Pharmaceutical Royalty Bonds: How Liquid, How Tradable, How Valued, How They Pay

Royalty bonds are the misunderstood instrument in pharmaceutical finance. Most market participants conflate four distinct security types under the same label.

| # | Category | Issuer | What it is | Tradable? |

|---|---|---|---|---|

| 1 | Fund-level corporate notes | Royalty Pharma plc, DRI Healthcare Trust | Unsecured corporate bond of a royalty fund. Pari passu on the fund's blended portfolio cash flow. Not backed by any specific royalty. | Yes, IG corporate market |

| 2 | 144A royalty securitizations | QHP Royalty Sub LLC, BioPharma Royalty Trust, DRI Capital Drug Royalty I/II/III | Notes issued by a bankruptcy-remote SPV holding an assigned royalty receivable. Coupon paid from the assigned cash flow under a contractual waterfall. | QIB-to-QIB only |

| 3 | Bilateral royalty-backed notes | REGENXBIO, Cytokinetics, Zymeworks, Denali, MorphoSys | Private placement under Section 4(a)(2). Non-recourse to the originator, secured by the assigned royalty stream. Usually amortizing to a MOIC cap rather than a fixed coupon. | No |

| 4 | Specialty royalty aggregators (public equity) | Ligand Pharmaceuticals, XOMA Royalty (Ligand-XOMA combined post-2026) | Publicly-listed equity vehicle holding a diversified pool of small-ticket royalty receivables. Functions as a bond-substitute for retail-accessible pharmaceutical royalty exposure. | Yes, Nasdaq equity market |

The four categories have radically different liquidity, tradability, and valuation profiles. Lumping them together is the source of most pricing errors.

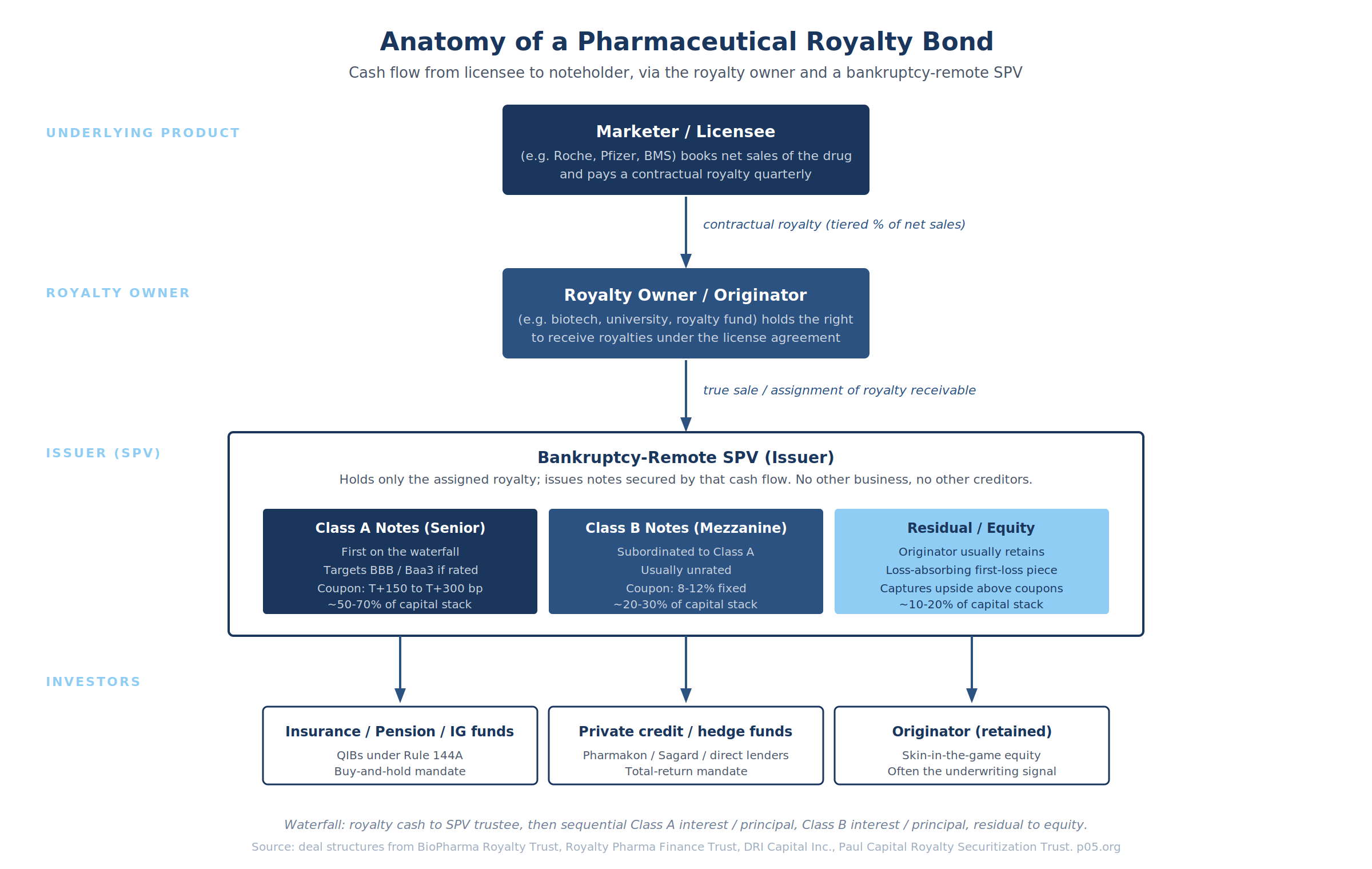

The textbook structure is a true securitization: a royalty owner (a university, a biotech, or a royalty fund) sells the royalty receivable to a bankruptcy-remote SPV, the SPV issues notes secured by that cash flow, and noteholders are repaid sequentially from royalty receipts under a contractual waterfall.

The contemporary market has largely moved away from that structure for reasons explained below.

This piece works through the historical evolution of the asset class, the structural mechanics of each contemporary category, the liquidity profile, the valuation framework (DCF stack plus illiquidity premium), the legal architecture, and the recent issuance cohort.

Written for counsel, royalty fund analysts, and treasury teams who have evaluated synthetic royalty financings and want to understand where the bond-format instruments fit in the same opportunity set.

A short history of pharmaceutical royalty securitization

The pharmaceutical royalty bond as a structured product is roughly 25 years old. The fate of the early issuances explains why the market looks the way it does in 2026.

| Year | Deal | Size | Outcome | What it taught the market |

|---|---|---|---|---|

| 2000 | BioPharma Royalty Trust I (Yale, Zerit, WestLB) | $60M senior + $22M mezz | Early amortization triggered 4Q01; surety (ZC Specialty Insurance) covered ~$600K mezz shortfall | Single-asset securitization is fragile: one inventory destocking event by the licensee broke the cash flow covenant within 18 months |

| 2003 | Royalty Pharma Finance Trust (CSFB) | $225M | Wrapped by MBIA, rated AAA/Aaa; 13-asset revolving pool; held to maturity | Diversification plus monoline wrap can reach AAA; the wrap was the rating, not the assets |

| 2004 | Royalty Pharma Trust securitization facility | Multi-vintage | Converted to syndicated term loan in 2007 | Securitization at fund level is structurally unstable once portfolio grows beyond a few assets; term loan is cheaper |

| 2009 | QHP PhaRMA Senior Secured Notes (PDL, Genentech royalties on Avastin/Herceptin/Lucentis/Xolair) | $300M @ 10.25% | Fully repaid by YE 2012, 27 months before stated 2015 maturity | Cash sweep on a high-quality multi-asset royalty pool retires bonds fast; modal exit is paydown, not secondary trade |

| 2014-2018 | DRI Capital Drug Royalty II/III (2014-1, 2016-1, 2017-1, 2018-1) | $450M, then incremental | BBB-rated by S&P and Kroll; master trust issuances on Stelara, Simponi, Tysabri, Keytruda, Eylea, Odefsey | Master trust structure with revolving pool is the only template that has scaled in the post-2008 vintage |

| 2021 | DRI Healthcare Trust IPO + corporate credit facility | $400M IPO + $632M facility | Replaced securitization shelf with fund-level corporate debt | Same pivot Royalty Pharma made in 2007 to 2020: from product-level securitization to fund-level corporate debt |

Three observations from this history.

The BioPharma Royalty Trust I episode is the founding cautionary tale. A $60M senior plus $22M mezzanine securitization of Yale's Zerit royalty, single-asset, single-licensee (Bristol-Myers Squibb), single-patent.

Bristol unloaded inventory at a discount in late 2001 as Zerit faced rising competition from newer HIV drugs. Royalty receipts collapsed. The mezzanine breached cash flow covenants in 4Q01, the senior in 1Q02, the mezzanine triggered rapid amortization in 2Q02, and ZC Specialty Insurance (a Center Re subsidiary) absorbed the shortfall via the monoline wrap.

The 2003 Royalty Pharma Finance Trust was explicitly structured to address what BioPharma I had got wrong: a 13-asset revolving pool with a three-year replacement window, an MBIA wrap on the senior, and a reserve account funded at closing.

The CSFB director on the trade told Asset Securitization Report at the time that "the previous deal's early amortization was taken into account."

The 2009 QHP PhaRMA notes are the most elegant single-issuer royalty bond ever placed and the proof that the format works when the underlying is strong enough.

PDL BioPharma sold to a newly-formed bankruptcy-remote subsidiary (QHP Royalty Sub LLC) 60% of its royalty stream from Genentech on Avastin, Herceptin, Lucentis, and Xolair. QHP issued $300M of 10.25% fixed-coupon Senior Secured Notes due March 2015 in a 144A private placement, secured by a continuing security interest in the assigned royalty receivable plus a pledge by PDL of its equity ownership interest in QHP.

The notes were redeemable at a make-whole price. The cash sweep retired the notes from $300M to $249.6M (June 2010) to $141.7M (June 2011) to $115.3M (September 2011) to $93.4M (YE 2011), and to zero by year-end 2012. The notes were fully repaid 27 months before the stated 2015 maturity.

There was never any meaningful secondary market because the make-whole call and the rapid amortization profile meant investors held to paydown. The 10.25% coupon in 2009 priced roughly 400-500 bp over the comparable IG corporate of the day. Investors who bought the QHP notes at issue earned that spread for three years, then got their principal back.

The asset class migrated from securitization to corporate debt at the fund level.

Royalty Pharma's 2004 securitization facility (the first product-level pharma royalty securitization, structured at fund level) became a 2007 syndicated term loan, then a 2020 corporate unsecured bond program now worth $9.2B. DRI Capital's 2014 to 2018 Drug Royalty III LP 1 securitization shelf was layered with the 2021 DRI Healthcare Trust IPO ($400M) and a November 2024 $631.6M corporate credit facility.

The pattern is consistent: once a royalty fund is large enough and diversified enough to support an investment-grade rating at the fund level, the cost-of-capital arbitrage versus single-asset securitization closes.

A Baa2/BBB- rated fund-level issuer borrows at 4-6% all-in; a single-asset 144A securitization clears at 8-12%. The securitization premium is the price of structural complexity plus illiquidity, and it disappears at scale.

What a pharmaceutical royalty bond is today

In 2026, four categories of "royalty bonds" coexist, and the structural differences between them dominate pricing.

Category 1: Fund-level corporate notes

These are conventional investment-grade corporate bonds issued by royalty funds. They are not backed by any specific royalty; they are pari passu corporate obligations paid from the fund's blended portfolio cash flow.

Royalty Pharma plc's most recent issuance, September 2025:

| Tranche | Size | Coupon | Maturity |

|---|---|---|---|

| 2031 Notes | $600M | 4.450% | 25 Mar 2031 |

| 2035 Notes | $900M | 5.200% | 25 Sep 2035 |

| 2055 Notes | $500M | 5.950% | 25 Sep 2055 |

Royalty Pharma is rated Baa2 (Moody's, upgraded from Baa3 in April 2025), BBB- (S&P), and BBB (Fitch, upgraded from BBB- in Q1 2026). The notes trade on the OTC corporate bond market with TRACE-reported prices, T+2 settlement, and 5-15 bp bid-ask spreads.

As of June 30, 2024, Royalty Pharma's total debt had a weighted-average duration of approximately 13 years and a weighted-average cost of debt of 3.1%, reflecting the legacy of low-rate 2020-2021 issuance. Total interest paid in 2025 was approximately $275M; the 2026 projection is roughly the same.

Category 2: 144A product-level securitizations

Rare in 2026 but not extinct. The QHP and BioPharma Royalty Trust templates remain the references.

DRI Capital's Drug Royalty III LP 1 master trust continues to issue: a $49.7M 2016 series, $101.8M 2017 series, and incremental 2018 issuance, all collateralized by royalty streams on patent-protected drugs including Keytruda, Eylea, and Odefsey, all BBB-rated by Kroll and S&P.

The DRI Drug Royalty III LP 1 series-2017-1 priced at coupons ranging from 4.94% on the AAA tranche to 6.78% on the B1 notes, illustrating the still-functional but narrow tranching that contemporary royalty securitization preserves.

Category 3: Bilateral product-level royalty-backed notes

The modal contemporary structure. A biotech with a contracted royalty (or future synthetic royalty) sells a private placement note to a royalty fund. The note is non-recourse, secured by the royalty stream, and typically amortizes to a multiple-of-money-invested cap rather than carrying a stated coupon. Three coupon archetypes coexist:

| Type | Example | Coupon mechanic | Implied yield |

|---|---|---|---|

| Floating-rate "Royalty Bond" | REGENXBIO-HCRx (May 2025) | 3M SOFR + 9.75%, with 4.25% SOFR floor; unpaid interest capitalizes to principal | ~14% floor, plus warrants |

| MOIC-cap note | Zymeworks-RPRX (Mar 2026) | No stated coupon; 1.65x MOIC cap by Dec 2033, 1.925x thereafter | ~10-12% IRR |

| Fixed-installment Development Funding Bond | MorphoSys (Sep 2022) | Defined quarterly cash payment independent of underlying sales | ~8% implied yield (sold at 5.35%) |

The REGENXBIO instrument is the cleanest contemporary product-level royalty bond because both parties explicitly call it a "Royalty Bond" in the SEC filing and it carries an explicit floating coupon.

HCRx will lend up to $250M (limited recourse) collateralized by REGENXBIO's anticipated royalties from Novartis on Zolgensma plus royalties and milestones from RGX-121, RGX-111, and the NAV Technology Platform licensees Rocket Pharmaceuticals and Ultragenyx.

The principal bears interest at 3-month SOFR plus 9.75% with a 4.25% SOFR floor; interest is payable from the royalty interest in arrears 60 days after each quarter, and if the royalty interest is insufficient, unpaid interest accrues to the principal balance.

The 10-year maturity extends two years on a specified patent term extension. HCRx also received warrants to purchase 268,096 shares at $14.92, a 100% premium to the 30-day weighted average price at signing.

The May 2024 Cytokinetics-Royalty Pharma Development Funding Loan Agreement uses the MOIC-cap template: tranches drawable up to $225M, each carrying an interest-free and payment-free period of six calendar quarters followed by 34 quarterly installments totaling 1.9x the amount drawn.

No coupon in the traditional sense; the embedded yield is implied by the discount of present value to face. The Royalty Pharma-Zymeworks $250M March 2026 royalty-backed note is closer to the Cytokinetics template but priced wider: a 1.65x MOIC cap by December 2033 or 1.925x thereafter, with no stated coupon but an implied yield in the 10-12% range given the time-to-cap.

The MorphoSys Development Funding Bonds were the cleanest fixed-installment structure in the contemporary cohort. The bonds delivered $9.7M per quarter on a defined schedule running through approximately 2034, secured by but not contingent on Tremfya royalty receipts. After Novartis acquired MorphoSys in 2024, the cash flow effectively became an A1-rated corporate obligation.

Royalty Pharma sold the position in January 2025 at a 5.35% discount rate, converting the original $300M September 2022 investment into $530M of total cash proceeds (including pre-sale repayments). This was the rare scenario where a bilateral product-level instrument actually traded.

Category 4: Specialty royalty aggregators (public equity vehicles)

A category that sits adjacent to the bond market rather than inside it, but functions as a bond substitute for investors who want diversified pharmaceutical royalty exposure without the QIB qualification or the bilateral underwriting cost. Two firms operate the model at scale: Ligand Pharmaceuticals (Nasdaq: LGND) and XOMA Royalty Corporation (Nasdaq: XOMA, renamed from XOMA Corporation in July 2024 to reflect the strategic pivot). A third firm, DRI Healthcare Trust (TSX: DHT.UN), runs a closely related model on the Toronto Stock Exchange.

The structural feature is that the issuer holds a diversified pool of small-ticket royalty receivables on the corporate balance sheet, finances the holdings with a mix of equity and modest corporate debt, and distributes royalty cash flow to public shareholders via dividends, buybacks, or reinvestment.

| Feature | Specialty royalty aggregator | Bilateral royalty-backed note (Category 3) |

|---|---|---|

| Issuer | Public Nasdaq / TSX company | Operating biotech |

| Investor entry point | Public equity at market price | Private placement to ~20-50 royalty funds |

| Underlying | Diversified portfolio (XOMA: 200+ assets; Ligand: 120+ pre-combination, 200+ post-combination) | Single product or small pipeline |

| Cash flow to investor | Dividends + capital appreciation + buybacks | Coupon or MOIC-cap repayment |

| Deal size at origination | Sub-$25M per royalty acquisition (XOMA); $50-200M (Ligand) | $50M-$2B |

| Stage focus | Pre-commercial / early-stage (XOMA); mid-stage to commercial (Ligand) | Late-stage / commercial |

| Default behavior | Diversified across many assets; isolated credit losses are absorbed by the portfolio | Single-asset, non-recourse, binary on the underlying |

XOMA Royalty's 2025 financial results illustrate the model. The firm recorded $50.5M in cash receipts (royalties $33.6M up 68% YoY, milestones $16.9M), deployed $25M to acquire seven new royalty positions across eight partnered programs, repurchased $16M of stock, and ended the year with $133.7M of cash.

The "deal size below $25M" is the structural differentiator versus Royalty Pharma or HCRx: XOMA can underwrite a $5M acquisition of a Phase 1 royalty that the larger funds will not look at because the diligence cost overwhelms the deal size.

Across the aggregator portfolio, isolated credit losses are absorbed by the diversification: the 2024 credit losses of $30.9M on Agenus ($14M), Aronora ($9M), and Talphera ($7.9M) hit XOMA's earnings but did not threaten the going-concern of the platform.

Ligand operates the same model with a different focus. Its 2025 royalty portfolio is anchored by Filspari (Travere), Ohtuvayre (Verona, now Merck following the $10B 2025 acquisition with a 13% royalty, stepping to 20%/7% if certain Backbeat clinical milestones are not met by January 2027), Capvaxive, Vaxneuvance, Rylaze, Pneumosil, Teriparatide, Qarziba, and Zelsuvmi (via the July 2025 Pelthos Therapeutics spinout at a 13% royalty).

The 2025 cohort of new investments included the $50M lead investment in Castle Creek D-Fi (with XOMA in the $25M syndicate), an Orchestra BioMed cardiology royalty, and an Arecor warrant deal. Ligand entered 2026 with approximately $1B of deployable capital and a stated 23% royalty receipts CAGR target through 2030.

The Ligand-XOMA merger of April 2026. On 27 April 2026, Ligand announced the acquisition of XOMA Royalty for $39.00 per share in cash plus one non-transferable Contingent Value Right (CVR) per share entitling the holder to 75% of net proceeds from XOMA's pending Tremfya / J&J Janssen litigation. The cash consideration is approximately $739M, representing a 14% premium to XOMA's 30-day VWAP as of 24 April 2026.

The transaction is expected to close in Q3 2026, immediately accretive to Ligand adjusted EPS (2026 guidance raised to $8.50-$9.50, expected $1.50/share accretion in 2027), and funded with Ligand's existing cash plus a draw on its credit facility.

Post-close the combined entity will hold more than 200 royalty assets, adding seven new commercial products to Ligand including Roche's VABYSMO (faricimab), Day One's OJEMDA (tovorafenib), and Zevra's MIPLYFFA (arimoclomol), plus 14 programs in late-stage development including Takeda's mezagitamab, osavampator, volixibat, and OHB-607.

Ligand CEO Todd Davis stated on the deal call that the combined platform can absorb the XOMA portfolio "with almost 100% synergies" since "there's no commercial infrastructure required, there's no manufacturing infrastructure, there's no clinical development infrastructure", illustrating the asset-light economics of the aggregator model.

The merger consolidates the specialty royalty aggregator category. Before April 2026, Ligand and XOMA were the two principal publicly-listed pharmaceutical royalty aggregators in the US market with complementary stage focus (Ligand mid-to-late stage, XOMA pre-commercial).

Post-merger, the combined Ligand-XOMA platform plus DRI Healthcare Trust on the Toronto Stock Exchange are the two principal public-equity vehicles globally for diversified pharmaceutical royalty exposure.

Royalty Pharma is the much larger third comparator but operates more like a corporate fund-of-funds with bond-level liquidity at the debt layer rather than equity-level retail accessibility.

The Ligand-XOMA combination is the first significant consolidation event in the specialty aggregator segment, and the rationale (deal flow synergies, expanded balance sheet, broader negotiating leverage across the deal-size spectrum) is the same logic that drove DRI's 2021 IPO and Royalty Pharma's IPO in 2020.

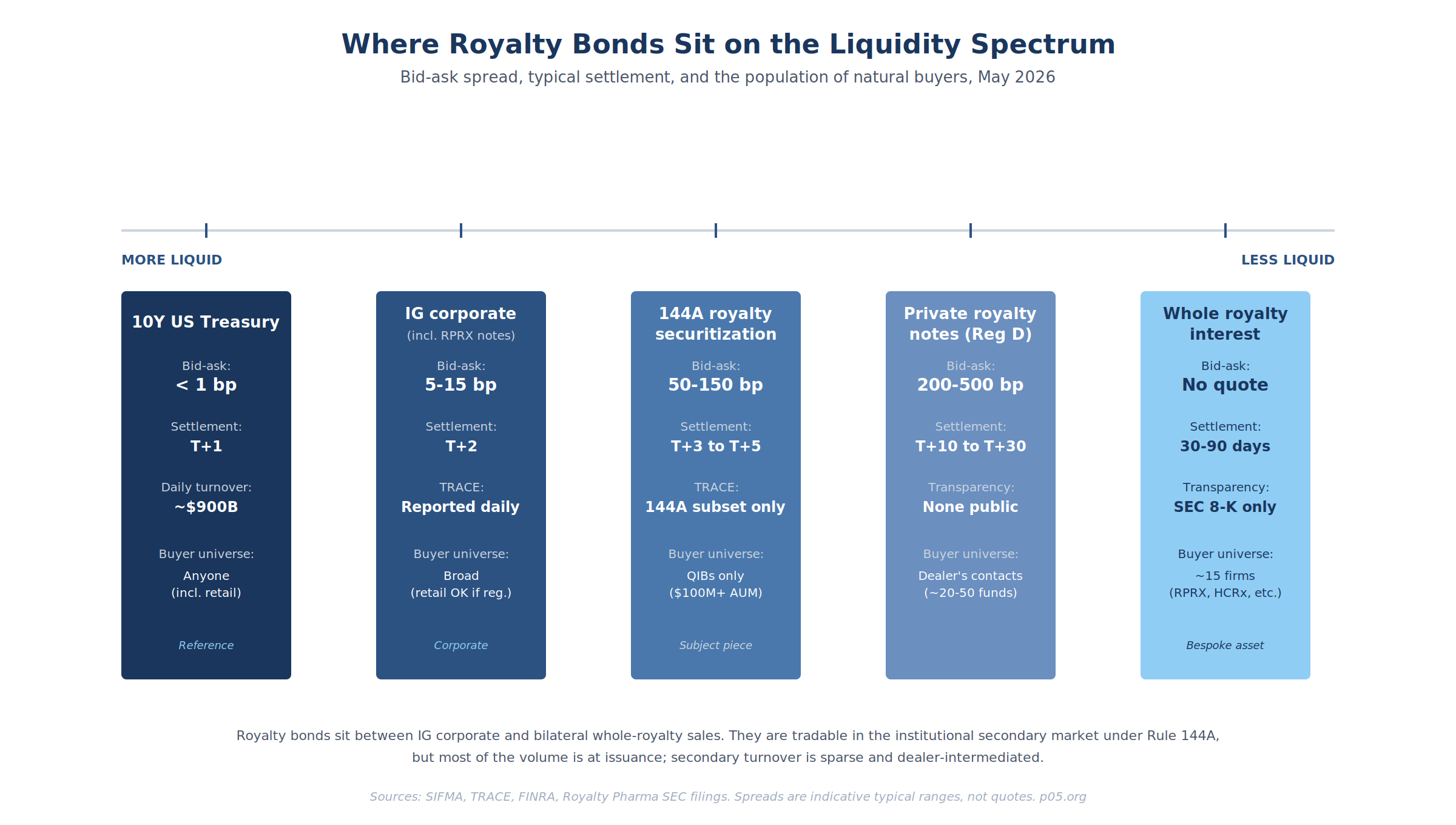

Tradability: who can buy, who can sell, and what trades

The tradability of a pharmaceutical royalty bond is determined by three factors: the registration regime, the population of eligible buyers, and the existence of a dealer market making secondary quotes.

| Instrument type | Settlement | Bid-ask | Buyer universe | TRACE? |

|---|---|---|---|---|

| 10Y US Treasury | T+1 | < 1 bp | Anyone, incl. retail | Yes |

| IG corporate (incl. RPRX notes) | T+2 | 5-15 bp | Broad institutional + retail | Yes |

| 144A royalty securitization | T+3 to T+5 | 50-150 bp | QIBs only ($100M+ AUM) | Subset only |

| Private royalty note (Reg D) | T+10 to T+30 | 200-500 bp | ~20-50 royalty funds and direct lenders | No |

| Whole royalty interest | 30-90 days | No quote | ~15 firms globally | No, SEC 8-K only |

Fund-level notes are freely tradable. Royalty Pharma's notes trade like any other IG corporate. The September 2025 deal was bookrun by BofA, Goldman Sachs, J.P. Morgan, Morgan Stanley, and TD Securities; all five maintain ongoing market-making.

The 2031 senior unsecured note issued at a 2.15% coupon in July 2021 traded at a 5.40% yield to maturity in mid-2023 and currently trades in the 4.5-5.0% YTM range, well inside the issue spread.

144A securitizations exist in a narrow secondary market. Rule 144A provides a safe harbor for QIB-to-QIB resales without SEC registration, but most royalty securitization tranches trade two to five times in their life, almost always through the original bookrunner.

The QHP PhaRMA notes were never widely quoted in the secondary because the make-whole call and the rapid cash-sweep amortization meant there was no upside for any secondary buyer.

The DRI Drug Royalty III LP 1 master trust notes are the rare exception: a multi-vintage shelf with sufficient outstanding to support intermittent dealer activity, although volumes remain thin.

Bilateral private placements are not transferable. The REGENXBIO, Cytokinetics, Zymeworks, Denali, Nuvation Bio, and Castle Creek examples are all Section 4(a)(2) private placements with no contemplated secondary distribution. Where transfer occurs, it requires the underlying obligor's consent and is negotiated bilaterally.

Whole royalty interests trade bilaterally. The buyer universe is the ~15 firms that buy royalties professionally: Royalty Pharma, HealthCare Royalty Partners (now KKR-controlled), Sagard Healthcare Partners, BioPharma Credit / Pharmakon, DRI Healthcare Trust, OMERS Life Sciences, Blackstone Life Sciences, Ligand, XOMA Royalty, and a tail of smaller funds.

The distinction matters because the tradability question dominates pricing. A bilateral royalty-backed note on a comparable underlying prices at 200-500 bp wider than a fund-level corporate of the same issuer because the buyer is being compensated for illiquidity, structural complexity, and the absence of a competing bid.

The REGENXBIO Royalty Bond at SOFR+975 / 14% floor is the cleanest contemporary data point: an approved gene therapy royalty (Zolgensma) plus pipeline upside, structured as a limited-recourse loan with warrants attached, clearing at roughly 850-1000 bp wide of where the fund-level IG corporate prints.

The same instrument issued via securitization with diversification, a wrap, and a settled market would have cleared 200-400 bp tighter; the gap between bilateral and securitized pricing has roughly doubled in 15 years.

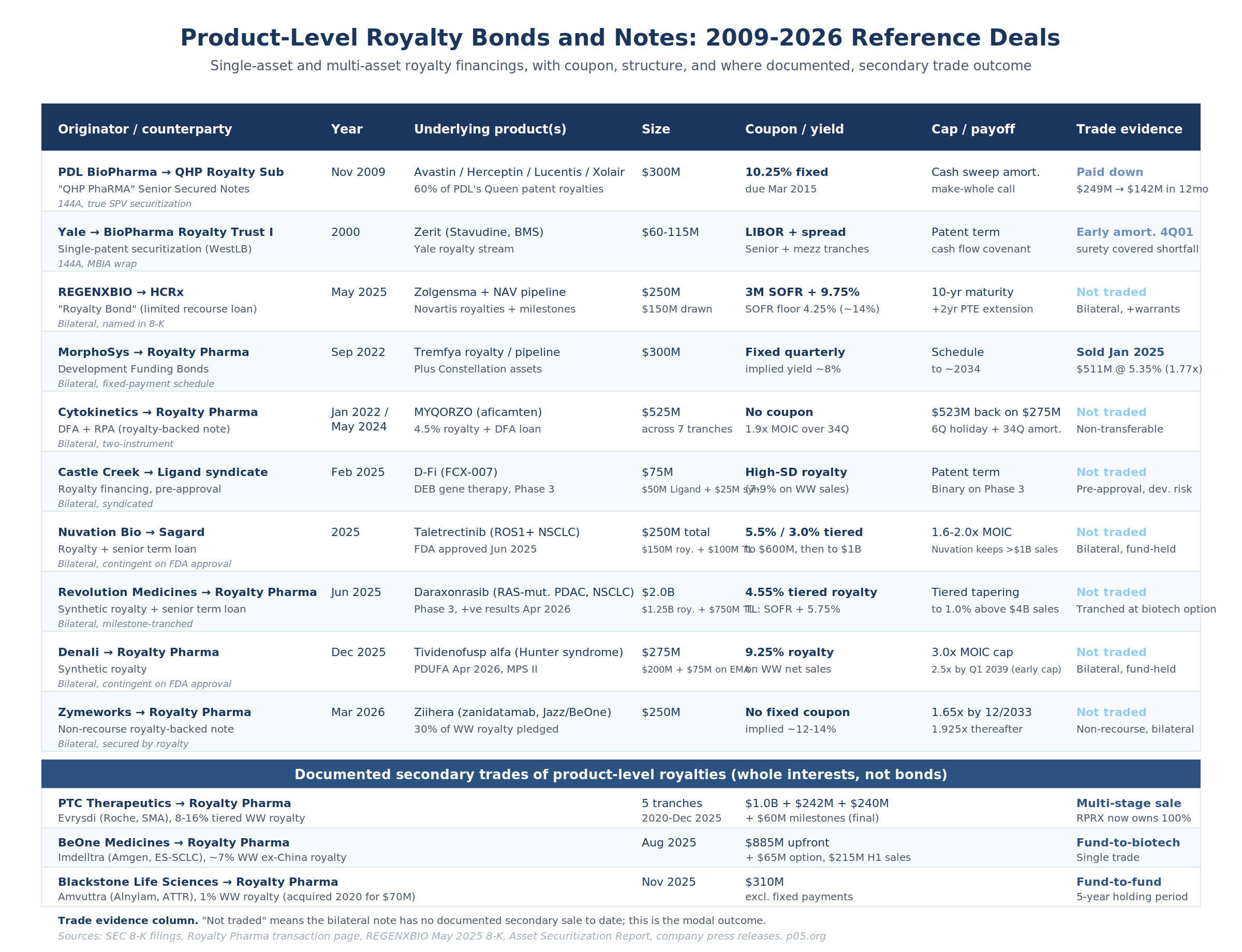

Documented secondary trades, 2025 to 2026

The closest the asset class gets to bond secondary trading is the bilateral sale of whole royalty interests between sophisticated counterparties.

Four transactions in the past 18 months illustrate the range. None of these is a sale of the wrapper instrument; they are sales of the underlying royalty itself, with the instrument layer either dissolved or restructured at the trade.

| Date | Seller | Buyer | Product | Royalty interest | Price | Holding period | Implied multiple |

|---|---|---|---|---|---|---|---|

| Jan 2025 | Royalty Pharma | (third party) | MorphoSys Development Funding Bonds (Tremfya royalty + pipeline) | Fixed-payment schedule | $511M upfront; total $530M on $300M cost | 28 months | 1.77x |

| Aug 2025 | BeOne Medicines | Royalty Pharma | Imdelltra (Amgen, ES-SCLC) | ~7% WW ex-China royalty | $885M upfront + $65M option | Earned via 2019 Amgen-BeiGene collaboration | n/a (no cash basis) |

| Nov 2025 | Blackstone Life Sciences | Royalty Pharma | Amvuttra (Alnylam, ATTR) | 1% WW royalty | $310M cash on 2020 $70M cost | 5 years | 4.4x |

| Dec 2025 | PTC Therapeutics | Royalty Pharma | Evrysdi (Roche, SMA) (final tranche) | Last portion of 8-16% tiered royalty | $240M + $60M milestones; cumulative $1.5B+ across five tranches 2020-2025 | 25 years (Roche license originated 2000) | n/a (multi-tranche) |

These are bilateral asset sales priced through bespoke valuation models, with multi-month diligence cycles and 30-90 day settlement. The bid-ask spread, in any conventional sense, does not exist.

The MorphoSys Development Funding Bonds exit is the closest to a true bond secondary trade in the asset class. The instrument was bond-like in form (fixed quarterly payments, defined maturity schedule), and the Novartis acquisition of MorphoSys converted the obligor credit from biotech to investment-grade, allowing Royalty Pharma to sell the position at a 5.35% discount rate.

Without the Novartis acquisition, this trade would not have happened: the position would have remained on Royalty Pharma's balance sheet and amortized to maturity.

The Pablo Legorreta quote in the press release is unusually explicit on this point: "Novartis' acquisition of MorphoSys created a unique opportunity to convert a fixed stream of long-term payments with no potential for outperformance into a large cash inflow today at an attractive return for shareholders."

The Blackstone-to-RPRX Amvuttra trade is the cleanest example of fund-to-fund secondary in the asset class. Blackstone Life Sciences acquired the 1% royalty in 2020 for $70M as part of the Alnylam HELIOS-B financing collaboration, held it for five years through the trial readout and US/EU approval, then sold for $310M to Royalty Pharma in November 2025.

That is a 4.4x cash multiple over five years, an unlevered IRR in the mid-30s.

The trade required no securitization wrapper, no rating, and no dealer; it required Blackstone's willingness to monetize and Royalty Pharma's underwriting of nucresiran competition risk against Alnylam's own follow-on.

The PTC Evrysdi sequence (five tranches from 2020 through December 2025, cumulative cash proceeds to PTC of more than $1.5B against the original Roche license signed in 2000) illustrates a different mechanic.

Royalty Pharma did not buy the royalty in one transaction; it built the position over five years through repeated tranche acquisitions, each priced to the then-prevailing forecast and discount rate. The final $240M tranche in December 2025 brought Royalty Pharma's position to 100% ownership of the 8-16% tiered Roche royalty.

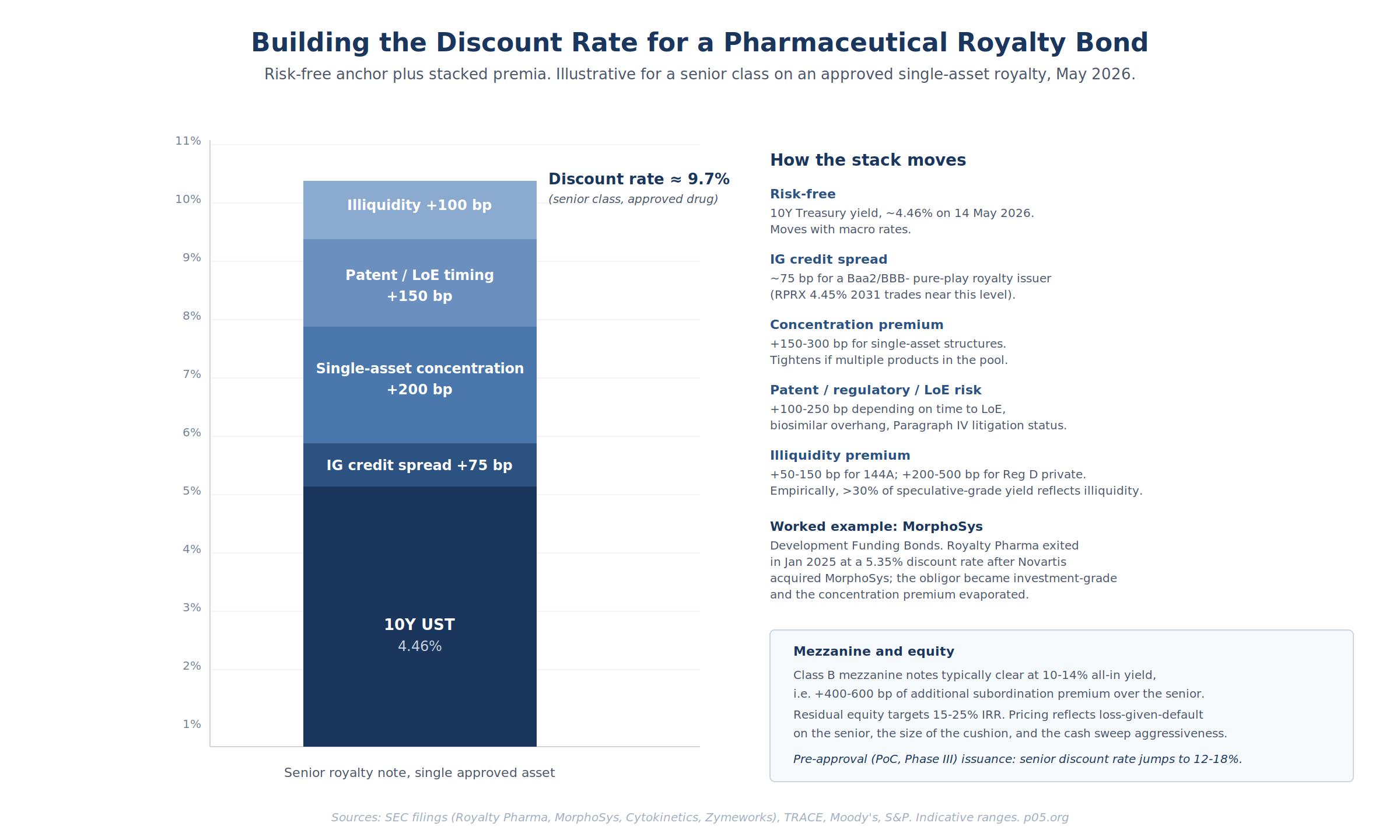

Valuation: the discount rate stack

Valuation of a pharmaceutical royalty bond is a discounted cash flow exercise. The complexity lives in two places: the projection of underlying royalty cash flows (sales forecasts, patent expiry timing, biosimilar penetration, IRA impact, foreign exchange) and the construction of the discount rate.

The discount rate is built as a stack of premia over the risk-free anchor.

| Layer | Spread | Drives |

|---|---|---|

| 10Y US Treasury | 4.46% | Macro rate environment (14 May 2026) |

| IG credit spread | +75 bp | Baa2/BBB- pure-play royalty issuer, 5-7yr |

| Concentration premium | +200 bp | Single-asset structure; compresses for multi-asset pools and master trusts |

| Patent / LoE / regulatory risk | +150 bp | Up to +400 bp for short-runway or Paragraph IV litigation |

| Illiquidity (144A) | +100 bp | 50-150 bp range; up to +500 bp for Reg D private |

| Total: senior class, approved single asset | ~9.7% | Indicative; varies materially by deal |

The risk-free anchor is the 10Y Treasury yield, currently around 4.46%. Above that, the IG credit spread for a Baa2/BBB- pure-play royalty issuer sits at roughly 75 bp for 5-7 year maturities and 100-130 bp for 10-30 year.

Royalty Pharma's September 2025 30-year note priced at 5.950%, implying a spread of approximately 130 bp over the 30Y Treasury at the time of issuance. This is the baseline for fund-level royalty bonds.

The concentration premium compensates for the absence of diversification. A single-asset royalty stream carries an additional 150-300 bp over the IG benchmark; a two-asset structure compresses this to roughly 100-200 bp. The REGENXBIO Royalty Bond (Zolgensma plus three pipeline royalties) is in the middle of this range.

The 2003 13-asset BioPharma Royalty Trust II reduced the concentration premium to near-zero, although the rating uplift in that case came from the MBIA wrap rather than the diversification per se.

The patent / LoE / regulatory risk layer is the most analyst-intensive: every royalty has a different patent landscape, regulatory exclusivity profile, and competitive picture, and the premium ranges from 50-100 bp for 10+ year runway clean assets to 200-400 bp for 4-6 year runway assets facing Paragraph IV litigation or late-stage biosimilar competition.

The illiquidity premium is structurally larger than most generalist bond investors would expect. Empirical work on the corporate bond market shows that for speculative-grade issuers, more than 30% of the cost of borrowing reflects illiquidity rather than credit risk. For royalty securitizations, the illiquidity premium is 50-150 bp for 144A format and 200-500 bp for true private placements.

When a royalty fund sells a bilateral royalty-backed note to a second royalty fund in a secondary transaction, the discount rate is typically 200 bp above where the same note would clear if it had been securitized at issuance. Subordination economics layer on top:

| Layer | Indicative yield | Spread over senior |

|---|---|---|

| Senior (Class A) | 9-11% | Baseline |

| Mezzanine (Class B) | 10-14% | +400-600 bp |

| Residual equity | 15-25% IRR target | Captures the call option |

| Pre-approval (Phase 3) senior | 12-18% | +300-700 bp over approved senior |

The historical comparison is instructive. The QHP PhaRMA notes priced at 10.25% in 2009, in a market where the comparable IG corporate would have priced at roughly 5-6%, giving a 400-500 bp royalty-bond premium.

The contemporary REGENXBIO Royalty Bond prices at SOFR + 9.75% with a 4.25% SOFR floor (so a ~14% all-in floor coupon, plus warrants), in a market where RPRX corporate notes price at 4.45% to 5.95%, giving an 850-1000 bp royalty-bond premium. The premium has roughly doubled in 15 years.

The reasons: the post-2008 illiquidity premium is structurally higher, the rated-securitization buyer base has thinned (fewer monoline wraps, fewer real-money funds with the analytical capacity), and the dominant royalty funds are now investment-grade corporate borrowers themselves, which collapses the alternative-instrument pricing.

The 4.25% SOFR floor in the REGENXBIO bond is itself a structural feature of the new market: it caps the lender's exposure to a falling-rate environment, which has become a routine ask in private credit since 2023.

The MorphoSys exit at 5.35% in January 2025 is the low end of the historical range, and the drivers were specific: the Novartis acquisition converted the obligor credit, the underlying payments were fixed (not contingent on Tremfya sales performance), and the concentration premium evaporated because the cash flow was effectively an A1-rated corporate obligation.

A more typical single-asset, single-drug, biotech-obligor structure prices wider.

Empirical default risk in the asset class is not negligible. XOMA Royalty Corp recorded $30.9M of credit losses on purchased receivables in 2024, comprising $14.0M on the 2018 Agenus transaction, $9.0M on the 2019 Aronora transaction, and $7.9M on the Talphera transaction.

Across an aggregator portfolio with multiple pre-approval positions, the base rate for default is meaningfully above zero. Sophisticated valuation overlays a Monte Carlo simulation on the underlying variables (sales path, patent challenge probabilities, IRA selection risk) and prices the bond at the expected NPV, sometimes with a separate value-at-risk haircut for the variance.

Coupons and cash mechanics, by category

The coupon question depends on the category, and the differences are larger than they appear.

| Category | Example | Coupon | Payment | Maturity / payoff |

|---|---|---|---|---|

| Fund-level corporate | RPRX 2055 Notes | 5.950% fixed | Semi-annual | Bullet, Sep 2055 |

| Product-level securitization | QHP PhaRMA (historic) | 10.25% fixed | Quarterly | Cash sweep from assigned royalty; make-whole call |

| DRI Drug Royalty III LP 1 senior | 2017-1 AAA tranche | 4.94% fixed | Quarterly | Cash sweep; overcollateralization buffer |

| Floating-rate product bond | REGENXBIO-HCRx | 3M SOFR + 9.75%, 4.25% SOFR floor | Quarterly, 60 days arrears | 10yr stated, +2yr on patent term extension |

| Fixed-installment Development Funding Bond | MorphoSys | Fixed quarterly $ amount | Quarterly | Schedule, ~2034 |

| MOIC-cap note | Cytokinetics DFA | None stated; embedded yield | 1.9x over 34Q after 6Q holiday | Repayment cap = 1.9x principal |

| MOIC-cap synthetic royalty | Denali tividenofusp | 9.25% royalty on net sales | Quarterly | 3.0x MOIC cap (2.5x if reached by Q1 2039) |

| Tiered synthetic royalty + term loan | Revolution Medicines / RPRX | 4.55% tiered royalty + SOFR + 5.75% TL | Quarterly | Royalty: tiered to 1.0% above $4B sales; TL: standard amortization |

Fund-level corporate bonds. Conventional fixed coupon, semi-annual payment, bullet maturity. Standard issuer-level coverage and incurrence covenants; no link to any specific royalty. The 2021 RPRX vintage issued at a 2.15% coupon for the 2031 tranche; the 2025 vintage issued at 4.450% / 5.200% / 5.950% across 2031 / 2035 / 2055 maturities.

Product-level securitizations. The QHP PhaRMA template is the cleanest reference: a fixed 10.25% coupon, make-whole call, sole-source repayment from the assigned royalty receivable, with a continuing security interest plus an equity pledge of the SPV.

The BioPharma Royalty Trust template used a floating LIBOR-plus-spread coupon for the senior class with a cash flow covenant; the mezzanine carried a higher fixed coupon with a surety wrap.

The DRI master trust template combines a tranched structure (4.94% AAA at the senior, 6.78% B1 at the mezzanine in the 2017-1 series) with 36-52% overcollateralization and a six-month interest reserve. All three templates share the cash-sweep amortization mechanic: principal pays down as royalty cash arrives, often well ahead of stated maturity.

Bilateral product-level royalty bonds. Three coupon archetypes coexist in 2026.

The first is the floating-rate Royalty Bond (REGENXBIO-HCRx template). SOFR plus spread with a SOFR floor, interest paid from the assigned royalty receivable in arrears, unpaid interest capitalizing to principal if the royalty is insufficient. Plus warrants. This is the most explicitly bond-like structure of the contemporary set and the one a fixed-income desk would recognize most easily.

The second is the MOIC-cap note (Cytokinetics, Zymeworks, Denali, Nuvation, Revolution Medicines synthetic royalty template). No stated coupon; repayment as a defined multiple over a defined cash period.

The MOIC multiple depends on the maturity profile and the perceived risk: 1.65x by year 7 (Zymeworks/Ziihera, implied ~10% IRR), 1.9x over ~10 years (Cytokinetics, implied ~7% IRR), 3.0x with no time cap (Denali/tividenofusp, implied 11-13% IRR depending on sales ramp).

The MOIC cap construction is closer to a participating preferred equity than a bond, and it should be modeled as such; the implicit coupon to the holder rises with sales upside but is capped on the downside by the time horizon to the multiple.

The third is the fixed-installment Development Funding Bond (MorphoSys template). A defined quarterly repayment schedule independent of underlying sales performance, secured by the assigned royalty receivable but not contingent on it. The MorphoSys structure delivered $9.7M per quarter through approximately 2034 before the January 2025 monetization.

This is the closest to a true bond in cash-mechanic terms: fixed cash flow, known maturity, no contingency to underlying sales.

The economic difference between a stated coupon and a MOIC cap is the contingent profile. A stated coupon is a contractual obligation regardless of underlying sales performance, subject only to covenant breach and default.

A MOIC cap defines the maximum payout but not the minimum: if the underlying royalty underperforms, the noteholder receives less than the implied yield and the payback period lengthens; if it overperforms, the cap binds and the residual flows to the originator.

The MOIC cap structure has become standard in 2025-2026 because it solves the biotech's concern about open-ended royalty obligations (the BridgeBio / HCRx / Blue Owl royalty terminates at 1.45x on $300M; the Revolution Medicines synthetic royalty terminates at a tiered cap on each $250M tranche) while preserving the royalty fund's upside participation up to a defined multiple.

Recent issuance, 2009 to 2026

The 2009 to 2026 cohort confirms the bifurcation between fund-level corporate debt and product-level bilateral private placements.

At the fund level, public corporate issuance has been robust: Royalty Pharma's $9.2B of IG debt at March 2026, HCRx's $680M credit facility (October 2023), DRI Healthcare Trust's $631.6M credit facility (November 2024), KKR's

acquisition of HCRx in July 2025 under the $6.5B Asset-Based Finance Partners II vehicle, and the institutionalization of mid-market royalty credit through Sagard, Pharmakon, and Ligand.

At the single-asset level, the market is bilateral. The 2025 to 2026 cohort:

| Date | Deal | Size | Coupon / yield | Cap / payoff |

|---|---|---|---|---|

| Feb 2025 | Castle Creek D-Fi (Ligand syndicate) | $75M | High single-digit royalty | Patent term, binary on Phase 3 |

| May 2025 | REGENXBIO Royalty Bond (HCRx) | $250M ($150M drawn) | 3M SOFR + 9.75%, 4.25% floor | 10yr + 2yr PTE extension |

| Jun 2025 | Revolution Medicines (RPRX) | $2.0B ($1.25B royalty + $750M TL) | 4.55% tiered royalty / TL SOFR + 5.75% | Tiered tapering to 1.0% above $4B sales |

| 2025 | Nuvation Bio taletrectinib (Sagard) | $250M ($150M royalty + $100M TL) | 5.5% / 3.0% tiered | 1.6-2.0x MOIC |

| Dec 2025 | Denali tividenofusp (RPRX) | $275M ($200M + $75M on EMA) | 9.25% royalty on WW net sales | 3.0x MOIC (2.5x by Q1 2039) |

| Mar 2026 | Zymeworks Ziihera (RPRX) | $250M | No fixed coupon | 1.65x by 12/2033, 1.925x after |

None of these instruments is tradable in any practical sense. The MorphoSys exit in January 2025 was a bilateral sale to an unnamed third party at a 5.35% discount rate, not a market transaction. Across the broader bilateral cohort, only three transactions have been resolved through anything resembling a secondary event: the MorphoSys Development Funding Bonds (sold), the QHP PhaRMA notes (cash-sweep amortization to zero by YE 2012), and the BioPharma Royalty Trust I early-amortization event of late 2001.

In each case the resolution was an internal restructuring, an asset sale, or a cash-sweep paydown, not a secondary trade in the bond sense.

The conspicuous absence is a meaningful population of new 144A product-level securitizations. The reasons are structural.

- Cost of capital arbitrage at the fund level. Royalty Pharma borrows at 4-6%; a single-asset 144A securitization clears at 8-12%. The fund prefers to hold the whole royalty and finance the position with fund-level corporate debt.

- Investment Company Act treatment. The Section 3(c)(5)(A) exemption requires that the issuer's portfolio be primarily royalty receivables; smaller single-asset securitizations face higher legal cost for the same structuring benefit.

- Market-maker infrastructure atrophy. The 144A pharmaceutical ABS dealer infrastructure thinned after 2008 and has not been rebuilt. DRI Capital's continued issuance through Drug Royalty III LP 1 is the exception, not the rule.

Legal architecture: six provisions that drive everything

For counsel structuring or evaluating royalty bonds:

| Provision | What to look for | Why it matters |

|---|---|---|

| True-sale opinion | Article 9 UCC characterization. True sale to SPV vs. secured loan. | True-sale failure consolidates the royalty into the originator's estate in bankruptcy, defeating the SPV's bankruptcy-remoteness |

| Change of control | Whether the underlying royalty is transferable without licensee consent | Co-promotion contracts and bespoke structures often contain consent rights that the bond inherits |

| Audit and information rights | Whether the SPV trustee can enforce audit rights against the licensee | Practical question of trustee resources and incentive |

| Indemnities | Originator's patent prosecution, IP warranty, regulatory representation indemnities survive assignment | Reserve account or sub-account in modern structures |

| Tax | US withholding under Section 1442 for non-US noteholders; debt characterization for portfolio interest exemption | Single most important structuring question for foreign noteholders |

| ASC 808 vs 606 | Collaborative arrangement (ASC 808) vs. license (ASC 606) | Profit-share streams under ASC 808 are structurally less financeable through bond formats |

True-sale opinion. A royalty securitization requires that the assignment of the royalty receivable from the originator to the SPV qualify as a true sale under Article 9 of the UCC, not a secured loan. The QHP PhaRMA structure addressed this through a fully-documented sale (Purchase and Sale Agreement, true-sale opinion, separate SPV with independent director, equity pledge of the SPV) at the cost of additional structuring complexity.

Most bilateral product-level royalty bonds in 2026 are documented as limited-recourse secured loans rather than true sales, which preserves the originator's accounting treatment but sacrifices bankruptcy remoteness in exchange. The REGENXBIO Royalty Bond is explicit on this point: it is a "limited recourse loan," not a true sale.

Change of control of the underlying licensee. Royalty contracts typically transfer with the underlying license without consent, but co-promotion contracts and some bespoke structures contain change-of-control consent rights. A securitization that depends on a non-transferable royalty inherits that non-transferability and is harder to amend or restructure.

The 2024 Novartis acquisition of MorphoSys is the rare positive scenario: the underlying obligor became investment-grade, the Development Funding Bonds became effectively a Novartis credit obligation, and Royalty Pharma sold the position at a 5.35% discount rate that would have been unavailable when MorphoSys was a Phase 3-stage biotech.

Audit and information rights. The SPV must inherit the originator's audit rights against the licensee; the trustee must be able to enforce. Bilateral royalty-backed notes typically grant the noteholder direct audit rights against the licensee through the security agreement; securitization SPVs route through the trustee. The practical question is whether the trustee has the resources and incentive to enforce.

Indemnities and tail liabilities. The originator's contractual indemnities to the licensee (patent prosecution, IP warranties, regulatory representations) survive the assignment and can result in clawback.

Modern structures include a reserve account or indemnity sub-account to cover this risk; older structures relied on the originator's solvency, which proved inadequate when Yale and BMS disputed Zerit royalty calculations in 2001-2002 and the BioPharma Royalty Trust I entered rapid amortization.

Tax treatment of the noteholder. A US taxable noteholder treats coupon as ordinary income. A US tax-exempt noteholder (pension, endowment) is generally indifferent.

A non-US noteholder is subject to US withholding tax on royalty receipts under Section 1442 unless the SPV is structured to convert the royalty into a debt obligation for US tax purposes (the "debt characterization" question), in which case interest may qualify for the portfolio interest exemption. This is the single most important structuring question for foreign noteholders.

ASC 808 vs ASC 606 classification of the underlying. If the underlying contract is a collaborative arrangement under ASC 808 rather than a license under ASC 606, the cash flow is "collaboration revenue" or a reduction of operating expenses, not royalty revenue. Securitization of an ASC 808 cash flow is structurally more complex and is generally priced wider.

The 2024 to 2026 trend toward co-promotion and 50/50 profit-share contracts in pharmaceutical licensing means that an increasing share of the available royalty universe is structurally less financeable through bond formats.

What this means for new issuance

Three implications for 2026 and beyond.

For royalty funds with diversified portfolios. Fund-level corporate unsecured debt at Baa2/BBB- is the cheapest source of long-duration capital available to the asset class. Royalty Pharma's weighted-average cost of debt of 3.1% as of mid-2024 (legacy) and the September 2025 issuance at 4.450% to 5.950% (current) suggest a fund-level all-in cost of debt in the 4-6% range for incremental capital.

The arbitrage versus the 7-10% target IRR on new royalty acquisitions and the 10-12% target on development-stage assets is durable so long as the IG rating holds.

The Royalty Pharma 2007-to-2020 pivot from securitization to term loan to corporate unsecured debt, and DRI Capital's 2021 follow-up via the DRI Healthcare Trust IPO plus credit facility, are the proof of concept.

For single-asset originators. Bilateral product-level royalty bonds are the practical alternative to a clean royalty sale. The 2025 cohort prices the implicit yield at 9-14% all-in for approved assets (REGENXBIO at SOFR+975 floor 14%; Denali at 9.25% with a 3.0x MOIC cap implying 11-13% IRR; Zymeworks at no-coupon 1.65x by 2033 implying ~10% IRR) and 12-18% for development-stage. This is meaningfully wider than what a securitization would clear at if the structural and legal cost of a true ABS could be amortized.

For transactions above $300M with a clean royalty profile, a 144A securitization remains the cheaper option in principle; in practice, the absence of a settled market means most deals route through bilateral private placement instead. The biotech that signs a MOIC-cap note today should expect to be holding it (or being held by it) to the cap; secondary liquidity is not a realistic exit assumption.

For the buy side. The bond-format royalty market in 2026 splits into two pools: liquid IG corporate paper from a handful of royalty fund issuers, and illiquid private placements that are functionally portfolio holdings rather than tradable securities. The pricing differential between the two is large (300-900 bp depending on the structure), and it does not all reflect credit risk; a meaningful share is pure illiquidity premium captured by the private placement buyer.

For funds with the mandate and the underwriting capacity to hold private royalty-backed notes, this is a structural source of return. For funds that need mark-to-market liquidity, the IG corporate market is the only viable entry.

The next two to three years will reveal whether the 144A securitization market reopens for the post-2010 vintage. The conditions are in place: investment-grade royalty fund issuers exist, dealer infrastructure has been partially rebuilt around the IG corporate market, and the underlying royalty universe is larger and more diversified than at any prior point.

The blockers are the cost of capital arbitrage at the fund level (which makes securitization redundant for the largest holders) and the absence of demand from real-money buyers who would price 144A royalty ABS competitively against IG corporate. The DRI Drug Royalty III LP 1 master trust continues to issue, but the broader securitization market has not followed. Both could change; neither has yet.

Outlook: more of this, or bundled and sold properly?

The asset class as a whole has roughly doubled in six years. Gibson Dunn's 2026 royalty finance market update puts aggregate 2025 royalty finance transaction value at approximately $6.5B across 25-27 deals, up from $5.7B in 2024 and a 37% growth from $5.2B in 2020.

The early 2000s baseline was less than $200M per year. The trajectory is clear. The structural question for 2026 to 2030 is whether the bond-format and securitization-format part of that market scales with the underlying, or remains stuck at the bilateral private placement layer.

What is plausibly going to happen

| Driver | Direction | Timing |

|---|---|---|

| Fund-level IG corporate issuance | More of the same. RPRX, DRI Healthcare Trust, BioPharma Credit are the established issuers; ABF mandates at KKR, Blackstone, Apollo, Blue Owl are adding capacity at the fund level. | Continuous |

| Bilateral product-level royalty notes | Continued growth. Modal contemporary structure, format is settled, biotech demand is structural. | 2026-2028 |

| Big Pharma using bilateral royalty notes for de-risking | New trend, accelerating. Blackstone-Merck $700M sac-TMT (Q4 2025) is the template: not a financing-driven deal, a portfolio-management deal. | 2026-2028 |

| Specialty royalty aggregator consolidation | Underway. The April 2026 Ligand-XOMA merger ($739M) is the first significant consolidation event in the public-equity aggregator segment. | Active now |

| Master trust securitizations (DRI template) | Slow continuation; no new issuer in three years. Investment Company Act complexity plus thin dealer market. | Indeterminate |

| True multi-asset 144A royalty ABS with diversified buyer base | Conditional. Requires either insurance demand or a new monoline-equivalent credit support mechanism. | 2027-2030 if at all |

| Synthetic royalty + retained equity tranche structures | Emerging. Originator-retained residuals are now common (Revolution Medicines, Zymeworks) and create the precondition for tranching. | 2026-2028 |

| Geographic-tranche bundling (US royalty as one bond, ex-US as another) | Conceptual. The Roche-Zealand structure and the BridgeBio European-only sale to HCRx+Blue Owl are precedents. | 2027-2030 |

Why securitization has not yet reopened

The honest answer is that the contemporary royalty finance market, in its bilateral form, is structurally cheaper for the dominant participants than any plausible securitization. Royalty Pharma's all-in cost of debt is in the 4-6% range; it acquires royalties at 7-12% IRR; the spread is the franchise. There is no incentive for the firm to securitize a portfolio of acquired royalties when its own corporate bonds price tighter than any rated tranche of a single-asset ABS would.

The same logic holds for DRI Healthcare Trust (which followed Royalty Pharma's pivot in 2021), and increasingly for HCRx after the KKR acquisition, where royalty origination feeds into KKR's broader Asset-Based Finance Partners II mandate rather than into a dedicated securitization vehicle.

The buy side mirror image is that the real-money insurance and pension buyers that would naturally hold pharmaceutical royalty ABS face a tightening regulatory environment, not a loosening one. The NAIC's 2025 Fall National Meeting advanced new disclosure requirements for SPV-issued debt held by insurers, and the Life Risk-Based Capital Working Group has reopened the RBC factor discussion for collateral loans and ABS structures, with proposals exposed in February 2026.

The direction of travel is toward higher capital charges for opaque or bespoke structured products, not lower. A single-asset pharma royalty 144A ABS, even rated BBB, faces a higher post-2026 RBC capital charge than a comparably-rated IG corporate. That is dispositive for the marginal insurance buyer.

The private credit dislocation visible in May 2026 is a near-term complication. Apollo is weighing the sale of a $3B fund; Blackstone and KKR have stepped in to support some of their own vehicles; rising defaults in mid-market lending have prompted a broader reassessment of the private credit model.

This is not a royalty-bond-specific story (pharma royalty performance has held up), but it tightens the bid environment for any new structured credit issuance, including any prospective royalty ABS revival.

The bundling question: can this be done at scale?

The conceptual case for bundling product-level royalty bonds into a diversified ABS is straightforward. A pool of 20 product-level royalty bonds with uncorrelated patent, regulatory, and commercial risks should price meaningfully tighter than any of the individual instruments.

The 2003 Royalty Pharma Finance Trust proved this with a 13-asset pool reaching AAA on the back of an MBIA wrap, and the DRI Drug Royalty III LP 1 master trust continues to issue BBB-rated paper on the same logic at smaller scale today.

The blockers are mechanical, not theoretical.

| Blocker | Current state | What would unblock |

|---|---|---|

| Originator concentration | Royalty Pharma owns most marketed royalties worth securitizing; refuses to sell into a competing instrument | A second large royalty fund willing to securitize, or a Big Pharma converting bilateral notes into a tradable wrapper |

| Credit enhancement | No surviving monoline wrap market; reserve accounts and overcollateralization are weaker alternatives | A re-emergence of monoline coverage for specialty ABS, or a senior-mezz-equity tranching deep enough to absorb single-asset failures |

| Investment Company Act treatment | Section 3(c)(5)(A) requires the issuer's portfolio be primarily royalty receivables; sub-scale single-asset structures face higher legal cost | Already resolved for diversified pools; not a binding constraint at 10+ assets |

| Buyer base | Real-money insurance / pension demand for life sciences ABS is thin; specialty credit funds are sized for bilateral, not pooled | Insurance RBC clarification; ratings agency methodologies that distinguish pharma ABS from generic specialty credit |

| Originator incentive | Bilateral private placement captures more economics for the seller than securitization | A tradable wrapper that prices tighter than the bilateral note, even net of structuring cost, which requires a buyer base that does not yet exist |

The clearest pathway to a bundled product is not a true Article 9 securitization but a fund-level corporate bond issued by a vehicle that holds a diversified pool of bilateral royalty notes. This is what BioPharma Credit plc (Pharmakon's listed vehicle) does in a different format: senior secured loans rather than royalty notes, held in a portfolio at the fund level, financed with shareholder equity and a modest amount of debt.

A scaled-up version with $5-10B of AUM, holding product-level royalty bonds rather than direct royalties, financed with Baa-rated corporate unsecured notes, is the most realistic shape of a new bond-format wrapper.

The market is not currently moving in that direction at any speed. The capital is flowing into bilateral origination, which is more lucrative for the originating fund and faster to deploy.

A scaled bundled-bond vehicle would require either (a) a sponsor large enough to commit $1-2B of seed equity (KKR-HCRx is the most plausible candidate, given the Asset-Based Finance Partners II mandate, although the focus to date has been on bilateral origination, not securitization) or (b) an institutional-investor consortium demanding tradable life sciences exposure at a scale the bilateral market cannot provide. Neither is in evidence in May 2026.

The structural shift to watch

The most consequential development for the bond-format royalty market is not on the financing side but on the originator side. The Blackstone-Merck $700M sac-TMT clinical funding agreement in Q4 2025 is the template: a large, profitable, investment-grade pharmaceutical company using a synthetic royalty structure not as a financing of last resort but as a portfolio de-risking and capital optimization tool.

The Big Pharma counterparty changes the credit profile of the receivable: instead of a biotech obligor with Phase 3 binary risk, the underlying credit is Merck. A pool of 20 Big Pharma synthetic royalty receivables would price wholly differently from a pool of 20 biotech bilateral notes.

If three or four more Big Pharma deals of the sac-TMT type close in 2026 and 2027, the building blocks for a genuine multi-asset royalty ABS with broad institutional appeal start to exist.

The investment-grade nature of the obligor solves the concentration premium problem at the underlying credit level; the diversification of the pool solves the single-product risk problem; the rated tranching solves the buyer-base problem. This is the pathway that closes the 850-1000 bp royalty bond premium back toward the 200-300 bp pre-2008 spread.

A parallel pathway is already running through the specialty royalty aggregator segment. The Ligand-XOMA merger in April 2026 consolidates the two largest US-listed pharmaceutical royalty aggregators into a single platform with 200+ assets and approximately $1B of deployable capital.

The combined Ligand-XOMA, together with DRI Healthcare Trust on the TSX, gives retail and smaller institutional investors a tradable public-equity proxy for diversified pharmaceutical royalty exposure that would otherwise require QIB qualification or bilateral underwriting access.

The aggregator vehicles do not solve the bond-format problem (they are equity, not debt), but they validate the underlying logic of pooled royalty exposure: the diversification thesis works, the cash flows compound, and the public-market investor base is willing to underwrite the structure at scale.

If the Ligand-XOMA combined platform issues investment-grade corporate debt to finance further portfolio expansion (a plausible next step given the deployable capital target and the asset-light economics), the asset class gains a second public-equity-backed bond issuer alongside DRI Healthcare Trust. That widens the buyer base for pharmaceutical royalty paper without requiring the 144A securitization market to reopen.

The probability of either pathway delivering a tradable, scaled, bond-format royalty market by 2030 is, in our assessment, low but not negligible. The royalty finance market doubled in six years on the back of structural biotech funding pressure and a single-buyer (Royalty Pharma) franchise model. The next doubling, if it comes, requires multiple buyers and tradable wrappers.

Whether it gets there depends on whether the major asset managers building Asset-Based Finance platforms (KKR, Blackstone, Apollo, Blue Owl) decide that pharmaceutical royalties are a category large enough to warrant dedicated securitization infrastructure rather than a sub-strategy within broader specialty credit, and on whether the specialty aggregator segment continues to consolidate and tap the corporate bond market. The 2025 to 2030 period will be the test.

This article reflects publicly available information as of May 2026. It does not constitute investment, legal, or tax advice. Yield, spread, and discount rate ranges are indicative and derived from SEC filings, press releases, and published market commentary. Specific instruments should be evaluated against their offering documents and applicable counsel.