to be truly non-recourse.

It is also distinct from Covington's description of typical synthetic royalty put rights, where the purchaser may demand immediate payment of an agreed return upon bankruptcy, change of control, or breach—events that give the investor a corporate-level claim. In a non-recourse note, these protections are deliberately absent or limited to the pledged collateral.

For investors, this means the underwriting exercise is entirely about modelling the drug's commercial trajectory: peak sales estimates, royalty tier arithmetic, patent expiry timelines, and competitive dynamics. Corporate credit analysis—balance sheet strength, management quality, diversification—becomes largely irrelevant.

Prevalence and Market Adoption

Non-recourse royalty-backed notes are not yet the dominant structure in pharmaceutical royalty financing, but they are growing in frequency. The more common structures remain full or partial royalty purchases (true sales) and synthetic royalties with limited recourse provisions.

Several factors are driving adoption of the note structure specifically. First, biotech companies increasingly want to retain upside in their royalty streams—particularly when they believe the asset is undervalued by the market. A company trading at a steep discount to the net present value of its royalty portfolio (as Zymeworks apparently believes it is) has a strong incentive to borrow against the stream rather than sell it outright.

Second, the royalty financing investor base has deepened substantially. WilmerHale documented the growth trajectory: royalty financings have grown rapidly due to their flexible and non-dilutive structure, with economics less closely tethered to macroeconomic forces than traditional equity or debt. New investors have entered the market alongside established players like Royalty Pharma, HealthCare Royalty, Blackstone, and Oberland.

Third, as Gibson Dunn has tracked, even large, well-capitalised pharmaceutical companies are now using these structures for portfolio de-risking and capital optimisation, not just as emergency fundraising tools. Blackstone's synthetic funding arrangement with Merck in 2025 was a notable signal in this direction. The note structure's clean separation from the corporate balance sheet makes it especially attractive for companies that want to avoid covenant-heavy or dilutive alternatives.

Selected Precedent Transactions

The royalty-backed note has appeared in various forms across the market. A few key precedents illustrate the structural variation:

| Deal | Year | Size | Structure | Key Features |

|---|---|---|---|---|

| Agenus–Oberland | 2015 | $115M | Note Purchase Agreement | Limited recourse; 100% royalties until P+I repaid; make-whole provision; 13.5% interest |

| RPRX–BioCryst (Orladeyo) | 2020 | $125M | Partial royalty sale (not note) | Tiered rates 8.75%→2.75%→0%; cap at $550M sales tier |

| RPRX–Zymeworks (Ziihera) | 2026 | $250M | Non-recourse royalty-backed note | 30% of stream pledged; 1.65–1.925× cap; milestones retained; full reversion |

The Agenus–Oberland deal is the closest structural analogue to the Zymeworks transaction, but with an important distinction: Agenus' note included a make-whole mechanism (effectively limited corporate recourse if royalties underperformed), while Zymeworks' note appears fully non-recourse. The BioCryst deal, by contrast, was a true sale with a built-in sunset (royalty drops to zero above a sales threshold)—a different risk-sharing mechanism achieving a similar economic outcome.

Structural Risks and Investor Considerations

From the investor's perspective, the non-recourse note carries drug-specific risks that a diversified credit investor would not typically face:

Commercial risk. If Ziihera fails to achieve meaningful market share in GEA or other HER2-positive indications, the royalty stream may be insufficient to repay the note at the capped return. The investor has no mechanism to recover the shortfall from Zymeworks' corporate assets.

Competitive and IP risk. Biosimilar entry, competing bispecific antibodies, or patent challenges could erode the royalty base. The note's security is only as durable as the underlying product's commercial exclusivity.

Licensee execution risk. Jazz Pharmaceuticals and BeOne Medicines control the commercialisation of Ziihera. Their marketing decisions, pricing strategies, and reimbursement outcomes directly determine the royalty stream's magnitude. The investor cannot influence these decisions.

Tiering and cap arithmetic. The effective royalty to the investor is approximately low-to-mid-single digits on net sales. At the 1.65× cap ($412.5M by 2033), and assuming peak sales of $2–3 billion globally, the math works if the drug launches successfully in multiple indications on a reasonable timeline. If regulatory delays compress the window, the cap may be harder to reach.

Structural subordination to milestones. The carve-out of milestones from the note's collateral pool means the investor does not participate in the most binary (and potentially most valuable) elements of the Ziihera story. This is a deliberate trade-off: the investor accepts a lower-risk, royalty-only exposure.

Accounting and Tax Treatment

Royalty-backed notes are generally treated as debt on the issuer's balance sheet—the company records a liability, and royalty payments directed to the noteholder are treated as repayment of principal and interest rather than as a sale of an asset. This has the advantage of avoiding the immediate P&L impact of a gain on sale (which can be substantial for a company with a low cost basis in the royalty), but it does create a long-term liability that must be serviced.

For tax purposes, the characterisation depends on the specific terms and jurisdiction. RSM's analysis of royalty monetisation tax treatment highlights that a transaction's tax characterisation is determined by its substance, not merely its form. A royalty-backed note that walks and talks like debt (fixed repayment obligation, interest, security interest, no permanent transfer of ownership) is likely to be treated as debt for tax purposes, meaning the issuer continues to recognise the royalty income and deducts the interest component of payments to the noteholder.

For the investor, this means the returns are interest income rather than capital gains—a distinction that matters for fund economics and investor reporting, particularly for tax-exempt institutional investors who may prefer one characterisation over the other.

When Does the Note Structure Make Sense?

Not every royalty monetisation is suited to the note structure. It tends to work best when:

The issuer believes the underlying asset is undervalued and wants to retain long-term upside. A note with a hard return cap and full reversion accomplishes this.

The issuer wants non-dilutive capital without adding corporate-level leverage. The non-recourse feature isolates the transaction from the issuer's existing capital structure.

The underlying royalty stream is large enough to support a meaningful note while still leaving the majority of the economics with the issuer. In the Zymeworks case, pledging only 30% of the stream gives Royalty Pharma sufficient repayment coverage while preserving 70% for Zymeworks.

The investor has high conviction in the drug's commercial trajectory and is comfortable bearing all downside risk in exchange for a defined, capped return. This is an asset-level bet, not a credit bet.

The issuer has strategic uses for the capital that justify the cost (implied interest rate on the note) rather than waiting for royalties to accrue organically. Zymeworks' cited uses—buybacks, acquisitions, and runway extension—suggest a time-sensitive capital deployment thesis.

A Maturing Market

The non-recourse royalty-backed note represents the latest evolution in what has been a two-decade journey from a niche financing technique to a mainstream corporate finance tool. Royalty Pharma's S-1 filing in 2020 (when it went public at $28 per share) described the market it had helped create; the SEC no-action letter from 2010 that cleared Royalty Pharma's status under the Investment Company Act was, in some sense, the moment the structure received institutional legitimacy.

What has changed since is the sophistication of terms. Early deals were binary: buy the royalty or don't. Today's market offers a full spectrum of instruments—from revenue-interest loans with full recourse and corporate covenants, through synthetic royalties with limited recourse and product-specific security, to royalty-backed notes with non-recourse structures and capped returns, and finally to full true-sale purchases. Each occupies a different position in the risk-return continuum and serves a different strategic purpose.

The Zymeworks–Royalty Pharma transaction announced today is notable not because it is a first-of-its-kind structure, but because it represents the crystallisation of a market convention. Non-recourse, capped, retained-majority, milestone-carved-out, fully reverting: these are the building blocks of a standardised financing product that, a decade ago, did not exist in this form.

For biotech CFOs evaluating their options, the royalty-backed note adds a tool that sits precisely between selling the franchise's future and borrowing against the balance sheet. For royalty investors, it offers a defined-risk, defined-return profile that is increasingly attractive in a market where drug-level underwriting is their core competency.

The market will continue to evolve—structures will get more bespoke, caps more creative, collateral pools more complex. But the fundamental architecture of the non-recourse royalty-backed note appears to have found its place.

All information in this article was accurate as of the publication date and is derived from publicly available sources including company press releases, SEC filings, regulatory announcements, and financial news reporting. Information may have changed since publication. This content is for informational purposes only and does not constitute investment, legal, or financial advice. The author is not a lawyer or financial adviser.

Member discussion